Automotive Optoelectronics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

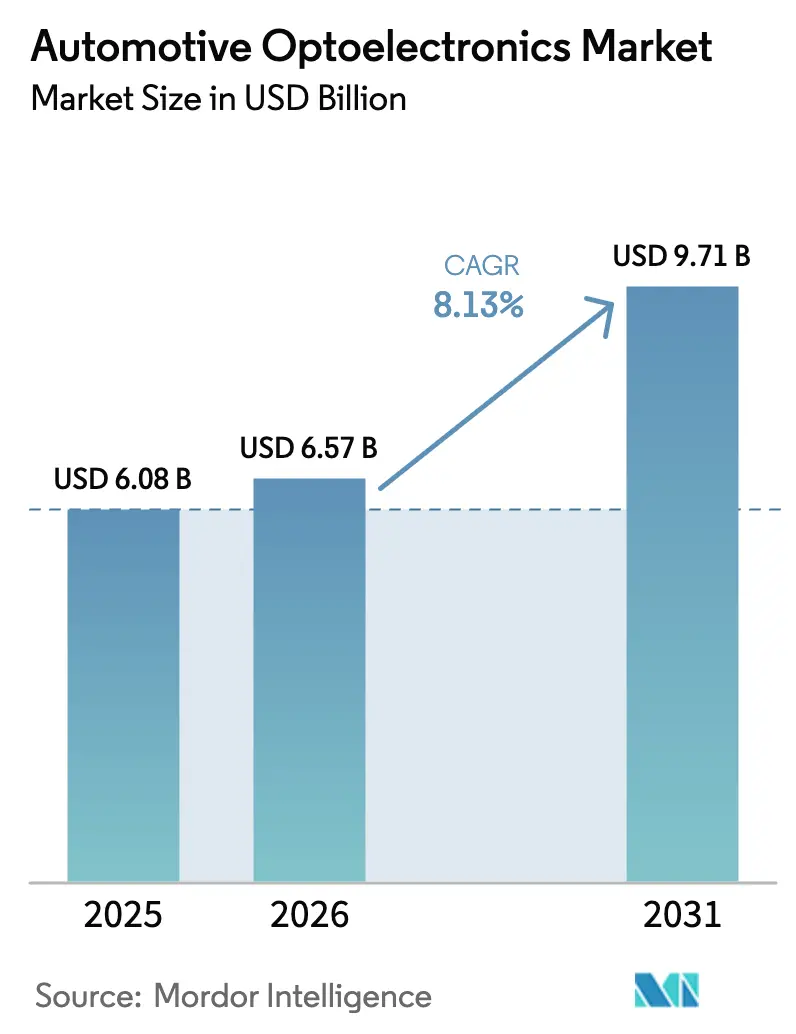

| Market Size (2026) | USD 6.57 Billion |

| Market Size (2031) | USD 9.71 Billion |

| Growth Rate (2026 - 2031) | 8.13% CAGR |

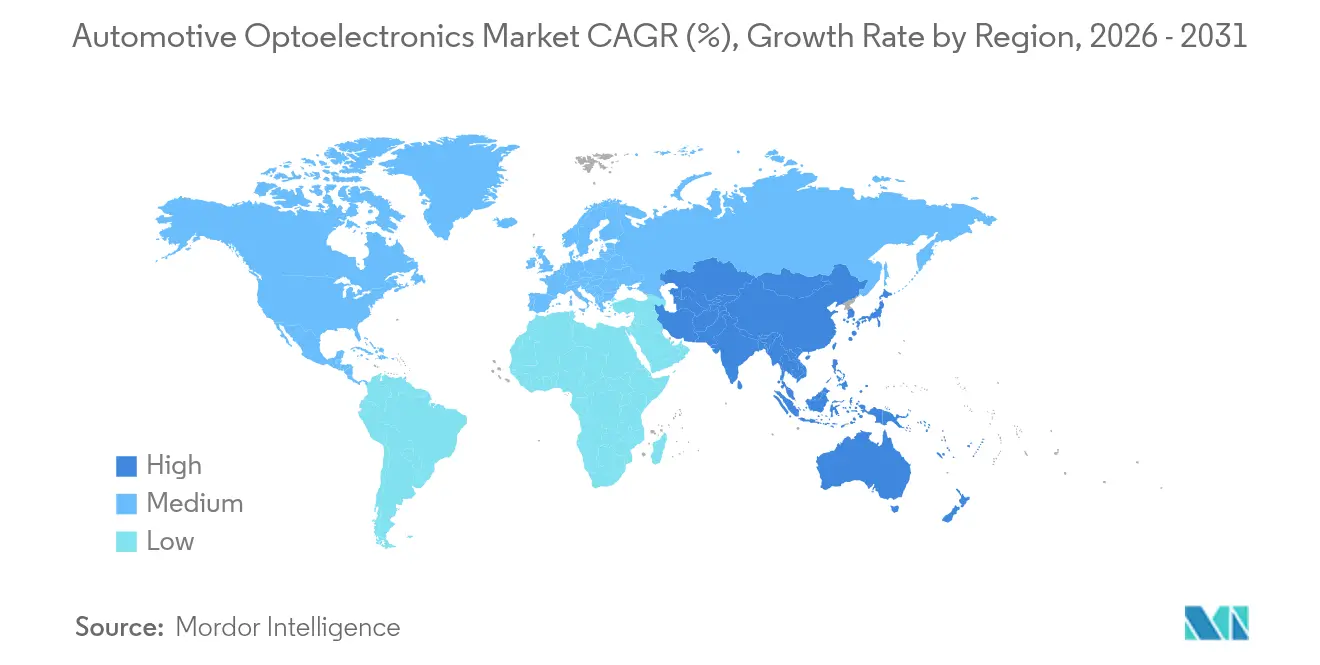

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Optoelectronics Market Analysis by Mordor Intelligence

The automotive optoelectronics market size is expected to grow from USD 6.08 billion in 2025 to USD 6.57 billion in 2026 and is forecast to reach USD 9.71 billion by 2031 at 8.13% CAGR over 2026-2031. Heightened safety mandates, electrification, and the move toward software-defined vehicles turned optoelectronic devices into indispensable building blocks for perception, illumination, and in-cabin interaction. Asia Pacific retained leadership thanks to China’s scale in vehicle output and semiconductor fabrication, while Europe’s rulemaking around driver monitoring and adaptive lighting set stringent technology baselines. Rapid expansion of Battery Electric Vehicles (BEVs) deepened demand for compact, thermally efficient optical components, and breakthroughs in GaN and VCSEL architectures lifted performance ceilings for LiDAR and laser headlamp modules. Tight supplies of automotive-qualified GaAs/GaN wafers, however, continued to expose supply-chain vulnerabilities that incumbents addressed through vertical integration measures.

Key Report Takeaways

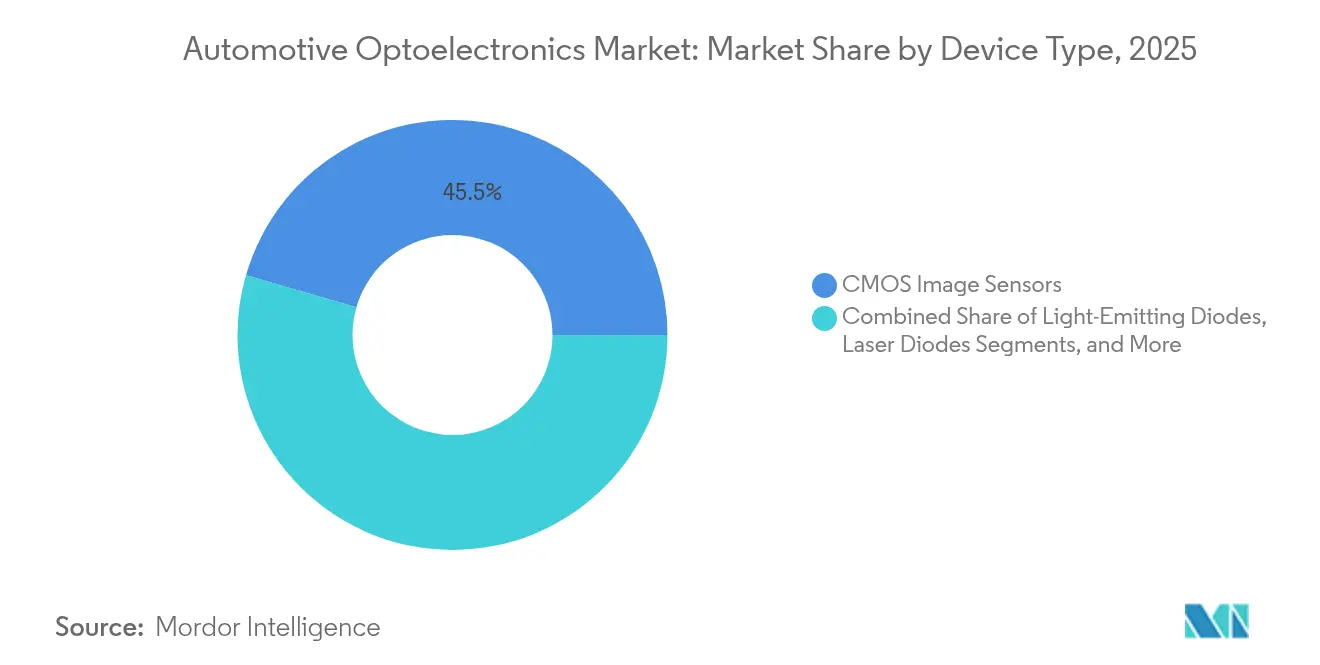

- By device type, CMOS image sensors led with 45.52% revenue share in 2025; laser diodes are projected to expand at a 14.88% CAGR through 2031.

- By application, exterior lighting accounted for 38.02% share of the automotive optoelectronics market size in 2025, while ADAS is advancing at a 16.72% CAGR to 2031.

- By vehicle type, passenger cars held 71.62% of the automotive optoelectronics market share in 2025; heavy commercial vehicles are expected to grow at a 13.28% CAGR.

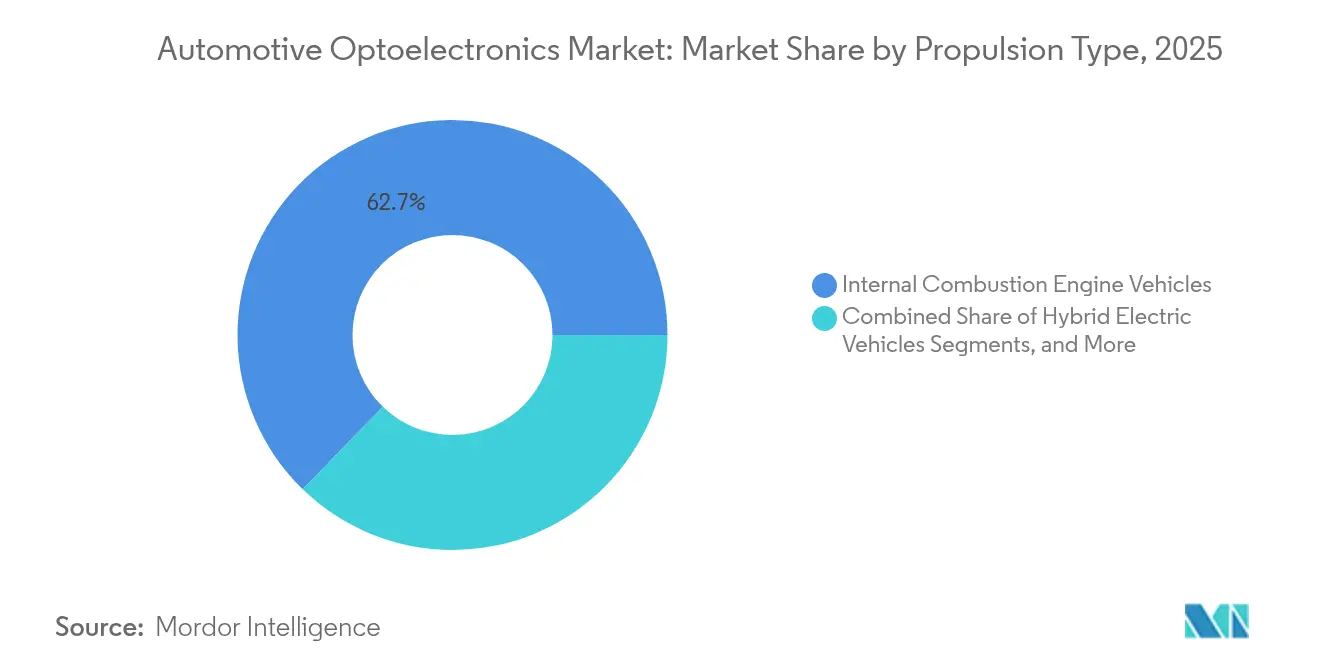

- By propulsion type, internal combustion engine vehicles captured 62.74% share of the automotive optoelectronics market size in 2025, whereas battery electric vehicles are rising at a 19.62% CAGR.

- By sales channel, OEMs dominated with an 88.35% share in 2025; the aftermarket is forecast to expand at a 9.62% CAGR.

- By geography, Asia Pacific led with a 43.12% share in 2025 and is projected to register a 14.05% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Optoelectronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for high-resolution CMOS image sensors in ADAS-centric premium vehicles | +1.5% | Europe, North America | Medium term (2-4 years) |

| Rapid OEM shift toward solid-state headlamps and laser high-beam modules in China | +1.2% | Asia Pacific (China) | Short term (≤ 2 years) |

| Legislative mandates for Adaptive Driving Beam (ADB) and rear-end signaling in Japan and the EU | +0.9% | Europe, Japan | Short term (≤ 2 years) |

| Integration of infrared VCSELs for driver-monitoring systems in electric SUVs | +0.8% | Global, strong in Europe | Medium term (2-4 years) |

| Automotive-grade micro-LED adoption for next-gen in-cabin displays | +0.7% | Korea, Taiwan, Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for High-Resolution CMOS Image Sensors in ADAS-Centric Premium Vehicles

Premium models in Europe and North America adopted 8-megapixel image sensors throughout 2024, enabling refined object detection at extended ranges required for Level 2+ autonomy. Dual-gain pixels and wide-dynamic-range circuitry minimized over- and under-exposure, while on-chip AI accelerators lowered latency for perception algorithms.[1]onsemi, “A Journey Through Advancements in Automotive Image Sensors,” onsemi.com Suppliers reported compounded performance gains as each resolution jump allowed more sophisticated neural-network training, pushing collision-avoidance accuracy toward human-level performance thresholds.

Rapid OEM Shift Toward Solid-State Headlamps and Laser High-Beam Modules in China

Chinese brands displayed solid-state laser units generating intensities near 100,000 candelas at the 2024 Shanghai Auto Lamp Exhibition, shrinking optical stacks while cutting package depth. The EVIYOS 2.0 matrix, with 25,600 micro-LEDs, modulated light zones in real time, enabling road-projection warnings and V2X signalling without glare. Domestic semiconductor capacity gave local OEMs a cost edge, accelerating penetration across mid-segment BEVs.

Legislative Mandates for Adaptive Driving Beam (ADB) and Rear-End Signaling in Japan and EU

Regulations that came into force in 2024 compelled ADB adoption in all new passenger vehicles, driving fitment rates above 75% in conventional cars and 96% in EVs. Micro- and mini-LED arrays created pixel-level control, enhancing night-time visibility and standardising advanced lighting across trim levels, which in turn lowered unit costs through volume scaling.

Integration of Infrared VCSELs for Driver-Monitoring Systems in Electric SUVs

Europe’s 2024 General Safety Regulation mandated driver-monitoring, triggering rapid VCSEL uptake for gaze and drowsiness sensing. VCSEL efficiency above 45% cut power draw, a critical factor for BEVs, while eye-safe wavelengths enabled continuous illumination indoors. The technology is now evolving toward recognising gestures and emotional cues, paving the way for more intuitive HMI functions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply crunch of automotive-qualified 8-inch GaAs/GaN wafers | -0.6% | Global, severe in Europe | Medium term (2-4 years) |

| Heat dissipation and reliability challenges in 25 W+ laser lighting modules | -0.5% | Global | Short term (≤ 2 years) |

| Price erosion in standard exterior LEDs compressing tier-2 margins | -0.4% | Asia Pacific, North America | Short term (≤ 2 years) |

| Complex ISO 26262 certification cycles delaying time-to-market for novel photonics ICs | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Crunch of Automotive-Qualified 8-Inch GaAs/GaN Wafers

Throughout 2024, the automotive sector competed with AI servers for GaN capacity, inflating prices and stretching lead times for laser diodes and power devices. Top suppliers responded by building captive epitaxy lines and securing joint ventures; ST Microelectronics’ expansion in Catania and onsemi’s upward integration in the US lifted self-sufficiency, yet only partially alleviated the deficit.

Heat Dissipation and Reliability Challenges in 25 W+ Laser Lighting Modules

Laser headlamps and LiDAR stacks above 25 W generated localized heat that shifted emission wavelengths and degraded lifetime. Research teams demonstrated multi-junction VCSEL arrays achieving 190 W peaks with 1.64 kW/mm² density, but packaging thermal paths remained bottlenecks, delaying rollout in high-volume models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: CMOS Sensors Redefine Vehicle Perception

CMOS image sensors captured 45.52% of the 2025 automotive optoelectronics market size, reflecting their migration from simple backup cameras to central perception hubs in ADAS suites. Enhanced dynamic-range circuitry, on-chip HDR, and dual-gain pixel architectures raised detection fidelity in high-contrast scenes. Laser diodes, particularly VCSEL arrays for LiDAR, are anticipated to post a 14.88% CAGR through 2031, buoyed by autonomous-driving roadmaps. LEDs continued to evolve via LED-on-foil substrates that enabled free-form surface illumination, while optocouplers maintained relevance for galvanic isolation in high-voltage drivetrains. The automotive optoelectronics market is therefore pivoting from discrete illumination nodes to multifunctional optoelectronic modules that merge sensing, signalling, and processing.

Advances in GaN epi-layers shrank die sizes and lifted power density, easing integration within space-constrained headlamp housings. Photovoltaic photodiodes surfaced as auxiliary energy harvesters for sensor clusters, marginally extending BEV range. Collectively, device-level innovation is compressing the bill-of-materials and shortening optical paths, a prerequisite for cost-effective mass deployment across vehicle classes.

By Application: ADAS Drives Innovation Surge

Exterior lighting held 38.02% share of the automotive optoelectronics market size in 2025, yet ADAS is forecast to outpace it at 16.72% CAGR as LiDAR and camera fusion push toward higher autonomy. Transparent nanocarbon heaters protected sensor windows from fogging while preserving >90% transmittance, allowing tightly packaged sensor pods to function reliably in winter conditions. Interior lighting also evolved; mini-LED strips synchronised ambient hues with driving modes, enhancing the brand signature. Battery and powertrain monitoring adopted fiber-optic sensors capable of real-time state-of-charge measurements, avoiding electromagnetic interference common in high-current BEV packs.

The automotive optoelectronics market is thus diversifying across safety, comfort, and powertrain monitoring domains. This breadth cushions suppliers against demand swings in any single application while encouraging platform-level consolidation of optical functions.

By Vehicle Type: Commercial Vehicles Embrace Advanced Optics

Passenger cars dominated with 71.62% automotive optoelectronics market share in 2025, reflecting their role as first adopters of adaptive headlights, surround-view cameras, and digital OLED rear lamps. Heavy commercial vehicles are set for a 13.28% CAGR as fleet operators prioritise accident reduction and uptime. Fog-detection sensors paired with automated lighting shortened driver reaction times during low-visibility haulage, while high-dynamic-range cameras improved blind-spot coverage for articulated trailers.

Light commercial vehicles migrated toward ruggedised sensors tested for vibration and wide-temperature tolerance. Growth across all commercial segments indicates that optoelectronic advances developed for premium cars are now diffusing into revenue-generating fleets, enlarging the addressable base for suppliers.

By Propulsion Type: BEVs Accelerate Optoelectronic Innovation

Internal combustion models still contributed 62.74% of the automotive optoelectronics market size in 2025, but BEVs are on track for a 19.62% CAGR as zero-emission mandates tighten. Optical fiber probes embedded in battery modules measured temperature and strain in real time, mitigating thermal-runaway risk. GaN switching devices trimmed conversion losses in on-board chargers, freeing thermal headroom for high-power LED arrays within compact fascia designs. Fuel-cell vehicles, though niche, demanded hydrogen-leak detection via mid-infrared photonic sensors. Hybrid architectures blended ICE robustness with BEV electrical sophistication, offering suppliers a broad spectrum of design wins.

By Sales Channel: OEMs Drive Integration Strategies

OEM installations accounted for 88.35% of 2025 revenue, underlining the deep integration required for safety-critical optics. Software-defined architectures let carmakers unlock dormant hardware through subscriptions, blurring the line between factory and aftermarket upgrades. Nevertheless, the aftermarket is projected to grow 9.62% annually as owners retrofit LED headlights and camera kits to ageing vehicles, particularly in regions with long fleet life cycles. Plug-and-play modules reduced installation time, widening the consumer base beyond specialist garages.

Geography Analysis

Asia Pacific provided 43.12% of 2025 revenue and is forecast for a 14.05% CAGR, cementing its role as the growth engine of the automotive optoelectronics market. China produced more than 31 million vehicles that year and saw battery-electric penetration approach 50% of new sales, catalysing large-scale demand for adaptive headlights, LiDAR, and transparent displays showcased at the Beijing Auto Show. Regional LED and micro-LED capacity anchored cost advantages; AUO and PlayNitride launched a USD 21.5 million micro-LED line dedicated to automotive panels in 2025, shortening development loops for transparent cluster displays.

Europe ranked second, propelled by stringent General Safety Regulation deadlines. Mandatory driver-monitoring from mid-2024 created a ready market for VCSEL-based eye-tracking cameras, while premium OEMs led early rollouts of digital OLED rear lamps. The continent also invested in optical interconnects for domain controllers; KDPOF’s EC-funded facility in Madrid prepares fiber-optic transceivers for model-year 2027 launches, reducing electromagnetic interference inside zonal architectures. North America preserved an innovation hub status despite lower BEV uptake—EVs formed roughly 10% of US light-vehicle sales in 2024. Start-ups in Silicon Valley advanced solid-state LiDAR units, while Detroit-based OEMs focused on over-the-air activation of lighting signatures. Government incentives for domestic semiconductor fabs may rebalance supply-chain risks over the forecast window. In ASEAN, Thailand and Indonesia positioned themselves as BEV manufacturing nodes for 2030, lifting regional optoelectronic demand as policymakers offered tax breaks for energy-efficient headlights. The Middle East and Africa saw luxury import channels introducing adaptive laser lamps, whereas South America’s momentum remained sensitive to macroeconomic volatility but benefited from safety equipment import incentives in Brazil and Argentina.

Competitive Landscape

The competitive field remained moderately fragmented, with the top five players majority of revenue share. Technology convergence encouraged cross-disciplinary partnerships: lighting specialists worked with semiconductor foundries to co-package LEDs, VCSELs, and control ICs in single substrates, shrinking footprints. ST Microelectronics safeguarded SiC supply by commissioning a dedicated epitaxy plant in Italy and partnering with Chinese wafer producers to hedge geopolitical risk. onsemi targeted 50% internal material sufficiency, reflecting the strategic imperative to de-risk upstream inputs.

Innovators leveraged LED-on-foil technology to carve niches in flexible light panels that wrap interior surfaces, challenging traditional molded-optic vendors.[4]AMS OSRAM, “ALIYOS™ LED-on-foil Technology,” ams-osram.com Patent filings in 2024 signalled sustained R&D in multi-junction laser diodes and liquid-metal thermal interfaces, areas likely to decide next-generation LiDAR dominance. Meanwhile, Infineon’s USD 2.5 billion purchase of a Marvell automotive Ethernet unit bolstered its grip on in-vehicle data backbones, illustrating that horizontal acquisitions remain a viable route to portfolio completeness.

Start-ups focusing on niche applications—such as holographic windshield displays demonstrated by ZEISS and Hyundai Mobis—gained traction through co-development with Tier-1s, expediting validation cycles. Consolidation pressure is expected to intensify as wafer shortages persist, prompting further vertical integration moves across the value chain.

Automotive Optoelectronics Industry Leaders

Samsung Electronics Co., Ltd.

Ams Osram AG

Sony Group Corporation

ON Semiconductor (onsemi)

Infineon Technologies AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Ennostar showcased Micro- and Mini-LED adaptive headlamps and transparent displays tailored for high-value automotive programs at Touch Taiwan 2025.

- April 2025: Infineon Technologies acquired Marvell’s automotive Ethernet unit for USD 2.5 billion, expanding its connectivity solutions for next-generation vehicles.

- March 2025: AUO and PlayNitride invested USD 21.5 million in a micro-LED production line aimed at automotive and TV panels.

- January 2025: Ennostar, AUO, and TADA unveiled 5,000-nit interactive matrix displays for in-car applications at CES 2025.

Global Automotive Optoelectronics Market Report Scope

Optoelectronic devices are electronic devices and systems that involve the study, detection, and control of light. They are considered a sub-field of photonics and are used to convert electrical energy into light or vice versa. The study tracks the revenue accrued through the sale of automotive optoelectronics by various players worldwide. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market.

The automotive optoelectronics market is segmented by device type (LED, laser diode, image sensors, optocouplers, photovoltaic cells, and other device types) and geography (United States, Europe, China, Japan, Korea, Taiwan, and the Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Light-Emitting Diodes (LEDs) |

| Laser Diodes |

| Complementary Metal–Oxide–Semiconductor (CMOS) Image Sensors |

| Optocouplers |

| Photovoltaic Cells |

| Other Device Types |

| Exterior Lighting | Headlamps |

| Daytime Running Lamps | |

| Signal and Rear Combination Lamps | |

| Interior and Ambient Lighting | |

| Advanced Driver Assistance Systems (LiDAR, Camera) | |

| Infotainment and Central Display | |

| Battery and Power-train Monitoring | |

| Photovoltaic Energy Harvesting |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Heavy Commercial Vehicles (HCVs) |

| Internal Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| Fuel-Cell Electric Vehicles |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN | ||

| Taiwan | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Device Type | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Complementary Metal–Oxide–Semiconductor (CMOS) Image Sensors | |||

| Optocouplers | |||

| Photovoltaic Cells | |||

| Other Device Types | |||

| By Application | Exterior Lighting | Headlamps | |

| Daytime Running Lamps | |||

| Signal and Rear Combination Lamps | |||

| Interior and Ambient Lighting | |||

| Advanced Driver Assistance Systems (LiDAR, Camera) | |||

| Infotainment and Central Display | |||

| Battery and Power-train Monitoring | |||

| Photovoltaic Energy Harvesting | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles (LCVs) | |||

| Heavy Commercial Vehicles (HCVs) | |||

| By Propulsion Type | Internal Combustion Engine Vehicles | ||

| Hybrid Electric Vehicles | |||

| Battery Electric Vehicles | |||

| Fuel-Cell Electric Vehicles | |||

| By Sales Channel | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| ASEAN | |||

| Taiwan | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current market size of automotive optoelectronics?

The automotive optoelectronics market stood at USD 6.57 billion in 2026 and is projected to reach USD 9.71 billion by 2031, growing at an 8.13% CAGR over 2026-2031.

Which device category dominates revenue today?

CMOS image sensors led in 2025 with a 45.52% revenue share, owing to their critical role in ADAS vision systems.

Which application will grow fastest through 2031?

ADAS is expected to register the highest CAGR at 16.72% as automakers integrate LiDAR and high-resolution cameras to enable higher levels of driving automation.

How fast is optoelectronic content expanding in battery electric vehicles?

BEV-related optoelectronic demand is forecast to climb at a 19.62% CAGR as electrified platforms rely on compact, energy-efficient optical devices.

Why are GaAs/GaN wafer shortages significant?

8-inch GaAs/GaN wafer scarcity constrains the output of high-power laser diodes and SiC devices, delaying advanced headlamp and power-train programs and trimming industry CAGR by an estimated 0.6%.

Which region offers the largest growth opportunity?

Asia Pacific, already holding 43.12% share in 2025, is forecast for the fastest regional CAGR at 14.05%, driven by China’s EV surge and regional semiconductor capacity.

Page last updated on: