China Automotive Microcontroller Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

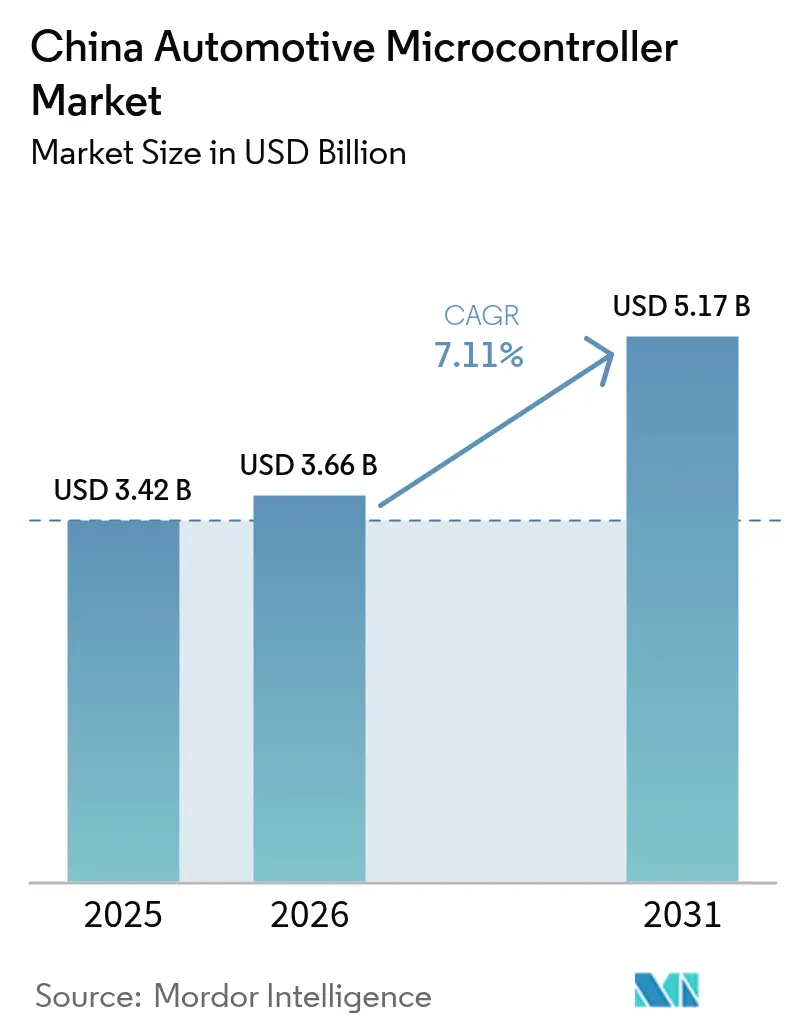

| Base Year Market Size (2025) | USD 3.42 Billion |

| Market Size (2026) | USD 3.66 Billion |

| Market Size (2031) | USD 5.17 Billion |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

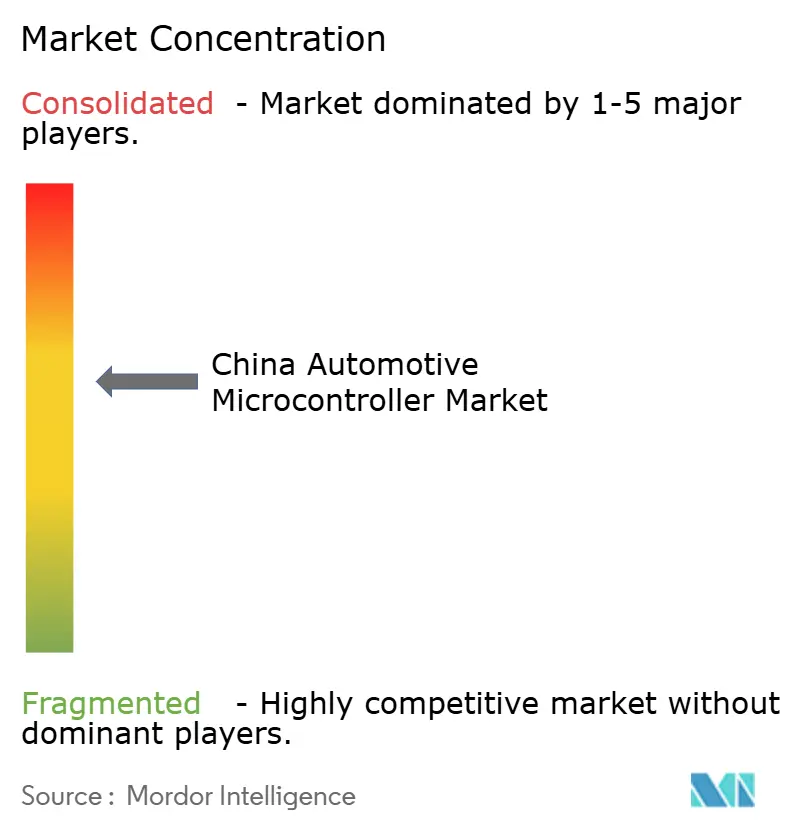

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Automotive Microcontroller Market Analysis by Mordor Intelligence

The China automotive microcontroller market size is expected to grow from USD 3.42 billion in 2025 to USD 3.66 billion in 2026 and is forecast to reach USD 5.17 billion by 2031 at 7.11% CAGR over 2026-2031. The upward curve reflects Beijing’s semiconductor self-reliance agenda converging with the world’s largest new-energy vehicle base, mounting demand for 32-bit and 64-bit chips, and a supportive regulatory push for ISO 26262-compliant devices. Firmware-rich battery packs, domain controllers, and zonal architectures are increasing silicon value per vehicle even as low-end body electronics commoditize. Competitive dynamics are shifting as GigaDevice, CEC Huada, and BYD Semiconductor gain ASIL-D credentials, forcing global incumbents to defend higher-margin safety and powertrain niches. At the same time, export-control frictions on sub-28-nanometer design tools temper the domestic supply chain’s speed of maturation.[1]Bloomberg News, “China Pushes Semiconductor Self-Sufficiency with $47 Billion Fund,” Bloomberg, bloomberg.com

Key Report Takeaways

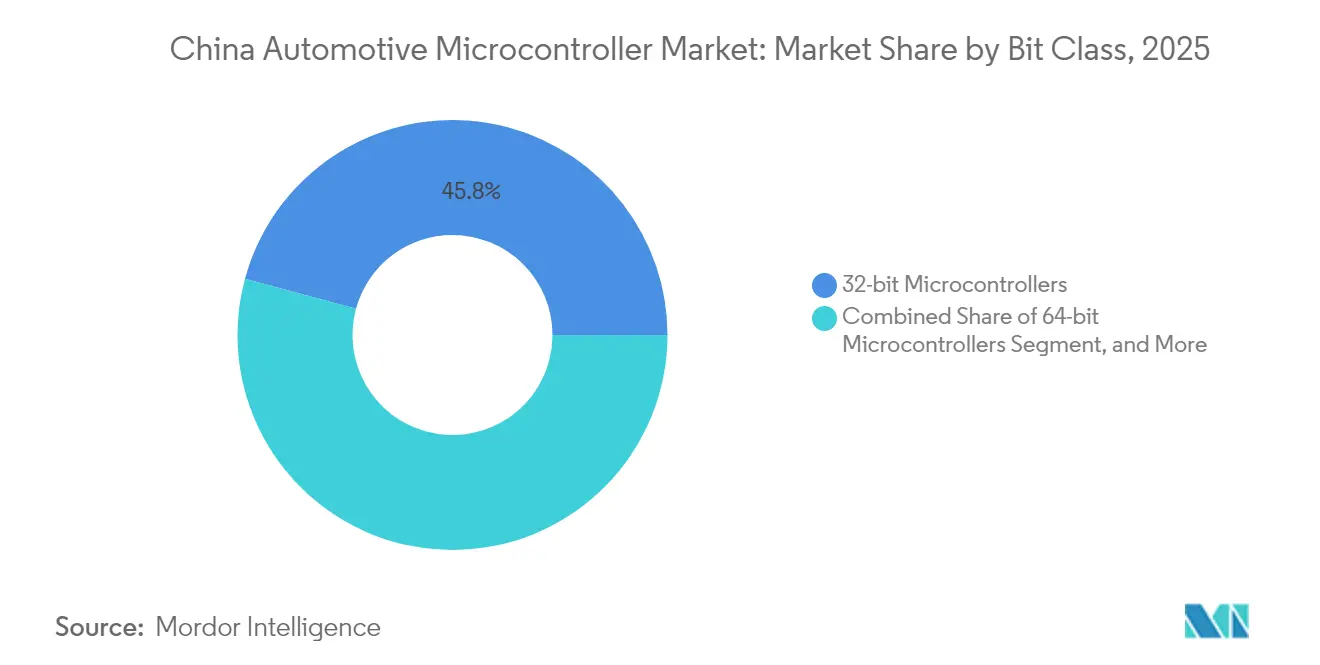

- By bit class, 32-bit devices led with a 45.78% share of China's automotive microcontroller market in 2025, while 64-bit chips are projected to grow at an 8.78% CAGR through 2031.

- By application, safety and ADAS captured a 34.05% revenue share in 2025, whereas battery management system controllers are projected to record the highest CAGR at 10.26% through 2031.

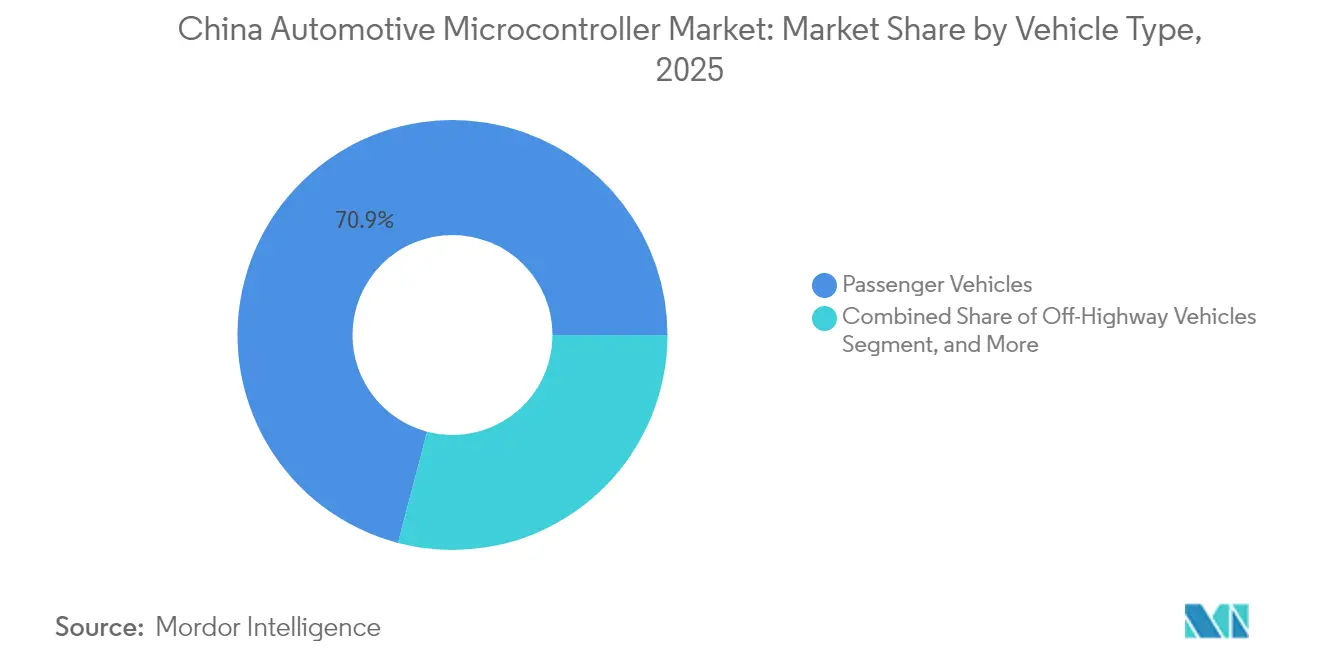

- By vehicle type, passenger cars accounted for 70.92% of the Chinese automotive microcontroller market size in 2025; off-highway equipment is expected to show the fastest CAGR of 8.28% from 2026 to 2031.

- By propulsion, internal-combustion platforms retained a 52.96% share in 2025; however, battery electric vehicles are expected to expand at an 11.05% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Automotive Microcontroller Market Trends and Insights

Drivers Impact Analysis*

| Growing adoption of new energy vehicles | +2.1% | National, Guangdong, Shanghai, Zhejiang, Jiangsu | Medium term (2-4 years) |

|---|---|---|---|

| Rising integration of advanced driver assistance systems | +1.6% | National, tier-1 cities and premium segments | Medium term (2-4 years) |

| Enforcement of stricter automotive safety regulations | +1.2% | National, aligned with GB standards and C-NCAP | Long term (≥4 years) |

| Government push for semiconductor self-sufficiency | +1.4% | National, MIIT and NDRC support | Long term (≥4 years) |

| Shift to zonal electrical architecture in smart vehicles | +0.9% | National, early BYD, NIO, XPeng, Li Auto adoption | Short term (≤2 years) |

| Emergence of domain controller-based platforms | +0.8% | National, premium and mid-tier segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of New Energy Vehicles

China produced 10.4 million new-energy vehicles in 2024, accounting for 35% of the country's national auto output. Each battery electric model uses 50-80 microcontrollers, compared to 30-50 in internal-combustion cars, which also include traction inverters, chargers, and thermal-loop controllers. BYD’s Blade battery embeds distributed chips that sample voltage and temperature across more than 200 cells to avert thermal runaway.[2]Financial Times Reporting Team, “BYD’s Blade Battery Technology Reshapes EV Safety Standards,” Financial Times, ft.com MIIT targets 40% new-energy penetration by 2030, securing long-term demand for silicon. CATL’s Shenxing pack, capable of reaching 80% charge in 10 minutes, relies on 32-bit controllers that balance current at a millisecond cadence.[3]Reuters Staff, “CATL’s Shenxing Battery Achieves 10-Minute Fast Charging Milestone,” Reuters, reuters.com

Rising Integration of Advanced Driver Assistance Systems

China’s 2024 GB 7258 update made automatic emergency braking and lane-keeping assist mandatory, pushing automakers to deploy ASIL-D-rated microcontrollers for actuator redundancy. NIO’s Adam supercomputer still pairs high-level NVIDIA Orin processors with discrete 32-bit chips for fail-safe steering and braking. XPeng’s 2024 XNGP launch confirms a hybrid compute model where perception runs on domain CPUs but low-latency control stays with real-time microcontrollers. The 2025 C-NCAP upgrade introduces V2X and driver-monitoring requirements, thereby increasing controller content for secure wireless and infrared modules.

Government Push for Semiconductor Self-Sufficiency

MIIT earmarked CNY 344 billion (USD 47 billion) through the “Big Fund” Phase III to scale local design and fabrication. The program follows the 2023 shortages that exposed reliance on overseas nodes. GigaDevice earned ASIL-D for its GD32A503 in March 2024 and won slots at SAIC and Geely. Preferential procurement rules give domestic chips a 10% price edge in government fleets, accelerating uptake despite narrower portfolios. Beijing’s 70-standard framework aims to develop indigenous IP and test protocols by 2030.

Shift to Zonal Electrical Architecture in Smart Vehicles

BYD’s e-platform 3.0, deployed in the Seal sedan, consolidates 120 former electronic control units into 75 higher-power nodes, lowering harness mass by 15 kg and demanding Ethernet-equipped 32-bit controllers. Li Auto’s L9 replicated the concept, slashing wire cost and allowing over-the-air updates for body functions. Zonal designs accelerate 64-bit adoption because a single chip must run concurrent door, seat, and lighting stacks, as well as cybersecurity modules. Legacy 8-bit suppliers face a margin squeeze as volumes decline, but compute power per device rises.

Restraints Impact Analysis*

| Persistent semiconductor supply chain volatility | -0.8% | National, spillover from Taiwan and Southeast Asia | Short term (≤2 years) |

|---|---|---|---|

| Intense price competition from low-end local vendors | -0.6% | National, body electronics and telematics | Medium term (2-4 years) |

| Complexity of achieving ASIL-D compliance | -0.5% | National, domestic safety-critical entrants | Long term (≥4 years) |

| Export controls on advanced design tools | -0.7% | National, sub-28-nm development | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Persistent Semiconductor Supply Chain Volatility

Sixty-five percent of automotive-grade wafer output still originates from Taiwan, Japan, and South Korea, leaving China vulnerable to natural disasters and geopolitical shocks.[4]Reuters Staff, “US Export Controls on Chip Tools Hit Chinese Semiconductor Ambitions,” Reuters, reuters.com The April 2024 Taiwan earthquake halted TSMC’s 28-nm lines for three weeks, delaying shipments from Renesas and NXP, and forcing GAC and Changan to cut their output. Domestic foundries, such as SMIC, have raised 40-nm automotive yields yet remain 15-20 points below their global peers, inflating lead times. Penang flooding in August 2024 halted Infineon backend packaging, underscoring fragility. Safety-stock buffers mitigate the impact but cannot eliminate systemic risk until local capacity is scaled.

Intense Price Competition From Low-End Local Vendors

Average selling prices for 8-bit body-control devices dropped 22% in 2024 as ChipON, Holtek, and Puolop undercut global brands by up to 40%. STMicroelectronics cited a 4.2-point margin dip, linking it to “aggressive pricing in China’s body-electronics market”. Domestic vendors leverage subsidies and lower profit targets, accelerating commoditization, while incumbents retreat to premium, safety-critical tiers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bit Class: Premium Compute Gains Traction

The China automotive microcontroller market size for 32-bit devices reached USD 1.57 billion in 2025, accounting for 45.78% of the total value. Zonal and domain architectures drive consolidation of multiple low-end units into fewer, higher-power chips, propelling 64-bit controllers toward an 8.78% CAGR through 2031. BYD replaced 45 distributed 8-bit modules with 12 Ethernet-based 32-bit units, cutting harness weight while enabling over-the-air updates. NIO’s Adam platform incorporates 64-bit Cortex-A76 controllers to manage redundant power and sensor synchronization, underscoring the demand for virtualization and security accelerators.

Legacy 8-bit parts remain dominant in low-risk body niches, such as window lifts, although their market share in the China automotive microcontroller market is contracting. The 16-bit category is facing a structural decline because tool-chain scarcity is pushing automakers to leapfrog directly to 32-bit Arm cores. ISO 26262 compliance favors 32-bit and 64-bit devices, as pre-certified libraries reduce validation cycles, thereby outweighing the higher die cost. As a result, suppliers that offer scalable pin-compatible families across bit classes defend platform loyalty.

By Application: Battery and Safety Dominate Value Creation

Safety and ADAS applications generated USD 1.16 billion in 2025, accounting for 34.05% of China automotive microcontroller market value. Mandated AEB and lane-keeping systems elevate demand for ASIL-D-rated chips that coordinate brake, steer, and redundant power paths. Battery management systems, however, will record the fastest 10.26% CAGR, fueled by high-density cell-to-pack chemistries that require cell-level sensing at millisecond speed. CATL’s Qilin battery achieves 255 Wh/kg by employing distributed 32-bit nodes with 0.3 mV ADC resolution.

The powertrain and chassis segments are adding steady volume as 48-volt hybrids proliferate. Telematics controllers ride 5G rollout, while body electronics confront margin erosion amid local commoditization. Regulatory frameworks GB 38031 for battery safety and GB 34660 for functional safety ensure persistent silicon upgrades across the application stack.

By Vehicle Type: Passenger Cars Still Rule, Off-Highway Accelerates

Passenger models accounted for 70.92% of units in 2025, reflecting a 26 million vehicle output and rapidly rising electronics content. China automotive microcontroller market size is expected to grow at an 8.28% CAGR to 2031, as construction and mining fleets adopt electrification to meet carbon targets. XCMG’s 14-ton electric excavator features dedicated 32-bit boards governing electric actuators and regenerative boom control.

Light commercial vans are gaining market share in tier-1 zero-emission zones, driving up battery management volumes, while heavy trucks are integrating 48-volt mild hybrids to meet China VI emissions regulations. Safety mandates apply across vehicle classes, solidifying the demand for microcontrollers in braking, steering, and stability systems, even in commercial models.

By Propulsion Technology: Battery Electric Platforms Multiply Silicon Content

Internal-combustion vehicles retained a 52.96% share in 2025; however, battery electric models are projected to log an 11.05% CAGR through 2031, as MIIT aims for a 40% new-energy sales penetration. A typical battery electric car embeds 68 microcontrollers, 40% more than a comparable gasoline vehicle, covering traction, charging, DCDC, and thermal loops. The Han sedan underscores this jump, integrating 68 units against the Qin Pro’s 48.

Hybrid platforms bridge the transition by combining 48-volt starter-generators with high-voltage packs, thereby incorporating dual-domain controller sets. Fuel-cell trucks remain a niche market, but they demand ASIL-C controllers for hydrogen flow and compressor control. GB 38032 rules shape safety needs in these emerging segments.

Geography Analysis

Shanghai’s Yangtze River Delta commanded 41.35% of 2025 consumption as SAIC, Geely, and NIO assembled 8.2 million vehicles across the cluster. Chip designers, tier ones, and fabs operate within a 300 km radius, which lowers logistics costs and speeds up engineering iterations. Shenzhen-Guangzhou’s Pearl River Delta contributed 27.62%, anchored by BYD and GAC facilities that prioritize domestic chips in line with localization targets.

MIIT’s 2024 semiconductor roadmap named 15 integrated-circuit hubs, extending tax breaks and subsidized land to spur inland migration. Chongqing, Sichuan, and Shaanxi now host emerging fabs and packaging plants. Chongqing alone built 620,000 new-energy vehicles in 2024, driving demand for battery and inverter controllers. The National Development and Reform Commission's allocation of CNY 180 billion (USD 25 billion) supports the Western cluster's expansion and supply-chain resilience.

Tier-2 and tier-3 cities generate 55% of the electric-vehicle sales growth as license-plate exemptions narrow the price gap versus gasoline cars. This geographic broadening diversifies the Chinese automotive microcontroller market, spreading opportunity beyond historic coastal strongholds and buffering suppliers against regional production swings.

Regulatory Landscape

China is tightening intelligent connected vehicle (ICV) governance in ways that raise compliance requirements for automotive microcontrollers used in safety, cybersecurity, and OTA-enabled ECUs. In January 2026, GB 44496-2024 on vehicle software update general technical requirements entered implementation, formalizing management systems and technical expectations around OTA. In parallel, GB 44495-2024/XG1-2026 updated technical requirements for vehicle cybersecurity, linking MCU selection to secure boot, secure update, and in-vehicle network protection requirements.

In 2026, MIIT issued the 2026 Key Tasks for Automotive Standardization as an annual roadmap under the 15th Five-Year Plan, explicitly prioritizing standards work spanning automotive chips across control, computing, communication, and power domains. Beyond technical standards, January 2026 cross-border automotive data transfer guidance issued by multiple ministries (including MIIT and CAC) increased operational obligations around data classification and handling across defined automotive scenarios. In March 2026, the State Council issued Decree No. 834 on supply chain and industrial chain security, reinforcing monitoring and risk-warning mechanisms for critical components and technology supply chains relevant to automotive-grade semiconductors.

Value Chain Analysis

The China automotive microcontroller value chain spans IP and EDA tools, MCU design (global leaders and an expanding domestic cohort), wafer fabrication on mature nodes (commonly 55 nm, 40 nm, and 28 nm for automotive MCUs), packaging and test, tier-1 ECU/module integration, and OEM vehicle assembly and aftersales software maintenance. Policy-driven standardization is a key upstream-to-downstream enabler: in January 2024, MIIT released the Guidelines for the Construction of the National Automotive Chip Standardization System, targeting over 30 key automotive chip standards by 2025 and over 70 by 2030. This shapes qualification flow, reliability expectations, functional-safety evidence, and information-security validation demanded by tier-1s and OEMs.

Downstream pull is increasingly organized through localized ecosystems and consortiums that shorten design-in cycles and accelerate qualification. One example is Dongfeng Motor-backed ecosystem activity around its DF30 automotive-grade MCU, released by the Hubei Automotive Grade Chip Industry Technology Innovation Consortium in November 2024. The value chain is also adapting technically through alternative instruction-set and platform choices, including RISC-V-based MCU efforts by Chinese firms, to reduce dependence on constrained external tool and IP pipelines and to align more closely with evolving GB and GB-T cybersecurity and OTA-related requirements. In parallel, domestic control-chip vendors have scaled shipment volumes, with Indiemicro reporting cumulative shipments exceeding 300 million automotive control chips by June 2025.

Competitive Landscape

The five global leaders—NXP, Infineon, Renesas, STMicroelectronics, and Texas Instruments—held a majority of share in 2024 but now face 15 domestic challengers that have gained ISO 26262 stamps. Incumbents retain an edge in premium segments through long safety pedigrees, secure boot IP, and tool-chain maturity; however, pricing leverage in low-end body electronics erodes as ChipON and Holtek commoditize 8-bit parts.

White space exists in 64-bit zonal controllers, where neither global nor Chinese vendors have achieved a dominant position. BYD Semiconductor leverages vertical integration to capture margins across design, packaging, and system assembly, while GigaDevice cross-sells from its NAND base into the automotive sector. Technology roadmaps diverge: multinationals push 5-nm application processors but keep microcontrollers at mature 40-nm nodes; local firms focus on accessible 55-nm and 40-nm flows through SMIC partnerships.

Strategic moves in 2025 illustrate shifting terrain. NXP is expanding its Tianjin packaging lines, Infineon has enlarged its Wuxi design center, and Renesas has opened a Beijing co-design hub with SAIC. On the Chinese side, BYD Semiconductor secured ASIL-D certification for its battery chips, and CEC Huada landed GAC’s largest domestic microcontroller contract. These plays underline escalating R&D and localization commitments despite export-control headwinds.

China Automotive Microcontroller Industry Leaders

NXP Semiconductors N.V

Microchip Technology Inc.

Renesas Electronics Corporation

STMicroelectronics

Sunplus Innovation Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrating where compliance-heavy and software-centric vehicle architectures increase the value of MCU features beyond basic body control, especially secure OTA, in-vehicle cybersecurity, and zonal or domain control nodes that consolidate multiple legacy ECUs. The January 2026 implementation of GB 44496-2024 for vehicle software updates and the updated GB 44495-2024/XG1-2026 cybersecurity technical requirements push OEMs and tier-1s to re-architect update and security chains. That, in turn, supports demand for microcontrollers with hardware security, deterministic real-time control, and robust lifecycle support across safety and connectivity domains.

Localization programs are moving from component substitution toward subsystem-level redesign, creating whitespace for domestic MCU suppliers and for global vendors willing to localize manufacturing and engineering support in China. A concrete signal came in July 2026, when FORVIA HELLA began mass production of a headlamp ECU in China powered entirely by domestically sourced semiconductor chips, showing how tier-1 modules can be engineered around localized semiconductor stacks. At the same time, MIIT's 2026 Automotive Standardization Work Plan prioritizes acceleration of automotive chip standards across control, computing, communication, and power categories, which increases the importance of testing, certification, and reference-platform ecosystems as OEMs and tier-1s standardize architectures for software-defined vehicles.

Recent Industry Developments

- June 2026: STMicroelectronics announced expansion of the STM32 local production footprint in China, adding lines at Hua Hong and exploring additional facilities to meet localization requirements. ST also indicated additional series are planned for local production later in 2026, extending the localization footprint beyond an initial device set.

- December 2025: NXP Semiconductors initiated strategic cooperation with the China Automotive Technology and Research Center (CATARC) to work on automotive chip standard systems, test evaluations, and application scenario laboratories. The partnership aligns NXP platforms with China-specific compliance and validation processes, shortening qualification cycles for safety and cybersecurity-relevant MCUs and processors used by local OEMs and tier-1s.

- January 2024: MIIT released Guidelines for the Construction of the National Automotive Chip Standardization System, targeting over 30 key automotive chip standards by 2025 and over 70 by 2030. The guidelines shape qualification flow, reliability evidence, functional-safety validation, and information-security validation demanded by tier-1s and OEMs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from automotive-grade microcontroller units (MCUs) sold for use in vehicles manufactured and sold in China, across key electronic control functions in the vehicle. It counts device shipments valued at the selling price level that is typically reported for the semiconductor supply chain.

Scope exclusions: We exclude non-automotive MCUs, development tools, and software-only revenues, and we also exclude adjacent automotive semiconductors such as sensors, discrete power devices, and memory chips.

Segmentation Overview

- By Bit Class

- 8-bit Microcontrollers

- 16-bit Microcontrollers

- 32-bit Microcontrollers

- 64-bit Microcontrollers

- By Application

- Safety and ADAS

- Body Electronics

- Telematics and Infotainment

- Powertrain and Chassis

- Battery Management System

- By Vehicle Type

- Passenger Vehicles

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Off-Highway Vehicles

- By Propulsion Technology

- Internal Combustion Engine Vehicles

- Hybrid Electric Vehicles

- Battery Electric Vehicles

- Fuel Cell Electric Vehicles

Data Sources, Market Sizing, and Validation

Desk Research

For desk research, we first build the demand environment for China vehicle production and the electronics content that sits inside them, before moving to the MCU specific layer. Common starting points include public statistics and releases such as the China Association of Automobile Manufacturers (CAAM), the National Bureau of Statistics of China (NBS), China Customs trade data, and standards and regulation updates published by MIIT, along with technical context from SAE papers and peer-reviewed journals.

From there, the market model is shaped using broader, regularly updated public information such as company annual reports, earnings decks, product briefs, and reputable industry press coverage. We also use select paid databases for company financials and intelligence, patent databases, and shipment-level import and export records where it is relevant for cross-checks around supply availability. These examples are not exhaustive, and many other public sources were also used to collect data, validate assumptions, and clarify gaps found during research.

Primary Interviews and Surveys

Primary work was used to pressure test the desk research view of automotive MCU demand in China, particularly how content per vehicle is changing as EV penetration rises, and as ADAS and body electronics add more features. We spoke with stakeholders across the semiconductor value chain, including chip suppliers, distribution and channel participants, automotive electronics design and manufacturing teams, and Tier supplier sales and product roles. We then cross-checked the assumptions across the main China vehicle production hubs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 16% | |

| Mid tier: 44% | Functional/Unit leaders: 28% | |

| Smaller Players: 21% | Managers: 56% |

Market-Sizing & Forecasting

The sizing starts with a top-down build that reconstructs the China automotive MCU revenue pool from vehicle production and sales signals, and then applies usage and value factors that reflect how many MCUs are typically designed into a vehicle and how pricing differs by performance needs. To keep the output realistic, selective bottom-up approximations are used as a check, such as sampled ASP-by-bit class and application, channel feedback on sell-in versus sell-through, and supplier-side sanity checks for the addressable automotive portion.

Key inputs that tend to move the model in this market include China passenger and commercial vehicle production volumes, EV and hybrid penetration, the mix shift toward ADAS and safety content, the spread of domain and zonal architectures that changes MCU count per vehicle, and average selling price progression for 8-bit, 16-bit, and 32-bit devices. Where a variable cannot be observed cleanly, the gap is handled by using a bounded range from interviews and then selecting the midpoint that best matches independent signals.

For forecasting, scenario analysis is applied around vehicle volume and EV mix, and the price and content assumptions are aligned to what industry experts expect for the next design cycles. Once the demand and ASP paths are consistent with what the market is shipping today, the forward values are extended year by year and reviewed for internal consistency.

Data Validation & Update Cycle

Results are validated through triangulation across multiple signals, and variance checks are run to catch unusual jumps in implied MCU content per vehicle or unrealistic price moves. A second analyst review is used to challenge the main assumptions, and follow-up calls are triggered when the model output diverges from trade flow indicators, public production data, or the levels described by interviewees.

The report is refreshed on an annual cycle, and interim updates are made when material events can shift supply or demand (for example, major policy moves, large capacity changes, or sudden demand swings). Before delivery, a final data pass is done so the published numbers reflect the latest available public releases and the most recent expert feedback.

Mordor Intelligence's China Automotive Microcontroller Market Size Versus Other Published Estimates

Published market values for China automotive microcontrollers often do not match each other because the scope boundary and the pricing layer are not handled in the same way, and the forecast period assumptions can also vary. Some studies lean more on a single base year and then extend growth mechanically, while others tie sizing to a richer set of vehicle and electronics signals.

Vehicle production volumes, EV penetration, and independent checks on MCU content per vehicle are the evidence points that keep Mordor Intelligence grounded in a China automotive demand pool, and this reduces the chance of counting adjacent non-automotive MCU demand or folding in other automotive semiconductors by accident.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.66 B (2026) | |

| Global Consultancy A | USD 6.30 B (2024) | Uses an earlier base year and appears to apply a broader revenue capture approach that can mix in wider automotive electronics value, and it does not clearly show how China-only automotive MCU pricing and content-per-vehicle checks were validated. |

| Industry Report B | USD 2.45 B (2024) | Anchors the estimate on a narrower automotive-grade MCU definition and local currency tables, and it can understate value when it does not fully reflect higher ASP devices used in ADAS and centralized architectures or apply consistent currency conversion timing. |

The spread across the three figures is mainly explained by what gets counted as automotive MCU revenue in China, plus how pricing and content per vehicle are updated over time. By keeping the assumptions traceable to vehicle output, propulsion mix, and MCU content signals, the final number stays balanced and can be repeated with the same steps in the next refresh.

Key Questions Answered in the Report

How fast is electronic content per vehicle rising in China’s passenger-car segment?

Average microcontroller count in a battery electric car rose from about 50 in 2023 to 68 in 2024 and is still climbing due to domain and zonal architectures.

Why are 64-bit controllers becoming crucial for Chinese automakers?

Zonal and domain platforms consolidate many legacy units into fewer, higher-power nodes that need virtualization, Ethernet, and security, functions best served by 64-bit devices.

What is the biggest demand driver for automotive microcontrollers through 2031?

China’s regulatory target of 40% new-energy vehicle sales by 2031, each requiring substantially more microcontrollers than gasoline cars, leads demand growth.

How are export controls affecting domestic chip designers?

Restrictions on advanced design tools complicate sub-28-nm verification, forcing local firms to rely on older software or invest in homegrown alternatives, slowing premium-node rollout.

Which applications offer the strongest margin prospects?

Safety, ADAS, and battery-management systems maintain healthier margins because they require ASIL-compliant, feature-rich controllers that are harder for low-cost entrants to copy.

What regions inside China are emerging semiconductor hubs?

Beyond Shanghai and Shenzhen, inland cities such as Chongqing, Chengdu, and Xi’an are attracting fabs and design houses through generous incentives and expanding EV production bases.

Page last updated on: