Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

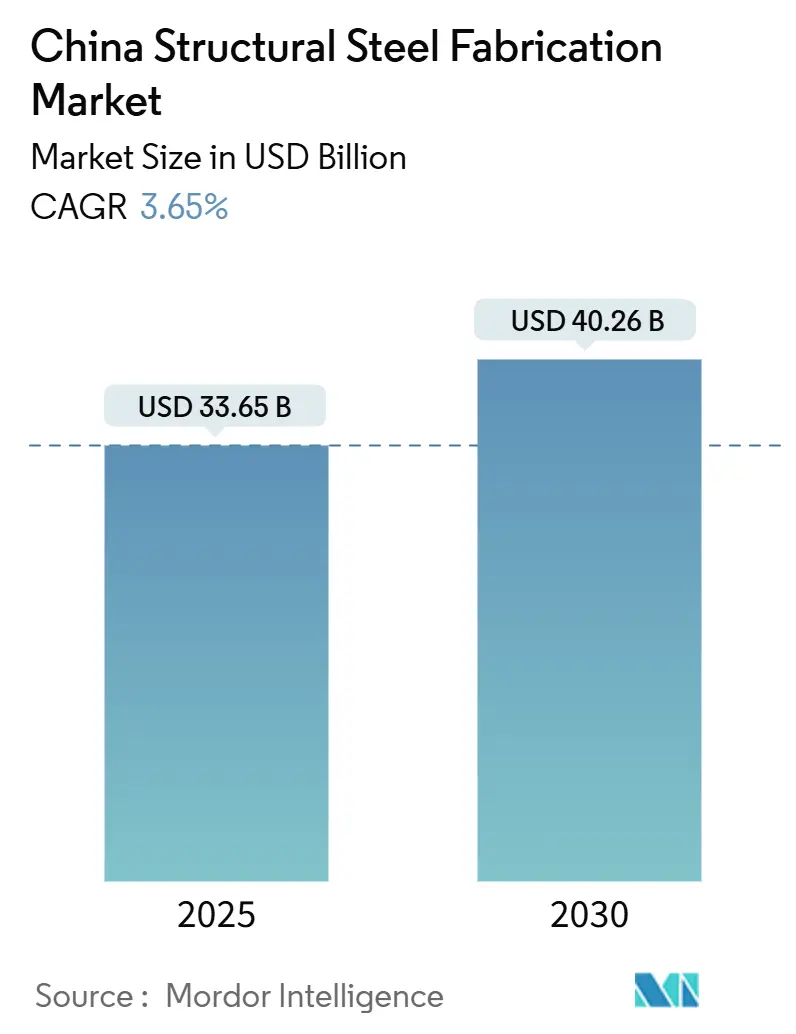

| Market Size (2025) | USD 33.65 Billion |

| Market Size (2030) | USD 40.26 Billion |

| Growth Rate (2025 - 2030) | 3.65% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Structural Steel Fabrication Market Analysis by Mordor Intelligence

The China Structural Steel Fabrication Market size stood at USD 33.65 billion in 2025 and is forecast to reach USD 40.26 billion by 2030, advancing at a 3.65% CAGR. Growth moderates from past peaks yet remains resilient as Beijing’s 14th Five-Year Plan channels funds toward ultra-high-voltage grids, high-speed rail corridors, and modular public housing. Fabricators that automate welding lines, deploy digital-twin production cells, and secure GB-standard certifications capture premium contracts, while low-carbon steel mandates shift procurement toward electric-arc-furnace output and scrap-based feedstocks. Government capacity-replacement rules tighten emissions and energy-efficiency thresholds, nudging small shops toward consolidation or exit, and expanding opportunities for integrated groups that already control upstream slabs and downstream logistics. At the same time, export demand from Belt and Road projects anchors coastal order books, cushioning domestic cyclical swings and reinforcing the China structural fabricated steel market as a pivotal supplier within global infrastructure value chains[1]National Development and Reform Commission, “14th Five-Year Plan 2025 Project Catalogue,” ndrc.gov.cn.

Key Report Takeaways

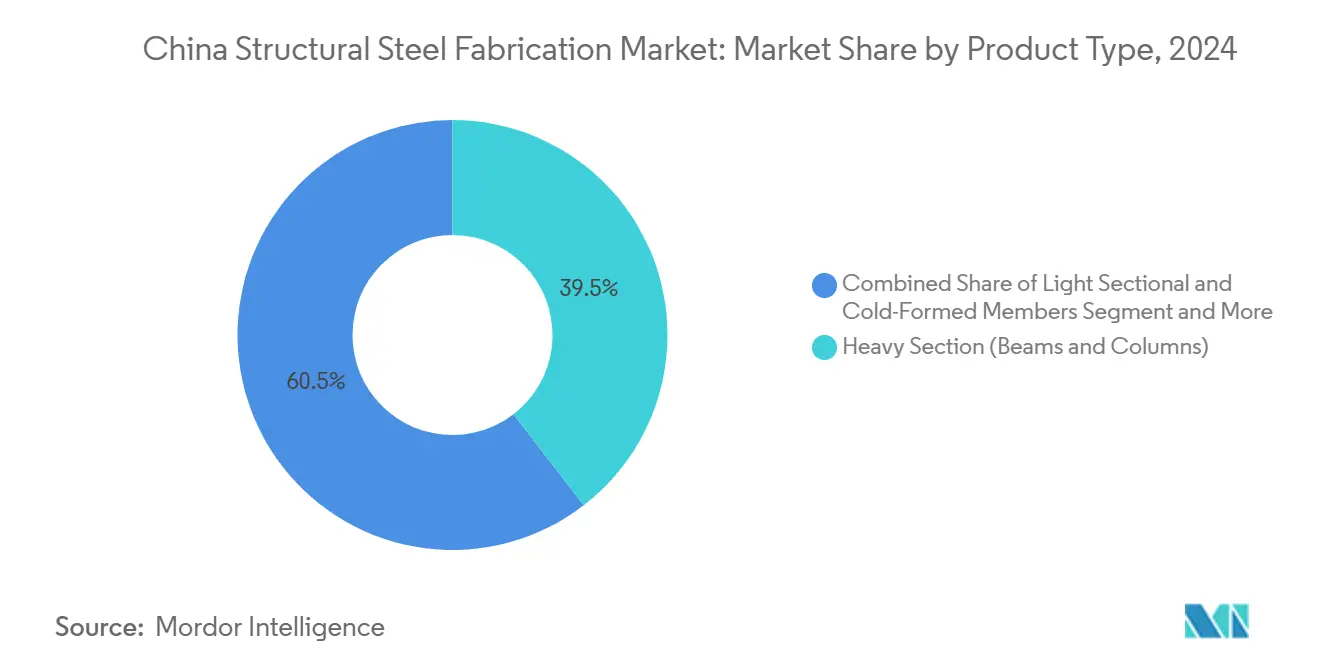

- By product type, heavy sections captured 39.54% of the Chinese structural fabricated steel market share in 2024.

- By end-user industry, infrastructure transport recorded the highest projected CAGR at 5.3% through 2030.

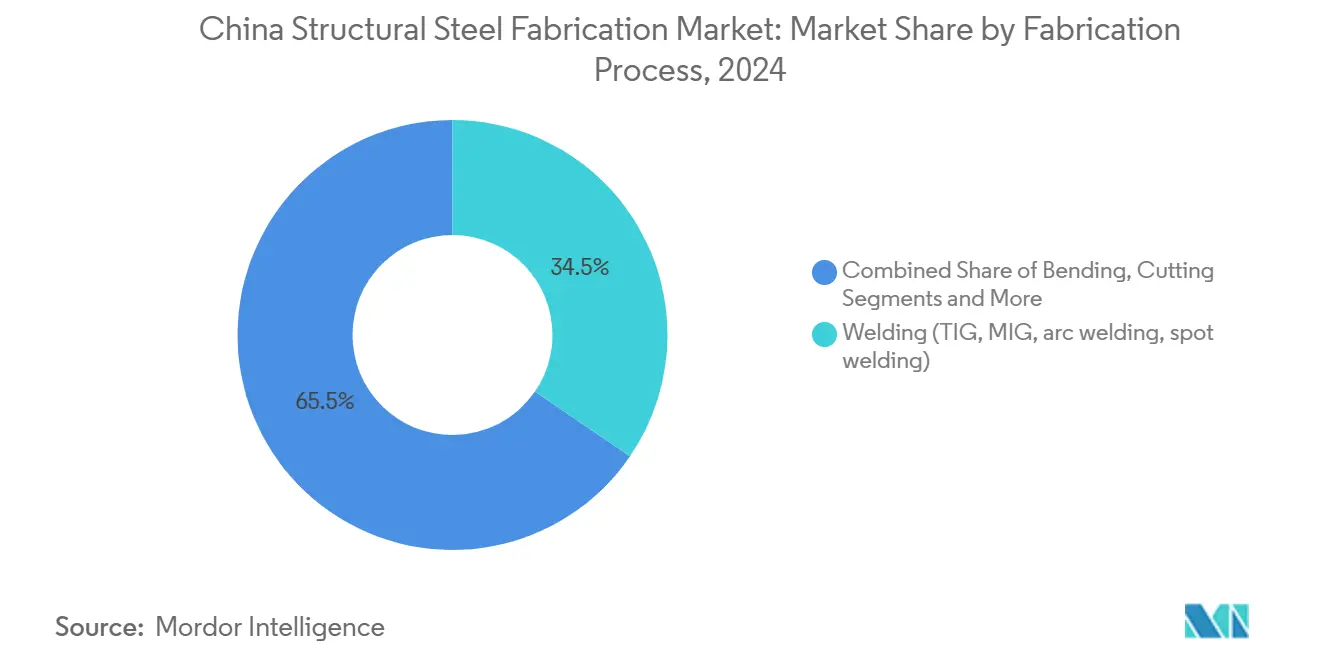

- By fabrication process, cutting technologies are set to expand at a 4.69% CAGR between 2025-2030.

- By geography, Jiangsu led with 16.2% revenue share in 2024, whereas the Rest of China is forecast to grow at 4.56% CAGR to 2030.

China Structural Steel Fabrication Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government infrastructure spending under the 14th FYP | +1.2% | National, especially Jiangsu, Guangdong, and Beijing | Medium term (2-4 years) |

| Prefabricated & modular construction uptake | +0.8% | National, early adoption in Shenzhen, Guangdong | Long term (≥ 4 years) |

| Urbanization & mega-cluster high-rise demand | +0.6% | Tier-1 cities, the Yangtze River Delta, the Pearl River Delta | Medium term (2-4 years) |

| Decarbonization policies favoring low-carbon steel | +0.4% | National, stricter in Beijing-Tianjin-Hebei | Long term (≥ 4 years) |

| AI-driven robotic welding & digital twins | +0.3% | Jiangsu, Guangdong, and Shanghai hubs | Short term (≤ 2 years) |

| Export of fabricated modules for Belt & Road | +0.2% | Coastal provinces, Guangdong, Zhejiang | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Infrastructure Spending Under The 14th FYP

State investment is a primary catalyst for the Chinese structural fabricated steel market. In 2025, State Grid Corporation tendered 568,000 metric tons of steel towers for ultra-high-voltage lines, 115% above 2024 levels. New rail corridors such as the 552 km Xiong’an-Shangqiu route multiply demand for box girders and bridge trusses. Liaoning’s USD 121 billion clean-energy program accelerates grid-connected renewables that require corrosion-resistant lattice structures. Fabricators able to document GB/T 700 compliance and traceable quality control secure the bulk of these long-cycle orders, translating policy directives directly into yard utilization gains[2]State Grid Corporation of China, “UHV Transmission Tender Notice 2025,” sgcc.com.

Prefabricated & Modular Construction Uptake

China targets 30% of new buildings to adopt assembled methods by 2025, propelling factory-finished steel frames into mainstream acceptance. CIMC MBI and CSCEC Steel now ship bathroom pods and volumetric hotel rooms where 80-90% of components arrive pre-installed, compressing site schedules by more than half. Shenzhen mandates prefabrication ratios on public works and backs developers with green-credit incentives, turning the city into a proof-of-concept hub. Modularization also benefits western provinces that lack skilled field labor, redirecting off-site production capacity from coastal zones into inland demand.

Urbanization & Mega-Cluster High-Rise Demand

Rapid urban migration sustains tower construction across the Greater Bay Area and the Yangtze River Delta. Projects like Guangzhou’s International Financial City require high-strength H-columns with sub-millimeter tolerances that only a handful of fabricators can deliver repeatedly. BIM-driven coordination between architects, rebar suppliers, and façade installers tightens lead times and lowers rework costs. Yet municipal debt ceilings occasionally postpone metro and airport expansions, reminding suppliers to balance order books across private, public, and export channels.

Decarbonization Policies Favoring Low-Carbon Steel

China’s 2060 neutrality pledge redefines procurement. Donghua Iron & Steel ordered twin electric-arc furnaces with Zerobucket charging that save 50 kWh per ton and cut direct CO₂ emissions. Fabricators purchasing EAF plates gain a marketing edge with renewable developers and foreign buyers facing border-adjustment taxes. Scrap-loop recycling, on-site solar arrays, and ISO 14064 verification emerge as tender prerequisites, reshaping the competitive field toward firms with the capital and digital tools to quantify footprint reductions.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.7% | National, acute in import-dependent coastal regions | Short term (≤ 2 years) |

| Industry overcapacity & price competition | -0.5% | National, concentrated in Hebei, Jiangsu, Liaoning | Medium term (2-4 years) |

| Stricter GB emissions standards for fabricators | -0.4% | National, stricter enforcement in Beijing-Tianjin-Hebei region | Medium term (2-4 years) |

| Skilled labour shortage in advanced welding/BIM | -0.3% | Manufacturing hubs in Jiangsu, Guangdong, Shanghai | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Billet prices hit CNY 3,310 per ton (USD 466) in October 2024 as stimulus programs rekindled construction demand. Fabricators without long-term ore contracts faced sudden cash-flow stress, particularly those exporting on fixed-price clauses denominated in USD. Integrated mills cushion the swings through captive mines and coke plants, but independent workshops shoulder the full impact. Forward-buying and futures hedging remain underutilized among SMEs, leaving margins exposed during price spikes.

Industry Overcapacity & Price Competition

China’s fabrication nameplate capacity already exceeds demand by more than 50 million tons and could swell toward 250 million tons within a decade. Excess beams and tubular sections flood tender boards, suppressing commodity pricing and driving a flight to quality and specialization. The National Development and Reform Commission now enforces one-for-one capacity swaps, yet uneven provincial implementation delays rationalization. Forward-looking companies diversify into niche segments like wind-turbine towers or LNG storage tanks, where technical barriers shield margins from volume-driven price wars.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heavy Sections Anchor a Diversified Mix

Heavy sections captured 39.54% of the Chinese structural steel fabrication market share in 2024 on the back of rail bridge launches and city-center skyscrapers. The segment’s reliance on GB/T 11263 rolled H-beams aligns with public works specifications, ensuring predictable tender flow even when residential starts waver. Down the forecast window, heavy sections still outpace light members due to 5.3% CAGR growth in the transport corridor program that strings together bridges, depots, and elevated viaducts. Fabricators such as Baowu Construction integrate robotic coping and ultrasonic inspection to meet 80 m span girder tolerances, strengthening their bid positions on design-build contracts.

Light sections and cold-formed members ride the modular boom in schools and mid-rise apartments where standardized C-purlins and Z-girts slash erection time. Hollow structural sections thrive in façade grids and mechanical platforms, aided by manufacturers like LEFIN that offer EN 10219 and ASTM A500 dual certifications. Meanwhile, plate-worked girders for petrochemical racks receive a boost from refinery upgrades, including CNOOC’s USD 2.7 billion Daxie Island expansion scheduled for 2026 handover. Collectively, these niches keep order books healthy even if headline gross-floor-area additions slow, reinforcing the balanced revenue base inside the China structural fabricated steel market.

By End-User Industry: Construction Dominates, Energy Accelerates

Construction accounted for 47.68% of the Chinese structural steel fabrication market size in 2024, with commercial towers and transport hubs as volume pillars. Infrastructure transport will lead growth at a forecast 5.3% CAGR to 2030 as 200+ km/h rail corridors link inland cities to coastal ports. Urban renewal drives retrofit demand for seismic-grade beams in Beijing and Shanghai, while public-private partnerships fund suburban light-rail lines that require elevated guideway segments.

Power and energy demand advances at a 5.05% CAGR as wind-turbine tower orders and solar tracker frames multiply under renewable quotas. Fabricators able to roll 120 mm thick flanges or machine gear-box seating plates secure recurring contracts from turbine OEMs. Industrial equipment, spanning automated warehouses to semiconductor fabs, offers steady mid-single-digit growth supported by Beijing’s manufacturing-upgrade incentives. Petrochemical and LNG players commission heavy-wall pressure-vessel shells that test the high-heat forming skills of specialized shops, diversifying revenue away from volume-driven building segments inside the Chinese structural fabricated steel market.

By Fabrication Process: Welding Commands, Cutting Innovations

Welding dominated with 34.54% contribution to the China structural steel fabrication market in 2024 as multi-pass submerged-arc lines stitched together beams longer than 40 m. AI-enabled robots now realign torch angles on the fly, reducing rework scrap by 60% and elevating pass-through yield above 95%. High-frequency twin-wire MIG accelerates root-pass lay-down, critical in LNG tank rings where distortion must stay below 2 mm. Training partnerships between Lincoln Electric and vocational institutes address skilled operator shortages, broadening the labor pool.

Cutting processes will grow fastest at 4.69% CAGR, driven by fiber-laser machines that slice 40 mm plates at 40 m/min with oxide-free edges, ready for direct weld assembly. Plasma tables with automatic bevel heads and water-jet systems for stainless parts round out a toolkit that underpins lean batching. Machining, forming, and casting retain roles in niche jobs, including turbine hubs and architectural nodes, and digital-twin monitoring across all shops establishes a continuous improvement loop that undergirds competitiveness in the Chinese structural fabricated steel market.

Geography Analysis

Jiangsu held 16.2% of national revenue in 2024 thanks to an entrenched supplier base near shipyards, chemical parks, and metro tunnel sites. Provincial incentives for industrial robotics slashed payback periods to under three years, prompting medium-sized fabricators to replace manual FCAW with gantry robots. Nearby Shanghai’s white-collar clusters demand premium façades, letting Jiangsu yards deploy advanced CNC bending and 3-D laser cutting to edge competitors from Hebei.

Guangdong captures export-oriented orders bound for ASEAN and the Middle East, where clients prefer suppliers certified to both GB and EN codes. Its Pearl River Delta logistics grid compresses container-to-wharf times below 24 hours, a critical differentiator for modular-shipment contracts. Zhejiang adds entrepreneurial agility, with many factories adopting build-to-order MES systems that absorb short notices for bespoke stadium roofs. Combined, the coastal trio anchors more than half of the Chinese structural fabricated steel market, yet growth prospects tilt inland.

The Rest of China segment will post the fastest 4.56% CAGR through 2030 as Chongqing, Sichuan, and Shaanxi lure machinery plants away from high-cost seaboard zones. Rail freight subsidies and lower land prices offset longer export distances, and access to nearby ore mines curbs billet transport charges. Provincial planners channel central funds into bridges across the Yangtze tributaries and wind farms atop the Loess Plateau, each demanding tonnage that feeds new beam and tubular mills. The geographic spread hedges macro risk and smooths demand cycles across the Chinese structural fabricated steel market[3]Ministry of Commerce, “Belt and Road Equipment Export Statistics 2024,” mofcom.gov.

Competitive Landscape

The Chinese structural steel fabrication market features moderate fragmentation. State-owned conglomerates such as Baowu and China Railway Construction bridge material supply, fabrication, and project execution, leveraging scale to negotiate ore contracts and to finance multi-site robotic upgrades. Private players respond by specializing in tight-tolerance, quick-turn segments, from wind-tower cans to data-center trusses, staking reputations on agility rather than volume.

Automation races define competitive narratives. China Petroleum Pipeline Engineering introduced a self-propelled robotic welder that trims joint cycle time from seven hours to one, setting a benchmark others scramble to match. Smaller firms pool capital via regional cooperatives to lease similar equipment, leveling the technology field while retaining ownership independence. Digital-twin adoption accelerates among firms serving petrochemical modules, with cloud-based dashboards that simulate weld-shrinkage before production starts, reducing fit-up delays on site.

Strategic alliances multiply. ArcelorMittal’s USD 1.84 billion joint venture with China Oriental infuses international coil grades into domestic electrical-steel demand for EV motors. Baosteel acquires a 50% stake in Chongqing plate shop to secure western hydro-dam contracts. Alongside these deals, capacity-swap mandates compel marginal mills to shutter older lines, allowing stronger peers to consolidate quotas legally. The endgame is a more technology-intensive landscape where efficiency, certification, and environmental scores trump raw tonnage in shaping leadership within the Chinese structural fabricated steel market.

China Structural Steel Fabrication Industry Leaders

China Steel Structure Co. Ltd.

Hebei Baofeng Steel Structure Co. Ltd.

Qingdao Xinguangzheng Steel Structure Co. Ltd.

United Steel Structures Ltd.

Qingdao Havit Steel Structure Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Chongqing Iron & Steel submits a USD 150 million bid for four production lines including 4,100 mm and 2,700 mm plate mills, plus wire-rod and rebar units being sold by parent Chongqing Steel Group, a move aimed at broadening its fabrication portfolio.

- March 2025: China National Offshore Oil Company begins a USD 2.7 billion upgrade at Daxie Island, adding 120,000 bpd of crude-processing capacity that requires specialized steel structures for new process units and storage tanks.

- January 2025: Shell and joint-venture partner CSPC approve an expansion of the Guangdong petrochemical hub, targeting 1.6 million tpy of ethylene and 320,000 tpy of specialty chemicals by 2028, an investment that calls for sizable structural-steel packages.

- October 2024: China Oriental Group and ArcelorMittal create two 50-50 joint ventures totaling USD 1.84 billion to manufacture electrical steel for automotive and renewable-energy customers, each venture needing tailored structural components.

China Structural Steel Fabrication Market Report Scope

By Product Type

| Heavy Section(Beams & Columns) |

| Light Sectional & Cold-Formed Members |

| Tubular & Hollow Structural Sections (HSS) |

| Other Product Types(Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) |

By End-user Industry

| Construction | Commercial |

| Residential | |

| Industrial Buildings | |

| Infrastructure (Transport) | |

| Power & Energy (include utilities and renewable energy) | |

| Manufacturing & Industrial Equipment | |

| Oil and Gas | |

| Automotive & Transportation (railways systems, metro components, etc.) | |

| Other End User Industries(Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, and Telecommunications) |

By Fabrication Process

| Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) |

| Bending (Press brakes, roll bending, rotary bending) |

| Welding (TIG, MIG, arc welding, spot welding) |

| Machining (Milling, turning, drilling, grinding, CNC machining) |

| Forming (Stamping, forging, rolling, hydroforming) |

| Casting (Sand casting, die casting, investment casting) |

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) |

By Geography

| Jiangsu |

| Guangdong |

| Zhejiang |

| Beijing |

| Shanghai |

| Rest Of China |

| By Product Type | Heavy Section(Beams & Columns) | |

| Light Sectional & Cold-Formed Members | ||

| Tubular & Hollow Structural Sections (HSS) | ||

| Other Product Types(Plate-worked Girders & Trusses, Custom-built Modules & Skids, etc.) | ||

| By End-user Industry | Construction | Commercial |

| Residential | ||

| Industrial Buildings | ||

| Infrastructure (Transport) | ||

| Power & Energy (include utilities and renewable energy) | ||

| Manufacturing & Industrial Equipment | ||

| Oil and Gas | ||

| Automotive & Transportation (railways systems, metro components, etc.) | ||

| Other End User Industries(Mining, Shipbuilding & Marine, Defense & Aerospace, Agriculture & Food Processing, and Telecommunications) | ||

| By Fabrication Process | Cutting (Laser cutting, plasma cutting, water jet cutting, sawing, shearing, etc.) | |

| Bending (Press brakes, roll bending, rotary bending) | ||

| Welding (TIG, MIG, arc welding, spot welding) | ||

| Machining (Milling, turning, drilling, grinding, CNC machining) | ||

| Forming (Stamping, forging, rolling, hydroforming) | ||

| Casting (Sand casting, die casting, investment casting) | ||

| Others (Plating, Surface Treatment, Punching, Finishing, Fastening, Assembly, Heat Treatment, Engraving, Hydroforming, Spinning, etc.) | ||

| By Geography | Jiangsu | |

| Guangdong | ||

| Zhejiang | ||

| Beijing | ||

| Shanghai | ||

| Rest Of China | ||

Key Questions Answered in the Report

What is the projected value of the Chinese structural fabricated steel market in 2030?

Forecasts place it at USD 40.26 billion, implying a 3.65% CAGR from 2025.

Which product holds the largest share in Chinese structural fabrication?

Heavy sections, mainly beams and columns, accounted for 39.54% of 2024 revenue.

Which end-use will grow fastest through 2030?

Infrastructure transport fabrications, underpinned by high-speed rail builds, are set for a 5.3% CAGR.

Why are cutting technologies expanding quickly?

Fiber-laser and CNC plasma systems lift precision and throughput, pushing cutting processes toward a 4.69% CAGR.

Which province leads fabrication output?

Jiangsu ranked first with a 16.2% revenue share in 2024 owing to its dense industrial corridor.

How are decarbonization policies influencing the sector?

Buyers increasingly specify low-carbon EAF plate, rewarding fabricators that document emissions reductions and scrap-recycling practices.

Page last updated on: