Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.03 Billion |

| Market Size (2026) | USD 2.13 Billion |

| Market Size (2031) | USD 2.68 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

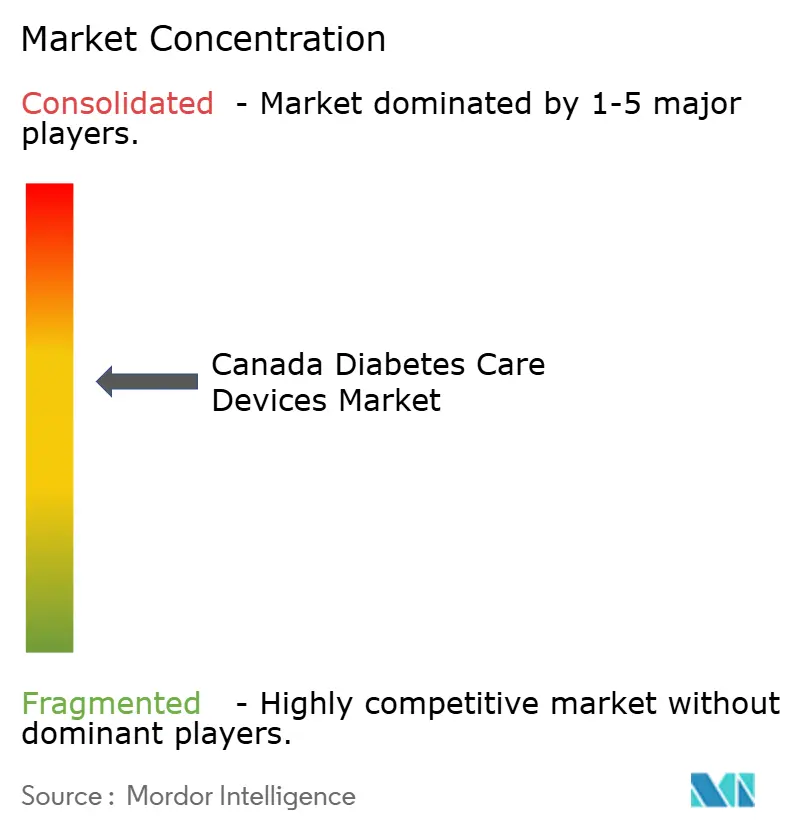

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Diabetes Devices Market Analysis by Mordor Intelligence

The Canada diabetes devices market size was valued at USD 2.03 billion in 2025 and estimated to grow from USD 2.13 billion in 2026 to reach USD 2.68 billion by 2031, at a CAGR of 4.74% during the forecast period (2026-2031). Rising disease prevalence—3.7 million people live with diabetes and more than 200,000 new cases are diagnosed each year—continues to strain provincial health budgets and accelerate adoption of technology-enabled solutions. Continuous glucose monitoring (CGM) systems, hybrid closed-loop pumps, and smartphone-linked wearables are reshaping therapy from episodic testing to real-time, predictive care. Parallel policy shifts, including Bill C-64 that introduces single-payer pharmacare, are poised to widen access to devices and reduce out-of-pocket costs. British Columbia’s progressive reimbursement model and Alberta’s streamlined CGM coverage illustrate how targeted public funding is catalyzing growth in the Canada diabetes devices market. Competitive dynamics are also shifting: Medtronic plans to spin off its diabetes unit, while Abbott and several drug makers highlight complementary outcomes when GLP-1 medicines are paired with sensors, signaling a move toward integrated therapeutic ecosystems.

Key Report Takeaways

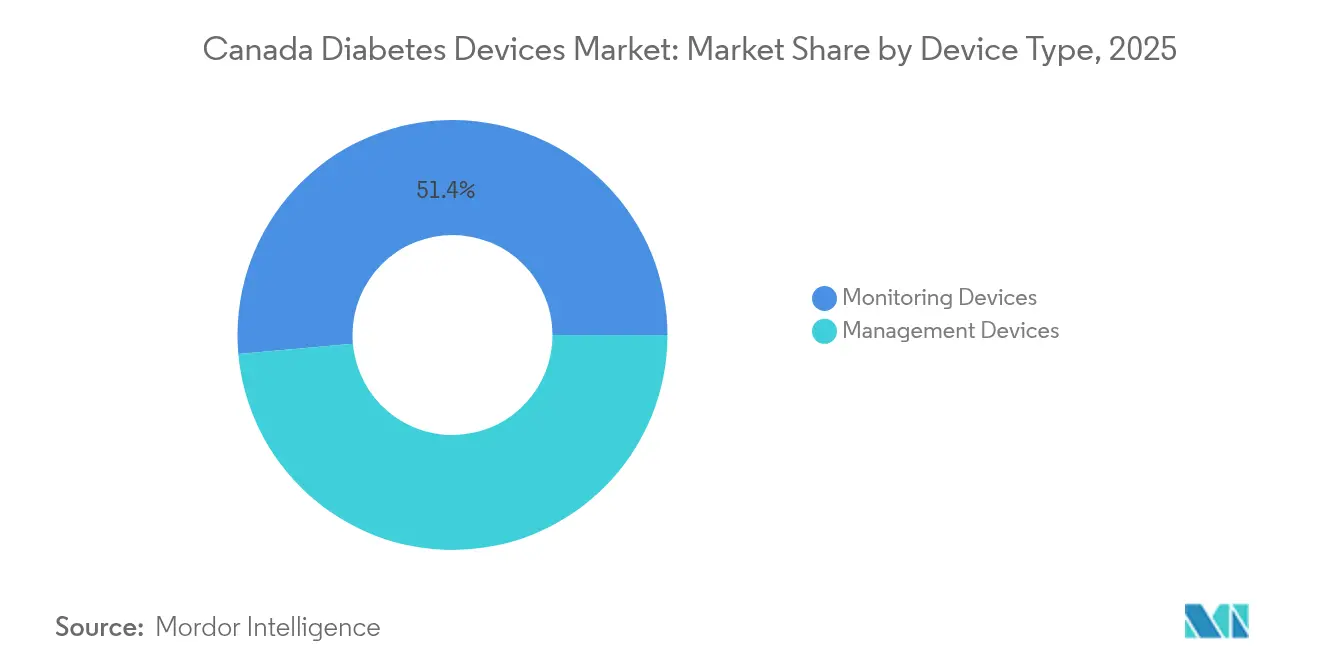

- By device type, monitoring products captured 51.40% of the Canada diabetes devices market share in 2025, whereas management devices are forecast to expand at a 5.06% CAGR through 2031.

- By end user, home-care settings commanded 49.30% share of the Canada diabetes devices market size in 2025; specialty diabetes centers are projected to post the fastest 5.44% CAGR to 2031.

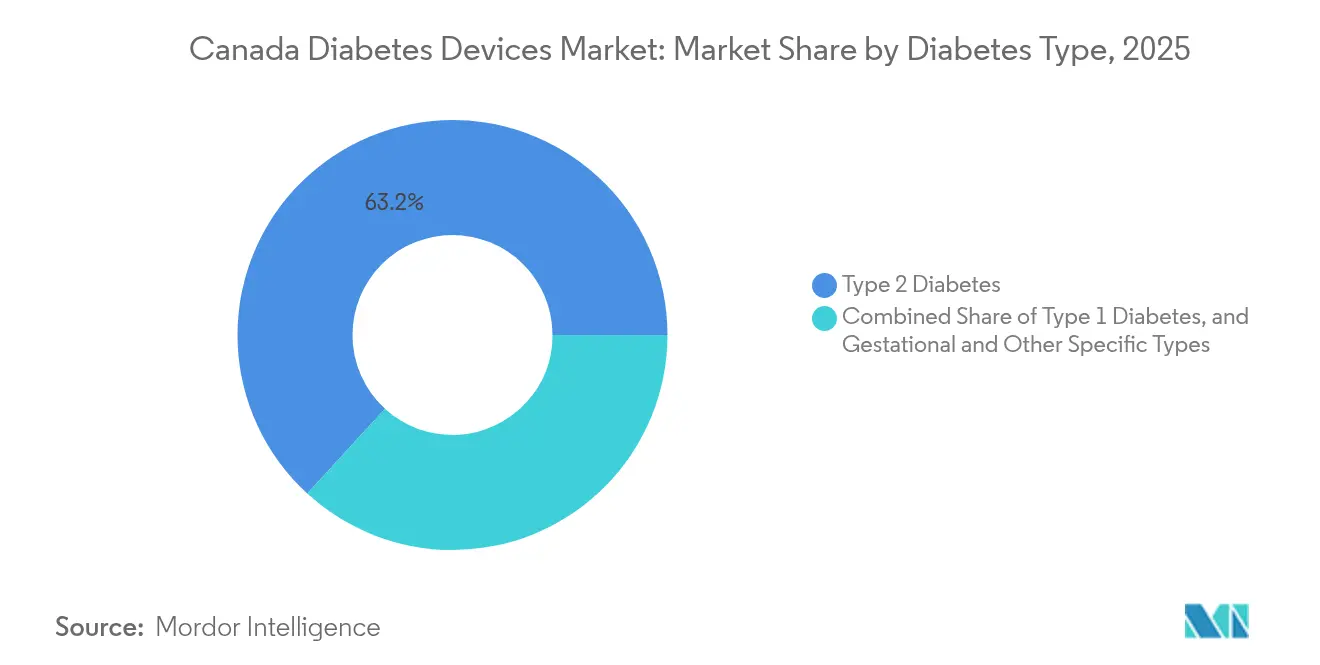

- By diabetes type, Type 2 accounted for 63.20% of the Canada diabetes devices market size in 2025, while Type 1 is expected to grow at 5.27% CAGR between 2026-2031.

- By province, Ontario led with 36.60% revenue share in the Canada diabetes devices market in 2025; British Columbia is set to grow the quickest at a 5.08% CAGR to 2031.

- By distribution channel, offline retail pharmacies held 44.20% of the Canada diabetes devices market share in 2025, whereas online pharmacies are on track for a 5.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Diabetes Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanded reimbursement for CGM and flash systems | +1.2% | Ontario, Quebec, British Columbia, Alberta | Medium term (2-4 years) |

| Accelerating diabetes burden in Indigenous and northern communities | +0.8% | Northern territories, British Columbia, Alberta, Saskatchewan, Manitoba | Long term (≥ 4 years) |

| Surge in hybrid closed-loop adoption among tech-savvy adults | +1.0% | Ontario, British Columbia, Alberta | Short term (≤ 2 years) |

| Pharmacy-led diabetes programs with device dispensing fees | +0.7% | National (early gains in Ontario, Quebec) | Medium term (2-4 years) |

| Smartphone-integrated wearables driving patient engagement | +0.6% | National (urban focus) | Short term (≤ 2 years) |

| Federal assistive-device tax credits boosting affordability | +0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanded Reimbursement for CGM and Flash Systems

Provincial expansion of CGM funding is resetting expectations for equitable access. Saskatchewan’s 2025 budget marked the newest pledge, adding coverage for children under 18 and insulin-treated Type 2 adults. Alberta already reimburses Dexcom G6, Dexcom G7, Freestyle Libre 2, and Medtronic systems through a streamlined approval process. Nova Scotia introduced CGM coverage in June 2024 for both Type 1 and Type 2 patients on insulin, while Quebec's Beneva insurer added Dexcom G7 to its formulary. Despite progress, geographic inequities persist—Ontario maintains the most complex reimbursement pathway, creating a postal-code lottery for device access. Research shows 97% of Canadians believe CGM would improve their diabetes management, yet many remain ineligible under current criteria.

Accelerating Diabetes Burden in Indigenous Communities

The disproportionate impact of diabetes on Indigenous populations demands culturally appropriate solutions. Prevalence rates are dramatically higher among First Nations (17.2% on-reserve, 12.7% off-reserve), Inuit (4.7%), and Métis (9.9%) compared to 5.0% in the general population [1]Diabetes Canada, "Indigenous communities and diabetes," Diabetes Canada, diabetes.ca. This disparity drives innovation in remote care delivery, exemplified by British Columbia's Mobile Diabetes Telemedicine Clinic serving 120 sites annually and demonstrating measurable improvements in diabetes control among First Nations communities. The Non-Insured Health Benefits program expanded CGM coverage to all First Nations and Inuit people using insulin in 2023, a significant policy shift from previous age-restricted eligibility. Despite these advances, significant barriers persist—fragmented healthcare systems, lack of culturally appropriate services, and socioeconomic inequalities stemming from colonization require continued investment in Indigenous-led initiatives

Surge in Hybrid Closed-Loop Adoption

The rapid uptake of hybrid closed-loop (HCL) systems is transforming diabetes management across Canada. Multiple systems now compete for market share: Medtronic's MiniMed 780G, Tandem's Control-IQ, and Insulet's Omnipod 5, which launched in early 2025 as the first tubeless, waterproof automated insulin delivery system. Clinical data confirms these systems significantly improve glycemic control—the MiniMed 780G shows a mean Time In Range of 72.3% across approximately 600,000 users globally. Health Canada recently approved the mylife YpsoPump with CamAPS FX algorithm, which demonstrates reduced HbA1c levels and increased time in target glucose range while minimizing hypoglycemia. Despite these innovations, only 12% of Type 1 diabetes patients globally use automated insulin delivery systems, indicating substantial growth potential as awareness and accessibility improve.

Pharmacy-Led Diabetes Management Programs

Pharmacy-based diabetes management services are driving device adoption and improving outcomes. Recent studies show significant reductions in hemoglobin A1c levels from 9.5% to 9% over six months through remote pharmacist interventions. These programs leverage pharmacists' unique position to enhance medication management, device training, and ongoing support. A systematic review of 12 studies found pharmacist involvement in diabetes care is often cost-effective or dominant in terms of both cost savings and clinical effectiveness. Digital health informatics integration is further enhancing clinical prioritization for people with diabetes, as demonstrated in a cohort study of 4,022 patients that emphasized data-driven strategies for managing care backlogs. These programs create new revenue streams for pharmacies through dispensing fees while simultaneously improving accessibility and adherence to diabetes management technologies.

Smartphone-Integrated Wearables Driving Engagement

The integration of diabetes management tools with smartphones and wearable devices is revolutionizing patient engagement. Clinical trials demonstrate significant improvements in physical activity adherence and cardiometabolic health markers among people with Type 2 diabetes. The MOTIVATE-T2D trial, conducted across Canada and the UK, showed participants using smartwatches paired with health apps achieved reduced blood glucose and blood pressure, with an impressive 82% retention rate indicating strong user acceptance. The Canadian diabetes technology landscape increasingly embraces these integrated solutions, exemplified by the Integrated Diabetes Management App that connects with Dexcom CGM devices and popular fitness trackers to automate data collection. These technologies enhance self-management among diverse populations, including Indigenous communities where traditional healthcare access may be limited, though challenges remain in ensuring digital readiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Provincial reimbursement disparities limiting equitable access | -0.9% | National (greater impact in smaller provinces) | Medium term (2-4 years) |

| PMPRB price-control framework compressing margins | -0.7% | National | Long term (≥ 4 years) |

| Semiconductor-Sensor Supply Bottlenecks Post-COVID | -0.3% | National | Medium term (2-4 years) |

| Uptake of GLP-1 drugs moderating device volume growth | -0.5% | National (early impact in urban centers) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PMPRB Price-Control Framework Compressing Margins

The Patented Medicine Prices Review Board regulatory framework creates significant pricing pressure on diabetes devices and related pharmaceuticals. Recent reforms removed Switzerland and the US from the reference price basket and required companies to disclose net prices, increasing the number of drugs subject to price regulation. Major manufacturers like Novo Nordisk have expressed concerns about the framework's impact, particularly regarding potential arbitrary price reductions during annual reviews that could compress profit margins and limit investment in the Canadian market. The regulatory environment has contributed to higher Canadian prices for diabetes medications compared to other countries, leading to an estimated additional spending of USD 703 million and potentially limiting patient access to innovative diabetes care technologies. This pricing pressure is particularly significant for advanced diabetes devices that rely on integration with pharmaceutical products

Provincial Reimbursement Disparities Limiting Access

The fragmented provincial coverage landscape creates significant barriers to diabetes device access. Eligibility criteria vary dramatically by province and often depend on age, income, and treatment type. This geographic lottery is particularly evident in CGM coverage, where Ontario has established the most complex reimbursement process while Alberta has implemented more streamlined approaches. The disparities extend to insulin pump coverage, with British Columbia's PharmaCare covering pumps from manufacturers like Medtronic, Tandem, Omnipod, and Ypsomed for patients with Type 1 diabetes, while coverage in other provinces may be more limited. These inconsistencies create a two-tier system where access to life-changing technologies depends on postal code rather than medical need, with approximately 3% of Canadians lacking any coverage and over 10% not enrolled in public or private plans.

Uptake of GLP-1 Drugs Moderating Device Volume Growth

The rapid adoption of GLP-1 receptor agonists is creating complex market dynamics for diabetes devices, with expenditures on semaglutide (Ozempic) rising dramatically. While initially viewed as potential competition for device manufacturers, emerging evidence suggests a more nuanced relationship. Real-world data shows that Type 2 diabetes patients using GLP-1 medicines alongside FreeStyle Libre technology experience significantly greater improvements in HbA1C levels (-1.5% and -2.4%) compared to those using GLP-1 therapy alone. The impact on insulin pump markets appears limited, with analysts projecting only minor effects on insulin pump adoption. However, the overall market dynamics are shifting as GLP-1 medications continue their rapid growth trajectory, with volume increasing by 78% from 2023 to 2024, potentially moderating the growth of certain diabetes device segments while creating new opportunities for integrated care solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Monitoring Devices Lead Through Enhanced Connectivity

Monitoring devices dominate the Canadian diabetes landscape with 51.40% market share in 2025, driven by expanding coverage of continuous glucose monitoring systems across provincial health plans. The integration of CGM data with electronic health records enhances clinical decision-making, with healthcare providers increasingly relying on these metrics to guide treatment adjustments. Management devices are projected to grow at 5.06% CAGR from 2026-2031, outpacing the overall Canada diabetes devices market as hybrid closed-loop systems gain traction among tech-savvy patients seeking automated insulin delivery solutions. The Omnipod 5, launched in Canada in early 2025, exemplifies this trend as the first tubeless, waterproof automated insulin delivery system compatible with both Dexcom G6 and G7 CGM systems.

The monitoring devices segment is witnessing significant innovation beyond traditional CGM, with emerging non-invasive glucose monitoring technologies gaining attention for their potential to reduce patient discomfort and increase adherence. Companies are developing advanced sensor technologies such as optical and electromagnetic sensors that provide pain-free glucose level detection, while wearable devices offer continuous glucose readings with smartphone integration for real-time tracking. Within management devices, insulin pumps are evolving rapidly with the introduction of systems like the Tandem t:slim X2 insulin pump, which now features compatibility with the Dexcom G7 CGM in Canada, enhancing diabetes management options through automated insulin delivery algorithms.

By End User: Home-Care Settings Expand Through Digital Connectivity

Home-care settings capture 49.30% market share in 2025, reflecting the fundamental shift toward patient-centered diabetes management enabled by remote monitoring technologies and telehealth services. The COVID-19 pandemic accelerated this transition, establishing new patterns of care delivery that have persisted due to their convenience and effectiveness. Specialty diabetes centers are growing at the fastest rate with a 5.44% CAGR from 2026-2031, as these facilities adopt multidisciplinary approaches that integrate advanced technologies with comprehensive care models. These centers are particularly effective for managing complex cases and providing specialized education on new diabetes technologies, serving as innovation hubs that often introduce cutting-edge devices before broader adoption.

The hospital and clinic segment maintains a significant presence in the Canada diabetes devices market, particularly for initial diagnosis, technology training, and managing acute complications. Recent advances in integrating CGM systems into hospital workflows are improving inpatient diabetes management, with consensus guidelines recommending CGM use in hospital settings to enhance glycemic control and reduce healthcare worker exposure. Retail and community pharmacies are emerging as increasingly important players in the diabetes care ecosystem, with pharmacist-led diabetes management programs demonstrating significant improvements in clinical outcomes. A recent pilot program showed a reduction in hemoglobin A1c from 9.5% to 9% over six months through remote pharmacist interventions, highlighting the potential for these settings to expand their role in diabetes device distribution and support.

By Diabetes Type: Type 2 Dominates While Type 1 Grows Faster

Type 2 diabetes accounts for 63.20% market share in 2025, reflecting its higher prevalence in the Canadian population where approximately 30% of adults are affected by diabetes or pre-diabetes. The growing adoption of CGM technology among Type 2 diabetes patients is reshaping management approaches, with recent evidence suggesting that CGM can be beneficial even for patients not on intensive insulin therapy. Type 1 diabetes is the fastest-growing segment at 5.27% CAGR from 2026-2031, driven by increasing incidence rates and the rapid adoption of advanced technologies like automated insulin delivery systems. The Canada diabetes devices market size for Type 1 diabetes is expanding as incidence rates rise significantly, with a reported 5.4% annual increase in the Greater Montréal area, creating urgency for improved management solutions .

The gestational and other specific types segment represents a smaller but clinically important market, with specialized needs for monitoring and management during pregnancy. The CamAPS FX hybrid closed-loop algorithm stands out as the only algorithm approved for pregnancy, offering specialized support for this vulnerable population. Recent advances in diabetes technology are increasingly tailored to the specific needs of different diabetes types, with the International Society for Pediatric and Adolescent Diabetes proposing more ambitious glycemic targets that reflect the evolving capabilities of diabetes devices. The integration of GLP-1 receptor agonists with monitoring technologies is creating new management paradigms particularly for Type 2 diabetes, with evidence showing that combining these approaches yields better outcomes than either alone.

By Distribution Channel: Online Pharmacies Disrupt Traditional Retail Dominance

Offline retail pharmacies maintain the largest market share at 44.20% in 2025, leveraging their established presence and the trust they've built with diabetes patients through face-to-face consultations and immediate product availability. These pharmacies are increasingly expanding their diabetes care offerings beyond medication dispensing to include device training, monitoring services, and comprehensive management programs. Online pharmacies are experiencing the fastest growth at 5.52% CAGR from 2026-2031, disrupting traditional distribution models through competitive pricing, convenient home delivery, and expanded product selection. Canadian online pharmacies specializing in diabetes , such as Diabetic Online, are gaining traction by offering significant cost savings and a wide range of healthcare products, including prescription medications and diabetes devices.

Hospital pharmacies and direct tenders continue to play a crucial role in the distribution of diabetes devices, particularly for inpatient care and specialized diabetes centers. These channels benefit from bulk purchasing power and direct relationships with manufacturers, often securing favorable pricing for advanced technologies. The national pharmacy network offered by services like Diabetes Express illustrates the evolving distribution landscape, collaborating with local private insurance and governmental coverage plans to directly bill diabetes supplies, simplifying the reimbursement process for patients. The introduction of Bill C-64 and the establishment of a Device Fund to improve access to essential diabetes management supplies could significantly impact distribution channels by altering reimbursement pathways and potentially increasing the role of public procurement in the Canada diabetes devices market.

Geography Analysis

Ontario dominates the Canadian diabetes devices market with 36.60% share in 2025, leveraging its population advantage and comprehensive diabetes care infrastructure. The province's diabetes burden is substantial, contributing significantly to the national prevalence where nearly 12 million Canadians have diabetes, expected to rise to 32% of the population by 2030. Despite leading in market size, Ontario faces challenges in device access, with the Canada CGM Policy Position Working Group identifying it as having the most complex reimbursement process for continuous glucose monitoring devices. The province has established specialized diabetes education programs and care networks that enhance device adoption and patient support, creating a foundation for the projected growth from 2026-2031. Recent policy developments, including the introduction of Bill C-64 for universal pharmacare, are expected to significantly impact the Ontario Canada diabetes devices market by improving access to diabetes medications and potentially increasing demand for complementary monitoring devices.

British Columbia is positioned as the fastest-growing provincial market at 5.08% CAGR from 2026-2031, outpacing the national average due to its progressive reimbursement policies and innovative care delivery models. The province's PharmaCare program provides comprehensive coverage for diabetes supplies, including insulin, insulin pumps from manufacturers like Medtronic, Tandem, Omnipod, and Ypsomed, blood glucose test strips, and continuous glucose monitors . British Columbia has also pioneered mobile health solutions for remote communities, exemplified by the Mobile Diabetes Telemedicine Clinic that serves approximately 120 sites annually and has demonstrated improvements in diabetes control among First Nations communities. The province's emphasis on technology-enabled care aligns with broader market trends toward home-based management and remote monitoring, positioning it for continued growth in the diabetes devices sector. Alberta and Quebec represent significant markets with unique characteristics, with Alberta implementing streamlined access to CGM devices and Quebec offering broader coverage of GLP-1 agonists compared to other provinces.

The smaller provinces and territories face distinct challenges in diabetes care access, with geographic isolation and limited healthcare infrastructure creating barriers to device adoption. However, recent developments such as Saskatchewan's 2025 budget announcement of new diabetes device coverage indicate progress in addressing these disparities. The diabetes burden is particularly acute in northern and Indigenous communities, where prevalence rates significantly exceed the national average, creating urgent demand for culturally appropriate diabetes care solutions. The Non-Insured Health Benefits program's 2023 expansion of CGM coverage to all First Nations and Inuit people using insulin represents a significant policy shift that could accelerate device adoption in these communities . Across all provinces, the introduction of national pharmacare and the establishment of a Device Fund are expected to reduce provincial disparities in access to diabetes care technologies, potentially creating a more equitable landscape for device adoption throughout Canada.

Competitive Landscape

The Canadian diabetes devices market features moderate concentration with intense competition among established players and emerging innovators across both monitoring and management device segments. Strategic partnerships between device manufacturers and pharmaceutical companies are reshaping competitive dynamics, exemplified by Abbott's emphasis on the complementary relationship between their FreeStyle Libre systems and GLP-1 medications, which has shown significant improvements in glycemic control when used together. The market is witnessing significant structural changes, most notably Medtronic's May 2025 announcement to separate its diabetes business into a standalone company focused on intensive insulin management, a move expected to enhance innovation and market responsiveness in the Canadian diabetes devices market.

White-space opportunities exist in addressing the needs of underserved populations, particularly in remote and Indigenous communities where diabetes prevalence significantly exceeds the national average. Companies are increasingly leveraging digital health technologies to differentiate their offerings, with the integration of artificial intelligence and machine learning algorithms enhancing the predictive capabilities of diabetes management systems. Tandem Diabetes Care reported significant sales growth, with total sales reaching USD 657.6 million for the nine months ended September 30, 2024, up from USD 550.9 million in the same period in 2023, indicating strong market momentum for advanced insulin delivery systems. The competitive landscape is further evolving with the emergence of non-invasive glucose monitoring technologies and the increasing integration of diabetes management tools with smartphones and wearable devices, creating new competitive fronts beyond traditional device categories.

The Canadian diabetes devices market is seeing increased focus on Indigenous-specific solutions, recognizing the disproportionate impact of diabetes on these communities. Several companies are developing culturally appropriate technologies and remote monitoring solutions tailored to the unique needs of northern and rural populations. The competitive environment is also being shaped by the growing influence of pharmacy chains, which are expanding their role from product distribution to comprehensive diabetes management services. This shift is creating new partnership opportunities for device manufacturers seeking to enhance patient education and support. Meanwhile, the planned separation of Medtronic's diabetes business signals a potential restructuring of the competitive landscape, with the possibility of more focused innovation and market-specific strategies from the standalone entity.

Canada Diabetes Devices Industry Leaders

-

Dexcom

-

Medtronic

-

Novo Nordisk A/S

-

F. Hoffmann-La Roche AG

-

Abbott Diabetes Care

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Medtronic announced plans to separate its Diabetes business into a standalone company, enhancing focus on intensive insulin management through an IPO expected to be completed within 18 months, a strategic move aimed at creating a more streamlined Medtronic and a dedicated Diabetes company positioned to drive innovation in the automated insulin delivery market.

- May 2025: Insulet Corporation launched the Omnipod 5 Automated Insulin Delivery System in Canada, the first tubeless, waterproof AID System approved in the country, compatible with Dexcom G6 and G7 CGM Systems, with public reimbursement currently available in Ontario and Nova Scotia and plans to expand coverage to other provinces.

- March 2025: The Saskatchewan government announced new coverage for diabetes devices in its 2025 budget, aiming to improve access to essential diabetes care technologies for residents, representing a significant expansion of provincial support for diabetes management tools.

- February 2025: The Government of Canada introduced Bill C-64 for universal pharmacare, aiming to provide single-payer coverage for diabetes medications and establishing a fund to support access to diabetes supplies, including insulin pumps and glucose monitors, with approximately 3.7 million Canadians living with diabetes set to benefit from the initiative.

- July 2024: Tandem Diabetes Care announced compatibility between the t:slim X2 insulin pump and Dexcom G7 CGM in Canada, enhancing diabetes management options for patients by integrating two leading technologies in the automated insulin delivery space.

- November 2024: Ypsomed and CamDiab received Health Canada approval for the mylife YpsoPump insulin pump and CamAPS FX hybrid closed-loop algorithm, providing an automated insulin delivery system aimed at improving glycemic control for the over 300,000 Canadians living with Type 1 diabetes.

- June 2024: Dexcom announced expanded coverage for the Dexcom G7 CGM system through more private insurers and provincial programs, including coverage from Beneva in Quebec, Saskatchewan Health Authority for individuals under 18, and Nova Scotia's new CGM coverage for Type 1 and Type 2 diabetes patients using insulin.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Canada diabetes devices market as sales of hardware and integrated software that monitor blood glucose or deliver insulin, specifically glucometers with strips and lancets, continuous glucose monitors, insulin pens, pumps, jet injectors, and emerging closed-loop systems. The definition purposely tracks only factory-built finished devices and their proprietary disposables that reach end users through retail, hospital, or tender channels.

Scope exclusion: the model omits bulk insulin drugs, mobile coaching subscriptions sold without companion hardware, and aftermarket pump accessories.

Segmentation Overview

-

By Device Type

-

Management Devices

-

Insulin Pump

- Insulin Pump Device

- Insulin Pump Reservoir

- Infusion Set

- Insulin Syringes

- Insulin Disposable Pens

- Insulin Cartridges in Reusable Pens

- Insulin Jet Injectors

- Automatic / Hybrid Closed-Loop Systems

-

Insulin Pump

-

Monitoring Devices

-

Self-Monitoring Blood Glucose (SMBG)

- Glucometer Devices

- Test Strips

- Lancets

-

Continuous Glucose Monitoring (CGM)

- Sensors

- Receivers & Transmitters

-

Self-Monitoring Blood Glucose (SMBG)

-

Management Devices

-

By End User

- Hospitals & Clinics

- Specialty Diabetes Centers

- Home-Care Settings

- Retail & Community Pharmacies

-

By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

- Gestational & Other Specific Types

-

By Province

- Ontario

- Quebec

- British Columbia

- Alberta

- Rest of Canada

-

By Distribution Channel

- Offline Retail Pharmacies

- Online Pharmacies

- Hospital Pharmacies & Direct Tenders

Detailed Research Methodology and Data Validation

Primary Research

Multiple touchpoints with endocrinologists, certified diabetes educators, provincial tender managers, and channel buyers across Ontario, Quebec, Alberta, and the Atlantic provinces were conducted. Their insights clarified CGM penetration rates, average selling prices, stocking lead times, and likely adoption curves for hybrid closed-loop systems, allowing us to adjust desk-based assumptions before final modeling.

Desk Research

Mordor analysts began with standard public data sets such as Statistics Canada's chronic disease tables, the Canadian Institute for Health Information's hospitalization files, federal customs import codes for HS 9027 and HS 9018, and peer-reviewed prevalence work published in Diabetes Care. We enriched these with association briefs from Diabetes Canada and provincial pharmacare formularies that spell out funded CGM and pump criteria. Paid databases, including D&B Hoovers for distributor revenues and Dow Jones Factiva for device recall news, helped size company footprints and validate shipment timing. Company 10-K filings, investor decks, tender notices on Tenders Info, and Health Canada device approval registries rounded out the desk review. This list is illustrative; many other verified sources fed into data gathering, cross-checks, and context setting.

Market-Sizing & Forecasting

The core model starts with a top-down reconstruction of domestic demand by linking diagnosed diabetes prevalence to device ownership ratios and replacement cycles. Results are then sense-checked through selective bottom-up roll-ups of leading supplier shipments and representative retail ASP × unit calculations, which highlight any material variance. Input fingerprints include: 1) diagnosed adult diabetes population, 2) CGM reimbursement roll-out by province, 3) pump upgrade interval, 4) online pharmacy share shift, and 5) U.S.-CAD exchange movement affecting import costs. A multivariate regression marries these variables with three macro indicators: population aging, GDP per capita, and obesity rate to forecast volume and value through 2030. Where bottom-up evidence is sparse, we apply weighted averages from primary interviews to bridge gaps.

Data Validation & Update Cycle

Intermediate outputs are triangulated against independent prevalence studies and import statistics. Any anomaly above a ±8 percent threshold triggers an analyst re-run and senior review. Reports refresh every twelve months, with mid-cycle updates should reimbursement policy or major product approvals materially change. Clients therefore receive the most up-to-date baseline each time they log in.

Why Mordor's Canada Diabetes Devices Baseline Earns Trust

Published estimates often diverge because firms vary device inclusions, base years, and refresh frequency. Our disciplined scope selection, variable tracking, and annual renewal compress those gaps for decision makers.

Key gap drivers include broader digital-health add-ons in some studies, conservative ASP assumptions in others, and inconsistent inflation or currency treatment. We document every assumption, revisit them with experts, and update immediately after policy or technology shifts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.03 B (2025) | Mordor Intelligence | |

| USD 1.84 B (2023) | Regional Consultancy A | Includes coaching apps and uses constant 2023 dollars without inflation or currency adjustments |

| USD 1.22 B (2022) | Industry Association B | Excludes closed-loop and CGM volumes, relies largely on import code 9018 data and updates biennially |

The comparison shows why Mordor's balanced, transparent baseline, grounded in clear scope, multi-source validation, and timely refresh, offers Canadian stakeholders a dependable reference for planning and investment.

Key Questions Answered in the Report

What is driving growth in the Canadian diabetes devices market

The market is primarily driven by expanding provincial reimbursement for CGM systems, rising diabetes prevalence (especially in Indigenous communities), and increasing adoption of hybrid closed-loop insulin delivery systems. These factors collectively contribute to the projected 4.74% CAGR through 2031.

Which diabetes devices have the best insurance coverage in Canada?

Coverage varies significantly by province. British Columbia offers the most comprehensive coverage for insulin pumps and CGM systems, while Alberta has streamlined access to devices like Dexcom G6/G7 and FreeStyle Libre 2. Ontario has extensive coverage but more complex reimbursement processes.

How will Bill C-64 affect diabetes device access in Canada?

Bill C-64 introduces universal pharmacare for diabetes medications and establishes a Device Fund to support access to insulin pumps and glucose monitors. This national initiative aims to reduce provincial disparities and improve affordability for the 3.7 million Canadians living with diabetes.

Which segment of the diabetes devices market is growing fastest?

Online pharmacies are experiencing the fastest growth at 5.52% CAGR (2026-2031), disrupting traditional distribution models through competitive pricing and home delivery. Among end users, specialty diabetes centers lead with 5.44% CAGR, while British Columbia shows the highest provincial growth at 5.08% CAGR.

Page last updated on: