Cerebrospinal Fluid Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

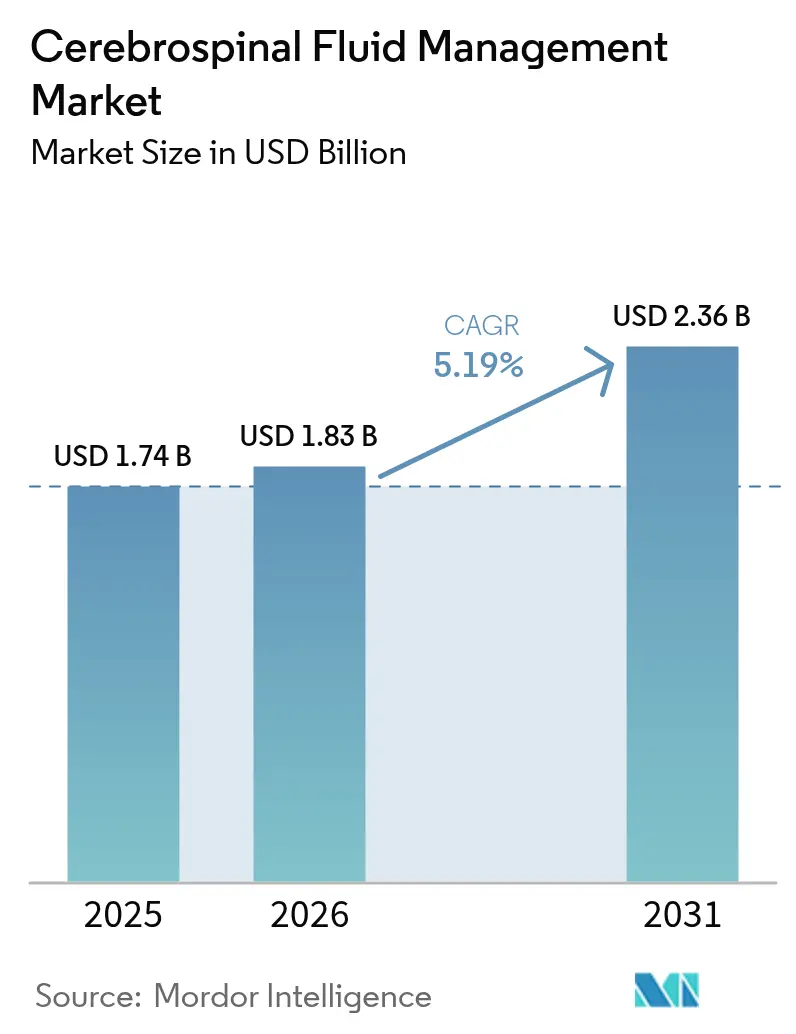

| Market Size (2026) | USD 1.83 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 5.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cerebrospinal Fluid Management Market Analysis by Mordor Intelligence

The Cerebrospinal Fluid Management Market size was valued at USD 1.74 billion in 2025 and estimated to grow from USD 1.83 billion in 2026 to reach USD 2.36 billion by 2031, at a CAGR of 5.19% during the forecast period (2026-2031).

Demographic aging in high-income economies, rapid uptake of smart programmable shunts, and growing recognition of normal pressure hydrocephalus are reinforcing demand. Hospitals remain the principal treatment venue, yet outpatient facilities are gaining traction as minimally invasive procedures shorten recovery times. Venture funding for endovascular shunt start-ups has accelerated, while FDA breakthrough designations are shortening time-to-market for novel implants. Supply chain fragilities for silicone and rare-earth magnets continue to create intermittent device shortages, motivating OEMs to dual-source components and redesign valves for material flexibility.

Key Report Takeaways

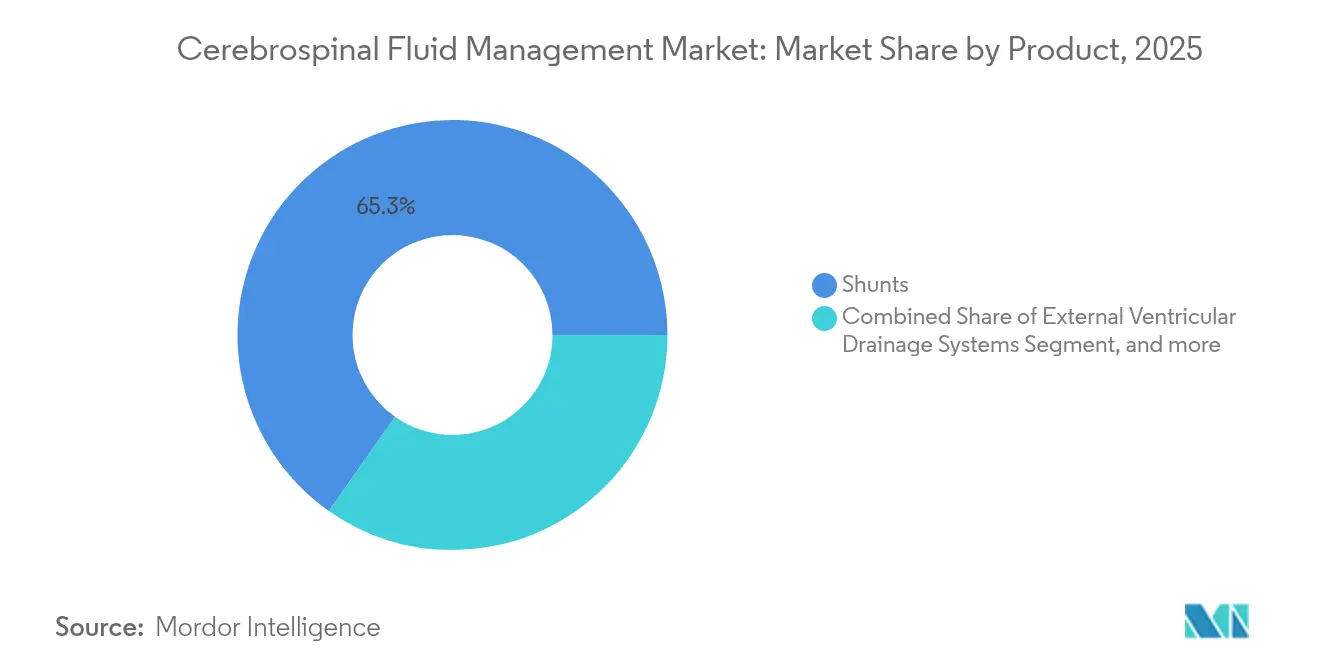

- By product category, shunts led with 65.25% revenue share in 2025; intracranial pressure monitoring devices are forecast to expand at a 6.78% CAGR to 2031.

- By patient age group, the pediatric segment held 51.20% of the cerebrospinal fluid management market share in 2025, while the geriatric segment is projected to post the fastest 7.36% CAGR through 2031.

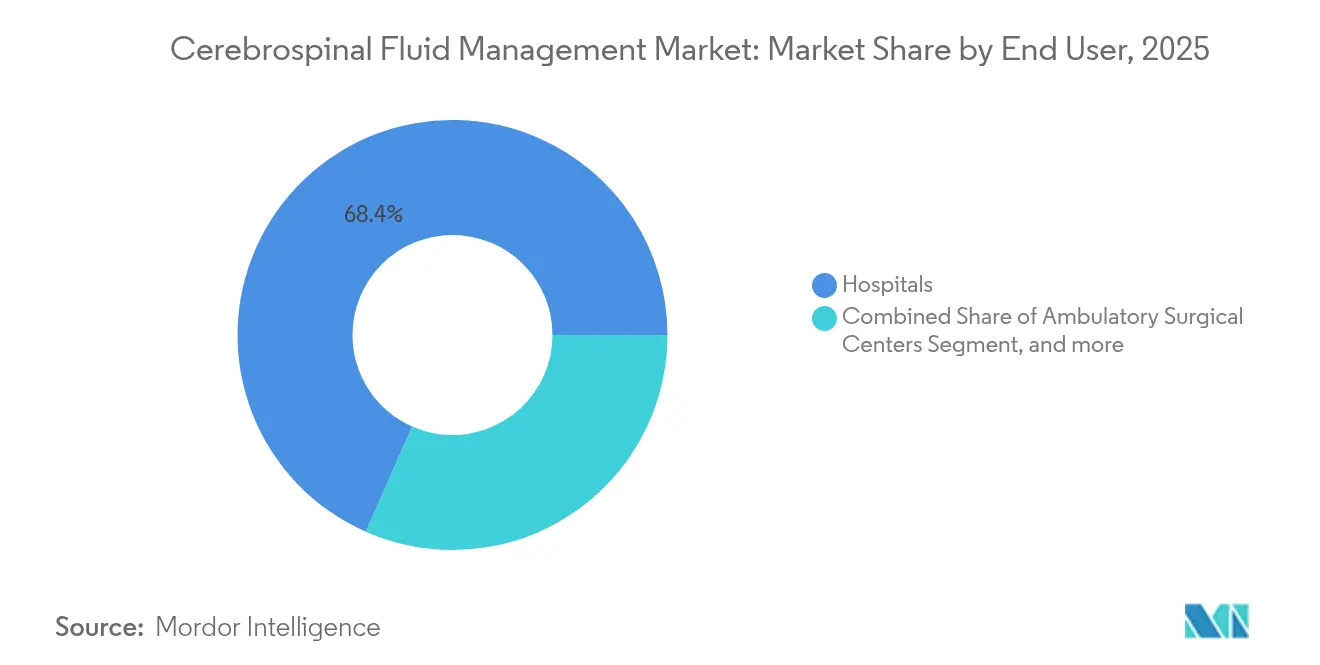

- By end user, hospitals captured 68.40% share of the cerebrospinal fluid management market size in 2025 and ambulatory surgical centers are advancing at an 7.79% CAGR to 2031.

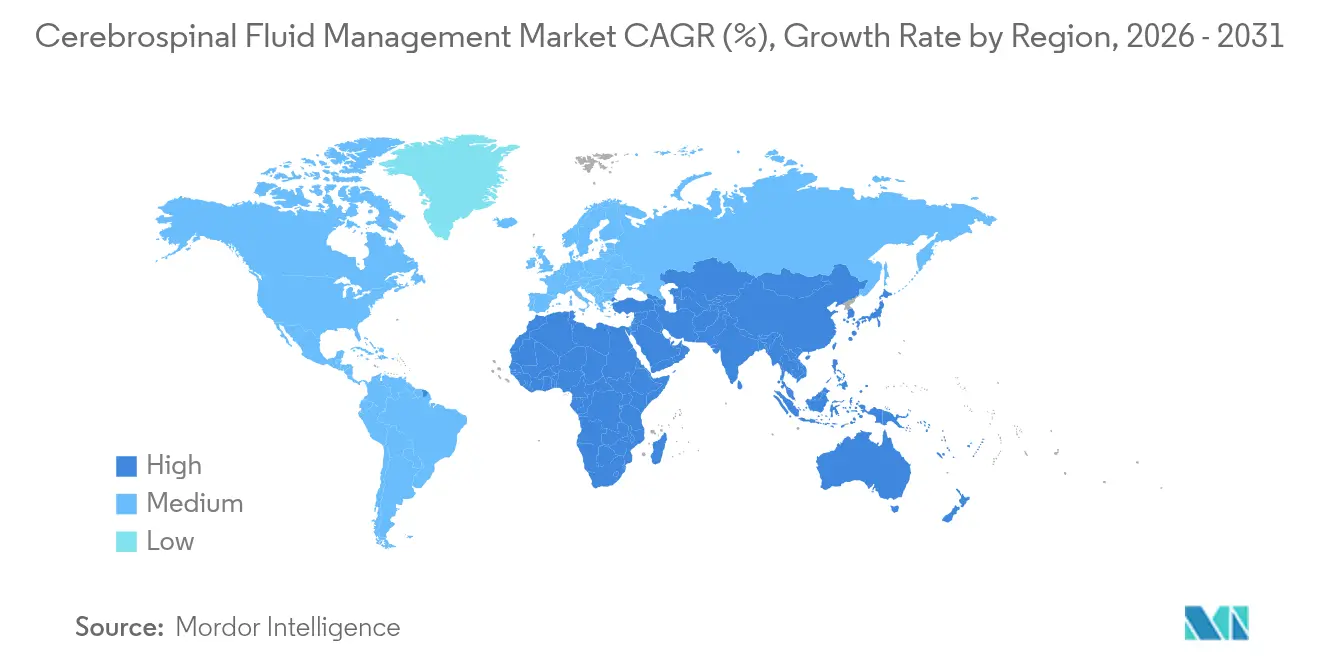

- By geography, North America accounted for 37.28% of revenue in 2025; Asia-Pacific is set to grow at a 7.02% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cerebrospinal Fluid Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing burden of hydrocephalus & intracranial hypertension | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Growing adoption of minimally invasive neuro-endoscopy & shuntless ETV/CPC | +0.8% | Global, early uptake in high-income countries | Short term (≤2 years) |

| Advances in smart programmable shunts with telemetric ICP monitoring | +1.0% | North America and Europe first, Asia-Pacific next | Medium term (2-4 years) |

| Rising geriatric population susceptible to normal pressure hydrocephalus | +1.4% | Global, most pronounced in developed economies | Long term (≥4 years) |

| Expanding reimbursement for CSF diversion in emerging markets | +0.6% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥4 years) |

| Emerging endovascular eShunt & ReFlow devices reducing revisions | +0.5% | North America and Europe, spreading worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Burden of Hydrocephalus & Intracranial Hypertension

Globally, normal pressure hydrocephalus affects 1.5% of people aged 70 years, underscoring a large pool of undiagnosed candidates for intervention. The disease now encompasses glymphatic dysregulation and venous outflow disturbances, pushing clinicians toward multimodal monitoring approaches. In low- and middle-income regions, post-infectious etiologies still account for 10.7% of pediatric cases, creating region-specific product demand.[1]Bradley K. Dlouhy, “ETV/CPC Outcomes in Pediatric Hydrocephalus,” Journal of Neurosurgery: Pediatrics, thejns.org Shunt infections cost a median USD 28,686 per episode, so payers increasingly endorse technologies that cut revision risk. Health systems have expanded screening and multidisciplinary clinics, yet unmet need remains significant, enabling steady expansion of the cerebrospinal fluid management market.

Growing Adoption of Minimally Invasive Neuro-Endoscopy & Shuntless ETV/CPC

Endoscopic third ventriculostomy with choroid plexus cauterization shows 76% 6-month success in multi-center cohorts. Infection rates drop markedly compared with shunting, and dependence on lifelong hardware is eliminated. In post-fetal myelomeningocele repair, ETV/CPC records 17% failure versus 86% for ventriculoperitoneal shunts, extending median time to failure to 17.5 months. Surgeons now leverage HD endoscopes and flexible instruments that broaden the eligible age window, though outcomes still hinge on operator training. With payers rewarding lower revision incidence, demand for endoscopic solutions is rising in the cerebrospinal fluid management market.

Advances in Smart Programmable Shunts with Telemetric ICP Monitoring

Telemetric systems such as the OSAKA telesensor reveal posture-dependent ICP shifts of nearly 20 mmHg, guiding immediate valve re-programming and lowering revision events.[2]Sunil H. Patel, “Intracranial Pressure Patterns With Telemetric Sensors,” Neurosurgery, academic.oup.com FDA breakthrough acknowledgement for the M.scio platform affirms U.S. regulatory support for remote pressure measurement. Gravitational valves like proGAV incorporate Active-Lock features that shield settings from external magnets. Coupled with IoT data pipelines and machine learning, these devices enable predictive maintenance schedules that aim to cut first-year failure from 30% to single digits. Adoption is climbing first in North America and Europe and is expected to accelerate Asia-Pacific growth in the cerebrospinal fluid management market.

Rising Geriatric Population Susceptible to Normal Pressure Hydrocephalus

Germany recorded a 48% jump in normal pressure hydrocephalus diagnoses, reaching 8.0 cases per 100,000 inhabitants. Population studies find a prevalence of 1.5% in 70-year-olds, with male predominance at 2.1%. Median survival after shunt placement stands at 8.82 years, creating durable follow-up demand for shunt adjustments. Specialized clinics and AI-assisted diagnostic panels now accelerate referral pathways, expanding the addressable base. The demographic surge underpins long-term growth in the cerebrospinal fluid management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High revision and failure rates of traditional shunt systems | -1.8% | Global, most acute in lower-resource centers | Short term (≤2 years) |

| Lack of neurosurgical capacity in low-income regions | -1.2% | Sub-Saharan Africa, South Asia, parts of Latin America | Long term (≥4 years) |

| Infection risk associated with external ventricular drainage | -0.7% | Global, higher where infection control is weak | Short term (≤2 years) |

| Supply-chain dependency on silicone and rare-earth magnets | -0.5% | Global, spikes during logistics disruptions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Revision and Failure Rates of Traditional Shunt Systems

Failure approaches 40% within 12 months, largely due to blockage, infection, or disconnection. One pediatric center reported 31.2% total failures, with revision shunts faring worse than initial procedures.[3]Adele H. Mini, “Shunt Failure Mechanisms in Children,” Child’s Nervous System, link.springer.com Each infection episode costs USD 28,686, and patients undergo an average of 10 lifetime revisions. Antibiotic-impregnated catheters now cut infection from 4.0% to 1.2%, yet mechanical occlusion persists as a dominant issue. ReFlow flushing catheters reduced revisions from 14 down to 1 over 4 years in early cohorts, offering partial relief.

Lack of Neurosurgical Capacity in Low-Income Regions

Africa averages one neurosurgeon per 2.2 million residents, far below the workforce needed for timely hydrocephalus care. Ethiopian data show surgeons clustered in referral hospitals, leaving vast rural zones underserved. Imaging, ICU beds, and sterile theatres are also scarce, compounding access barriers. Nigerian families wait a median of 14 weeks for surgery, with longer delays in lower socioeconomic groups. While low-cost shunts and task-sharing models are emerging, sustainable progress requires investment in training and infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Shunts dominate yet innovation pressure mounts

Shunts generated 65.25% of revenue in 2025, underscoring their entrenched role in cerebrospinal fluid diversion. Ventriculoperitoneal models lead volume demand, though adjustable valves are expanding quickest as clinicians prioritize non-surgical pressure tweaks. Intracranial pressure monitoring devices, growing at a 6.78% CAGR, are benefitting from bundled sales with programmable valves, thereby enlarging the overall cerebrospinal fluid management market. External ventricular drains continue as critical tools in trauma and post-infectious cases, supporting a steady accessories business for antibiotic-coated catheters.

Endovascular shunting concepts led by CereVasc aim to shorten hospital stays and enable outpatient implantation, but large-scale adoption hinges on pivotal trial outcomes. Accessories such as flushing adapters are creating preventive maintenance niches and could lengthen device lifecycles. The cerebrospinal fluid management market size for shunt consumables is expected to track the installed base, providing recurring revenue even as next-generation solutions emerge.

By Patient Age Group: Pediatric holds share, geriatric accelerates

Pediatric cases represented 51.20% of procedures in 2025 as congenital and post-infectious etiologies remained prevalent in low-income settings. The Endoscopic Third Ventriculostomy Success Score guides therapy choice, revealing reduced success under 3 months of age and shaping surgical timing. Meanwhile, the geriatric cohort is growing at 7.36% CAGR, buoyed by rising detection of normal pressure hydrocephalus and improved screening in memory clinics. Adult patients keep a stable share, associated chiefly with trauma and tumor sequelae.

Age impacts hardware selection. Children require growth-adaptable catheters, whereas seniors benefit from programmable and gravitational valves that offset posture changes. Early-life surgery before 40 weeks postconception predicts higher failure, influencing pediatric clinical pathways. Expansion of geriatric indications enlarges the cerebrospinal fluid management market and puts pressure on device makers to tailor products for fragile, multimorbid patients.

By End User: Hospitals command but ASCs gain momentum

Hospitals captured 68.40% of global revenue in 2025 thanks to ICU support, neuro-imaging access, and emergency care readiness. ASC share is growing rapidly at 7.79% CAGR, propelled by payer incentives and minimally invasive workflows. Outpatient pathways are feasible for ETV/CPC and endovascular shunts that average 1.3-day stays versus 3 days for conventional implants.

Specialty neurology clinics absorb diagnostic and follow-up volume, using telemedicine for programmable valve checks. COVID-19 catalyzed migration to lower acuity settings, and digital remote monitoring now underpins this shift. Sustained ASC growth will widen the cerebrospinal fluid management market size across decentralized care sites while hospitals continue handling high-risk revisions.

Geography Analysis

North America held 37.28% of 2025 revenue on the back of advanced reimbursement frameworks, dense neurosurgical networks, and early uptake of telemetric valves. The United States hosts multiple FDA breakthrough projects, accelerating introduction of next-generation implants and consolidating regional leadership in the cerebrospinal fluid management market. Canada benefits from universal coverage that funds shunt replacements but lags in AI diagnostic adoption.

Europe ranks second, with Germany exhibiting a 48% rise in normal pressure hydrocephalus diagnoses, signaling improved detection rather than incidence shift. National health systems finance programmable valves extensively, though procurement cycles favor multi-year tenders that can slow product refresh rates. United Kingdom centers are piloting outpatient ETV clinics, reinforcing the continent’s tilt toward minimally invasive care.

Asia-Pacific is the fastest-growing region at 7.02% CAGR, driven by China’s hospital expansion and Japan’s rapid aging. Post-infectious hydrocephalus still burdens South and South-East Asia, sustaining demand for low-cost ventriculoperitoneal shunts. Simultaneously, high-income subregions like South Korea procure telemetric valves, broadening the regional cerebrospinal fluid management market. Government capacity-building programs that sponsor fellowship training are gradually reducing surgeon shortages.

Latin America shows moderate progress as Brazilian tertiary centers adopt antibiotic catheters, yet heterogeneous reimbursement limits uniform technology diffusion. Middle East and Africa face acute workforce scarcity, with Central Africa averaging one neurosurgeon per 2.2 million people. International aid missions, public-private partnerships, and low-cost device innovations are vital to expand access. Collective efforts are expected to narrow the treatment gap and spur incremental market growth.

Competitive Landscape

The market is moderately consolidated. Medtronic, B. Braun, and Integra LifeSciences offer full portfolios encompassing programmable valves, gravitational add-ons, and ICP monitors, securing long-term supply contracts with university hospitals. B. Braun’s proGAV line incorporates Active-Lock magnets that resist unintended field exposure, differentiating the firm in the premium programmable segment.

Disruptive entrants are well funded. CereVasc raised USD 70 million in Series B financing in 2024 to advance its endovascular eShunt, targeting patients averse to craniotomy. Quantalx received FDA breakthrough status for Delphi-MD, an AI algorithm predicting shunt responsiveness, underscoring digital diagnostics as a new contest arena. Luciole Medical’s acquisition of Spiegelberg adds pressure sensors and advanced monitoring catheters to its cerebral oximetry line, positioning the firm as an integrated brain monitoring supplier.

Strategic alliances are proliferating. Device manufacturers partner with telehealth platforms to deliver remote valve checkups, while contract manufacturers explore silicone-free catheter materials to mitigate supply shocks. The FDA’s clear Class II pathway under 21 CFR 882.5550 encourages mid-sized OEMs to enter the cerebrospinal fluid management market with niche innovations. Overall rivalry centers on lowering revision rates, minimizing invasiveness, and embedding data connectivity.

Cerebrospinal Fluid Management Industry Leaders

Medtronic

Integra LifeSciences Holdings Corp.

Natus Medical Inc.

Sophysa SA

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is forming around technologies and care pathways that directly target the market's biggest cost and outcome pain points: shunt revisions, infections, and long follow-up cycles. With shunt failure approaching 40% within 12 months in traditional systems and infections carrying high per-episode treatment costs, device makers have room to expand portfolios that pair programmable valves and gravitational elements with integrated or paired intracranial pressure (ICP) monitoring. This approach supports non-invasive adjustments and earlier intervention.

Demand is also widening beyond acute inpatient episodes as ambulatory surgical centers gain traction for minimally invasive approaches. That shift creates opportunities for simplified implant workflows and service models that support remote valve checks and longitudinal monitoring. In the United States, regulatory and product refresh cadence provides a workable entry and iteration path for adjacent players and niche innovators, as CSF shunts and components under 21 CFR 882.5550 continue to see 510(k) clearances without mandatory clinical trials for substantial equivalence submissions. Recent FDA 510(k) clearances for neurology devices that touch CSF drainage and shunt-adjacent categories (including Sophysa external CSF drainage catheters in June 2025, Phasor Health EVAC in June 2025, and Brainspace Intellidrop in December 2025) indicate active commercialization and ongoing replacement cycles across external drainage and monitoring-related workflows. OEMs are also pursuing MRI-stable and programmable architectures (for example, Sophysa Polaris valve positioning) and tighter linkage between pressure sensors and clinical decision support. At the same time, supply-chain fragility in silicone and rare-earth magnets keeps material flexibility and dual-sourcing as tangible levers for reliable fulfillment.

Recent Industry Developments

- June 2026: Medtronic participated in an USD 85 million Series C financing round for CereVasc, which is developing an endovascular approach to treat cerebrospinal fluid buildup. The investment highlights strategic interest in less invasive CSF diversion concepts that could shift the procedure mix and reduce dependence on conventional open shunt placements.

- December 2025: Brainspace, Inc. received FDA 510(k) clearance (K251598) for Intellidrop as a Class II neurology device. The clearance enables new product availability in CSF management-adjacent monitoring and workflow tooling, supporting ongoing refresh cycles in hospital and neurocritical care purchasing.

- May 2024: CereVasc secured USD 70 million in Series B funding to advance its eShunt technology for cerebrospinal fluid management. The funding accelerated development of endovascular shunting approaches and increased competitive pressure on legacy shunt portfolios focused on revision reduction and minimally invasive care pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers medical devices and related disposable items used to drain, divert, or monitor cerebrospinal fluid in clinical care, mainly in neurosurgery and neurocritical settings. The sizing is value based and reflects device sales used across key care sites.

Scope exclusions: We exclude pharmaceuticals, general neurosurgical instruments not specific to CSF handling, and broader ICU fluid drainage products that do not manage CSF.

Segmentation Overview

- By Product

- Shunts

- By Valve

- Adjustable Valve Shunts

- Monopressure / Fixed Valve Shunts

- By Type

- Ventriculoperitoneal (VP) Shunts

- Ventriculoatrial (VA) Shunts

- Lumboperitoneal (LP) Shunts

- Ventriculopleural (VPL) Shunts

- By Valve

- External Ventricular Drainage (EVD) Systems

- Intracranial Pressure (ICP) Monitoring Devices

- Accessories & Consumables

- Shunts

- By Patient Age Group

- Pediatric (0-17 yrs)

- Adult (18-64 yrs)

- Geriatric (65+ yrs)

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics & Neurology Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting model structure and to keep assumptions anchored to real procedure and care patterns. We reviewed public healthcare statistics and surveillance sources such as CDC datasets, WHO health statistics, OECD health indicators, and national health ministry publications, then cross-checked CSF device context using FDA device databases and PubMed-indexed clinical literature.

To translate clinical demand into market value, we also used company filings, investor presentations, reputable press, and association websites to understand product mix and adoption trends across hospital settings. In a few places, paid subscriptions for company financials and patent databases were used to confirm product pipelines and to avoid double counting when brands change ownership. The desk sources listed above are illustrative, and we used additional public references to support data collection, validation, and assumption clarification.

Primary Interviews and Surveys

Primary input was used to validate procedure drivers and how product selection shifts by care setting, in particular between shunts, external ventricular drainage, ICP monitoring, and related consumables. We spoke with a mix of clinical and commercial stakeholders across major regions so utilization, replacement behavior, and pricing logic could be stress-tested, then adjusted where desk inputs were not specific enough to the local pathway.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 13% | APAC: 45% |

| Mid tier: 46% | Functional/Unit leaders: 38% | EMEA: 35% |

| Smaller Players: 15% | Managers: 49% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where procedure volumes and treated patient pools are reconstructed by region, then mapped to typical device usage per case for CSF diversion, drainage, and monitoring. Since reporting quality varies across countries, the model is anchored on signals that are generally trackable, such as hydrocephalus and neurotrauma burden, neurosurgical capacity, ICU admission trends for severe neurologic events, and the mix of shunt versus temporary drainage approaches.

Those demand pools are converted to value using blended ASP bands by device class, together with the expected share of accessories and consumables that move with placements and revisions. We corroborate totals using selective bottom-up checks, including sampled supplier revenue ranges, channel feedback on unit shipments, and spot checks on typical hospital tender pricing. Where direct data gaps exist, we use proxy markets with similar care pathways, then refine through expert review.

For forecasting, scenario analysis is used to carry forward the variables above, since procedure growth, revision rates, and reimbursement pressure do not follow a straight line year to year. Assumptions around pricing progression and mix shifts were stress-tested with interview inputs, and the final curve was kept consistent with observable adoption patterns for adjustable valves, infection prevention protocols, and ICU monitoring practices.

Data Validation & Update Cycle

Validation is done through stepwise checks so that no single weak input distorts the final number. Our team compares outputs against independent signals like procedure trends, import-export direction for relevant device categories where available, and public financial commentary on neurosurgical portfolios, then investigates large variances before sign-off.

When an anomaly is identified, we rework the underlying assumptions and, if needed, run a follow-up discussion with a relevant respondent group to confirm the change. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory actions, reimbursement changes, or supply disruptions. Before delivery, we conduct a final review pass so clients get the most current view based on the latest available inputs.

Mordor Intelligence's Cerebrospinal Fluid Management Market Sizing Compared With Other Published Estimates

Different published market sizes for CSF management can vary even when they use similar product labels, because the included device classes and the timing of the base year are not always aligned. The gap tends to widen when a study blends adjacent neuro device categories into one total or uses different currency conversion timing for multinational sales.

A second source of differences comes from how pricing and volume are built. Some estimates rely more heavily on list prices or assume uniform usage per procedure across regions, but in practice ASP bands change with hospital purchasing, revision rates vary by patient group, and accessories can be counted either as part of system value or only when sold separately, which moves the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.74 B (2025) | |

| Global Publisher A | USD 1.93 B (2025) | Uses a broader device basket and can blend in adjacent neurology device revenue, and it is less clear if accessories and consumables are counted as recurring sales or bundled into system value throughout the series. |

| Market Platform B | USD 0.86 B (2025) | Appears to focus mainly on shunts and external drainage, and it can understate value if ICP monitoring devices and higher-priced shunt variants are not fully included in the same scope. |

The table indicates that the spread is largely explained by what gets counted as CSF-specific device revenue and how recurring consumables are treated. By keeping ICP monitoring and CSF accessories in-scope only when they are used for CSF pathway management, then rechecking the implied procedure-to-unit ratios in interviews, the final total stays traceable to clinical demand signals. This modeling choice is applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current size of the cerebrospinal fluid management market?

The market stands at USD 1.83 billion in 2026 and is on track to reach USD 2.36 billion by 2031.

Which product segment is growing the fastest?

Intracranial pressure monitoring devices are projected to advance at a 6.78% CAGR through 2031, outpacing other categories.

How significant is the pediatric patient population?

Children aged 0-17 years account for 51.20% of total procedures, underscoring the segment’s ongoing importance despite growth in geriatric cases.

Why are ambulatory surgical centers gaining share?

Minimally invasive techniques and shorter recovery periods permit suitable patients to undergo treatment in lower-cost outpatient settings, driving an 7.79% CAGR for ASCs.

What technological trends are shaping future growth?

Smart programmable valves with telemetric monitoring, AI-based diagnostic algorithms, and endovascular shunt systems are set to reduce revision rates and expand patient candidacy.

Which region offers the highest growth potential?

Asia-Pacific leads with a forecast 7.02% CAGR due to strengthening healthcare infrastructure and rising awareness of hydrocephalus therapies.

Page last updated on: