Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

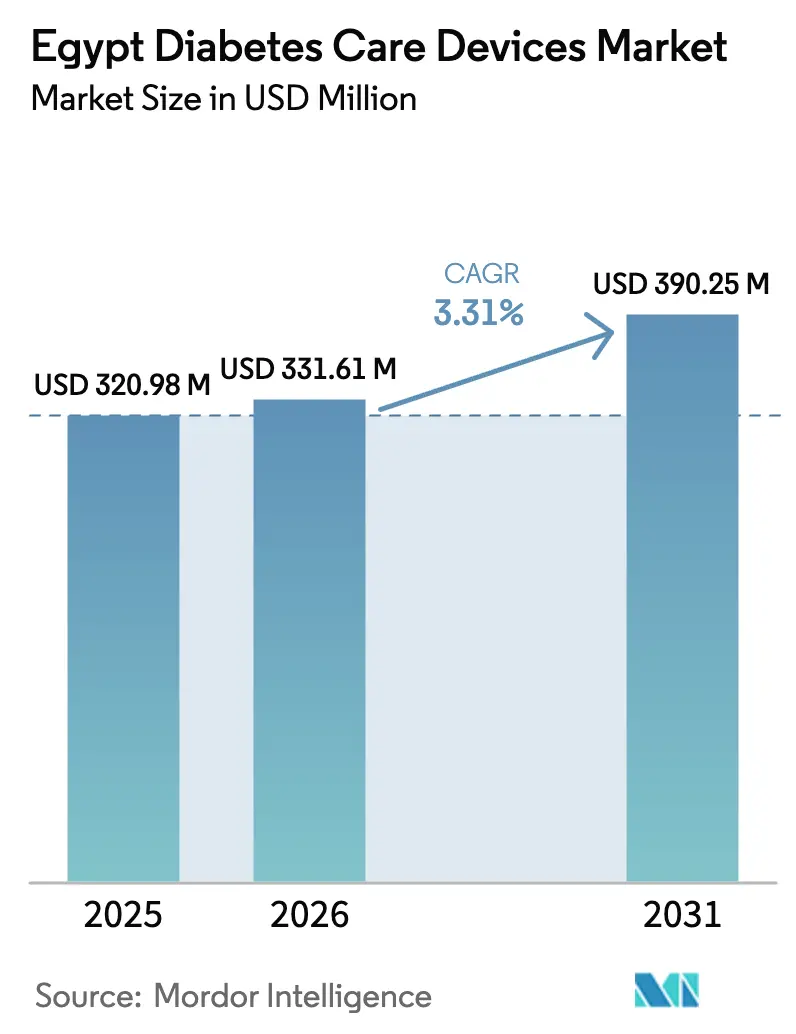

| Base Year Market Size (2025) | USD 320.98 Million |

| Market Size (2026) | USD 331.61 Million |

| Market Size (2031) | USD 390.25 Million |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Diabetes Care Devices Market Analysis by Mordor Intelligence

The Egypt diabetes care devices market size was valued at USD 320.98 million in 2025 and estimated to grow from USD 331.61 million in 2026 to reach USD 390.25 million by 2031, at a CAGR of 3.31% during the forecast period (2026-2031). This performance reflects a delicate balance between wider health-insurance coverage, rapid urbanization, and persistent affordability constraints. The Universal Health Insurance (UHI) roll-out is enlarging the reimbursable patient base, while government price caps on insulin pens are unlocking demand for ancillary consumables. Multinational technology leaders continue to dominate premium segments, but state-backed localization incentives are drawing local producers into high-volume categories, gradually reshaping competitive cost structures. Digital payments and rising smartphone use are opening new direct-to-patient channels, although counterfeit test strips and fragmented reimbursement threaten to erode consumer confidence and curb testing frequency. Overall, the Egypt diabetes care devices market is expected to post steady, mid-single-digit growth as stakeholders converge on affordability, localization, and culturally-aligned digital solutions.

Key Report Takeaways

- By device type, Monitoring Devices led with 62.34% revenue share in 2025; Management Devices are projected to advance at a 3.93% CAGR through 2031.

- By patient type, Type-2 Diabetes accounted for 81.02% of the Egypt diabetes care devices market share in 2025, while the segment is forecast to grow at 5.19% CAGR to 2031.

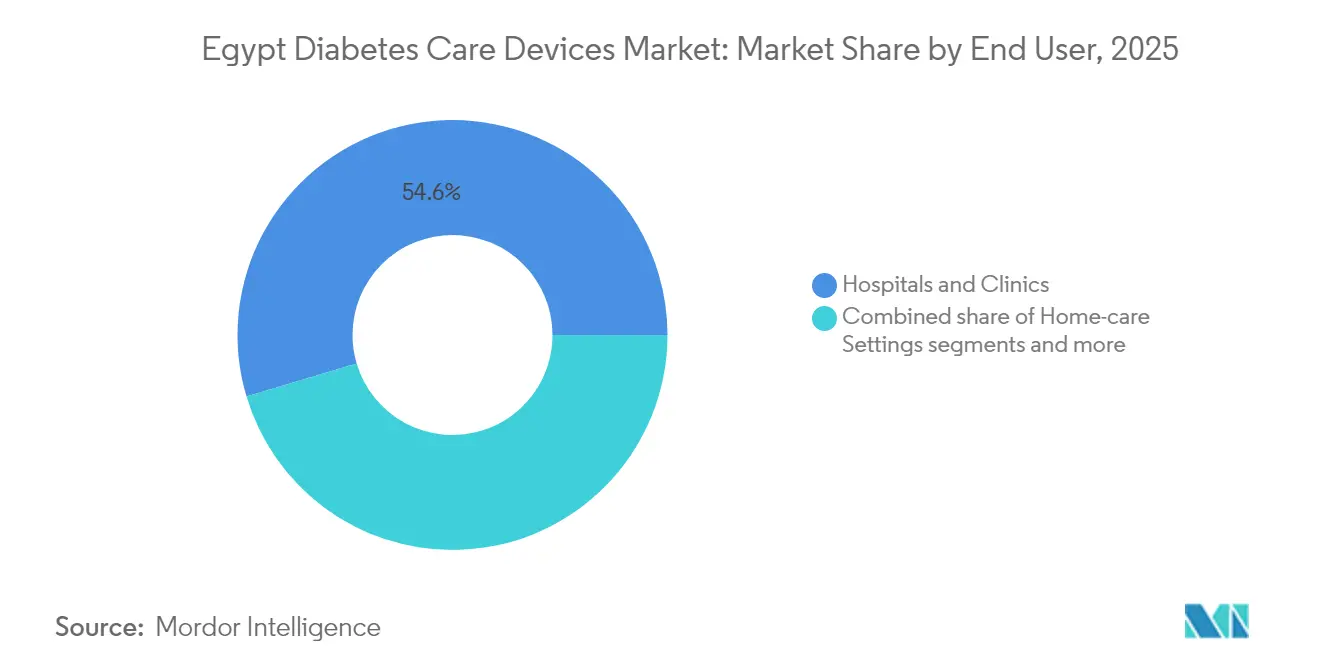

- By end-user, Hospitals & Clinics commanded 54.62% of the Egypt diabetes care devices market size in 2025; Home-care Settings are growing fastest at a 4.72% CAGR between 2026 and 2031.

- By distribution channel, Retail Pharmacies held 51.44% share in 2025, whereas Online Pharmacies are set to record the highest CAGR at 5.11% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Diabetes Care Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Health Insurance Expansion Enabling Reimbursement for SMBG & CGM | +0.8% | National, with early gains in urban centers | Medium term (2-4 years) |

| Surge in Urban Obesity Rates in Greater | +0.6% | Urban centers, particularly Greater Cairo and Alexandria | Long term (≥ 4 years) |

| Proliferation of Private Diabetes Centers Adopting Insulin Pumps | +0.4% | Urban centers, primarily Cairo, Alexandria, and Giza | Medium term (2-4 years) |

| Government-Capped Insulin Pen Prices Catalyzing Pen Needle Uptake | +0.5% | National | Short term (≤ 2 years) |

| Mobile Wallet & E-Pharmacy Growth Fuelling Online Strip Sales | +0.3% | Urban centers with digital infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National Health Insurance expansion supports SMBG & CGM

Egypt’s UHI scheme is methodically extending chronic-disease benefits from Port Said to new governorates, creating first-time reimbursement pathways for self-monitoring blood glucose (SMBG) meters and, in select cases, continuous glucose monitoring (CGM) systems. Digital interoperability built into the insurance platform allows remote data uploads, enabling physicians to tailor dosage adjustments and flag high-risk patterns early[1]Source: Hesham Diana, “Sustainability and Resilience in the Egyptian Health System,” World Economic Forum, WEFORUM.ORG . Uptake calculations show a 15-20% jump in device utilization in newly covered areas, with middle-income households posting the sharpest acceleration. By normalizing reimbursement, the initiative is expected to lift the Egypt diabetes care devices market beyond purely out-of-pocket demand and smooth seasonal spending swings tied to household income cycles.

Escalating urban obesity rates

Half of Egyptian men and up to 80% of women in large cities now qualify as overweight or obese, a trend that is strongly correlated with Type-2 diabetes onset. Co-existing hepatitis C infections—prevalent in roughly 15% of adults—create compounded metabolic stress, prompting clinicians to recommend more granular glucose tracking such as CGM. Healthcare providers increasingly bundle test strips, lancets, and sensors into starter kits for newly diagnosed obese patients, pushing average per-patient spend well above the national mean. The Egypt diabetes care devices market therefore benefits from a widening base of urban users who require frequent monitoring and closer therapeutic oversight.

Private diabetes centers adopting insulin pumps

Public-private diabetes centers are multiplying in Cairo, Alexandria, and Giza, often operating under concessionary land or tax deals that accelerate breakeven periods. These facilities are standardizing advanced therapies, with real-world trials of the MiniMed 780G showing time-in-range values exceeding 70% during Ramadan fasting . Such outcomes are persuading payers and physicians to revisit pump protocols for complex cases previously managed with multiple daily injections. The centers also train staff in Arabic-language dosing algorithms, increasing technology acceptance among patients who had viewed pump therapy as culturally or operationally inaccessible. The mid-term ripple effect boosts both algorithm-enabled pumps and allied consumables across the broader Egypt diabetes care devices market.

Mobile-wallet adoption and e-pharmacies

Digital payment transactions handled by Vodafone Cash and Fawry scaled above the 100 million mark in 2025, reducing friction in online health-product purchasing. Specialized e-pharmacies now offer subscription packages that home-deliver test strips at discounts funded by small monthly fees. Early analytics show Type-1 adolescents increasing test-strip adherence by 15-20% under these models, reinforcing the business case for data-driven, direct-to-consumer replenishment. The Egypt diabetes care devices market is thus evolving toward predictive restocking and usage-based pricing, enabled by fintech penetration and consumer familiarity with mobile wallets.

Fragmented reimbursement— less than 25% test-strip coverage

Only a quarter of Egyptians enjoy consistent strip reimbursement, compelling 75% of patients to self-fund consumables that can cost up to 15% of monthly income. In response, many reduce testing frequency to one quarter of clinical recommendations, raising complication rates and ultimately increasing hospitalization costs. Disparate coverage rules across civil-service, military, and private schemes further confuse eligibilities, stalling device renewals and suppressing overall volumes in the Egypt diabetes care devices market. Until the UHI fully harmonizes benefits, growth remains structurally capped by affordability stresses concentrated in rural Upper Egypt.

Counterfeit glucometer strips in informal channels

Regulators estimate that 15-20% of strips sold through informal stalls yield inaccurate readings, leading to mis-dosed insulin and avoidable hypoglycemia[2]Source: Egyptian Drug Authority, “Counterfeit Medical Devices Inspection Update,” EGYPTIANDRUGAUTHORITY.GOV . Patient mistrust lingers even after counterfeit seizures, dampening repeat purchases through legitimate outlets. Manufacturers are trialing QR-code validation and tamper-evident seals, but the added packaging cost feeds back into retail prices, complicating affordability. The Egypt diabetes care devices market thus contends with a negative feedback loop in which counterfeit exposure suppresses legitimate demand and narrows the pool of price-sensitive consumers willing to test regularly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Monitoring Devices anchor volumes while Management Devices accelerate

Monitoring Devices generated 62.34% of 2025 revenue, driven chiefly by SMBG meters and their recurrent strip demand. Test-strip consumption averages 50–100 units per patient per month, embedding high predictability into distributor cash flows. CGM uptake, though still niche, shows CAGR rates approaching double digits among private-insurance and pediatric cohorts, pointing to an emerging premium tier within the Egypt diabetes care devices market. Hospitals rely heavily on strip-based meters for inpatient glycemic checks, so institutional procurement remains skewed toward bulk SMBG kits.

Management Devices are projected to grow at a 3.93% CAGR to 2031 as insulin pens gain price-controlled momentum. Pen adoption eases patient anxiety over dosing accuracy and supports discreet injections, aligning with cultural norms around public medication use. Ramadan fasting creates unique use-case spikes for automated insulin-delivery algorithms that can adapt basal rates without caloric input. Although pump penetration is under 2% of treated diabetics, each new pump user purchases sensors, infusion sets, and reservoirs, adding multi-fold revenue per patient. Localization incentives for pen-needle production promise to stabilize supply chains and reduce foreign-exchange exposure, strengthening the medium-term performance of the Egypt diabetes care devices market.

By Patient Type: Type-2 prevalence drives scale while Type-1 sets technology tone

Type-2 Diabetes represented 81.02% of market sales in 2025 and is forecast to post a 5.19% CAGR through 2031, anchored by rising urban obesity and an aging population. Device vendors therefore prioritize simplified meter interfaces, large display fonts, and bundled education materials tailored to older adults. Government screening days inside large employers generate one-off demand spikes for starter SMBG kits, further enlarging the Type-2 customer base within the Egypt diabetes care devices market.

Type-1 Diabetes remains numerically smaller but economically strategic because per-patient spend is 2–3 times higher than Type-2 patients. Pediatric studies at Ain Shams University show 71% of patients above target HbA1c, prompting clinicians to recommend CGM or hybrid-closed-loop pumps. Manufacturers thus use Type-1 success stories to showcase product efficacy, influencing regulatory approvals and insurance formularies. Gestational diabetes, though a minor share today, is gaining visibility as obstetricians adopt point-of-care glucose monitoring to mitigate fetal risk, adding another specialized sub-stream to the Egypt diabetes care devices market.

By End-user: Hospitals dominate initiation, Home-care signals future migration

Hospitals & Clinics accounted for 54.62% of 2025 device spending because most diagnoses and therapy adjustments occur within institutional settings. Specialized diabetes wards in tertiary hospitals frequently undertake basal-bolus optimization, driving high strip and sensor demand for inpatient titration. Emerging diabetes centers further intensify device utilization by providing on-site nutritionists and certified educators who reinforce structured testing regimens.

Home-care Settings, the fastest-expanding channel at a 4.72% CAGR, reflect rising patient empowerment and a policy push to decongest tertiary facilities. Arabic-language video tutorials bundled with Bluetooth-enabled meters are improving adherence, while teleconsultation platforms let physicians adjust insulin within minutes of data upload. These workflow innovations reduce unnecessary clinic visits and distribute revenue more evenly across geographies, an important trend for the Egypt diabetes care devices market given inter-region access gaps.

By Distribution Channel: Brick-and-mortar leads but e-commerce reconfigures access

Retail Pharmacies retained 51.44% share in 2025, benefiting from more than 80,000 storefronts and pharmacists who double as informal diabetes counselors . Routine strip purchases often coincide with prescription renewals, locking in customer loyalty and enabling pharmacies to negotiate bulk discounts from importers. Visa-branded debit and emerging Buy-Now-Pay-Later options further cement pharmacies as the default replenishment point for older adults.

Online Pharmacies, however, are projected to clock 5.11% CAGR as mobile data plans proliferate and courier logistics improve in outer Cairo. Subscription models distribute strip shipments monthly for a flat fee, smoothing cash outlays for younger cohorts. Data harvested from click-stream behavior guides manufacturers on color-coding lancets, packaging text sizes, and price-point elasticity, injecting valuable feedback into product-development cycles. The dual-channel interplay ultimately broadens the Egypt diabetes care devices market by catering to both traditional and digital buyers.

Geography Analysis

Greater Cairo, Alexandria, and the Nile Delta collectively absorb nearly 65% of device shipments, driven by higher diabetes prevalence and denser healthcare infrastructure. Urban dwellers exhibit more frequent glucose testing and higher willingness to pay for CGM, lifting average revenue per user. UHI pilot phases in Port Said documented a 17% rise in SMBG meter uptake once reimbursement activated, demonstrating policy leverage on urban demand clusters.

Lower Egypt enjoys better physician-to-patient ratios and faster UHI rollout, translating into broader formulary adoption of meters and pen needles. Conversely, Upper Egypt struggles with lower clinic density, leading to delayed diagnoses and periodic stock-outs of quality strips. Government initiatives are funding mobile medical caravans that conduct screening and meter distribution drives, partially narrowing the access chasm, yet logistics costs remain elevated.

Telehealth platforms, though still nascent outside cities, are beginning to bridge regional disparities by routing consults to centralized endocrinology hubs. Where 4G coverage is reliable, patients are uploading glucose logs and receiving dosage feedback within hours, demonstrating that digital care can seed demand for home-care-oriented devices. Continued network upgrades are therefore poised to unlock latent rural segments within the broader Egypt diabetes care devices market.

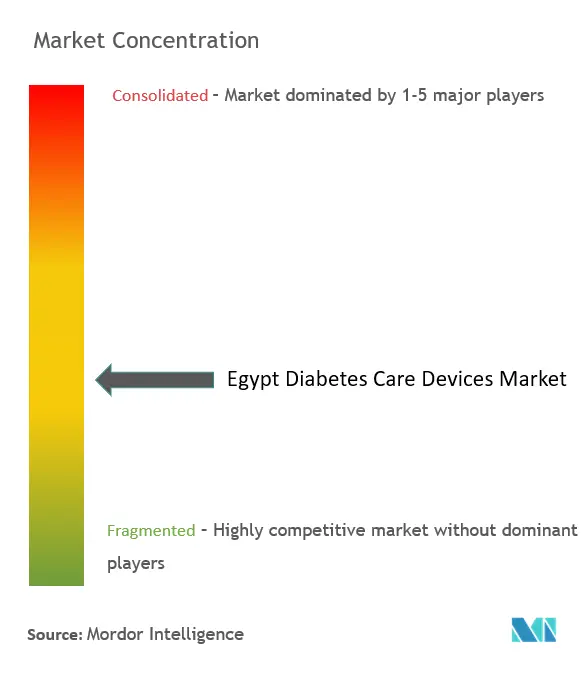

Competitive Landscape

Global majors such as Abbott, Roche, Medtronic, and Novo Nordisk retain leadership in technology-intensive categories—respectively sensors, meters, pumps, and insulin analogues. Local champions, notably the Egyptian German Insulin Company (EGIC) and VACSERA, leverage tariff exemptions and proximity advantages to carve share in pen-needle and strip manufacturing. Policy makers favor bidders with domestic production footprints, compelling multinationals to consider joint ventures or contract manufacturing to protect public-tender volumes.

Insulin supply remains oligopolistic: three suppliers control 96% of MENA volume and 99% of value, raising policy alarms over supply security. Monitoring devices, by contrast, display moderate fragmentation, with at least eight brands exceeding 2% share each. Competitive differentiation is shifting from raw accuracy claims to integrated data platforms that slot into hospital electronic medical records and consumer mobile apps.

Localization policy is spurring technology transfers; for example, Novo Nordisk’s Aspen partnership seeks to bottle insulin cartridges domestically for African distribution. Meanwhile, Medtronic’s local clinical data on MiniMed 780G during Ramadan serves as a culturally-relevant marketing edge. Smaller Egyptian distributors focus on low-cost, no-frills meters to capture rural share, using aggressive cashback promotions financed by import duty savings. Collectively, these moves suggest a moderate consolidation trajectory for the Egypt diabetes care devices market as economies of scale favor vertically-integrated or locally-embedded operators.

Egypt Diabetes Care Devices Industry Leaders

Abbott Diabetes Care

Medtronic PLC

Roche Diabetes Care

Eli Lilly and Company

Novo Nordisk A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Ministry of Health and GE Healthcare agreed to co-produce diagnostic equipment—covering select diabetes-related devices—to reduce import reliance

- November 2024: Medtronic published Egyptian real-world results for MiniMed 780G showing 70.7–84.7% time-in-range, including fasting periods

Egypt Diabetes Care Devices Market Report Scope

Diabetes care devices are the hardware, equipment, and software used by diabetes patients to regulate blood glucose levels, prevent diabetes complications, lessen the burden of diabetes, and enhance the quality of life. The Egypt Diabetes Care Devices Market is segmented into monitoring devices (self-monitoring blood glucose devices (glucometer devices, blood glucose test strips, and lancets), continuous glucose monitoring devices (sensors and durables (receivers and transmitters)), management devices (insulin pumps (insulin pump device, insulin pump reservoir, and infusion set), insulin syringes, cartridges in reusable pens, disposable pens, and jet injectors). The report offers the value (USD) and volume (units) for the above segments.

By Device Type

| Monitoring Devices | Self-Monitoring Blood Glucose | Glucometer Devices |

| Test Strips | ||

| Lancets | ||

| Continuous Glucose Monitoring | Sensors | |

| Durables | ||

| Management Devices | Insulin Pumps | Insulin Pump Device |

| Insulin Pump Reservoir | ||

| Infusion Set | ||

| Insulin Syringes | ||

| Insulin Pens | ||

| Jet Injectors | ||

By Patient Type

| Type-1 Diabetes |

| Type-2 Diabetes |

| Gestational & Others |

By End-user

| Hospitals & Clinics |

| Home-care Settings |

| Ambulatory Surgical Centres |

| Pharmacies & Retail Chains |

By Distribution Channel

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Direct-to-Consumer E-commerce |

| By Device Type | Monitoring Devices | Self-Monitoring Blood Glucose | Glucometer Devices |

| Test Strips | |||

| Lancets | |||

| Continuous Glucose Monitoring | Sensors | ||

| Durables | |||

| Management Devices | Insulin Pumps | Insulin Pump Device | |

| Insulin Pump Reservoir | |||

| Infusion Set | |||

| Insulin Syringes | |||

| Insulin Pens | |||

| Jet Injectors | |||

| By Patient Type | Type-1 Diabetes | ||

| Type-2 Diabetes | |||

| Gestational & Others | |||

| By End-user | Hospitals & Clinics | ||

| Home-care Settings | |||

| Ambulatory Surgical Centres | |||

| Pharmacies & Retail Chains | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail Pharmacies | |||

| Online Pharmacies | |||

| Direct-to-Consumer E-commerce | |||

Key Questions Answered in the Report

What is the current value of the Egypt diabetes care devices market?

The market is valued at USD 331.61 million in 2026 and is projected to reach USD 390.25 million by 2031.

Which device category dominates sales?

Monitoring Devices lead, accounting for 62.34% of 2025 revenue, primarily due to strong strip-based SMBG demand.

How fast are Online Pharmacies expanding in Egypt?

Online Pharmacies are projected to grow at a 5.11% CAGR between 2026 and 2031, the fastest among distribution channels.

Why are pen needles gaining traction?

Government price caps on insulin pens have boosted pen uptake, and each pen user consumes 30–45 needles monthly, driving steady consumable demand.

Page last updated on: