Automotive Semiconductor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 107.34 Billion |

| Market Size (2031) | USD 148.57 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

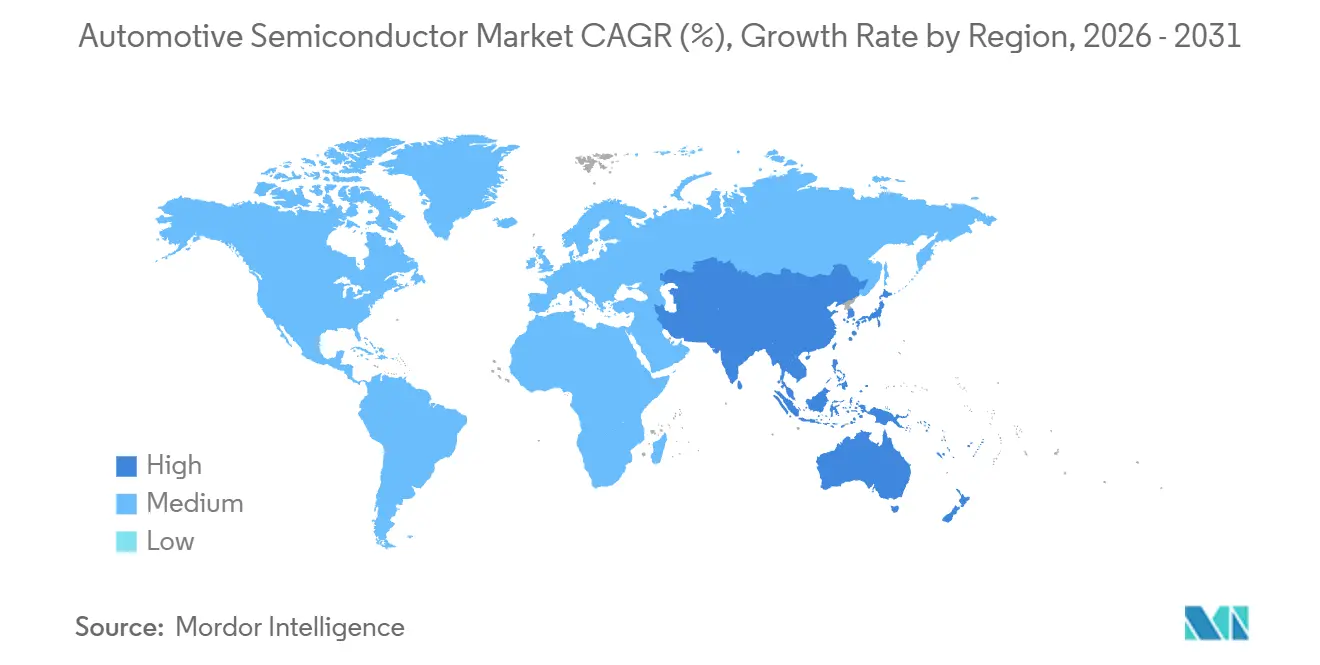

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Semiconductor Market Analysis by Mordor Intelligence

The Automotive Semiconductor Market size is projected to expand from USD 99.74 billion in 2025 and USD 107.34 billion in 2026 to USD 148.57 billion by 2031, registering a CAGR of 6.72% between 2026 to 2031. Zonal electrical-and-electronic (E/E) architectures, rising electric-vehicle penetration, and regulatory pressure for advanced safety have collectively pushed chip content per vehicle to historic highs. Battery electric models already account for more than half of global semiconductor demand, despite representing a smaller share of production, confirming that value growth now depends far more on content per unit than on unit volumes. High-performance system-on-chip (SoC) platforms have transitioned from concept to mainstream as automakers adopt software-defined vehicles and shorten their product cycles. The Asia Pacific leads in revenue thanks to a robust Chinese industrial policy, while sovereign wealth programs in the Middle East have made that region the fastest-growing frontier. Competitive intensity is rising as traditional integrated device manufacturers (IDMs) confront hyperscalers and mobile-chip specialists that leverage leading-edge nodes to win centralized-compute sockets.

Key Report Takeaways

- By propulsion type, battery electric vehicles accounted for 54.19% of the automotive semiconductor market share in 2025; internal-combustion vehicles are forecast to trail with a 17.49% CAGR through 2031.

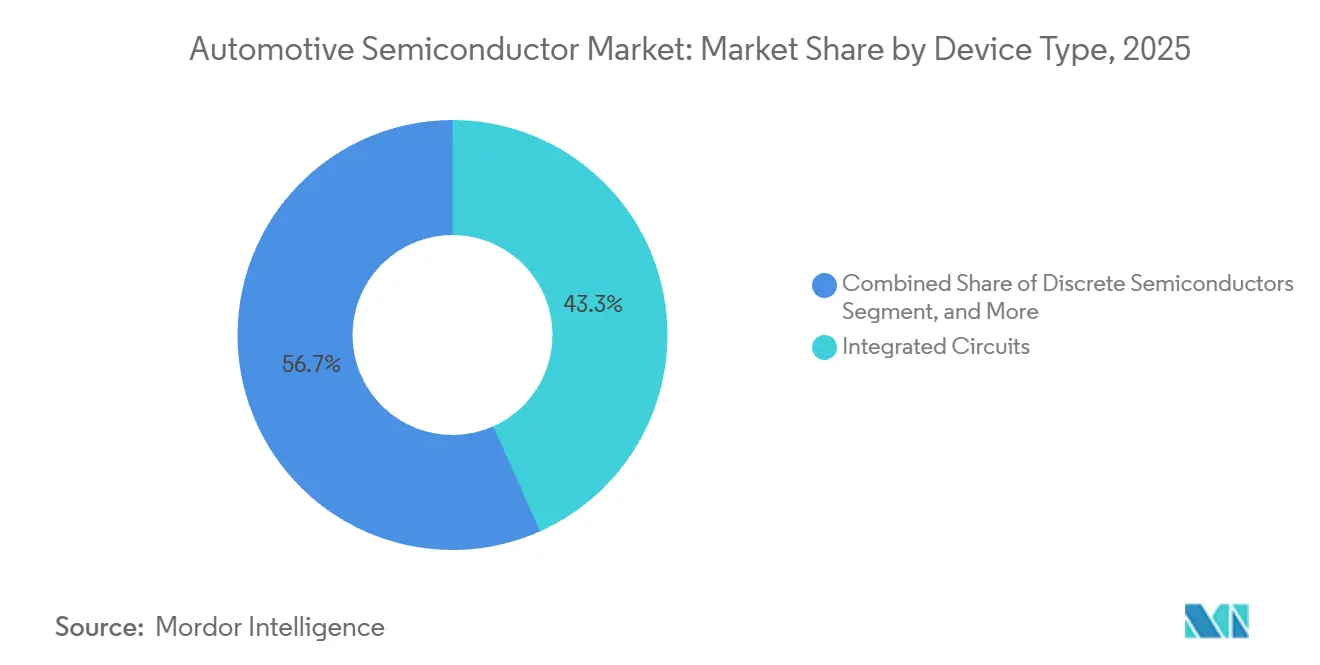

- By device category, integrated circuits led with 43.32% revenue share in 2025, while sensors and microelectromechanical systems are poised to expand at a 17.61% CAGR to 2031.

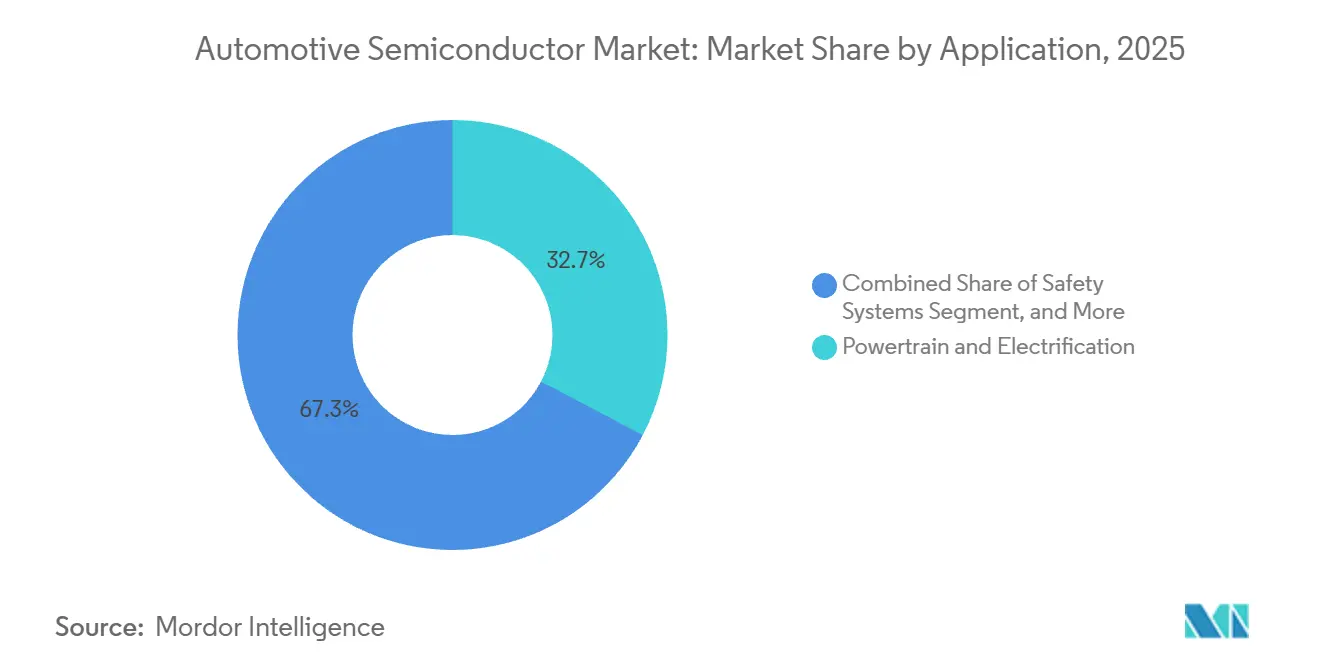

- By application, powertrain and electrification captured 32.71% of 2025 revenue; advanced driver-assistance systems are projected to post the fastest growth rate of 17.81% between 2026 and 2031.

- By business model, IDMs retained a 67.58% share in 2025, yet fabless vendors are tracking an 18.43% CAGR through 2031.

- By geography, Asia Pacific commanded 45.87% of 2025 revenue, whereas the Middle East is expected to log an 18.12% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing vehicle production in emerging economies | +2.8% | Asia Pacific, Middle East and Africa | Medium term (2-4 years) |

| Rising demand for advanced safety and comfort systems | +3.2% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Electrification boosting semiconductor content per vehicle | +4.1% | Global, led by China, Europe and North America | Medium term (2-4 years) |

| Zonal E/E architectures and software-defined vehicles spur high-end processors | +2.9% | Global, concentrated in premium segments | Long term (≥ 4 years) |

| Government incentives for auto-grade foundry capacity expansion | +1.7% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Adoption of SiC and GaN power devices in electric powertrains | +2.4% | Global, strong uptake in China and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Vehicle Production in Emerging Economies

Light-vehicle output in India reached 5.8 million units in 2025, a 9% annual rise, while Southeast Asian assembly topped 3.2 million units, pushing semiconductor demand for entry-level models that now ship with stability control and basic connectivity as standard. New assembly and test capacity under India’s Production-Linked Incentive scheme is localizing supply and trimming import costs, a shift mirrored by incentive-backed investments in Mexico and the Gulf states. These moves shorten supply chains, anchor design talent regionally, and accelerate time to qualification. As emerging-market buyers demand safety features once reserved for premium segments, chip volumes per vehicle continue to climb. The result is sustained structural expansion for the automotive semiconductor market well beyond global vehicle growth rates.

Rising Demand for Advanced Safety and Comfort Systems

The European Union's General Safety Regulation mandated intelligent speed assistance, advanced emergency braking, and driver monitoring for all new type approvals after July 2024, effectively standardizing radar and camera content across mainstream models. U.S. crash-reduction data have reinforced the business case, enabling insurers to lower premiums for vehicles fitted with automated emergency braking, which, in turn, spurs consumer uptake. China’s New Car Assessment Program raised its five-star standard in 2025, prompting domestic brands to incorporate higher-resolution sensors capable of detecting pedestrians up to 100 meters away. These mandates are spreading to cost-sensitive regions, lifting average semiconductor bill-of-materials values for even compact cars. Tier-one suppliers with deep functional-safety pedigrees are well positioned, as ISO 26262 barriers favor proven platforms.

Electrification Boosting Semiconductor Content per Vehicle

Battery electric vehicles averaged USD 1,200 in semiconductor content during 2025, almost triple internal-combustion equivalents, due to traction inverters, onboard chargers, and battery-management integrated circuits.[1]International Energy Agency, “Global EV Outlook 2025,” iea.org Silicon-carbide metal-oxide-semiconductor transistors enable 800-volt architectures that slash charging times below 20 minutes, though substrate capacity remains constrained until new 200-millimeter wafer lines reach scale. Automakers increasingly sign long-term supply agreements to lock in wide-bandgap materials, ensuring cost visibility and design stability. Gallium-nitride devices have begun displacing silicon in onboard chargers for vehicles priced above USD 50,000, leveraging higher switching frequencies to shrink magnetics. With the International Energy Agency forecasting 17 million electric cars in 2026, incremental chip revenue tied to electrification alone is set to exceed USD 10 billion annually.

Zonal E/E Architectures and Software-Defined Vehicles Spur High-End Processors

Major tier-one suppliers secured 2025 production awards for zonal controllers that collapse dozens of electronic control units into a handful of high-compute nodes. NXP’s S32 family on TSMC 5 nanometer merges real-time safety cores, application processors, and hardware security to support over-the-air updates without compromising ASIL-D requirements. Renesas started producing a 3 nanometer SoC that delivers 200 TOPS for sensor fusion, highlighting the rapid migration of automotive logic to cutting-edge nodes. This compute density lets automakers sell post-sale feature unlocks, creating durable revenue streams while shortening hardware replacement cycles. Consequently, demand is pivoting toward advanced substrates, fast memory, and high-speed interconnects, reinforcing the secular uptrend in the automotive semiconductor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced-feature vehicles | -1.9% | Global, pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Persistent supply-chain constraints and chip shortages | -1.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Scarcity and cost of wide-bandgap substrates | -0.8% | Global, affects high-voltage EV platforms | Medium term (2-4 years) |

| Lengthy automotive qualification cycles slow time-to-market | -1.1% | Global, impacting all OEMs and tier-ones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced-Feature Vehicles

Equipping a mainstream vehicle with Level 2 driver assistance pushes average transaction prices above USD 48,000 in the United States, making such cars 22% costlier than segment norms. Semiconductor content for these feature packs often exceeds USD 1,000, and automakers apply significant mark-ups to recover R&D and validation costs. Emerging markets with high price elasticity feel the effect most acutely, limiting penetration to upper trims. Redundant sensor architectures raise costs further because regulators insist on fail-operational designs for pedestrian safety. Although suppliers are exploring lower-cost sensor fusion that reduces lidar reliance, functional-safety ceilings still restrain rapid cost downs.

Persistent Supply-Chain Constraints and Chip Shortages

Automotive chip lead times averaged 22 weeks in late 2025, still markedly above the pre-pandemic baseline of 12-14 weeks.[2]Semiconductor Equipment and Materials International, “Long-Term Lead-Time Trends,” semi.org European OEMs lost an estimated 180,000 units of output in 2025 to microcontroller shortages, and many tier-one suppliers doubled buffer inventory to hedge risk, depressing their return on invested capital. Geopolitical trade friction has pushed automakers to qualify multiple foundries, but dual-sourcing critical components consumes engineering bandwidth and prolongs validation. Roughly 40% of analog and power capacity remains on 200-millimeter tools with limited scope for expansion, so bottlenecks persist even as new subsidized fabs arrive later in the decade. Until mature-node capacity broadens, supply risk will continue tempering the automotive semiconductor market’s growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integration Dominates, Sensors Accelerate

The automotive semiconductor market size for integrated circuits stood highest in 2025, capturing 43.32% revenue thanks to microcontrollers, SoCs, and memory that underpin zonal and centralized architectures. Growing compute density, embedded hardware security, and over-the-air update readiness make these devices indispensable. Market participants note that the latest SoCs combine heterogeneous CPU clusters, graphics engines, and neural processors, allowing a single package to handle cockpit, connectivity, and low-speed autonomy workloads. Demand for embedded memory continues to surge as map data and neural network weights expand.

Sensors and microelectromechanical systems are forecast to post a 17.61% CAGR, the fastest pace among device categories. Radar, lidar, camera, ultrasonic, and inertial units now ship in redundant arrays to deliver 360-degree perception for mandated safety functions. Texas Instruments’ corner-radar chip, which integrates an RF front-end and signal processing on one die, typifies this consolidation trend. Meanwhile, wide-bandgap power discretes are migrating into multichip modules, slightly tempering discrete unit growth but lifting average selling prices. The pathway ahead favors suppliers that can blend sensing, processing, and actuation into integrated platforms, reinforcing scale advantages in the automotive semiconductor market.

By Vehicle Propulsion: Combustion Retains Volume, Battery Electric Drives Value

Battery electric vehicles still deliver the highest semiconductor value per vehicle, giving them 54.19% of 2025 semiconductor revenue. Mild-hybrid 48-volt systems add converters and controllers, nudging chip content upward even before full electrification. In contrast, the automotive semiconductor market size tied to internal-combustion vehicles will expand at a projected 17.49% CAGR, influenced by increasing electronic content even in conventional platforms. Each battery electric car carries USD 600-USD 800 of power electronics alone, dwarfing combustion counterparts.

Hybrid configurations offer a bridge solution, demanding dual power-management architectures that lift per-vehicle chip value to roughly USD 700. Fuel-cell variants remain niche but command specialized high-voltage converters, hinting at future upside should hydrogen infrastructure mature. Automakers such as BYD and Stellantis have announced standardized 400-volt and 800-volt platforms that rely heavily on silicon-carbide modules, tightening the link between propulsion choice and semiconductor bill of materials. The data confirm that value growth will hinge on electrified drivetrains, even as combustion engines dominate production counts through the near term.

By Application: Powertrain Leads, ADAS Surges

Powertrain and electrification yielded 32.71% of 2025 revenue, cementing their role as the single largest application block. Content ranges from gate-driver ICs and current sensors to battery-management and thermal-control ASICs. Silicon-carbide MOSFET modules priced well above traditional IGBTs are gradually standardizing in premium electric vehicles, raising revenue density per inverter.

Advanced driver-assistance systems stand out as the fastest-growing slice, projected to grow 17.81% annually through 2031. Mandates for automated emergency braking, lane-keeping, and driver monitoring ensure baseline demand, while premium brands push toward Level 3 conditional automation that requires centralized perception compute of 200-2,000 TOPS. Here, the automotive semiconductor market share increasingly tilts toward graphics-oriented SoCs from players like NVIDIA and custom ASIL-D designs by tier-one integrators. Body electronics and infotainment maintain steady trajectories, but their relative weight diminishes as high-performance compute and powertrain semiconductors command a larger revenue mix.

By Business Model: IDMs Hold Scale, Fabless Vendors Accelerate

IDMs secured 67.58% of 2025 revenue, leveraging captive fabs to guarantee supply, iterate quickly on automotive qualification, and retain full margin stacks. Infineon and Renesas continue to press this advantage by extending silicon-carbide and microcontroller capacity. Still, fabless players are scaling faster, aided by foundry commitments to qualify sub-10 nanometer nodes for automotive reliability. The automotive semiconductor market size attributable to fabless vendors is projected to post an 18.43% CAGR, as OEMs value custom silicon aligned with proprietary software.

Foundry partners such as TSMC and Samsung have earmarked dedicated automotive lines, absorbing AEC-Q validation costs and lowering entry barriers. Automakers hiring silicon design teams further blur the traditional IDM–fabless divide. Over time, the ecosystem will likely converge on hybrid models that mix in-house design with external manufacturing, but the present cycle still rewards IDMs for their vertical resilience during supply shortages.

Geography Analysis

Asia Pacific generated 45.87% of 2025 revenue, anchored by China’s 9 million electric-vehicle sales and its 25% domestic-content mandate for new-energy vehicles.[3]China Association of Automobile Manufacturers, “New-Energy Vehicle Sales,” caam.org.cn Proximity to foundries and assembly houses enables faster design-for-cost loops and the prompt qualification of custom devices, thereby strengthening the region’s influence on semiconductor roadmaps. South Korea’s memory giants have pledged to dedicate 15% of their 300-millimeter wafer output to automotive customers by 2027, thereby deepening the supply-chain cluster.

North America and Europe combined for roughly 35% of revenue. Aggressive safety and decarbonization targets continue to drive high semiconductor intensity, while public incentives under the United States CHIPS and Science Act and the European Union Chips Act channel billions of dollars into domestic fabs. Those plants will not fully ramp up until 2027-2028, leaving the regions reliant on Asian imports in the interim.

The Middle East, although a small base today, is expected to log an 18.12% CAGR through 2031. Sovereign funds in the United Arab Emirates and Saudi Arabia are backing electric fleet mandates and local assembly that specify advanced driver-assistance and battery-management features, pulling global tier-one suppliers into greenfield partnerships. Africa and South America remain volume markets for entry-level vehicles, yet regulatory adoption of electronic stability control and tire-pressure monitoring is gradually lifting chip demand.

Mordor Intelligence provides coverage of the automotive semiconductor market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The top ten suppliers accounted for approximately 65% of the 2025 revenue, indicating a moderately concentrated structure. NXP Semiconductors, Infineon Technologies, and Renesas Electronics collectively hold more than 40% of the microcontroller and power-discrete revenue, benefiting from rich automotive pedigrees and deep customer relationships. Yet hyperscalers and mobile-SoC leaders, including NVIDIA and Qualcomm, are claiming centralized compute sockets in premium nameplates by porting graphics and modem roadmaps to zonal architectures.

Government-subsidized capacity expansions have become a strategic lever. TSMC’s Arizona mega-fab, for example, secured USD 40 billion in pledges, part of which targets AEC-Q-qualified 4-nanometer production lines from 2027. In Europe, STMicroelectronics and GlobalFoundries are jointly building an 18-nanometer fab in France, with funding partly provided by Chips Act grants. Strategic alliances between automakers and chip designers also intensified, as seen in General Motors’ 2025 partnership with Qualcomm on custom cockpit and driver-assistance processors.

White-space innovation centers on edge AI accelerators designed for low-latency sensor fusion. Ambarella’s 120-TOPS SoC positions the firm as a challenger in perception processing. Chinese vendors such as Horizon Robotics leverage domestic policy support to gain share in local markets. Across the board, compliance with ISO 26262 and UNECE WP.29 cybersecurity rules has become a competitive moat, rewarding suppliers that can certify ASIL-D systems and deliver secure over-the-air updates.

Automotive Semiconductor Industry Leaders

NXP Semiconductors N.V.

Infineon Technologies AG

Renesas Electronics Corporation

STMicroelectronics N.V.

Texas Instruments Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Renesas Electronics began mass production of the R-Car X5H SoC on TSMC 3 nanometer lines, targeting centralized compute in 2027 model-year luxury vehicles.

- November 2025: TSMC confirmed its Arizona fab will allocate one 300-millimeter line for AEC-Q100-qualified 4-nanometer and 5-nanometer processes, with volume starting H2 2027.

- October 2025: Wolfspeed ramped its 200-millimeter silicon-carbide wafer facility in New York to full output, under multi-year supply deals with Mercedes-Benz and General Motors.

- September 2025: Qualcomm and General Motors signed a multi-year agreement to co-develop bespoke cockpit and driver-assistance processors based on Snapdragon Digital Chassis.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the automotive semiconductor market as the yearly revenue generated from new, application-grade integrated circuits, discrete power devices, sensors, memories, and analog components that are designed, fabricated, or packaged expressly for on-road passenger and commercial vehicles. The scope stretches from basic engine-control chips to high-bandwidth SoCs used in ADAS, but excludes aftermarket remanufactured parts and generic consumer semiconductors designed for non-automotive use.

Scope exclusion: refurb-grade chips sold through independent distributors are not covered.

Segmentation Overview

- By Device Type

- Discrete Semiconductors

- Diodes

- Transistors

- Power Transistors

- Rectifiers and Thyristors

- Other Discrete Devices

- Optoelectronics

- Light-Emitting Diodes (LEDs)

- Laser Diodes

- Image Sensors

- Optocouplers

- Other Optoelectronic Devices

- Sensors and MEMS

- Pressure Sensors

- Magnetic Field Sensors

- Actuators

- Acceleration and Yaw-Rate Sensors

- Temperature and Other Sensors

- Integrated Circuits

- By Integrated Circuit Type

- Analog

- Micro

- Microprocessors (MPU)

- Microcontrollers (MCU)

- Digital Signal Processors

- Logic

- Memory

- By Technology Node (Shipment Volume Not Applicable)

- < 3 nm

- 3 nm

- 5 nm

- 7 nm

- 16 nm

- 28 nm

- > 28 nm

- By Integrated Circuit Type

- Discrete Semiconductors

- By Vehicle Propulsion

- Internal Combustion Engine Vehicles

- Hybrid Vehicles

- Battery Electric Vehicles

- Fuel-Cell Electric Vehicles

- By Application

- Powertrain and Electrification

- Advanced Driver-Assistance Systems (ADAS) and Autonomous Driving

- Body Electronics and Comfort

- Infotainment and Connectivity

- Safety Systems

- By Business Model

- Integrated Device Manufacturer (IDM)

- Design / Fabless Vendor

- Foundry Service Provider

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed chip designers, tier-1 electronics suppliers, and procurement managers across Asia-Pacific, Europe, and North America. These conversations clarified average semiconductor content per BEV versus ICE models, verified channel mark-ups, and stress-tested assumed ASP erosion curves before forecasts were locked.

Desk Research

We began by mapping the market universe through publicly available tier-1 data sets, WSTS monthly automotive IC billings, OICA vehicle production tallies, IEA EV stock numbers, UN Comtrade HS-8541/8542 trade flows, and technical papers indexed in IEEE Xplore. Company 10-Ks, investor decks, and trade association portals such as SEMI and ACEA provided unit-cost clues and design-win disclosures. Supplementary insight was pulled from D&B Hoovers financials and Questel patent analytics, enabling us to gauge technology diffusion speeds. The sources cited above illustrate, not exhaust, the reference pool consulted.

Market-Sizing & Forecasting

A blended top-down build, vehicle production volumes multiplied by semiconductor bill-of-material values that vary by drivetrain, safety grade, and automation level created the first demand pool, which we cross-checked with selective bottom-up roll-ups of leading supplier revenues. Key variables inside our model include: 1. Average chips-per-vehicle, 2. Regional BEV penetration trajectory, 3. Power device ASP migration from silicon to SiC, 4. Memory density per infotainment stack, and 5. WSTS automotive IC shipment indices.

Multivariate regression on these drivers underpins a forecast for the specified period, while scenario analysis captures supply chain shocks. Gaps in the bottom-up corroboration, such as missing private-company revenue splits, were bridged using channel shipment ratios derived from customs data.

Data Validation & Update Cycle

Outputs flow through dual analyst reviews that flag +/-5% variances against external shipment signals. When quarterly OEM production deviates materially, we refresh the model ahead of the scheduled annual update, ensuring clients receive the latest viewpoint.

Why Our Automotive Semiconductor Baseline Earns Trust

Published estimates often diverge because firms choose different functional scopes, cost assumptions, and refresh rhythms.

Key gap drivers include narrower component baskets, conservative EV adoption curves, or single-source ASP assumptions used by other publishers, whereas our study blends real-world bill-of-materials audits with continuous production tracking.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 100.48 B (2025) | Mordor Intelligence | - |

| USD 42.9 B (2022) | Global Consultancy A | Excludes sensors and memory; older base year |

| USD 71.97 B (2024) | Industry Journal B | Uses fixed ASP decline, limited EV segmentation |

| USD 44.94 B (2023) | Regional Consultancy C | Focuses on discrete power only; no regional mix shift |

In sum, our disciplined scope selection, mixed-method modeling, and annual refresh cadence give decision-makers a baseline that aligns with observable production realities while remaining transparent and repeatable.

Key Questions Answered in the Report

How large is the automotive semiconductor market in 2026?

The market is estimated at USD 107.34 billion in 2026 and is projected to reach USD 148.57 billion by 2031.

What is driving semiconductor demand in battery electric vehicles?

Each battery electric car carries USD 1,200 of semiconductor content, mainly for traction inverters, onboard chargers, and battery-management systems.

Which region leads automotive semiconductor revenue?

Asia Pacific held 45.87% of global revenue in 2025, propelled by Chinese electric-vehicle production and domestic-content mandates.

Why are zonal E/E architectures important?

They consolidate dozens of control units into high-compute nodes, enabling over-the-air updates and reducing wiring complexity, thereby boosting demand for advanced SoCs.

How are supply shortages affecting automakers?

Lead times for key microcontrollers remain near 22 weeks, forcing OEMs to carry higher inventory, reschedule production, and dual-source components to mitigate risk.

Page last updated on: