Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

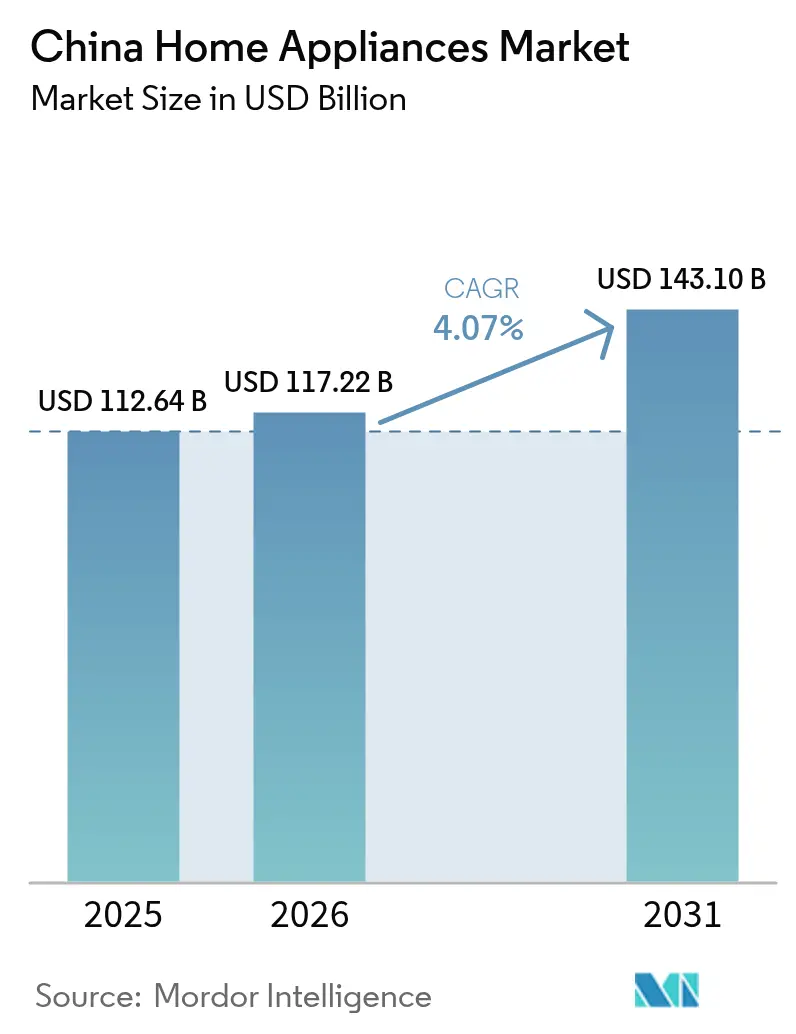

| Base Year Market Size (2025) | USD 112.64 Billion |

| Market Size (2026) | USD 117.22 Billion |

| Market Size (2031) | USD 143.1 Billion |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Home Appliances Market Analysis by Mordor Intelligence

China home appliances market size in 2026 is estimated at USD 117.22 billion, growing from 2025 value of USD 112.64 billion with 2031 projections showing USD 143.1 billion, growing at 4.07% CAGR over 2026-2031. A decisive shift from volume-led expansion to premium, value-oriented growth is underway as manufacturers integrate AI, IoT, and energy-efficiency features into both major and small appliances. Government trade-in subsidies covering 15-20% of the price for Grade 1 products and rising disposable incomes in urban centers underpin steady replacement demand. E-commerce platforms streamline subsidy applications and old-unit collection, accelerating channel migration while multi-brand stores respond with experiential showrooms and bundled installation services. Regional dynamics also shape market opportunities: East China retains leadership through its manufacturing clusters and high incomes, whereas Southwestern China delivers the fastest CAGR thanks to infrastructure spending and rapid urbanization. Competitive intensity remains moderate yet technology-focused, with leading brands embedding large language models for predictive maintenance and voice control in refrigerators, washing machines, and HVAC systems.

Key Report Takeaways

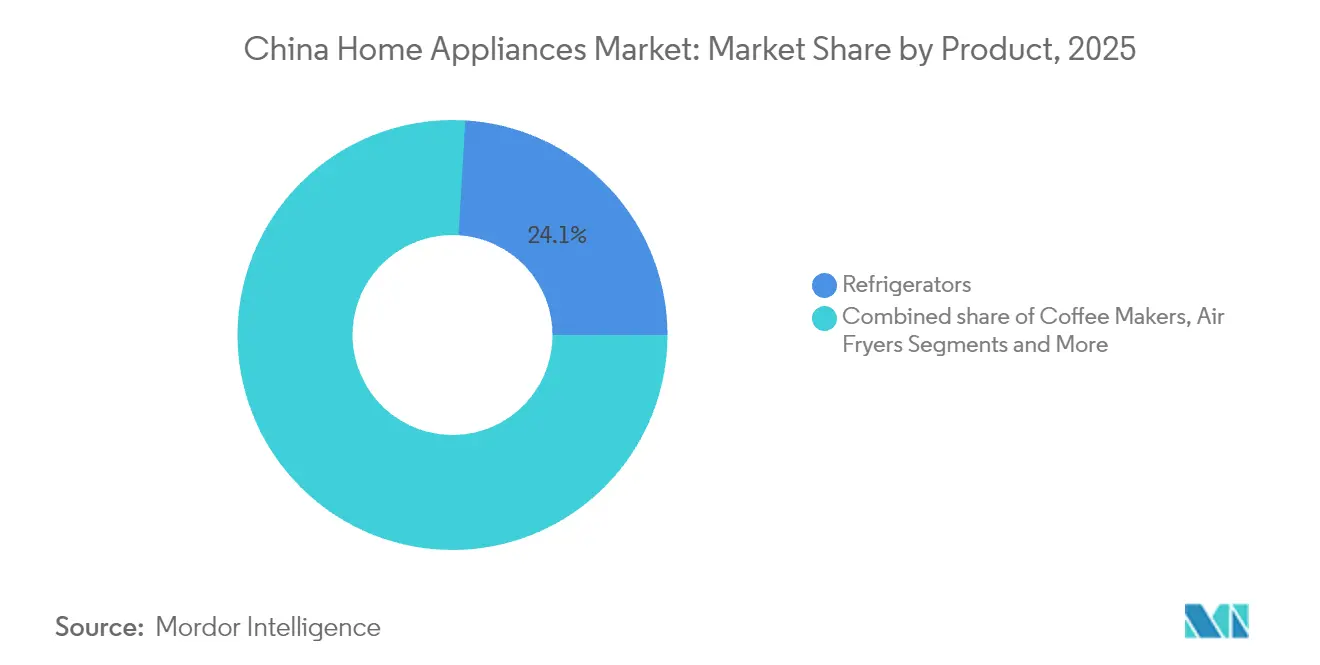

- By product type, refrigerators accounted for 24.05% of the China home appliances market share in 2025, while the China home appliances market size for air fryers is forecast to grow at the fastest CAGR of 5.23% between 2026 and 2031.

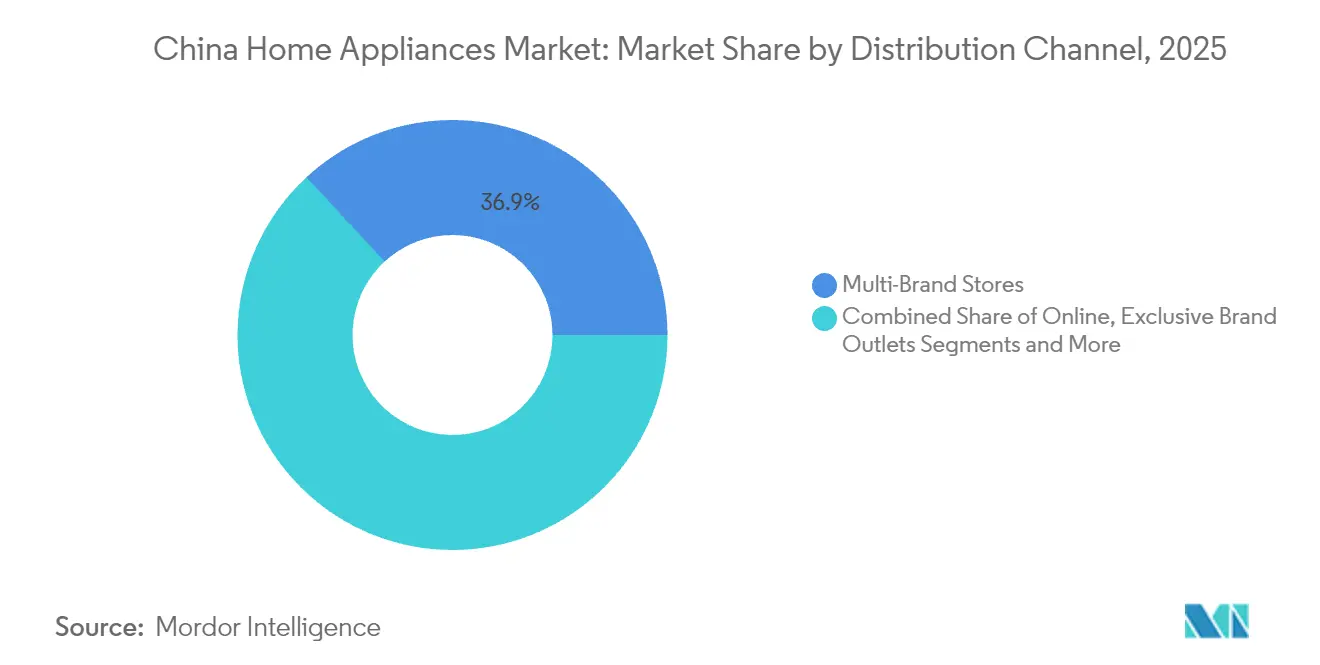

- By distribution channel, multi-brand stores captured 36.88% of the China home appliances market share in 2025, whereas the China home appliances market size for online channels is projected to expand fastest at a CAGR of 6.05% over 2026-2031.

- By geography, East China led with 31.28% of the China home appliances market share in 2025, while the China home appliances market size in Southwestern China is anticipated to grow at the highest CAGR of 4.98% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes among urban households | +1.2% | East China, North China, South Central China | Medium term (2-4 years) |

| Rapid urbanization & residential construction boom | +0.8% | Southwestern China, Northwestern China, Northeast China | Long term (≥ 4 years) |

| Demand surge for energy-efficient & smart appliances | +1.5% | Global, with early adoption in Tier-1 cities | Short term (≤ 2 years) |

| E-commerce expansion & omnichannel retailing | +0.9% | National, with strongest penetration in East China | Medium term (2-4 years) |

| Emergence of rental economy & appliance leasing | +0.3% | Tier-1 cities expanding to Tier-2 markets | Long term (≥ 4 years) |

| Rural revitalization subsidies for appliance upgrades | +0.7% | Rural regions across all provinces | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Incomes

Accelerating wage growth in major urban centers fuels an appetite for premium, smart, and energy-efficient products. Middle-class households now prioritize lifestyle enhancement over first-time purchases, boosting uptake of AI-enabled refrigerators, voice-controlled washers, and multi-function rice cookers. Brands capitalize on this willingness to pay by bundling extended warranties and predictive-maintenance subscriptions that generate recurring revenue. Higher incomes also spur demand for design-oriented small appliances such as retro-style coffee makers and countertop ovens, creating new value pools in an otherwise mature sector. In Tier-1 cities, dual-income professionals increasingly favor built-in dishwashers and centralized HVAC solutions, accelerating the upgrade cycle. Rising affluence therefore sustains growth despite market saturation in early-adopter regions. Government incentives further amplify this effect by rewarding high-efficiency purchases with instant rebates, closing the affordability gap for premium models.

Urbanization and Residential Construction

China targets a 70% urbanization rate by 2030, necessitating large-scale residential projects that act as natural demand motors for major appliances. Newly constructed apartments often include pre-installed smart home gateways, prompting developers to procure IoT-ready air conditioners, water heaters, and refrigerators in bulk. Compact urban living spaces inspire manufacturers to design slim, multi-functional units that fit standardized kitchen cabinetry, thus opening innovation opportunities. Migrants moving into Tier-2 and Tier-3 cities create incremental first-time demand for entry-level washing machines and affordable cooling units. Infrastructure expansion in Southwest and Northwest China also improves last-mile logistics, reducing distribution costs and expanding retailer footprints in previously under-served locales. As urbanization deepens, replacement cycles shorten because consumers expect appliances to match the rapidly rising smart-home baseline. The construction boom, therefore, underpins both initial sales and future upgrade momentum[1]Ministry of Housing and Urban-Rural Development, “2024 Residential Construction Data,” mohurd.gov.cn..

Demand for Energy-Efficient Smart Appliances

China’s carbon-peaking and carbon-neutrality pledges are turning energy labels from optional messaging into mandatory selling points. Grade 1 models qualify for higher subsidies and command price premiums that consumers are increasingly willing to pay. Brands incorporate inverter compressors, heat-pump drying, and label-driven eco-modes—features that translate directly into lower utility bills. Parallel advances in AI allow appliances to learn user habits, optimize cycle times, and send remote alerts before faults occur. This convergence of efficiency and intelligence elevates perceived value, prompting mid-life replacements even when existing units remain operational. Retailers leverage live-stream demos to visualize electricity savings, translating technical specs into tangible cost benefits for shoppers. Higher uptake of smart speakers and domestic 5G also eases device onboarding, making the incremental cost of connectivity more acceptable across demographics[2]Source: China Energy Conservation Association, “Appliance Energy Label White Paper,” cec.org.cn..

E-commerce Expansion and Omnichannel Retail

Online channels’ 6.22% CAGR leads all distribution modes, driven by seamless trade-in workflows, same-day delivery for small appliances, and influencer-led product discovery. Platforms integrate government subsidy verification, allowing shoppers to apply discounts at checkout and schedule old-unit collection in one click. Brands now launch flagships on Douyin and JD Live, gathering real-time feedback that feeds iterative design and demand forecasting. Multi-brand stores counter with experiential spaces where consumers test smart-home interoperability and receive on-site installation. The convergence of online research and offline fulfillment spawns a true omnichannel model where QR-code pricing, virtual reality demos, and supply-chain-wide inventory visibility merge. Hybrid shoppers often browse in-store, finalize purchases online, and redeem loyalty benefits across both ecosystems. The result is higher basket sizes and lower returns, reinforcing the profitability of digitally enabled strategies[3]Source: JD.com, “Appliance Omnichannel Trends Report 2025,” jd.com..

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense price competition squeezing margins | -0.8% | National, most severe in Tier-2 and Tier-3 cities | Short term (≤ 2 years) |

| Supply-chain disruptions & raw-material cost swings | -0.6% | Global supply chains affecting all regions | Medium term (2-4 years) |

| Stricter e-waste regulations raising compliance costs | -0.4% | National, with pilot programs in major cities | Long term (≥ 4 years) |

| Market saturation in Tier-1 cities | -0.5% | Beijing, Shanghai, Guangzhou, Shenzhen | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense Price Competition Squeezing Margins

The commoditization of core white-goods technologies keeps ASP growth muted despite rising feature counts. Domestic mid-tier brands often sacrifice gross margin to hold shelf space in hypermarkets and rural franchise stores. Flash sales and “618/Double-11” megasales create consumer expectations for deep discounts, pulling forward demand but eroding profitability. Export pressures compound the situation as global buyers push for FOB reductions amid exchange-rate fluctuations. To mitigate, leading firms invest in vertically integrated component production, lowering unit costs while protecting IP. Smaller manufacturers without scale advantages risk exit or consolidation, nudging overall market concentration upward. Service-led differentiation, such as IoT-driven diagnostics and subscription consumables, emerges as a buffer against pure price wars.

Supply-Chain Volatility and Raw-Material Cost Swings

Aluminum, copper, and steel account for more than half of bill-of-materials costs in refrigerators, AC compressors, and washing-machine drums. Pandemic-era logistical disruptions highlighted vulnerabilities in single-source strategies, prompting firms to dual-source critical inputs and stock higher safety buffers. Commodity price spikes compress margins or force retail pass-throughs that dampen demand elasticity. Geopolitical shifts encourage regional manufacturing in Southeast Asia and Latin America, but nearshoring adds capex burdens and management complexity. Container shortages and port congestion elevate lead times, complicating just-in-time production models. Domestic freight cost inflation, driven by fuel variability, further pressures the bottom line. Predictive analytics and blockchain-enabled traceability gain traction as risk-mitigation tools, yet require significant digital-capability investments[4]Source: Yicai Global, “China’s home appliances go overseas under the reconstruction of globalization,” yicaiglobal.com..

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Refrigerators Remain Core While Air Fryers Propel Small-Appliance Momentum

Refrigerators commanded 24.05% of the China home appliances market share in 2025, reflecting their essential role in daily living and higher average selling prices. Manufacturers refreshed portfolios with four-door, zero-degree preservation zones and inverter-driven cooling, contributing to sustained replacement demand. The China home appliances market size for refrigerators also benefits from growing preference for larger 500-liter models that meet family lifestyle changes. In parallel, small-appliance innovation cycles accelerate: air fryers post a 5.23% CAGR, buoyed by health-conscious cooking trends and social-media recipe virality. Brands differentiate through dual-zone heating and AI-guided temperature profiles, which justify incremental premiums despite stiff competition. Coffee makers, juicers, and countertop ovens piggyback on this momentum, leveraging influencer-led marketing to drive impulse purchases. Collectively, cross-category bundling helps retailers raise basket sizes, while extended warranties and recipe-subscription services diversify revenue streams.

Second-generation smart products integrate large language models that learn user habits, automatically reorder water filters, and provide app-based energy-optimization tips. Refrigerators now offer touchscreen family hubs that sync shopping lists with e-commerce grocery portals, further embedding the appliance into daily digital routines. Multi-door formats enhance spatial segmentation, enabling precise humidity zones for produce and meat. In washing machines, heat-pump dryers gain favor for their 60% energy savings versus vented units, and AI-based fabric recognition optimizes detergent dosing. This constant innovation sustains high-value replacements even in saturated urban markets. Meanwhile rural revitalization projects distribute entry-level cooling and laundry units, enlarging the total addressable base.

By Distribution Channel: Multi-Brand Stores Adapt to Online Acceleration

Multi-brand stores controlled 36.88% of the China home appliances market in 2025 because shoppers favor side-by-side comparisons and instant installation scheduling. These outlets now augment sales floors with AR-powered product visualizers that demonstrate color variations and kitchen fit. However, the online channel’s 6.05% CAGR underscores a decisive shift in consumer purchase journeys, research, price comparison, and checkout frequently occur on mobile apps. The China home appliances market size allocated to online platforms rises steadily as voucher stacking, live-stream flash sales, and one-hour delivery for small appliances become industry norms. Retailers embrace click-and-collect models, turning physical stores into micro-fulfillment hubs that optimize last-mile costs.

Exclusive brand stores invest in immersive smart-home showrooms where visitors orchestrate lighting, HVAC, and appliance scenes via a single console. This experiential focus helps brands articulate value beyond technical specifications, fostering emotional connections that reduce price sensitivity. Omnichannel data integration gives manufacturers visibility into inventory, allowing real-time price parity across touchpoints. For rural areas, franchise-led stores combined with app-based order management bring branded experiences closer to township consumers. Online penetration levels plateau in high-ticket items where installation complexity and post-sale service matter, reinforcing the complementary nature of physical interaction. Ultimately, channel strategies converge: QR-tagged appliances enable in-aisle mobile checkout, and post-purchase apps schedule technician visits, creating a seamless ecosystem that maximizes customer lifetime value.

Geography Analysis

East China contributed 31.28% to the China home appliances market size in 2025, leveraging manufacturing clusters in Jiangsu, Zhejiang, and Shanghai that compress lead times and support rapid product iterations. High disposable incomes elevate average selling prices, while early smart-home adoption offers fertile ground for AI-embedded refrigerators and predictive-maintenance air conditioners. Provincial subsidy programs amplify this propensity to upgrade, leading to shorter replacement cycles relative to national averages. Coastal logistics infrastructure further empowers East-China-based exporters, reinforcing the region’s strategic relevance. Meanwhile, industrial-internet pilots accelerate factory digitalization, enhancing quality control and lowering unit costs. Ecosystem synergies among component suppliers, OEMs, and design houses foster innovation spillovers, reinforcing the region’s competitive lead.

Southwestern China is projected to register the fastest regional expansion at a 4.98% CAGR to 2031, propelled by urbanization in Chengdu, Chongqing, and Kunming. Infrastructure upgrades—including high-speed rail networks and logistics parks—improve appliance distribution economics, narrowing the cost gap with coastal regions. Rising middle-class households prioritize energy-efficient air conditioners to counter humid subtropical climates, spurring first-time purchases and qualitative upgrades alike. Government-backed rural revitalization programs subsidize entry-level refrigerators and washers, enlarging the addressable market. Manufacturers increasingly site assembly plants in Sichuan to capitalize on lower labor costs and proximity to inland demand.

North China and South-Central China contribute steady growth by virtue of established urban hubs like Beijing, Tianjin, Wuhan, and Changsha. New housing completions stimulate built-in appliance demand, notably dishwashers and range hoods compliant with stricter indoor-air-quality standards. The China home appliances market share in these regions benefits from provincial energy-saving campaigns that promote inverter compressors and heat-pump dryers. Conversely, Northeast China grapples with population decline, tempering long-run potential despite short-term boosts from winter heating subsidies. Northwestern China presents emerging opportunities as Belt-and-Road infrastructure enhances connectivity, reducing historical distribution bottlenecks. Climate diversity across Xinjiang and Gansu also broadens product-mix requirements, prompting brands to offer wide-temperature-range freezers.

Regulatory Landscape

China's policy mix continues to steer demand toward safer, more efficient, and more interoperable appliances, with compliance increasingly linked to consumer incentive eligibility. A nationwide trade-in subsidy program commenced in January 2026 for six core categories (refrigerators, washing machines, televisions, air conditioners, water heaters, and computers), offering a 15% price subsidy capped at RMB 1,500 per item. This design effectively prioritizes higher-efficiency replacement purchases.

Regulators are also tightening product governance on labeling and safety. NDRC and SAMR issued the Energy Efficiency Labeling Catalogue (2026 Edition) in April 2026, and updated labeling rules began implementation for refrigerators in June 2026 with a two-year transition for legacy inventory. CNCA published GB/T 4706.1-2024 in July 2024, with mandatory implementation under CCC from August 1, 2026, which raises recertification and testing needs across household electrical appliances. Smart-home interoperability is moving toward mandatory national standards under MIIT-led drafting, referenced in March 2026 reporting.

Value Chain Analysis

The value chain runs from upstream metals and chemicals (steel, copper, plastics) into core components such as compressors, motors, sensors, and smart controllers, before finished-goods assembly across major and small appliances. Downstream, the chain extends to distribution, installation, after-sales service, and recycling. East China manufacturing clusters help create dense supplier networks and shorten iteration cycles, while omnichannel retailing, combining online platforms with multi-brand stores, increasingly bundles delivery, installation, and trade-in collection into the purchase journey.

Digitization and resilience initiatives are changing how manufacturers manage sourcing and fulfillment. A domestic standard for digital supply chain construction and management (T/CASME 1555-2024, effective July 12, 2024) formalizes practices such as risk prediction and disposal, which supports scale in lower-tier markets. Leading players are also building local-for-local production footprints to hedge trade and logistics risks, including Hisense's Intelligent Manufacturing Park in Thailand, which began construction in September 2025 with phase 1 scheduled for mid-2026. Haier's 2026 priorities emphasize faster rollout of AI-embedded appliances and integrated platform approaches that connect air conditioning, water solutions, and smart building capabilities.

Competitive Landscape

The China home appliances market is moderately consolidated, with the top five companies accounting for a significant portion of total revenue. Haier Smart Home is the market leader, having integrated its “Smart Home Brain” ecosystem across refrigerators, washers, and HVAC units. Midea Group is the second-largest player, capitalizing on AIoT platforms and expanding its manufacturing presence globally. Gree Electric ranks third, emphasizing variable-frequency compressors and whole-house energy-management systems. Hisense and TCL round out the top tier, each investing in large language models for context-aware voice interfaces. Strategic partnerships proliferate: Midea and Electrolux formed a premium brand joint venture in Guangdong to capture high-end consumers, while Haier collaborates with Tencent Cloud on edge-AI chips for real-time diagnostics.

Technology differentiation now eclipses traditional scale advantages. Leading brands pilot self-healing coatings, lidar-based object detection for robotic vacuums, and bio-enzyme deodorization in refrigerators. Vertical integration remains pivotal; Gree produces its own power electronics to circumvent chip shortages and safeguard intellectual property. Mid-tier brands pursue niche leadership Joyoung specializes in soy-milk makers, Supor targets pressure-cooker aficionados using direct-to-consumer channels to maintain relevance. International entrants such as Whirlpool and Panasonic position themselves in premium smart-kitchen bundles, often leveraging local contract manufacturing to achieve cost parity. Competitive pressure intensifies during festival seasons, yet the margin impact varies: scale leaders absorb price cuts, while smaller firms rely on differentiated features and social-commerce communities to defend niches.

AI adoption inside factories also becomes a competitive lever. Sichuan Changhong plans 66 AI-enabled plants where machine-vision algorithms flag defects in real-time, reducing rework costs and accelerating time-to-market. Midea deploys digital twins to simulate HVAC performance, trimming R&D cycles and enhancing energy-efficiency rankings. Such investments raise entry barriers, potentially lifting market concentration over the forecast horizon. Nonetheless, rapid consumer-taste evolution ensures space for agile upstarts that pivot quickly on emerging trends like multifunctional air fryers or countertop dishwashers. Overall, success hinges on harmonizing hardware excellence, AI-driven experience, and an omnichannel service model that meets the escalating expectations of Chinese consumers.

China Home Appliances Industry Leaders

Haier Smart Home

Midea Group

Gree Electric

Hisense Home Appliances

TCL Technology

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Trade-in subsidies and standards upgrades create room for premiumization focused on energy efficiency, water efficiency, and smart connectivity. By April 11, 2026, cumulative sales under the national trade-in program reached about 100.35 million units, indicating an active replacement pipeline that favors Grade 1 products and accelerates the shift toward inverter-based, heat-pump, and AI-enabled models. With MOFCOM-led program caps in place, including up to RMB 1,500 per household appliance item under the 2026 scheme, brands and retailers can build higher-value bundles around installation, extended warranties, and connected maintenance. This also depends on whether platforms can handle subsidy verification and old-unit collection end-to-end.

Interoperability standardization is creating cross-brand options across major appliances, kitchen products, and smart-home controllers. CHEAA's 2024-2035 technology roadmap prioritizes AI integration, green low-carbon technology, and full-lifecycle reliability, while national standards GB/T 46456.1-2025 and GB/T 46505.1-2025 took effect in February and May 2026 to formalize smart-home architecture and appliance application scenarios. As MIIT advances drafts for mandatory smart-home interconnection standards, reported in March 2026, manufacturers that previously relied on closed ecosystems can differentiate through compliant, multi-brand connectivity. Channel partners can also monetize interoperability through packaged smart-home deployments in new housing and retrofit installations.

Recent Industry Developments

- July 2026: Midea Group opened a new portable air conditioner production line on July 7, doubling daily capacity to 6,000 units to address overseas demand. The change strengthens supply responsiveness for cooling appliances and supports faster allocation of output between export surges and domestic peak-season needs.

- May 2026: Samsung publicly confirmed its exit from China's home appliance market to concentrate on other businesses including semiconductors and mobile. This reduces foreign brand intensity in several appliance categories and creates incremental shelf-space and channel opportunity for domestic leaders and fast-scaling local ecosystems.

- March 2025: Seven provinces and cities including Zhejiang, Hainan, Fujian, Shanghai, Shaanxi, Hunan, and Suzhou expanded subsidy coverage beyond core appliances into kitchen products and smart home, offering rebates up to 20% with per-household caps reaching RMB 30,000. The broader scope increased the addressable replacement basket and pushed retailers to operationalize bundled delivery, installation, and old-unit collection for more categories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of home appliances sold in China, covering major and small household appliances purchased for residential use through offline and online channels.

Scope exclusions: It excludes commercial or industrial equipment, spare parts sold standalone, and non-appliance consumer electronics unless bundled as part of an appliance sale.

Segmentation Overview

- By Product

- Major Home Appliances

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Incl. Combi & Microwave)

- Air Conditioners

- Other Major Home Appliances

- Small Home Appliances

- Coffee Makers

- Food Processors

- Grills & Roasters

- Electric Kettles

- Juicers & Blenders

- Air Fryers

- Vacuum Cleaners

- Electric Rice Cookers

- Toasters

- Countertop Ovens

- Other Small Home Appliances

- Major Home Appliances

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- East China

- Southwestern China

- North China

- South Central China

- Northeast China

- Northwestern China

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the fact base for demand drivers, shipment direction, and price movement patterns for home appliances in China. We reviewed public statistical releases and policy notes that influence replacement cycles and discretionary spending, then linked those signals to category-level growth direction.

Sources included public data from the National Bureau of Statistics of China, Ministry of Commerce updates on consumption support, and China Customs trade statistics for relevant HS codes. We also reviewed industry association publications such as CHEAA, and peer-reviewed journals that cover energy efficiency and smart appliance adoption. To capture shifts in product mix and margin indicators, we used company annual reports and investor presentations, alongside trusted press and retail-channel commentary. Where needed, we referenced paid subscriptions for company financials and news screening, shipment-level import and export checks, and patent databases to track how quickly smart features are entering mass products. These examples are not exhaustive, and additional sources were reviewed for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work was used to validate what we learned from public sources and to fill gaps where published numbers are not consistent by category or channel. We spoke with a mix of manufacturers, distributors, retailers, and service ecosystem participants, and the interviews also clarified regional demand differences across China and the pace of smart and energy-efficient upgrades.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | |

| Mid tier: 54% | Functional/Unit leaders: 32% | |

| Smaller Players: 18% | Managers: 56% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where category demand pools were reconstructed from household formation and replacement behavior, plus macro indicators that influence discretionary appliance purchases. The totals were then checked with selective bottom-up approximations, such as sampled price times volume builds by category and channel, and channel checks on online versus offline mix, so the overall value stayed realistic.

Key model inputs included urbanization and household formation trends, disposable income and consumer confidence direction, penetration of key appliance types by household, replacement cycle timing for large appliances, smart appliance adoption (connected features), and observed price and discounting patterns by channel. Where public data did not provide clean splits, we used primary feedback to set ranges and then applied conservative midpoint assumptions, followed by sensitivity checks.

For forecasting, scenario analysis was used around replacement-led demand and policy-driven upgrades, and the yearly series was smoothed using simple time-series techniques so short-term noise did not dominate the trend. Assumptions on pricing were handled through category-level average selling price logic, with adjustments for premiumization and energy-efficiency mix rather than a single inflation factor across all products.

Data Validation & Update Cycle

Validation was done by triangulating the model totals against independent signals such as retail momentum indicators, trade movement for relevant product groups, and company commentary on volumes and pricing. Outliers were reviewed at category and channel level, and when the variance looked structural, assumptions were re-tested through follow-up calls.

A multi-step internal review is followed before sign-off so arithmetic links, currency treatment, and growth drivers stay consistent across the time series. Reports are refreshed annually, and interim updates are triggered when material events occur, such as new trade-in programs, tariff changes, or sharp commodity and FX swings. Before delivery, we do a final update pass to ensure the latest public releases are reflected.

Mordor Intelligence's China Home Appliances Market Market Size Compared Against Other Published Estimates

Published market values for China home appliances often do not match because the boundaries are not consistent, and timing choices also differ. The year used for currency conversion, the way average selling prices move in the forecast, and how online discounting is treated can all shift the final USD figure.

In this study, year-by-year FX timing and category-level ASP progression are refreshed when new retail and policy signals show a change in mix, and the checks are rerun before the estimate is finalized, which is a refresh-led reason behind the number reported by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 112.64 B (2025) | |

| Global Consultancy A | USD 131.95 B (2024) | Uses a different base year and may treat revenue recognition and channel pricing differently, which can raise the USD total when online discounting and mix shifts are not normalized consistently across categories. |

| Industry Association B | USD 271.00 B (2024) | This figure is derived from an industry revenue headline reported in CNY, and when converted to USD it can capture a broader industry boundary and a single-period FX rate effect rather than category and channel level market sales logic. |

The spread in published numbers is mainly explained by scope boundary and conversion timing, followed by how pricing and mix are carried through the forecast years. By keeping inputs tied to clear demand signals and by rechecking pricing and FX assumptions at each update, our approach stays easier to trace and repeat when new data arrives.

Key Questions Answered in the Report

How fast is smart-appliance adoption growing in China?

Smart, AI-enabled products are expanding faster than the 4.07% overall CAGR, driven by government subsidies and rising urban incomes.

Which product category holds the largest value share?

Refrigerators remain the highest-value segment with 24.05% of revenue in 2025.

Why is Southwestern China the fastest-growing region?

Government infrastructure projects and rapid urbanization give Southwestern China a projected 4.98% CAGR to 2031.

How are e-commerce platforms changing appliance sales?

Online channels integrate trade-in subsidies and one-hour delivery, driving a 6.05% CAGR and reshaping consumer purchase journeys.

What challenges threaten manufacturer profitability?

Intense price competition and raw-material cost volatility squeeze margins, especially for mid-tier brands.

Page last updated on: