Canada Diabetes Care Drugs And Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

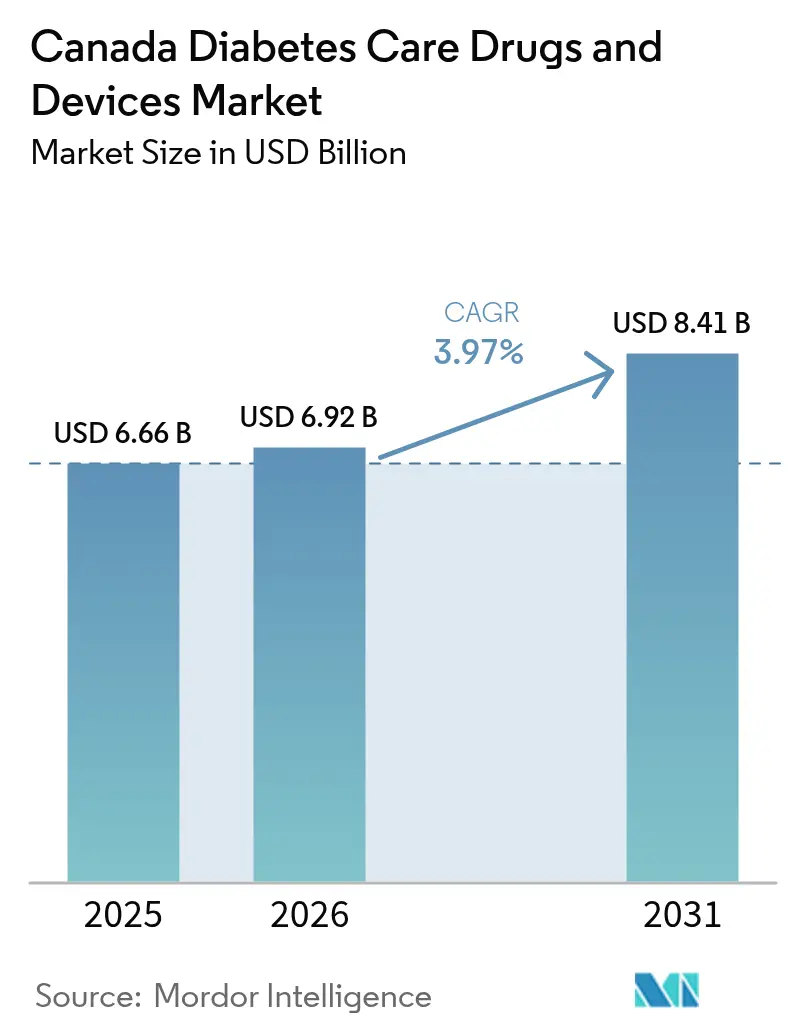

| Base Year Market Size (2025) | USD 6.66 Billion |

| Market Size (2026) | USD 6.92 Billion |

| Market Size (2031) | USD 8.41 Billion |

| Growth Rate (2026 - 2031) | 3.97% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Diabetes Care Drugs And Devices Market Analysis by Mordor Intelligence

The Canada Diabetes Care Drugs And Devices Market size was valued at USD 6.66 billion in 2025 and estimated to grow from USD 6.92 billion in 2026 to reach USD 8.41 billion by 2031, at a CAGR of 3.97% during the forecast period (2026-2031).

Universal pharmacare, population ageing and rapid device innovation act together to keep demand on a stable upward track. Federal coverage for diabetes medicines, provincial funding for continuous glucose monitoring (CGM) and insulin pumps, and the arrival of once-weekly insulins are broadening patient access while lifting revenue visibility for suppliers. Strategic alliances that join sensors, pumps and decision-support software are reshaping competitive boundaries, and private insurers have started testing premium models tied to glycemic outcomes. Nevertheless, disparate provincial tendering practices, high out-of-pocket insulin costs and privacy concerns in cloud-based monitoring continue to temper the adoption pace.

Key Report Takeaways

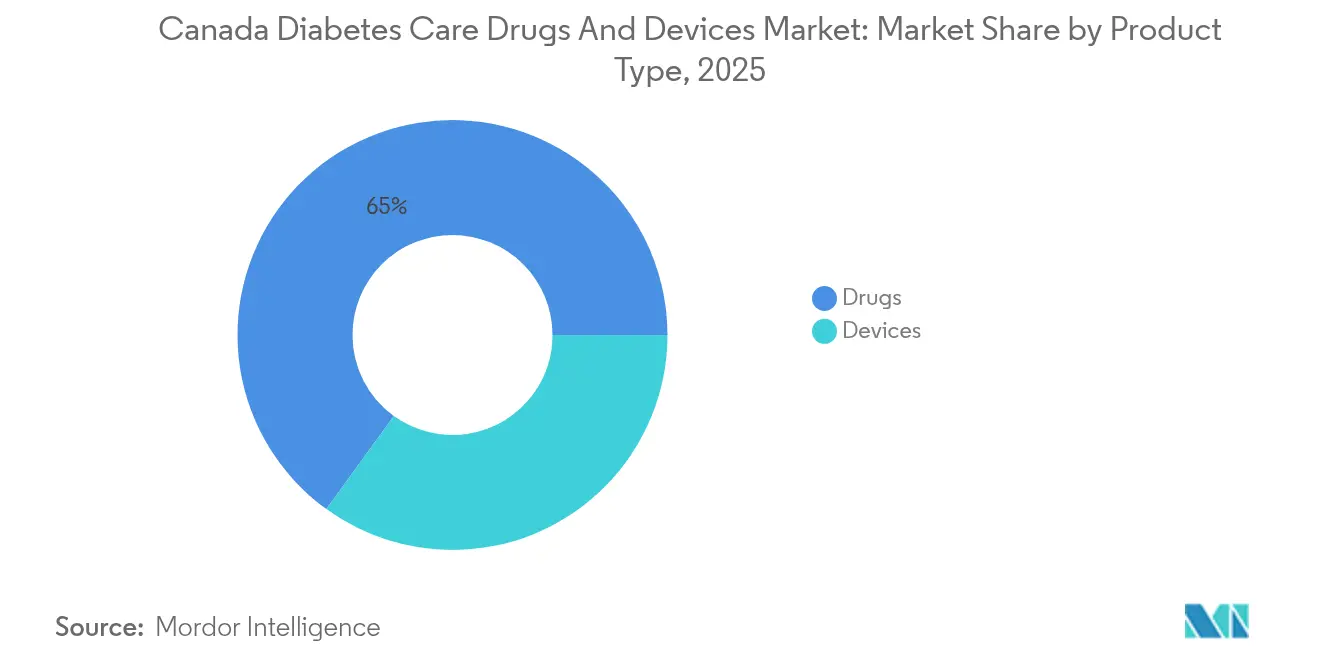

- By product type, drugs accounted for 65.02% of the Canada diabetes care drugs and devices market share in 2025, whereas devices are projected to grow at a 4.74% CAGR to 2031.

- By diabetes type, Type 2 dominated with 89.85% revenue share in 2025; Type 1 is expected to advance at a 4.86% CAGR through 2031.

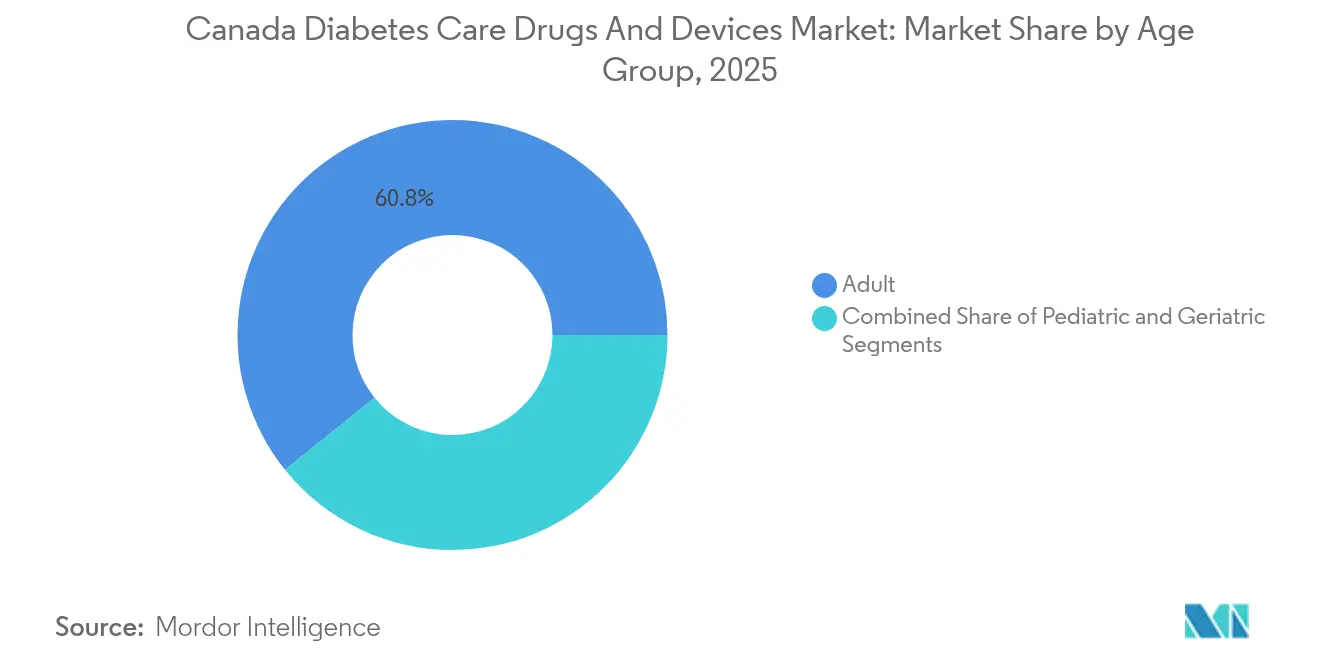

- By age group, adults held 60.78% share of the Canada diabetes care drugs and devices market size in 2025, while the geriatric cohort is poised for 4.92% CAGR expansion.

- By distribution channel, offline retail and hospital pharmacies captured 73.62% share in 2025; online platforms exhibit the highest growth at 4.95% CAGR, supported by subscription-based CGM offerings.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Diabetes Care Drugs And Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of Type-2 diabetes | +1.2% | National, with higher concentration in Ontario, Quebec, Alberta | Long term (≥ 4 years) |

| Government reimbursement expansion for CGM & pumps | +0.8% | Provincial variations, with BC and Nova Scotia leading | Medium term (2-4 years) |

| Uptake of once-weekly and oral GLP-1s | +0.7% | National, with urban centers showing faster adoption | Medium term (2-4 years) |

| Digital-therapeutic integrations with HbA1c-linked insurance premiums | +0.4% | National, with private insurance markets in Ontario, Alberta | Short term (≤ 2 years) |

| Venture investment surge in Canadian diabetes tech start-ups | +0.3% | Concentrated in Toronto, Vancouver, Montreal tech hubs | Short term (≤ 2 years) |

| AI-driven closed-loop for smart pens and phone ecosystems | +0.5% | National, with early adoption in metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Type 2 Diabetes

Diagnosed cases are set to jump from 4 million in 2024 to 5.2 million by 2030, equal to nearly 13% of Canadian adults. Indigenous communities face a 17.2% prevalence rate, and Black Canadians experience double the mortality risk compared with white Canadians. More than 7,700 diabetes-related lower-limb amputations occur each year, 85% of which are preventable with timely intervention [1]Canadian Institute for Health Information, “Lower-Limb Amputations Among Adults with Diabetes,” cihi.ca. Provincial disparities widen market opportunities—for example, Saskatchewan already counts 29% of residents living with diabetes or pre-diabetes, while Alberta’s 28% prevalence equates to 587,710 diagnosed patients and USD 556 million in direct medical costs. Over the next decade, the economic burden is forecast to exceed USD 15.3 billion, underscoring the value of preventive devices and integrated care models that demonstrate measurable outcome improvements.

Government Reimbursement Expansion for CGM & Pumps

Nova Scotia broadened public funding for insulin pumps and CGM in February 2024, and Saskatchewan now fully covers Dexcom G6 and G7 sensors for eligible residents, eliminating out-of-pocket costs [2]JDRF Canada, “Insulin Pump and CGM Coverage Expands in Nova Scotia,” jdrf.ca . FreeStyle Libre 2 is publicly reimbursed in most provinces; Ontario’s drug program funds 33 sensors a year for insulin-dependent patients, while Quebec reimburses children under 18 and adults on intensive insulin therapy. In British Columbia, a four-year USD 670 million pharmacare deal will deliver universal diabetes coverage from March 2026.

Uptake of Once-Weekly and Oral GLP-1s

Health Canada cleared Awiqli, the world’s first once-weekly insulin icodec, in March 2024. The therapy lists at USD 1,350 per year and reduces injection frequency from 365 to 52 doses. Ozempic revenues climbed 26% to DKK 120.3 billion in 2024, reflecting strong GLP-1 momentum, whereas Lilly’s Mounjaro delivered USD 3.09 billion in Q2 2024 sales [3]Eli Lilly and Company, “Q2 2024 Earnings Release,” lilly.com . University of British Columbia scientists are advancing an oral insulin drop that exploits sublingual absorption, potentially altering administration patterns for 11.7 million Canadians living with diabetes or pre-diabetes.

Digital Therapeutics Linked to Insurance Premiums

Medavie Blue Cross attributes 11% of claims spending to diabetes drugs, with the ave rage claimant cost reaching USD 1,534 in 2024. Its 360 Total Care program marries drug coverage with virtual coaching, showcasing how digital platforms translate adherence gains into measurable payor savings. Machine-learning algorithms such as XGBoost have begun powering predictive models for glycemic excursions, letting insurers adjust premiums against real-time HbA1c metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket cost for long-acting analog insulins | -0.6% | National, with higher impact in provinces with limited coverage | Long term (≥ 4 years) |

| Fragmented provincial tendering delays device adoption | -0.4% | Provincial variations, particularly affecting smaller provinces | Medium term (2-4 years) |

| Data-privacy concerns slowing cloud-based monitoring | -0.3% | National, with higher concern in Quebec due to language laws | Short term (≤ 2 years) |

| Limited French-language support in mobile apps affecting Québec uptake | -0.2% | Quebec-specific, affecting 23% of Canadian population | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost for Long-Acting Analog Insulins

Canadian spending on antidiabetic drugs doubled to USD 2.7 billion between 2012 and 2021, with list prices remaining above peer-country levels, adding USD 703 million in excess costs. Blood-glucose test strips average USD 0.79 each, yet reimbursement thresholds differ widely by province, and Quebec residents pay nearly USD 500 per month for Ozempic when prescribed for weight management rather than diabetes. Downstream complications inflate system expenses; diabetes-related amputations alone exceed USD 750 million annually.

Fragmented Provincial Tendering Delays Device Adoption

Each province runs its own tender and formulary process, producing variable timelines for CGM and hybrid closed-loop coverage. CADTH projects that fully funding closed-loop systems would raise public spending by USD 823 million over three years, a hurdle that slows coordinated uptake. Different prior-authorization rules and age cut-offs force suppliers to navigate 15 distinct public plans, stretching administrative lead times and eroding the scale benefits of nationwide launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Drive Innovation Despite Drug Dominance

Drugs captured 65.02% of the Canada diabetes care drugs and devices market share in 2025, reflecting entrenched use of insulin analogues and GLP-1 receptor agonists. Novo Nordisk’s diabetes care division posted DKK 290.4 billion in 2024 sales, a 25% jump that underscores the segment’s resilience. Still, the devices category is slated for the fastest advance at a 4.74% CAGR to 2031. Monitoring devices form the largest slice; CGM adoption continues to displace finger-stick meters as public and private plans expand reimbursement coverage. Management devices such as hybrid closed-loop pumps are scaling quickly, helped by Abbott–Medtronic integration that links FreeStyle Libre sensors to automated delivery algorithms, broadening the addressable user base and opening a USD 100 million incremental sales channel for Abbott.

Market participants are refining go-to-market tactics. Abbott emphasizes affordability to penetrate the Type 2 population, whereas Dexcom keeps focus on the intensive insulin cohort where alarm accuracy and real-time data sharing command premium pricing. Tandem Diabetes Care’s t:slim X2 pump integrated with Dexcom G7 won notice among Canadian endocrinologists because software upgrades are delivered online, cutting replacement cycles and supporting iterative innovation. Collectively, these trends keep the devices segment central to value creation even though drugs still dominate total revenue.

By Diabetes Type: Type 1 Innovation Drives Disproportionate Growth

The Canada diabetes care drugs and devices market size for Type 2 patients accounted for USD 5.98 billion in 2025, equal to 89.85% of total market revenue. Expanded GLP-1 indications for cardiovascular and renal protection reinforce this concentration, yet Type 1 is positioned for a faster 4.86% CAGR, powered by technology-intensive therapy. Health Canada approved Insulet’s Omnipod 5 automated insulin delivery system in April 2024, giving Type 1 users a tubeless option that integrates with Dexcom sensors and smartphone control. Type 1 households show higher device penetration because sustained exogenous insulin demands favour adoption of closed-loop systems that reduce hypo- and hyper-glycemic excursions.

Within Type 2, weekly insulins and oral GLP-1s are attracting patients who previously relied solely on tablets. Cardiovascular-outcome data for semaglutide and dapagliflozin have made combination therapy more common in primary care. Gestational diabetes care remains a small but technically dynamic subsegment; researchers reviewing 15 mobile apps found only three offered culturally relevant features, highlighting product gaps for diverse Canadian families. Vendors able to overlay French and Indigenous-language support may capture outsized loyalty in Quebec and remote communities respectively.

By Age Group: Geriatric Segment Accelerates Amid Demographic Shift

Adults aged 18-64 controlled 60.78% of market revenue in 2025, yet the geriatric cohort is on course for 4.92% CAGR growth. Population ageing, multi-morbidity and longer life expectancy keep clinical complexity high among seniors, driving demand for simplified dosing and automated monitoring solutions. Telehealth adoption among older adults accelerated after COVID-19, with established physician relationships cited as a chief facilitator even as sensory and dexterity limitations complicate device training.

For working-age adults managing Type 1 diabetes, remote peer-support initiatives such as the TRIFECTA program improved quality-of-life metrics in early trials, showing how digital forums reinforce adherence outside clinical settings. Pediatric volumes remain comparatively small but carry high long-term lifetime value, since early positioning of pump-CGM bundles can lock in brand preference for decades. However, coverage gaps in some provinces still push families toward charitable funding channels, an issue advocacy groups lobby to rectify through broader pharmacare equity.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Offline channels—chain pharmacies, hospital dispensaries and durable medical equipment retailers—retained 73.62% of sales in 2025. Direct-billing agreements with public plans shield patients from immediate out-of-pocket costs, and in-store diabetes educators provide set-up and training services. Online sales, while smaller, are expanding at 4.95% CAGR to 2031 as consumer comfort with e-commerce and tele-consults improves. Dexcom’s Canadian subscription bundles ship sensors and transmitters to households on a scheduled cadence and offer financing plans that reduce upfront burden.

AI-driven recommendation engines underpin many digital pharmacies, matching refill reminders with glycemic-trend analytics to limit stock-outs and improve medication persistence. Still, rural broadband limitations, particularly in northern territories, constrain online penetration, requiring hybrid models that marry web ordering with local pick-up points or nurse-supported drop-offs.

Geography Analysis

Regional variation characterizes the Canada diabetes care drugs and devices market, as each province balances demographic realities with fiscal capacity. Ontario is the single largest market, serving nearly 1.5 million people with diabetes through programs that co-fund insulin pumps and CGM sensors under the Assistive Devices Program. Quebec follows, where French-language mandates and unique reimbursement algorithms force vendors to localize software interfaces and patient education; The Régie de l’assurance maladie du Québec administers more than 40 health schemes that include tailored diabetes coverage.

British Columbia’s USD 670 million pharmacare accord with Ottawa will take effect in March 2026, offering a template for universal diabetes coverage that other provinces are evaluating. Alberta faces an estimated USD 556 million annual cost burden tied to diabetes, prompting expanded CGM eligibility under its insulin therapy benefit.

Saskatchewan offers full public funding for Dexcom G6 and G7 sensors to residents aged 18-25 and those over 65, a configuration that eliminates many affordability concerns. Atlantic provinces, led by Nova Scotia, are rapidly enhancing pump and CGM programs to address ageing populations scattered across rural geographies. In the North, tele-endocrinology pilots and culturally adapted education materials aim to narrow outcome gaps among Indigenous communities where prevalence exceeds national averages.

Regulatory Landscape

Health Canada regulates diabetes medicines, devices, and drug-device combination products under the Food and Drugs Act, using either the Food and Drug Regulations or the Medical Devices Regulations based on the product's principal mechanism of action (PMOA). For products at the device-drug interface, Health Canada classification support (including the Health Product Classification Unit and, where applicable, the Therapeutic Products Classification Committee) helps define the submission pathway and evidence requirements, which is particularly relevant for connected insulin delivery, CGM, and automated insulin delivery systems.

Recent approvals and label expansions have widened the regulated product set in Canada across both drugs and devices. In 2026, Health Canada authorized additional options that can influence formulary and tender dynamics, including an expanded cardiovascular risk-reduction indication for semaglutide products (Rybelsus in January 2026 and Ozempic in March 2026), authorizations for generic semaglutide injections (Health Canada announcements in April 2026 and May 2026), and CGM-related device authorizations such as Dexcom G7 15 Day (July 2026). On the device-therapy side, Medtronic reported a Health Canada license for Simplera Sync sensor integration with the MiniMed 780G system for a Type 2 diabetes indication (April 2026), adding to the set of regulated automated and connected-care configurations entering the market.

Competitive Landscape

The Canada diabetes care drugs and devices industry features a fragmented supply side. Top pharmaceutical players—Novo Nordisk, Eli Lilly and Sanofi—control most insulin and GLP-1 revenue. On the device front, Abbott and Dexcom form an effective duopoly in CGM, yet they pursue different population segments to avoid direct overlap. Abbott’s FreeStyle Libre focuses on cost-sensitive Type 2 users, while Dexcom targets accuracy-driven Type 1 patients.

Strategic alliances now blur boundaries: Abbott’s partnership with Medtronic allows FreeStyle Libre sensors to feed Medtronic’s closed-loop algorithms, a move projected to generate at least USD 100 million in incremental annual revenue for Abbott. Insulet’s Omnipod 5 and Tandem’s t:slim X2 secure competitive positions by enabling software updates over the air, shortening product cycles and keeping users within branded ecosystems. Start-ups out of Toronto, Vancouver and Montreal attracted fresh venture capital in 2024 to develop culturally specific decision-support apps, though privacy and bilingual design add scaling complexity.

Entry hurdles remain material. Suppliers must pass Health Canada’s device class reviews and adjust marketing to meet Quebec language law, while disparate tender calendars across 13 jurisdictions dilute launch efficiency. Companies able to align multi-channel reimbursement dossiers, bilingual user support and robust cloud-security assurances are more likely to command durable share.

Canada Diabetes Care Drugs And Devices Industry Leaders

Roche

Sanofi

Novo Nordisk

Abbott Laboratories

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

National pharmacare actions and provincial bilateral agreements create whitespace for suppliers that can align evidence generation with reimbursement requirements across drugs, devices, and integrated ecosystems. The Pharmacare Act framework, along with federal communications on universal access to diabetes medications and a diabetes device fund, increases the importance of coverage pathways for supplies and advanced technologies such as CGM and hybrid closed-loop systems. Canada’s Drug Agency (formerly CADTH) continues to shape reimbursement criteria through health technology reviews and recommendations, which raises the bar for manufacturers to provide comparative clinical and real-world evidence for rtCGM, isCGM, and automated insulin delivery performance in Canadian practice.

Product and pricing dynamics also add access levers for suppliers, especially where payors evaluate total cost of care. Health Canada authorizations for generic semaglutide injections in 2026 provide a specific affordability lever for public plans and private insurers. At the same time, new device authorizations and funding decisions expand the eligible monitored population and create room for subscription and direct-to-patient fulfillment models. Suppliers that combine bilingual patient support (including Quebec localization), cloud-security assurances, and outcomes data compatible with public reimbursement dossiers and private payer programs (for example, digital coaching paired with drug coverage) can differentiate within Canada’s fragmented provincial procurement environment.

Recent Industry Developments

- July 2026: Dexcom received Health Canada authorization for the Dexcom G7 15 Day continuous glucose monitoring system, extending wear duration for adults living with diabetes. The authorization strengthens Dexcom’s product ladder in Canada and increases competitive pressure in CGM tenders as provinces weigh cost, wear-time, and data-continuity trade-offs.

- May 2025: Sanofi Canada announced Health Canada approval (Notice of Compliance) for Tzield (teplizumab) to delay stage 3 type 1 diabetes in adults and children aged 8 years and older. The introduction of a disease-modifying therapy expands the Canada diabetes care market beyond glucose control and adds new reimbursement and specialist-care pathways tied to earlier-stage identification.

- June 2024: Novo Nordisk launched Awiqli (insulin icodec) in Canada as a once-weekly basal insulin for adults with diabetes mellitus. Fewer injections shift adherence and persistence conversations and can influence payer contracting and patient preference within the basal insulin segment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of diabetes care drugs and diabetes care devices sold in Canada for managing and monitoring diabetes. It is measured as annual revenue in USD across all sales channels, based on products used by patients and prescribed or recommended by care teams.

Scope exclusions: Veterinary diabetes products, bariatric surgical products, and lifestyle coaching services that do not include a drug or device sale are excluded.

Segmentation Overview

- By Product Type

- Devices

- Monitoring Devices

- Self-Monitoring Blood Glucose Meters

- Continuous Glucose Monitoring Systems

- Management Devices

- Monitoring Devices

- Drugs

- Oral Anti-Diabetic Drugs

- Insulin Drugs

- Non-Insulin Injectables

- Combination Drugs

- Devices

- By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

- By Age Group

- Adult

- Geriatric

- Pediatric

- By Distribution Channel

- Offline

- Online

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the first draft of the demand pool and pricing logic that later gets checked in interviews. Public health and utilization signals were taken from sources such as the Public Health Agency of Canada and Statistics Canada, and reimbursement context was reviewed using provincial drug plan and formulary publications.

To keep the product boundary clean, we also used sources such as Health Canada databases for approvals and safety updates, the Canadian Institute for Health Information for care setting indicators, and peer reviewed clinical and outcomes literature that discusses therapy patterns and monitoring adoption. On the supply and trade side, we referenced company filings and investor materials for Canada exposure, plus selective use of paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export data when it helped confirm device flow and pricing direction. The specific sources listed here are illustrative, and many other public documents and datasets were also reviewed for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what is actually used in practice across Canada and how quickly newer therapy and monitoring options are moving into routine care. We spoke with a mix of manufacturers, distributors, pharmacy and procurement stakeholders, and clinicians, and then used those inputs to test adoption rates, average selling price movements, and channel mix assumptions across provinces.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 20% | |

| Mid tier: 47% | Functional/Unit leaders: 23% | |

| Smaller Players: 20% | Managers: 57% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs Canada sales from the treated diabetes population and the share receiving each therapy approach, and then extends that logic into device usage tied to monitoring frequency and insulin delivery needs. The model is then corroborated with selective bottom-up checks, such as supplier and channel roll ups in key categories, and sampled ASP times volume math for strips, sensors, pens, and pumps, which helps us catch over-counting.

Key inputs used in the model include diagnosed prevalence and therapy eligible cohorts, insulin versus non-insulin treatment mix, SMBG strip consumption per active user, continuous glucose monitoring penetration and sensor change intervals, pump and pen utilization, and average unit price progression after reimbursement or tender changes. When category detail is missing, gaps are handled by using proxy utilization from comparable provinces and then adjusting it using interview guidance on access and prescribing behavior. Forecasts were built using scenario analysis around adoption curves and pricing, supported by short time series smoothing for stable categories where utilization changes slowly, and the final outlook is aligned to expert consensus on what is practical in the next few years.

Data Validation & Update Cycle

Outputs are checked through multiple passes so obvious inconsistencies are caught early. We compare category totals against independent signals like public health prevalence trends, formulary and reimbursement changes, import and shipment direction for devices, and major product lifecycle events, and then investigate variances before the model is signed off.

If a number moves outside a reasonable range, the assumptions behind penetration, usage intensity, or pricing are revisited and relevant respondents are re-contacted for clarification. Reports are refreshed annually, and interim updates are made when there are material events that can shift demand or pricing. Before delivery, an analyst completes a final review pass so clients receive the most current view available at the time.

Mordor Intelligence's Canada Diabetes Care Drugs and Devices Market Size Compared With Other Published Estimates

Published market values for Canada diabetes care often do not match because teams draw the boundary in different places and they also do not always line up their year, currency timing, and pricing steps. Differences also show up when one estimate leans more on broad spending proxies, while another tries to tie revenues back to product usage.

Prescription mix signals, CGM and strip usage intensity checks, and cross-checks against import flows for device hardware are the kinds of evidence that keep Mordor Intelligence's estimate anchored to what gets consumed in Canada and what is actually paid for through channels. Gaps usually come from including adjacent categories like pure wellness services or broader endocrine care, using a faster adoption curve for CGM and pumps without validating refill and replacement cycles, or applying average price lifts that do not reflect provincial reimbursement pressure and tender dynamics.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.66 B (2025) | |

| Industry Data Publisher A | USD 6.97 B (2025) | Uses a broader "devices and therapeutics" framing that can fold in extra diagnosis and monitoring items and applies a higher near-term growth narrative, which can inflate the current-year total if replacement cycles and reimbursement effects are not fully normalized. |

| Market Research Firm B | USD 5.35 B (2024) | Starts from a different base year and can apply a narrower counted scope or more conservative pricing, which lowers the value when inflation timing and channel mix (retail versus institutional) are handled differently. |

Taken together, the spread is best explained by scope boundaries and how usage and pricing are translated into revenue for each product group. By keeping therapy uptake, monitoring frequency, and device replacement cycles explicit in the model, the final number stays traceable to clear inputs that can be reviewed and repeated over time.

Key Questions Answered in the Report

How large is the Canada diabetes care drugs and devices market in 2026?

The Canada diabetes care drugs and devices market size stands at USD 6.92 billion in 2026 and is projected to reach USD 8.41 billion by 2031.

Which segment holds the biggest Canada diabetes care drugs and devices market share?

Drugs led with 65.02% share in 2025, while devices are expanding faster at a 4.74% CAGR through 2031.

What is driving growth in CGM adoption across Canada?

Provincial reimbursement expansion, falling sensor prices and partnerships that integrate CGM data with insulin pumps are key drivers.

Why is Type 1 diabetes showing faster growth than Type 2?

Type 1 patients adopt premium technologies—including closed-loop pumps—at higher rates, pushing a 4.86% CAGR despite smaller population size.

How will universal pharmacare affect the competitive landscape?

National coverage lowers patient cost barriers, increases prescription volumes and encourages multi-province procurement, benefiting scale-ready suppliers.

What challenges do manufacturers face in Quebec?

French-language requirements for apps and manuals, plus distinct reimbursement criteria, demand additional localisation investment before product launch.

Page last updated on: