Medium Chain Triglycerides (MCT) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

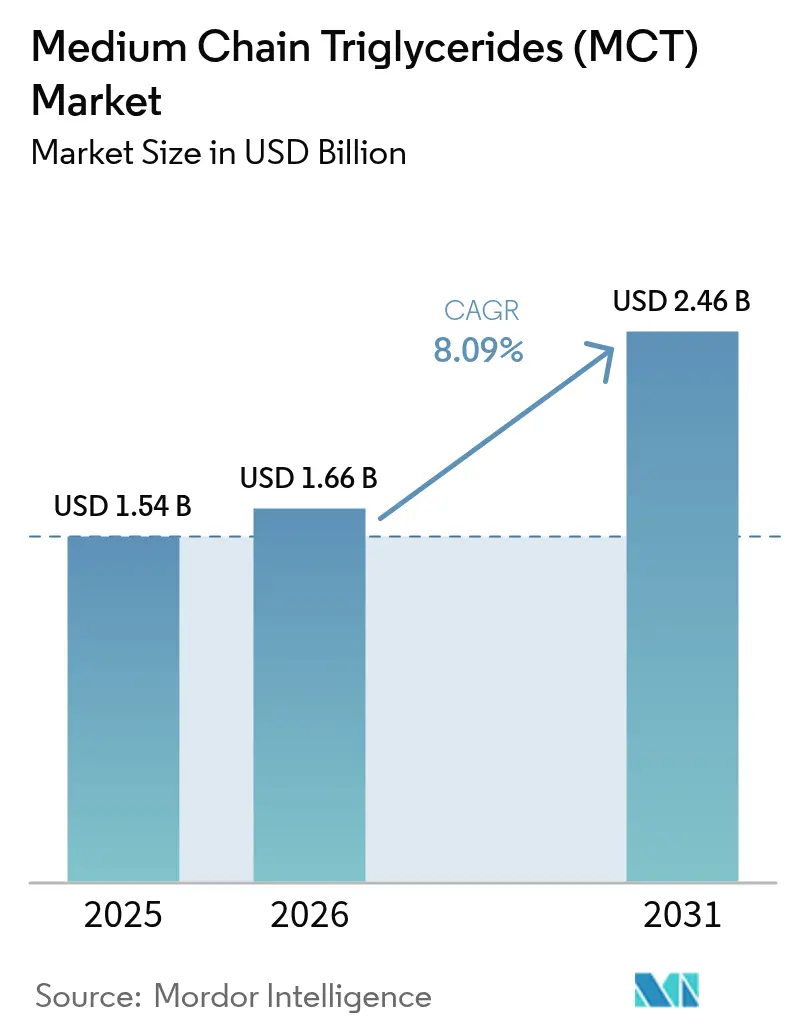

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.46 Billion |

| Growth Rate (2026 - 2031) | 8.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medium Chain Triglycerides (MCT) Market Analysis by Mordor Intelligence

The Medium Chain Triglycerides market size is expected to grow from USD 1.54 billion in 2025 to USD 1.66 billion in 2026 and is forecast to reach USD 2.46 billion by 2031 at 8.09% CAGR over 2026-2031. Growth is led by widening usage in sports nutrition, ketogenic diets, premium infant formulas, and lipid-based drug delivery systems. Liquid formats, particularly those sourced from coconut oil, underpin mainstream adoption because they blend easily into foods and beverages while delivering rapid, stomach-friendly energy. Pharmaceutical formulators value MCTs’ portal-vein absorption pathway, which enhances bioavailability for poorly soluble actives, and cosmetic brands prize their light texture and clean-label positioning. Supply-side strategies now center on source diversification—especially into certified palm kernel oil and emerging oil crops—to hedge climate-related price swings, while technology investments focus on purity upgrades and tailored fatty-acid blends. Competitive intensity remains moderate as vertically integrated players scale production, yet niche innovators secure premium contracts in clinical nutrition and specialty cosmetics.

Key Report Takeaways

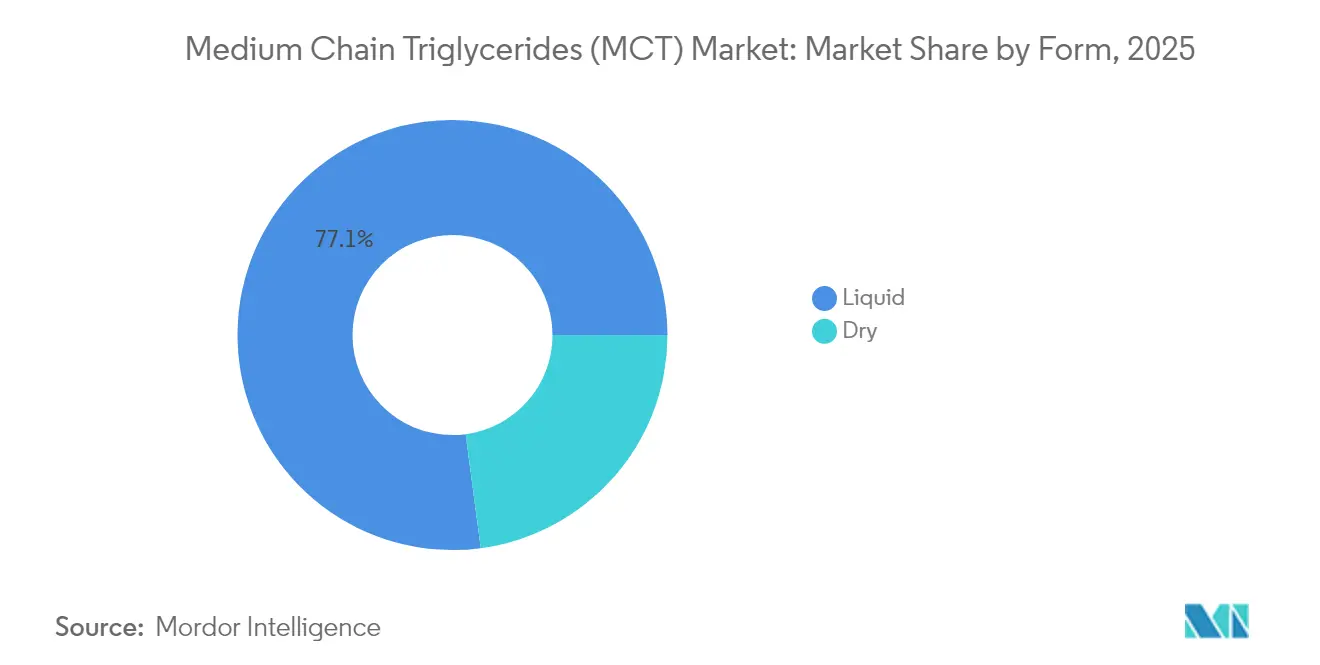

- By form, liquid products held 77.10% of the medium chain triglycerides market share in 2025, and are projected to expand at an 8.74% CAGR through 2031.

- By source, coconut oil accounted for 75.60% of the medium chain triglycerides market share in 2025, while palm kernel oil is projected to expand at an 8.56% CAGR through 2031, the fastest among all raw-material categories.

- By fatty-acid type, caprylic acid commanded 65.30% share of the medium chain triglycerides market size in 2025 and is on track to grow at 8.61% CAGR to 2031.

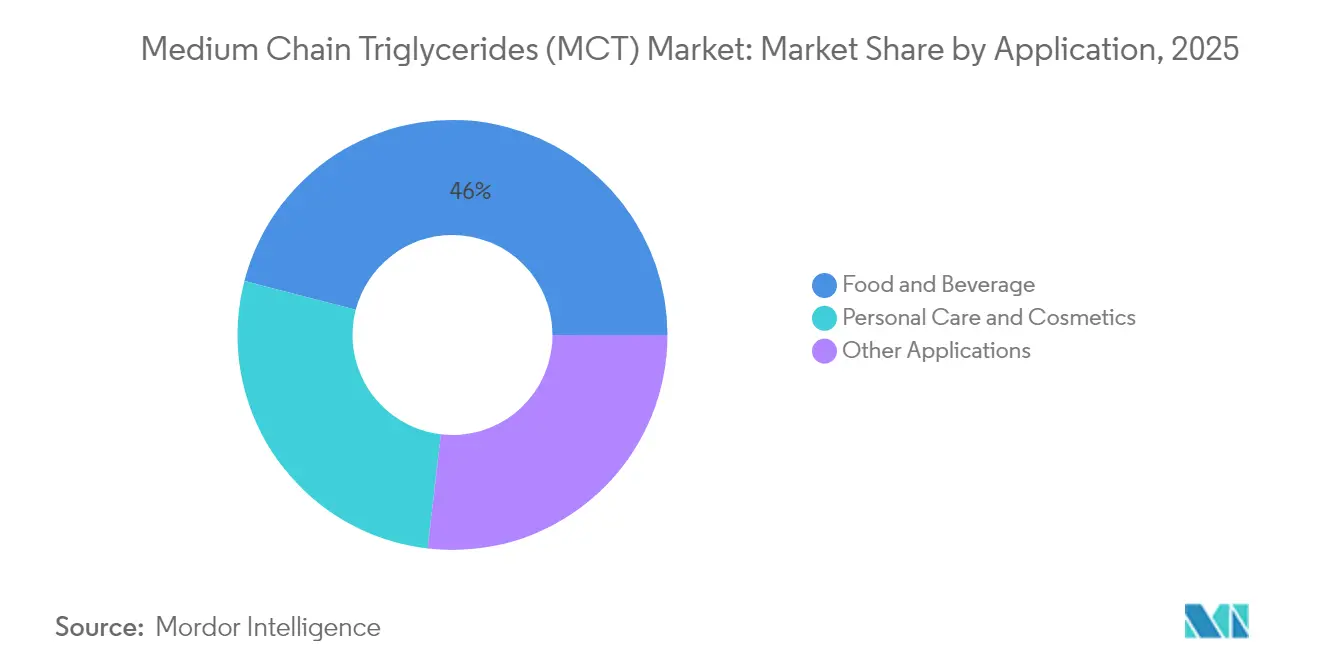

- By application, food and beverages generated 45.95% revenue in 2025, and are projected to register 8.21% CAGR during 2026-2031.

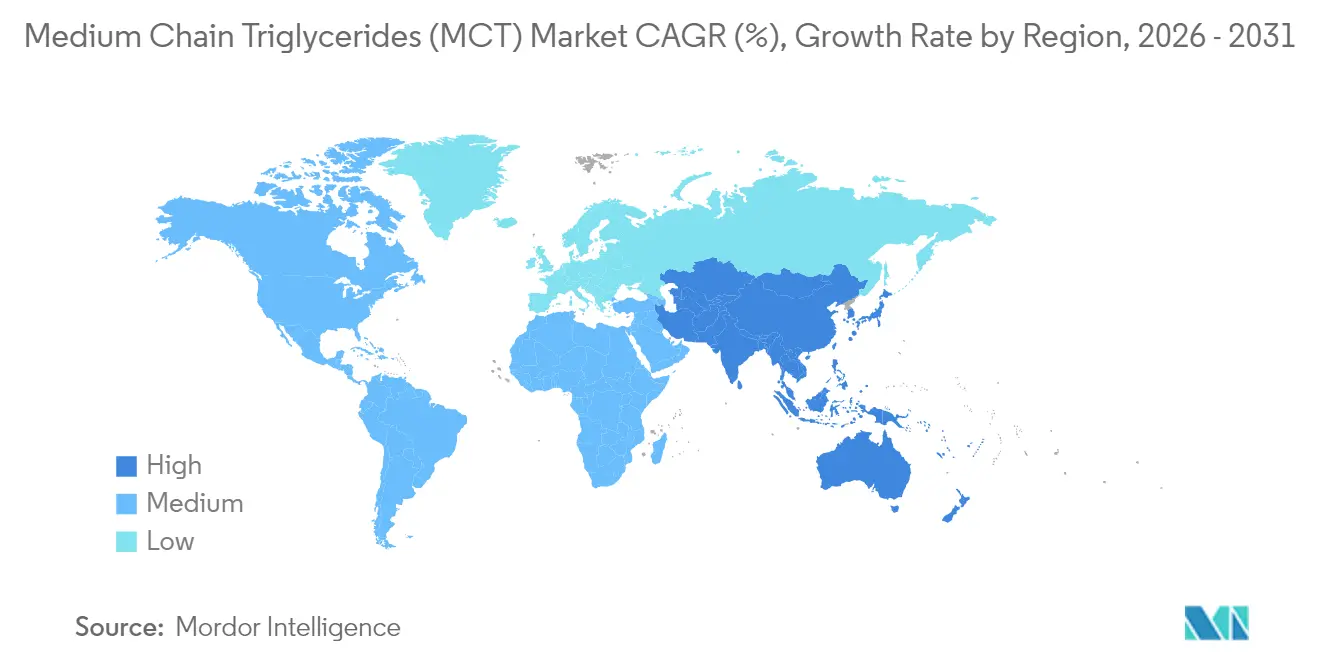

- By geography, North America commanded 37.90% revenue in 2025. Asia-Pacific is poised to grow at an 8.76% CAGR toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medium Chain Triglycerides (MCT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing usage of MCTs in sports & performance nutrition | +1.80% | Global, with North America & Europe leading adoption | Medium term (2-4 years) |

| Rising adoption of ketogenic & low-carb diets | +1.50% | North America & Europe core, expanding to APAC urban centers | Short term (≤ 2 years) |

| Expansion in personal care & cosmetics applications | +1.20% | Global, with premium segments in developed markets | Long term (≥ 4 years) |

| MCTs in lipid-based drug delivery systems | +0.90% | North America & Europe regulatory-driven markets | Long term (≥ 4 years) |

| Premium infant formula demand in Asia | +1.10% | APAC core, particularly China, India, and Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Usage in Sports & Performance Nutrition

Athletes increasingly replace long-chain fats and simple carbohydrates with MCT-fortified gels, shots, and powders because caprylic-dominant oils generate ketones within minutes, sustaining endurance without glycemic spikes. Clinical work in older adults shows that daily MCT supplementation enhances muscle quality while lowering glucose oxidation, hinting at crossover benefits for recovery and healthy aging[1]Tatsushi Mutoh, “Medium-Chain Triglyceride Dietary Supplements Reduce Glucose Metabolism,” Nutrients, mdpi.com . Research highlights that a significant portion of sports-nutrition buyers are willing to pay a premium for recognizable, single-origin lipids that align with clean-label diets. Brand owners now list specific chain-length ratios on front-of-pack claims to differentiate performance profiles, pushing processors toward tighter fractionation and purity specifications. North American contract-manufacturers report double-digit order growth for keto-friendly ready-to-drink beverages that rely on liquid MCTs for smooth mouthfeel and shelf stability. Sustainable palm kernel supply chains that carry RSPO certification are being tapped to manage cost while meeting Environmental, Social, and Governance (ESG) targets in athlete-focused product lines.

Rising Adoption of Ketogenic & Low-Carb Diets

Widespread interest in ketogenic eating is re-shaping grocery aisles as shoppers seek ingredients that elevate circulating ketone bodies quickly. Caprylic-dominant tricaprylin delivers the most efficient ketogenic response compared with traditional coconut oil, driving its dominance in concentrated drops and shots[2]Lucia Gabriny, “Coconut-Sourced MCT Oil: Its Potential Health Benefits Beyond Traditional Coconut Oil,” Springer, springer.com . Medical professionals now prescribe MCT-enriched meal plans to epilepsy patients because medium-chain triglyceride formulations allow higher carbohydrate intake than classical ketogenic protocols without compromising seizure control. Social-media recipe influencers amplify this clinical endorsement, accelerating household penetration in the United States, Canada, and Western Europe. Asian urban consumers are joining the trend as e-commerce platforms bundle MCT oil with glucomannan fibers in low-carb starter packs, prompting regional refiners to add smaller SKUs and flavored variants. The dietary shift sustains robust baseline demand and mitigates seasonality, anchoring revenue streams for vertically integrated producers.

Expansion in Personal Care & Cosmetics Applications

Cosmetic formulators value MCTs for their fast-absorbing, non-greasy sensory profile and ability to solubilize fat-soluble actives such as retinol and CoQ10. New emollient blends combine C8/C10 fractions with natural esters to create water-light face oils that lock in moisture without pore blockage, a key requirement for blemish-prone consumers. In anti-aging lines, MCTs serve as carriers for collagen-boosting peptides, improving dermal penetration and product efficacy. Clean beauty regulations in the European Union—which restrict certain silicones—are nudging brands toward biodegradable lipid bases, and certified-sustainable palm kernel MCTs meet this criteria. Margin upside is substantial: unit prices for cosmetics-grade MCTs run 25–35% above food-grade equivalents, supporting capital investment in ultra-refinement and odor-removal technology. Long-term growth is expected from hybrid skincare-nutraceutical products such as edible beauty drops, blurring the boundary between topical and ingestible formats.

MCTs in Lipid-Based Drug Delivery Systems

Pharmaceutical innovators turn to medium-chain triglycerides when tasked with elevating solubility for lipophilic APIs. Self-emulsifying drug delivery systems (SEDDS) containing high-purity C8/C10 oils have tripled oral bioavailability for compounds such as CoQ10 in phase-II trials. Patent filings for steroid hormone compositions solubilized in MCT oils have grown steadily, underscoring the molecule’s role as both vehicle and permeability enhancer. North American CDMOs now maintain dedicated tanks for pharma-grade MCTs free of residual pesticides and 3-MCPD contaminants to satisfy stringent US FDA guidance. As biologics pipelines swell, demand for lipid nanoparticles that integrate controlled chain-length triglycerides is poised to climb, extending MCT relevance beyond small-molecule delivery. European novel-food approvals that allow MCT use as a standardizing agent for bioactives further streamline regulatory pathways for combination products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile coconut & palm kernel oil prices | -1.40% | Global, with APAC production regions most affected | Short term (≤ 2 years) |

| Availability of alternative functional lipids | -0.80% | North America & Europe where innovation is concentrated | Medium term (2-4 years) |

| Sustainability certification costs for palm sourcing | -0.60% | Global supply chains with EU regulatory compliance focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Coconut & Palm Kernel Oil Prices

Weather-driven supply shocks frequently lift feedstock prices. Statistical modelling shows that a 1% uptick in palm kernel oil prices can push coconut-oil demand higher by 1.89% as buyers substitute between the two inputs, amplifying volatility. Erratic rainfall in Indonesia and Malaysia, the twin pillars of palm supply, depresses fresh-fruit bunch yields and spills into refined-oleochemical pricing. Such spikes compress gross margins for MCT refiners that operate on three-month fixed-price contracts with food manufacturers. Vertical integration into plantations offers a natural hedge, but smaller processors without acreage must rely on financial derivatives or long-term supply agreements, which can raise working-capital requirements.

Availability of Alternative Functional Lipids

Structured lipids and fermentation-based oils present competitive headwinds. Smart-fat emulsions engineered by European biotech firms cut saturated fat by up to 50% while retaining mouthfeel valued in plant-based meats, challenging MCTs’ hold in that category. Microalgae-derived omega-3 oils appeal to sustainability-minded consumers and offer similar oxidative stability in shelf-stable beverages. Medium- and long-chain triacylglycerol (MLCT) blends optimize energy density and lipid digestion in medical-nutrition drinks, encroaching on traditional MCT territory[3]Xingguo Wang, “Medium- and Long-Chain Triacylglycerol: Preparation, Health Benefits,” Annual Review of Food Science and Technology, annualreviews.org . As R&D pipelines widen, formulators may down-spec MCT inclusion levels, limiting volume growth, though entrenched ketogenic and clinical data advantages temper full substitution risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Dominance Drives Market Penetration

Liquid products accounted for 77.10% sales in 2025, a commanding lead that will widen as sports-drink, RTD coffee, and medical-nutrition brands prefer pourable formats for quick dispersion. The liquid sub-category is projected to grow at 8.74% CAGR, outpacing powders. One-shot ampoules targeting endurance athletes illustrate the trend: formulators achieve isotonic profiles without emulsifiers, preserving label simplicity. In contrast, powders cater to bars, bakery mixes, and sachets, where low moisture and long shelf life matter. Advancements in spray-drying and encapsulation have significantly improved oil-load capacity, reducing the cost per gram of active lipid. However, challenges like bulk density and mouth-feel limitations continue to confine these powders to specialized applications. Innovations such as agglomerated granules with lecithin carriers could expand penetration into instant beverages.

By Source: Coconut Oil Leadership Faces Palm Kernel Challenge

Coconut oil retained a 75.60% share in 2025 thanks to positive consumer perception and long-standing supply chains across the Philippines, Indonesia, and India. That dominance masks rapid palm kernel oil gains: the latter is forecast at 8.56% CAGR. Malaysian refiners are investing in mid-stream fractionation to supply pharmaceutical-grade C8/C10 cuts, eroding brand-owner prejudice. Alternative feedstocks like macauba and synthetic esters are gaining attention due to their climate-resilient yields, despite their limited adoption. Multinationals trial blended-source strategies to hedge climate risks and harmonize fatty-acid spectra, a sign that supply diversification will become standard by the decade’s end.

By Fatty Acid Type: Caprylic Acid Maintains Therapeutic Edge

Caprylic acid held 65.30% revenue in 2025 and will maintain leadership because it achieves the highest plasma ketone response, a key selling point for ketogenic supplements. Premium C8 concentrates price at 30–35% above typical C8/C10 blends, yet demand remains strong in medical-food channels. Capric acid provides a slower, sustained energy curve favored in recovery beverages, while lauric acid’s antimicrobial traits keep it relevant in dermatological creams and oral-care rinses. Caproic acid usage stays marginal due to sensory drawbacks, though pharma developers utilize it in taste-masked capsules for pediatric glycogen-storage-disease formulas. Suppliers are refining fractional distillation and short-path evaporation to customize chain-length ratios, opening bespoke blends for targeted outcomes.

By Application: Food & Beverage Segment Faces Diversification Pressure

The medium chain triglycerides market size for food and beverages is forecast to grow at 8.21% CAGR as mainstream brands roll out keto-friendly launches. Nonetheless, its share will edge down as high-margin segments—cosmetics and pharmaceuticals—expand faster. In beauty, MCTs enable transparent cleansing balms and silicone-free serums that resonate with eco-conscious consumers. Pharmaceutical uptake hinges on patent-protected delivery systems and orphan-drug nutrition regimens, both commanding premium transfer prices. Industrial uses—inks, lubricants, and agrochemicals—provide steady but low-growth outlet streams, mainly absorbing lower-purity cuts that accumulate during high-grade production runs.

Geography Analysis

North America captured 37.90% revenue in 2025. The region benefits from well-defined FDA GRAS rulings, enabling swift cross-category adoption. Canadian functional-food regulations similarly streamline MCT-supplement launches, cementing regional leadership.

Asia-Pacific is the fastest-growing territory at 8.76% CAGR. China’s dual-circulation policy encourages domestic production of high-value oleochemicals, catalyzing investments such as KLK’s expanded refinery in Jiangsu. Rising birth rates in India and Indonesia underpin robust infant-formula demand, while Japan’s aging population fuels clinical-nutrition consumption. Import duties on refined coconut oil were cut in Vietnam and Thailand during 2024, facilitating intra-ASEAN trade and lowering landed costs for local blenders.

Europe maintains a technology-driven market. Germany, France, and the United Kingdom source high-purity MCTs for drug-delivery platforms and cosmeceuticals. The EU’s 2024 novel-food approvals cement regulatory certainty, yet the imminent Deforestation Regulation raises compliance hurdles for non-segregated palm-kernel material; as a result, suppliers are accelerating satellite-based traceability systems. Eastern European processors increasingly import raw coconut oil via the Black Sea corridor, then fractionate internally to sidestep RSPO premium charges, a tactic that trims cost yet demands stringent in-house sustainability audits.

South America shows steady growth as Brazil’s sports-nutrition category broadens and domestic macauba plantations promise future feedstock resilience. Middle East & Africa remain nascent but are opening via medical-nutrition tenders and halal-certified personal-care launches in the Gulf Cooperation Council states. Trade incentives in the African Continental Free Trade Area may foster local fractionation hubs over the next decade, though infrastructure and feedstock availability remain early-stage.

Competitive Landscape

The medium chain triglycerides market exhibits moderately consolidated concentration. The market hosts a blend of vertically integrated agribusinesses and specialized oleochemical players. Wilmar International leverages plantation assets and state-of-the-art refineries to deliver scale; its food-products EBIT rose 77% in H1 2024, aided by robust MCT throughput. KLK Oleo reinforced its European footprint by acquiring Temix Oleo, adding esterification capacity tailored to pharma-grade fractions. Stepan Company markets the NEOBEE line, supported by proprietary purification technology that removes process contaminants while preserving triglyceride integrity.

Mid-tier firms focus on differentiated niches: US-based Bioriginal specializes in turnkey ketogenic sachets, while Germany’s IOI-Oleochemicals offers cGMP-certified pharma excipients. Asian newcomers emphasize cost competitiveness, yet many also invest in RSPO segregated supply to satisfy export buyers. Intellectual-property filings have risen around chain-length optimization and microencapsulation, signaling that process innovation, not just feedstock access, will define long-term advantage.

Medium Chain Triglycerides (MCT) Industry Leaders

Croda International Plc

IOI Oleo GmbH

KLK Oleo

Musim Mas Group

Stepan Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Azelis, one of the leading specialty chemicals and food ingredients innovation service providers, has established a distribution partnership with BASF. The agreement enables Azelis to distribute BASF's Medium Chain Triglyceride (MCT) products, which serve as essential ingredients in bakery, beverage, and other applications.

- April 2023: KLK OLEO completed the acquisition of Temix Oleo. The strategic acquisition strengthens the company's growth objectives through expanded product offerings, enhanced customer reach, and increased product specialization in European operations, which is expected to boost the medium chain triglycerides market growth.

Global Medium Chain Triglycerides (MCT) Market Report Scope

Medium-chain triglycerides (MCTs) are a type of fatty acid derived from coconut oil or palm kernel oil. They are called "medium chain" because they have a shorter chain length than most other fatty acids. These can be used to make dietary supplements, bakery goods, beverages, dairy products, skincare products, and hair care products. Moreover, they can used as an excipient in drug formulations.

The medium chain triglycerides (MCT) market is segmented by form, fatty acid type, application, and geography. By form, the market is segmented into dry and liquid. By fatty acid type, the market is segmented into caprylic acid, capric acid, lauric acid, and caproic acid. By application, the market is segmented into food and beverages, personal care and cosmetics, and other applications (pharmaceuticals, etc.). The report also covers the market size and forecasts for the medium chain triglycerides (MCT) market in 27 countries across major regions. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| Dry |

| Liquid |

| Coconut Oil |

| Palm Kernel Oil |

| Others |

| Caprylic (C8) |

| Capric (C10) |

| Lauric (C12) |

| Caproic (C6) |

| Food and Beverage |

| Personal Care and Cosmetics |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Form | Dry | |

| Liquid | ||

| By Source | Coconut Oil | |

| Palm Kernel Oil | ||

| Others | ||

| By Fatty Acid Type | Caprylic (C8) | |

| Capric (C10) | ||

| Lauric (C12) | ||

| Caproic (C6) | ||

| By Application | Food and Beverage | |

| Personal Care and Cosmetics | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the rapid growth of the medium chain triglycerides market?

Sports-nutrition adoption, ketogenic diet popularity, and expanding pharmaceutical uses are propelling an 8.09% CAGR through 2031.

Which MCT form dominates sales today?

Liquid products account for 77.10% global revenue thanks to superior bioavailability and ease of incorporation into beverages and shots.

Why is caprylic (C8) acid highly valued?

C8 generates the fastest ketone response, supporting cognitive and endurance claims and capturing 65.30% fatty-acid revenue in 2025.

Which region is expanding the quickest?

Asia-Pacific leads with an 8.76% CAGR through 2031, fueled by premium infant-formula demand and rising urban health awareness.

Are alternative lipids a serious threat to MCTs?

Structured fats and microalgae oils offer functional competition, yet entrenched clinical data and keto efficacy preserve MCT advantages for now.

Page last updated on: