Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

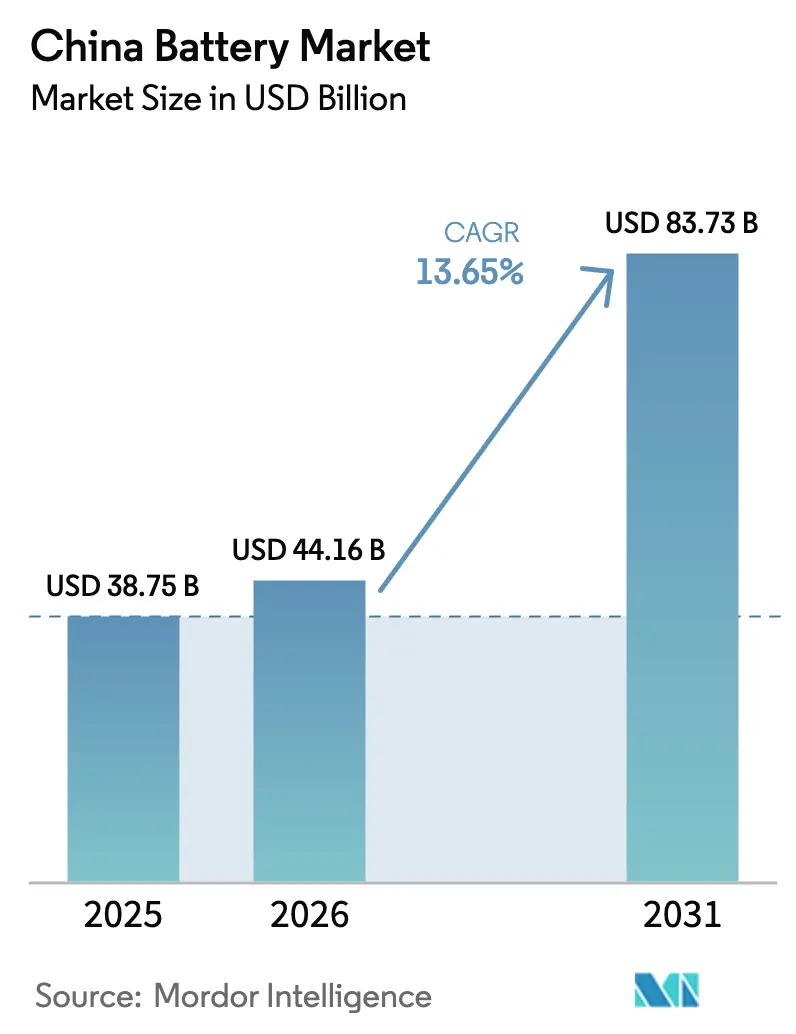

| Base Year Market Size (2025) | USD 38.75 Billion |

| Market Size (2026) | USD 44.16 Billion |

| Market Size (2031) | USD 83.73 Billion |

| Growth Rate (2026 - 2031) | 13.65% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Battery Market Analysis by Mordor Intelligence

The China Battery Market was valued at USD 38.75 billion in 2025 and expected to grow from USD 44.16 billion in 2026 to reach USD 83.73 billion by 2031, at a CAGR of 13.65% during the forecast period (2026-2031).

The expansion is driven by nationwide new-energy-vehicle (NEV) mandates that widen lithium-ion adoption into second- and third-tier cities, a grid-scale storage boom designed to absorb renewable curtailment, and vertical integration strategies that compress supply-chain costs. Aggressive capacity additions totaling 1.3 TWh have lowered cell production lead times but have also raised the risk of near-term oversupply that could pressure margins. Provincial recycling quotas enacted in 2024 enhance secondary raw-material streams, easing reliance on imported lithium and reinforcing the closed-loop advantage for integrated manufacturers. Preferential value-added-tax (VAT) rebates on domestic cathode precursors further tilt cost curves in favor of local suppliers.

Key Report Takeaways

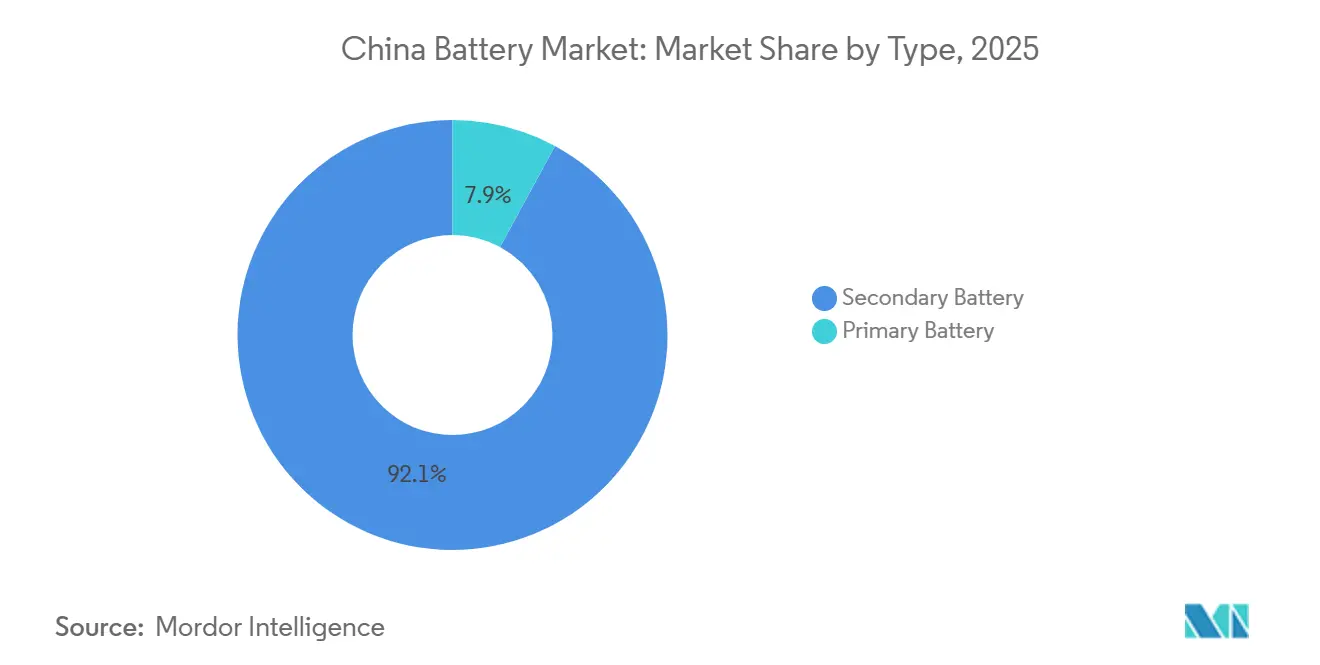

- By type, secondary batteries held 92.1% of China's battery market share in 2025; primary batteries are forecast to trail at a single-digit CAGR through 2031.

- By technology, lithium-ion dominated with a 75.5% share in 2025, while sodium-ion is expected to register the fastest CAGR of 18% between 2026 and 2031.

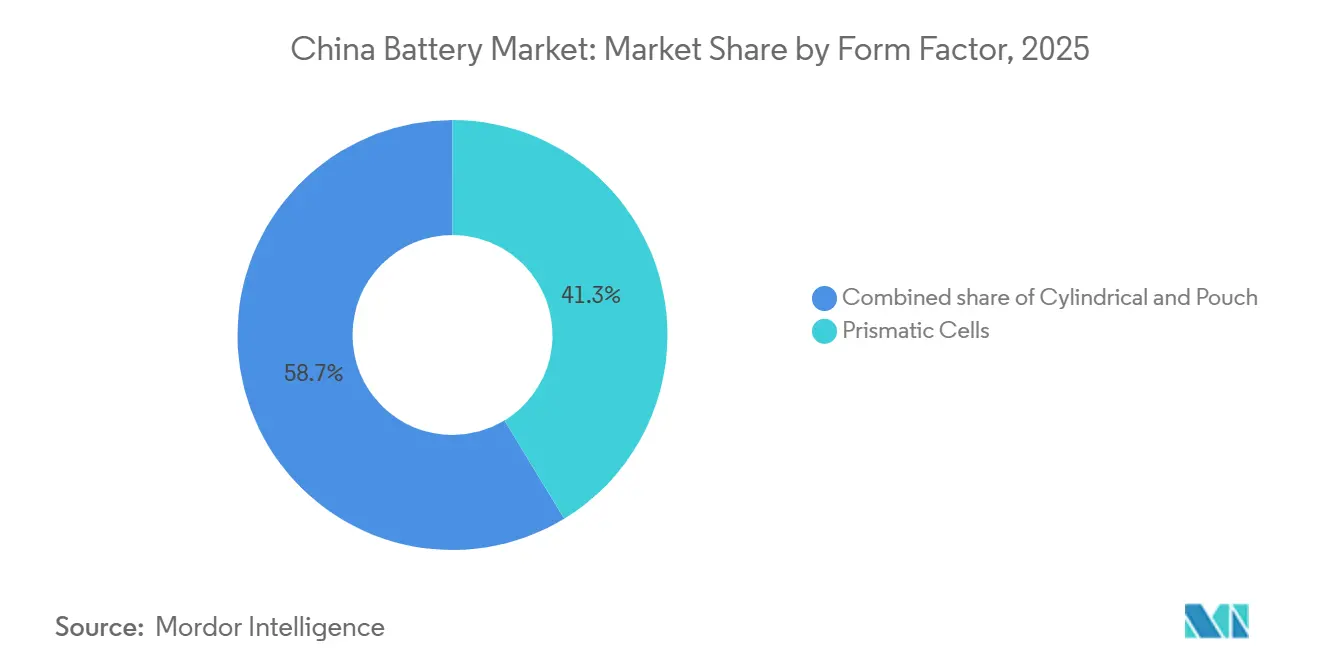

- By form factor, prismatic cells led with 41.3% revenue share in 2025, whereas pouch cells are projected to expand at an 18.1% CAGR.

- By application, automotive accounted for 60.2% of China's battery market size in 2025, and energy storage systems are set to advance at a 16.5% CAGR through 2031.

- By company, Contemporary Amperex Technology Co. Limited retained 36.7% of the China battery market share in 2025, and BYD followed with 17.9%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nationwide NEV Mandates Driving Lithium-Ion Demand Surge in Tier-2 & 3 Cities | +3.2% | National, with accelerated adoption in Jiangsu, Zhejiang, Sichuan, Hubei | Medium term (2-4 years) |

| Grid-Scale Storage Boom Triggered by 30% Renewable Curtailment Targets | +2.8% | National, concentrated in Inner Mongolia, Gansu, Xinjiang, Qinghai | Medium term (2-4 years) |

| Price Parity of LFP Packs (< USD 80/kWh) Accelerating Lead-Acid Replacement | +2.1% | National, strongest in industrial and two-wheeler segments | Short term (≤ 2 years) |

| Vertical Integration by CATL & BYD Reducing Supply-Chain Bottlenecks and Costs | +1.9% | National, with spillover to Southeast Asia manufacturing hubs | Long term (≥ 4 years) |

| Provincial Recycling Quotas Creating Secondary Raw-Material Stream for New Cells | +1.5% | National, early implementation in Guangdong, Jiangsu, Shandong | Long term (≥ 4 years) |

| Preferential VAT Rebate on Domestic Battery Materials Boosting Local Production | +1.2% | National, benefiting cathode and anode material producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Nationwide NEV Mandates Driving Lithium-Ion Demand Surge In Tier-2 And Tier-3 Cities

Tier-2 and Tier-3 municipalities now match coastal EV adoption targets, propelled by 2024 subsidies that cover up to 15% of battery pack costs. Sixty percent of China’s vehicle sales occur in these cities, making infrastructure pivotal; 120,000 public fast-charging stations deployed in 2025 eliminated range anxiety and unlocked an estimated 50 GWh of new cell demand. Automakers responded with sub-USD 15,000 models fitted with 40-50 kWh LFP packs, delivering total-cost-of-ownership parity with internal-combustion cars. Battery makers strategically position gigafactories near local assembly lines, shrinking logistics costs and compressing delivery cycles. This localization fragments market share, allowing smaller suppliers to secure captive contracts and challenge incumbents outside coastal hubs.

Grid-Scale Storage Boom Triggered By 30% Renewable Curtailment Targets

Curtailment rates reached 30% in renewable-rich provinces during 2024, prompting mandatory co-located storage for projects above 100 MW. Utility-scale battery installations hit 73.76 GW in 2024 and are on course for 180 GW by 2027. CATL’s Tener LFP system delivers 6,000 cycles, matching 15-year power-purchase agreements and lowering coal-peaking reliance. Adoption of pouch cells improves thermal management and shrinks container footprint by 20% compared with prismatic equivalents. Enforcement of GB 44240-2024 safety norms in August 2025 accelerates modern system uptake, as legacy installations failed propagation tests.

Price Parity Of LFP Packs Accelerating Lead-Acid Replacement

Pack-level LFP costs slipped below USD 80/kWh in early 2025, undercutting lead-acid alternatives on a lifecycle basis. The 3,000-cycle longevity of LFP trounces the 500-cycle life of lead-acid, eliminating the latter’s upfront cost edge. Industrial forklifts, telecom towers, and two-wheelers retrofitted LFP modules, creating an incremental 15 GWh of demand in 2025. BYD’s Blade Battery reached USD 75/kWh by removing module housings, driving legacy suppliers to pivot or exit. Lead-acid’s share slid from 18% in 2024 to 12% in 2025, and forward cost curves signal further erosion toward 2027.

Vertical Integration By CATL And BYD Reducing Supply-Chain Bottlenecks And Costs

Backward integration into lithium refining and separator film production trims bill-of-material costs by up to 15% versus non-integrated peers. CATL’s Jiangxi hydroxide facility secured 40,000 t/yr, sheltering margins from lithium spot volatility. BYD’s in-house separator lines cut lead times to four weeks, enabling rapid new-product introduction. The companies’ recycling plants re-inject recovered metals, lowering virgin-material purchases by 20% by 2027. Smaller rivals lack capital for end-to-end footprints and remain exposed to input shocks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imminent Overcapacity Risk from 1.3 TWh Announced Cell Plants Depressing Margins | -2.4% | National, with acute pressure in Jiangsu, Guangdong, Fujian | Short term (≤ 2 years) |

| Regulatory Cap on New Coal-Power for Cathode Processing Limiting Energy Cost Advantage | -1.6% | National, concentrated in Hunan, Sichuan, Yunnan cathode hubs | Medium term (2-4 years) |

| Critical Mineral Import Volatility amid Indonesia & DRC Export Policy Shifts | -1.3% | National, with upstream exposure in nickel and cobalt supply chains | Medium term (2-4 years) |

| Intensifying IP Litigation on Solid-State Electrolyte Patents Delaying Commercialization | -0.9% | National, affecting R&D timelines for CATL, BYD, CALB, WeLion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imminent overcapacity risk from 1.3 TWh cell plants depressing margins

Planned capacity outstrips 2026 demand of 600 GWh, implying sub-50% utilization and a price ceiling near USD 70/kWh that could trigger distress among thinly capitalized producers.[1]Staff Reporter, “Battery Overcapacity Looms,” Bloomberg, bloomberg.com Policy barriers restrict export relief, and anti-dumping tariffs in the United States and Europe narrow outlets for surplus cells. Larger incumbents can carry negative margins temporarily, but smaller firms risk liquidity crunches by 2027. The dynamic echoes the solar shakeout of the 2010s, where overbuild forced consolidation. Asset sales and restructurings are likely once creditors enforce covenants.

Regulatory Cap On New Coal-Power For Cathode Processing Limiting Energy Cost Advantage

The 2024 halt on coal plants in cathode hubs raises power tariffs by up to 40%, erasing China’s historical energy-cost edge over overseas rivals.[2]Staff Reporter, “CATL Launches Million-Mile Cell,” Bloomberg, bloomberg.com Precursor calcination consumes 15 kWh/kg, so cost inflation pushes producers to relocate to hydropower provinces or import renewables at premium rates. Expansion timelines slip by 18 months as firms await clean-power permits, reducing near-term supply elasticity. The rule narrows the landed-cost gap for high-nickel chemistries produced in Korea and Japan, shifting some demand offshore. Producers must accelerate energy-efficiency upgrades or face margin erosion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Secondary Batteries Anchor Market Structure

Secondary batteries occupied 92.1% of the Chinese battery market share in 2025, expanding at a projected 13.9% CAGR as NEV penetration hit 38% of passenger-car sales. Primary batteries remain niche, constrained by regulatory disposal costs and miniaturization of energy-harvesting devices. CATL’s Qilin cell guarantees 1.5 million km, extending vehicle service life to 15 years and improving total ownership economics.[3]Staff Reporter, “Tesla’s Shanghai Megafactory Comes Online,” Reuters, reuters.com Second-life programs turn retired automotive packs into stationary assets, doubling revenue per kilowatt-hour harvested from each cell.

Lead-acid’s decline accelerates as LFP cycle life multiples erase remaining cost advantages. Electric two-wheelers retrofit lithium packs that pay back within 18 months, and industrial battery suppliers recorded 25% sales falls in 2025. The secondary segment’s CAGR is therefore chemistry-substitution driven rather than pure demand growth, underscoring the need for strategic positioning as legacy chemistries fade.

By Technology: Lithium-Ion Dominance Reshapes Chemistry Mix

Lithium-ion retained 75.5% share in 2025 and is forecast to grow at 14.8% through 2031, reinforcing its leadership in the Chinese battery market. Within lithium-ion, LFP captured roughly 70% of automotive cell shipments, buoyed by lower costs and cobalt-free bills of material. Blade and M3P variants extend LFP’s range applicability, eroding the nickel-rich chemistry share.

Sodium-ion commercial shipments started in 2025 at 160 Wh/kg, positioning the chemistry for sub-USD 10,000 vehicles and stationary storage where volumetric density is less critical. Solid-state remains pilot-scale due to IP disputes and manufacturing yields. Together, emerging chemistries diversify supply risk, though lithium-ion’s economic moat holds firm through 2031.

By Form Factor: Pouch Gains Ground On Flexibility

Prismatic cells led with 41.3% of the share in 2025, benefiting from entrenched automotive pack standards. However, pouch formats will post an 18.1% CAGR on weight savings and flexible geometries that raise volumetric efficiency by up to 8% per vehicle. LG Energy Solution and SK On champion pouch adoption via joint ventures that meet European OEM specifications.

Capital intensity remains higher for pouch lines, yet energy-density advantages justify premiums in performance-sensitive segments. CATL’s 2025 introduction of a pouch Qilin variant signals a strategic hedge against potential share loss, while cylindrical cells hold niche relevance in modular energy storage.

By Application: Energy Storage Systems Outpace Automotive Growth

Automotive allocated 60.2% of the China battery market size in 2025, but energy storage posts the highest 16.5% CAGR as grid operators target 180 GW of installed capacity by 2027. Passenger cars account for three-quarters of automotive demand, yet logistics fleets grow quickly under zero-emission zones.

Utility-scale storage, averaging 100 MWh installations, captures 70% of the segment and cycles daily to shift solar output to evening peaks. Industrial batteries migrate from lead-acid to lithium, and portable electronics track device shipments. The application mix tilts toward stationary use, favoring cost-effective chemistries such as LFP and sodium-ion.

Geography Analysis

Guangdong anchors 55% of national cell output through BYD and CATL complexes, leveraging proximity to electronics supply chains. Jiangsu and Zhejiang specialize in pouch production for export-oriented automakers, while Sichuan and Hunan dominate cathode precursors near lithium and manganese deposits. Tesla’s 40 GWh Shanghai Megafactory underscores the imperative of local production to avoid tariffs.[4]Staff Reporter, “Tesla’s Shanghai Megafactory Comes Online,” Reuters, reuters.com

Provincial competition for investment fragments capacity across 20 provinces via land subsidies and tax holidays. Jiangsu’s 50% land discounts lured CALB’s 30 GWh expansion, while Sichuan offers hydropower contracts to attract low-carbon cathode projects. Recycling mandates requiring in-province processing spur localized hydrometallurgical plants, deepening closed-loop advantages.

Western provinces with high curtailment rates, such as Qinghai and Xinjiang, emerge as energy-storage hubs. Smaller manufacturers target these markets to avoid head-to-head competition with CATL and BYD in automotive clusters, trading scale for niche margins.

Competitive Landscape

Market concentration remains moderate as CATL controls 36.7% of the share and BYD holds 17.9%, yet more than 15 gigawatt-scale rivals sustain fierce price competition. CALB’s EUR 2 billion Portugal plant exemplifies internationalization to hedge against trade barriers, while EVE Energy’s cylindrical specialization delivered 22% revenue growth in 2025.

Vertical integration defines leadership strategy, allowing CATL and BYD to debut chemistries such as M3P in 18 months from lab to scale. Foreign entrants recalibrate China exposure in light of export controls exceeding 300 Wh/kg density thresholds, with Panasonic trimming shipments by 30% in 2025. Compliance with GB 44240-2024 thermal standards reorders competitiveness, favoring suppliers with robust safety engineering.

White-space opportunities persist in sodium-ion, solid-state, and ultra-fast-charging technologies where intellectual property remains unsettled, enabling agile firms to secure early licensing revenue. Consolidation pressure will intensify if overcapacity drives sustained sub-USD 70/kWh pricing.

China Battery Industry Leaders

-

Contemporary Amperex Technology Co Ltd

-

BYD Company Limited

-

CALB Group Co., Ltd.

-

EVE Energy Co Ltd

-

Gotion High tech Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CATL completed its Hong Kong IPO, raising HK$35.7 billion (USD 4.57 billion) to finance global expansion.

- March 2025: Researchers from China, in collaboration with Wuxi Beita Pharmatech and Northwest Normal University, unveiled a groundbreaking carbon-14 (C-14) nuclear battery prototype named “Zhulong-1.”

- November 2024: CATL and Chery announced a solid-state sodium-ion battery collaboration for 2027 commercialization.

- November 2024: BYD, CATL, and Huawei unveiled new sodium-ion initiatives, with BYD building a CNY 10 billion facility.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we define the China battery market as the revenue from new primary and secondary electro-chemical cells and assembled packs sold inside China for automotive, stationary storage, motive power, and consumer electronics uses. The scope covers lithium-ion, lead-acid, nickel metal hydride, sodium-ion, and early solid-state prototypes.

Scope exclusion: raw-material mining and refining, battery-manufacturing equipment, and standalone battery-management electronics are not counted.

Segmentation Overview

-

By Type

- Primary Battery

- Secondary Battery

-

By Technology

- Lead-acid Battery

- Lithium-ion Battery

- Other Technologies (Ni-MH, Zinc-air, Sodium-ion, Solid-State Prototype)

-

By Form Factor

- Cylindrical

- Prismatic

- Pouch

-

By Application

- Automotive (Passenger Electric Vehicles and Commercial Electric Vehicles)

- Energy Storage Systems (Utility-Scale and Commercial and Industrial)

- Industrial Batteries

- Portable Electronics

- Others (Medical Devices, Defence, Marine)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cell engineers, cathode suppliers, energy-storage integrators, and fleet operators across Guangdong, Jiangsu, Sichuan, and Hebei. These conversations validated utilization rates, emerging chemistries, average selling prices, and tender pipelines that secondary sources miss.

Desk Research

We began with high-credibility datasets, pulling monthly production and trade lines from MIIT, China Customs, and the China Energy Storage Alliance, and then cross-checking them with International Energy Agency supply tables. Company 10-K filings, provincial subsidy ledgers, and investor decks revealed shipment splits and price moves, while paid feeds such as D&B Hoovers and Questel traced revenue and patent trends that signal technology maturity. These examples illustrate our desk review; numerous other public releases and national statistics informed the model.

Market-Sizing & Forecasting

A top-down demand pool was built from NEV production counts, grid-storage tender gigawatt-hours, and telecom base-station rollouts, which are then split by chemistry through interview-derived penetration ratios. Because reported output often inflates prototype runs, we correct MIIT tallies with utilization figures before the numbers feed the model, and sampled supplier shipments multiplied by confirmed ASPs provide a bottom-up check that held totals within four percent. A multivariate regression using five drivers, EV output, storage additions, LFP pack price, lithium carbonate spot, and lead-acid displacement, projects values to 2030, with gaps bridged by weighted moving averages.

Data Validation & Update Cycle

Quarterly, our team reconciles outputs against fresh customs exports and CNESA dashboards, flags deviations exceeding two standard deviations, and reruns sensitivities; a full refresh is issued every year, with interim updates after major policy or capacity shifts.

Why Mordor's China Battery Baseline Commands Reliability

Published estimates differ because firms choose varying chemistries, price bases, and refresh cadences.

By anchoring revenues to factory-gate prices, aligning scope with domestic consumption, and updating annually, Mordor Intelligence reduces such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 38.75 B (2025) | Mordor Intelligence | - |

| USD 42.88 B (2024) | Regional Consultancy A | excludes primary cells and uses undiscounted pack markup |

| USD 37.26 B (2023) | Global Analytics B | older base year, no price normalization |

| USD 43.76 B (2025) | Trade Journal C | lithium-ion only, adds module assembly revenue |

These contrasts show that our disciplined scope control, live price normalization, and yearly refresh give decision-makers a dependable baseline that is tightly linked to observable production and pricing indicators.

Key Questions Answered in the Report

What is the current value of the China battery market?

The China battery market size stands at USD 44.16 billion in 2026.

How fast is the sector expected to grow?

The market is forecast to record a 13.65% CAGR between 2026 and 2031.

Which segment is expanding the fastest?

Energy storage systems lead growth with a 16.5% CAGR through 2031.

Why are pouch cells gaining traction?

Pouch formats offer 10-15% weight savings and flexible geometries that improve vehicle range.

What risks could slow market growth?

Overcapacity, critical mineral volatility, and solid-state patent litigation pose downside risks.

Page last updated on: