India Video Surveillance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.40 Billion |

| Market Size (2026) | USD 4.84 Billion |

| Market Size (2031) | USD 7.77 Billion |

| Growth Rate (2026 - 2031) | 9.94% CAGR |

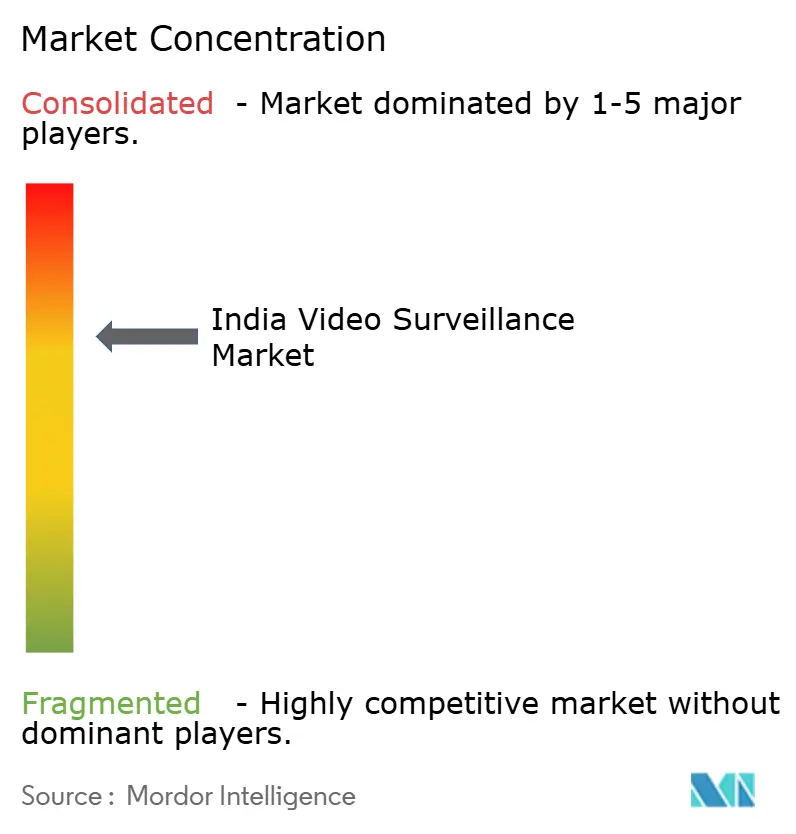

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Video Surveillance Market Analysis by Mordor Intelligence

The India video surveillance market size was valued at USD 4.40 billion in 2025 and estimated to grow from USD 4.84 billion in 2026 to reach USD 7.77 billion by 2031, at a CAGR of 9.94% during the forecast period (2026-2031). Demand accelerates as national and state agencies weave cameras into integrated command-and-control centers that manage traffic, safety and municipal services. Enterprises are replacing analog equipment with IP devices that bundle edge analytics, while falling hardware prices shorten replacement cycles. Data-sovereignty provisions in the Digital Personal Data Protection Act keep most large installations on-premises even as cloud-based video management gains traction among small and mid-sized firms. Competitive intensity is reshuffling as Chinese brands lose public-sector access, allowing domestic manufacturers and global technology suppliers to capture new contracts.

Key Report Takeaways

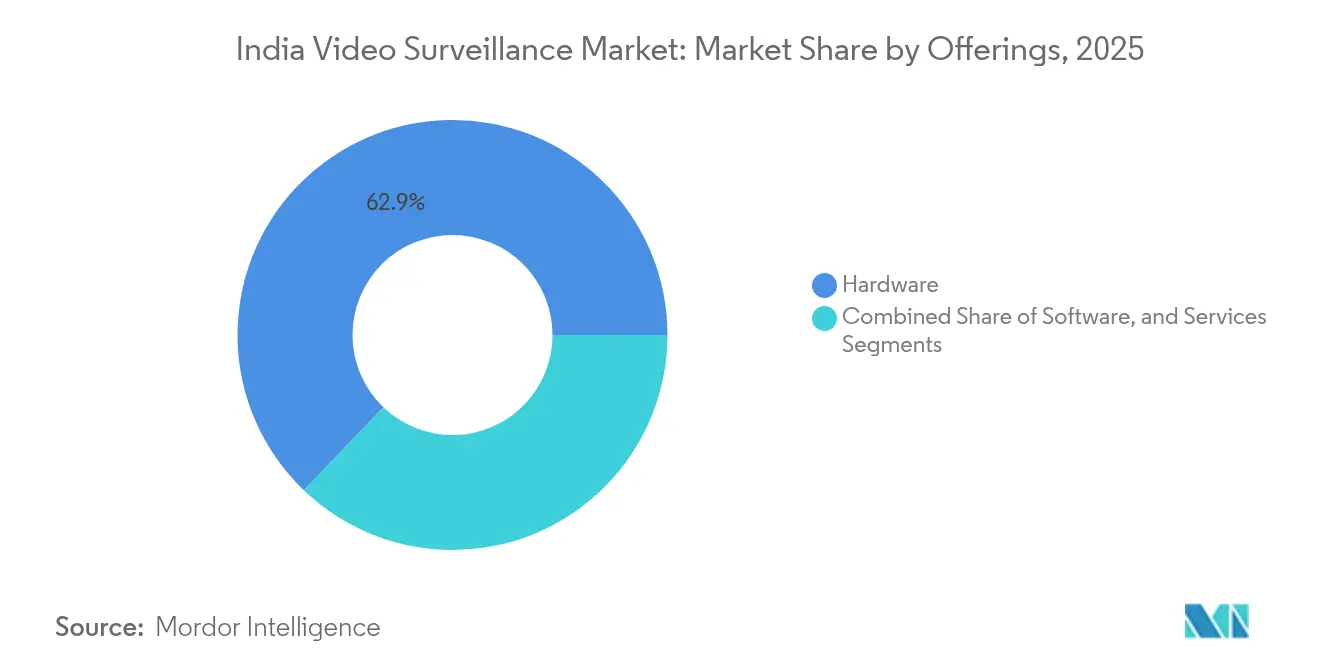

- By offering, hardware led with 62.85% of the India video surveillance market share in 2025, whereas Video-Surveillance-as-a-Service (VSaaS) posts the highest growth at 11.19% CAGR through 2031.

- By system, IP deployments commanded 54.73% of the India video surveillance market in 2025, and the IP segment is expanding at a 10.82% CAGR.

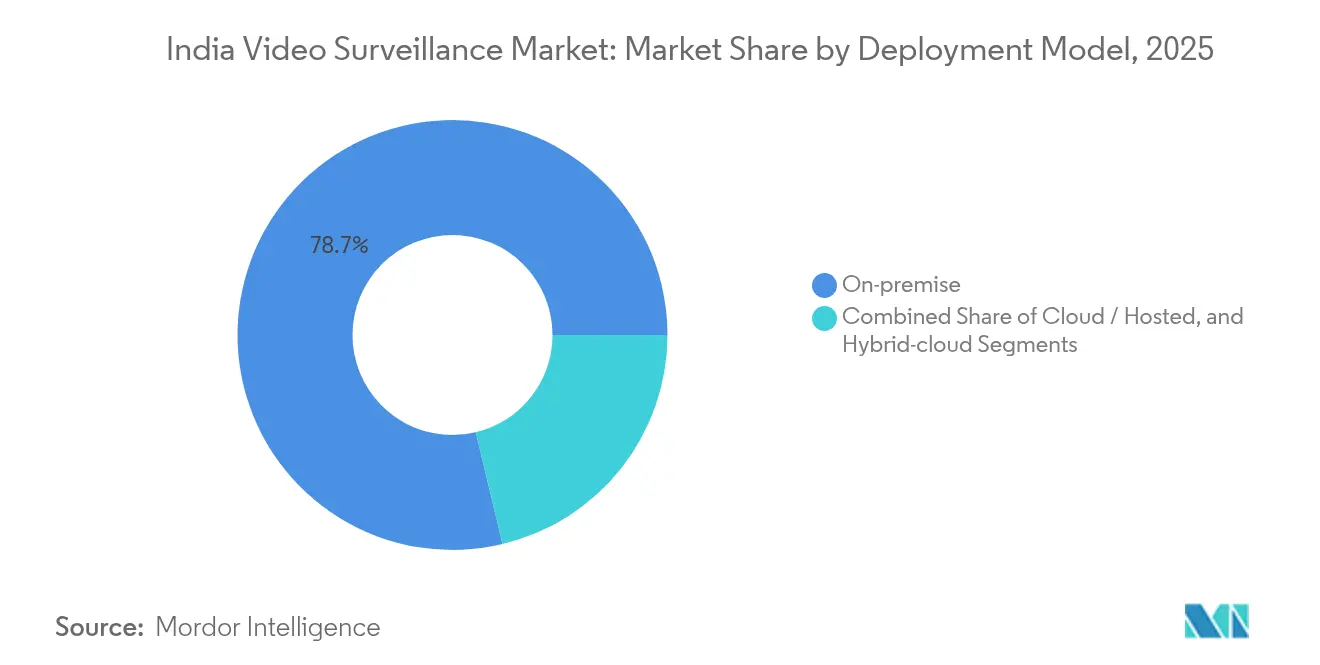

- By deployment model, on-premises held 78.74% share of the India video surveillance market size in 2025, while cloud architectures are expanding at an 11.08% CAGR.

- By end-user vertical, commercial facilities accounted for 28.05% of the India video surveillance market size in 2025, and infrastructure / smart-city rollouts are advancing at a 10.5% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Video Surveillance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IP-camera price erosion and performance leap | +2.3% | National, with early gains in tier-1 cities | Medium term (2-4 years) |

| Smart-city and Safe-city tenders (100-city mission) | +2.8% | National, concentrated in 100 designated smart cities | Long term (≥ 4 years) |

| Post-COVID shift to unmanned remote monitoring | +1.9% | Global, with strong adoption in commercial and institutional sectors | Short term (≤ 2 years) |

| Mandatory CCTV rules for banks, ATMs and schools | +1.7% | National, regulatory compliance driven | Medium term (2-4 years) |

| Edge-AI analytics for traffic-violation e-challans | +1.1% | State-level implementation, expanding to tier-2 cities | Medium term (2-4 years) |

| Solar-powered cameras for power-scarce sites | +0.8% | Rural and remote areas, northeastern states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IP Camera Price Erosion and Performance Leap

Entry-level network cameras now sit within 15% of HD-analog prices, removing cost objections and accelerating the India video surveillance market migration to IP platforms. Devices ship with embedded GPUs that execute object detection on the edge, cutting bandwidth by off-loading analytics from the server.[1]Press Release, “Bosch Building Technologies Launches Made-in-India FLEXIDOME Cameras,” bosch-press.in Vendors highlight future-proof firmware and Power-over-Ethernet to reduce installation costs. Procurement teams across tier-2 municipalities stipulate IP compliance in tender documents, ensuring interoperability with city-scale fiber backbones. As a result, replacement cycles have shortened to roughly five years, fueling recurring hardware demand.

Smart-City and Safe-City Tenders

The Smart Cities Mission allocates dedicated budgets for integrated surveillance, traffic analytics and emergency response nodes, ensuring multi-year order visibility for suppliers. Cameras form the sensor layer feeding command centers that manage lighting, parking and waste services, widening addressable use-cases for the India video surveillance market. Mohali’s system issued 1,150 e-challans on day one, proving the revenue-generation thesis and encouraging replication. Emerging tenders specify open-protocol VMS, nudging vendors toward ONVIF-compliant platforms.

Post-COVID Shift to Remote Monitoring and VSaaS

Lockdown restrictions normalized remote site management, prompting enterprises to centralize security operations and subscribe to VSaaS platforms that bundle storage, analytics and health monitoring. Monthly fees turn capital expense into operating expense, a strong fit for budget-focused SMEs entering the India video surveillance market. Mobile apps delivering real-time alerts now come standard, and cloud providers have opened local data centers to address sovereignty mandates. Hybrid architectures place critical footage on-premises while using cloud resources for analytics bursts, balancing compliance and scalability.

Mandatory CCTV Rules in Banks, ATMs and Schools

The Reserve Bank of India mandates continuous recording, facial clarity and tamper alarms for every ATM, driving steady demand even in mature metro markets. State education boards require full-campus coverage with 30-day retention, adding thousands of school sites annually to the India video surveillance market. Compliance audits create replacement cycles when cameras fail to meet low-light or storage standards, ensuring baseline growth independent of macro conditions. Integrators profit from long-term maintenance contracts as institutions outsource system health checks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and draft Digital Personal Data Bill | -1.8% | National, affecting all surveillance deployments | Medium term (2-4 years) |

| Cyber-attacks on Chinese-origin firmware | -1.2% | National, concentrated in government and critical infrastructure | Short term (≤ 2 years) |

| High GST slabs on fully-built cameras (28%) | -0.9% | National, impacting import-dependent segments | Short term (≤ 2 years) |

| Shortfall of trained VSaaS-ready integrators | -0.7% | Urban centers expanding to tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Personal Data Protection Act Compliance Costs

The 2023 Act forces private operators to run impact assessments, document consent flows and store footage in India, inflating project budgets by 8-12% on average.[2]Khaitan & Co., “How India’s New Data Protection Law Works at the Workplace,” khaitanco.com Cloud vendors responded with locally hosted tiers, yet encryption and audit logging remain mandatory. Uncertainty around final rules delays investment as boards weigh liabilities linked to biometric analytics. Government projects enjoy broad exemptions, tilting procurement in favor of public deployments.

Cyber-Attacks Targeting Chinese-Origin Firmware

Back-door vulnerabilities rated CVSS 10.0 in 2024 prompted the Ministry of Electronics and IT to require penetration testing and encryption on every camera sold in India.[3]Brian Karas, “Hikvision Backdoor Confirmed,” ipvm.com Procurers now score bids on cybersecurity compliance, eroding the low-price advantage of some imports. Public-sector bans under General Financial Rules 2017 exclude several Chinese brands, compelling integrators to redesign bills of material. Private firms also segment networks to isolate legacy Chinese devices, adding routing hardware and raising implementation costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Dominance with Rapid VSaaS Upswing

Hardware captured 62.85% of India video surveillance market share in 2025 and continues to anchor large government rollouts. Camera counts per intersection rise under safe-city mandates, while higher megapixel ratings drive demand for network-attached storage. Edge analytics modules built into cameras enable real-time incident detection without server overload. Services revenue scales in parallel because complex deployments need design, installation and annual maintenance contracts. Software growth centers on open-architecture video management systems that let operators mix camera brands and bolt on analytics without forklift upgrades. VSaaS, showing an 11.19% CAGR, wins mid-market accounts wanting subscription pricing and automated firmware updates, a pattern expected to double cloud-connected nodes by 2031.

Adoption of VSaaS also broadens geographic reach: smaller towns lacking local integrators can procure managed service bundles remotely. National payment gateways ease recurring billing, simplifying customer onboarding for platform providers. Regulatory push for cyber-secure devices steers buyers toward vendors offering end-to-end encrypted storage pipelines. Collectively, these factors sustain a robust hardware foundation while shifting incremental growth toward cloud-delivered functionality in the India video surveillance market.

By System: IP Leadership Amid Hybrid Transitional Paths

IP architectures accounted for 54.73% of 2025 deployments thanks to PoE cabling, remote configuration and firmware-level AI engines. Municipalities demand IPv6-ready cameras to future-proof their fiber backbones. Hybrid video recorders breathe new life into analog loops by digitizing them, granting cost-relief to public-school boards still operating legacy coaxial lines. Over the forecast, analog shipments shrink yet persist in cash-limited rural cooperatives. The India video surveillance market size for IP endpoints is projected to exhibit double-digit growth, fed by camera-embedded GPUs that allow people-masking to protect privacy before footage hits storage.

Systems integrators now pitch “IP-first” frameworks, adding media converters only where cable retrofits are infeasible. Failure diagnostics run remotely, reducing truck rolls and downtime. Network segmentation and device certificates address rising cyber-threats flagged by MeitY guidelines. At the same time, hybrid NVRs extend the life of sunk analog assets, smoothing capital allocation for districts phasing upgrades over multiple budget cycles.

By Deployment Model: On-Premises Preference Counter-Balanced by Cloud Momentum

On-premises architectures held 78.74% of the India video surveillance market in 2025 because state regulations obligate public-safety footage to remain inside national borders. Air-gapped storage clusters in police data centers assure chain-of-custody for evidence. Enterprises with dedicated IT staff maintain private networks to minimize latency and cyber risk. Nevertheless, cloud subscriptions are clocking an 11.08% CAGR, a trend propelled by affordable bandwidth tariffs and the operational appeal of managed patches.

Multisite retailers employ hybrid layouts, storing recent days on the edge for instant playback and archiving older footage in regional clouds. Cloud providers now issue cryptographic attestations that data reside in Indian availability zones, satisfying auditors. Integrated disaster recovery, auto-scaling analytics and per-camera licensing simplify TCO models, encouraging mid-tier adopters. This push-pull dynamic keeps on-premises revenues dominant while the incremental dollar tilts toward cloud in the India video surveillance market.

By End-User Vertical: Commercial Leads, Infrastructure Surges

Commercial facilities retained 28.05% of 2025 revenue, spanning organized retail, office campuses and hospitality. Theft mitigation, queue management and occupancy analytics justify upgrades every three to four years. Integration with POS and access-control platforms deepens return on investment, sustaining camera density per square meter. Infrastructure and smart-city projects, climbing at 10.5% CAGR, are funded through central grants and municipal bonds, propelling large-lot orders that reshape vendor rankings.

Airports and metros deploy analytics layers for unattended-bag alerts and crowd-flow predictions that feed scheduling algorithms. Border-security agencies adopt thermal drones linked to fixed camera grids, creating composite surveillance meshes. Residential societies gravitate to app-enabled cloud kits bundled with fiber broadband, extending growth into consumer segments. Collectively, these trends diversify revenue streams, stabilizing the India video surveillance market against single-sector shocks.

Geography Analysis

Western India, dominated by Maharashtra, Gujarat, and Karnataka, accounts for the largest slice of current deployments, underpinned by dense industrial corridors, IT parks, and early smart-city funding approvals. Mumbai’s high-rise clusters demand expansive CCTV grids that integrate with traffic control and emergency services, while Pune’s automotive plants deploy license-plate recognition for logistics yards. Gujarat’s Dholera Special Investment Region positions surveillance as core digital infrastructure, requiring resilient fiber rings and solar-powered poles for its arid terrain.

Northern states such as Delhi, Punjab, and Haryana post the fastest incremental gains as local governments exploit e-challan revenue to finance upgrades. Chandigarh’s 2,085 AI-enabled cameras generated 985,451 traffic violations in 2024, validating payback models that other municipalities rapidly emulate. Delhi’s high-security zone requires encrypted links and redundant storage housed within secretariat premises, pushing integrators toward Tier-4 data-center builds. Haryana’s agrarian belt, where power outages are common, is trialing solar-panel kits paired with 4G routers to keep village panchayat systems online. Southern hubs, Telangana, Tamil Nadu and Andhra Pradesh, feature sustained corporate demand and proactive state data-center policies that accelerate cloud adoption. Hyderabad incubates several VSaaS start-ups piggybacking on the state’s T-Hub innovation platform. Chennai’s manufacturing clusters integrate cameras with predictive-maintenance systems, linking vibration anomalies to real-time video for root-cause analysis. Coastal cyclone exposure drives hardened enclosures and stainless hardware specs, creating specialized sub-segments within the India video surveillance market. Eastern and northeastern states remain nascent yet promising as BharatNet fiber reaches remote blocks, unlocking connectivity for camera back-haul and centralized monitoring.

Competitive Landscape

Global incumbents, Bosch, Axis, Honeywell and Hanwha, leverage cybersecurity certifications and open APIs to win high-spec tenders. CP Plus leads domestic production with its Kadapa plant turning out 2.5 million units per month, helping it secure Make-in-India preference points in public bids. Magellanic Cloud’s February 2025 NSE listing funds R&D for its Scanalitix SaaS, aiming to serve the mid-market with AI-rich analytics.

Chinese brands still dominate private small-business channels through aggressive pricing, but bans on government contracts shrink their overall relevance within the India video surveillance market. Taiwanese ODMs quietly expand, offering white-label cybersecurity-hardened units to Indian brands. Strategic alliances surface: Bosch partners with RailTel for pan-India railway safety, while HCL teams with Axis to supply secured VMS for defense projects.

Technology roadmaps focus on edge AI, zero-trust device onboarding, and H.265+ compression to curb storage costs. Vendors differentiate via bundled analytics libraries, crowd density, PPE detection, and smoke alarms, rather than raw megapixel count. Customer support centers shift to regional languages, aligning with tier-3 city adoption. As market share realigns, partner training and post-install service quality emerge as decisive factors.

India Video Surveillance Industry Leaders

Axis Communications AB

Samsung Group

Robert Bosch GmbH (Security and Safety Systems)

Panasonic Connect Co., Ltd.

Honeywell International Inc. (Honeywell Security)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Punjab launched Phase-I of its AI-powered City Surveillance and Traffic Management System in Mohali, installing 351 high-resolution cameras across 17 junctions.

- February 2025: Magellanic Cloud Limited listed on the NSE to expand its indigenous VMS and analytics SaaS platform.

- January 2025: MeitY issued Draft Digital Personal Data Protection Rules 2025 for public consultation, outlining surveillance-data handling obligations.

- December 2025: Ahmedabad traffic police equipped 32 patrol cars with dash cameras and 28 mobile AI units linked to the One Nation, One Challan portal.

India Video Surveillance Market Report Scope

Video surveillance systems contain one or more video cameras connected to a network that sends the captured video or audio data to a specific location. The captured images are monitored in real-time or sent to a central location for recording and storage. Many applications, such as crime prevention, industrial process monitoring, and traffic management, increasingly utilize video surveillance systems.

The Indian video surveillance systems market is segmented by type (hardware [camera [analog, IP cameras, and hybrid], storage], software [video analytics, video management software], and services [VSaaS]) and end-user vertical (commercial, infrastructure, institutional, industrial, defense, and residential). The report offers market forecasts and size in value (USD) for all the above segments.

| Hardware | Cameras | Analog |

| HD-Analog (HD-TVI/CVI/AHD) | ||

| IP / Network | ||

| Storage (DVR, NVR, NAS, SAN) | ||

| Monitors and Accessories | ||

| Software | Video Management Software (VMS) | |

| Video Analytics | ||

| Services | Video Surveillance-as-a-Service (VSaaS) |

| Analog |

| IP |

| Hybrid |

| On-premises |

| Cloud / Hosted |

| Hybrid-cloud |

| Commercial |

| Infrastructure and Smart-City |

| Institutional (Education and Healthcare) |

| Industrial and Manufacturing |

| Defense and Homeland Security |

| Residential |

| Other End-user Verticals |

| By Offering | Hardware | Cameras | Analog |

| HD-Analog (HD-TVI/CVI/AHD) | |||

| IP / Network | |||

| Storage (DVR, NVR, NAS, SAN) | |||

| Monitors and Accessories | |||

| Software | Video Management Software (VMS) | ||

| Video Analytics | |||

| Services | Video Surveillance-as-a-Service (VSaaS) | ||

| By System | Analog | ||

| IP | |||

| Hybrid | |||

| By Deployment Model | On-premises | ||

| Cloud / Hosted | |||

| Hybrid-cloud | |||

| By End-user Vertical | Commercial | ||

| Infrastructure and Smart-City | |||

| Institutional (Education and Healthcare) | |||

| Industrial and Manufacturing | |||

| Defense and Homeland Security | |||

| Residential | |||

| Other End-user Verticals | |||

Key Questions Answered in the Report

What is the current value of the India video surveillance market?

The market stands at USD 4.84 billion in 2026 and is projected to expand steadily through 2031.

Which segment grows fastest within Indian video surveillance?

Video-Surveillance-as-a-Service posts the highest CAGR at 11.19%, propelled by SME and multi-site retail adoption.

How does the Digital Personal Data Protection Act affect surveillance rollouts?

It raises compliance costs through data-localization, encryption and audit requirements, nudging buyers toward certified vendors.

Why are IP cameras overtaking analog in India?

Price gaps have narrowed, and IP models provide edge analytics, PoE power and easier integration with smart-city networks.

Which regions deploy the most surveillance systems?

Western states such as Maharashtra, Gujarat and Karnataka lead in installed base, while northern states record the fastest year-on-year growth.

Page last updated on: