China Timber Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 17.95 Billion |

| Market Size (2026) | USD 18.97 Billion |

| Market Size (2031) | USD 24.29 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

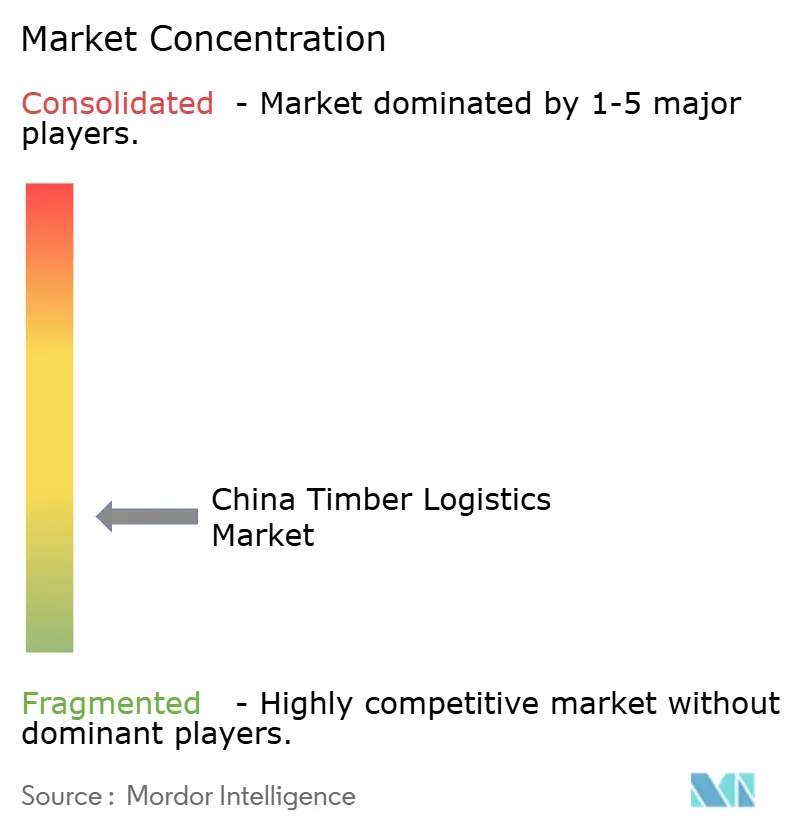

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Timber Logistics Market Analysis by Mordor Intelligence

The China timber logistics market size was valued at USD 17.95 billion in 2025 and estimated to grow from USD 18.97 billion in 2026 to reach USD 24.29 billion by 2031, at a CAGR of 5.07% during the forecast period 2026-2031.

The China timber logistics market remains supported by structural import dependence, as domestic output has not fully replaced the large softwood logs and tropical hardwood grades needed by downstream manufacturers, despite domestic timber production estimated at 144 million m³ in 2025. The China timber logistics market is also being reshaped by port-centered handling, inland rail links, and specialized sea-rail services that keep cargo moving into major processing belts at faster speeds and with greater coordination. Compliance demands are becoming more commercialized in the China timber logistics market as imported wood-based panels now face a clearer inspection framework under the August 2025 customs announcement, which increases the need for documentation, yard planning, and timed release management. The China timber logistics market is still under pressure from the property downturn and remains far below 2020 levels, weakening construction-linked timber throughput even as logistics operators pushed more value-added services into contracts. Even with softer raw volume conditions, the China timber logistics market is preserving growth through repricing toward integrated services such as sorting, fumigation, bonded storage, route visibility, and digitally managed inventory control.

Key Report Takeaways

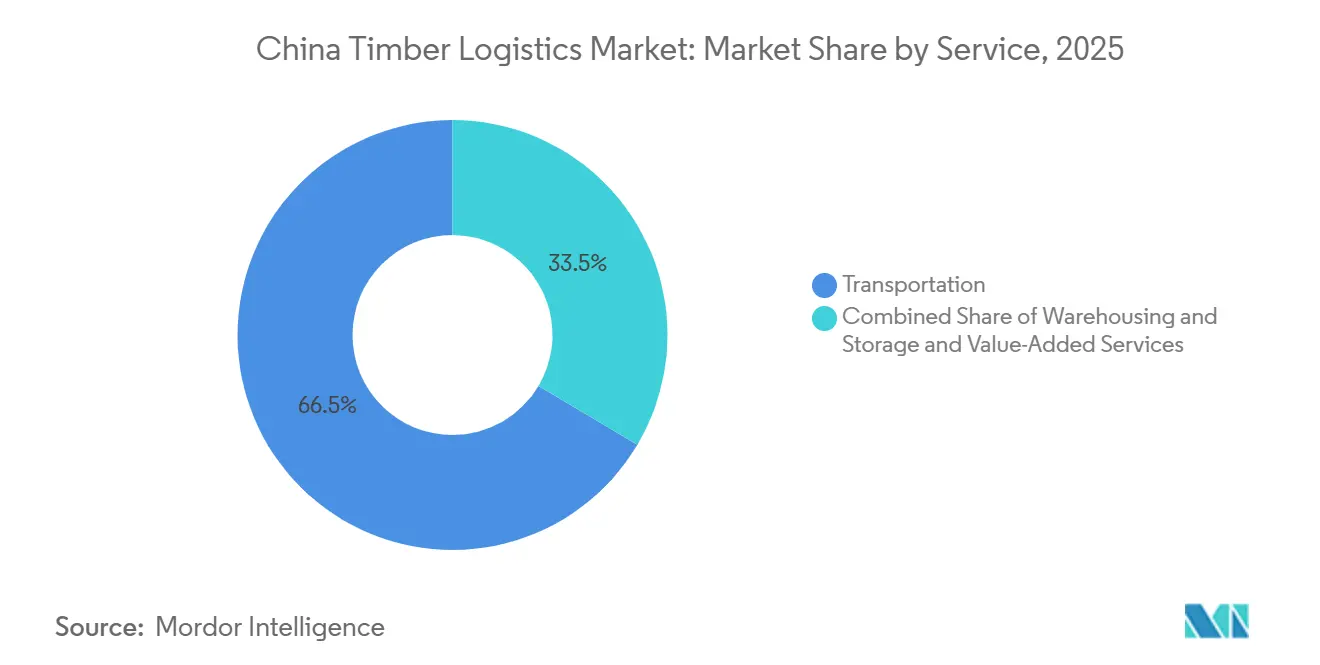

- By service, transportation accounted for 66.48% of the China timber logistics market share in 2025, while value-added services recorded the highest projected CAGR of 7.30% through 2031.

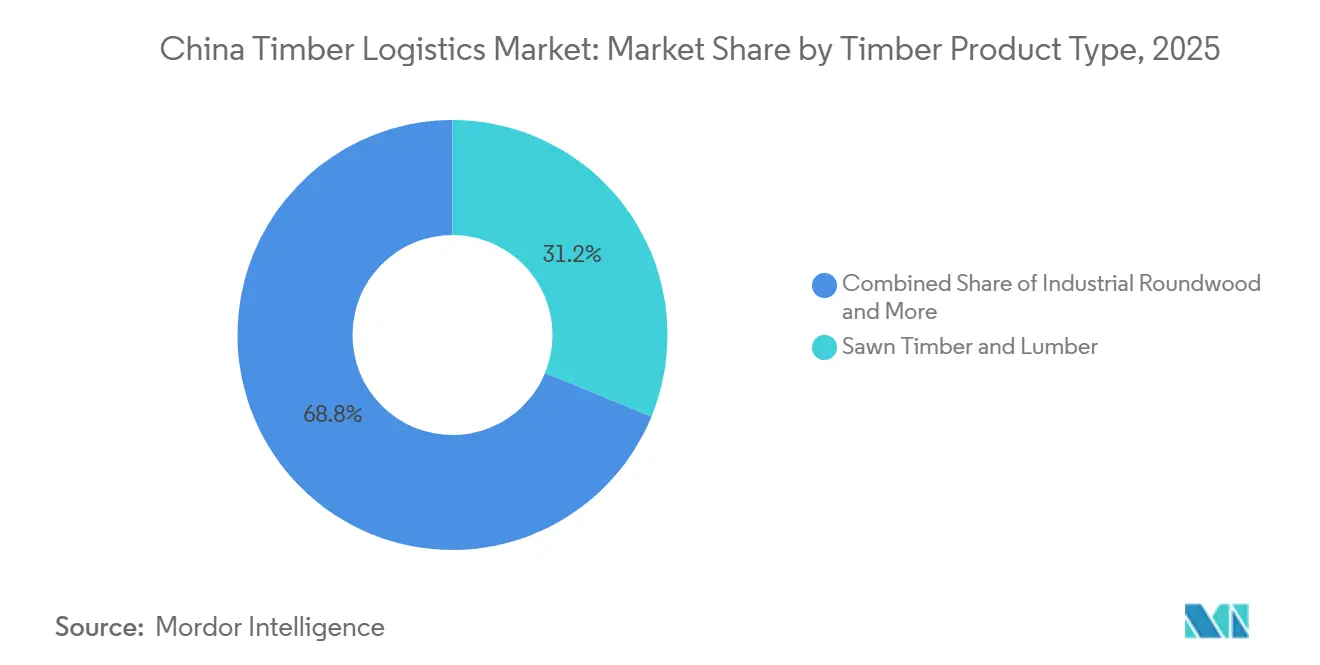

- By timber product type, sawn timber and lumber accounted for 31.19% of product type logistics value in 2025, while engineered wood products are projected to expand at an 8.23% CAGR through 2031.

- By end-use industry, construction and infrastructure accounted for 44.03% of the China timber logistics market size in 2025, while packaging is forecast to grow at a 7.82% CAGR through 2031.

- By geography, East China accounted for 39.24% of the China timber logistics market share in 2025, while South China is forecast to grow at a 6.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Timber Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained Import Dependence for Log and Lumber Flows | +1.2% | East China core including Rizhao, Taicang, and Zhangjiagang, with secondary gains in Northeast and North China | Short term (≤ 2 years) |

| Port-Centric Distribution Networks Along the East Coast | +0.9% | East China, especially the Yangtze River Delta, with spillover to the Bohai Rim and Pearl River Delta | Medium term (2-4 years) |

| Rail and Intermodal Connectivity Into Inland Processing Clusters | +0.8% | Southwest and Central China through the ILSTC corridor, along with Northeast and North China inland hubs | Medium term (2-4 years) |

| Rising Traceability Requirements Across Cross-Border Timber Flows | +0.4% | Global, with compliance concentration in East and South China export clusters | Long term (≥ 4 years) |

| Supply Diversification Away From Single-Origin Dependence | +0.7% | North and Northeast China for Russia alternatives, and South and Southwest China for ASEAN inflows | Short term (≤ 2 years) |

| Digital Yard, Inventory, and Route Visibility Adoption | +0.5% | East China smart port zones and South China bonded logistics parks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustained Import Dependence for Log and Lumber Flows

The China timber logistics market remains tied to imported timber because domestic production does not fully cover the species mix and log dimensions used by furniture, panel, and engineered wood producers. China produced an estimated 144 million m³ of timber in 2025, yet imported wood still filled critical supply gaps for processors that depend on large-diameter softwood and tropical hardwood inputs[1]USDA Foreign Agricultural Service, “Solid Wood Products Annual 2025, China,” GAIN Report CH2026-0020, apps.fas.usda.gov. That dependence keeps the China timber logistics market active across seaborne arrivals, port handling, fumigation, and inland distribution even when end demand softens. The cargo mix also underscores the value of specialized logistics, as timber buyers need sorting, origin control, and timing support beyond freight movement alone. This is why the China timber logistics market keeps expanding in revenue terms even when raw throughput does not rise at the same pace.

Port-Centric Distribution Networks Along the East Coast

The China timber logistics market is still organized around East Coast ports because these locations offer berth access, bonded storage, customs capacity, and proximity to the country’s largest wood-processing belts. Jiangsu, Shandong, Shanghai, Guangdong, Fujian, and Hebei remained the 6 leading wood-import provinces in the USDA account, underscoring how strongly import geography shapes the national logistics system. This concentration gives the China timber logistics market a clear coastal backbone, with inland processors depending on efficient transfer from the port gate to the industrial park. The model also supports higher service intensity because bonded yards near the ports can stage sorting, temporary storage, and release scheduling before timber moves inland. As a result, coastal logistics operators retain pricing power across service layers beyond base freight.

Rail And Intermodal Connectivity Into Inland Processing Clusters

The China timber logistics market is becoming more flexible as rail and sea-rail services are narrowing the long-standing cost gap between coastal buyers and inland processors. Ganzhou International Inland Port has operated more than 1,700 China-Europe freight trains since 2015, and timber from Europe has been reaching Jiangxi in around 12 days at lower logistics costs, demonstrating how inland sourcing options have improved[2]People’s Daily Online, “China-Europe Freight Train Turns Inland Furniture Hub into Global Trade Player,” People’s Daily Online, en.people.cn. China Railway has also formalized specialized timber service offerings within the China Railway Express product system, which supports better planning for wood cargo on long-distance corridors. This shift matters for the China timber logistics market because inland plants in Central and Southwest China now have more routing options and greater leverage when negotiating service terms. It also pushes coastal operators to extend their role beyond port handling and into deeper inland coordination.

Digital Yard, Inventory, and Route Visibility Adoption

The China timber logistics market is moving toward greater digital control as timber yards and warehouses face pressure to improve traceability, cycle times, and inventory accuracy. Cloud-based warehouse management systems designed for timber use RFID, barcode scanning, and connected monitoring tools to improve stock visibility and yard discipline[3]Mutouyun, “Mutouyun Warehouse Management System Product,” Mutouyun, mutouyun.com. These tools matter in the China timber logistics market because they help operators separate species, track origin information, and prepare cleaner dispatch records for customers and inspectors. Better visibility also supports revenue growth since buyers are more willing to pay for reliable inventory data and faster release planning when supply conditions are uncertain. Over time, the gap between digitally capable operators and manual operators is likely to widen within the China timber logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real Estate Downcycle Weakening Timber Throughput | -1.0% | National, with deeper effects in North China, Northeast China, and major Yangtze Delta processing clusters | Short term (≤ 2 years) |

| Phytosanitary Holds and Border Inspection Delays | -0.5% | East China ports including Lanshan, Taicang, and Beilun, along with Northeast gateways | Short term (≤ 2 years) |

| Export Bans in Supplier Countries Constraining Inbound Volumes | -0.6% | East and South China tropical hardwood ports, along with Northeast China softwood corridors | Medium term (2-4 years) |

| Fragmented Inland Haulage and Empty-Backhaul Inefficiency | -0.4% | Central, Southwest, and Northwest China, especially non hub inland distribution legs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Real Estate Downcycle Weakening Timber Throughput

The China timber logistics market is facing its clearest demand restraint from the property downturn because new housing starts fell 20% in 2025 and remained 74% below 2020 levels. Lower residential activity reduces structural timber demand, softens fit-out related wood consumption, and weakens furniture demand tied to the housing cycle. That pressure feeds directly into the China timber logistics market through lower port throughput, lower storage yard utilization, and weaker turns on inland routes. Infrastructure spending still provides some support, but the timber mix in those projects is less favorable than that from residential construction. This leaves operators with heavier exposure to construction corridors under more strain than players that can sell bundled handling or compliance services.

Phytosanitary Holds And Border Inspection Delays

The China timber logistics market also faces friction from quarantine checks and border inspection procedures, which create uncertainty around cargo release timing and inventory planning. The August 2025 customs framework for imported wood-based panels added a clearer inspection structure, but it also reinforced compliance tasks that can extend dwell time when documentation or testing workflows are not aligned[4]China Council for the Promotion of International Trade, “Understanding Regulatory Rules for the Adoption of Inspection Results on Imported Wood-Based Panel,” CCEECCIC, cceeccic.org. That creates a direct cost burden in the China timber logistics market because storage, sequencing, and truck scheduling all become harder when release windows shift. Providers with stronger customs support and in-house documentation capability are better placed to protect service quality under these conditions. Smaller operators with weaker compliance systems are more exposed to margin pressure from delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Dominance Masks Value-Added Service Momentum

Transportation held 66.48% of the China timber logistics market share in 2025, making it the largest service category across the report. Road haulage still handled the core movement between coastal log terminals and inland processing parks, while inland waterway flows on the Yangtze and Pearl River systems remained important for bulk distribution. Rail also became more relevant as inland processors looked for more stable long-distance routing. This kept transportation at the center of the China timber logistics market even as margins became more uneven across modes.

Value-added services are forecast to expand at a 7.30% CAGR through 2031, making them the fastest-growing service layer in the China timber logistics market. Debarking, grading, fumigation, wood chip processing, and supply chain financing are increasingly being sold as part of broader logistics contracts rather than as separate add-ons. This trend is strongest in bonded port parks where operators can handle sorting and verification before domestic release. China Railway’s specialized timber service offerings also support more coordinated multimodal solutions that raise the value of managed transport packages.

By Timber Product Type: Sawn Timber Leads, Engineered Wood Accelerates

Sawn timber and lumber accounted for 31.19% of product type logistics value in 2025, making it the largest timber product segment in the Chinese timber logistics market. This reflected the importance of imported softwood lumber for furniture manufacturing, residential fit-out, and broader wood-processing demand. Russia alone accounted for 70% of China’s softwood lumber arrivals, keeping northern and northeastern corridors closely tied to that supply chain. Industrial roundwood and logs remained another major flow, with logistics centered on coastal fumigation, short-haul transfer, and dispatch into nearby mills.

Engineered wood products are projected to grow at an 8.23% CAGR from 2026 to 2031, making them the fastest-growing product segment in the Chinese timber logistics market. Their growth reflects rising interest in green building materials and broader use of products such as CLT and laminated veneer lumber in non-residential structures. This shift favors logistics operators that can handle cleaner storage, product segregation, and more controlled inland movement. Pulpwood, chips, and fiber still provide a stable base, while pellets and briquettes remain smaller but gradually expanding flows linked to energy transition demand.

By End-Use Industry: Construction Anchors Volume, Packaging Drives Growth

Construction and infrastructure accounted for 44.03% of the China timber logistics market size in 2025, making it the largest end-use segment. Its lead came from the scale of building and infrastructure activity that still required timber-related inputs even during a softer housing cycle. Urban renewal, water conservancy, and transport projects helped preserve movement volumes, although the timber mix shifted toward formwork panels and engineered components. This kept construction as the main volume anchor in the China timber logistics market, even as residential demand remained weak.

Packaging is expected to record a 7.82% CAGR through 2031, which makes it the fastest-growing end use in the China timber logistics market. The segment is benefiting from cross-border e-commerce and the growing demand for engineered wood crating for electronics, automotive parts, and industrial equipment. Furniture manufacturing remained the second largest end user, but it faced pressure in 2025 as softer domestic demand and weaker export conditions reduced procurement appetite. Pulp and paper, energy and biomass, and smaller specialty uses continue to provide a diversified demand base for the China timber logistics industry.

Geography Analysis

East China accounted for 39.24% of the China timber logistics market share in 2025, which made it the largest regional cluster. The region benefits from long-established import infrastructure, dense processing belts, and strong links between ports and manufacturing centers. Ningbo Zhoushan Port processed more than 1.4 billion tons of cargo in 2025 and remained the world’s busiest port by throughput, while the Tiaozhoumen Channel expansion improved access for large vessels and eased a key operating constraint. That scale supports the China timber logistics market by enabling faster vessel handling, stronger storage capacity, and better onward dispatch to Jiangsu, Zhejiang, and Shandong. North China also plays an important role because Tianjin and Qingdao connect imported lumber flows to large inland demand centers across Hebei, Beijing, and Inner Mongolia.

South China is projected to grow at a 6.97% CAGR from 2026 to 2031, which makes it the fastest-growing regional segment in the China timber logistics market. Guangdong’s furniture and manufacturing base, especially around Foshan, Dongguan, and Zhongshan, continues to support hardwood imports and secondary packaging demand. The Pearl River Delta adds another layer of demand because export oriented producers need timber based packing materials for electronics, consumer goods, and equipment shipments. Central China is also becoming more relevant as rail connectivity improves access to coastal ports and lowers the disadvantage that inland plants once faced. The Ganzhou corridor shows that inland timber movement can now be faster and more cost effective, which strengthens the position of processors in Jiangxi and nearby provinces.

Southwest China does not have the largest current base in the China timber logistics market, but its logistics role is rising as corridor investment improves access between inland parks and the Beibu Gulf gateway. The Pinglu Canal was more than 90% complete in 2026, which points to better waterway access for future cargo movement into Southwest China. Northeast China remains important for softwood linked trade, while Northwest China is still the smallest regional segment but is gradually gaining freight rail relevance through broader western connectivity. Together, these changes show that the China timber logistics market is still coastal in structure, but it is becoming more geographically flexible than it was in earlier years.

Competitive Landscape

The China timber logistics market is moderately fragmented, with large state-backed port and shipping groups leading bulk handling while specialized operators compete in value-added and digitally managed services. The strongest incumbents control port access, bonded yards, fumigation capability, and on-dock processing support, which gives them a real edge on the first logistics leg. That edge matters because timber buyers often prefer a single operator who can manage unloading, temporary storage, customs coordination, and inland dispatch in a single chain. At the same time, the China timber logistics market still leaves room for smaller specialists that can serve niche corridors, product-specific handling needs, or digitally intensive customer requirements. This keeps competition active even though scale remains important.

The main strategic divide in the China timber logistics market is between players building deeper, more integrated networks and those trying to expand origin and route coverage. COSCO SHIPPING Holdings launched the Hefei Integrated Warehouse Yard Project in May 2026, which linked transport corridors, container yards, and warehousing into a single inland distribution platform for flows in the Yangtze River Delta and Central China. Guangzhou Port Group also moved to strengthen cross regional coordination in April 2026 through formal exchanges with Hebei Port Group and Tianjin Port Group on network optimization, smart port work, and north south coordination. Ningbo Zhoushan Port’s channel expansion in late 2025 was another important competitive move because it improved deep water access and supported higher vessel efficiency in East China. These moves show how leading groups are protecting their position through network depth and infrastructure quality rather than only price.

Digital capability is becoming a clearer separator in the China timber logistics market because customers want better visibility on stock, origin, and release timing. Timber focused warehouse systems that use connected tracking tools help operators reduce yard friction and improve dispatch accuracy. This matters because compliance and traceability requirements are becoming more central to commercial service quality. Operators that cannot provide reliable documentation, real time inventory visibility, or coordinated inland planning are likely to lose bargaining power. As a result, the China timber logistics market is still open to many players, but the winners are increasingly those that combine infrastructure scale with stronger systems.

China Timber Logistics Industry Leaders

China National Forest Products Group (CFPC)

Jiangsu Wanlin Modern Logistics Co., Ltd.

Rizhao Port Co., Ltd.

COSCO SHIPPING Holdings Co., Ltd.

Sinotrans Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: A.P. Moller – Maersk launched the FI2 ocean service connecting Far East Asia, including Shanghai, to the Indian Subcontinent with the first westbound sailing departing on June 4, 2026, responding to growing customer demand for China-India trade capacity. The service complements the existing FI3 route and improves frequency and routing flexibility, strengthening supply chain resilience across one of the fastest-growing emerging trade lanes.

- May 2026: COSCO SHIPPING Holdings launched the Hefei Integrated Warehouse-Yard Project through subsidiary Shanghai Pan Asia Shipping and COSCO SHIPPING Logistics, establishing a three-in-one logistics ecosystem integrating transport corridors, container yards, and warehousing within the Yangtze River Delta. The project advances the group's Channel + Hub + Network inland logistics strategy and positions the company to capture timber and industrial cargo redistribution flows from East China ports into Central China processing clusters.

- April 2026: Guangzhou Port Group led a delegation to Hebei Port Group and Tianjin Port Group to formalize collaboration on shipping network optimization, green and smart port initiatives, and North-South port-shipping coordination. The engagement signals a strategic push by South China's largest port group to build a national port ecosystem capable of routing timber inflows more efficiently between originating berths and hinterland demand centers.

- December 2025: Ningbo-Zhoushan Port achieved trial navigation of its expanded Tiaozhoumen Channel, enabling 300,000-ton vessels to transit during high tide and 200,000-ton container ships to navigate at all times, creating a dual deep-water channel configuration that removes infrastructure constraints for ultra-large timber-carrying bulk carriers.

China Timber Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Waterway | |

| Multimodal | |

| Warehousing and Storage | |

| Value-Added Services |

| Industrial Roundwood / Logs |

| Fuelwood & Biomass |

| Sawn Timber & Lumber |

| Engineered Wood Products |

| Pulpwood, Chips, and Fibre |

| Pellets and Briquettes |

| Other Timber Types |

| Construction & Infrastructure |

| Pulp & Paper Industry |

| Furniture Manufacturing |

| Packaging Industry |

| Energy & Biomass Industry |

| Other End-Use Industries |

| East China |

| South China |

| North China |

| Northeast China |

| Central China |

| Southwest China |

| Northwest China |

| By Service | Transportation | Road |

| Rail | ||

| Waterway | ||

| Multimodal | ||

| Warehousing and Storage | ||

| Value-Added Services | ||

| By Timber Product Type | Industrial Roundwood / Logs | |

| Fuelwood & Biomass | ||

| Sawn Timber & Lumber | ||

| Engineered Wood Products | ||

| Pulpwood, Chips, and Fibre | ||

| Pellets and Briquettes | ||

| Other Timber Types | ||

| By End-Use Industry | Construction & Infrastructure | |

| Pulp & Paper Industry | ||

| Furniture Manufacturing | ||

| Packaging Industry | ||

| Energy & Biomass Industry | ||

| Other End-Use Industries | ||

| By Geography | East China | |

| South China | ||

| North China | ||

| Northeast China | ||

| Central China | ||

| Southwest China | ||

| Northwest China |

Key Questions Answered in the Report

What is the current size of the China timber logistics market?

The China timber logistics market stood at USD 17.95 billion in 2025 and is valued at USD 18.97 billion in 2026, with a forecast of USD 24.29 billion by 2031.

How fast is timber logistics in China expected to grow through 2031?

The report projects the China timber logistics market to grow at a 5.07% CAGR from 2026 to 2031.

Which service area leads revenue in China timber logistics?

Transportation remained the largest service segment, holding 66.48% of revenue in 2025 because road, waterway, and rail movements still anchor the full supply chain.

Which product category is growing the fastest in timber logistics across China?

Engineered wood products are forecast to grow the fastest, with an 8.23% CAGR through 2031, supported by broader use in green building applications.

Which end use sector creates the most demand for timber movement in China?

Construction and infrastructure remained the largest end use segment in 2025 with a 44.03% share, even though the property downturn weakened some residential linked flows.

Which region is most important for timber logistics growth in China?

East China remained the largest regional base with 39.24% share in 2025, while South China is expected to grow the fastest at a 6.97% CAGR through 2031.

Page last updated on: