Dental Biomaterials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.02 Billion |

| Market Size (2031) | USD 11.34 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

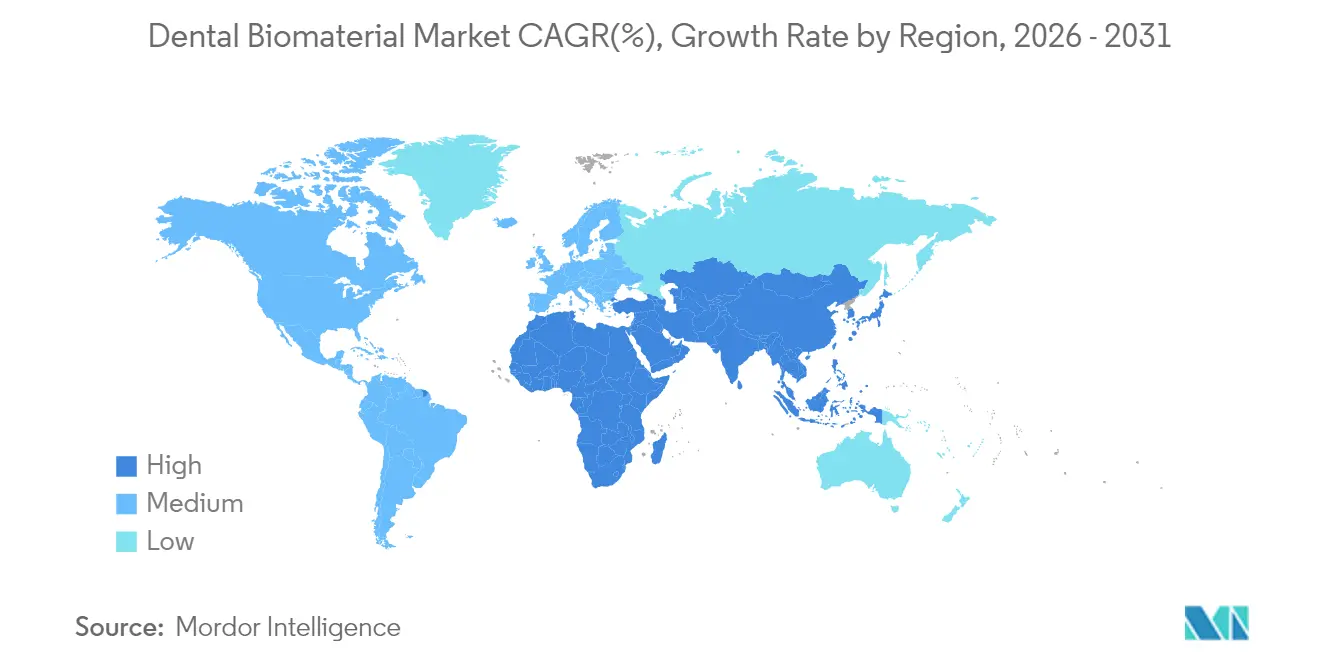

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

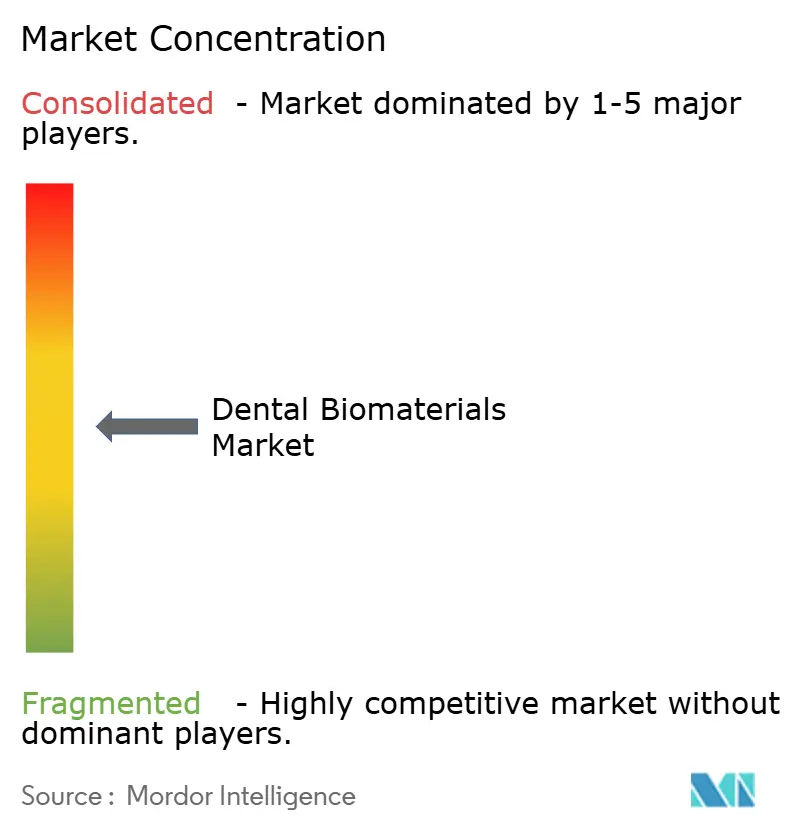

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Biomaterials Market Analysis by Mordor Intelligence

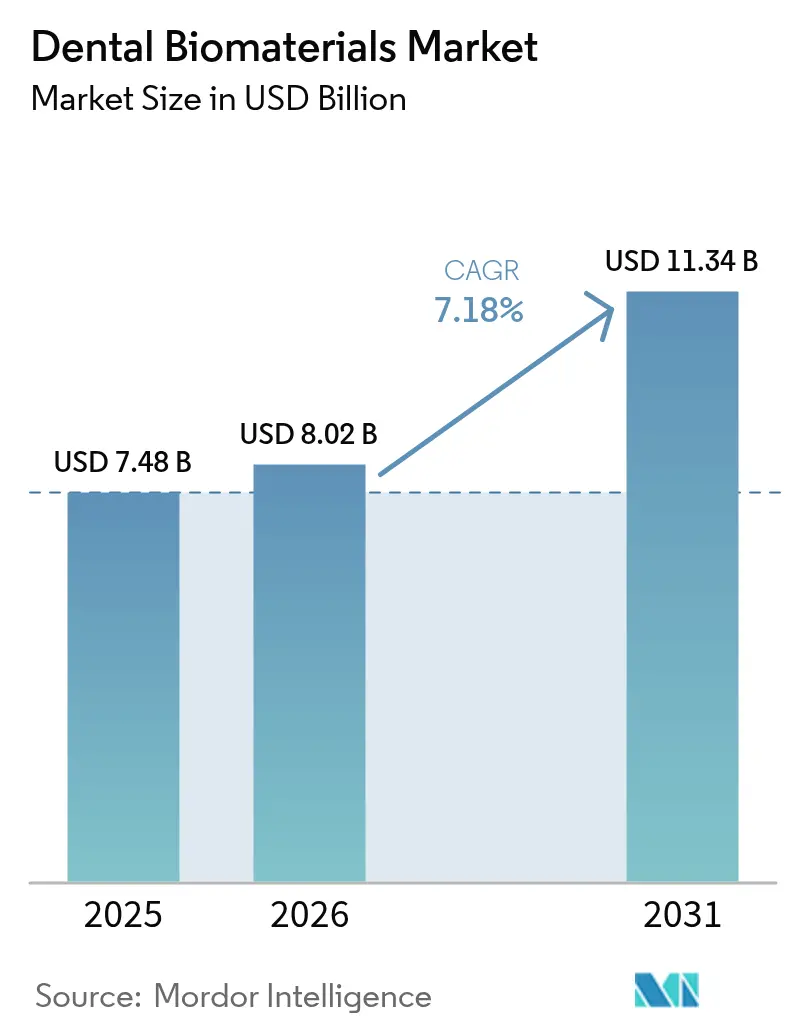

The Dental Biomaterials Market size is expected to grow from USD 7.48 billion in 2025 to USD 8.02 billion in 2026 and is forecast to reach USD 11.34 billion by 2031 at 7.18% CAGR over 2026-2031.

Rising edentulism in aging populations, broader insurance coverage for implantology, and expanding dental tourism corridors are reshaping purchase decisions and supply-chain priorities. Rapid adoption of CAD/CAM milling, 3D printing, and nano-engineering is shortening restoration cycles and opening premium pricing tiers for bioactive ceramics and hybrid composites. Post-2025 launches of regenerative scaffolds that stimulate osteogenesis represent a pivot from passive compatibility to active tissue integration. Intensifying price competition from Asia-Pacific laboratories compels Western manufacturers to refine zirconia sourcing and intensify chair-side digital workflows, allowing same-day crowns and bridges that align with evolving patient expectations for convenience and aesthetics.

Key Report Takeaways

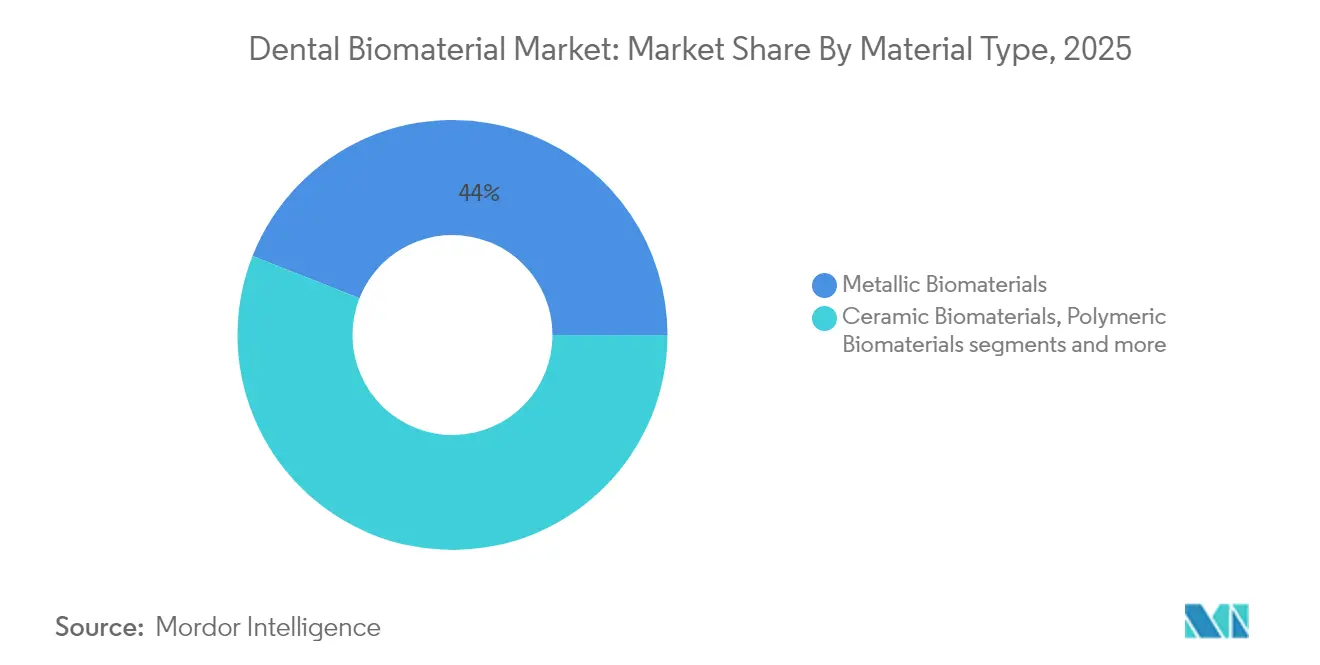

- By material type, metallic biomaterials led with 44.02% revenue share in 2025; ceramic biomaterials are projected to expand at an 8.54% CAGR through 2031.

- By application, implantology accounted for 49.20% of the dental biomaterials market share in 2025, while regenerative dentistry is advancing at a 8.75% CAGR to 2031.

- By geography, North America commanded 38.10% share in 2025; Asia-Pacific is growing fastest at a 8.55% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Biomaterials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & edentulism surge | 2.50% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Rising adoption of dental implants & prosthetics | 1.80% | Global, accelerated in Asia-Pacific emerging markets | Medium term (2-4 years) |

| Advances in CAD/CAM, 3-D printing & nano-engineering | 1.20% | North America & Europe core, spill-over to APAC | Short term (≤ 2 years) |

| Dental tourism in emerging markets | 0.90% | Asia-Pacific, Latin America, Eastern Europe | Medium term (2-4 years) |

| Emergence of bioactive / regenerative biomaterials post-2025 | 0.60% | Global, early adoption in developed markets | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Ageing population & edentulism surge

Longer life expectancy combined with higher expectations for oral function is transforming demand in the Dental biomaterials market. Edentulous rates remain highest in people over 65, and this cohort increasingly requests metal-free, highly aesthetic materials that closely replicate natural enamel. The pivot from removable dentures to implant-anchored restorations is especially clear in North America and Western Europe, where public and private insurers are slowly broadening coverage for implant therapy. Senior patients also present more challenging bone physiology, which has encouraged clinicians to switch toward oxide-ceramic implants to avoid corrosion risk and facilitate soft-tissue response. Between 2025 and 2030, active seniors are expected to constitute the single largest purchasing segment, and their willingness to pay for premium materials should offset pricing pressure elsewhere in the value chain.

Rising adoption of dental implants & prosthetics

Average five-year implant survival now exceeds 95%, a milestone that has removed long-standing clinical hesitancy and widened patient eligibility. Treatment workflows that integrate CBCT imaging, guided-surgery sleeves and chair-side milling cut operative times dramatically, making implant therapy viable for busy urban clinics. Suppliers such as Straumann have introduced protocols that trim patient visits by 40%, allowing practices to generate higher daily throughput while improving patient satisfaction. Surface-texturing technologies and bioactive coatings push osseointegration speed higher, enabling immediate-load protocols that appeal to younger, working-age patients who cannot accommodate lengthy healing periods. These dynamics are multiplying unit volumes in the Dental biomaterials market and stimulating demand for grafts, membranes and abutment materials that complement the fixture itself.

Advances in CAD/CAM, 3-D printing & nano-engineering

Computer-aided design and additive manufacturing are collapsing the traditional divide between laboratory and clinic, shifting more fabrication in-house and raising expectations for same-day service. High-speed chair-side mills now handle translucent zirconia blocks, while photopolymer printers can directly produce splints, surgical guides and temporary crowns from biocompatible resins. At the material level, nano-engineering introduces antibacterial ions or osteogenic cues without compromising structural integrity, an advance with immediate relevance for peri-implantitis reduction. Artificial-intelligence algorithms further refine lattice structures for patient-specific scaffolds, improving stress distribution and reducing residual monomer release. Together, these technologies accelerate product cycles and reinforce the transition toward personalised therapeutic approaches within the Dental biomaterials market.

Dental tourism in emerging markets

Price differentials of up to 70% compared with OECD countries continue to draw foreign patients to Thailand, Turkey, Mexico and Malaysia for complex procedures. Governments in these destinations actively promote “dental holiday” packages, offering fast-tracked visas and tax incentives for high-spec clinics that invest in advanced equipment. Malaysia’s perconal healthcare expenditure sector is predicted to reach USD 2.8 billion in 2027 on 6.4% compound growth, underscoring the spill-over opportunity for biomaterial suppliers [1]Source: International Trade Administration, “Malaysia Health Services Report 2025,” trade.gov. International patients typically request branded implants and FDA-approved ceramics to ensure post-treatment compatibility when they return home, nudging local dentists toward premium imports. The influx of foreign demand thus expands the addressable Dental biomaterials market but simultaneously exposes operators to quality-control and follow-up challenges across borders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced biomaterials & limited reimbursement | –1.1% | Global, acute in emerging markets | Medium term (2-4 years) |

| Stringent multi-region regulatory clearances | –0.8% | Global, particularly US-EU-APAC coordination | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of advanced biomaterials & limited reimbursement

Premium zirconia blanks, osteoinductive grafts and nano-coated implants often retail at two to five times the price of base-grade alternatives, placing them out of reach for cash-pay patients in low-income settings. Insurance cover remains patchy; in many OECD countries the benefit caps for dental still sit below USD 2,000 per year, forcing patients to self-fund extensive rehabilitation. In April 2025, new tariffs added up to 54% to the landed price of certain imported dental materials in the United States, prompting clinicians to reassess inventory strategies. These price shocks threaten to slow diffusion of innovative materials just as clinical evidence mounts in their favour. Suppliers are responding with tiered product lines and subscription-style consumable bundles, but affordability remains a critical drag on the Dental biomaterials market.

Stringent multi-region regulatory clearances

Manufacturers seeking global launch must navigate disparate dossier formats, biocompatibility test norms and post-market surveillance rules. The FDA’s 2024 update on performance criteria for implants and composite resins tightened fatigue and corrosion benchmarks, extending 510(k) review cycles by several months for many applicants. The European Union’s MDR framework requires clinical data even for legacy products when formulations change, adding cost and time. Although China’s NMPA offers an expedited route for “innovative” devices, duplicative testing still occurs when companies aim for simultaneous approvals in Japan, Korea or Australia. Compliance expenditures divert resources from R&D and lengthen the clock on revenue generation, thereby dampening near-term growth in the Dental biomaterials market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Ceramic Innovation Challenges Metallic Dominance

Metals commanded 44.02% capture of the Dental biomaterials market share in 2025, underpinned by titanium’s proven biomechanical profile and clinician familiarity. Unit volumes remain high in posterior load-bearing zones and full-arch prosthetics, where fatigue resistance overrides aesthetic concerns. Yet ceramics, led by zirconia, are growing at an 8.54% CAGR as translucency advances narrow the visual gap with lithium-disilicate glass. Elevated consumer demand for metal-free restorations along with growing sensitivity to allergic reactions accelerates the ceramic migration path. Suppliers now pitch multi-layer zirconia discs that blend flexural strength cores with enamel-like surface layers, allowing one-piece full-contour crowns milled chair-side without veneering. That capability aligns neatly with single-visit dentistry trends and positions ceramics for continued share gain inside the Dental biomaterials market.

Digital design requirements are reshaping R&D agendas across all material classes. New polymer-infiltrated ceramic networks target hybrid indications, promising fracture toughness comparable to metals and polishing behaviour that mitigates antagonist wear. At the same time, resin-matrix composites with nano-filler scaffolds are capturing interim and long-span indications where weight savings matter. In the metals segment, cold-spray and selective-laser-melting processes are lowering porosity and enabling lattice-style structures that tune elasticity closer to cortical bone. Such improvements reinforce the incumbent position of metals in specialty cases even as cosmetic dentistry swings toward ceramics. The result is a nuanced competitive landscape in which each formulation occupies a clearly delineated price-performance niche, sustaining multi-material coexistence within the broader Dental biomaterials market.

By Application: Regenerative Dentistry Disrupts Traditional Hierarchies

Implantology retained 49.20% share of the Dental biomaterials market size in 2025 thanks to its composite demand for fixtures, abutments, grafts and barriers that extend the revenue footprint of every procedure. Implants have become the default standard of care whenever viable bone is present, and even in compromised cases clinicians increasingly rely on guided-bone-regeneration rather than opting for removable prostheses. However, regenerative dentistry outpaces all other groups with a 8.75% CAGR, propelled by breakthroughs in cell-laden hydrogels and growth-factor soaked membranes that stimulate endogenous healing. Academic-industry partnerships are moving enamel-matrix derivatives from periodontal therapy into broader alveolar-bone applications, setting the stage for a sizeable future revenue pocket inside the Dental biomaterials market.

Interdisciplinary overlaps are rising. Complex full-arch cases often marry implantology with sinus-lift grafts and onlay regenerative membranes, blurring category lines and lifting average selling prices per patient. Endodontics too is being revitalised as bioceramic sealers enable regenerative apexification protocols that keep teeth viable and delay extraction. Orthodontic anchorage screws fabricated from beta-titanium alloys now come pretreated with antibacterial nano-silver to limit peri-implantitis, illustrating continuous cross-pollination of material science. The competitive opportunity therefore hinges on platform technologies adaptable across applications rather than on standalone products, a trend that favours suppliers with broad portfolios in the Dental biomaterials market.

By Product Category: CAD/CAM Blocks Challenge Traditional Grafting Dominance

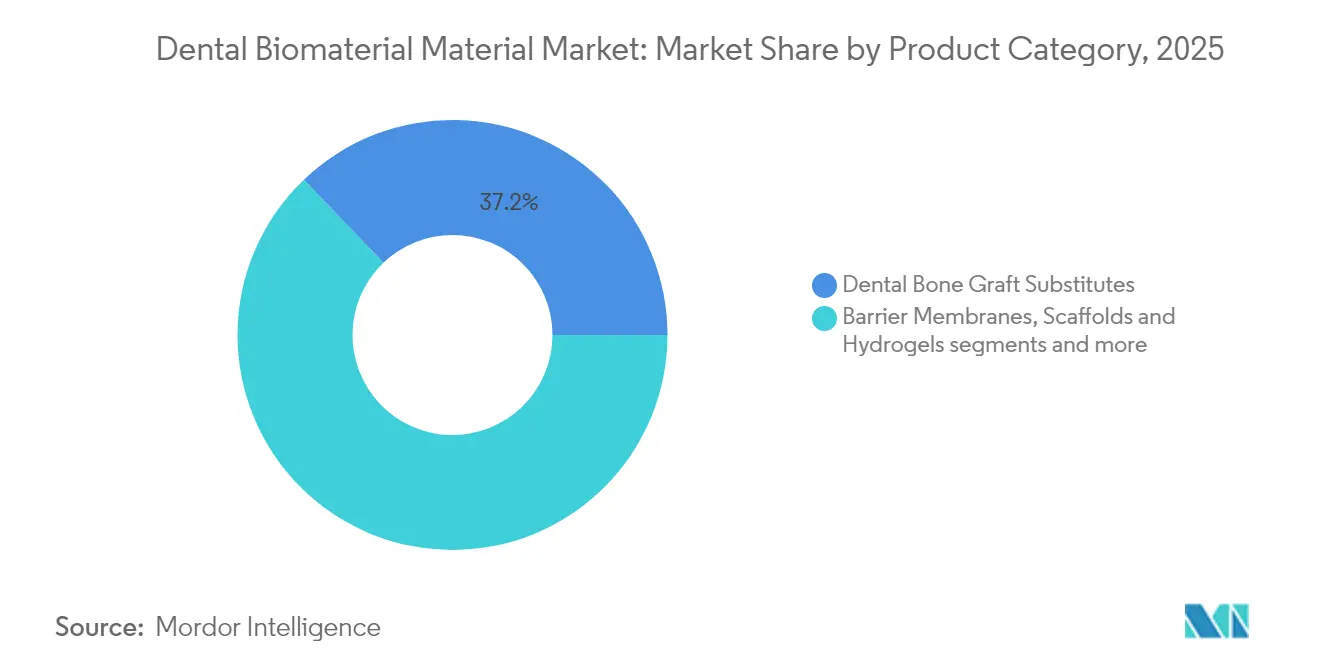

Bone-graft substitutes held the largest 37.15% slice of the Dental biomaterials market size in 2025, anchored by the ubiquity of ridge-preservation and sinus-augmentation procedures. Xenografts and alloplasts dominate volume, yet synthetics infused with bioactive glass are capturing value at the premium end by offering controlled resorption and ion release that encourages angiogenesis. The fast-growing challenger group is CAD/CAM blocks and discs, tracking an 7.68% CAGR as in-office systems gain reliability and cost per crown falls. One chair-side mill can now finish a full-contour zirconia crown in under nine minutes, compressing the restorative cycle into a single appointment and locking in practitioner loyalty.

Product convergence accelerates innovation. Membrane-graft combos packaged in ready-to-use delivery kits simplify chair workflow and reduce contamination risk. Coral-inspired scaffolds from Swansea University achieve full vascularised bone integration within months, showing potential to shrink healing windows for implant placement. Adhesives and luting cements evolve toward universal chemistries compatible with multiple substrates, boosting inventory efficiency in clinics. While liners and bases remain stable low-growth categories, nano-hydroxyapatite fillers are lifting their radiopacity and strengthening their relevance for deep-class cavities. Overall, the shift from single-function to multifunctional offerings elevates switching costs and entrenches long-term supplier-clinic relationships inside the Dental biomaterials market.

By End User: Dental Clinics Drive Market Evolution

Dental clinics controlled 56.90% of the Dental biomaterials market size in 2025 and also posted the fastest 8.22% CAGR, reflecting consolidation under dental-service-organisation (DSO) models and aggressive investment in digital workflow. Clinics wield direct influence over material choice, and their ability to amortise in-house milling capital costs across high procedure volumes makes them critical gateways for new product launches. Hospitals and academic centres maintain a vital role for maxillofacial trauma and complex oncology cases, but they account for a smaller share of routine restorative material consumption. Laboratories, once central to crown production, are pivoting toward niche aesthetic layering and implant superstructure design as simpler jobs migrate to chair-side solutions.

The operational economics in clinics favour vendor bundles that include training, software upgrades and replenishment consumables on subscription. Such service wraps help practices manage cash flow while guaranteeing suppliers a predictable revenue stream, deepening customer stickiness in the Dental biomaterials market. Dental tourism magnifies the influence of high-spec clinics in Bangkok, Istanbul and Tijuana, which showcase state-of-the-art materials on social media to attract international patients. Meanwhile, teledentistry platforms funnel case planning to remote prosthodontists who pre-approve material lists, standardising purchasing behaviour across distributed practice networks and further accelerating clinic-centric growth.

Geography Analysis

North America remains the single largest regional contributor to the Dental biomaterials market, driven by a high incidence of implant procedures, robust insurance penetration, and rapid adoption of digital chair-side systems. The United States sees pronounced demand in sun-belt states where older retirees cluster and where DSOs roll out scalable care models that standardise material protocols. Canada mirrors these trends on a smaller scale but benefits from public reimbursement frameworks that now fund select implant cases for seniors, extending addressable volume.

Europe follows closely, though growth patterns vary by sub-region. Western Europe sustains replacement cycles for ageing fixed prostheses and increasingly favours ceramic-based materials in response to patient demand for metal-free smiles. Central and Eastern Europe, led by Poland and Hungary, have built a thriving dental tourism corridor catering primarily to German and Nordic patients seeking lower procedure costs. This inflow pushes clinics to stock branded implants and high-translucency zirconia, lifting average selling prices and enriching the Dental biomaterials market.

Asia-Pacific records the fastest aggregate expansion, propelled by rising disposable incomes, aggressive infrastructure investments, and supportive government measures in South Korea and Japan that subsidise implant therapy for seniors. China’s tier-one cities host cutting-edge university spin-offs producing nano-engineered grafts, yet uneven insurance cover keeps adoption skewed toward coastal metros. India and Southeast Asia benefit from returning medical tourists and cost-competitive labour, though import tariffs on premium biomaterials push clinics toward domestic alternatives. Collectively these vectors position the region as the foremost incremental growth engine for suppliers operating in the global Dental biomaterials market.

Competitive Landscape

The dental biomaterials market is moderately competitive, with the presence of local and international players in the market. The major share of the market has been grabbed by global players, whereas small to mid-sized companies are posing intense competition with the help of novel technologies. In the future, it is expected that the market share will be distributed among international players and small players as well due to the focus on new entrants to come up with innovative products. Some of the major players in the market are Straumann Holding AG, Dentsply Sirona Inc., 3M Company, ZimVie Inc., and Botiss Biomaterials GmbH among others.

Dental Biomaterials Industry Leaders

Straumann Holding AG

ZimVie Inc.

3M Company

Dentsply Sirona, Inc

botiss biomaterials GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Straumann launched the BLX Pro implant line with a bioactive osseointegration surface designed for immediate loading.

- November 2024: The FDA issued updated performance criteria for dental composite resins, raising minimum flexural strength requirements.

- June 2024: Kuraray Noritake released KATANA Zirconia YML, a multi-layer disc combining high flexural strength with enamel-level translucency.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our team defines the dental biomaterials market as the worldwide sale, at manufacturer prices, of biocompatible metals, ceramics, polymers, composites, and natural matrices that dentists and labs use in restorative, implantology, prosthodontic, orthodontic, and regenerative procedures.

Scope exclusion: handpieces, scanners, cements, or any consumables whose primary role is non-integrative lie outside this study.

Segmentation Overview

- By Material Type (Value)

- Metallic Biomaterials

- Ceramic Biomaterials

- Polymeric Biomaterials

- Metal-Ceramic Hybrids

- Natural / Bio-derived Materials

- By Application (Value)

- Implantology

- Prosthodontics

- Orthodontics

- Regenerative Dentistry

- Periodontics

- Endodontics

- By Product Category (Value)

- Dental Bone Graft Substitutes

- Barrier MembranesScaffolds & Hydrogels

- Barrier Membranes

- Scaffolds & Hydrogels

- Adhesives & Cements

- CAD/CAM Blocks & Discs

- Liners & Bases

- By End User (Value)

- Dental Clinics

- Hospitals & Multi-Specialty Centers

- Dental Laboratories

- Academic & Research Institutes

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC Countries

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with oral surgeons, lab managers, material scientists, and distributors across North America, Europe, China, and Brazil. Their views on grams used per case, regional price spreads, and emerging bioactive ceramics filled gaps and grounded our assumptions before final triangulation.

Desk Research

We began with open datasets such as WHO oral-health surveys, UN population projections, and OECD health-expenditure dashboards to size treated populations. Customs HS codes tracking zirconia blocks and titanium powders, along with FDI World Dental Federation and American Academy of Implant Dentistry procedure counts, revealed product flows and intervention volumes.

Annual reports, FDA 510(k) files, European CE databases, and news archived in Dow Jones Factiva added pricing and capacity clues, while D&B Hoovers broke out supplier revenues. Numerous additional sources informed data checks that are not all named here.

Market-Sizing & Forecasting

We built a top-down model that multiplies yearly implant, crown, and ridge-augmentation counts by average material weights and ex-factory prices, then adjusts for regional procedure mix. Supplier roll-ups, channel checks, and sampled ASP-times-volume acted as a bottom-up sense check. Key drivers include implant penetration per 10,000 population, zirconia price trends, elective dentistry spend, and regulatory approvals. A multivariate regression blended with scenario analysis projects values through 2030, and missing inputs are prorated from import shares when needed.

Data Validation & Update Cycle

Outputs pass variance alarms, peer review, and final analyst sign-off. Mordor refreshes every twelve months, with mid-cycle updates triggered by material regulatory, pricing, or demand shocks.

Why Our Dental Biomaterials Baseline Commands Reliability

Published estimates differ because firms vary scope, price vintage, and refresh cadence. We surface these factors so users see where totals diverge.

Key gap drivers include whether natural grafts are folded into scope, the treatment of chair-side CAD/CAM blanks, ASP escalation methods, and the age of procedure counts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.48 B (2025) | Mordor Intelligence | - |

| USD 3.15 B (2024) | Global Consultancy A | Narrows scope to metallics and relies on 2019 prices |

| USD 1.11 B (2024) | Regional Consultancy B | Tracks only hospital buyers, omits import reconciliation |

| USD 10.70 B (2024) | Industry Journal C | Bundles dental cements and uses a single-year currency fix |

The comparison shows that our disciplined scope choices, live price tracking, and annual refresh give decision-makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is driving current growth in the Dental biomaterials market?

Growth stems from ageing demographics, rising implant adoption, and accelerated digital manufacturing that shortens treatment cycles.

Which material segment is gaining share the fastest?

Ceramic biomaterials led by translucent zirconia are expanding at an 8.54% CAGR due to demand for metal-free aesthetic restorations.

How big is implantology within the Dental biomaterials market?

Implantology accounted for 49.20% share of the Dental biomaterials market size in 2025, reflecting its multi-product revenue footprint.

Why are clinics the dominant end user for biomaterials?

Clinics control 56.90% of spending because they sit at the point of care, dictate material choices, and increasingly own in-house milling capacity.

What barriers could slow biomaterial innovation?

High product costs, fragmented reimbursement, and protracted multi-jurisdiction regulatory approvals can dampen near-term adoption.

Are regenerative materials close to commercial reality?

Bioactive scaffolds and stem-cell therapies are progressing through early trials and could begin meaningful market entry after 2026 as regulatory clarity improves.

Page last updated on: