Electric Boiler Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 11.68 Billion |

| Market Size (2030) | USD 18.89 Billion |

| Growth Rate (2025 - 2030) | 10.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

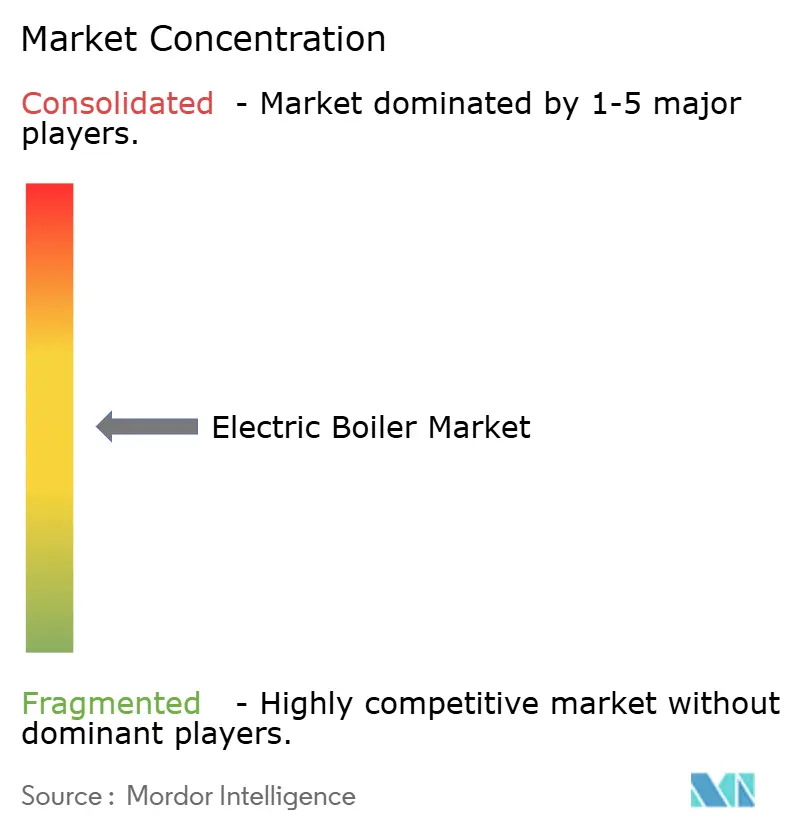

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Boiler Market Analysis by Mordor Intelligence

The Electric Boiler Market size is estimated at USD 11.68 billion in 2025, and is expected to reach USD 18.89 billion by 2030, at a CAGR of 10.09% during the forecast period (2025-2030).

This rapid expansion reflects the convergence of building-sector electrification mandates, fossil-fuel phase-outs, and falling renewable-power costs that are reshaping industrial and residential heating choices. Regulatory bans on new fossil-fuel boilers across the European Union and several U.S. states are turning compliance spending into long-term electrification budgets, while grid operators view large electric boilers as flexible loads that soak up surplus solar and wind output. Demand is reinforced by heat-pump proliferation, which drives hybrid system adoption in commercial real estate and district heating schemes. Finally, expanding industrial demand-response programs allow owners to monetize load flexibility, tilting total cost of ownership in favor of electric heating assets.

Key Report Takeaways

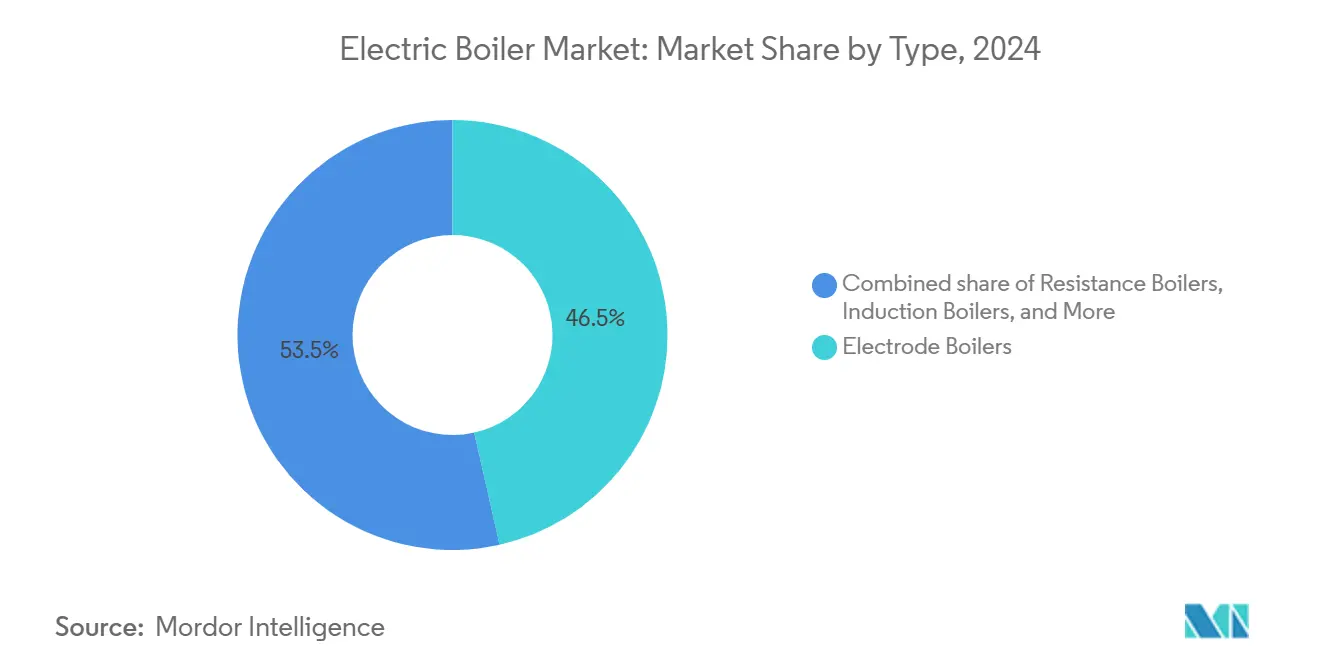

- By type, electrode boilers held 46.5% of the electric boiler market share in 2024, whereas induction boilers are projected to post the fastest 12.5% CAGR through 2030.

- By application, hot-water systems captured 62.0% of the electric boiler market size in 2024, while district heating is set to rise at a 12.8% CAGR over the same period.

- By end-user, residential installations accounted for 48.0% of 2024 revenues, whereas industrial deployments are forecast to expand at an 11.4% CAGR to 2030.

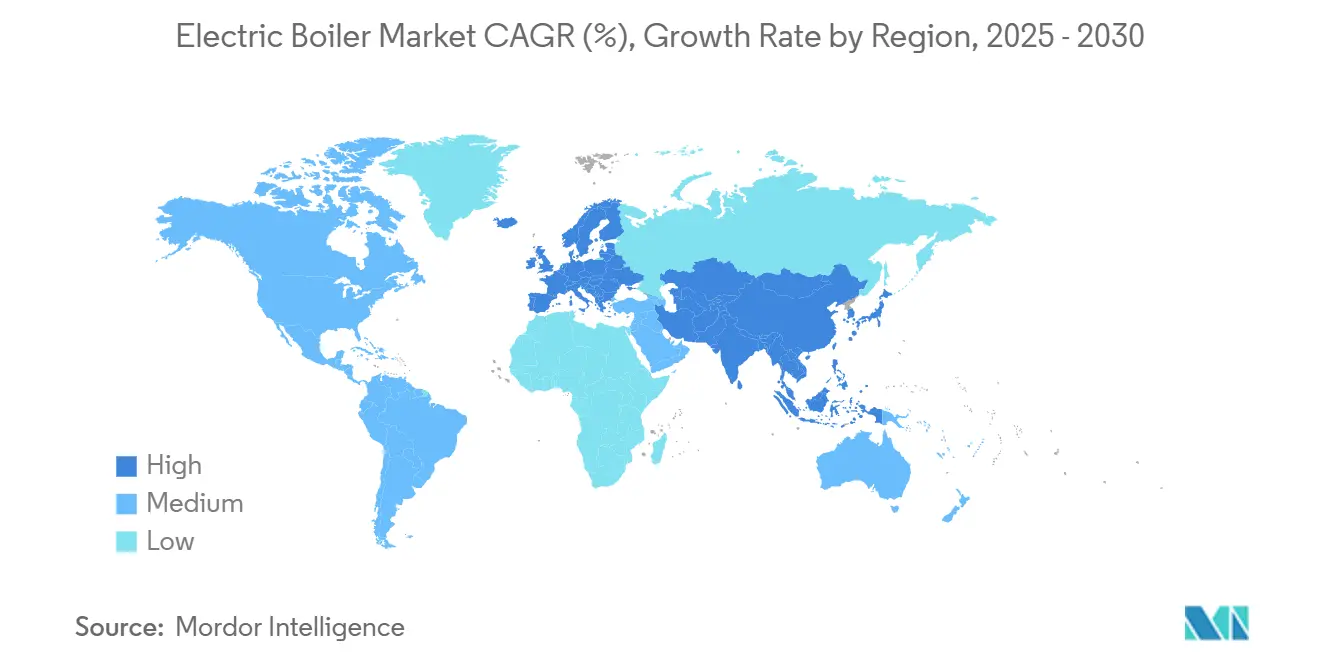

- By geography, Asia-Pacific commanded 38.0% revenue share in 2024 and is poised for the quickest 11.3% CAGR through 2030.

Global Electric Boiler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent building-sector electrification mandates | 2.80% | EU core, expanding to North America | Medium term (2-4 years) |

| Mandated phase-out of fossil fuel boilers in EU & select US states | 3.10% | EU, California, New York, Washington | Short term (≤ 2 years) |

| Falling levelised cost of renewables powering electric boilers | 1.90% | Global, with APAC and EU leadership | Long term (≥ 4 years) |

| Rapid heat-pump adoption driving complementary hybrid e-boilers | 1.40% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Under-utilised grid balancing revenues via industrial demand response | 0.70% | APAC core, expanding to EU and North America | Long term (≥ 4 years) |

| Surging green-hydrogen projects needing zero-emission steam back-up | 0.60% | EU, Australia, select US states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Building-Sector Electrification Mandates

Municipal and state mandates translate climate goals into binding equipment rules that lock in long-run demand for the electric boiler market. Denver’s Building and Fire Code requires that any major boiler replacement after January 2027 provide at least 50% electric heating capacity, a standard reinforced by California’s Title 24 “electric-ready” provisions for new multifamily builds. Similar measures under review in the U.K. propose raising minimum electric-boiler efficiency from 36% to 47%, aligning appliance ratings with the rising renewable share in national electricity mixes. Localized rollouts cluster installations, driving cost efficiencies for distributors and installers. Utility planners, meanwhile, must accommodate higher coincident loads, making electric boilers a core element in distribution-level resource plans. The mandates shift capital planning and operational risk from building owners to grid operators, accelerating procurement cycles for compliant equipment.

Mandated Phase-Out of Fossil-Fuel Boilers

The European “renovation wave” calls for eliminating fossil-fuel heating systems by 2040, compressing commercial and multifamily stock replacement cycles. In the United States, the South Coast Air Quality Management District Rule 1146.2 obliges zero-emission water heaters in most buildings starting January 2026, with a full retrofit deadline of 2033.[1]South Coast Air Quality Management District, “Rule 1146.2 Zero-Emission Water Heaters,” aqmd.gov Similar zero-emission standards are advancing in California, New York, and Washington. These measures establish predictable replacement windows and remove stranded-asset risk for owners shifting budgets from gas to electric equipment. Because compliance dates are fixed, project timelines are accelerated, favoring technologies—such as packaged electric boilers—that can be ordered and commissioned quickly.

Falling Levelized Cost of Renewables Powering Electric Boilers

The International Energy Agency projects that renewables will meet almost all new electricity demand through 2027, creating frequent periods of surplus supply. Hourly price volatility favors flexible electric loads that can absorb low-cost power, improving lifetime economics for the electric boiler market. When electricity prices in high-solar regions fall below USD 20/MWh during midday, industrial operators find that electric steam can undercut natural-gas steam on a variable-cost basis. Expanding grid-scale renewables means every kWh consumed carries a lower carbon intensity, helping facilities simultaneously hit scope 1 and scope 2 decarbonization targets. Finally, the growing volume of corporate power-purchase agreements guarantees off-takers stable clean-energy prices, creating hedge structures that smooth boiler operating costs.

Rapid Heat-Pump Adoption Driving Hybrid E-Boilers

Heat-pump sales in Europe rose 38% in 2024, expanding the installed base to almost 20 million units. Large commercial buildings increasingly pair heat pumps for baseload heat with electric boilers for peak demand or redundancy. Stadtwerke Jena’s district heating network illustrates that heat pumps cover most annual load, while 50 MW of electrode-boiler capacity meets extreme-weather peaks and enables power-to-heat balancing. The hybrid approach circumvents heat-pump performance drops at sub-zero outdoor temperatures, keeps distribution temperatures stable, and delivers grid services by modulating boiler output in real time. As controls and system integration mature, the electric boiler market stands to gain incremental volumes tied directly to heat-pump rollouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High peak-time electricity tariffs & grid capacity constraints | -1.80% | Global, particularly acute in EU and select US markets | Short term (≤ 2 years) |

| Capital-cost premium versus gas boilers in >10 MW installations | -1.20% | Global, with higher impact in industrial applications | Medium term (2-4 years) |

| Transformer & switchgear shortages delaying HV electrode projects | -0.90% | Global supply chain impact, acute in North America | Short term (≤ 2 years) |

| Limited installer skill-base for megawatt-scale e-boilers | -0.60% | Global, with regional variations in technical education | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Peak-Time Electricity Tariffs & Grid Capacity Constraints

Time-of-use pricing in regions with high renewables can raise electric-steam costs 40-60% during evening peaks, eroding full-load-hour economics for factories that cannot shift production schedules. In dense urban cores, distribution transformers operate near thermal limits; connecting multi-megawatt electrode boilers may require months-long grid-upgrade studies and utility approvals. These hurdles lengthen project timelines and raise capital budgets. Demand-response revenue, however, can offset part of the tariff shock by rewarding fast-ramping electric boilers that absorb solar over-generation or shed load during congestion. Grid-modernization funds earmarked under EU RePower and the U.S. IIJA will gradually alleviate infrastructure bottlenecks, but near-term economics remain sensitive to local tariff design.

Capital-Cost Premium Versus Gas Boilers in Above 10 MW Installations

A 20 MW electrode boiler package can cost two to three times a comparably sized gas-fired water-tube unit once transformers, switchgear, and cabling are included.[2]Source: U.S. Department of Energy, “High-Voltage Electrode-Boiler Cost Study,” energy.gov While carbon prices and compliance fines tilt life-cycle economics toward electric solutions, high front-end outlays still deter privately financed industrial retrofits. Recent supply agreements show equipment costs falling as silicon-controlled rectifier prices decline, yet total installed cost parity is unlikely before 2027 in most regions. Innovative models—such as utility ownership with capacity contracts—are emerging to transfer capex from plant operators to rate-regulated entities, smoothing adoption but adding regulatory complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electrode Technology Leads Market Evolution

The electric boiler market size for electrode units reached USD 4.92 billion in 2024, representing 46.5% of total revenues. Electrode designs scale efficiently into the 10–120 MW range and ramp from standby to full output in under 30 seconds, allowing owners to capture frequency-response payments on liberalized power markets. Though holding a smaller revenue share, induction boilers are growing at a 12.5% CAGR because falling silicon-steel prices reduce core losses. Resistance boilers retain relevance below 1 MW, chiefly in multifamily retrofits where simplicity outweighs efficiency. Across all types, smart inverters and predictive controls now ship as standard, creating software-as-a-service revenue that strengthens equipment suppliers’ post-sale margins.

Market preference continues to split by end-use. Utilities buy electrode units for district-energy peaks, heavy industry gravitates to induction where electromagnetic interference must be minimized, and residential buyers default to resistance elements integrated with storage tanks. Patents on electrode geometry and dielectric coatings climbed 14% year-on-year in 2024, underscoring a race among OEMs to boost current density while minimizing corrosion. Miura’s 2024 acquisition of Cleaver-Brooks extends Japanese power-electronics know-how into U.S. steel and food-processing verticals, illustrating how cross-border consolidation seeks scale economies in product development and service networks.[3]Miura Co. Ltd., “FY 2024 Integrated Report,” miuraz.co.jp

By Application: District Heating Drives Growth Acceleration

Hot-water installations dominated the electric boiler market share at 62.0% in 2024 because single-family and light-commercial buildings favor plug-and-play replacements for gas tank heaters. Yet district-heating projects, often sized above 30 MW, are on track for a 12.8% CAGR. Cologne’s 150 MW fluvial-heat-pump and electrode-boiler complex will supply roughly 50,000 households with zero-combustion heat once fully online in 2026. Industrial process-heat adoption up to 200 °C now benefits from improved immersion-tube metallurgy, letting breweries, dairies, and chemical plants electrify steam loops without redesigning upstream processes. Steam-generation still grows, albeit slower, constrained by high specific electricity demand at saturated-steam temperatures.

District-energy operators value boilers not only for heat but also for grid flexibility. When wholesale power prices decrease during windy nights in northern Germany, a 60 MW electrode unit can convert excess electrons to thermal energy stored in 10,000 m³ buffer tanks. Heat sold hours later effectively arbitrages the market, boosting project IRRs. Process-heat users, meanwhile, exploit the fast-cycling nature of electric boilers to match batch production patterns, reducing idling losses common to gas-fired assets. As both business models mature, technology suppliers are bundling performance guarantees that link availability metrics to service-fee revenues, signalling an evolution from capex sales to outcome-based contracts.

By End-User: Industrial Segment Accelerates Adoption

Residential buyers represented 48.0% of 2024 revenue, reflecting compulsory electrification in new builds across the EU and select U.S. jurisdictions. Industrial purchases, by contrast, are rising at an 11.4% CAGR because corporate decarbonization roadmaps target process heat—a sector contributing about one-fifth of global CO₂ emissions.[4]International Energy Agency, “Renewables 2024,” iea.org Food-processing plants lead deployments under pressure from consumer brands to meet scope 3 targets, followed by chemicals and pharmaceuticals that prize tight temperature control. Commercial campuses and hospitals continue steady uptake, supported by utility rebate programs that cover up to 40% of project capital.

The economic logic varies by sector. Households prioritize compliance and upfront rebates, while factories value fuel flexibility plus the ability to earn demand-response income. Equipment choice mirrors these priorities: resistance elements dominate 10–30 kW residential ranges, whereas multi-MW electrode units prevail in food and beverage sterilization lines. Financing models are also diverging—energy—as—a—service contracts backstop over 30 industrial sites in North America, bundling boilers, transformers, and controls under 10-year heat-supply agreements that hedge energy price risk for plant owners.

Geography Analysis

Asia-Pacific’s 38.0% revenue share in 2024 underscores its demand anchor and manufacturing hub role. China alone installed more than 2 GW of new electric-steam capacity in 2024 as provincial governments offered power-tariff discounts for off-peak industrial loads. India is following with boiler-specific fiscal incentives under its Perform-Achieve-Trade energy-efficiency scheme, encouraging cement and textile mills to adopt 5–15 MW electrode units. South Korea’s industrial decarbonization fund reimburses up to 30% of project capex for electric heating assets, while Japan’s Green Transformation policy prioritizes high-voltage demand-response assets, ensuring advanced control systems become standard in new installations.

Europe’s policy environment remains the world’s most assertive. Germany’s Building Energy Act phases out new fossil-fuel boilers from 2026, driving municipalities to electrify district heat loops. The U.K. Clean Heat Market Mechanism sets quotas requiring gas-boiler brands to sell a rising share of electric appliances beginning in 2026, effectively translating quota deficits into cash transfers subsidizing electric boiler sales. Nordic utilities continue to demonstrate power-to-heat economics: Helsinki and Stockholm each commissioned >100 MW electrode boilers in 2024 to absorb wind-power surpluses, underscoring how grid-service revenue co-funds heating infrastructure.

North America presents a mixed picture. Policy ambition is high in coastal states, yet abundant shale gas keeps relative fuel costs low in many regions. California’s Advanced Clean Buildings program offers USD 180/kW incentives for large boilers that provide dispatchable load. New York’s Climate Action Council similarly links electrification grants to participation in the NYISO demand-response market. Canada’s carbon price, which rose to CAD 80/t CO₂ in 2024, shortens payback for electric boilers in provinces with hydro-dominated grids. Mexico’s Reforma Energética encourages private renewable generation, making hybrid solar-plus-boiler plants attractive for industrial parks in Nuevo León and Jalisco.

Competitive Landscape

Competition remains moderately fragmented: the top five vendors account for roughly 35% of global shipments, leaving room for regional specialists and start-ups. Established combustion-boiler giants—such as Cleaver-Brooks and Bosch Thermotechnik—use their service networks to penetrate electric retrofits, while pure-play electric firms like Vapor Power International differentiate via electrode design and high-frequency controls. The 2024 Miura–Cleaver-Brooks merger signaled a trend toward scale plays that fuse Japanese power-electronics expertise with North American distribution footprints, giving the combined entity a 12% share of 2024 global revenue.

Digitalization is now the main axis of competition. Vendors package edge analytics modules that predict element degradation and optimize dispatch against day-ahead prices. IoT connectivity also unlocks subscription revenues: Miura’s Colormetry suite, for instance, bills clients USD 0.35 per operating hour for continuous diagnostics. Industrial users welcome these services because unexpected downtime can halt multimillion-dollar production lines. Utilities, meanwhile, seek cyber-secure interfaces so boilers can be bid into ancillary-service markets without breaching grid-code requirements.

Capital markets endorse the growth story. AtmosZero raised USD 21 million in Series A funding during 2024 to commercialize modular 15 MW electric-steam skids for high-temperature process heat, attracting investors familiar with stationary-storage and hydrogen sectors. Venture funding complements strategic deals such as Daikin’s 49% stake in Miura Applied Systems, which blends HVAC and steam technologies into turnkey thermal-energy platforms. Overall, consolidation and partnership activity signal maturing technology trajectories and an intensifying race for channel access.

Electric Boiler Industry Leaders

Cleaver-Brooks

Bosch Thermotechnology

Chromalox (Spirax-Sarco)

Acme Engineering Products

Vapor Power International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Rinnai America unveiled its REHP Series electric heat-pump water heater, delivering up to 4.0 UEF, and commercial boilers rated 98% thermal efficiency, underscoring the company’s pivot toward fully electric portfolios.

- June 2024: AtmosZero secured USD 21 million Series A to advance industrial electric-steam technology focused on 200–300 °C applications.

- May 2025: FUJIFILM Holdings Corporation has introduced an electric boiler system at FUJIFILM Manufacturing Europe B.V.'s facilities in the Netherlands, which produce photographic materials and cell culture media.

- June 2025: Skretting Australia invested AUD 3.05 million to upgrade the boiler system at its Cambridge plant. Covered in the 2023 budget, the project replaced ageing gas boilers with low-voltage electric models, cutting CO₂ emissions by 8% and contributing significantly to its carbon reduction plan under Nutreco’s Roadmap 2025.

Global Electric Boiler Market Report Scope

| Electrode Boilers |

| Resistance Boilers |

| Induction Boilers |

| Hybrid Electric-Gas Boilers |

| Hot Water |

| Steam Generation |

| Process Heat (Up to 200 °C) |

| District and Campus Heating |

| Residential |

| Commercial and Institutional |

| Industrial |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Electrode Boilers | |

| Resistance Boilers | ||

| Induction Boilers | ||

| Hybrid Electric-Gas Boilers | ||

| By Application | Hot Water | |

| Steam Generation | ||

| Process Heat (Up to 200 °C) | ||

| District and Campus Heating | ||

| By End-user | Residential | |

| Commercial and Institutional | ||

| Industrial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the electric boiler market in 2025?

It was valued at USD 11.68 billion in 2025.

What CAGR is forecast for electric boilers from 2025-2030?

A 10.09% CAGR is projected through 2030.

Which region leads electric-boiler demand?

Asia-Pacific held 38.0% revenue share in 2024 and shows the fastest 11.3% CAGR outlook.

Why are hybrid electric boilers gaining traction?

They complement heat-pump efficiency by covering peak loads and offering grid-balancing flexibility, improving total economics.

What restrains rapid industrial adoption of >10 MW units?

High upfront capital costs and grid-capacity upgrades delay large installations despite favorable operating economics.

Who recently invested in industrial electric-steam technology?

AtmosZero raised USD 21 million Series A funding in 2024.

Page last updated on: