Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

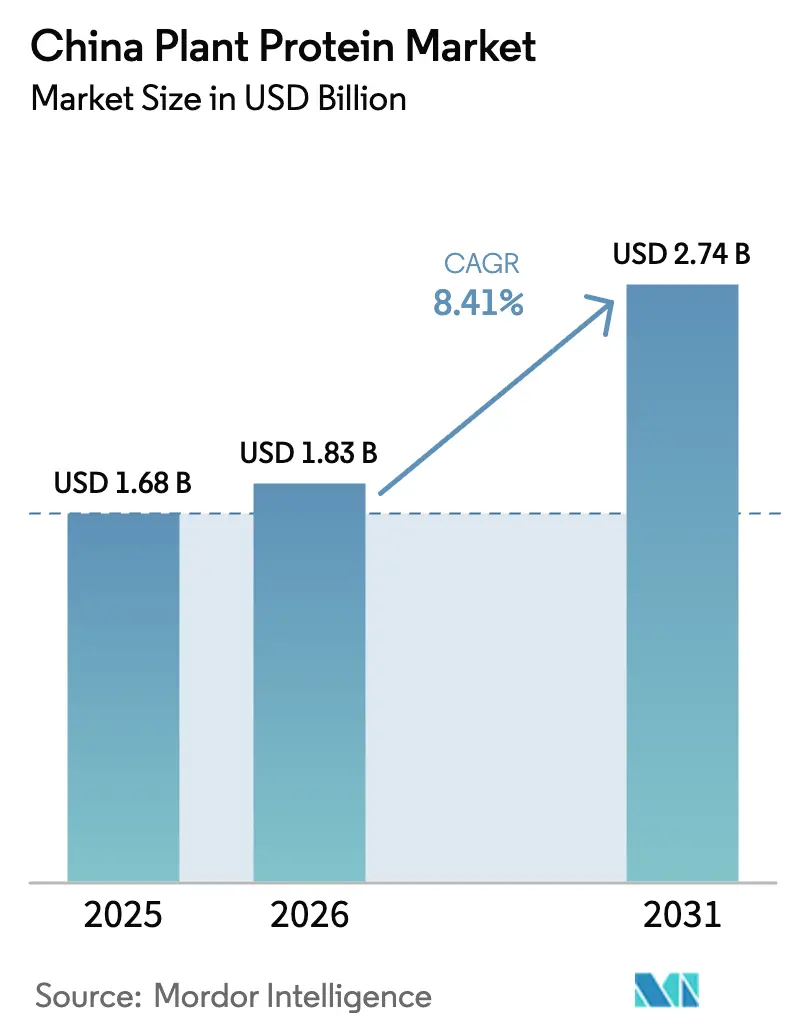

| Base Year Market Size (2025) | USD 1.68 Billion |

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 2.74 Billion |

| Growth Rate (2026 - 2031) | 8.41% CAGR |

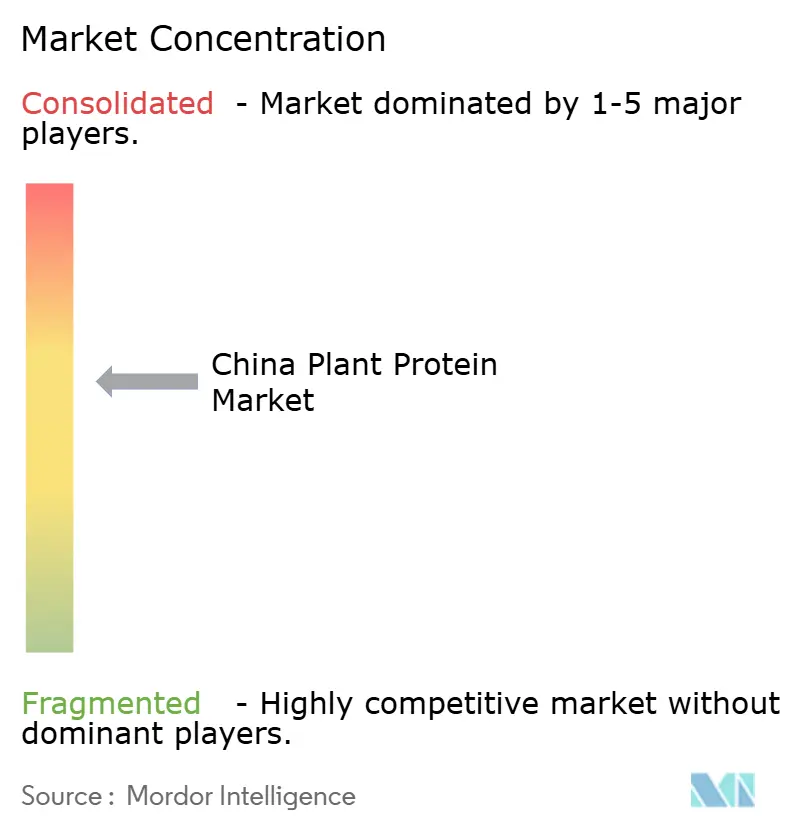

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Plant Protein Market Analysis by Mordor Intelligence

The China Plant Protein Market size is expected to grow from USD 1.68 billion in 2025 to USD 1.83 billion in 2026 and is forecast to reach USD 2.74 billion by 2031 at 8.41% CAGR over 2026-2031. This growth is largely driven by Beijing's "Healthy China 2030" nutrition goals, swift advancements in extrusion and precision fermentation technologies, and corporate strategies aligning with the nation's dual-carbon commitment. While soy remains the leading ingredient, there's a noticeable shift as capacities for pea, wheat, and specialty proteins expand, hinting at a diversification in raw material sources. Consumer interest is evolving, moving beyond just beverages and meat substitutes to include functional beauty products. Simultaneously, feed formulators are turning to plant proteins, aiming to reduce dependence on imported fishmeal and adhere to sustainability goals. In this competitive landscape, success now relies on scalable texturization, clean-label authenticity, and certified deforestation-free supply chains. This shift allows innovators to command premium prices, even as traditional bulk soy suppliers focus on maintaining market share through cost leadership.

Key Report Takeaways

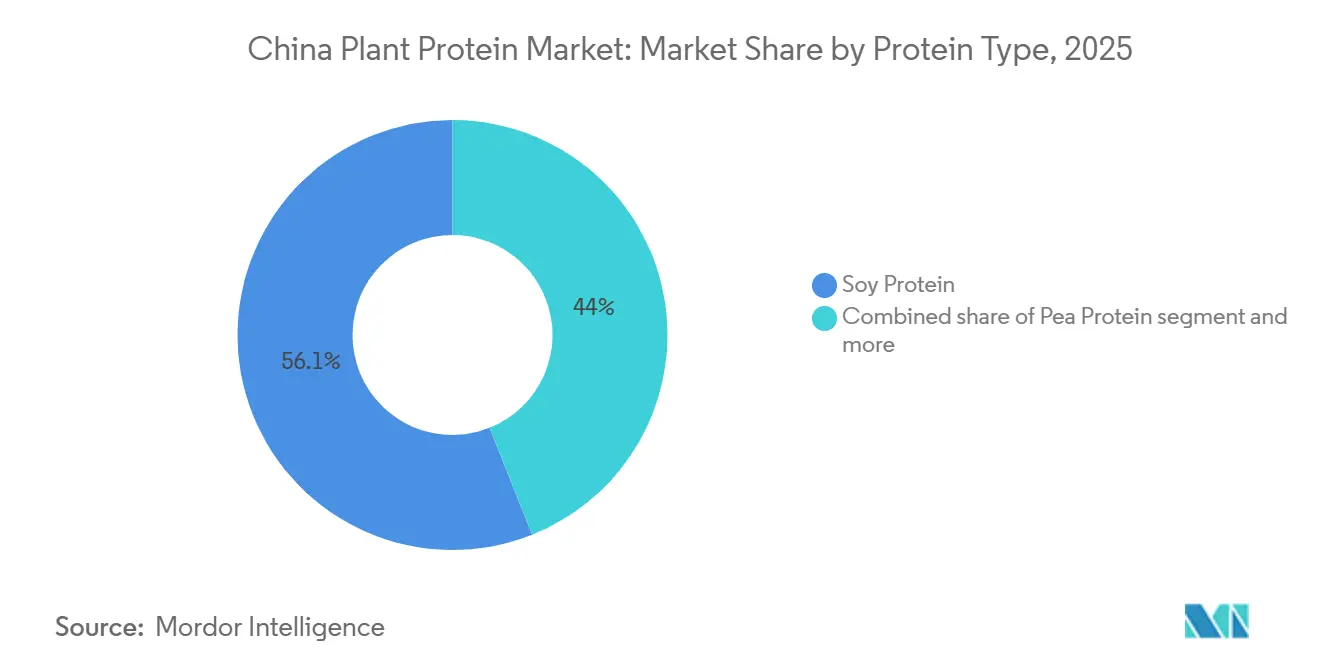

- By protein type, soy protein commanded 56.05% of the China plant protein market share in 2025, whereas pea protein is expanding at a 9.02% CAGR to 2031.

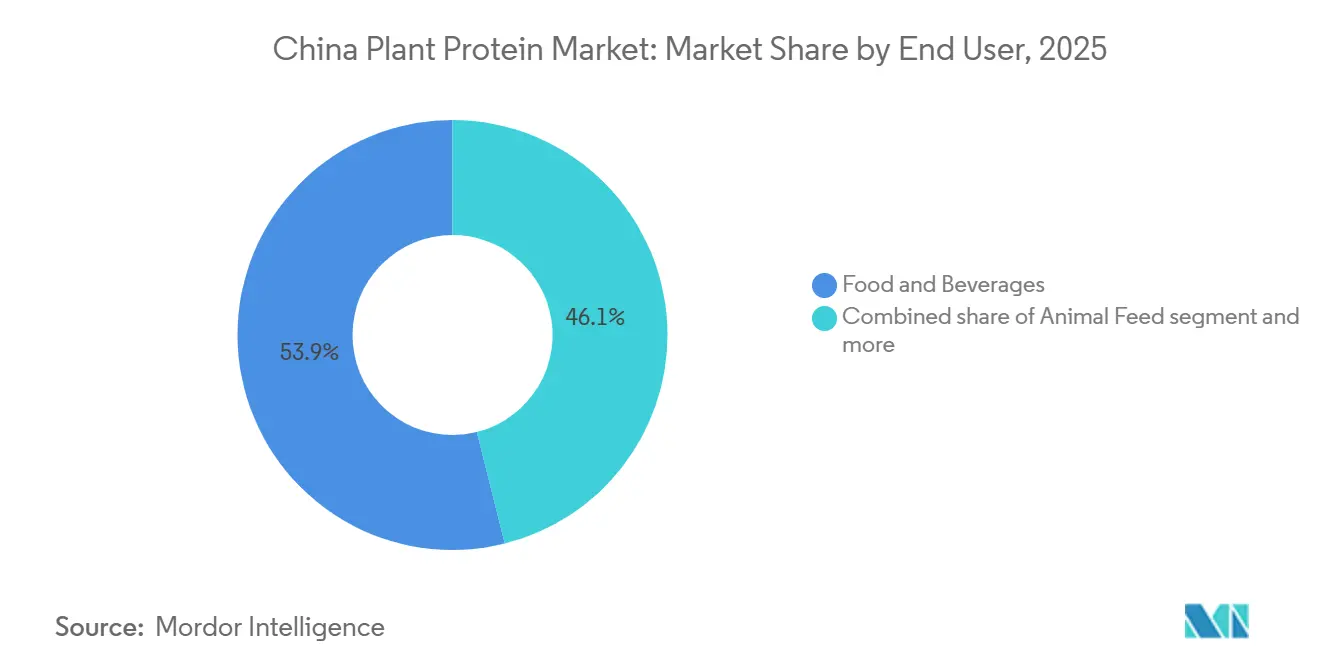

- By end user, food and beverages held 53.91% revenue share of the China plant protein market in 2025, while animal feed is forecast to post the highest 9.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Plant Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of flexitarian and vegan lifestyles | +1.2% | National, with concentration in Tier-1 and Tier-2 cities (Beijing, Shanghai, Guangzhou, Shenzhen, Chengdu) | Medium term (2-4 years) |

| "Healthy China 2030" and "Grand Food Vision" initiatives | +1.8% | National, with policy implementation led by the Ministry of Agriculture and provincial health bureaus | Long term (≥ 4 years) |

| Breakthroughs in texturization and fermentation | +1.5% | National, with research and development hubs in Shandong, Jiangsu, and Guangdong provinces | Medium term (2-4 years) |

| Rise of the "beauty-from-within" sector | +0.9% | National, with early adoption in coastal cities and e-commerce channels | Short term (≤ 2 years) |

| Sustainability and "dual carbon" goals | +1.4% | National, with priority enforcement in industrial zones and state-owned enterprises | Long term (≥ 4 years) |

| Demand for clean-label and non-GMO transparency | +1.0% | National, with the strongest demand in Tier-1 cities and premium retail channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of flexitarian and vegan lifestyles

In Tier-1 cities, urban Chinese consumers, especially millennials and Gen Z, are increasingly turning to flexitarian diets. These diets reduce, but don't completely eliminate, animal protein. This trend is largely driven by health concerns, such as obesity and cardiovascular diseases, and the influence of global plant-based food trends, which have gained traction through social media and international quick-service restaurant (QSR) chains. As a result of this dietary shift, there's a growing demand for convenient and flavorful plant protein products. These products seamlessly integrate into everyday meals, such as oat milk lattes at Starbucks and Luckin Coffee, plant-based nuggets at KFC, and ready-to-cook meat alternatives available in fresh formats at Hema and Freshippo. In February 2024, Yili's Plant Selected brand introduced chocolate soy milk, followed by a high-calcium soy milk collection in August 2024[1]Source: Yili Group, “Plant Selected Launches Functional Soy Milk,” yili.com. Both products, boasting 5.2 grams of plant protein per carton and made from 100% non-GMO soybeans sourced from Northeast China, are aimed at younger consumers who prioritize functional nutrition in familiar beverage formats. The real opportunity for flexitarianism isn't in persuading die-hard meat lovers to change their ways. Instead, it's about tapping into moments like weekday lunches, post-workout snacks, and "Meatless Mondays." Here, the focus is on taste and convenience rather than ideology. Yet, it's worth noting that this segment is sensitive to pricing, which restricts its reach and frequency, especially outside of affluent households.

"Healthy China 2030" and "grand food vision" initiatives

Beijing's long-term nutrition strategy aims to boost legume and plant protein consumption to combat diet-related chronic diseases and bolster food security. The Food and Nutrition Development Guideline (2025-2030) targets an increase in per capita legume consumption to 14 kilograms annually by 2030 and mandates that over 50% of dietary protein come from premium sources, such as soy and pea proteins. This policy is enacted through subsidies for domestic legume farming, research and development grants for plant protein processing, and nutrition education in schools and workplaces. The Ministry of Agriculture's "Grand Food Vision" underscores the need to diversify protein sources beyond pork and poultry, aiming to bolster resilience against African swine fever and feed price fluctuations. In provinces like Shandong, Heilongjiang, and Inner Mongolia, governments are encouraging farmers to increase soybean and pea cultivation by offering guaranteed purchase prices and crop insurance, ensuring a stable supply for processing investments. While China's State Council has integrated plant protein growth into its 14th Five-Year Plan, highlighting its importance, challenges loom. Local officials often favor grain self-sufficiency over specialty protein crops, especially when land-use disputes arise.

Breakthroughs in texturization and fermentation

High-moisture extrusion (HME) and precision fermentation technologies are bridging the sensory divide between plant proteins and animal meat, tackling the main hurdle to repeat purchases. In May 2025, Roquette introduced NUTRALYS Pea 700M (textured, minced) and 700FL (small chunks), offering fibrous, juicy textures for ground and poultry-style uses[2]Source: Roquette, “NUTRALYS Pea Protein Portfolio,” roquette.com. This innovation removes the need for manual shredding, allowing manufacturers to achieve a meat-like bite at reduced processing costs. Kerry's Plenti, a whole-muscle textured soy protein crafted using proprietary HME with Ojah technology, boasts ready-marinated, fibrous structures. With clean labels featuring just six ingredients, it's poised to attract premium plant-based brands that enjoy price premiums over traditional meat. Meanwhile, in the fermentation arena, Yihai Kerry's new subsidiary in Qinhuangdao, backed by a RMB 136 million investment, is diving into microbial protein production. This approach sidesteps traditional crop agriculture, aiming to offer cost-effective, scalable proteins with customized amino acid profiles, catering to sports nutrition and elder care. The message is unmistakable: firms excelling in texturization and fermentation stand to gain premium margins in consumer markets, while those dependent on commodity protein isolates will find themselves in price wars within industrial feed and ingredient sectors.

Rise of the "beauty-from-within" sector

Chinese consumers are turning to ingestible beauty products, such as collagen peptides, antioxidant drinks, and protein-enriched snacks, all promising benefits like skin hydration, elasticity, and anti-aging effects. This trend has carved out a lucrative niche for plant proteins boasting bioactive peptide profiles. Hydrolyzed rice, wheat, and soy proteins are now being crafted into beauty drinks, gummies, and powdered sachets. These products are marketed through e-commerce platforms and specialty beauty retailers, often in collaboration with skincare lines to bolster efficacy claims. Consumers in this segment prioritize hypoallergenic, clean-label ingredients over cost, allowing plant protein suppliers to charge 2-3 times more than standard protein isolates. Influencer marketing and references to clinical studies amplify this trend. Brands emphasize the peptide molecular weight (ideally between 500-3,000 Daltons for best absorption) and key amino acids (like proline, glycine, and hydroxyproline) to set themselves apart from standard collagen supplements. Although the beauty-from-within market is still modest compared to food and feed sectors, its rapid growth and premium pricing make it an attractive target for ingredient suppliers. These suppliers are eager to diversify away from commodity soy and seek refuge from margin pressures in bulk markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taste and texture discrepancies | -1.3% | National, with higher sensitivity in Tier-3 and rural markets | Medium term (2-4 years) |

| Regulatory hurdles for novel proteins | -0.8% | National, governed by NMPA and CFSA approval processes | Long term (≥ 4 years) |

| Dominance of traditional soy products | -1.1% | National, with the strongest impact in inland provinces and lower-income demographics | Long term (≥ 4 years) |

| Entrenched cultural preference for fresh meat | -1.5% | National, with the highest resistance in rural areas and older demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Taste and texture discrepancies

Despite advancements in extrusion and flavoring technologies, plant protein products still grapple with off-flavors (like beany, grassy, and bitter notes), a grainy or chalky mouthfeel, and a lack of juiciness compared to their animal meat counterparts. This has limited repeat purchases and hindered market penetration beyond early adopters. Studies on consumer acceptance reveal that while most urban millennials are open to trying plant-based meat alternatives, fewer than 10% consume them regularly, primarily due to sensory shortcomings. The challenge intensifies in applications demanding a whole-muscle texture, such as steaks, chicken breasts, and fish fillets, where plant proteins falter in mimicking the fibrous, anisotropic structure of animal muscle. In early 2024, Oatly's sub-brand 东边植造 (Dongbian Zhizao) introduced a rice milk plant-based protein drink. However, feedback from consumers pointed out concerns over its perceived high calorie content and the challenge of conveying its premium value, especially when rice is both ubiquitous and inexpensive in China. The sensory gap is closing. For example, Roquette's NUTRALYS Pea F853M isolate boasts high gel strength, allowing it to form firm, gel-like structures when heated. Meanwhile, Kerry's Plantfare specialty proteins employ proprietary masking technology to counteract off-notes. Yet, achieving true taste parity on a large scale is still 3-5 years away for many applications. In the interim, while plant proteins may find a foothold in flexitarian meals and ingredient fortifications, they face an uphill battle in displacing animal proteins during core meal occasions where taste reigns supreme.

Regulatory hurdles for novel proteins

Before commercialization, the NMPA and CFSA's framework for assessing novel food ingredients mandates multi-year safety dossiers, toxicology studies, and production process validation, delaying market entry for non-traditional plant proteins like hemp protein, potato protein isolates, and fermentation-derived mycoprotein. In April 2023, Shandong Shunfeng Biotechnology's high-oleic-acid gene-edited soybean received China's first plant gene-editing biosafety certificate. However, approvals for commercial cultivation and processing are still pending as regulators evaluate environmental impact and allergenicity. These regulatory hurdles disproportionately challenge smaller innovators lacking resources for clinical trials and navigating bureaucracy, consolidating market share among established soy and pea protein suppliers with existing approvals. International players face added complexity: ingredients approved in the EU or US require separate China-specific dossiers and cannot leverage foreign safety data, extending timelines by 18-24 months. Strategically, novel protein commercialization in China follows a "fast follower" approach. Domestic firms often wait for international brands to absorb regulatory risks and validation costs, then license technologies or develop biosimilar ingredients once approval pathways are clear. This dynamic slows innovation diffusion and limits the diversity of plant protein ingredients available to Chinese manufacturers compared to Western markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Protein Type: Pea Protein Disrupts Soy's Dominance

In 2025, soy protein held 56.05% of China's plant protein market, reflecting its established processing infrastructure, agronomic familiarity, and consumer acceptance in traditional forms like tofu, soymilk, and textured vegetable protein. However, pea protein is the fastest-growing segment, with a 9.02% CAGR from 2026 to 2031, driven by its hypoallergenic nature, non-GMO appeal, and functionality in meat alternatives and sports nutrition. Yantai Shuangta, with its 130,000-tonne annual pea protein capacity and partnerships with major brands, is a key supplier for plant-based meat trials in China[3]Source: Shuangta Food, “Annual Report 2024,” shuangtafood.com. Roquette's May 2025 launch of NUTRALYS Pea F853M isolate and H85 hydrolysate expands options for Chinese manufacturers seeking differentiation beyond soy isolates. Wheat protein, traditionally used in bakery and noodle applications, is gaining traction in meat analogues. Roquette's June 2025 launch of NUTRALYS T WHEAT 600L targets poultry-style products and offers simpler processing versus high-moisture extrusion.

Rice and potato proteins, though niche, are growing in hypoallergenic and clean-label markets, including soy and gluten-free infant formulas, medical nutrition, and allergen-free snacks. Hemp protein faces regulatory delays despite its complete amino acid profile and omega-3 content, as NMPA approval processes extend commercialization timelines by 18-24 months. Other plant proteins, such as sunflower, pumpkin seed, and fava bean, are in early trials, primarily for export-oriented formulations targeting Western brands. While soy retains volume leadership in feed and traditional food applications, margins and innovation are shifting to pea, wheat, and specialty proteins that enable premium positioning and functional differentiation. Suppliers investing in pea and wheat texturization capacity are well-positioned to capture growth in consumer-facing segments, while commodity soy suppliers face margin compression and increased competition in bulk ingredient markets.

By End User: Animal Feed Outpaces Consumer Applications

In 2025, food and beverages led the China plant protein market with a 53.91% share, covering dairy alternatives (oat, soy, almond milk), meat analogues (burgers, nuggets, sausages), high-protein bakery items, and ready-to-eat meals. The animal feed segment, growing at a 9.81% CAGR from 2026 to 2031, is driven by aquaculture and livestock producers seeking cost-effective, deforestation-free protein meals to replace imported fishmeal and improve feed conversion ratios. While soybean meal dominates feed formulations, pea protein and other plant proteins are gaining traction in premium aquaculture feeds (shrimp, salmon) due to superior digestibility and water stability. China's aquaculture, producing over 50 million tonnes annually, offers a structural opportunity for plant protein suppliers meeting cost and nutritional requirements. In food and beverages, dairy and alternatives dominate, with oat milk gaining popularity in coffee chains and soy milk innovations by Yili, Mengniu, and Vitasoy. Mengniu's H1 2025 launch of over 100 products, including lactose-free and dual-protein options, highlights hybrid dairy-plant products' potential. Meat, poultry, seafood, and plant-based alternatives remain niche but are expanding, with Cargill's PlantEver brand and Lawson collaborations showcasing retail and foodservice pathways. Manufacturers are fortifying beverages and ready-to-eat products with plant proteins to meet "high protein" claims and attract health-conscious consumers.

Personal care and cosmetics, though a smaller segment, command premium pricing. Hydrolyzed plant proteins (rice, wheat, soy peptides) are used in beauty beverages, gummies, and skincare products marketed via e-commerce and specialty retailers. Supplements, sports nutrition, elderly nutrition, and infant formula represent strategic niches where plant proteins (pea, rice, soy) offer allergen-free, vegan, and clean-label alternatives to whey and casein. Kerry's May 2025 expansion of its plant protein range, including pea, rice, and sunflower blends with PDCAAS up to 1.0, targets infant nutrition, senior beverages, and vegan products, reflecting ingredient suppliers' focus on specialized formulations. The end-user landscape is shifting: while animal feed and commodity food applications drive volume growth, supplements, personal care, and premium consumer products lead in margins and innovation, where functional benefits and clean-label positioning justify higher prices.

Geography Analysis

China's plant protein market, while nationally distributed, shows a pronounced regional concentration in both processing capacity and consumption patterns. Shandong province leads in upstream production, hosting major players like Yantai Shuangta (specializing in pea protein), Shandong Yuwang (with a capacity of 600,000 tonnes per year for soybean processing, 130,000 tonnes for soybean protein, and 20,000 tonnes for plant-based meat), alongside Shandong Jianyuan, Shandong Crown Protein, and Shandong Wonderful Industrial. These companies benefit from their proximity to legume cultivation areas and established food processing clusters. Meanwhile, Jiangsu and Guangdong provinces focus on downstream applications, producing dairy alternatives, meat analogues, and ingredients for personal care. These provinces enjoy advantages such as proximity to consumer markets, port infrastructure for both imports and exports, and a talent pool in food science and biotechnology research and development. Heilongjiang and Inner Mongolia play a crucial role by supplying soybeans and other legumes. Their provincial governments incentivize farmers to expand acreage through guaranteed minimum purchase prices and crop insurance, ensuring a stable upstream supply that supports downstream processing investments.

Tier-1 cities like Beijing, Shanghai, Guangzhou, and Shenzhen lead the way in per-capita consumption of premium plant protein products. These cities are seeing a surge in popularity for items like oat milk lattes, plant-based burgers, and beauty-from-within supplements. This trend is largely driven by the cities' higher disposable incomes, their exposure to global food trends, and a dense concentration of modern retail and foodservice channels. On the other hand, Tier-2 and Tier-3 cities, while currently showcasing lower penetration rates, are experiencing rapid growth. This uptick is largely attributed to the expansion of e-commerce platforms and convenience store chains, such as FamilyMart, 7-Eleven, and Lawson, which are broadening the distribution of plant protein products beyond the coastal markets.

In rural areas, traditional soy products like tofu and soymilk still reign supreme. There's a noticeable cultural resistance to adopting plant-based meat analogues. However, these regions do show a volume demand for animal feed, especially in agricultural zones where livestock and aquaculture operations are concentrated. The landscape presents an asymmetric opportunity: while consumer-facing brands should focus on Tier-1 and Tier-2 cities to build brand awareness and achieve critical mass, ingredient suppliers and feed manufacturers can tap into volume growth in inland provinces and agricultural zones. Here, the emphasis on cost competitiveness and functional performance often overshadows brand and sustainability messaging.

Competitive Landscape

The China plant protein market exhibits moderate fragmentation, with domestic leaders such as Yantai Shuangta, COFCO, Shandong Yuwang, and Wilmar/Yihai Kerry dominating soy and pea protein processing. International players like Roquette, ADM, Cargill, Bunge, and DuPont leverage proprietary technologies and global supply chains to target premium segments and export-oriented manufacturers. Competition is centered on three key areas: cost leadership in commodity soy and feed applications, driven by scale economies and vertical integration; functional differentiation in texturized and specialty proteins, enabled by extrusion technologies and clean-label credentials; and sustainability, where deforestation-free sourcing and carbon-neutral certifications secure B2B contracts with multinational food companies and institutional buyers. Yihai Kerry's establishment of a fermentation protein subsidiary with RMB 136 million in registered capital signals the growing importance of precision fermentation, which bypasses crop-based constraints and offers tailored amino acid profiles for specialized nutrition. White-space opportunities remain in hybrid dairy-plant protein products, allergen-free infant formulas, and plant-based seafood analogues, where incumbents have yet to establish dominance and consumer acceptance is still evolving.

Technology adoption is accelerating, as evidenced by Roquette's HME-produced textured proteins, Kerry's Plenti whole-muscle analogues, and Yantai Shuangta's partnerships with Beyond Meat and Nestlé. Suppliers investing in extrusion, fermentation, and co-manufacturing capabilities are well-positioned to capture growth in consumer-facing segments. Shandong Shunfeng Biotechnology's advancements, including an April 2023 biosafety certificate for high-oleic-acid gene-edited soybean (≥80% oleic acid) and a November 2024 patent grant for proprietary Cas12 gene-editing tools, highlight domestic efforts to develop IP-protected crop traits. These innovations aim to improve protein and oil profiles, reduce reliance on imported genetics, and enhance China's competitiveness in the plant protein value chain.

The competitive landscape is evolving from a focus on commodity volume competition to differentiated ingredient solutions. Emerging disruptors include fermentation protein startups, regional specialty protein processors focusing on hemp, pumpkin seed, and sunflower proteins, and ingredient platforms that aggregate multiple plant protein sources to create customized blends for specific applications. Success in this market will depend on processing technology, supply chain traceability, and the ability to co-develop formulations with brand owners and foodservice operators. Companies that excel in these areas are likely to secure a competitive edge in the rapidly growing plant protein market.

China Plant Protein Industry Leaders

Archer Daniels Midland Company

Wilmar International Ltd

Roquette Frères S.A.

Shandong Jianyuan Group

Yantai Shuangta Food

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bunge completed the acquisition of IFF's soy protein and lecithin business for approximately USD 240 million, consolidating its position in specialty soy ingredients for food, nutrition, and industrial applications. The transaction adds ~USD 240 million in annual revenue and strengthens Bunge's presence in China's plant protein value chain, where soy protein isolates and lecithin are critical ingredients in dairy alternatives, meat analogues, and bakery products.

- June 2025: Roquette launched NUTRALYS T WHEAT 600L (textured wheat protein) and NUTRALYS T PEA 700XC (large-chunk textured pea protein), expanding its portfolio of functional plant proteins for meat alternatives and hybrid products. The wheat protein ingredient offers extended fibers, light color, and compatibility with a wide equipment, enabling cost-effective production for Chinese manufacturers.

- May 2025: Roquette introduced four multi-functional pea protein ingredients, NUTRALYS Pea F853M (high gel strength isolate), NUTRALYS H85 (first food-grade hydrolysed pea protein), NUTRALYS Pea 700M (textured minced), and NUTRALYS Pea 700FL (textured small chunks), expanding formulation options for meat alternatives, high-protein bars, and beverages.

China Plant Protein Market Report Scope

Plant protein is protein derived from plant sources such as legumes (beans, lentils, peas), grains (quinoa, rice, wheat), nuts, and seeds. The China plant protein market is segmented by protein type and end user. By protein type, the market is segmented into Hemp Protein, Pea Protein, Potato Protein, Rice Protein, Soy Protein, Wheat Protein, and Other Plant Protein. By end user, the market is segmented into Animal Feed, Food and Beverages, Personal Care and Cosmetics, and Supplements. The food and beverages segment is further sub-segmented into bakery, beverages, breakfast cereals, condiments/sauces, confectionery, dairy and dairy alternative products, Meat/Poultry/Seafood and Meat Alternative products, RTE/RTC food products, and snacks. Similarly, the supplements segment is further sub-segmented into Baby Food and infant formula, elderly nutrition and medical nutrition, and sport/performance nutrition. The Market forecasts are provided in terms of value (USD) and volume (Tons).

Protein Type

| Hemp Protein |

| Pea Protein |

| Potato Protein |

| Rice Protein |

| Soy Protein |

| Wheat Protein |

| Other Plant Protein |

End User

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternative Products | |

| Meat/Poultry/Seafood and Meat Alternative products | |

| RTE/RTC Food Products | |

| Snacks | |

| Personal Care and Cosmetics | |

| Supplements | Baby Food and Infant Formula |

| Elderly Nutrition and Medical Nutrition | |

| Sport/Performance Nutrition |

| Protein Type | Hemp Protein | |

| Pea Protein | ||

| Potato Protein | ||

| Rice Protein | ||

| Soy Protein | ||

| Wheat Protein | ||

| Other Plant Protein | ||

| End User | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternative Products | ||

| Meat/Poultry/Seafood and Meat Alternative products | ||

| RTE/RTC Food Products | ||

| Snacks | ||

| Personal Care and Cosmetics | ||

| Supplements | Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | ||

| Sport/Performance Nutrition | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms