Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

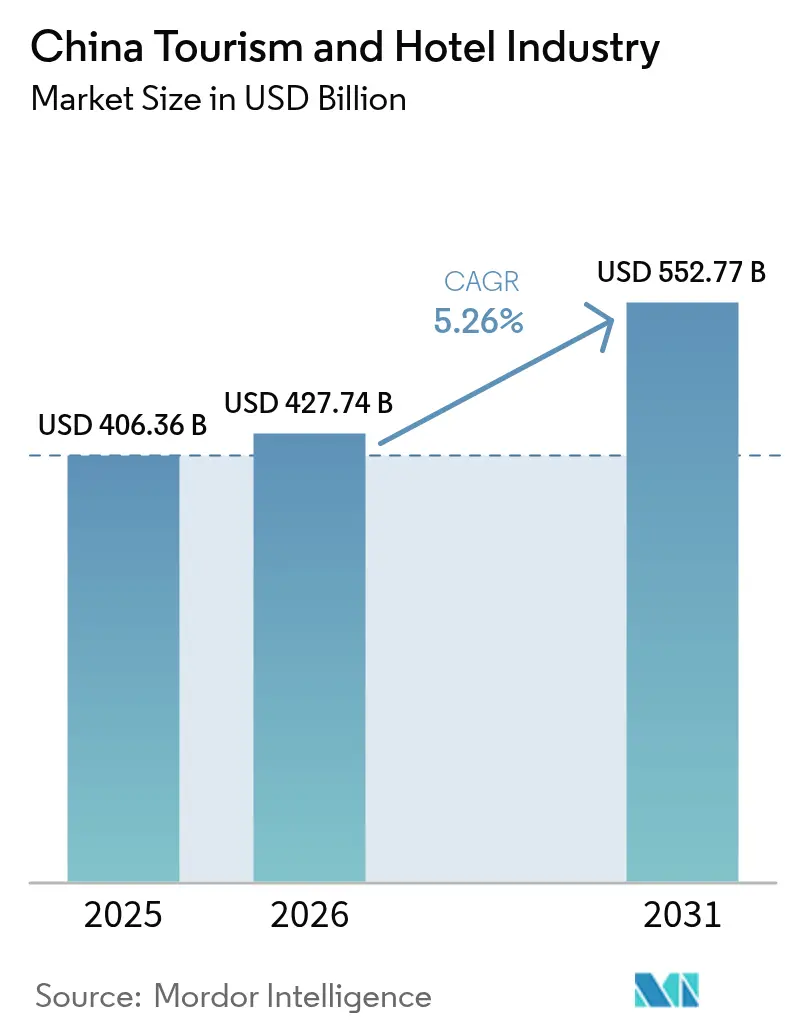

| Base Year Market Size (2025) | USD 406.36 Billion |

| Market Size (2026) | USD 427.74 Billion |

| Market Size (2031) | USD 552.77 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Tourism And Hotel Industry Analysis by Mordor Intelligence

The China Tourism And Hotel Industry market size is expected to grow from USD 406.36 billion in 2025 to USD 427.74 billion in 2026 and is forecast to reach USD 552.77 billion by 2031 at 5.26% CAGR over 2026-2031.

The China tourism and hotel industry stands at USD 406.36 billion in 2025 and is on track to reach USD 531.86 billion by 2030, supported by a healthy 5.31% CAGR. Domestic travel remains the backbone of demand, but a rebound in inbound arrivals, an expanding middle class, and rising wealth in lower-tier cities are widening revenue streams. Large-scale investment in railways, airports, and highways has opened fresh development corridors for hotel operators, while digital booking ecosystems continue to reshape distribution economics. Competition is intensifying in the mid-scale tier, yet the luxury pipeline is accelerating as affluent Chinese consumers seek high-touch, experiential stays. Tightening environmental rules and price pressure in smaller cities will test operator margins, but policy support for tourism and steady growth in event-related demand give the sector breadth and resilience.

Key Report Takeaways

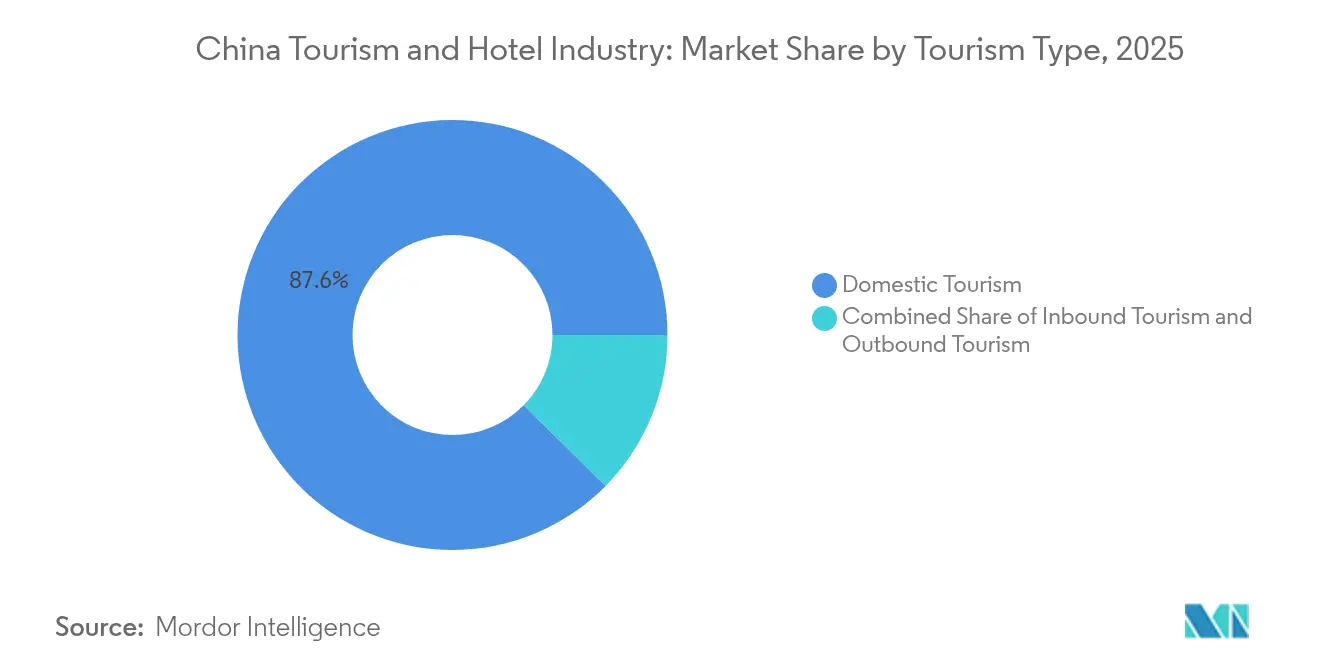

- By tourism type, domestic travel led with an 87.62% share of the China tourism and hotel industry in 2025; inbound tourism is forecast to expand at an 8.24% CAGR through 2031.

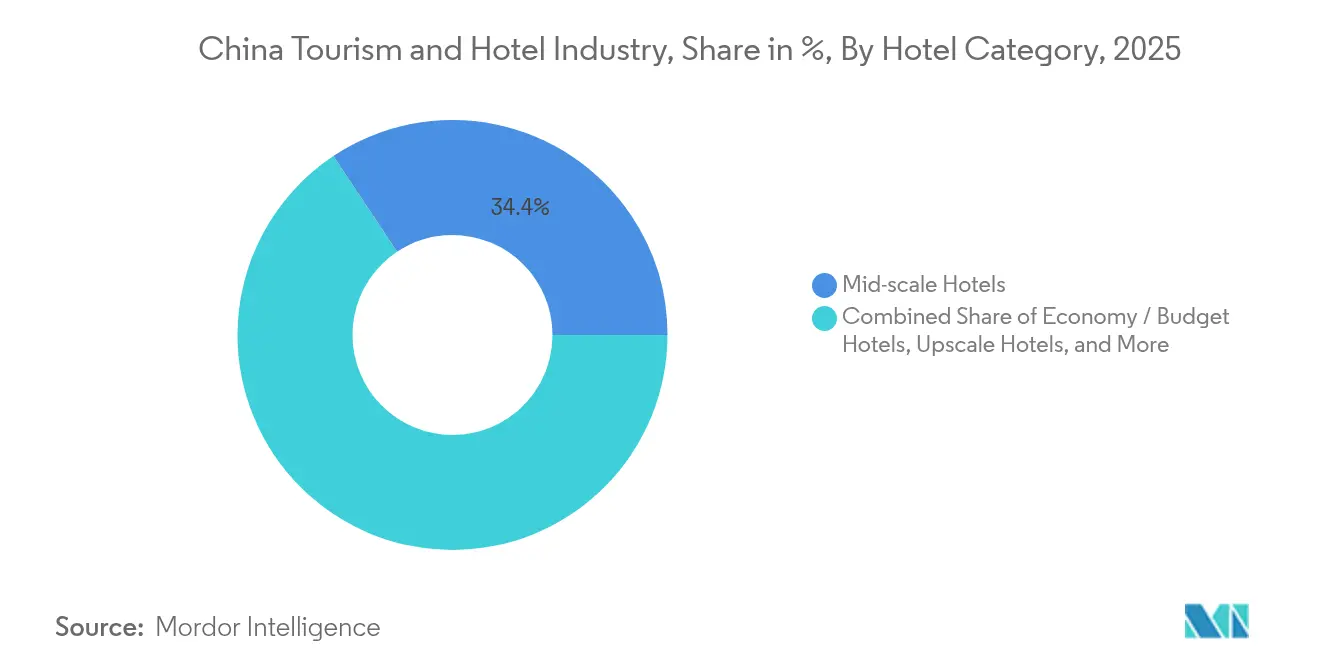

- By hotel category, mid-scale properties held 34.35% of the China tourism and hotel industry share in 2025, while luxury hotels are pacing the fastest growth at 9.52% CAGR to 2031.

- By purpose, leisure, adventure, and eco-tourism captured 63.25% of the China tourism and hotel industry size in 2025, whereas business and MICE postings are growing at a 12.05% CAGR through 2031.

- By booking channel, OTAs commanded 54.10% of the China tourism and hotel industry size in 2025; super-app ecosystems are rising at 11.78% CAGR between 2026-2031.

- By ownership, independent hotels accounted for 46.20% of the China tourism and hotel industry in 2025, but international chains are expanding at a 9.55% CAGR to 2031.

- The five leading operators—Jin Jiang International, Huazhu Group, BTG Homeinns, Marriott International, and Hilton Worldwide holds substantial market share of the China tourism in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Tourism And Hotel Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization & Infrastructure Development | +2.1% | National, with concentration in Tier 2 and Tier 3 cities | Long term (≥ 4 years) |

| Government Support & Policies Promoting Inbound and Domestic Tourism | +1.6% | Global, with emphasis on key source markets | Medium term (2-4 years) |

| Expansion of Luxury and Boutique Hotels | +0.8% | Tier 1 cities and premium tourism destinations | Medium term (2-4 years) |

| Increase in Event-Driven Tourism (MICE, Sports, Mega-Events) | +0.5% | Major urban centers (Beijing, Shanghai, Guangzhou) | Short term (≤ 2 years) |

| Growth in Domestic Tourism | +0.3% | National, with focus on cultural and natural attractions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urbanization and Infrastructure Development

Second- and third-tier cities are enjoying an unprecedented wave of hotel construction as high-speed rail and regional airports shorten travel times and lower trip costs. Developers have clustered around new transit hubs, converting land near stations into mixed-use districts anchored by mid-scale and upper-mid-scale hotels. The resulting spillover demand has broadened the China tourism and hotel market beyond traditional coastal gateways, spreading risk for operators and exposing investors to faster-growing local economies. The shift also underpins a deeper pipeline of domestically managed franchised hotels, many of which fit evolving government standards on green construction and energy efficiency.

Government Support and Policies Promoting Tourism

Streamlined e-visa procedures, expanded visa-free entry agreements, and nationwide destination marketing campaigns are spurring inbound arrivals, reinforcing confidence among international brands that paused projects in 2022-2023. Parallel reforms in mobile payment interoperability for foreign cards reduce day-to-day friction for guests, smoothing their path from the arrival hall to the hotel check-in. Local authorities continue to subsidize heritage site upgrades and rural homestay initiatives, widening the product mix under the China tourism and hotel market umbrella. These measures help stabilize seasonal occupancy swings and encourage hoteliers to maintain staff levels and service consistency.

Expansion of Luxury and Boutique Hotels

Affluent domestic travelers returning from overseas trips demand design-forward rooms, spa-centric wellness spaces, and hyper-local dining. Operators answer through soft-branded collections, cross-marketing heritage crafts, and revived urban mansions repurposed as intimate boutiques. International chains use flagship luxury hotels to showcase loyalty-program privileges, while leading domestic groups launch premium offshoots to capture upgrade traffic from their economy portfolios. Brand proliferation at the top end fosters service innovation and gives destinations like Sanya leverage to position themselves against other Asia-Pacific resort clusters.

Increase in Event-Driven Tourism (MICE, Sports, Mega-Events)

Purpose-built convention centers and stadium precincts in major cities are drawing corporate congresses, esports tournaments, and multiday music festivals. The resulting compression periods lift room rates and support higher F&B yields, cushioning hotels during weaker leisure windows. Developers are tailoring new properties around pillar-free ballrooms, broadcast-ready connectivity, and pop-up retail options that convert swiftly between conferences and consumer fairs. Technology adoption—from 5G to event-management apps—creates hybrid revenue models that range from livestream hosting to sponsorship partnerships.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lingering Pandemic-Era Visa & Quarantine Friction for Inbound Travelers | -0.8% | Global, particularly affecting long-haul source markets | Short term (≤ 2 years) |

| Intensifying Price Competition Among Domestic Hotel Chains | -0.5% | National, most acute in Tier 2 and Tier 3 cities | Medium term (2-4 years) |

| Rising ESG Compliance Costs for Hotel Properties | -0.3% | National, with greater impact on international chain properties | Medium term (2-4 years) |

| Geopolitical Tensions Dampening Long-Haul Source Markets | -0.3% | Primarily affecting North American and European source markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pandemic-Era Visa and Quarantine Friction

Although health protocols are lighter than in 2023, sporadic rule changes leave some long-haul travelers uncertain. Group bookings from Europe and North America remain sensitive to sudden testing requirements or flight capacity shifts. Hoteliers mitigate near-term volatility by targeting regional Asian traffic, offering flexible cancellation policies, and launching language-specific booking microsites to accelerate lead recovery once restrictions stabilize.

Intensifying price competition

Rapid franchising spurs a dense pipeline of mid-scale openings that compete on daily rates rather than differentiated brand experience. Operators chase economies of scale in procurement and central reservation systems, yet rising payroll and utility costs squeeze GOP margins. To defend share, chains experiment with paid memberships, dynamic pricing tied to app-based gamification, and cross-promotions with delivery platforms to grow non-room revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tourism Type: Domestic Demand Drives Market Resilience

Domestic travelers held 87.62% of the China tourism and hotel market in 2025, a dominance that kept nationwide occupancy above 60% even when borders tightened. Spending by city dwellers on weekend cultural escapes and multi-generational family trips continues to accelerate room demand in provincial capitals and scenic counties. Government holiday extensions and discounted rail passes encourage cross-province journeys that broaden stay patterns beyond the Golden Week peaks. Independent boutique hotels emphasize local heritage décor and farm-to-table menus to capture this culturally motivated segment.

Inbound tourism, though smaller, is the most dynamic component, posting an 8.24% CAGR to 2031. The China tourism and hotel market size attributable to international guests is expected to reach USD 74.63 billion by 2031 as flight capacity normalizes and visa-free corridors expand. Operators refurbish rooms with dual-language IPTV, foreign card-enabled kiosks, and globally recognized wellness amenities to raise RevPAR. Brand partnerships with international airlines and cruise lines further integrate booking funnels, reinforcing the nation’s ambitions to regain its pre-2020 status as a premier Asian gateway.

By Purpose: Leisure Travel Redefines Hotel Experiences

Leisure, adventure, and eco-oriented stays accounted for 63.25% of 2025 revenue, making pleasure trips the core engine of the China tourism and hotel market. Consumers seek curated journeys that blend outdoor activity with cultural immersion, prompting hotels to add bicycle rental stations, tea-ceremony workshops, and night-sky observation decks. Packages often bundle tickets to intangible heritage performances or geopark entry, driving higher total spend per guest and extending average length of stay.

Business and MICE travel is rebounding faster than total demand, with a 12.05% CAGR through 2031. The China tourism and hotel market size for meetings is projected to surpass USD 131.72 billion by the end of the decade as conferences scale alongside the digital-economy boom. Hoteliers install high-definition hybrid meeting studios, 24-hour co-working lounges, and carbon-offset calculators to cater to corporate policy shifts toward green events. Weekday occupancies buoyed by business groups allow stronger rate management over weekends, when leisure promotions fill remaining inventory.

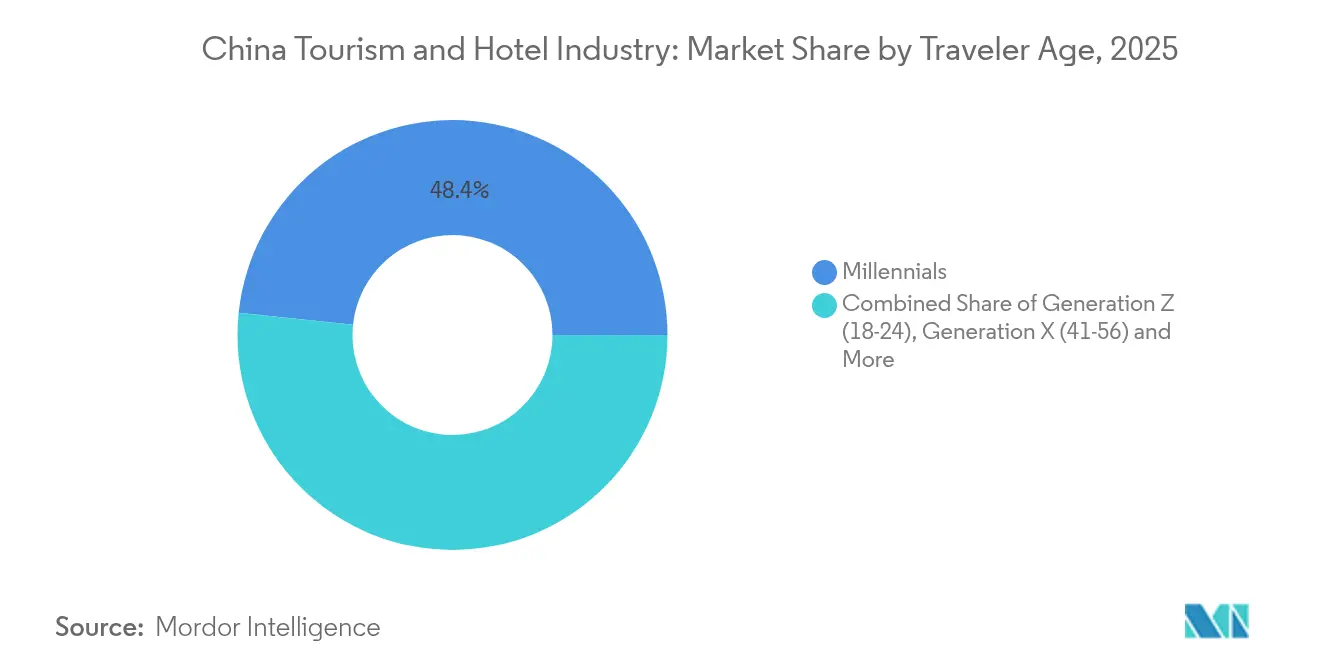

By Traveler Age: Generational Preferences Reshape Hotel Design

Millennials held a 48.35% share in 2025, shaping how brands approach loyalty, content, and amenity planning. A mobile-first mindset drives seamless check-in through QR codes and AI-powered room service chatbots. Hotels invest in open social spaces, communal kitchens, and pop-up art collaborations to foster peer engagement, reinforcing stickiness among this influential cohort within the wider China tourism and hotel market.

Baby Boomers, though numerically smaller, contribute a steady premium ADR through preference for upper-upscale properties that emphasize safety and wellness. Resorts increasingly add low-sodium menu options, barrier-free bathroom fittings, and guided mindfulness sessions to retain this demographic. Generation X balances both corporate and family priorities, favoring efficiency, express laundry, co-branded airport transfer packages, and clear loyalty-point redemption—thereby creating a bridge between younger and older guest expectations.

By Booking Channel: Digital Platforms Dominate Distribution Landscape

OTAs processed 54.10% of 2025 room transactions, cementing their position at the center of the China tourism and hotel market distribution chain. Their meta-search engines, livestream promotions, and deep discount flash sales sway price-sensitive consumers. Hotels seeking margin relief invest in direct-booking mini-programs embedded in social-commerce platforms, bundling extras such as complimentary breakfast or late checkout to lure guests away from commission-heavy intermediaries.

Super-app ecosystems, expanding at 11.78% CAGR, give consumers a one-stop path from trip inspiration to ride-hailing and dining reservations. Seamless linkage among payments, social feeds, and AI trip planners elevates convenience, triggering rapid share gains among Gen Z users. Hotels integrate loyalty status into these super-apps to deliver targeted push offers and real-time service chat, thereby nurturing lifetime value and data-driven upsell opportunities across the evolving China tourism and hotel market.

By Hotel Category: Mid-scale Dominance Amid Luxury Growth

Mid-scale hotels captured 34.35% of 2025 revenue, reflecting demand from price-aware travelers who still expect consistent quality. Chain groups standardize bedding, fragrance profiles, and breakfast buffets across thousands of units, using cloud-based PMS tools to optimize costs. The segment’s wide footprint shields operators during demand swings, but minor brand differentiation means continued rate competition in suburban nodes.

Luxury stock, while smaller today, is rising swiftly at 9.52% CAGR, and is forecast to comprise more than 13.25% of total rooms by 2031. Hotels differentiate through signature spas, destination restaurants helmed by celebrity chefs, and curated art collections echoing Chinese aesthetics. Enhanced RevPAR potential offsets higher build and operating costs, helping global brands justify aggressive expansion and fueling the experiential tier of the China tourism and hotel industry.

By Ownership/Branding: Chain Penetration Transforms Market Structure

Independent hotels represented 46.20% of rooms in 2025, giving the China tourism and hotel market its historically fragmented profile. Many properties leverage regional architectural styles and locally sourced amenities to retain character. Digital marketing partnerships with niche OTAs targeting heritage enthusiasts bolster occupancy, yet limited procurement scale and marketing budgets constrain competitiveness against larger chains.

Internationally branded chains, growing at 9.55% CAGR, add standardized service frameworks that reassure foreign visitors and upscale domestic travelers. Asset-light models centered on management contracts allow rapid penetration into secondary cities where land costs remain digestible. Domestic chains simultaneously scale their premium sub-brands, compressing the gap between global and local propositions and accelerating professionalization across the China tourism and hotel market.

Geography Analysis

East China retained the largest 36.72% revenue slice of the travel insurance market in 2025. The combined hotel inventory in Beijing, Shanghai, and Guangzhou delivers the highest ADR nationwide, yet maturity limits pipeline growth to selected repositioning’s and mixed-use megaprojects. Luxury clusters along the Bund or within Beijing’s historical courtyard zones anchor flagship launches by global brands that rely on gateway visibility to feed loyalty funnels and cross-sell across Asia.

Southwest China represents the most dynamic growth frontier, projected to advance at 7.62% CAGR over 2026-2031. Second-tier hubs such as Chengdu, Hangzhou, and Wuhan now supply the bulk of new room keys. Chengdu alone had 147 active projects at end-2024, mirroring its rise as a western logistics and digital-media node. Physical connectivity from expanded metro networks and high-speed rail spurs investor appetite, with developers seizing brownfield plots near tech parks or new convention centers. Average ADRs in these cities still trail coastal counterparts, yet faster RevPAR growth and lower land premiums create stronger yield potential within the broader China tourism and hotel market.

Destination resorts in Sanya, Guilin, and Lijiang ride seasonal peaks linked to school holidays and public festivals. High-season ADR surges above 40% of shoulder rates support year-round profitability despite occupancy dips in off-peak months. Operators deploy dynamic staffing models and short-term F&B pop-ups to match fluctuating demand, while bundling wellness, outdoor adventure, and cultural immersion into packaged offers that lengthen stays. Rural boutique clusters—often converted farmhouses—tap city-dweller appetites for nature and local cuisine, reinforcing geographic diversification and enriching the narrative of the China tourism and hotel market.

Competitive Landscape

Domestic groups such as Jin Jiang International and Huazhu leverage extensive loyalty bases, rapid prototype rollouts, and deep relationships with municipal authorities to accelerate franchise count. Their cloud-PMS and unified procurement platforms drive cost synergies that undercut smaller rivals. International chains, by contrast, emphasize brand segmentation, offering everything from extended-stay suites to lifestyle-driven luxury to capture discrete demand pools within the China tourism and hotel market.

Mid-scale warfare is the fiercest arena. Domestic leaders flood Tier 3 cities with standardized builds, while foreign groups localize select-service concepts tailored to Chinese breakfast preferences and family-friendly room layouts. The luxury race sees Marriott and Hilton competing on art-curation partnerships and marquee Michelin-level dining, while local upscale challenger BTG Homeinns positions Chinese cultural storytelling as a counterweight to imported glamour.

Specialized niches yield untapped upside. Wellness resorts bundle traditional medicine consultations with modern spa therapy. Long-stay products track technology-sector talent mobility. Senior-focused brands experiment with barrier-free design, on-site clinics, and age-friendly excursions. Concurrently, ESG expectations rise; brands adopt solar panels, rain-water harvesting, and AI-directed smart energy systems to meet new regulations without eroding margin, reinforcing service differentiation in the modern China tourism and hotel market.

China Tourism And Hotel Market Leaders

Jin Jiang International Holdings Co., Ltd.

Huazhu Group Ltd.

BTG Homeinns Hotels Group Co., Ltd.

Marriott International Inc.

Hilton Worldwide Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Marriott International signed 161 deals in Greater China, adding nearly 31,000 rooms, with a 73% increase in luxury room signings versus 2023 Marriott International.

- April 2025: H World Group Limited expanded its network to 11,147 hotels, totaling 1,088,218 rooms, and kept 3,013 hotels under development H World Group Limited.

- March 2025: H World Group Limited expanded its network to 11,147 hotels, totaling 1,088,218 rooms, and kept 3,013 hotels under development H World Group Limited.

- November 2024: IHG Hotels & Resorts launched the Atwell Suites lifestyle brand in Greater China IHG Hotels & Resorts.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines China's tourism and hotel market as all spending by domestic, inbound, and outbound travelers on accommodation services, room sales, in-property food and beverage, and hotel-led tour bundles booked through online travel agencies, direct digital channels, or offline agents.

Scope exclusion: airline passenger revenue, travel retail, and attraction-only tickets are not counted, preventing double counting.

Segmentation Overview

- By Tourism Type

- Domestic Tourism

- Inbound Tourism

- Outbound Tourism

- By Purpose

- Leisure & Adventure & Eco-Tourism

- Business / MICE

- By Traveler Age

- Generation Z (18-24)

- Millennials (25-40)

- Generation X (41-56)

- Baby Boomers (57+)

- By Booking Channel

- Online Travel Agencies (OTAs)

- Direct Hotel Websites & Apps

- Offline Travel Agencies

- By Hotel Category

- Economy / Budget Hotels

- Mid-scale Hotels

- Upscale Hotels

- Luxury Hotels

- Serviced Apartments & Long-Stay

- By Ownership / Branding

- Independent Hotels

- Domestic Chain-Affiliated Hotels

- International Chain-Affiliated Hotels

- By Region

- Central China

- East China

- North China

- Northeast China

- Northwest China

- South China

- Southwest China

Detailed Research Methodology and Data Validation

Primary Research

Analysts conduct expert interviews with property owners, OTA executives, and municipal tourism officers across tier-1 and emerging tier-2 cities, plus traveler pulse surveys. These conversations validate unreported average daily rates, holiday occupancy spikes, and forward pricing intentions.

Desk Research

Our team begins with Ministry of Culture and Tourism visitor surveys, National Bureau of Statistics hospitality census tables, and UNWTO arrival data, supplemented by China Hotel Association white papers. Company 10-Ks, provincial tourism investment plans, and policy circulars enrich historical trends. Paid repositories such as D&B Hoovers for chain financials and Dow Jones Factiva for deal flow give timely corporate datapoints. Numerous other reputable public documents are also consulted for cross-checks.

Market-Sizing and Forecasting

We apply a top-down build. 2024 visitor-night totals multiplied by spend per visitor (official and payment-platform disclosures) are sliced by hotel class using occupancy ratios, then benchmarked with bottom-up chain room counts multiplied by sampled average selling prices. Key drivers, domestic trip volume, visa policy shifts, online booking penetration, pipeline room additions, and ADR inflation, feed a multivariate regression blended with scenario analysis to 2030. Gaps in unbranded provincial stock are bridged through primary research heuristics.

Data Validation and Update Cycle

Outputs pass variance checks versus independent indicators, followed by multi-level analyst review. Models refresh annually, with interim revisions when policy or shock events materially alter demand. A last-mile check is run before every client release.

Why Mordor's China Tourism and Hotel Baseline Commands Reliability

Published estimates vary because reports differ on scope, price bases, and refresh cadence.

By tracking OTA commissions, unregistered rooms, and yearly exchange movements, we minimize blind spots. Key gap drivers elsewhere include narrow hotel-only focus, static exchange assumptions, and limited traveler-purpose splits.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 406.36 B (2025) | Mordor Intelligence | |

| USD 300 B (2024) | Global Consultancy A | OTA commissions excluded; limited traveler-purpose split |

| USD 400 B (2024) | Regional Consultancy B | Counts hotel F&B only; minimal adjustment for unregistered rooms |

| USD 83.63 B (2024) | Trade Journal C | Covers hotel room revenue alone; tourism spend omitted |

The comparison shows that once hidden revenue streams and consistent exchange rates are applied, Mordor's balanced, transparent baseline remains the dependable anchor for strategic planning.

Key Questions Answered in the Report

What is the current size of the China tourism and hotel market?

The market is valued at USD 427.7 billion in 2026 and is projected to climb to USD 552.8 billion by 2031.

Which hotel category holds the largest share?

Mid-scale hotels command 34.35% of 2025 revenue, benefiting from strong demand among value-conscious domestic travelers.

How fast is inbound tourism growing?

Inbound tourism is the fastest-growing segment, advancing at an 8.24% CAGR through 2031 as visa facilitation and flight recovery support arrivals.

What role do digital channels play in hotel bookings?

OTAs account for 54.10% of room nights, while super-app ecosystems are expanding at a 11.78% CAGR by bundling travel with everyday services.

Which cities are the hottest development markets?

Chengdu leads the construction pipeline, with Hangzhou and Wuhan close behind, driven by improved transport links and rising business activity.

Page last updated on: