Phenol Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

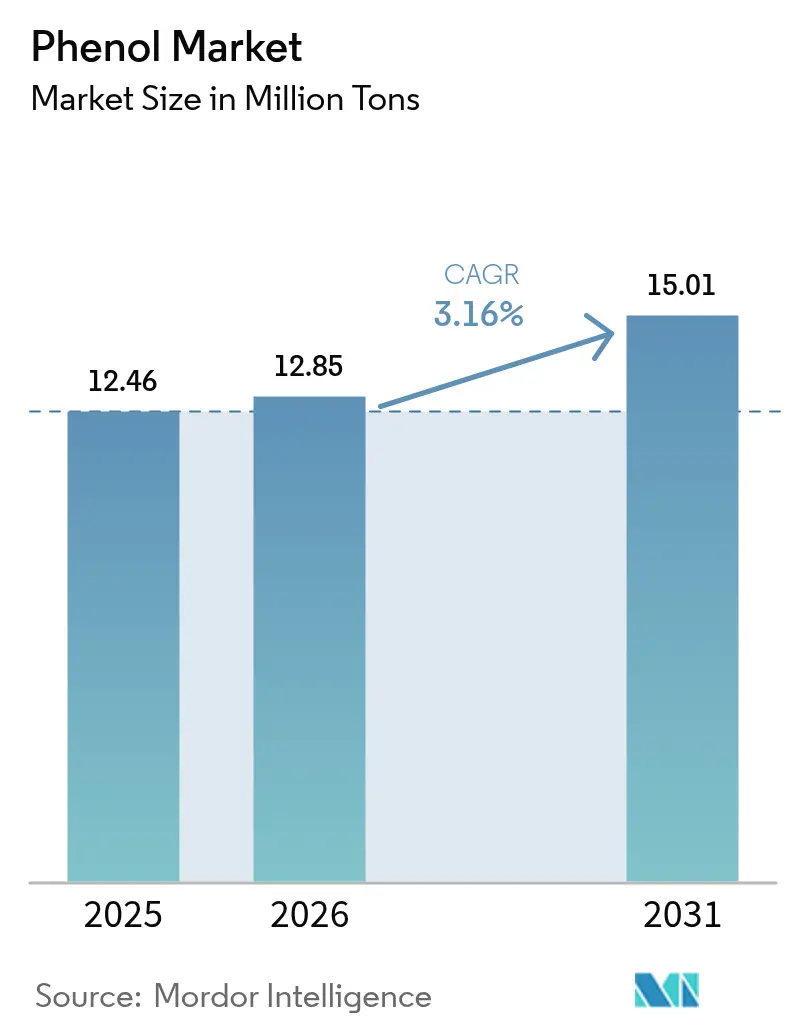

| Market Volume (2026) | 12.85 Million tons |

| Market Volume (2031) | 15.01 Million tons |

| Growth Rate (2026 - 2031) | 3.16% CAGR |

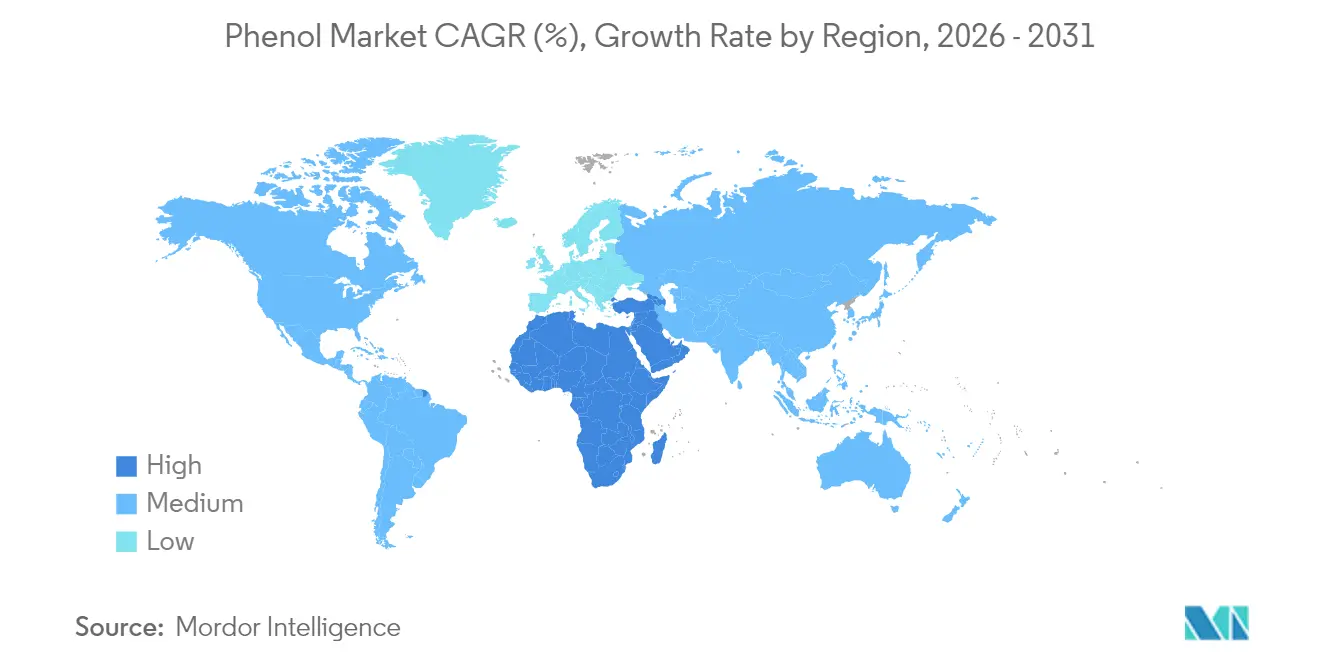

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Phenol Market Analysis by Mordor Intelligence

The Phenol market size is expected to grow from 12.46 Million tons in 2025 to 12.85 Million tons in 2026 and is forecast to reach 15.01 Million tons by 2031 at 3.16% CAGR over 2026-2031. This measured expansion reflects maturation in long-established applications, heavier regulatory oversight, and the steady rollout of sustainable production technologies. Increasing polycarbonate demand in electronics, expanding automotive lightweighting programs, and infrastructure investments that favor thermally efficient insulation are expected to keep incremental volume growth positive. Capacity additions in Asia-Pacific, particularly China, will continue to reshape global trade flows even as European producers rationalize higher-cost assets. At the same time, bio-based routes to cumene and lignin-derived phenolics are creating a dual-track innovation race that may compress traditional producer margins while allowing first movers to command specialty premiums. Competitive strategies therefore hinge on integration across the phenol–acetone–derivatives chain, feedstock flexibility, and rapid commercialization of low-carbon pathways.

Key Report Takeaways

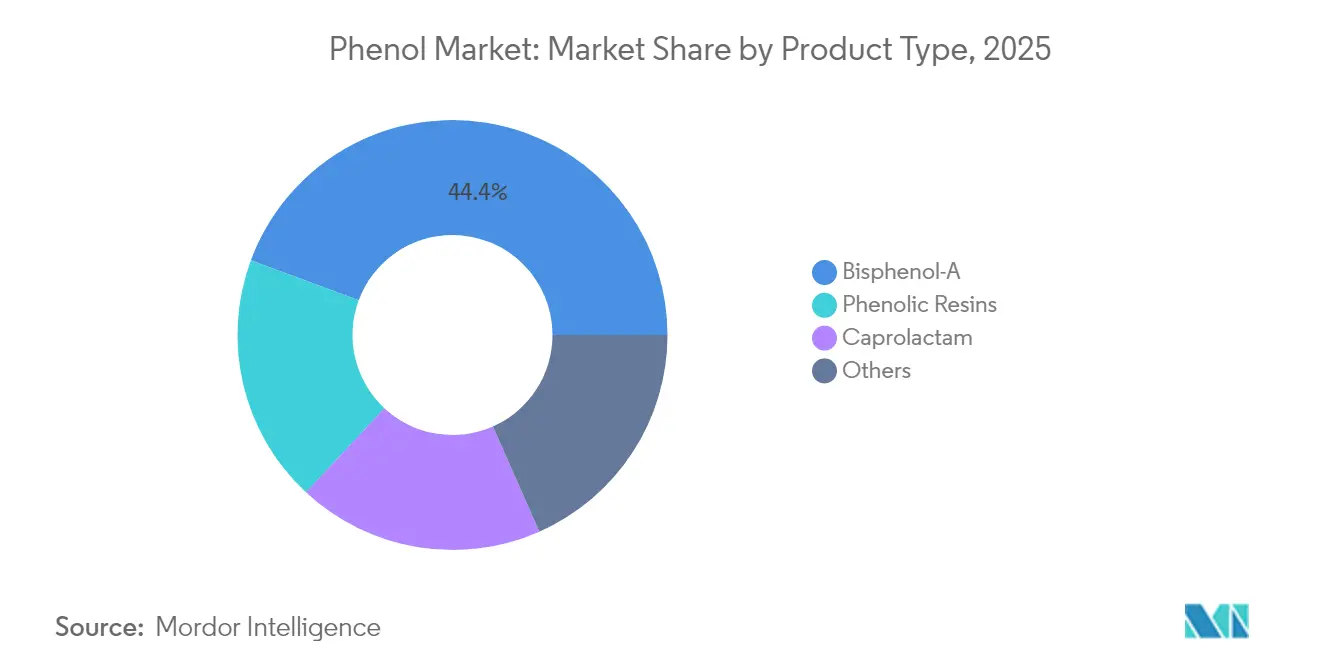

- By product type, bisphenol-A held 44.35% of the phenol market share in 2025, while caprolactam recorded the highest projected CAGR at 4.86% through 2031.

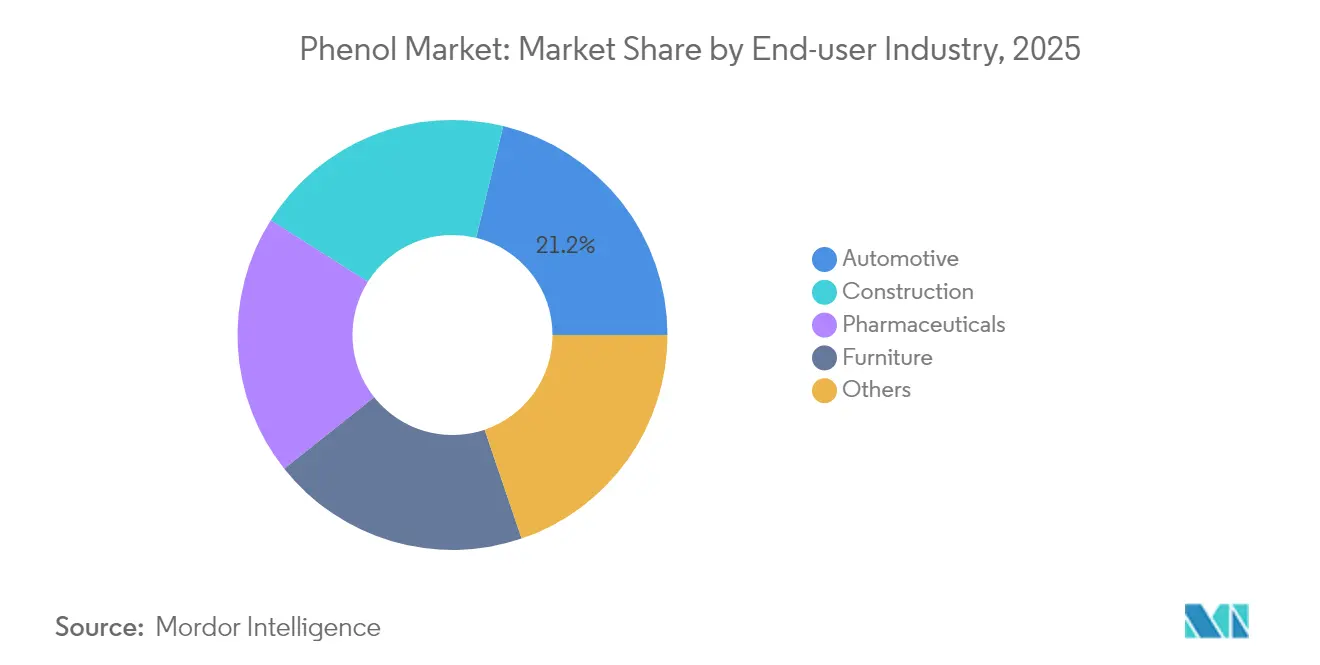

- By end-user industry, the automotive segment led with 21.21% revenue share in 2025; pharmaceuticals are forecast to advance at a 5.18% CAGR to 2031.

- By geography, Asia-Pacific commanded 53.94% of the phenol market size in 2025; the Middle East and Africa region is set to expand at a 5.42% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Phenol Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Demand for Bisphenol-A in Polycarbonates and Epoxy Resins | +0.8% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in Lightweight Automotive Phenolic Composites | +0.6% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Construction-Sector Uptake of Phenolic Insulation Boards | +0.4% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Sustainable Cumene Routes Using Bio/Green Propylene | +0.3% | Europe and North America initially, global expansion | Long term (≥ 4 years) |

| Integration of Phenol Units with On-Purpose PO/SM Complexes | +0.5% | Asia-Pacific and Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Demand for Bisphenol-A in Polycarbonates and Epoxy Resins

Bisphenol-A continues to be the backbone monomer for polycarbonate and epoxy resins used in electronics housings, automotive glazing, and medical devices where clarity and impact strength are non-negotiable[1]American Chemistry Council, “Polycarbonate Applications in EVs,” americanchemistry.com . Battery enclosures in electric vehicles now specify flame-retardant polycarbonate blends, further lifting BPA volumes even after Europe’s recent bans in food packaging. China and India are offsetting those European losses through aggressive electronics manufacturing and infrastructure projects that deploy large polycarbonate sheet volumes. Producers are maintaining capacity utilization by diverting cargoes to Southeast Asian converters and North American contract molders. Over the medium term, incremental BPA growth should keep operating rates near 85%, supporting the broader phenol market despite localized restrictions.

Growth in Lightweight Automotive Phenolic Composites

Automakers are validating phenolic composites beyond brake boosters and clutch plates, with structural intake manifolds and air-management components already proven at BMW’s series plants. The material’s ability to maintain dimensional stability at 140 °C while reducing mass by nearly 20% aligns with stringent emissions and range targets. Electric-vehicle platforms add another pull on phenol derivatives for battery module housings where flame-spread performance and mechanical integrity under thermal runaway are critical. Original equipment suppliers (OES) report 15-year durability cycles and consistent crash-resistance metrics, prompting tier-one composite processors in Europe and the United States to enter long-term offtake contracts. These developments elevate the phenol market by shifting demand toward high-value engineering applications with price-inelastic characteristics.

Construction-Sector Uptake of Phenolic Insulation Boards

Phenolic foam delivers thermal conductivities of 0.020–0.025 W/m·K, roughly 30% lower than conventional PUR foams, allowing thinner wall assemblies and higher usable floor space. European fire codes now prioritize insulation that withstands 1 300 °C flashover with minimal smoke toxicity, a standard phenolic boards comfortably meet. Developers of multi-family towers in the United Kingdom and Germany are specifying phenolic panels to comply with post-Grenfell façade requirements. North American builders increasingly cite life-cycle savings from reduced HVAC loads, while humidity-prone ASEAN markets value the closed-cell water resistance that delays mold growth. Collectively, these factors underpin stable growth in construction-related phenolic resin pull-through.

Sustainable Cumene Routes Using Bio/Green Propylene

Sumitomo Chemical’s ethanol-to-propylene pilot demonstrated 50% conversion efficiency, positioning bio-propylene as a direct drop-in to existing cumene units. Life-cycle assessments show carbon-intensity cuts of 60-80% relative to naphtha-sourced feedstock, appealing to brands committed to science-based targets. Early adopters forecast certificate-backed premiums of USD 120–150 per ton for low-carbon phenol, equalizing economics once carbon taxes exceed USD 55 per ton of CO₂. Producers already leveraging renewable power at integrated sites in Belgium and Texas can bolt on bio-propylene supply with modest debottlenecking, fast-tracking commercialization and supporting the phenol market transition toward greener chemistry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BPA Restrictions in Food-Contact Applications | -0.7% | Europe immediately, potential global expansion | Short term (≤ 2 years) |

| Feedstock (Benzene and Propylene) Price Volatility | -0.4% | Global, with higher impact in naphtha-dependent regions | Short term (≤ 2 years) |

| Rise of Bio-Based Phenolic Alternatives | -0.2% | Europe and North America initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BPA Restrictions in Food-Contact Applications

The European Commission’s 2024 regulation eliminated BPA from can coatings and reusable food containers, removing nearly one-fifth of regional demand. Allowed transition windows force packagers to requalify materials inside 18 months, disrupting procurement pipelines and triggering inventory run-downs at epoxy resin producers. Similar draft proposals in Canada and several U.S. states add downside risk through 2027. Although industrial uses remain intact, the public-health spotlight on endocrine disruptors may dampen investor confidence, compelling phenol market participants to diversify toward less contentious derivative portfolios.

Feedstock (Benzene and Propylene) Price Volatility

North American styrene plant closures are curtailing benzene by-product output, tightening supply and lifting contract prices that feed directly into cumene cash costs. Concurrently, LyondellBasell’s Houston refinery shutdown removed 136 000 tons of propylene capacity, while new polypropylene plants hoover up incremental barrels. Each 10% rise in either feedstock strips 6-8% off integrated phenol margins, pressuring swing producers to idle units or seek tolling agreements. Asian refiners, buoyed by cheaper condensate, will likely backfill any Western shortfall, but shipping differentials can erode arbitrage opportunities, injecting further uncertainty into the phenol market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: BPA Dominance Faces Regulatory Headwinds

Bisphenol-A retained a 44.35% phenol market share in 2025, underpinned by entrenched polycarbonate volumes despite Europe’s food-contact ban . The phenol market size attached to BPA is now projected to grow at just 2.22% annually through 2031, compared with 4.86% for caprolactam. Producers with Chinese or Middle-Eastern assets are lifting utilization to offset Western demand erosion, driving new supply chains that circumvent regulatory bottlenecks. Phenolic resins, the second-largest application, benefit from rebounding construction activity, especially in commercial retrofits that favor low-smoke insulation boards. The caprolactam segment’s 4.86% CAGR rests on nylon 6 fiber expansion for technical textiles and lightweight automotive parts. Specialty intermediates such as alkylphenols serve surfactants, while xylenols feed disinfectant markets that expanded after recent public health crises. Advances in alkaline hydrolysis enable nylon recycling at industrial scale, looping waste back into caprolactam synthesis and potentially supporting a circular phenol market.

Shifting product mix now prioritizes higher-margin derivatives as commodity phenol contracts face margin compression from oversupply and volatile benzene pricing. As such, investment flows favor debottlenecking caprolactam and high-purity phenolic resin lines rather than greenfield BPA in Europe. Over the forecast horizon, technology licensors expect 1.5% energy-efficiency gains per retrofit cycle, unlocking incremental cost reductions. Environmental, social and governance (ESG) metrics are influencing customer procurement decisions, nudging producers toward bio-based phenol streams and recycled phenolic resins that command price premiums when accompanied by verified carbon intensity data.

By End-User Industry: Automotive Leadership Amid Pharma Acceleration

The automotive sector consumed 21.21% of phenol in 2025, a share that is likely to hold steady as electric-vehicle architectures intensify use of phenolic composites in battery casings and under-floor protection panels. The phenol market size tied to automotive applications is forecast to rise 3.32% annually through 2031, driven by Asian vehicle output and North American electrification mandates. Construction remains the second-largest consumer, anchored by phenolic insulation boards that meet stringent fire and energy codes in Europe and increasingly in U.S. states adopting the International Building Code 2025 edition. Pharmaceutical uses, while smaller, clock the fastest 5.18% CAGR as antiseptic demand sustains post-pandemic healthcare spending. Purified phenol also serves as a key intermediate in analgesic and derivate synthesis, drawing premium pricing.

Furniture makers deploy phenolic resins in engineered wood and decorative laminates, with demand linked to residential renovation cycles and the rise of multipurpose home-office spaces. Electronics, adhesive formulations, and specialty chemical blends fall under “Others,” reflecting diverse outlets that grant producers a hedge against cyclical slowdowns in any single sector. Regulatory agencies such as the FDA and European Medicines Agency dictate pharmaceutical-grade phenol purity, prompting investment in dedicated separation trains that bolster value capture. Overall, end-user diversification softens volatility in the phenol market and supports steady consumption growth across the forecast period.

Geography Analysis

Asia-Pacific retained 53.94% of phenol market size in 2025, buoyed by China’s massive oil-to-chemicals complexes that achieve 40% chemical yield versus traditional 15-20% refinery lines. India’s USD 1.1 billion Gujarat project will add phenol, acetone, and BPA capacity by 2027, aligning with the country’s “Make in India” strategy for chemical self-sufficiency. Japan and South Korea supply high-end downstream derivatives, especially optical-grade polycarbonate and high-heat phenolic compounds for electronics, while ASEAN nations feed rising construction and furniture sectors. These market dynamics ensure Asia-Pacific remains the principal demand and supply node.

North America faces feedstock-induced volatility yet benefits from abundant shale gas that supports competitive acetone co-product pricing. However, refinery shutdowns have tightened propylene supply, compressing margins and prompting talks of tolling arrangements for split-feed cumene units. U.S. tariff policies and anti-dumping duties could offer temporary relief against surging Asian imports, although sustained competitiveness will depend on energy-efficiency investments and potential bio-propylene partnerships.

Europe’s phenol producers grapple with high energy costs and environmental regulations, prompting consolidation efforts such as LyondellBasell’s review of six assets. The continent’s demand outlook is further clouded by BPA restrictions and aggressive climate targets that favor bio-based alternatives. Middle East and Africa represent the fastest-growing region at a 5.42% CAGR, anchored by integrated refinery-petrochemical complexes in Saudi Arabia and the UAE that exploit favorable feedstock economics and proximity to Asian import hubs. South America is comparatively small but stable, with Brazil absorbing most phenol for automotive brake components and construction insulation boards. Economic reforms in Argentina could unlock modest upside, yet currency volatility remains a near-term risk. Collectively, geographic rebalancing underpins diverse growth vectors that reinforce a global phenol market.

Competitive Landscape

The phenol market is moderately concentrated, with the top five producers accounting for roughly 55% of installed capacity. Integrated players such as SABIC, INEOS, and Mitsubishi Chemical leverage captive benzene and propylene supplies to operate at lower unit costs, while Chang Chun, LG Chem, and Kumho P&B focus on regional downstream integration. SABIC’s Fujian complex showcases the shift toward Asian mega-sites with energy-efficient architectures based on KBR technology that recycles 99% of process water and reduces CO₂ by 400 kg per ton of phenol[2]KBR Process Technology, “Fujian Phenol Project,” kbr.com . LyondellBasell’s planned asset divestitures in Europe highlight margin pressures in high-cost jurisdictions and signal a potential eastward shift of production capacity.

Strategic moves in 2024–2025 include Deepak Nitrite’s investment in Gujarat and Stora Enso advancing NeoLigno® binder commercialization, each demonstrating divergent pathways—scale integration versus specialty innovation—for value creation in the phenol market. Technology licensors emphasize high-selectivity oxidation catalysts and advanced heat-integration schemes capable of 12% power consumption cuts compared with 2018-vintage lines. ESG compliance and customer carbon audits increasingly influence contract awards, favoring operators with renewable-powered plants or life-cycle-assessed low-carbon phenol. Suppliers that can certify chain-of-custody integrity through blockchain platforms are likely to secure premium long-term offtake agreements with multinational OEMs. Overall competitive intensity will remain elevated, particularly in Asia-Pacific, where new entrants backed by state-owned energy firms benefit from low interest rates and subsidized infrastructure.

Phenol Industry Leaders

INEOS Group

Moeve

Mitsubishi Chemical Group Corporation

Kumho P&B Chemicals Inc.

LG Chem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Deepak Nitrite Ltd's subsidiary Deepak Chem Tech invested Rs 3,500 crore (USD 40.6 million) through a combination of debt and equity to establish a manufacturing complex for phenol and solvents production. The facility aims to produce 185 KTA of acetone, 300 KTA of phenol, and 100 KTA of isopropyl alcohol (IPA), which will approximately double Deepak Chem's existing production capacity for phenol and acetone.

- April 2024: KBR secured a technology licensing agreement with SABIC Fujian Petrochemicals for a 250,000 tonnes per annum phenol plant at the SABIC Fujian Petrochemical Complex in China, with construction beginning in 2024 and completion expected in FY2026. The project represents one of the largest phenol capacity expansions in Asia-Pacific and indicates ongoing investment in integrated petrochemical facilities.

Global Phenol Market Report Scope

Phenol belongs to the family of organic compounds characterized by a hydroxyl (OH) group attached to a carbon atom that is part of an aromatic ring. Phenols are widely used in household products and as intermediates for industrial synthesis. It is used as a disinfectant in household cleaners and mouthwash. The phenol market is segmented by product type and geography. By product type, the market is segmented into phenolic resins, caprolactum, bisphenol-A, and other product types. The report also covers the market size and forecasts for the methanol market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (kilo tons).

| Bisphenol-A |

| Phenolic Resins |

| Caprolactam |

| Others |

| Automotive |

| Construction |

| Pharmaceuticals |

| Furniture |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Bisphenol-A | |

| Phenolic Resins | ||

| Caprolactam | ||

| Others | ||

| By End-user Industry | Automotive | |

| Construction | ||

| Pharmaceuticals | ||

| Furniture | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected volume demand for phenol by 2031?

Global consumption is expected to reach 15.01 million tons by 2031, reflecting a 3.16% CAGR from 2026.

Which region will contribute the most incremental phenol demand through 2031?

Asia-Pacific, led by China and India, will supply the bulk of new demand due to integrated petrochemical expansions and downstream manufacturing growth.

How will Europe’s BPA food-contact ban affect phenol producers?

The regulation removes nearly 20% of regional BPA demand, compelling producers to redirect volumes to Asia or pivot toward non-food applications.

What role do bio-based routes play in future phenol supply?

Bio-propylene and lignin-derived phenolics could cut product carbon intensity up to 80%, and early adopters may secure price premiums as ESG standards tighten.

Page last updated on: