Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

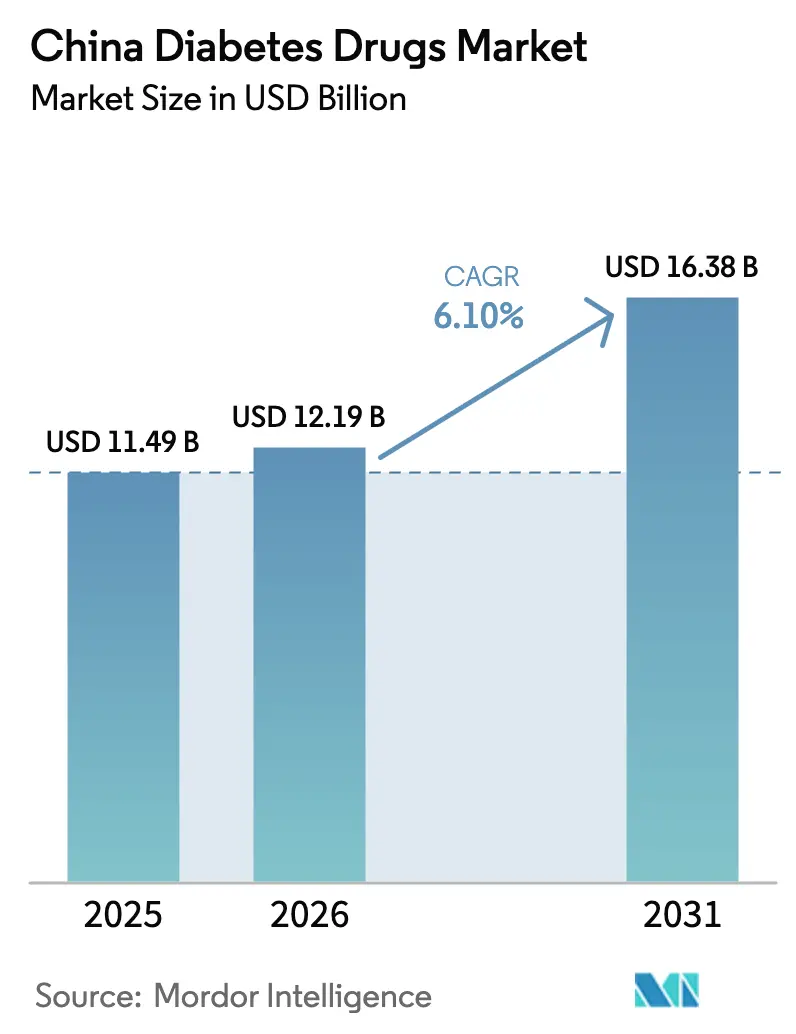

| Base Year Market Size (2025) | USD 11.49 Billion |

| Market Size (2026) | USD 12.19 Billion |

| Market Size (2031) | USD 16.38 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Diabetes Drugs Market Analysis by Mordor Intelligence

China diabetes drugs market size in 2026 is estimated at USD 12.19 billion, growing from 2025 value of USD 11.49 billion with 2031 projections showing USD 16.38 billion, growing at 6.10% CAGR over 2026-2031. A confluence of population aging, rising obesity, and earlier disease onset is expanding treatment demand, while government reimbursement reforms and domestic manufacturing capacity are redefining pricing power and competitive dynamics. Rapid uptake of next-generation GLP-1 and dual-agonist therapies is eroding insulin exclusivity, and digital prescription channels are redirecting volume away from hospitals toward retail and online outlets. Venture funding in peptide CDMO facilities, coupled with a pipeline of more than fifteen semaglutide biosimilars, underscores how local cost advantages and regulatory support are shaping product launches. Multinational companies respond by in-licensing Chinese assets and investing in local plants, signaling that the China diabetes drugs market will remain a focal point for global strategy.

Key Report Takeaways

- By drug class, insulins led with 46.02% of China diabetes drugs market share in 2025, whereas non-insulin injectables are advancing at a 10.12% CAGR through 2031.

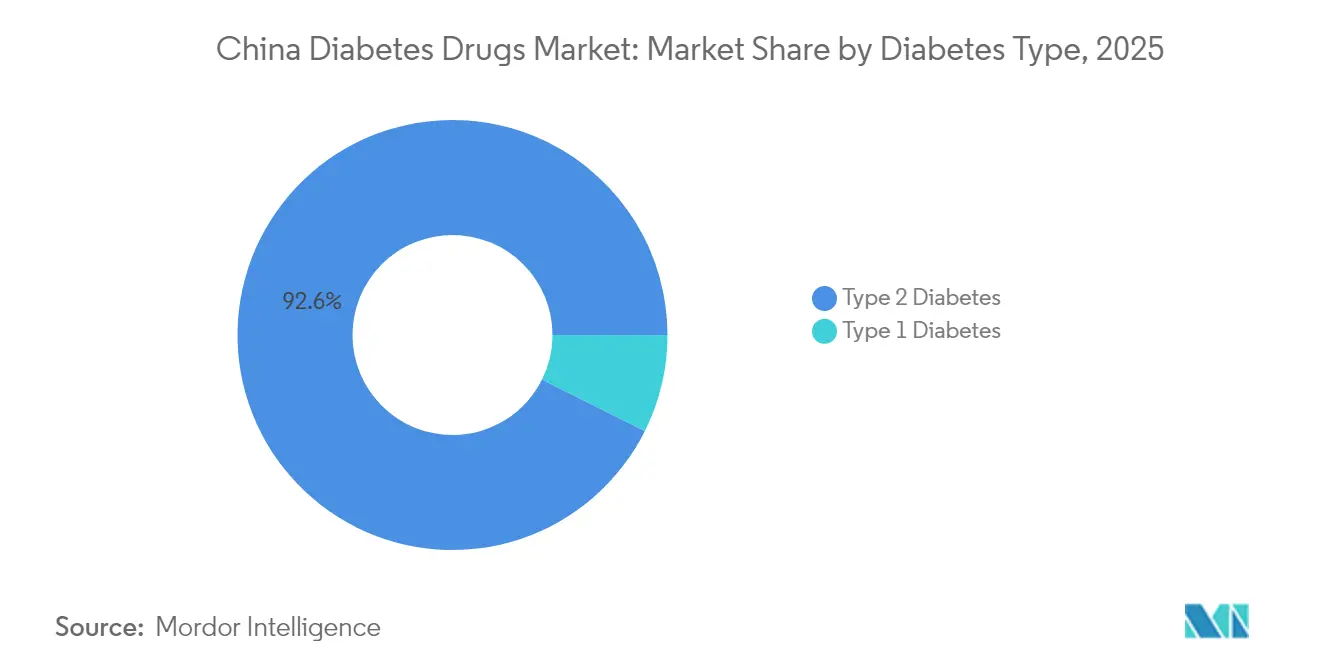

- By diabetes type, Type 2 therapies captured 92.64% of the China diabetes drugs market size in 2025 and are expanding at 7.78% CAGR to 2031.

- By drug origin, branded agents controlled 71.95% of the market in 2025, yet generics and biosimilars are growing at an 8.39% CAGR.

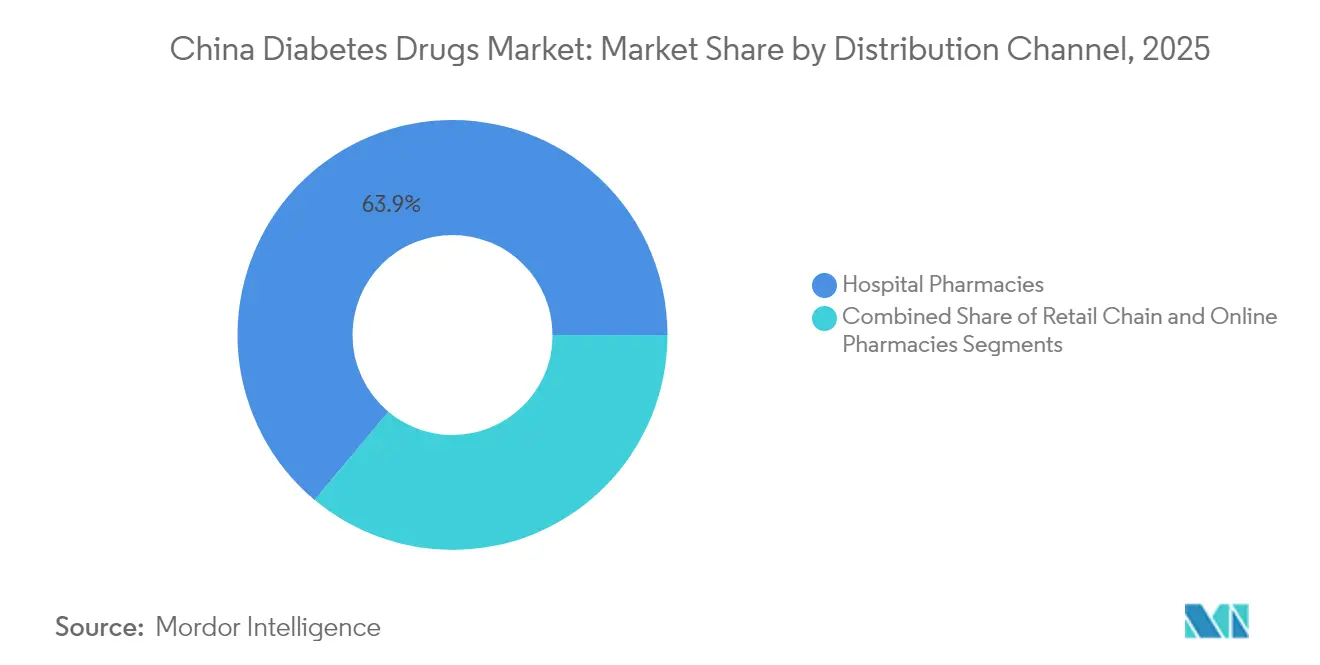

- By distribution channel, hospital pharmacies held 63.92% revenue share in 2025, while online and O2O platforms post the fastest 9.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Diabetes Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Rise in Diabetes prevalence & Earlier disease onset | 1.8% | National, with highest impact in urban centers Beijing, Shanghai, Tianjin | Long term (≥ 4 years) |

| Inclusion of more anti-diabetics in NRDL & volume-based procurement | 1.2% | National, with accelerated adoption in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Surge in GLP-1/Tirzepatide launches and domestic biosimilars | 2.1% | National, with early adoption in major metropolitan areas | Medium term (2-4 years) |

| Hospital-to-retail prescription outflow under "dual-invoice" policy | 0.7% | National, with stronger impact in developed provinces | Short term (≤ 2 years) |

| Internet hospitals & e-pharmacy platforms boosting adherence | 0.9% | National, with higher penetration in digitally advanced regions | Medium term (2-4 years) |

| Venture & PE funding for peptide CDMO capacity in China | 0.5% | Concentrated in pharmaceutical manufacturing hubs Jiangsu, Shanghai, Guangdong | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid rise in diabetes prevalence & earlier disease onset

Prevalence climbed to 15.88% in 2023 and could reach 29.1% by 2050 if current patterns persist.[1]Yu-Chang Zhou, “The National and Provincial Prevalence and Non-Fatal Burdens of Diabetes in China from 2005 to 2023 with Projections of Prevalence to 2050,” Military Medical Research, mmrjournal.biomedcentral.comUrban youth are being diagnosed earlier, extending lifetime demand for medicine and reshaping portfolio priorities toward long-term metabolic control. Beijing, Shanghai, and Tianjin report the highest incidence, yet rural enclaves are closing the gap as lifestyle and screening converge. This epidemiological swing forces firms to widen access beyond tertiary hospitals and design patient-support tools that span decades of therapy. Direct medical expenditure has already hit USD 165.3 billion, sharpening payer focus on drugs that deliver durable HbA1c control at sustainable prices.

Inclusion of more anti-diabetics in NRDL & volume-based procurement

The 2024 NRDL talks cleared 117 diabetes drugs with an 84.6% success rate, cutting median insulin prices by 42.08% and shifting share toward cost-effective brands.[2]Jing Yuan, “National Volume-Based Procurement (NVBP) Exclusively for Insulin: Towards Affordable Access in China and Beyond,” BMJ Global Health, gh.bmj.comStandardized reimbursement compresses margins for premium imports but simultaneously drives volume for listed molecules by reducing patient co-pays. Domestic manufacturers benefit disproportionately; 71% of newly listed agents originated from Chinese firms. For multinationals, survival hinges on differentiating via novel mechanisms or fixed-dose combinations that escape bulk-purchase ceilings.

Surge in GLP-1/tirzepatide launches and domestic biosimilars

Tirzepatide obtained NMPA clearance in May 2024 and entered clinics in January 2025 at CNY 1,758 per box . Semaglutide biosimilar filings from Hangzhou Jiuyuan, Boan Biotech, and others signal a rush to capture demand once patents lapse in 2026. Gan & Lee’s GZR18 reduced HbA1c by up to 2.32%, surpassing semaglutide’s 1.60% in head-to-head data. Competitive pricing and local supply chain heft are poised to redirect scripts toward domestic injectables, intensifying innovation cycles for originators.

Hospital-to-retail prescription outflow under dual-invoice policy

Uniform invoicing rules let physicians transmit electronic scripts to external dispensaries, breaking hospitals’ stranglehold on chronic-care prescriptions. Patients increasingly fill orders at chain pharmacies and online storefronts, prompting drug makers to reinforce retail relationships and invest in last-mile logistics. Provinces such as Guangdong and Zhejiang, where medical ecommerce is mature, are witnessing double-digit prescription migration rates. Manufacturers with omnichannel capability enjoy higher refill adherence and broader reach into self-pay segments supported by commercial insurance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin squeeze from successive NRDL price cuts | -1.4% | National, with stronger impact on multinational corporations | Medium term (2-4 years) |

| Intensifying safety scrutiny of long-term GLP-1 use | -0.8% | National, with heightened regulatory oversight in major cities | Long term (≥ 4 years) |

| Supply-chain bottlenecks for injectable-grade peptides | -0.6% | Concentrated in manufacturing regions, affecting global supply | Short term (≤ 2 years) |

| Physician inertia toward newer drug classes in lower-tier cities | -0.4% | Rural and lower-tier cities with limited specialist access | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Margin squeeze from successive NRDL price cuts

Repeated reimbursement rounds are driving a race to the bottom, with some imported agents reporting exit discussions due to unsustainable economics. Companies must localize production or innovate out of commoditization by bundling devices, apps, or combination regimens that justify premiums. Smaller firms lacking scale are prime acquisition targets as consolidation accelerates.

Intensifying safety scrutiny of long-term GLP-1 use

Reports of cholestatic hepatitis and pancreatitis have triggered extensive pharmacovigilance audits. NMPA reviewers now request larger real-world evidence packages and longer follow-up, extending time-to-market. Prescribers likewise temper enthusiasm, reserving powerful dual agonists for patients with lower cardiovascular or hepatic risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Non-insulin Injectables Drive Innovation

Non-insulin injectables account for 31.34% of 2025 revenue yet deliver the fastest 10.12% CAGR, reflecting strong payor acceptance once NRDL listing is secured. Insulin still holds the largest 46.02% slice of the China diabetes drugs market share, but its single-digit volume growth contrasts sharply with double-digit uptake of GLP-1 and dual agonists. Tirzepatide’s CNY 1,758 pricing undercuts earlier GLP-1 agents while showing over 20% weight loss efficacy, positioning it for rapid formulary wins. Oral DPP-4 inhibitors and SGLT-2 agents remain important entry therapies, often combined with GLP-1 injectables in advanced cases. Peptide capacity expansions by WuXi STA and Aurisco enable domestic suppliers to lower fill-finish costs, reinforcing competitiveness. Combination pens that co-formulate basal insulin with GLP-1 analogues are entering trials, promising simplified regimens and extended patent life. Because most new biologic approvals originate locally, domestic firms now own significant leverage during NRDL negotiations.

Sequential innovation is shifting clinical practice away from glycemic control alone toward holistic metabolic improvement. Many endocrinologists now start overweight patients on GLP-1 injectables earlier, a practice that could widen the China diabetes drugs market size for non-insulin products by an extra USD 2.62 billion through 2031. Meanwhile, insulin makers reposition ultra-rapid and time-in-range advantages to defend share. The pivot places pressure on production lines to flex between human insulin, analogues, and incretin mimetics to balance risk and sustain utilization.

By Diabetes Type: Type 2 Dominance Intensifies

Type 2 therapies generate 92.64% of 2025 sales and are forecast to expand at a 7.78% CAGR. Younger onset and higher obesity rates extend lifetime drug use, meaning even marginal improvements in adherence translate into substantial incremental revenue. Type 1 patients, though fewer, require complex multi-dose daily regimens and continuous glucose monitoring, fostering demand for sensor-integrated insulin delivery systems. Tonghua Dongbao’s CNY 350 million insulin plant upgrade aims to secure domestic supply for both groups, hedging against import disruptions.

Polypharmacy is common: peripheral neuropathy sufferers consume an average of 4.7 active agents versus 3.77 for uncomplicated patients.Add-on antiplatelet and lipid-lowering drugs often come from the same manufacturers, giving them cross-selling advantages. As complication management rises in profile, companies that bundle cardiometabolic solutions around GLP-1 anchors will broaden their footprint within the China diabetes drugs market. Population-scale remote monitoring pilots in Shanghai suggest HbA1c can be trimmed 0.45% when tele-coaching is offered, improving outcomes for both Type 2 and insulin-dependent cohorts.

By Drug Origin: Biosimilar Momentum Builds

Branded drugs still command 71.95% of spending, yet their volume edge is eroding as biosimilar pipelines mature. The segment holding the largest China diabetes drugs market size is forecast to cede 8-10 percentage points to generics by 2031, especially after semaglutide patents expire. Hangzhou Jiuyuan’s first-to-file semaglutide biosimilar and Boan’s dulaglutide copycat highlight aggressive timelines. Gan & Lee’s GZR18 Phase III win over Ozempic catalyzed investor confidence, and the drug is now positioned for NRDL entry in the 2026 cycle.

Pricing pressure accelerates brand erosion; median discounts for biosimilar insulins sit at 35%, while GLP-1 copies are expected to launch 20–30% below innovator tags. To defend value, originators emphasize device convenience (auto-retracting needles, smaller volumes), real-world cardiovascular data, and potential obesity co-indications. Domestic contenders exploit short supply chains to guarantee stock during NRDL rollouts, securing prescriber trust and patient loyalty. Over time, biosimilar penetration will widen formulary breadth but compress the revenue curve, compelling the China diabetes drugs industry to pivot toward first-in-class assets.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies accounted for 63.92% of 2025 turnover, yet the dual-invoice system and electronic prescription law are enabling retail and online sectors to grow at 9.21% CAGR. In pilot provinces, up to 40% of repeat scripts for GLP-1 analogues are now filled through e-pharmacy platforms that deliver next-day nationwide. Chain pharmacies strengthen their bargaining power by integrating telehealth booths, allowing onsite video consults that convert immediately into pharmacy sales.

Online traffic spikes when new drugs launch but remain excluded from public insurance; self-pay patients often discover products through social media, then purchase via cross-border channels until domestic supply stabilizes. Commercial insurers seize the gap by adding high-profile obesity-adjacent drugs to rider packages, fueling retail volume. For manufacturers, omnichannel success requires coordinated sample distribution, KOL livestreams, and AI-driven adherence reminders. As these elements synchronize, the China diabetes drugs market size derived from non-hospital channels could double from today’s USD 4.15 billion baseline by 2031.

Geography Analysis

Tier-1 municipalities—Beijing, Shanghai, and Tianjin—concentrate one-quarter of national spending, driven by higher disposable income and early adoption of injectables. Provincial bulk procurement equalizes list prices, but hospital formularies in wealthier regions still prioritize novel agents, lifting penetration rates. The eastern seaboard’s digital maturity fosters heavy use of internet hospitals, where up to 60% of follow-up insulin titrations occur virtually. Central and western provinces lag in endocrinologist density, translating into slower uptake of GLP-1 drugs; however, improved 4G coverage and lower device prices are narrowing the gap.

Manufacturing hubs in Jiangsu, Shanghai, and Guangdong give local firms logistical advantages, including reduced cold-chain transit times. Eli Lilly’s USD 212 million Suzhou upgrade and Sanofi’s EUR 1 billion Beijing insulin plant reflect a strategic pivot to “in-China-for-China” production that hedges against geopolitical shocks. API bottlenecks in inland Sichuan briefly constrained peptide yields in 2024, highlighting the need for multi-site redundancy.

Reimbursement pilots differ by region: Zhejiang tests outcome-based contracts that withhold 5% of payment until HbA1c goals are met, whereas Hainan’s Free Trade Port permits accelerated importation of unapproved foreign drugs under medical tourism schemes. These heterogeneities compel marketers to segment launch strategies by province, tailoring educational outreach to local prescriber norms.

Competitive Landscape

Competition is moderate but trending toward fragmentation. The top five manufacturers controlled about 48% of 2024 revenue, down from 53% three years earlier. Gan & Lee secured the second-highest insulin tender share by aligning pricing with NRDL ceilings while delivering clinical data superior to imported analogues. United Laboratories licensed UBT251, a triple receptor agonist, to Novo Nordisk for USD 2 billion, showing how domestic innovation is drawing global capital.

Multinationals still dominate R&D pipelines but are partnering locally to de-risk. Merck’s USD 2 billion pact with Hansoh Pharma grants co-development rights for an oral GLP-1 compound that leverages Hansoh’s Haimen plant for end-stage production. Meanwhile, Chinese CDMOs scale up peptide synthesis that supports both branded and biosimilar launches.

Strategic focus is pivoting from standalone drug efficacy to service-oriented ecosystems. Companies bundle glucose meters, apps, and nutritional counseling to differentiate products facing price ceilings. Venture-backed start-ups explore microneedle patches and once-monthly injectables, aiming to leapfrog current weekly standards. Patent cliffs, cost containment, and fast-track regulatory pathways ensure that out-licensing, M&A, and co-marketing deals will remain frequent as firms jockey for share within the China diabetes drugs market.

China Diabetes Drugs Industry Leaders

Eli Lilly

Sanofi

Novo Nordisk

Gan & Lee

Tonghua Dongbao

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Shanghai Yinnuo Pharmaceutical Technology obtained NMPA approval for Isu-Paglutide α, a long-acting GLP-1 agonist for controlling blood glucose in Type 2 diabetes.

- January 2025: CSPC Ouyi Pharmaceutical received NMPA clearance for Prusogliptin Tablets after a 623-day review, marking a new Class 1 small-molecule entry.

- May 2024: Eli Lilly initiated national launch of Mounjaro (tirzepatide) at CNY 1,758 per box; the product is not yet in the public insurance catalog.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China diabetes drugs market as the total value of prescription and pharmacy-dispensed medicines formulated for blood-glucose control in type 1 and type 2 patients. Products covered include insulins, oral antihyperglycemics, and non-insulin injectables distributed through hospital, retail, and online channels.

Scope Exclusions: Devices such as glucometers, insulin pumps, test strips, and purely diagnostic reagents are excluded.

Segmentation Overview

- By Drug Class

- Insulins

- Oral Anti-diabetic Drugs

- Non-Insulin Injectables (GLP-1, Amylin, GIP/GLP-1)

- Combination Drugs

- By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

- By Drug Origin

- Branded

- Generic / Biosimilar

- By Distribution Channel

- Hospital Pharmacies

- Retail Chain Pharmacies

- Online Pharmacies & O2O Platforms

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with endocrinologists, hospital pharmacists, provincial tender officials, and leading e-pharmacy executives across Tier 1, Tier 2, and Tier 3 cities. These discussions validated uptake rates for GLP-1 receptor agonists, gauged price pass-through after volume-based procurement, and highlighted regional formulary access gaps that secondary data alone could not resolve.

Desk Research

We built the evidence base from open sources such as the National Medical Products Administration approvals log, International Diabetes Federation prevalence surveys, National Health Commission reimbursement circulars, China National Bureau of Statistics demographic tables, and PubMed-indexed clinical journals. Company filings and investor presentations enriched pricing insights, while D&B Hoovers supplied revenue splits that anchor class-level sales. These references provided incidence curves, policy inflection points, and ceiling price data that guide our baseline. The sources named illustrate the breadth tapped; numerous additional public datasets aided further checks and clarifications.

Market-Sizing & Forecasting

A top-down construct converts diagnosed prevalence by age band into treated patient pools, multiplies each pool by class-specific average daily dose and annual therapy price, and is then benchmarked against sampled manufacturer sales and channel audits to fine-tune totals. Key variables tracked include diagnosed prevalence, treatment initiation share, magnitude of procurement price cuts, branded-to-biosimilar mix, and online pharmacy penetration. Multivariate regression projects every driver to 2030, while scenario analysis is applied wherever guidelines or reimbursement rules are poised to shift. When bottom-up samples show gaps, moving averages from three-year growth corridors bridge the shortfall.

Data Validation & Update Cycle

Outputs pass automated variance checks against shipment data and hospital purchase records before a two-step analyst review. Reports refresh each year, with interim updates triggered by major tenders, pivotal approvals, or material public-health events.

Why Mordor's China Diabetes Care Drugs Baseline Inspires Confidence

Published estimates diverge because firms vary product scope, price assumptions, and refresh cadence.

Key Gap Drivers: Our work reports net prescription spend after volume-based procurement, values the market in current-year US dollars, and refreshes annually. Other publishers may bundle devices, apply ex-factory prices, or rely on older exchange rates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.49 B (2025) | Mordor Intelligence | - |

| USD 12.34 B (2024) | Regional Consultancy A | Includes devices and uses ex-factory prices before rebates |

| USD 7.85 B (2025) | Trade Journal B | Omits non-insulin injectables and applies conservative patient coverage |

| USD 9.60 B (2023) | Global Consultancy C | Uses 2023 exchange rate and projects forward without annual refresh |

By anchoring on transparent scope choices, regularly updated drivers, and multi-source validation, Mordor Intelligence delivers a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the China diabetes drugs market?

The market is valued at USD 12.19 billion in 2026 and is projected to reach USD 16.38 billion by 2031.

Which drug class is growing fastest in China?

Non-insulin injectables, led by GLP-1 and dual-agonist therapies, are expanding at a 10.12% CAGR to 2031.

How significant is Type 2 diabetes in market demand?

Type 2 therapies make up 92.64% of 2025 revenue and are growing at 7.78% CAGR, reflecting earlier onset and rising obesity.

How are NRDL policies affecting drug prices?

Volume-based procurement linked to the NRDL cut median insulin prices by 42.08%, squeezing margins but boosting access.

Why are biosimilars gaining traction?

Patent expirations and expanded peptide manufacturing capacity are enabling domestic biosimilar launches at discounts of 20–35%, eroding branded share.

What role do online pharmacies play?

Hospital volumes still dominate, but e-pharmacy and O2O channels are growing at 9.21% CAGR as electronic prescriptions and retail insurance coverage expand.

Page last updated on: