Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 11.01 Billion |

| Market Size (2030) | USD 12.75 Billion |

| Growth Rate (2025 - 2030) | 2.98% CAGR |

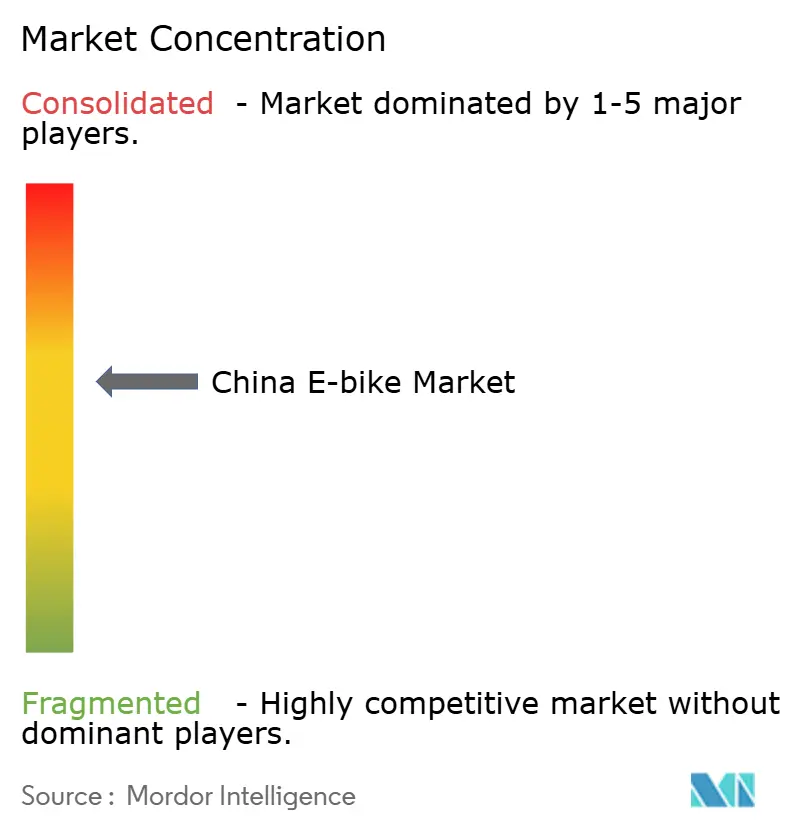

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China E-bike Market Analysis by Mordor Intelligence

The China E-bike Market size is estimated at USD 11.01 billion in 2025, and is expected to reach USD 12.75 billion by 2030, at a CAGR of 2.98% during the forecast period (2025-2030). The modest headline growth conceals a pivot toward higher-specification products, spurred by mandatory GB 43854-2024 lithium battery rules and urban micromobility subsidies that accelerate fleet renewal [1]“Notice on Implementation of GB 43854-2024 Battery Safety Requirements,” Ministry of Industry and Information Technology, miit.gov.cn . Intensifying cost decline in mid-drive motors, strong demand from 15-minute delivery platforms, and corporate commuter benefits keep the China e-bike market on a technology upgrade cycle, even as increased certification costs squeeze sub-USD 500 models. Counterfeit parts and 21700-cell shortages restrain the high-end segment, while export ambitions face anti-dumping barriers in Europe and North America. The convergence of IoT connectivity with e-bike telematics creates new service revenue streams. Yet, grid constraints for public fast-charging cabinets slow the adoption of larger-capacity battery packs in dense downtown districts. Established brands such as Yadea and Aima consolidate share in this environment by leveraging scale for compliance and vertical integration.

Key Report Takeaways

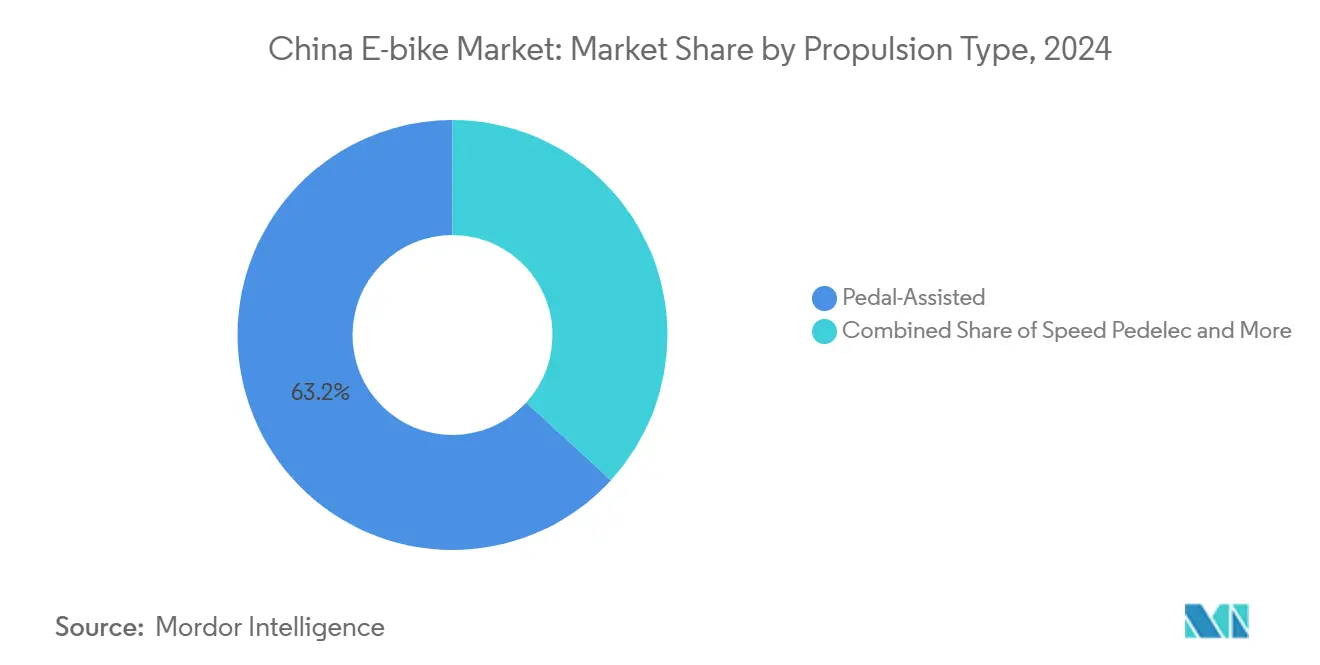

- By propulsion type, pedal-assisted models led with 63.17% of the China e-bike market share in 2024, while speed pedelecs are forecast to expand at a 3.41% CAGR through 2030.

- By application, city/urban use captured 72.35% of the Chinese e-bike market in 2024; cargo/utility is projected to post the fastest 3.33% CAGR to 2030.

- By battery type, lithium-ion commanded 71.15% of the China e-bike market size in 2024 and is set to grow at a 3.38% CAGR between 2025 and 2030.

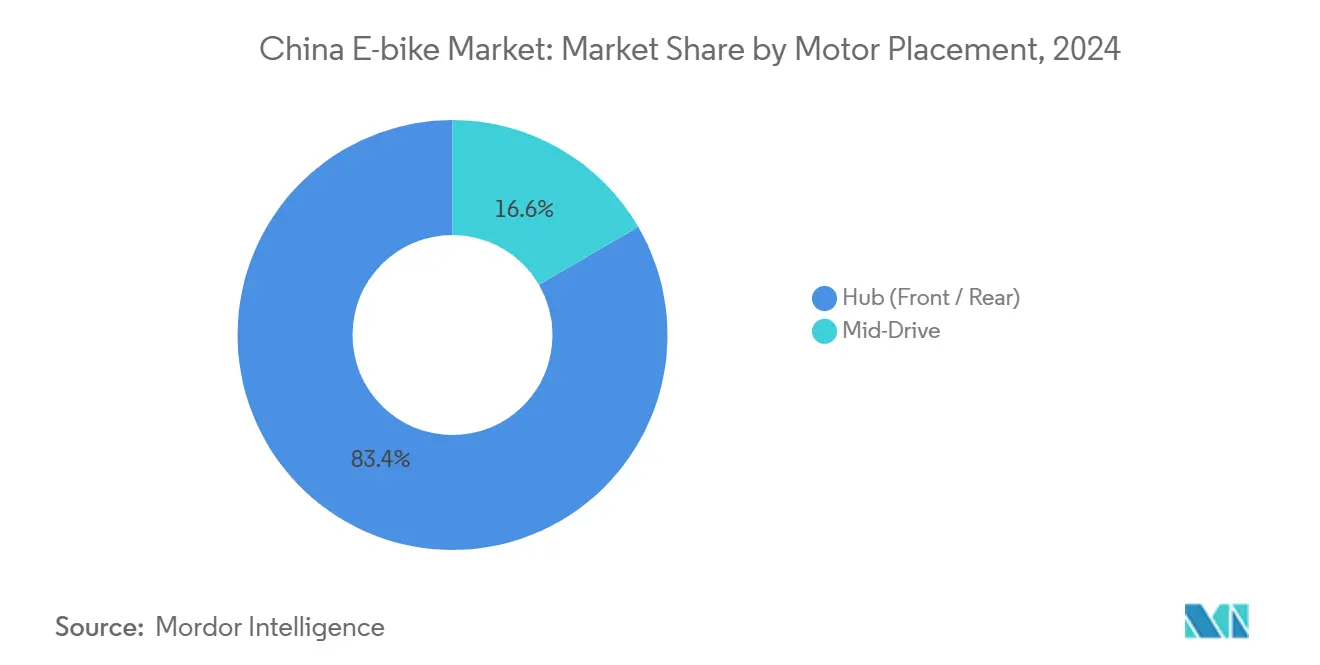

- By motor placement, hub motors held 83.44% share in 2024, whereas mid-drive systems are expected to accelerate at a 3.35% CAGR.

- By drive system, chain drives accounted for 87.83% share in 2024; belt drives are on track for a 3.39% CAGR through 2030.

- By motor power, sub-250 W units represented 61.24% share in 2024, while the 501-600 W band is forecast to climb at a 3.45% CAGR.

- By price band, entry-level models under USD 500 took 43.47% share in 2024; the USD 1,501-2,500 tier is projected to advance at a 3.37% CAGR.

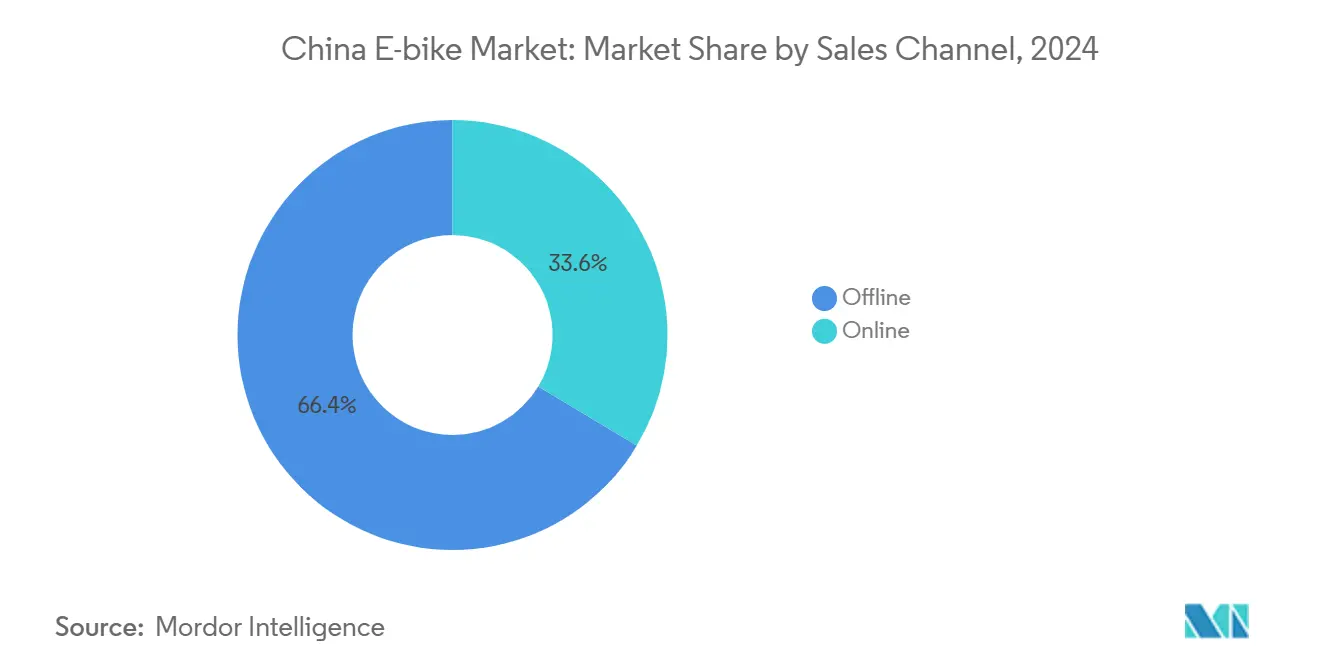

- By sales channel, offline retail controlled a 66.37% share in 2024, whereas online sales are projected to post a 3.46% CAGR.

- By end use, personal and family riding contributed 78.81% share in 2024, while commercial delivery is at a 3.44% CAGR.

China E-bike Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth Of Instant-Commerce Delivery Platforms | +0.9% | Urban centers nationwide, strongest in Beijing, Shanghai, Shenzhen | Short term (≤ 2 years) |

| Government Purchase Incentives | +0.7% | Tier-1 cities, expanding to tier-2 urban centers | Medium term (2-4 years) |

| Rapid Cost Decline In Mid-Drive Motors | +0.5% | Global, with manufacturing concentration in Jiangsu, Zhejiang | Long term (≥ 4 years) |

| Surge In Shared-Ownership Subscription Models | +0.5% | Urban centers, pilot programs in 20+ cities | Medium term (2-4 years) |

| Corporate Commuter-Benefit Programs | +0.2% | Tier-1 cities with corporate concentration | Medium term (2-4 years) |

| Export Demand Pull For High-Spec | +0.2% | Manufacturing hubs in Jiangsu, Zhejiang, Guangdong | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of Instant-Commerce (15-Min) Delivery Platforms

Meituan, with its extensive city presence, and Ele.me, boasting a vast restaurant network, collectively drive significant annual commercial unit sales. This surge anchors a robust demand for cargo-configured frames. Delivery operators, seeking an edge, invest substantial premiums on features like reinforced racks, GPS geo-fencing, and enhanced battery range. These specifications align closely with consumer desires for dependable long-distance performance. Following recent regulatory approval, JD Logistics rolled out three-wheeled e-cargo bikes across numerous municipalities, boosting chassis demand for motor OEMs. While necessary telematics integrations elevate cybersecurity compliance costs, they simultaneously bolster entry barriers for unbranded assemblers. This cargo-driven momentum is reshaping the landscape of the Chinese e-bike market, even as household purchases reach a plateau.

Government Purchase Incentives & Urban Micromobility Policies

Beijing’s national trade-in program shortened replacement cycles, channeling consumer spend toward models certified under GB 43854-2024. Dedicated bike lanes in Beijing and Shanghai surpass 1,200 km, amplifying subsidy impact by giving riders a safer network [2]“Bicycle Lane Network Plan 2025,” Beijing Municipal Transport Commission, bjnews.com.cn . The Ministry of Industry and Information Technology now requires OEMs to prove battery-recycling capacity before product registry, tilting the China e-bike market toward brands with nationwide after-sales networks. As local governments bundle e-bike sharing into public transport cards, ridership data feeds urban-planning algorithms that favor micromobility corridors. Mandatory recycling stipulations add cost pressure but reward vertically integrated players that can close material loops.

Rapid Cost Decline In Mid-Drive Motors & Smart-Drive Electronics

Automation at Changzhou and Wuxi motor plants has cut mid-drive unit cost by one-tenth annually since 2023, shrinking the price delta with hub motors and letting mass-market SKUs adopt premium hardware. Domestic MCU production substituted imports, trimming one-fourth off controller BOM costs and sidestepping United States tech restrictions [3]“Domestic MCU Output Statistics 2024,” China Semiconductor Industry Association, csia.net.cn . IoT capability penetration reached many new NIU models in Q3 2024, normalizing GPS theft-alarm features across numerous bikes. As volume scales, software subscription revenue—fleet analytics, remote diagnosis—emerges as a fresh monetization layer inside the China e-bike market. Component standardization also reduces warranty claims, supporting margins for large-volume brands.

Surge In Shared-Ownership Subscription Models

Shared-ownership subscription programs have moved beyond pilots to active service in more than 20 cities, offering riders app-based access to e-bikes without the burden of an upfront purchase. Monthly fees typically combine insurance, maintenance, and battery-swap privileges, lowering user outlay by roughly one-third compared with buying entry-level models. Fleet operators place bulk orders with compliant OEMs, creating predictable production runs that cushion factories against retail seasonality. Urban regulators support subscriptions because platform telematics enforces parking zones and time limits, reducing roadside clutter and improving traffic flow. High churn to newer hardware every 12 months pushes manufacturers to design modular batteries and quick-release racks that cut refurbishment time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Bottlenecks | -0.7% | Manufacturing centers in Jiangsu, Zhejiang, Guangdong | Medium term (2-4 years) |

| Tightening Fire-Safety Rules | -0.5% | National, with stricter enforcement in tier-1 cities | Short term (≤ 2 years) |

| Counterfeit Component Risk | -0.2% | Secondary cities and rural markets | Long term (≥ 4 years) |

| Grid-Capacity Constraints | -0.2% | Dense urban areas, particularly older city centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Bottlenecks For Premium 21700 Li-Ion Cells

CATL and BYD, two major players in the electric vehicle (EV) sector, are prioritizing their contracts, resulting in significantly extended lead times for e-bike cells. This shift has also driven up unit costs considerably compared to 2023 levels. Additionally, customs checks on imported materials, particularly nickel and cobalt, are lengthening logistics windows. This situation is especially challenging for smaller assemblers who lack the necessary hedging tools. While original equipment manufacturers (OEMs) are on the lookout for substitutes, sodium-ion pilot packs have surfaced as an alternative. However, they still lag behind lithium in terms of energy density. This supply crunch is not only hindering the rollout of high-range models but also moderating the growth of premium price bands in China's e-bike market.

Tightening Fire-Safety Rules On High-Density Battery Housing

GB 43854-2024 mandates OEMs to revamp thermal barriers, resulting in additional costs and extending engineering cycles significantly. Numerous municipalities have now prohibited indoor charging, encouraging residents to opt for outdoor cabinets. These outdoor solutions require landlord approvals, complicating and delaying replacement decisions. Backlogs at CCC labs have substantially increased certification lead-times, causing delays in model launches and leading to higher inventory levels. While these measures may limit immediate sales, they simultaneously purge the Chinese e-bike market of subpar products, bolstering consumer confidence in the process.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Speed Pedelecs Drive Premium Shift

Pedal-assisted units retained a 63.17% share in 2024, anchoring volume demand and keeping the China e-bike market accessible to first-time buyers. Their regulatory alignment with 25 km/h limits sustains street legality and reduces insurance costs. Yet corporate commuter schemes and wider protected lane networks lift appetite for 45 km/h speed pedelecs, the segment with a 3.41% CAGR forecast that injects premium ASPs. OEMs integrate torque sensors and finely graded power maps to stay within GB 17761-2018 caps while giving riders automotive-like acceleration. Fleet buyers specify dual-battery kits to extend range without violating weight limits, an underserved innovation niche. Marketing narratives now emphasize wellness, positioning pedal assist as calorie-burning mobility rather than pure convenience. The shift shapes the China e-bike market as riders balance exercise with commute time, nudging a gradual migration toward higher-spec platforms in prosperous districts.

Due to stricter enforcement, consumer sentiment toward throttle-only bikes cools inside tier-1 city perimeters. Still, it remains lively in peri-urban zones where cargo carts and agricultural errands dominate day-to-day tasks. Speed pedelecs benefit from employer subsidies that cover up to 30% of the purchase price, thereby seeding demand among white-collar workers. Integration of geofencing keeps higher-speed modes disabled in low-speed zones, helping municipal regulators accept the category. The continuous tug-of-war among safety, speed, and fitness functionality ensures propulsion innovation stays central to competitiveness in the Chinese e-bike market.

By Application Type: Cargo Utility Gains Commercial Traction

City and urban riding represented 72.35% of total demand in 2024, sustaining baseline volumes while reinforcing the China e-bike market’s role in daily commutes and errands. Infrastructure additions include dedicated lanes, smart parking posts, and reinforced urban adoption, mainly where local governments restrict motorcycle access. Cargo/utility is forecast to rise 3.33% CAGR as 15-minute delivery services widen their footprint in tier-2 cities. Frames with extended wheelbases, 100 kg payload certification, and swappable battery racks command 30-40% price premiums yet face no shortage of takers among platform operators. Instant-commerce players negotiate long-term supply contracts that cushion OEM order books against retail fluctuations.

Weekend leisure demand propels trekking/mountain into a boutique niche. Sales spike in provinces marketing ecotourism, where rental fleets prefer models equipped with 100 mm suspension forks and IP 67-rated battery housings. Cargo use cases stimulate ancillary service revenue, fleet telematics, predictive maintenance, and battery hot-swap stations, cementing commercial buyers as strategy focal points for brands eyeing stable recurring sales streams within the China e-bike market.

By Battery Type: Lithium-Ion Consolidates Market Position

Lithium-ion packs controlled 71.15% of 2024 shipments and grew at a robust CAGR of 3.38% till 2030, cementing energy density as the decisive attribute in the Chinese e-bike market. Average cell cost fell slightly yearly, widening the gap versus lead-acid alternatives that struggle with weight, charge cycles, and recycling liabilities. Upgraded BMS chips now bundle Bluetooth data links, theft lockouts, and over-the-air firmware that deliver aftermarket revenue through app subscriptions. Regulatory recycling mandates give lithium an edge, formal collection networks reclaim cobalt and nickel at more than four-fifths efficiency, compared with the scattered lead-acid ecosystem.

Alternative chemistries explore niches: sodium-ion pilots for budget fleet operators and LFP variants promising thermal stability in courier cargo rigs. Yet none match lithium for power-to-weight in consumer use cases, preserving its dominance in the Chinese e-bike market. Cell makers build specialized e-bike lines to buffer against auto-sector volatility, and vertical integration by Yadea locks in pack supply for flagship SKUs.

By Motor Placement: Mid-Drive Systems Gain Premium Positioning

Hub motors held an 83.44% market share in 2024 volumes, due to plug-and-play assembly that keeps the China e-bike market price competitive at entry tiers. However, mid-drive units attract enthusiasts and fleet buyers chasing center-of-gravity balance and hill-climb torque, which is why they are growing at a rate of 3.35% until 2030. A 20% cost slide since 2023 makes mid-drive viable for RMB 3,000-5,000, bridging the gap between commuter affordability and performance aspirations. OEMs pair torque sensors with CAN bus controllers that sync flawlessly with multi-speed drivetrains.

Delivery companies note one-fifth energy savings when swapping hub motors for mid-drive, enough to justify the higher upfront spend within 18 months. Shielded electronics help units pass stricter electromagnetic compatibility tests, an unseen but influential purchase criterion in the Chinese e-bike market. As unit economics converge, mid-drive penetration is set to outpace battery or frame upgrades in shaping next-generation ride quality.

By Drive Systems: Belt Drive Innovation Challenges Chain Dominance

Chain drives dominated 87.83% of units in 2024, reflecting commodity pricing and ubiquitous workshop familiarity. Though only a sliver of the Chinese e-bike market, Belt drives hold a 3.39% CAGR outlook by eliminating grease, noise, and rust. OEMs integrate carbon-fiber belts with internal gear hubs to cut maintenance frequency by one-third over two-year cycles. While licensing fees once inflated belt drive BOMs, rising order volumes shrink premiums to closer to one-fourth over chain setups.

Couriers see operational savings, fewer chain swaps, and reduced downtime, offsetting the higher purchase tag. Urban consumer sentiment warms to silent drivetrains that keep office attire clean. Limited after-sales knowledge outside megacities slows penetration, yet digital tutorials and modular replacement kits aim to bridge the skills gap, nudging belt drives into wider recognition across the Chinese e-bike market.

By Motor Power: Higher Wattage Segments Capture Commercial Demand

Sub-250 W motors met regulation in 61.24% of 2024 shipments, anchoring low-speed commuter volume. Nevertheless, cargo fleets gravitate to 501-600 W systems, expected to grow at a 3.45% CAGR, valuing torque for heavy loads over classification simplicity. Municipal pilot zones issue special tags for higher wattage rigs, easing legal barriers. Despite extended duty cycles, thermal-management advances, liquid cooling sleeves, and graphene heat pads keep the temperature within GB/T 18488 limits.

Powerful controllers enhance hill-start capability in Chongqing’s steep streets and maintain 25 km/h speeds under 70 kg payloads. OEMs cap top speed to 35 km/h, aligning with delivery-platform safety policies while sustaining performance perception, opening new revenue channels inside the China e-bike market.

By Price Band: Premium Segments Drive Market Evolution

Models under USD 500 still claim 43.47% of 2024 sales, but their numbers shrink as safety compliance inflates manufacturing cost. The USD 1,501-2,500 tier grows fastest at 3.37% CAGR, bundling lithium packs, app locks, and mid-drive motors. Consumer credit platforms, allied with Alipay and WeBank, spread payments over 24 months, dissolving sticker shock. Ultra-premium SKUs above USD 6,000, while niche, carve branding halo effects that ripple into mid-tier aspiration.

Regulatory audits drive consolidation; sub-scale factories exit rather than retool, handing share to compliant majors. Upward ASP drift elevates revenue even when unit volumes plateau, supporting healthier EBIT margins across the China e-bike market.

By Sales Channel: Online Growth Accelerates Digital Transformation

Brick-and-mortar (offline) dealers commanded 66.37% of 2024 turnover, prized for test rides and on-site servicing in a country where warranty credibility sways purchase decisions. E-commerce, however, shows a 3.46% CAGR glide path as AR model demos and doorstep test-ride vans replicate physical touchpoints. Manufacturers offer buy-online-pick-up-in-store options that keep local service partners in the loop.

Digital marketing via Douyin livestreams converts impulse interest into checkouts, driving 40% of NIU’s new customer acquisitions in 2024. Hybrid logistics factory-direct to city hub, then final-mile by courier cuts last-mile damage claims by 15%, making online a margin-friendly frontier within the China e-bike market.

By End Use: Commercial Applications Reshape Market Dynamics

Personal transport still dominated at 78.81% in 2024, underscoring the cultural fit of e-bikes in urban Chinese life. Commercial delivery, forecast at 3.44% CAGR, injects predictable, large-bundle orders. Fleet operators secure volume discounts and standardized parts, smoothing production planning for OEMs. Integration of telematics APIs into Meituan and Ele.me dispatch dashboards ties hardware to software ecosystems, discouraging brand switching.

Public-sector adoption, postal services, and campus security add institutional prestige, nudging hesitant consumer segments to perceive e-bikes as mainstream, not fringe. Such cross-pollination cements multipurpose positioning inside the Chinese e-bike market.

Geography Analysis

Tier-1 metropolises Beijing, Shanghai, and Shenzhen contributed one-third of 2024 unit demand despite housing only a few of the population, a testament to disposable-income leverage and dense cycling lanes. Premium SKUs embedded with IoT locked in early adoption, reinforcing the perception that the Chinese e-bike market is a vector for tech lifestyle status. Western inland provinces, benefiting from Belt-and-Road logistics nodes, see local governments subsidize charging infrastructure to cut motorcycle emissions, sparking incremental gains even at lower income levels.

Tier-2 cities are set for the strongest growth rates as municipalities upgrade biking grids and enforce motorcycle restrictions, funneling commuters toward compliant e-bikes. Regional regulations diverge: Shanghai mandates plate registration and insurance, while Chengdu tolerates throttle-only rigs within ring roads, shaping localized product mixes. Coastal manufacturing hubs, Jiangsu, Zhejiang, Guangdong, bundle production and consumption, slashing freight costs and accelerating iterative design cycles.

Climate profiles drive technical tweaks: northern provinces order battery warmers for sub-zero winters, while southern coastlines demand anti-corrosion coatings and IP 67 component sealing. Export-oriented factories cluster near Shenzhen ports but channel greater volume domestically after EU anti-dumping tariffs. Data transparency from public bike-lane usage sensors guides urban planners, who increase parking docks, reinforcing local network effects that root the China e-bike market in everyday mobility culture.

Competitive Landscape

In 2024, the leading brands in China's e-bike market collectively accounted for a significant portion of the industry's revenue. Compliance costs increased substantially due to the mandatory CCC certification, pushing many smaller assemblers out of the market. Yadea and Aima are vertically integrating by establishing their own battery lines and motor factories to mitigate supply risks and protect their margins amidst fluctuations in raw material prices. Meanwhile, NIU Technologies is carving out a niche emphasizing innovative connectivity features, such as over-the-air updates and theft recovery, allowing it to command a premium in tier-1 cities.

Tailg and Luyuan are catering to the needs of instant-commerce couriers by offering fleet packages that include telematics dashboards and on-site maintenance vans, ensuring near-perfect uptime. This shift indicates a broader industry trend, from focusing solely on competitive pricing to creating a comprehensive service ecosystem. While international expansion is on the agenda, it's fraught with challenges; for instance, EU anti-dumping duties have necessitated localized assembly partnerships, yet Southeast Asian free-trade agreements offer a silver lining.

As the industry evolves, supply-chain resilience emerges as a critical focus. Companies that manage in-house cell packaging and PCB etching are better positioned to navigate potential shortages, like the challenges associated with specific battery cells. At the same time, brands are diversifying their revenue streams by exploring subscriptions for battery leasing, insurance, and software analytics, countering the pressures on hardware margins. This evolution signals a broader trend in the Chinese e-bike market, with players increasingly positioning themselves as mobility-as-a-service platforms rather than mere vehicle sellers.

China E-bike Industry Leaders

Aima Technology Group Co. Ltd

Jiangsu Xinri E-Vehicle Co. Ltd

NIU Technologies

Shenzhen TAILG Technology Group Co., LTD.

Yadea Group Holdings Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: China issued comprehensive guidelines to tighten enforcement of the new national e-bike safety standards and enhance oversight of battery housing, fire prevention, and recycling requirements.

- July 2025: NIU launched the FXT Ultra 2025 and NXT Ultra 2025 models, which feature auto start/stop, cruise control, and extended-range batteries. This aligns the lineup with updated regulatory thresholds and boosts Q3 2025 sales.

China E-bike Market Report Scope

Pedal Assisted, Speed Pedelec, Throttle Assisted are covered as segments by Propulsion Type. Cargo/Utility, City/Urban, Trekking are covered as segments by Application Type. Lead Acid Battery, Lithium-ion Battery, Others are covered as segments by Battery Type.By Propulsion Type

| Pedal Assisted |

| Speed Pedelec |

| Throttle Assisted |

By Application Type

| Cargo / Utility |

| City / Urban |

| Trekking / Mountain |

By Battery Type

| Lead-Acid Battery |

| Lithium-ion Battery |

| Others |

By Motor Placement

| Hub (Front / Rear) |

| Mid-Drive |

By Drive Systems

| Chain Drive |

| Belt Drive |

By Motor Power

| Less than 250 W |

| 251–350 W |

| 351–500 W |

| 501–600 W |

| More than 600 W |

By Price Band (USD)

| Up to 500 USD |

| 501–800 USD |

| 801–1,000 USD |

| 1,001–1,500 USD |

| 1,501–2,500 USD |

| 2,501–3,500 USD |

| 3,501–6,000 USD |

| 6,001 USD and above |

By Sales Channel

| Online | |

| Offline | Specialized E-Bike Retailers |

| Traditional Bike Shops | |

| Department Stores & Sporting Goods Chains |

By End Use

| Commercial Delivery | Retail & Goods Delivery |

| Food & Beverage Delivery | |

| Service Providers | |

| Personal & Family Use | |

| Institutional | |

| Others |

| By Propulsion Type | Pedal Assisted | |

| Speed Pedelec | ||

| Throttle Assisted | ||

| By Application Type | Cargo / Utility | |

| City / Urban | ||

| Trekking / Mountain | ||

| By Battery Type | Lead-Acid Battery | |

| Lithium-ion Battery | ||

| Others | ||

| By Motor Placement | Hub (Front / Rear) | |

| Mid-Drive | ||

| By Drive Systems | Chain Drive | |

| Belt Drive | ||

| By Motor Power | Less than 250 W | |

| 251–350 W | ||

| 351–500 W | ||

| 501–600 W | ||

| More than 600 W | ||

| By Price Band (USD) | Up to 500 USD | |

| 501–800 USD | ||

| 801–1,000 USD | ||

| 1,001–1,500 USD | ||

| 1,501–2,500 USD | ||

| 2,501–3,500 USD | ||

| 3,501–6,000 USD | ||

| 6,001 USD and above | ||

| By Sales Channel | Online | |

| Offline | Specialized E-Bike Retailers | |

| Traditional Bike Shops | ||

| Department Stores & Sporting Goods Chains | ||

| By End Use | Commercial Delivery | Retail & Goods Delivery |

| Food & Beverage Delivery | ||

| Service Providers | ||

| Personal & Family Use | ||

| Institutional | ||

| Others | ||

Market Definition

- By Application Type - E-bikes considered under this segment include city/urban, trekking, and cargo/utility e-bikes. The common types of e-bikes under these three categories include off-road/hybrid, kids, ladies/gents, cross, MTB, folding, fat tire, and sports e-bike.

- By Battery Type - This segment includes lithium-ion batteries, lead-acid batteries, and other battery types. The other battery type category includes nickel-metal hydroxide (NiMH), silicon, and lithium-polymer batteries.

- By Propulsion Type - E-bikes considered under this segment include pedal-assisted e-bikes, throttle-assisted e-bikes, and speed pedelec. While the speed limit of pedal and throttle-assisted e-bikes is usually 25 km/h, the speed limit of speed pedelec is generally 45 km/h (28 mph).

| Keyword | Definition |

|---|---|

| Pedal Assisted | Pedal-assist or pedelec category refers to the electric bikes that provide limited power assistance through torque-assist system and do not have throttle for varying the speed. The power from the motor gets activated upon pedaling in these bikes and reduces human efforts. |

| Throttle Assisted | Throttle-based e-bikes are equipped with the throttle assistance grip, installed on the handlebar, similarly to motorbikes. The speed can be controlled by twisting the throttle directly without the need to pedal. The throttle response directly provides power to the motor installed in the bicycles and speeds up the vehicle without paddling. |

| Speed Pedelec | Speed pedelec is e-bikes similar to pedal-assist e-bikes as they do not have throttle functionality. However, these e-bikes are integrated with an electric motor which delivers power of approximately 500 W and more. The speed limit of such e-bikes is generally 45 km/h (28 mph) in most of the countries. |

| City/Urban | The city or urban e-bikes are designed with daily commuting standards and functions to be operated within the city and urban areas. The bicycles include various features and specifications such as comfortable seats, sit upright riding posture, tires for easy grip and comfortable ride, etc. |

| Trekking | Trekking and mountain bikes are special types of e-bikes that are designed for special purposes considering the robust and rough usage of the vehicles. These bicycles include a strong frame, and wide tires for better and advanced grip and are also equipped with various gear mechanisms which can be used while riding in different terrains, rough grounded, and tough mountainous roads. |

| Cargo/Utility | The e-cargo or utility e-bikes are designed to carry various types of cargo and packages for shorter distances such as within urban areas. These bikes are usually owned by local businesses and delivery partners to deliver packages and parcels at very low operational costs. |

| Lithium-ion Battery | A Li-ion battery is a rechargeable battery, which uses lithium and carbon as its constituent materials. The Li-Ion batteries have a higher density and lesser weight than sealed lead acid batteries and provide the rider with more range per charge than other types of batteries. |

| Lead Acid Battery | A lead acid battery refers to sealed lead acid battery having a very low energy-to-weight and energy-to-volume ratio. The battery can produce high surge currents, owing to its relatively high power-to-weight ratio as compared to other rechargeable batteries. |

| Other Batteries | This includes electric bikes using nickel–metal hydroxide (NiMH), silicon, and lithium-polymer batteries. |

| Business-to-Business (B2B) | The sales of e-bikes to business customers such as urban fleet and logistics company, rental/sharing operators, last-mile fleet operators, and corporate fleet operators are considered under this category. |

| Business-to-Customers (B2C) | The sales of electric scooters and motorcycles to direct consumers is considered under this category. The consumers acquire these vehicles either directly from manufacturers or from other distributers and dealers through online and offline channel. |

| Unorganized Local OEMs | These players are small local manufacturers and assemblers of e-bikes. Most of these manufacturers import the components from China and Taiwan and assemble them locally. They offer the product at low cost in this price sensitive market which give them advantage over organized manufacturers. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Dockless e-Bikes | Electric bikes that have self-locking mechanisms and a GPS tracking facility with an average top speed of around 15mph. These are mainly used by bike-sharing companies such as Bird, Lime, and Spin. |

| Electric Vehicle | A vehicle which uses one or more electric motors for propulsion. Includes cars, scooters, buses, trucks, motorcycles, and boats. This term includes all-electric vehicles and hybrid electric vehicles |

| Plug-in EV | An electric vehicle that can be externally charged and generally includes all-electric vehicles as well as plug-in hybrids. In this report we use the term for all-electric vehicles to differentiate them from plug-in hybrid electric vehicles. |

| Lithium-Sulphur Battery | A rechargeable battery that replaces the liquid or polymer electrolyte found in current lithium-ion batteries with sulfur. They have more capacity than Li-ion batteries. |

| Micromobility | Micromobility is one of the many modes of transport involving very-light-duty vehicles to travel short distances. These means of transportation include bikes, e-scooters, e-bikes, mopeds, and scooters. Such vehicles are used on a sharing basis for covering short distances, usually five miles or less. |

| Low Speed Electric Vehicls (LSEVs) | They are low speed (usually less than 25 kmph) light vehicles that do not have an internal combustion engine, and solely use electric energy for propulsion. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms