Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 28.40 Billion |

| Market Size (2026) | USD 30.02 Billion |

| Market Size (2031) | USD 37.51 Billion |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

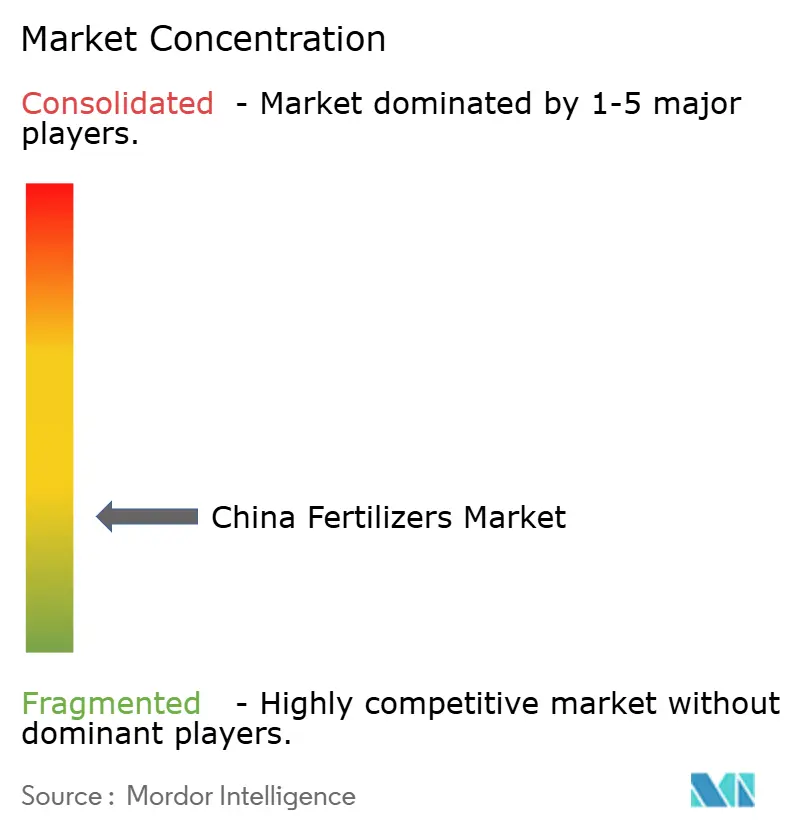

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Fertilizers Market Analysis by Mordor Intelligence

The China fertilizer market size is projected to grow from USD 28.40 billion in 2025 to USD 30.02 billion in 2026 and is forecast to reach USD 37.51 billion by 2031 at 4.56% CAGR over 2026-2031. Growth pivots on policy‐linked subsidies that reward balanced nutrient use, rising pressure to protect food security, and rapid uptake of digital tools that translate soil data into precise dosing plans. Expansion of protected cultivation acreage and a shift toward water-soluble, controlled-release, and slow-release grades strengthen value over volume, while early investment in green ammonia gives domestic producers a future cost advantage as carbon pricing spreads. Regional disparities color demand, mechanized grain belts in the Northeast favor bulk straight fertilizers, whereas the South Central and Southwest focus on premium products for high-value fruits and vegetables. The export policy has tightened phosphate outflows while spurring an eight-fold jump in NP and NPS exports, reshaping global trade and steering manufacturers toward value-added blends that command a premium.

Key Report Takeaways

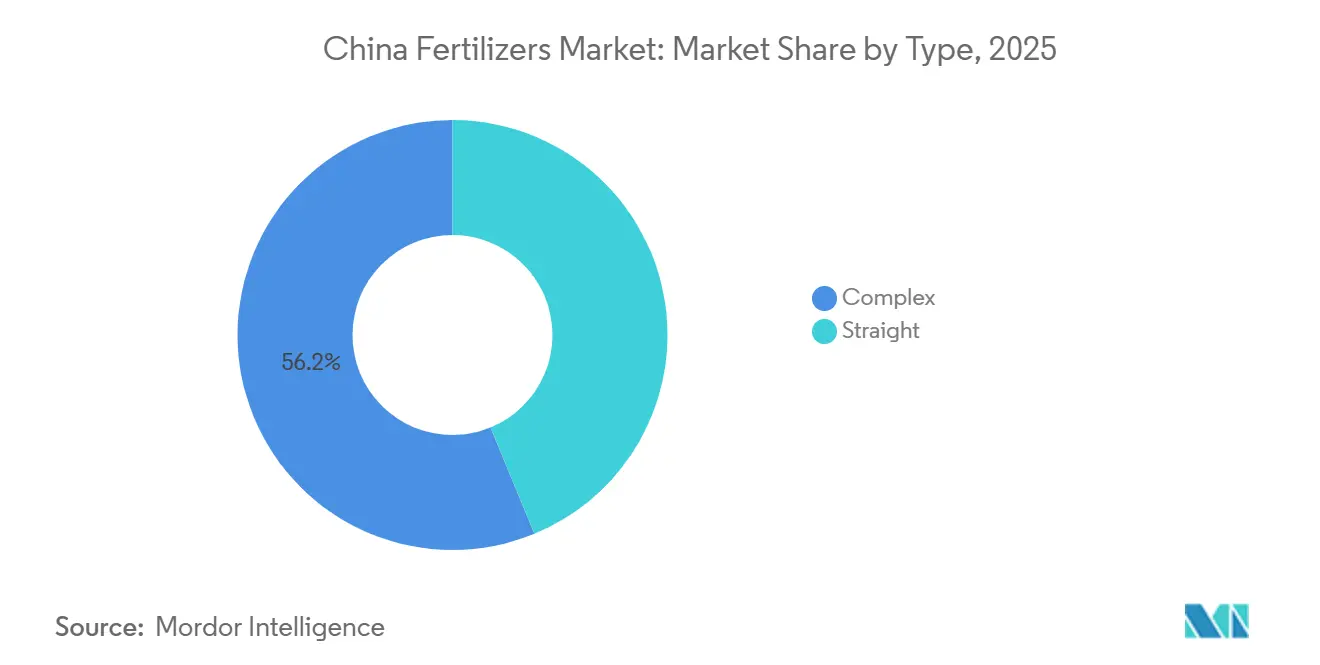

- By type, complex fertilizers held 56.2% of the China fertilizer market share in 2025 and are projected to register the fastest 6.0% CAGR through 2031.

- By form, conventional products captured 74.0% of the China fertilizer market size in 2025, while specialty fertilizers are forecast to expand at the fastest 6.1% CAGR through 2031.

- By application mode, soil led with a 74.3% share in 2025, and fertigation is set to be the fastest growing application method over the forecast period at a 6.2% CAGR through 2031.

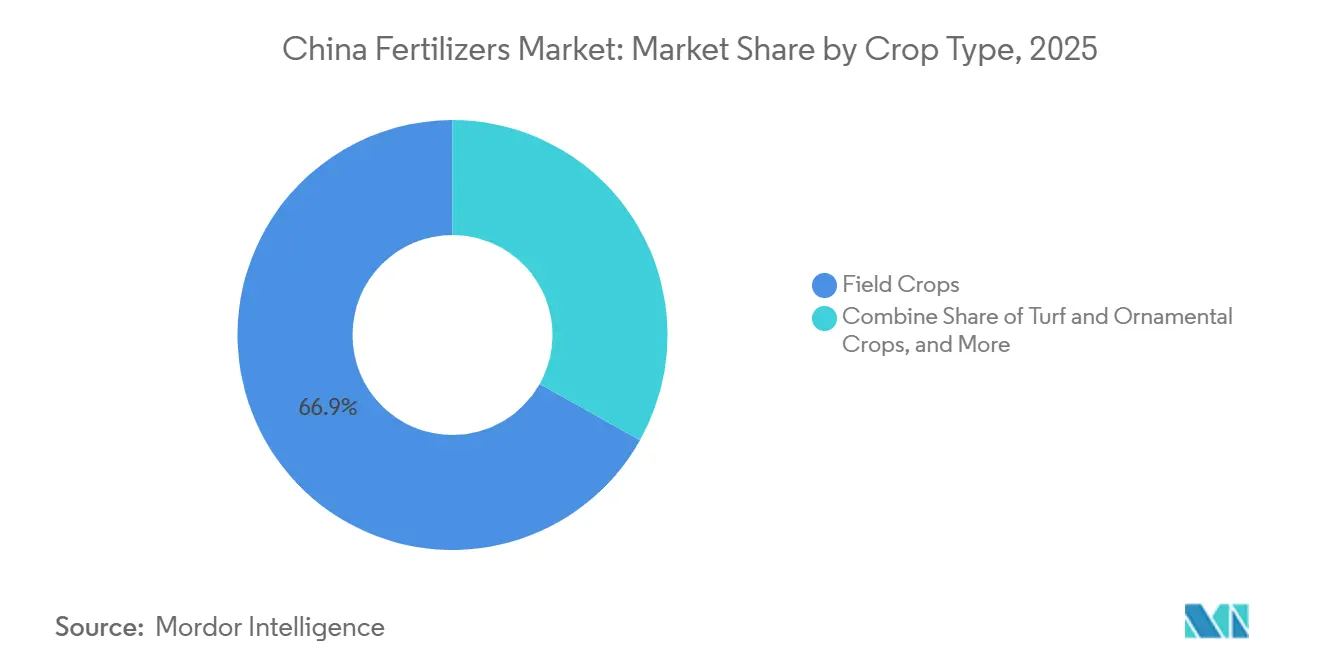

- By crop type, field crops accounted for 66.9% of demand in 2025, while horticultural crops are positioned for the fastest 7.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Fertilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government fertilizer‐use subsidy schemes | +1.2% | National, higher in major grain provinces | Medium term (2-4 years) |

| Chronic pressure to raise crop yields and quality | +0.9% | National, strongest in food-deficient regions | Long term (≥ 4 years) |

| Surge in specialty fertilizer consumption | +0.8% | East and South-Central China | Medium term (2-4 years) |

| Expansion of protected cultivation acreage needing fertigation | +0.6% | Peri-urban zones of East and South-Central China | Long term (≥ 4 years) |

| Emergence of digital agriculture platforms enabling precision dosing | +0.4% | National, early in tech-advanced regions | Long term (≥ 4 years) |

| Early adoption of low-carbon “green ammonia” production lines | +0.3% | Inner Mongolia and Xinjiang | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Fertilizer-Use Subsidy Schemes

Direct government subsidies for balanced fertilization and soil restoration under the Ministry of Agriculture and Rural Affairs programs are accelerating nutrient demand across China's agricultural regions. The agricultural machinery purchase subsidy program expanded to include precision fertilizer application equipment, with subsidy rates reaching 30% for eligible farmers in 2024[1]Source: Ministry of Agriculture and Rural Affairs, “Precision Fertilizer Subsidy Guidance,” MOA.GOV.CN. These policy interventions create artificial demand elasticity that supports premium pricing for efficiency-enhancing products while simultaneously driving volume growth in targeted nutrient categories. The subsidy framework particularly benefits controlled-release and water-soluble fertilizers that demonstrate measurable efficiency gains over conventional alternatives. Policy implementation varies significantly across provinces, with major grain-producing regions receiving proportionally higher subsidy allocations that distort regional competitive dynamics.

Chronic Pressure to Raise Crop Yields and Quality

Food security mandates embedded in China's national agricultural strategy create persistent upward pressure on fertilizer application intensity across all crop categories. The State Council's diversified food supply system opinion emphasizes yield maximization per hectare to offset limited arable land expansion, directly translating to increased nutrient input requirements. This policy framework operates independently of market pricing signals, creating inelastic demand for fertilizer products even during periods of agricultural commodity price volatility. Regional implementation focuses on closing yield gaps between average and potential productivity, with particular emphasis on grain crops that underpin national food security objectives. The pressure intensifies in regions where urbanization reduces agricultural land availability, forcing remaining farmland to achieve higher productivity levels through intensive fertilization practices.

Surge in Specialty Fertilizer Consumption

Rapid adoption of water-soluble fertilizers, controlled-release fertilizers, and slow-release fertilizers reflects a fundamental shift toward nutrient use efficiency optimization across China's agricultural sector. Specialty fertilizer consumption growth significantly outpaces conventional fertilizer demand, driven by demonstrated performance advantages in precision agriculture applications and regulatory compliance requirements. The transition is most pronounced in high-value horticultural crops where input cost optimization directly impacts profitability margins and market competitiveness. Controlled-release nitrogen fertilizers show particular promise in rice production systems, with field trials in Anhui Province demonstrating yield improvements and enhanced nitrogen use efficiency compared to conventional urea applications.

Expansion of Protected Cultivation Acreage Needing Fertigation

China's protected cultivation area exceeds 4 million hectares and continues expanding rapidly, creating concentrated demand for high-frequency fertigation systems that require specialized fertilizer formulations. Greenhouse and tunnel production systems generate fertilizer demand intensity 3-5 times higher than open-field cultivation, with application frequencies reaching daily intervals during peak growing seasons. This cultivation method shift fundamentally alters fertilizer market dynamics by creating premium-priced segments that support specialty product development and distribution infrastructure investment. Protected cultivation expansion concentrates in peri-urban zones where land values justify intensive production systems, creating geographic clustering effects that support specialized supply chains and technical service networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter nutrient-loss regulations and inspection regimes | -0.7% | National, tighter in sensitive watersheds | Short term (≤ 2 years) |

| Plateauing macronutrient demand in major grain belts | -0.5% | Northeast and North China Plain | Medium term (2-4 years) |

| Soil-test service bundles shifting farmers away from blanket NPK | -0.4% | Developed agricultural provinces | Medium term (2-4 years) |

| Carbon-pricing pilots boosting production costs for high-emission plants | -0.3% | ETS pilot provinces with large nitrogen capacity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Nutrient-Loss Regulations and Inspection Regimes

New GB 15618 soil quality standards impose penalties for excess nitrate leaching and phosphorus runoff, creating compliance costs that constrain fertilizer application rates across environmentally sensitive agricultural regions. The Ministry of Ecology and Environment has strengthened inspection protocols with real-time monitoring systems that track nutrient loading in watershed areas, forcing farmers to reduce application rates or face significant financial penalties [2]Source: Ministry of Ecology and Environment, “GB 15618 Soil Quality Standards,” MEE.GOV.CN. These regulatory constraints operate independently of agronomic optimization, creating situations where yield-maximizing fertilizer rates exceed legally permissible application levels. Compliance requirements favor efficiency-enhanced products that deliver equivalent nutritional value at lower application rates, but the transition period creates market disruption as farmers adjust application practices.

Plateauing Macronutrient Demand in Major Grain Belts

High historical fertilizer application rates in China's primary grain-producing regions have created soil nutrient saturation conditions that limit incremental NPK volume growth potential. Soil testing data from major grain belts indicate phosphorus and potassium levels that exceed crop requirements, reducing fertilizer responsiveness and economic returns from additional applications. This agronomic constraint creates natural demand ceilings that cannot be overcome through pricing or policy interventions, fundamentally limiting market expansion potential in the largest agricultural regions. The saturation effect is most pronounced in intensive production systems where decades of high-input agriculture have built soil nutrient reserves that support crop production with minimal external inputs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Complex Fertilizers Drive Market Leadership

Complex fertilizers are the largest segment, holding 56.2% of the China fertilizer market share in 2025, and are projected to register the fastest 6.0% CAGR through 2031. The complex segment benefits from precision agriculture trends that favor customized nutrient ratios matched to specific crop requirements and soil conditions. NPK compound fertilizers dominate the complex category, supported by established agronomic protocols that specify balanced nutrient ratios for major crop categories. Specialty complex formulations incorporating micronutrients and secondary macronutrients command premium pricing while addressing specific nutritional deficiencies identified through soil testing programs.

The segment's prominence is primarily attributed to its ability to provide multiple nutrients in a single application, making it highly efficient for farmers. Complex fertilizers are particularly crucial in China's urban greening sector, playing a vital role in maintaining decorative trees, high-quality grass, and nurturing flowers in greenhouses. The segment's strength is further reinforced by China's increasing reliance on NPK fertilizers, which typically account for about half of total fertilizer consumption. The granulation production method stands as the primary manufacturing approach, reflecting China's sophisticated fertilizer production landscape.

By Form: Conventional Products Maintain Dominance

Conventional products accounted for 74.0% of revenue in 2025, supported by established manufacturing infrastructure and cost advantages that align with price-sensitive agricultural markets. The conventional segment encompasses traditional granular and crystalline formulations that deliver nutrients reliably through proven application methods and equipment compatibility. Bulk handling advantages in conventional products support efficient distribution systems that serve large-scale agricultural operations with minimal logistical complexity. Manufacturing scale economies in conventional fertilizer production create cost structures that maintain competitive advantages over specialty alternatives in price-sensitive market segments.

Specialty variants are forecast to expand at the fastest pace of 6.1% CAGR through 2031. This segment is experiencing rapid advancement due to the increasing adoption of precision agriculture and modern irrigation methods. Water-soluble fertilizers, which account for about half of the specialty segment, are gaining particular traction due to their superior nutrient-delivery efficiency. The segment's growth is further propelled by rising awareness among farmers about the benefits of controlled-release fertilizers and their role in sustainable agriculture. The Chinese government's emphasis on environmental protection and the need for improved fertilizer efficiency are driving innovation in specialty fertilizer formulations.

By Application Mode: Fertigation Gains Momentum with Precision Agriculture Adoption

Soil led with a 74.3% of the China fertilizers market size in 2025. Broadcasting remains the most commonly employed soil application method among Chinese farmers due to its cost-effectiveness and ease of implementation. The segment's strong position is further reinforced by its extensive use in applying primary and secondary macronutrient fertilizers, with about 75.5% of primary macronutrients applied via soil application. While this method faces challenges such as uneven distribution and potential soil pollution, the development of controlled or slow-release fertilizers has helped address these concerns, contributing to the segment's continued market leadership.

Fertigation is set to maintain leadership over the forecast horizon at a 6.2% CAGR through 2031, reflecting the widespread adoption of irrigation-based fertilizer delivery systems that enable precise nutrient timing and dosing control. The dominance of this application method stems from water-scarce agricultural regions, where investment in irrigation infrastructure creates opportunities for integrated nutrient and water management systems. Fertigation systems reduce labor costs associated with separate fertilizer application while improving nutrient use efficiency through root-zone delivery and reduced surface losses.

By Crop Type: Field Crops Dominate Demand

Field crops represent 66.9% of fertilizer demand in 2025, driven by China's grain security priorities and the extensive acreage devoted to staple crop production, including rice, wheat, and corn. The segment's dominance reflects government policies that prioritize food self-sufficiency and support grain production through subsidies and technical assistance programs. Rice production systems account for the largest share of field crop fertilizer demand through intensive management practices that require multiple nutrient applications over extended growing seasons. Wheat and corn production contribute substantial demand volumes through mechanized application systems that enable efficient fertilizer distribution across large cultivation areas.

Horticultural crops are experiencing the fastest growth, with a 7.4% CAGR projected through 2031. This growth is driven by increasing demand for precision nutrition across fruits, vegetables, plantation crops, and spices. According to the China Agricultural Sector Development Report 2026, published by the Chinese Academy of Agricultural Sciences, export-oriented fruit and processed vegetable producers are increasingly adopting water-soluble, chelated, and controlled-release formulations to meet quality standards in international markets. In June 2025, China's Ministry of Agriculture and Rural Affairs (MARA) held a national horticulture sector meeting, emphasizing seed innovation and intelligent farming technologies. These advancements are structurally boosting the demand for advanced fertilizer programs in high-value crop systems. As a result, there is a growing per-hectare fertilizer expenditure gap between horticultural and field crop segments, prompting suppliers to adjust their product portfolios toward higher-margin specialty inputs. Ornamental plant production generates niche demand for specialty fertilizers that enhance aesthetic characteristics and plant health in landscape and greenhouse applications. The crop type segmentation reflects China's ongoing agricultural diversification, creating opportunities for value-added fertilizer products beyond traditional commodity crop applications.

Geography Analysis

Northeast China emerges as the largest regional market, capturing significant market share in 2025 through extensive grain production systems that require intensive fertilizer inputs across millions of hectares of mechanized farmland. The region's agricultural characteristics favor large-scale application systems and bulk fertilizer products that align with mechanized farming operations and commodity crop production economics. Heilongjiang Province leads regional fertilizer consumption through the largest provincial grain production area in China, while Jilin and Liaoning contribute substantial demand through diversified agricultural systems, including corn, soybeans, and rice production.

North China maintains a substantial market presence through intensive wheat and corn production systems that operate under water-scarce conditions requiring precise nutrient management and efficiency optimization. The North China Plain's agricultural intensity creates high fertilizer demand per unit area, while environmental constraints limit application rates and favor efficiency-enhanced products. Shandong Province contributes significant horticultural demand through intensive vegetable and fruit production systems that require specialty fertilizers and frequent application schedules. Regional water scarcity drives fertigation system adoption and creates demand for water-soluble fertilizer formulations that optimize nutrient delivery efficiency.

East China represents the fastest-growing regional market through agricultural modernization initiatives and specialty crop expansion that create demand for premium fertilizer products and precision application technologies. The region's economic development supports farmer investment in advanced fertilization systems and willingness to pay premium prices for efficiency-enhanced products. Jiangsu and Zhejiang provinces lead specialty fertilizer adoption through intensive horticultural production systems and protected cultivation expansion that require customized nutrient solutions.

Competitive Landscape

The Chinese fertilizer market is fragmented, with companies such as Sinofert Holdings Limited, Xinyangfeng Agricultural Technology Co., Ltd., Henan XinlianXin Chemicals Group Company Limited, Yara International ASA, and ICL Group Ltd creating strategic opportunities for both consolidation and niche specialization across diverse agricultural segments. This competitive structure reflects the market's evolution from commodity-focused distribution toward value-added services and specialty product differentiation.

Market leaders, including Sinofert Holdings, leverage integrated supply chains and extensive distribution networks to maintain competitive advantages, while smaller players focus on regional specialization and technical service capabilities. The competitive intensity varies significantly across product categories, with commodity fertilizers experiencing price-based competition and specialty segments supporting premium positioning through technical differentiation and service integration.

Strategic patterns emphasize vertical integration and technology adoption as key competitive differentiators, with leading companies investing in precision agriculture platforms and digital service capabilities that create customer switching costs and support premium pricing. Technology adoption patterns favor companies that can integrate IoT sensors, soil testing services, and customized fertilizer recommendations into comprehensive digital agriculture platforms that optimize farmer outcomes while generating valuable data assets for continuous product development and market segmentation strategies.

China Fertilizers Industry Leaders

Sinofert Holdings Limited

Xinyangfeng Agricultural Technology Co., Ltd.

Henan XinlianXin Chemicals Group Company Limited

Yara International ASA

ICL Group Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The National Energy Group announced a 3 million metric tons per year green fuel project in Bayannur, Inner Mongolia, incorporating renewable hydrogen-based ammonia production technology. This investment represents one of the largest commitments to low-carbon fertilizer manufacturing and signals industry-wide transformation toward sustainable production methods.

- April 2025: Stanley Agriculture Group has acquired a controlling stake in Chengde Lihe River Fertilizer for approximately RMB 244 million (USD 34.3 million), with legal counsel provided by JunHe. This acquisition enhances Stanley's upstream fertilizer capabilities. Additionally, the company is investing RMB 640 million (USD 90.0 million) to construct a 1 million-ton green compound fertilizer plant at the acquired company.

- August 2024: ICL has entered into a five-year partnership worth USD 170 million with AMP Holdings, a leading agricultural distributor in China. The agreement focuses on supplying specialty water-soluble fertilizers for high-value crops, such as fruits and vegetables cultivated using drip irrigation. Running until 2028, this partnership enhances ICL's position in China's specialty fertilizer market by providing Chinese growers with consistent access to its products.

China Fertilizers Market Report Scope

The China Fertilizers Market is Segmented by Type (Complex and Straight), by Form (Conventional and Specialty), by Application Mode (Fertigation, Foliar, and Soil), and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons)

Type

| Complex | ||

| Straight | Micronutrients | Boron |

| Copper | ||

| Iron | ||

| Manganese | ||

| Molybdenum | ||

| Zinc | ||

| Others | ||

| Nitrogenous | Urea | |

| Others | ||

| Phosphatic | DAP | |

| MAP | ||

| SSP | ||

| TSP | ||

| Potassic | MoP | |

| SoP | ||

| Others | ||

| Secondary Macronutrients | Calcium | |

| Magnesium | ||

| Sulfur | ||

Form

| Conventional | |

| Speciality | CRF |

| Liquid Fertilizer | |

| SRF | |

| Water Soluble |

Application Mode

| Fertigation |

| Foliar |

| Soil |

Crop Type

| Field Crops |

| Horticultural Crops |

| Turf & Ornamental |

| Type | Complex | ||

| Straight | Micronutrients | Boron | |

| Copper | |||

| Iron | |||

| Manganese | |||

| Molybdenum | |||

| Zinc | |||

| Others | |||

| Nitrogenous | Urea | ||

| Others | |||

| Phosphatic | DAP | ||

| MAP | |||

| SSP | |||

| TSP | |||

| Potassic | MoP | ||

| SoP | |||

| Others | |||

| Secondary Macronutrients | Calcium | ||

| Magnesium | |||

| Sulfur | |||

| Form | Conventional | ||

| Speciality | CRF | ||

| Liquid Fertilizer | |||

| SRF | |||

| Water Soluble | |||

| Application Mode | Fertigation | ||

| Foliar | |||

| Soil | |||

| Crop Type | Field Crops | ||

| Horticultural Crops | |||

| Turf & Ornamental | |||

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Primary Nutrients: N, P and K, Secondary Macronutrients: Ca, Mg and S, Micronutients: Zn, Mn, Cu, Fe, Mo, B, and Others

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms