Fluid Management Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

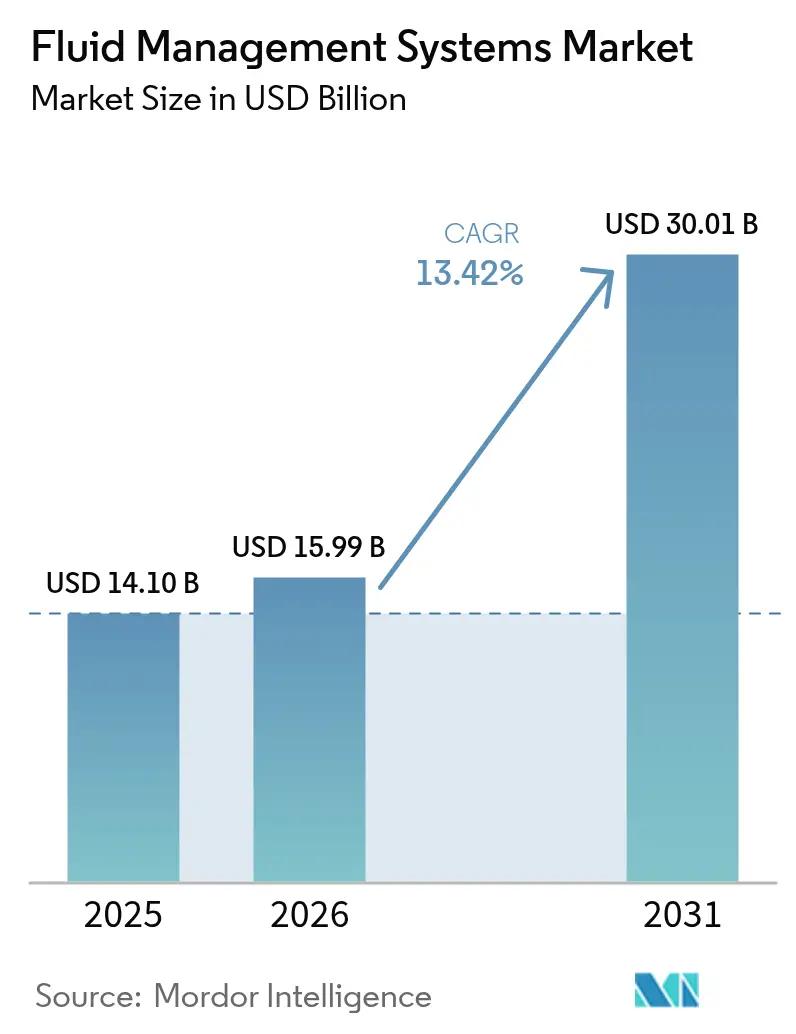

| Market Size (2026) | USD 15.99 Billion |

| Market Size (2031) | USD 30.01 Billion |

| Growth Rate (2026 - 2031) | 13.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fluid Management Systems Market Analysis by Mordor Intelligence

The Fluid Management Systems Market size is expected to grow from USD 14.10 billion in 2025 to USD 15.99 billion in 2026 and is forecast to reach USD 30.01 billion by 2031 at 13.42% CAGR over 2026-2031.

Rapid growth stems from rising minimally invasive surgery volumes, the increasing prevalence of chronic kidney disease, and accelerating adoption of AI-enabled closed-loop ultrafiltration platforms. Hospitals remain the primary purchasers, but home-care adoption is growing fast as portable dialysis devices enable in-home therapies. Competitive dynamics are intensifying as leading vendors bundle hardware, software, and analytics to deliver end-to-end solutions, yet shortages of surgeon talent and supply constraints on medical-grade polymers could temper near-term gains.

Key Report Takeaways

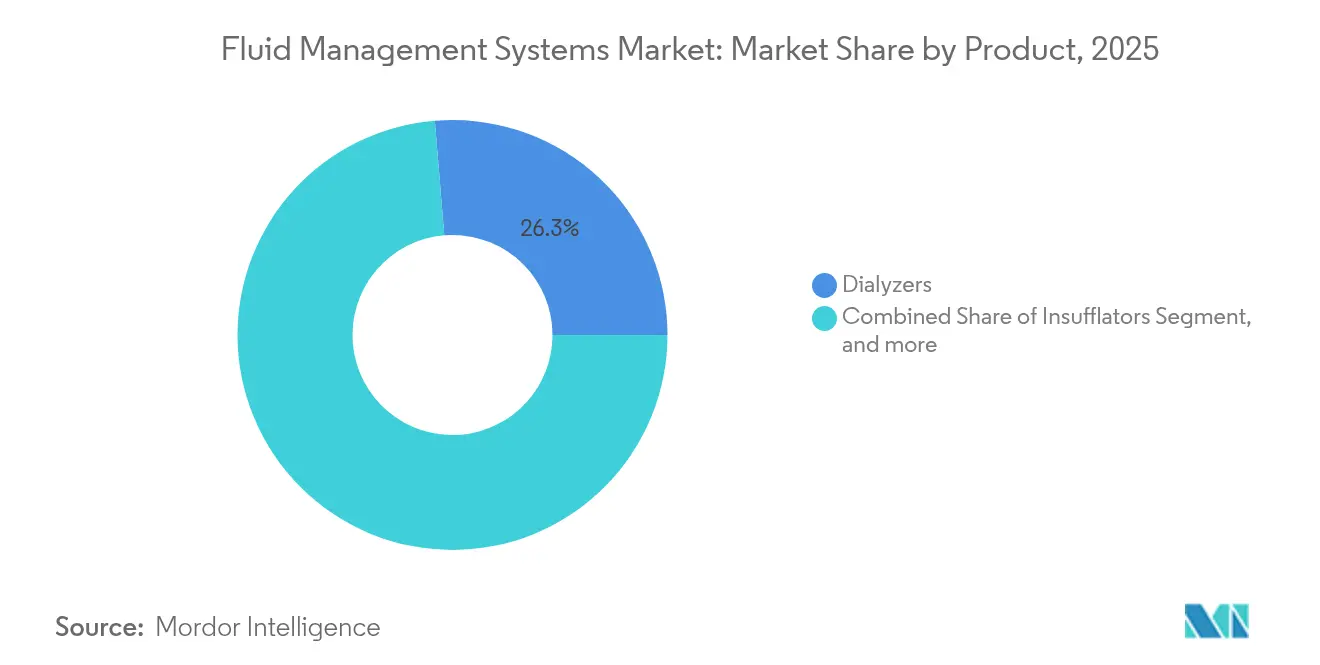

- By product, dialyzers led with 26.31% of fluid management systems market share in 2025; fluid-waste management systems are forecast to grow at a 14.09% CAGR to 2031.

- By disposables, catheters accounted for 33.02% of the fluid management systems market size in 2025, while valves are advancing at a 16.55% CAGR through 2031.

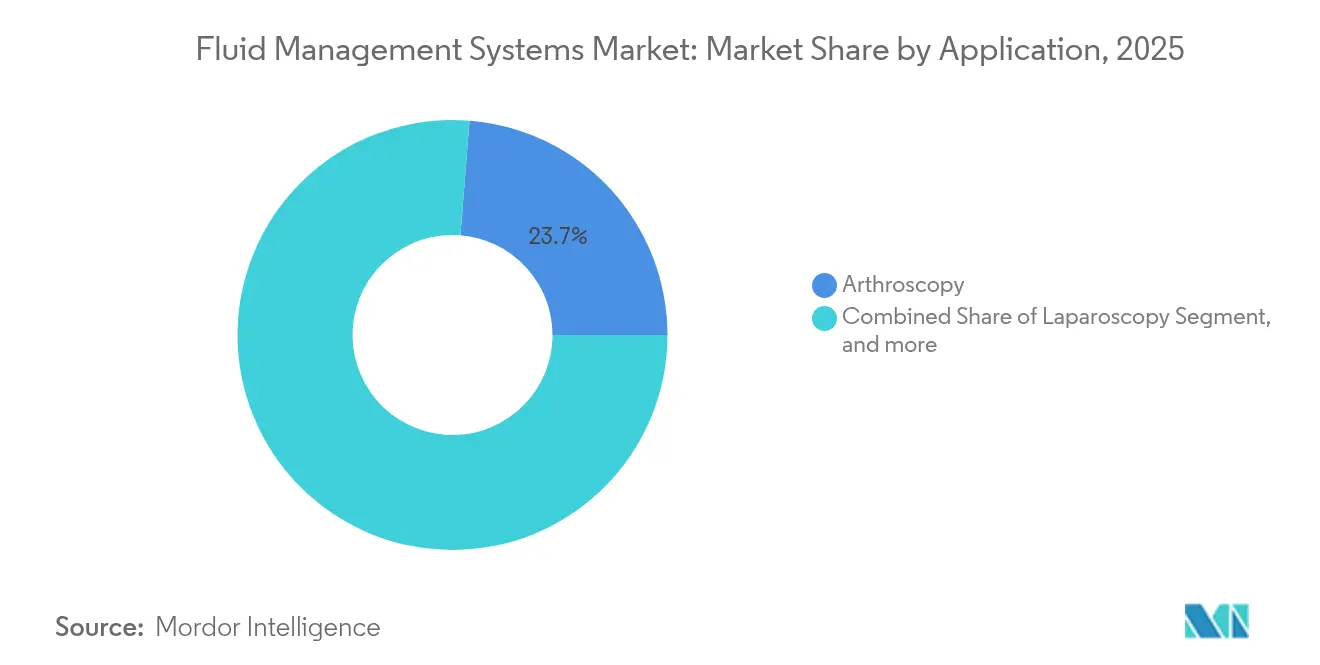

- By application, arthroscopy captured 23.74% share of the fluid management systems market size in 2025; laparoscopy is projected to expand at a 18.61% CAGR between 2026-2031.

- By end user, hospitals held 55.12% of the fluid management systems market share in 2025, whereas home-care settings are growing at a 14.54% CAGR to 2031.

- By geography, North America controlled 41.12% revenue in 2025; Asia-Pacific is the fastest riser with a 14.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fluid Management Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in minimally invasive surgery volumes | +2.1% | Global, led by North America & EU | Medium term (2-4 years) |

| Growing prevalence of chronic kidney disease & ESRD | +2.8% | Global, APAC highest growth | Long term (≥ 4 years) |

| AI-enabled closed-loop ultrafiltration control adoption | +1.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Integrated fluid-waste & disposable insufflation systems | +1.4% | Global, regulatory push in EU & North America | Short term (≤ 2 years) |

| Shift toward portable home-dialysis fluid platforms | +2.3% | North America leading | Long term (≥ 4 years) |

| Regulatory push on OR fluid-waste compliance | +1.2% | EU & North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in Minimally-Invasive Surgery Volumes

Minimally invasive procedures now dominate many orthopedic and general surgery service lines, increasing demand for irrigation, suction, and insufflation technologies that can maintain clear visibility and stable cavity pressure.[1]Stryker Corporation, “SurgiCount+ System Press Release,” stryker.com Ambulatory surgery centers are standardizing purchasing agreements with med-tech vendors to secure integrated fluid management platforms that streamline workflow and documentation. AI-enhanced devices are further optimizing flow parameters and reducing blood-loss variability. Together, these shifts are enlarging the installed base of high-specification systems in both hospitals and outpatient facilities.

Growing Prevalence of Chronic Kidney Disease & ESRD

Chronic kidney disease affects more than 850 million people worldwide, pushing dialysis procedure volumes higher and requiring new dialyzer membranes with needle-free connectors and bi-directional data feeds.[2]Fresenius Medical Care, “Annual Report 2024,” freseniusmedicalcare.com Hemodiafiltration rollouts in the United States during 2025 promise better toxin clearance, while closed-loop feedback controls have lowered intradialytic hypotension events in 23 of 28 clinical trials. These advancements underpin sustained unit demand for dialysis-specific fluid management platforms across clinics and home settings.

AI-Enabled Closed-Loop Ultrafiltration Control Adoption

Machine-learning algorithms embedded in pumps are predicting hypotension up to 15 minutes before onset and auto-adjusting flow rates, helping clinicians keep relative blood volume within safe ranges 63% of the time during pilot studies.[3]Oxford Academic Journals, “Pilot Study on Ultrafiltration Feedback Control,” academic.oup.com Vendors such as BD now combine hemodynamic monitoring with predictive software to reduce clinician workload and improve consistency in large-scale programs.

Integrated Fluid-Waste & Disposable Insufflation Systems

Regulators are tightening rules on operating-room waste capture, pushing hospitals to invest in platforms that merge delivery, collection, and disposal functions within a single closed loop. B. Braun’s DUPLEX drug-delivery technology trims drug-prep time and medication errors while meeting DEHP-free mandates. Such systems help providers hit environmental, safety, and efficiency targets simultaneously.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of endoscopy-trained surgeons | -1.8% | Global, rural areas hardest hit | Long term (≥ 4 years) |

| High capital cost of integrated platforms | -1.4% | Emerging markets, some developed sites | Medium term (2-4 years) |

| Single-use-plastic legislation inflating consumable costs | -1.1% | EU & North America | Short term (≤ 2 years) |

| Volatile supply of medical-grade polymers & resins | -1.3% | Global, APAC supply nodes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Endoscopy-Trained Surgeons

An 18% decline in surgical specialists projected by 2028 is delaying procedure backlogs in many regions. Rural hospitals find it hardest to recruit talent, limiting deployment of advanced endoscopic fluid systems and depressing utilization rates. Rural areas are disproportionately affected by surgeon shortages, limiting access to advanced fluid management technologies and creating geographic disparities in care delivery. The complexity of modern fluid management systems requires specialized training that may not be readily available in all healthcare settings, potentially limiting adoption rates despite technological advancement.

High Capital Cost of Integrated Platforms

State-of-the-art fluid management suites can cost USD 0.5-1.2 million per operating room, a hurdle for lower-tier facilities whose capital budgets are already pressured by inflation and competing IT upgrades. Financing innovations and pay-per-use models are emerging to soften the blow, yet adoption still lags in several emerging economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Dialyzers Sustain Leadership

Dialyzers generated 26.31% of 2025 revenue, reflecting the indispensable nature of renal replacement therapy within the broader fluid management systems market. Fresenius Medical Care posted EUR 21.5 billion in 2024 revenue, confirming the resilience of its dialyzer line. Fluid-waste management systems are set to rise at a 14.09% CAGR to 2031, propelled by stricter disposal mandates. Insufflators, suction units, and fluid warmers register steady gains as providers equip minimally invasive theaters with temperature-controlled, smoke-evacuation-ready kits that meet modern safety codes.

The long-tail “other products” bucket comprising AI sensors, cloud dashboards, and modular hubs could shift share toward software-centric vendors if predictive algorithms deliver measurable cost savings. Segment margins vary widely: dialyzer consumables enjoy high recurring revenue, whereas capital-intensive consoles face lengthier replacement cycles, underscoring distinct strategic imperatives within each sub-market.

By Disposables & Accessories: Catheters Dominate Usage

Catheters accounted for 33.02% of 2025 revenues in this category, reflecting universal application in vascular access, irrigation, and drainage across settings. LSI materials, antimicrobial coatings, and kink-resistant geometries differentiate premium SKUs and support hospitals’ infection-control targets. Valves headline future growth with a 16.55% CAGR, mirroring rising demand for automated shut-off and anti-reflux designs that pair seamlessly with smart pumps. Tubing sets and bloodlines represent high-volume staples, but value migration is underway toward integrated kits that bundle pressure sensors and RFID tracking.

Resin price spikes create margin volatility, prompting OEMs to dual-source polymers and redesign packaging to cut plastic weight. As EU legislation ratchets up recyclability thresholds, suppliers that calibrate formulations early could lock in multi-year supply contracts and solidify share positions within the fluid management systems market.

By Application: Arthroscopy Holds Share, Laparoscopy Accelerates

Arthroscopy procedures led with 23.74% revenue share in 2025 and remain core to orthopedic service lines. Visualization fidelity hinges on pristine irrigation control, spurring upgrades to pumps that automatically balance inflow and outflow pressures. Laparoscopy is the fastest-growing application, posting a 18.61% CAGR forecast as bariatric, colorectal, and gynecologic programs expand. Neurology and urology applications also climb as precision irrigation and suction become integral to tumor resection and stone management.

Cardiology relies on high-shear blood pumps and heparinized lines, while dental and gastroenterology segments adopt compact suction-irrigation modules that integrate with standard chairs and scopes. Vendors able to cross-bundle hardware with single-use packs stand to capture incremental procedure volume across diverse specialties within the fluid management systems market size hierarchy.

By End User: Hospitals Remain Primary Buyers

Hospitals capture 55.12% of 2025 expenditure, driven by large theater counts and critical-care units that require multifunction systems. Yet the fastest growth comes from home-care settings, expanding at 14.54% CAGR through 2031 as compact hemodialysis and peritoneal dialysis devices become wearable and connected.

Dialysis centers maintain steady market presence through their specialized focus on renal replacement therapy, with growth driven by increasing chronic kidney disease prevalence and technological advancement in dialysis equipment. Specialty clinics represent a growing segment as healthcare delivery shifts toward specialized care models that require dedicated fluid management systems tailored to specific procedures and patient populations.

Geography Analysis

North America produced 41.12% of 2025 revenues, lifted by robust reimbursement and early adoption of AI monitors. Boston Scientific’s USD 4.663 billion Q1 2025 sales underline the region’s appetite for high-end cardiovascular solutions that rely on precise perfusion control. FDA rule harmonization is expected to streamline multi-site rollouts, though looming surgical workforce shortages could temper growth.

Asia-Pacific is the engine of expansion, advancing at a 14.6% CAGR. China is scaling tertiary hospitals, while India channels public funding into dialysis clinics. Regulatory diversity requires tailored market-access pathways, yet overall device approvals are accelerating as agencies modernize frameworks.

Europe balances maturity with sustainability imperatives. EU directives on post-market surveillance and recyclable packaging are reshaping component design, favoring manufacturers that can verify cradle-to-grave compliance. Meanwhile, decentralization policies in Germany and France bolster outpatient procedure volumes that depend on mobile fluid equipment.

Middle East & Africa and South America trail in absolute size but offer double-digit growth pockets where infrastructure projects align with rising non-communicable disease burdens. Currency fluctuations and import tariffs remain headwinds, pushing suppliers toward local assembly and strategic distributor alliances to penetrate these segments of the fluid management systems market.

Regulatory Landscape

Regulation for fluid management systems is anchored in medical-device quality management and risk-based controls for sterile fluid pathways, including pressure and temperature monitoring, as well as post-market obligations. A major inflection point is the US FDA Quality Management System Regulation (QMSR), implemented on February 2, 2026, which amends 21 CFR Part 820 by incorporating ISO 13485:2016 by reference, tightening harmonized expectations for design controls, process validation, and supplier management across globalized supply chains.

On product-specific pathways, core categories such as hemodialysis delivery systems fall under defined FDA device classifications with 510(k) requirements tied to materials and performance parameters, reinforcing the need for verification and validation across disposables and consoles. In parallel, EU Medical Device Regulation (EU MDR 2017/745) compliance continues to shape technical documentation and lifecycle surveillance, while single-use disposables face added scrutiny from sustainability and plastics-related policies that can increase compliance and packaging redesign burdens for catheters, tubing, and sterile sets.

Competitive Landscape

The fluid management systems market features moderate fragmentation. Baxter, Medtronic, Fresenius Medical Care, and Johnson & Johnson occupy top tiers, leveraging deep R&D budgets to embed analytics within pumps and consoles. Baxter’s Novum IQ pump, cleared in 2024, integrates bidirectional EMR connectivity to reduce manual charting while enhancing dose accuracy. Medtronic recorded USD 33.5 billion FY25 revenue, with cardiovascular equipment up 6.6%, reflecting sustained demand for hemodynamic guidance.

Strategic M&A accelerates portfolio breadth. BD’s pending USD 4.2 billion purchase of Edwards Lifesciences’ Critical Care unit signals consolidation around data-rich monitoring assets. Teleflex’s EUR 760 million BIOTRONIK buy sharpens its vascular access lineup and captures synergy with existing catheter franchises.

Emerging competitors focus on home-dialysis wearables and AI decision-support layers. Breakthrough-device designation for a heparin-free dialysis circuit positions Fresenius to disrupt anticoagulation protocols and widen its moat against new entrants. Nevertheless, polymer shortages and single-use-plastic surcharges squeeze gross margins, pushing producers to invest in material science and dual sourcing.

Fluid Management Systems Industry Leaders

Baxter International Inc.

Smith & Nephew plc

Stryker Corporation

B. Braun Melsungen AG

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Early indicators point to a shift toward indication-specific control and monitoring in fluid management. In urology, the March 2026 FDA 510(k) clearance for the Asurys Fluid Management System, designed for intrarenal pressure management during endoscopic procedures, supports a premium segment for pressure-aware platforms that standardize documentation in high-throughput settings. Pediatric and specialty-care clearances are also extending use cases for warming and infusion hardware, including the February 2026 FDA clearance for pediatric use of the TSC Lifes Fluido Compact Fluid Warming System in the US and Canada.

MDR-ready evidence and interoperability standards are influencing rollout strategies for pumps, warmers, and disposable infusion ecosystems. The April 2026 CE marking for SQ Innovations Lasix ONYU infusor reinforces MDR readiness and lifecycle surveillance requirements for these systems.

Recent Industry Developments

- July 2026: Otsuka ICU Medical LLC announced a USD 500 million expansion of IV solutions manufacturing in North America, including a new 500,000-square-foot facility in Austin, Texas. The investment targets supply-chain resilience for high-volume IV fluids and supports a shift toward non-DEHP innovation, which can affect availability and compliance positioning for downstream fluid management workflows.

- April 2026: SQ Innovations Lasix ONYU infusor received CE marking under EU MDR. The approval reflects MDR-ready clinical evidence, interoperability standards for infusion sets, and lifecycle surveillance capabilities that support global deployment strategies.

- March 2026: Boston Scientific earned FDA 510(k) clearance for the Asurys Fluid Management System. The clearance expands options for intrarenal pressure management during endoscopic procedures and enables more standardized peri-procedural fluid handling workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers medical fluid management equipment and related disposables that help circulate, warm, irrigate, suction, and safely collect or dispose of physiological fluids during diagnostic and surgical procedures.

Scope exclusions: Industrial fluid power equipment and general-purpose non-medical fluid transfer components are excluded from this sizing.

Segmentation Overview

- By Product

- Dialyzers

- Insufflators

- Suction & Irrigation Systems

- Fluid-Warming Devices

- Fluid-Waste Management

- Other Products

- By Disposables & Accessories

- Catheters

- Bloodlines

- Transducers

- Valves

- Tubing Sets

- Other Disposables

- By Application

- Arthroscopy

- Laparoscopy

- Neurology

- Cardiology

- Urology

- Dental

- Gastroenterology

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Dialysis Centers

- Specialty Clinics

- Home-Care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping where demand comes from and which procedures typically use these systems, then checking how that demand appears in public data series. We used sources such as the World Health Organization, the World Bank, and OECD health statistics to understand procedure capacity signals, care access, and spending direction by region.

We also reviewed sources such as the US FDA databases (clearances, recalls, safety notices) and other regulator pages where available to sense product cycles and risk events that can shift adoption. Supporting reads included peer-reviewed clinical journals on procedure volumes and usage patterns, medical society or association publications, and company annual reports and investor presentations to understand product mix and geographic exposure. When the model needed numeric grounding, we used paid subscriptions for company financial intelligence, news and financials tracking, and patent databases to confirm timelines and cross-check claims. These examples are not exhaustive, and many other public and paid sources were also used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work was used to pressure-test the model with people who see pricing and adoption in real time, including manufacturers, distributors, hospital procurement staff, and clinicians involved in high fluid-use procedures. Because this is a global market, we ensured coverage across APAC, EMEA, and the Americas so regional procedure mix, reimbursement comfort, and product preferences could be reflected in the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 43% |

| Mid tier: 48% | Functional/Unit leaders: 32% | EMEA: 34% |

| Smaller Players: 15% | Managers: 54% | Americas: 23% |

Market-Sizing & Forecasting

Sizing begins from the demand pool, where procedure activity and care delivery capacity are used to reconstruct addressable consumption of fluid management systems and their associated consumables. We then translate those activity signals into revenue by applying region-appropriate adoption and replacement assumptions, followed by average selling price ranges that were verified through interview inputs.

To keep the model practical, a limited set of market fingerprints was used, such as the volume trend of endoscopy and arthroscopy, dialysis utilization, operating room throughput, installed base replacement timing for key equipment, and disposables consumption per procedure (which changes with protocol and case complexity). When the market is corroborated, selective bottom-up approximations are applied, such as sampled ASP times volume checks by region and channel, plus supplier revenue exposure checks, which help adjust totals where reporting lines are mixed or bundled.

For forecasting, scenario analysis is applied around procedure growth, pricing progression, and mix shift toward single-use disposables, and those scenarios are filtered through expert consensus gathered in primary calls. Where gaps exist in smaller countries or niche procedure areas, the missing values are estimated using proxy indicators like hospital capacity expansion and regional procedure mix, and then rechecked against nearby comparable markets before being accepted.

Data Validation & Update Cycle

Validation is handled through cross-checks that look for mismatches between the model output and independent signals such as procedure momentum, regulatory activity, and reported business exposure by geography. If large variances show up, the assumptions are revisited, and follow-up outreach is triggered to confirm whether the issue is scope, timing, or pricing, and then the model is corrected.

Before sign-off, the work is reviewed in steps so that calculation logic, unit consistency, and currency treatment are aligned across regions. Reports are refreshed annually, and interim updates are done when a material event shifts adoption, pricing, or supply. Right before delivery, a final freshness pass is completed so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's Global Fluid Management Systems Market Market Sizing Compared With Other Published Estimates

Published market values for fluid management systems can look far apart, even when the topic name sounds identical, because the scope boundary and the year used for sizing are not always treated the same way. Differences also come from how firms treat disposables versus equipment, and whether procedure-linked demand signals are used to keep the totals realistic.

Procedure coverage signals like dialysis, endoscopy, arthroscopy, and other fluid-intensive care settings are the checks that keep Mordor Intelligence's estimate aligned to medical fluid handling and disposal use cases, instead of drifting into industrial fluid transfer revenues. When other sources blend adjacent device categories, apply aggressive or conservative price paths without re-checking interview ranges, or use older currency conversion timing, the reported total can move meaningfully even if the headline forecast period looks similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.99 B (2026) | |

| Global Consultancy A | USD 11.65 B (2025) | Uses an earlier base year and a narrower counted value pool in some narratives, which can understate equipment plus disposables that are tied to procedure throughput in later years. |

| Industry Publisher B | USD 8.92 B (2024) | Likely reflects a different market boundary and timing, where parts of the disposable workflow or certain procedure settings may be treated inconsistently, and currency year alignment can compress the headline number. |

The spread in the table is mainly explained by scope and timing choices that shift what is counted and in which year it is valued. By tying revenue build-up to procedure demand signals and then validating ASP and adoption ranges through interviews, the model produces a practical midpoint that can be repeated and audited with clear inputs.

Key Questions Answered in the Report

What is the current size of the fluid management systems market?

The market was valued at USD 15.99 billion in 2026 and is projected to reach USD 30.01 billion by 2031, reflecting a 13.42% CAGR over 2026-2031.

Which region leads global sales?

North America generated 41.12% of 2025 revenue owing to advanced infrastructure and early AI adoption.

What segment represents the largest product share?

Dialyzers held 26.31% of 2025 revenue, driven by the high incidence of chronic kidney disease.

Where is the fastest growth expected?

Asia-Pacific is forecast to expand at a 14.6% CAGR through 2031 as healthcare spending and procedure volumes rise.

Why are home-care settings gaining importance?

Portable dialysis and remote monitoring technologies support self-care therapies, pushing home-care to a 14.54% CAGR over the forecast period.

What factors could restrain market expansion?

Surgeon shortages, high capital costs for integrated platforms, polymer price volatility, and single-use-plastic legislation may temper growth through 2030.

Page last updated on: