China Surveillance Storage Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

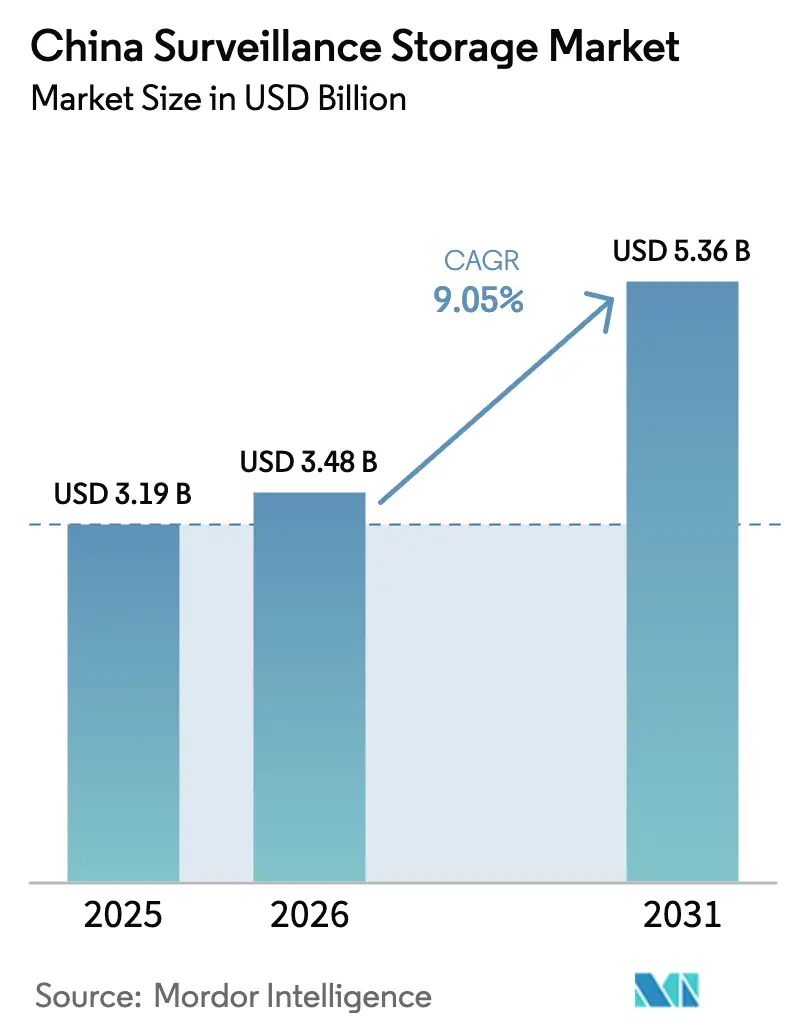

| Base Year Market Size (2025) | USD 3.19 Billion |

| Market Size (2026) | USD 3.48 Billion |

| Market Size (2031) | USD 5.36 Billion |

| Growth Rate (2026 - 2031) | 9.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Surveillance Storage Market Analysis by Mordor Intelligence

The China surveillance storage market size is expected to grow from USD 3.19 billion in 2025 to USD 3.48 billion in 2026 and is forecast to reach USD 5.36 billion by 2031 at 9.05% CAGR over 2026-2031. Robust fiscal outlays behind the Sharp Eyes Phase-III build-out, mandatory 90-day video retention rules, and the ongoing “Eastern Data Western Compute” re-architecture jointly reinforce sustained demand for petabyte-scale repositories. High-resolution camera proliferation, especially 8 MP and 4 K devices, is lifting ingest rates to 20 Tbps and above, nudging buyers toward NVMe-accelerated tiering models. Edge-to-core data flows, enabled by 100 Gbps links, keep latency below 10 ms for real-time analytics even as archival workloads migrate to western data-center clusters powered largely by renewable energy. Supply-chain localization, propelled by heightened US export controls, continues to influence pricing, lead times, and specifications across the value chain. Finally, rising utility tariffs in coastal provinces are shifting deployment preferences toward energy-efficient hardware and western low-cost power zones.

Key Report Takeaways

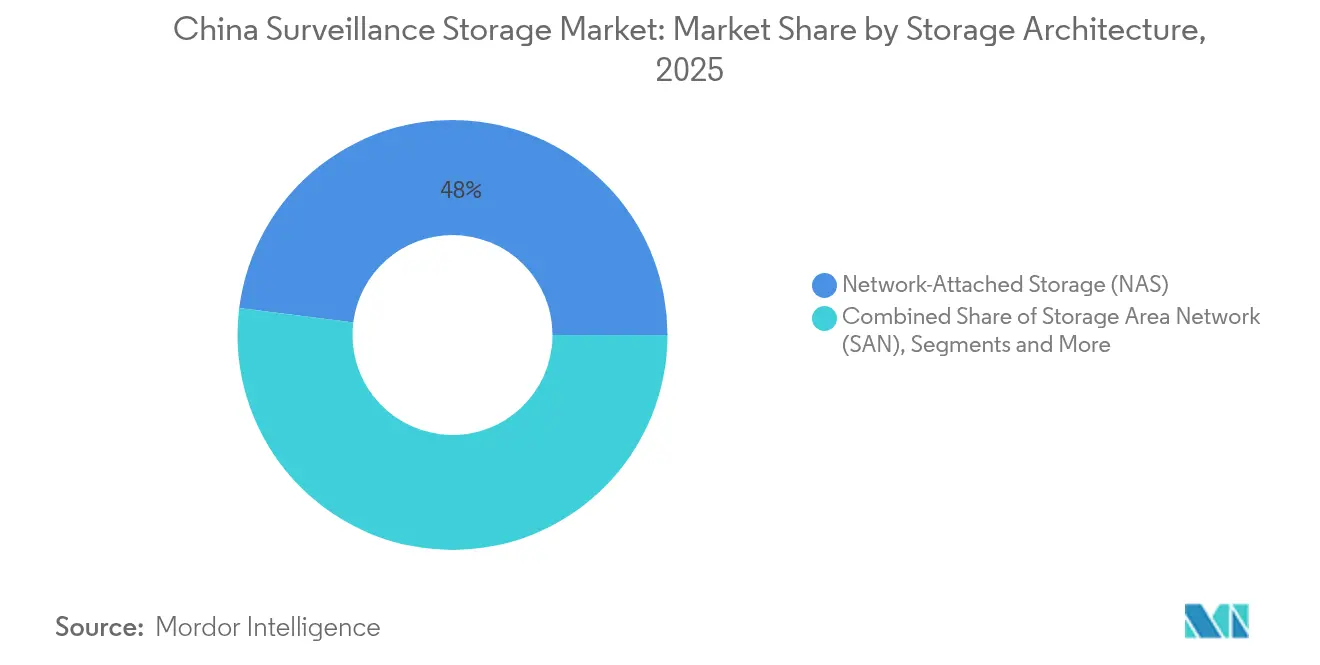

- By storage architecture, Network-Attached Storage led with 48.00% of 2025 revenue, while hyper-converged video appliances are forecast to expand at a 11.72% CAGR to 2031

- By storage media, surveillance-optimised HDDs retained 70.75% of 2025 demand; NVMe SSDs record the fastest 10.12% CAGR through 2031

- By deployment, on-premise edge and core installations held 62.45% of 2025 revenue; public-cloud VSSaaS is set to grow at 10.36% CAGR through 2031

- By capacity tier, the >16 TB class is projected to post an 11.09% CAGR, whereas 8-16 TB drives captured 37.80% of the China surveillance storage market share in 2025

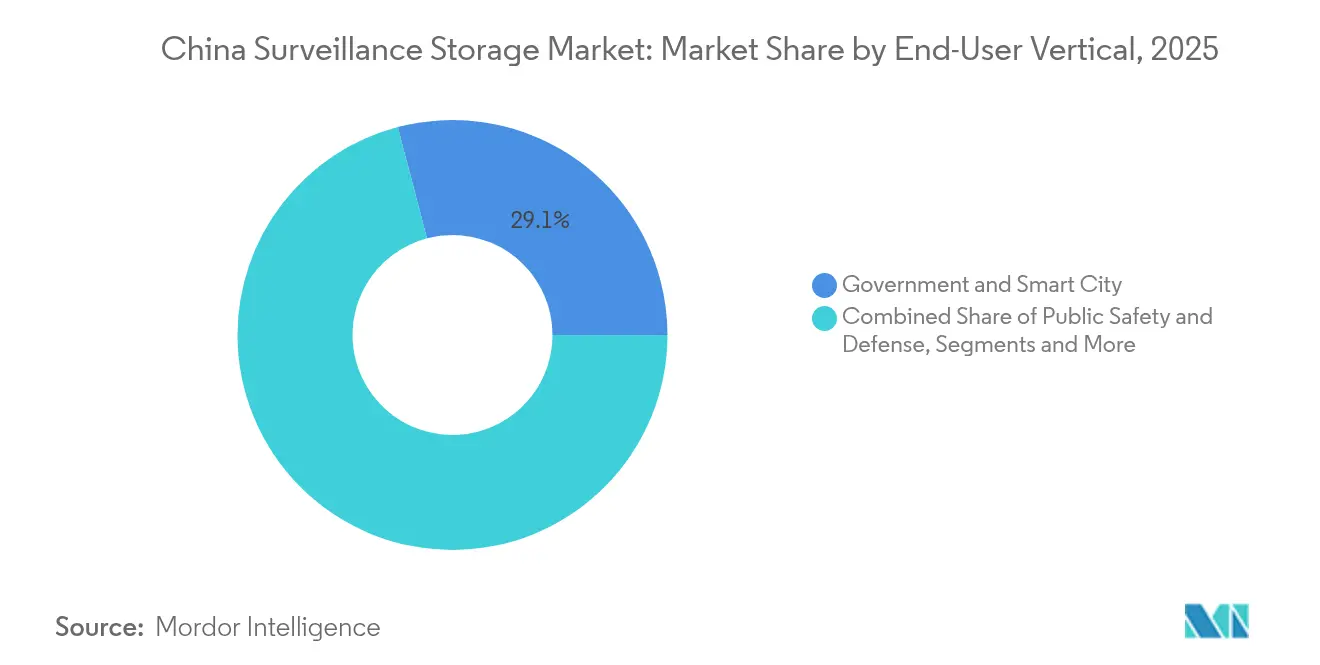

- By end-user vertical, Government & Smart City captured 29.10% revenue in 2025; Healthcare will grow at a 9.88% CAGR to 2031

- By camera resolution, 5-8 MP units represented 35.85% of 2025 shipments, yet >8 MP/4K devices are on track for a 10.44% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Surveillance Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Roll-out of "Sharp Eyes" Phase-III Projects in Tier-3/4 Cities | +2.1% | National, with concentrated deployment in Jiangsu, Shandong, Henan tier-3/4 municipalities | Medium term (2-4 years) |

| Mandatory ≥90-Day Video Retention Rules for Key Vertical Sites (Public Security Ministry Notice 785) | +1.8% | National, with stricter enforcement in Beijing, Shanghai, Guangdong provincial jurisdictions | Short term (≤ 2 years) |

| Edge-to-Core Architecture Upgrades in China's "Eastern Data Western Compute" Program | +1.5% | National, with primary hubs in Inner Mongolia, Guizhou, Gansu, Ningxia | Long term (≥ 4 years) |

| Surge in 8 MP + Camera Deployments for AI Analytics Requiring ≥20 Tbps Ingest | +1.3% | National, with early adoption in Tier-1 cities expanding to Tier-2/3 markets | Medium term (2-4 years) |

| Rapid Price Decline of 20+ TB SMR HDDs Enabling Petabyte-Scale NVRs | +1.0% | Global supply chain impact with domestic assembly concentration in Shenzhen, Suzhou | Short term (≤ 2 years) |

| Adoption of AI-Optimised NVMe SSD Caching in Traffic-Management Command Centres | +0.9% | National, with priority deployment in major transportation hubs and smart city projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Roll-out of “Sharp Eyes” Phase-III Projects in Tier-3/4 Cities

Phase-III deployments typically add 15 000–25 000 cameras per city and generate monthly data volumes of 2–4 PB, compelling local authorities to procure high-density arrays with mixed SSD–HDD tiers. Real-time facial recognition and “One Person, One File” mandates are amplifying active-storage demand, while government subsidies accelerate procurement cycles targeting 80% coverage by 2026. Hybrid NAS clusters dominate as they blend cost-effectiveness with ease of scaling, positioning the China surveillance storage market for sustained double-digit urban tier expansion.

Mandatory ≥90-Day Video Retention Rules for Key Vertical Sites

Notice 785 requires critical facilities, hospitals, transportation hubs, financial institutions, and schools to triple their storage reserves, transitioning from 30-day to 90-day buffers. Healthcare organizations now average 500–800 TB per hospital for compliance, promoting blockchain-based WORM options for evidentiary protection. Consolidation pressure on smaller operators amplifies the demand for cloud storage-as-a-service; however, domestic data-residency clauses often lock most contracts to Chinese providers, thereby reinforcing revenue for local vendors in the China surveillance storage market.

Edge-to-Core Architecture Upgrades in “Eastern Data Western Compute”

Eight national super-nodes and ten regional clusters will host 300 EFLOPS by 2025, with surveillance analytics a primary workload. Edge devices buffer short-term feeds while western-region data lakes store long-term archives at electricity rates 40–60% lower than coastal averages. Consequently, inter-cluster replication requirements spur adoption of 100 Gbps fibre and software-defined storage that orchestrates data placement by latency, cost, and sovereignty, driving heterogeneous procurements across the China surveillance storage market.

Surge in 8 MP+ Camera Deployments for AI Analytics

Sustained ingest rates above 20 Tbps force arrays to fuse NVMe caches with massive HDD pools to maintain sub-millisecond fetch times for AI-driven alerts. Dynamic tiering engines now relocate footage according to analytic value, ensuring critical seconds remain on flash while bulk archives transition to SMR media. This architectural evolution underpins a higher ASP per terabyte, materially lifting value growth within the China surveillance storage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Risk from US BIS Restrictions on Advanced NAND & Controller ICs | -1.4% | National, with acute impact on Shenzhen, Shanghai technology manufacturing hubs | Short term (≤ 2 years) |

| Rising Electricity Tariffs Undermining OPEX of Provincial Data-Lake Nodes | -0.8% | National, with severe impact in Guangdong, Jiangsu, Zhejiang industrial provinces | Medium term (2-4 years) |

| Fragmented Provincial Cyber-Security Audits Delaying Cloud VSSaaS Uptake | -0.6% | National, with varying implementation across provincial jurisdictions | Medium term (2-4 years) |

| Short Lifecycle (≤3 yrs) of Consumer-Grade SD Cards in SMB/Home Segments | -0.4% | National, with concentrated impact in tier-3/4 cities and rural deployment areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Risk from US BIS Restrictions on Advanced NAND & Controller ICs

The October 2025 BIS update casts a licensing net over storage controllers and advanced NAND, inflating input prices 15–25% as Chinese vendors pivot to second-tier sources.[1]U.S. Department of Commerce, “Commerce Strengthens Restrictions on Advanced Computing Semiconductors,” bis.govYMTC’s capacity build-out narrows the gap yet still trails global peers by two nodes, curbing performance envelopes for high-end appliances. Short-term volatility confines feature adoption such as PCIe 5.0 and computational storage, marginally suppressing top-line growth for the China surveillance storage market

Rising Electricity Tariffs Undermining OPEX of Provincial Data-Lake Nodes

Industrial electricity rates climbed 12–18% year-on-year in coastal provinces, squeezing cloud VSSaaS margins. Operators employ drive spin-down and chilled-water retrofits but still face opex headwinds that shift new workloads to western green-power clusters. The resulting east–west data segmentation demands additional replication overhead, adding complexity to the China surveillance storage market’s cost equation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Architecture: NAS Dominance, Hyper-Converged Momentum

NAS accounted for 48.00% revenue in 2025, cementing its role as the de facto backbone for multi-site roll-outs across public-sector deployments.Its IP-based simplicity lowers administrative overhead while satisfying the mandatory 90-day retention frameworks, providing a proven baseline for the China surveillance storage market to expand into tier-3/4 cities. SAN continues to serve workloads that demand deterministic sub-millisecond performance, whereas DAS sustains niche, air-gapped scenarios.

Hyper-converged appliances, combining compute, GPU, and storage, exhibit a 11.72% CAGR through 2031, propelled by AI edge analytics. Municipal traffic bureaus adopting these nodes record 35% rack-footprint savings and faster rollout intervals. Vendors now preload Kubernetes-ready data services, reducing post-install engineering and contributing incremental value per terabyte within the China surveillance storage market.

By Storage Media: HDD Reliability Meets NVMe Acceleration

Surveillance-optimised HDDs retained 70.75% of 2025 shipments, leveraging firmware tuned for 24/7 workloads and vibration damping. Meanwhile, 30 TB HAMR drives introduced in 2024 enable 1.2 PB per 4U chassis, cutting rack counts by 40%. Enterprise and data-center HDDs serve high-capacity archival applications, while SATA SSDs provide performance acceleration for frequently accessed video content and metadata indexing operations.

NVMe SSDs, growing at 10.12% CAGR, furnish the flash tier essential for AI model inference. Hybrid flash arrays blending QLC NVMe with SMR HDDs now underpin edge-core hierarchies, sustaining throughput while trimming acquisition cost for the China surveillance storage market. The storage media landscape is experiencing significant technological advancement, with manufacturers like Seagate introducing 30TB HAMR (Heat-Assisted Magnetic Recording) drives that enable petabyte-scale deployments in compact form factors.

By Deployment: Edge Dominance with Cloud Upside

On-premise edge and core configurations captured 62.45% of 2025 spend, underscoring data-sovereignty imperatives as well as real-time analytics needs. Edge recorder clusters safeguard operation continuity during network brownouts, a critical factor for tier-3/4 municipal grids. Core data-center deployments provide centralized storage and processing capabilities for multi-site surveillance operations, with typical installations supporting 10,000-50,000 cameras across distributed locations.

However, public cloud VSSaaS represents the fastest-growing segment at 10.36% CAGR through 2031, driven by cost optimization initiatives and the availability of AI-powered analytics services that would be prohibitively expensive to deploy on-premise. Hybrid models, orchestrated via single-pane-of-glass consoles, now migrate cold archives to green-energy western facilities, reducing footprint in the more expensive coastal metro zones of the China surveillance storage market.

By Capacity Tier: Shift Toward 20 TB+ Drives

The 8–16 TB bracket delivered 37.80% of revenue in 2025, representing a sweet spot that balances unit cost with rack density requirements for 500–2,000 camera installations. This capacity range aligns with standard rack configurations and power consumption constraints while providing sufficient storage for 30-90 day retention requirements mandated by regulatory frameworks.

Above 16 TB, volumes expand at an 11.09% CAGR, thanks to SMR and HAMR advances. Governments favour high-capacity tiers to streamline maintenance by reducing the drive count per rack, thereby lowering the risk of vibration-induced failure. Greater density also compresses power envelopes-yet further evidence of sustainability becoming a purchase criterion in the China surveillance storage market. The capacity tier evolution reflects technological advancements in drive density and the economic benefits of deploying fewer, higher-capacity drives to reduce infrastructure complexity and operational costs.

By End-User Vertical: Public Sector Leads, Healthcare Accelerates

Government & Smart City applications commanded a 29.10% share in 2025, propelled by Sharp Eyes budgets and national security mandates. Projects integrate traffic, police, and urban-management feeds into unified command platforms. Public Safety & Defense applications maintain a strong demand for high-security storage solutions with advanced encryption and access control features, while the Transportation and Logistics sectors implement specialized storage systems for cargo monitoring and fleet management applications.

Healthcare, posting a 9.88% CAGR, reflects stringent retention rules for patient-area monitoring and drug custody, making blockchain WORM arrays standard for audit compliance. BFSI and retail sectors employ advanced analytics to bolster fraud detection and shopper insights; nonetheless, procurement cycles remain longer compared to public tenders, moderating their share expansion within the China surveillance storage market.

By Camera Resolution: 4K Uptake Stokes Throughput

While 5–8 MP devices held 35.85% shipment share in 2025, >8 MP/4K cameras advance at 10.44% CAGR, driven by AI object-recognition accuracy gains. Each 4K stream doubles bitrate against 1080p, pushing integrators toward multi-tier architectures with NVMe front-ends. The resolution evolution reflects the industry's transition toward AI-powered surveillance systems that require high-quality imagery for advanced analytics capabilities including facial recognition, license plate reading, and behavioral pattern analysis.

Adaptive compression engines reduce bitrates by 35% during low-motion intervals, mitigating budget impact. This capability, however, raises metadata management complexity, which vendors now address via GPU-assisted encoding modules inside leading China surveillance storage market platforms.

Geography Analysis

Tier-1 cities, including Beijing, Shanghai, Guangzhou, and Shenzhen, host mature surveillance systems with over 50,000 cameras each, necessitating multi-petabyte mirrored clusters interfaced with national intelligence grids.Their early adoption of 8 MP+ cameras and AI behavioral analytics has positioned them as technology testbeds that influence national procurement standards. As these municipalities embrace containerised edge nodes, the China surveillance storage market benefits from premium ASPs and trailblazing reference architectures.

Tier-2 and tier-3 cities constitute the principal growth reservoir as Phase-III Sharp Eyes budgets cascade downward. Municipalities of 5,00,000–3 million residents typically deploy 15,000–25,000 cameras, translating into 2-4 PB incremental demand per city. Vendors offering turnkey financing and managed services gain traction as local governments balance capital constraints with compliance deadlines. Here, the China surveillance storage market witnesses elevated competition from domestic integrators employing fully localised component stacks.

Western provinces, including Inner Mongolia, Guizhou, Gansu, and Ningxia, now attract archival workloads under Eastern Data Western Compute. Renewable power rates 40–60% below coastal tariffs and cool ambient temperatures reduce PUE, enabling aggressive multi-tenancy economics. Data-sovereignty clauses keep physical media within China, further anchoring spend inside national borders. Rural and border regions, although smaller in absolute volumes, procure ruggedised enclosures rated for dust, vibration, and extended temperatures, diversifying demand dynamics in the overarching China surveillance storage market.

Competitive Landscape

Market concentration remains moderate, with the top five vendors holding roughly 45% of the revenue, signaling room for challenger incursion. Hikvision and Dahua leverage vertical stacks that span cameras, NVRs, and storage arrays, yielding price-performance packages that are difficult for pure-play storage firms to counter. Huawei positions its OceanStor Pacific line as an AI-ready data lake, bundling heterogeneous media under a unified namespace. Western brands, such as Dell, NetApp, and Hitachi, focus on enterprise-grade resiliency for BFSI and healthcare but face longer security-review cycles.

Strategic moves centre on full-stack integration. Huawei’s May 2025 launch of an AI data lake platform simplifies deployment by collapsing analytics, compute, and storage layers, slashing provisioning time by 35%. Dahua’s sale of consumer-facing Lorex refocuses resources on core professional segments, sharpening R&D on AI-optimised firmware. International suppliers face supply-chain friction from BIS rules, prompting joint ventures with domestic fabs to maintain their local market share in China's surveillance storage market.

Helium-filled drives, adaptive caching, and containerised cooling score points in western data-centre tenders tied to national green mandates. Cyber-resiliency emerges as another battleground; immutable snapshots and zero-trust transport protocols increasingly appear in RFPs as municipalities seek to harden infrastructure against ransomware. Vendors able to certify compliance with the March 2025 facial-recognition data-protection decree gain a procurement edge. Collectively, these vectors elevate the sophistication ceiling and encourage ecosystem alliances throughout the China surveillance storage market.

China Surveillance Storage Industry Leaders

Hangzhou Hikvision Digital Technology Co., Ltd.

Dahua Technology Co., Ltd

Seagate Technology Holdings plc

Western Digital Corp.

Huawei Technologies Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Huawei debuted its full-stack AI data-lake platform for surveillance analytics, integrating OceanStor Pacific storage with compute.

- March 2025: National Internet Information Office issued facial-recognition security rules mandating encryption and access audits, reshaping system design.

- January 2025: U.S. Commerce Department tightened export controls on advanced storage controllers, prompting Chinese OEMs to accelerate domestic silicon road-maps.

- April 2024: Seagate unveiled 30 TB HAMR HDDs under the Mozaic 3+ banner, offering higher density for surveillance arrays.

China Surveillance Storage Market Report Scope

Surveillance systems refer to a combination of recording devices installed for surveillance to prevent crime in private and public locations. Data storage is a critical component of the surveillance infrastructure. The scope and the market size only cover the video surveillance storage market.

The Chinese surveillance storage market is segmented by product (NAS, SAN, and DAS), storage media (HDD and SSD), deployment (cloud and on-premise), and end-user vertical (government and defense, education, BFSI, retail, transportation and logistics, utilities, healthcare, home security, and other end-user verticals). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Network-Attached Storage (NAS) |

| Storage Area Network (SAN) |

| Direct-Attached Storage (DAS) |

| Hyper-Converged Video Storage Appliances |

| Surveillance-Optimised HDD |

| Enterprise / Data-centre HDD |

| SATA SSD |

| NVMe SSD |

| Hybrid Flash Array |

| On-Premise Edge Recorder |

| On-Premise Core Data-Centre |

| Public Cloud VSSaaS |

| Private / Hybrid Cloud |

| ≤4 TB |

| 4 - 8 TB |

| 8 - 16 TB |

| > 16 TB |

| ≤2 MP |

| 2 - 5 MP |

| 5 - 8 MP |

| > 8 MP / 4K |

| Government and Smart City |

| Public Safety and Defense |

| Transportation and Logistics |

| BFSI |

| Retail and Mall |

| Education |

| Healthcare |

| Energy and Utilities |

| Manufacturing and Industrial |

| Home and SMB |

| By Storage Architecture | Network-Attached Storage (NAS) |

| Storage Area Network (SAN) | |

| Direct-Attached Storage (DAS) | |

| Hyper-Converged Video Storage Appliances | |

| By Storage Media | Surveillance-Optimised HDD |

| Enterprise / Data-centre HDD | |

| SATA SSD | |

| NVMe SSD | |

| Hybrid Flash Array | |

| By Deployment | On-Premise Edge Recorder |

| On-Premise Core Data-Centre | |

| Public Cloud VSSaaS | |

| Private / Hybrid Cloud | |

| By Capacity Tier (Per Device) | ≤4 TB |

| 4 - 8 TB | |

| 8 - 16 TB | |

| > 16 TB | |

| By Camera Resolution Supported | ≤2 MP |

| 2 - 5 MP | |

| 5 - 8 MP | |

| > 8 MP / 4K | |

| By End-User Vertical | Government and Smart City |

| Public Safety and Defense | |

| Transportation and Logistics | |

| BFSI | |

| Retail and Mall | |

| Education | |

| Healthcare | |

| Energy and Utilities | |

| Manufacturing and Industrial | |

| Home and SMB |

Key Questions Answered in the Report

What is the current size of the China surveillance storage market?

It stands at USD 3.48 billion in 2026, with a forecast to reach USD 5.36 billion by 2031 at a 9.05% CAGR.

Which storage architecture leads the market?

Network-Attached Storage leads with 48.00% revenue share in 2025, favored for its plug-and-play scalability.

How are 4K cameras affecting storage demand?

4K adoption is growing at a 10.44% CAGR, doubling bitrate per stream and accelerating deployment of NVMe-accelerated tiered arrays.

Why is Western China becoming an archival hub?

Renewable energy availability and electricity prices 40–60% below coastal averages make western data centres cost-effective for long-term storage.

How do new US export controls influence suppliers?

Restrictions on NAND and controller ICs raise component costs 15–25%, prompting Chinese vendors to localise semiconductor production.

What vertical shows the fastest growth?

Healthcare leads with a 9.88% CAGR to 2031, driven by regulatory mandates for comprehensive patient-area monitoring.

Page last updated on: