Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

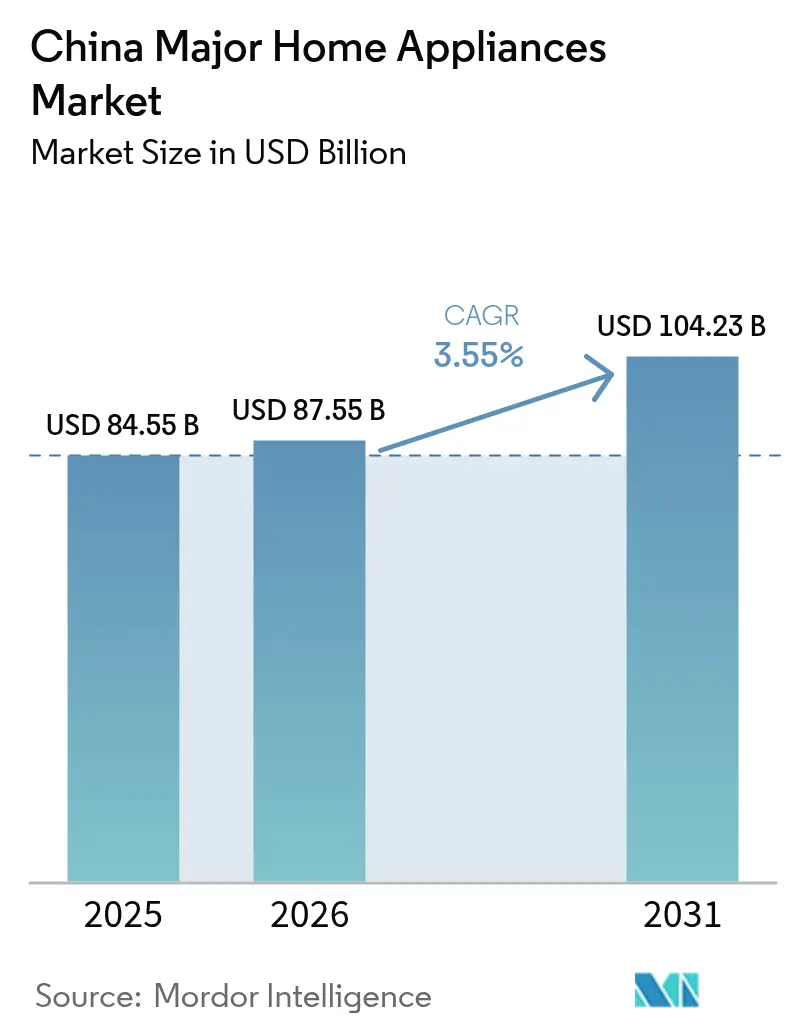

| Base Year Market Size (2025) | USD 84.55 Billion |

| Market Size (2026) | USD 87.55 Billion |

| Market Size (2031) | USD 104.23 Billion |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

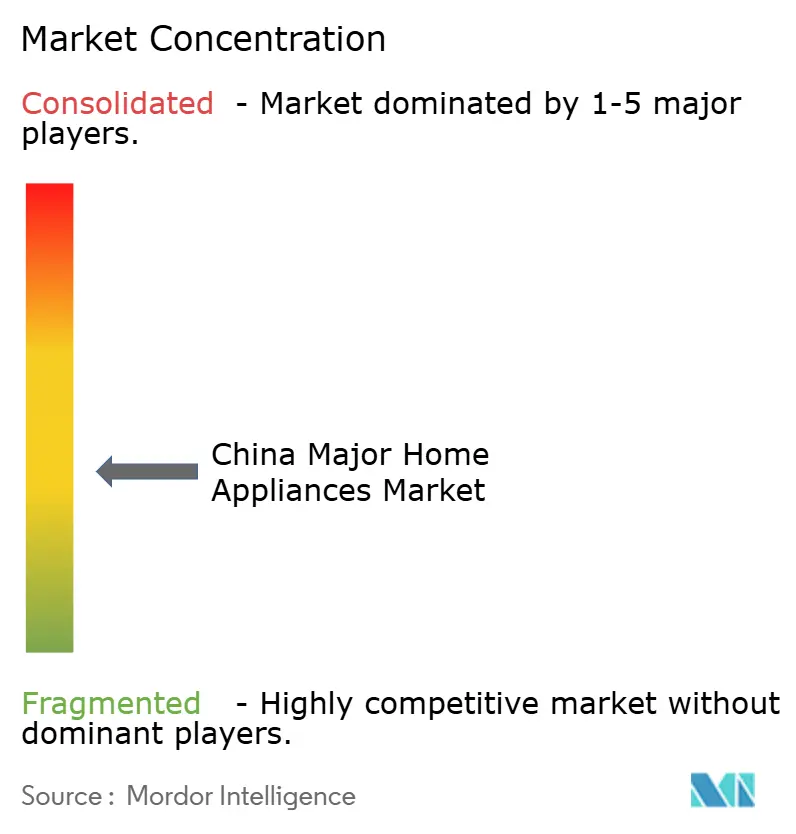

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Major Home Appliances Market Analysis by Mordor Intelligence

China major home appliances market size in 2026 is estimated at USD 87.55 billion, growing from 2025 value of USD 84.55 billion with 2031 projections showing USD 104.23 billion, growing at 3.55% CAGR over 2026-2031. Rising middle-class spending power, policy-led replacement schemes, and rapid uptake of smart living solutions sustain demand even as the industry enters a mature phase. Government trade-in incentives introduced in 2024 lifted refrigerator retail volume by 5.4% and value by 8.5%, signaling the immediate impact of consumption subsidies[1]China Household Electrical Appliances Association, “Trade-in Policies Boost Refrigerator Sales,” cheaa.org. Domestic manufacturers now dominate sales, helped by extensive local distribution networks and cost advantages, while international brands defend niche premium positions. Online channels remain an engine of structural change because digital discovery, price transparency, and livestream sales keep shifting consumer journeys away from legacy retail formats. At the same time, raw-material inflation and decarbonisation investments compress margins, forcing producers to automate plants, redesign supply chains, and move up the value curve through AI-enabled features and ecosystem services.

Key Report Takeaways

- By product category, refrigerators led with 27.50% revenue share of the China major home appliances market in 2025; dishwashers are projected to deliver the fastest 4.05% CAGR to 2031.

- By region, East China accounted for a 33.10% share of the China major home appliances market in 2025, while South Central China is forecast to expand at a 3.7% CAGR through 2031.

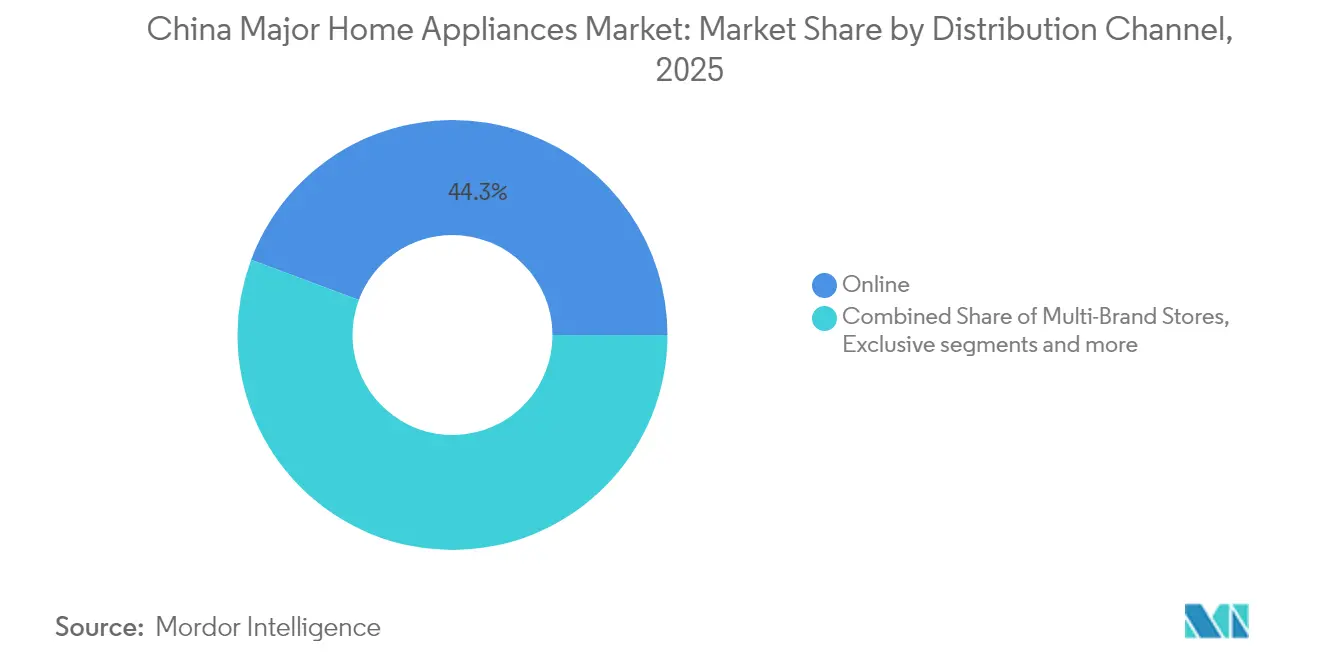

- By distribution channel, online platforms captured 44.30% of the China major home appliances market share in 2025 and are advancing at a 4.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Major Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable income & urbanization | +0.8% | National, stronger in Tier-2 & 3 cities | Medium term (2-4 years) |

| Rapid adoption of smart/IoT-enabled appliances | +1.2% | East China & major urban centres, expanding to lower tiers | Long term (≥ 4 years) |

| Government incentives for green appliances | +0.6% | National, focus in developed regions | Short term (≤ 2 years) |

| Rising housing completions & renovations | +0.4% | East China, South Central China, metro areas | Medium term (2-4 years) |

| Strong e-commerce & omnichannel distribution | +0.7% | National, higher penetration in urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income and Urbanization

Per-capita disposable income climbed to CNY 41,314 (USD 5,700) in 2024, up 5.3% year on year, with rural growth outpacing urban for a second consecutive year. That convergence opens fresh pools of first-time buyers in lower-tier cities where appliance ownership trails metropolitan averages. Manufacturers respond by widening distribution footprints and tailoring entry-level smart models to local spending thresholds. Rising housing completions in emerging metropolitan clusters further stimulate purchases as new homeowners prioritize durable goods, especially air conditioners and refrigerators. The combination of income growth and accelerated urban migration, therefore, underpins structural demand across the China major home appliances market.

Rapid Adoption of Smart and IoT-Enabled Appliances

Smart functionality has shifted from novelty to a core purchase criterion. Haier’s U+ Smart Life Platform connects refrigerators, washers, ovens, and air conditioners into scene-based routines and has recorded more than 20 million active users by 2023, with most adopters in Gen Z and millennial urban households [2]Haier Smart Home, “Haier Maintains Global Major-Appliance Leadership,” haiersmarthome.com. Generative AI now powers predictive maintenance, adaptive temperature zones, and personalised usage analytics that widen value beyond basic connectivity. Younger consumers view intelligent appliances as lifestyle infrastructure, which justifies premium pricing and raises average selling prices across categories. The AWE 2025 fair showcased over 1,000 brands focused on AI living concepts, proving industry-wide commitment to embedded intelligence. As software ecosystems mature, recurring service revenues will complement hardware margins and differentiate market leaders.

Government Incentives for Green Appliances

A national trade-in scheme launched in 2024 subsidises the replacement of energy-intensive refrigerators and air conditioners, stimulating immediate sales while accelerating the retirement of legacy stock. The initiative helped lift refrigerator volume despite macro headwinds, illustrating how policy can override cyclical softness. Meanwhile, new safety and efficiency standards effective in 2026 compel firms to redesign product lines using low-GWP refrigerants and advanced insulation. Compliance expenditure pressures cash flow but also weeds out sub-scale competitors, consolidating share among technology leaders with established R&D pipelines.

Strong E-Commerce and Omnichannel Distribution

Digital retail captured 45% of the China major home appliances market in 2024, cementing the channel as the dominant route to market [3]Fujian Provincial Department of Commerce, “E-Commerce Penetration in Home Appliances,” fujian.gov.cn. Livestream demonstrations, user-generated reviews, and instant couponing compress decision cycles and drive higher conversion versus store-only journeys. Traditional retailers respond by integrating online order fulfilment, click-and-collect, and AR showrooms that replicate product interaction. Manufacturers adopt platform-specific bundles and limited-time launches to harness traffic peaks such as Singles’ Day, while flagship brand outlets pivot to service-experience hubs for installation, repair, and smart-home tutorials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material & component cost fluctuation | –0.9% | National, high impact on manufacturing hubs | Short term (≤ 2 years) |

| Urban Tier-1/2 market saturation causing price wars | –0.7% | East China & top metro areas | Medium term (2-4 years) |

| Supply-chain decarbonization cost inflation | –0.4% | National, export-oriented factories | Long term (≥ 4 years) |

| Intensified price competition & margin pressure | –0.6% | National, all segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material and Component Cost Fluctuation

Copper and aluminium price swings inflated production outlays during 2024, with Hisense flagging a material hit to margin due to metal cost spikes [4]Ebrun, “Hisense Faces Raw Material Cost Surge,” ebrun.com . Concurrent US tariffs on Chinese refrigerators, dishwashers, and related components amplify volatility for export-oriented firms. In June 2025, the US raised most tariffs on imported steel and aluminum to 50%, aiming to limit China’s expanding influence in global trade. Manufacturers hedge risk through multi-region sourcing, forward contracts, and accelerated automation to trim labour content. Nonetheless, recurrent cost pass-through remains challenging in price-sensitive domestic tiers, dampening profit elasticity across the Chinese major home appliances market.

Urban Tier-1 & 2 Market Saturation Causing Price Wars

In mature metropolitan areas, replacement cycles lengthen and brand substitution intensifies, triggering promotional battles that erode unit profitability. Domestic air-conditioner shipments slipped 1.5% in 2024 even as nationwide exports grew, confirming diminishing incremental demand in saturated enclaves. Precision marketing and differentiated smart features partly offset discount pressure, yet the fundamental slack in first-install demand continues to compress operating leverage. Firms, therefore, redirect growth strategies to lower-tier cities, cross-border expansion, and premium niches to stabilise earnings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Refrigerators Lead, Dishwashers Accelerate

Refrigerators retained a commanding 27.50% share of the China major home appliances market in 2025 owing to essential-use status, higher average ticket, and continuous energy-efficiency upgrades. Large-capacity multi-door models with AI freshness management and embedded cameras extend replacement rationale among affluent households. Manufacturers advertise nutrient-preserving zones, automated defrost cycles, and eco-friendly refrigerants to differentiate premium lines. Meanwhile, the segment benefits from government subsidies tied to energy ratings, which shorten payback periods for upgrades. Enhanced insulation materials and inverter compressors also reduce lifetime operating cost, adding to value perception.

Dishwashers record the fastest 4.05% CAGR through 2031 as societal norms around kitchen hygiene evolve. Penetration remains below 10% nationally, leaving significant headroom compared with developed economies. Rising single-patient and dual-income households in urban cores translate to limited time for manual dishwashing, elevating demand for compact built-ins and countertop models. The China major home appliances market size for dishwashers is expected to expand steadily as manufacturers localise spray-arm designs, mould-resistant interiors, and low-noise motors for apartment living. The Siemens Intelligent Clean Cube launch underlines ongoing innovation in water-efficiency and targeted grease removal, which strengthens consumer confidence in adoption. Export-oriented producers also favour the segment because dishwasher demand remains less cyclical than discretionary kitchen electronics internationally. Washing machines and air conditioners show flatter volume trajectories, but shift to heat-pump dryers and variable-frequency compressors supports margin protection. Ovens, steamers, and combination cookers benefit from the growing middle-class cooking culture and home-baking popularity ignited during pandemic restrictions. Freezers ride export momentum, particularly to Southeast Asian and African markets where cold-chain infrastructure upgrades increase commercial orders. Overall, a gradual mix move toward smart, integrated, and aesthetically aligned appliances elevates average selling price and cushions volume maturity pressures in legacy categories.

By Distribution Channel: Online Dominance Reshapes Retail

Online platforms accounted for 44.30% of China major home appliances market sales in 2025 and will outpace all offline formats at a 4.75% CAGR through 2031. Heavy traffic promotions and social-commerce livestreams compress awareness and conversion into a single session, boosting impulse upgrades. Gigabyte-level broadband plus 5G rollout enhance product video quality, allowing shoppers to assess interior components and installation requirements virtually. Algorithmic recommendation engines amplify cross-sell rates by bundling appliances with compatible smart-home devices.

Omnichannel remains critical because many large appliances still require tactile evaluation and post-sale services. Retailers transform showrooms into experience centres where customers schedule VR demonstrations, confirm cabinet cut-outs, and arrange same-day installation. The China major home appliances market size for offline exclusive brand outlets is stabilising as these stores shift from revenue hubs to service nodes that secure lifetime customer value. Hypermarkets and multi-brand electronics chains rationalise footprints but invest in rapid-delivery micro-warehouses to defend convenience advantages. Ultimately, success relies on seamless stock visibility, unified pricing, and integrated loyalty programmes that allow consumers to navigate effortlessly across digital and physical touchpoints.

Geography Analysis

East China led the China major home appliances market with a 33.10% revenue share in 2025, due to higher disposable incomes, tech-savvy consumers, and dense retail networks. The area’s manufacturing clusters in Guangdong, Zhejiang, and Jiangsu cut logistics costs and speed product launches, while local authorities offer rebates for low-carbon production upgrades. Premium refrigerator and washing-machine lines record above-average uptake here because shoppers value convenience, smart connectivity, and status signaling. Importantly, corporate fleet replacement programmes for rental apartments and furnished offices reinforce base demand outside household channels.

South Central China is projected to register the fastest 3.7% CAGR from 2026 to 2031. Urbanisation in Wuhan, Changsha, and Zhengzhou pulls rural households into mid-income brackets, adding millions of first-time buyers. Housing starts in these cities incorporate modern kitchen and laundry layouts that require built-in appliances, therefore boosting dishwasher and oven penetration. Rising consumer credit availability also encourages bundled purchases during property handover, shortening the replacement cycle relative to wealthier regions. North China remains sizeable due to Beijing and Tianjin's purchasing power, although demand tilts toward premium smart variants rather than basic equipment. Southwestern provinces benefit from tourism-led economic growth that spurs hotel and rental renovation projects, supporting institutional procurement of refrigerators, washing machines, and commercial freezers. Northeast China faces slower wage growth and population decline, so manufacturers focus on value positioning and extended-warranty offers. Northwestern regions offer long-term upside as Belt and Road investments improve road and e-commerce delivery infrastructure; early market entrants cultivate loyalty through affordable smart packages geared to newly electrified rural areas. Regional diversification therefore mitigates saturation risk and underpins steady aggregate expansion for the China major home appliances market.

Competitive Landscape

Market concentration is moderately fragmented. Their integrated R&D, component manufacturing, and omnichannel distribution ecosystems produce consistent cost and speed advantages over smaller peers. Midea and Hisense announced a strategic pact in May 2025 that pools AI algorithms, robotic logistics, and overseas plant capacity to accelerate smart manufacturing scale economies.

Competition now revolves around software ecosystems that bind multiple product categories into a unified interface. Haier’s Smart Home App integrates voice control, predictive maintenance, and energy optimisation, encouraging multi-product ownership within brand boundaries. Midea’s industrial internet platform drives factory digital twins that cut defect rates and compress delivery cycles, reinforcing the firm’s price competitiveness without sacrificing margin. Gree leverages precision air-conditioning expertise to cross-sell dehumidifiers, heaters, and air purifiers, capturing indoor-climate wallet share. Foreign entrants concentrate on premium niches; Bosch-Siemens aims at high-income dishwasher adopters, while Panasonic focuses on health-oriented refrigerators with nano-water mist preservation systems.

Cost inflation accelerates automation plans across the industry. Haier’s Qingdao mega-plant runs AI-guided flexible lines that can switch between 80 SKU variations without downtime, shortening time-to-market for customized orders. Environmental mandates push all majors to adopt green factories powered by rooftop solar and recycled water, positioning sustainability as both a license to operate and a marketing asset within the Chinese major home appliances market.

China Major Home Appliances Industry Leaders

Haier Group Corporation

Midea Group

Gree Electric Appliances, Inc.

Hisense Group Co., Ltd.

TCL Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The AWE 2025 exhibition in Shanghai hosted over 1,000 global brands and launched the 2025 National Home Appliance Consumption Season.

- September 2024: BSH Home Appliances won three awards at the China Dishwasher Industry Summit for Siemens' Intelligent Clean Cube technology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China major home appliances market as factory-built large "white goods" sold for residential use, namely refrigerators, freezers, washing machines, dryers, dishwashers, ovens, ranges, air conditioners, and range hoods.

Scope exclusion: small countertop devices, handheld vacuums, personal-care gadgets, and televisions remain outside this valuation, keeping totals focused on core durable appliances.

Segmentation Overview

- By Product

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Incl. Combi & Microwave)

- Air Conditioners

- Other Major Home Appliances (range hoods, cooktops, etc.)

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- East China

- Southwestern China

- North China

- South Central China

- Northeast China

- Northwestern China

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed appliance assemblers in Guangdong, component makers in Anhui, logistics partners, and leading e-commerce retailers across Tier 1-3 cities. These conversations clarified warranty replacement rates, subsidy pass-throughs, and online channel mark-ups, filling gaps spotted in secondary data and helping us triangulate assumptions.

Desk Research

We drew on national production statistics from the National Bureau of Statistics, export-import ledgers from China Customs, and retail turnover reported by the China Household Electrical Appliances Association, which together reveal shipment flows and pricing corridors. Energy-efficiency catalogues, patent alerts from Questel, and contract postings on Volza or Tenders Info supplied model counts and benchmark bids. Company 10-Ks, investor decks, and reputable press added channel ASPs and policy context. The sources named are illustrative; many additional open datasets underpinned data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down construct converts official domestic output, import subtraction, and export addition into apparent domestic demand, which is then tested with selective bottom-up roll-ups of listed suppliers' unit sales. Key variables like real-estate completions, household formation, urban disposable income, trade-in voucher uptake, and room-air-conditioner prevalence feed a multivariate regression that projects volume and value. Scenario analysis adjusts for property-market volatility, and gaps in supplier data are bridged by sampled ASP × volume checks.

Data Validation & Update Cycle

Outputs pass variance screens against CHEAA retail sales and internal peer review before sign-off. Reports refresh each year, with interim updates triggered by policy shifts, tariff moves, or currency swings; a fresh analyst pass precedes every client delivery.

Why Mordor's China Major Home Appliances Baseline Commands Reliability

Estimates often diverge because product baskets, price bases, and refresh paces vary across publishers. Our disciplined scope, dual-lens model, and yearly recalibration create a dependable anchor for planning decisions.

The comparison shows that our transparent scope selection, balanced model logic, and tight refresh cadence deliver the most reliable baseline for executives seeking decisions rooted in numbers they can trace and replicate.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 84.55 B (2025) | Mordor Intelligence | |

| USD 131.95 B (2024) | Regional Consultancy A | Counts small appliances and applies retail invoice pricing |

| USD 50.5 B (2024) | Trade Journal B | Omits air conditioners; relies solely on branded factory shipments |

The comparison shows that our transparent scope selection, balanced model logic, and tight refresh cadence deliver the most reliable baseline for executives seeking decisions rooted in numbers they can trace and replicate.

Key Questions Answered in the Report

What is the current value of the China major home appliances market?

The market is worth USD 87.55 billion in 2026.

How fast will the China major home appliances market grow through 2031?

It is projected to expand at a 3.55% CAGR, reaching USD 104.23 billion by 2031.

Which product category leads sales in the China major home appliances market?

Refrigerators lead with a 27.50% revenue share in 2025.

Which region shows the fastest growth outlook?

South Central China is expected to register a 3.7% CAGR from 2026 to 2031.

How large is the online channel in appliance retail?

Online platforms captured 44.30% of market sales in 2025 and are growing at 4.75% CAGR.

What is the main challenge for manufacturers over the next two years?

Raw-material cost volatility, particularly in copper and aluminium, is the most immediate headwind.

Page last updated on: