Fractional Flow Reserve Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

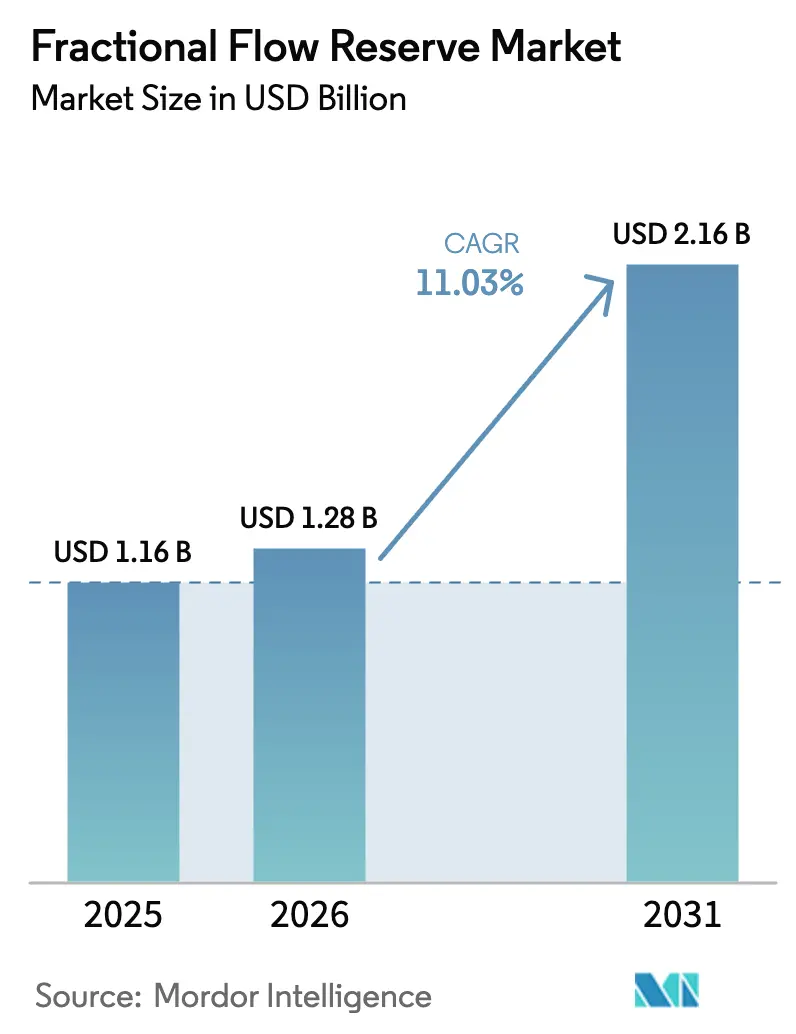

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 2.16 Billion |

| Growth Rate (2026 - 2031) | 11.03% CAGR |

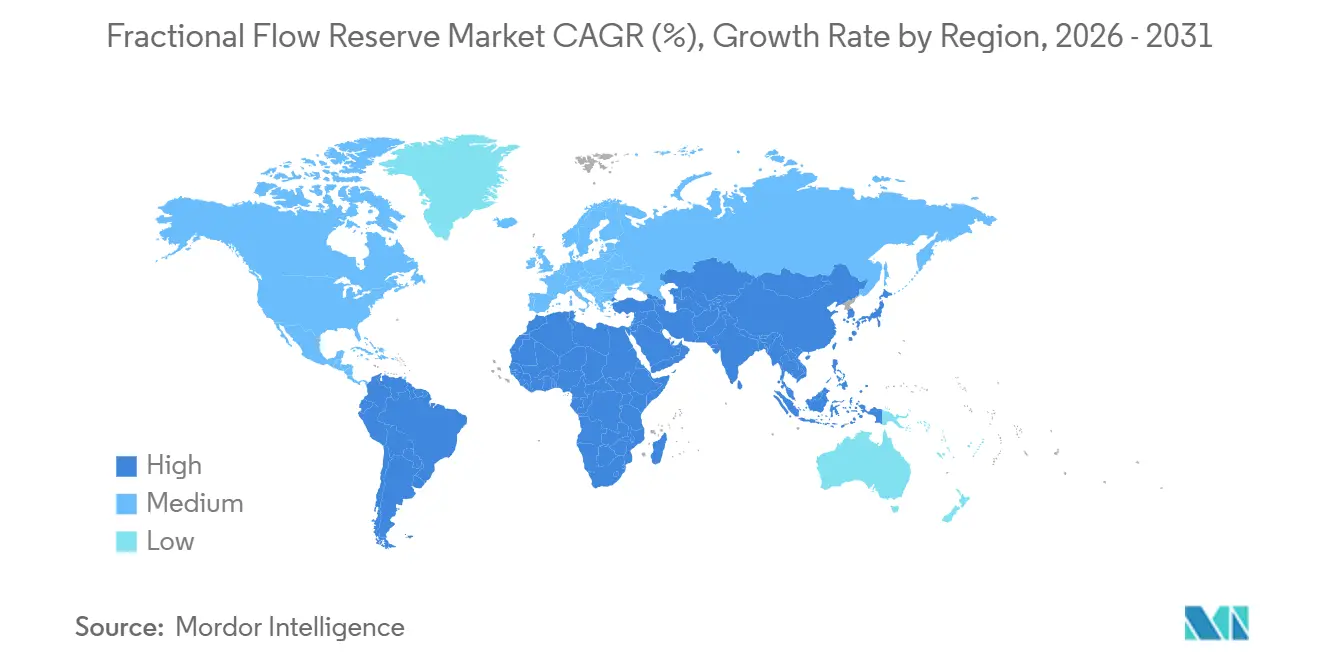

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

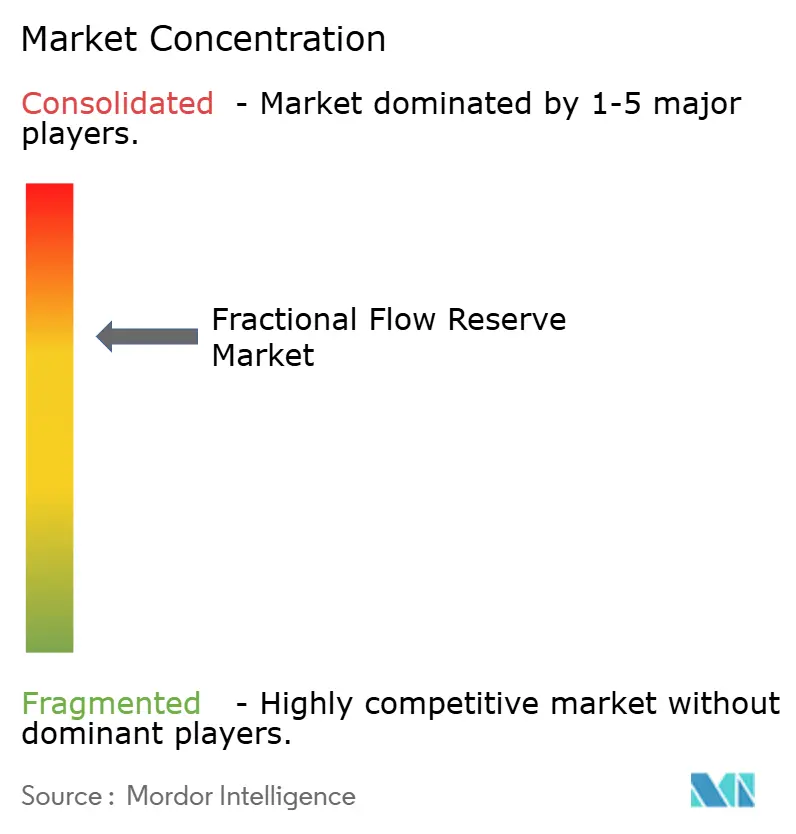

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fractional Flow Reserve Market Analysis by Mordor Intelligence

The Fractional Flow Reserve Market size is projected to be USD 1.16 billion in 2025, USD 1.28 billion in 2026, and reach USD 2.16 billion by 2031, growing at a CAGR of 11.03% from 2026 to 2031.

Growing guideline mandates for physiology-guided revascularization, wider reimbursement for non-invasive imaging, and technology miniaturization are steering clinicians away from angiography-only decision-making. Pressure-wire systems remain the procedural workhorse in catheterization laboratories, yet software-based FFR-CT platforms are accelerating fastest as outpatient imaging centers integrate computational fluid dynamics into routine chest-pain workup. Sensor innovation is splitting between premium optical-fiber designs and cost-scalable MEMS chips, while AI-driven angio-FFR is cutting procedure time and adenosine expenses in high-volume centers. North America leads adoption thanks to Medicare coverage, but Asia-Pacific is the quickest climber as China funds catheterization infrastructure and Japan’s aging population swells the coronary-disease pool. Competitive dynamics pivot on ecosystem lock-in: incumbents bundle consoles, cloud analytics, and training, whereas challengers push disposable-free software that slashes per-case cost.

Key Report Takeaways

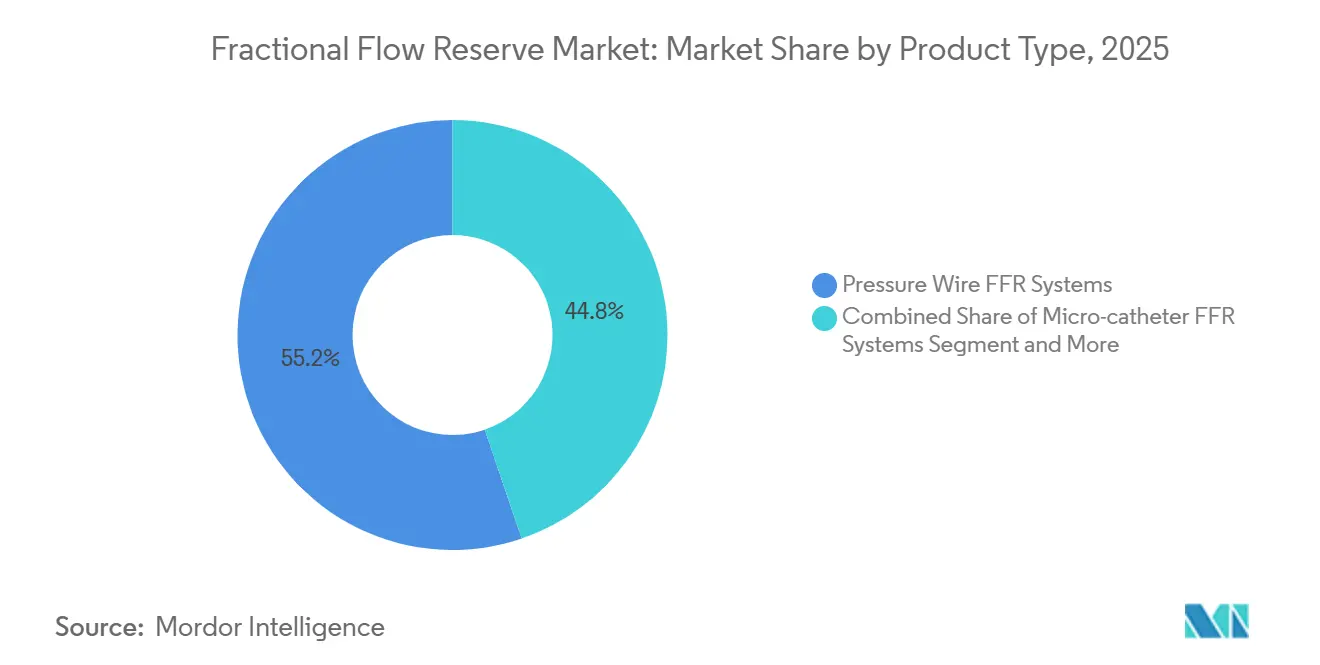

- By product type, pressure-wire systems led with 55.22% revenue share in 2025, while FFR-CT software platforms are projected to grow at a 15.24% CAGR through 2031.

- By sensor technology, optical-fiber sensors captured 46.52% of 2025 sales, whereas MEMS sensors are forecast to expand at a 14.55% CAGR up to 2031.

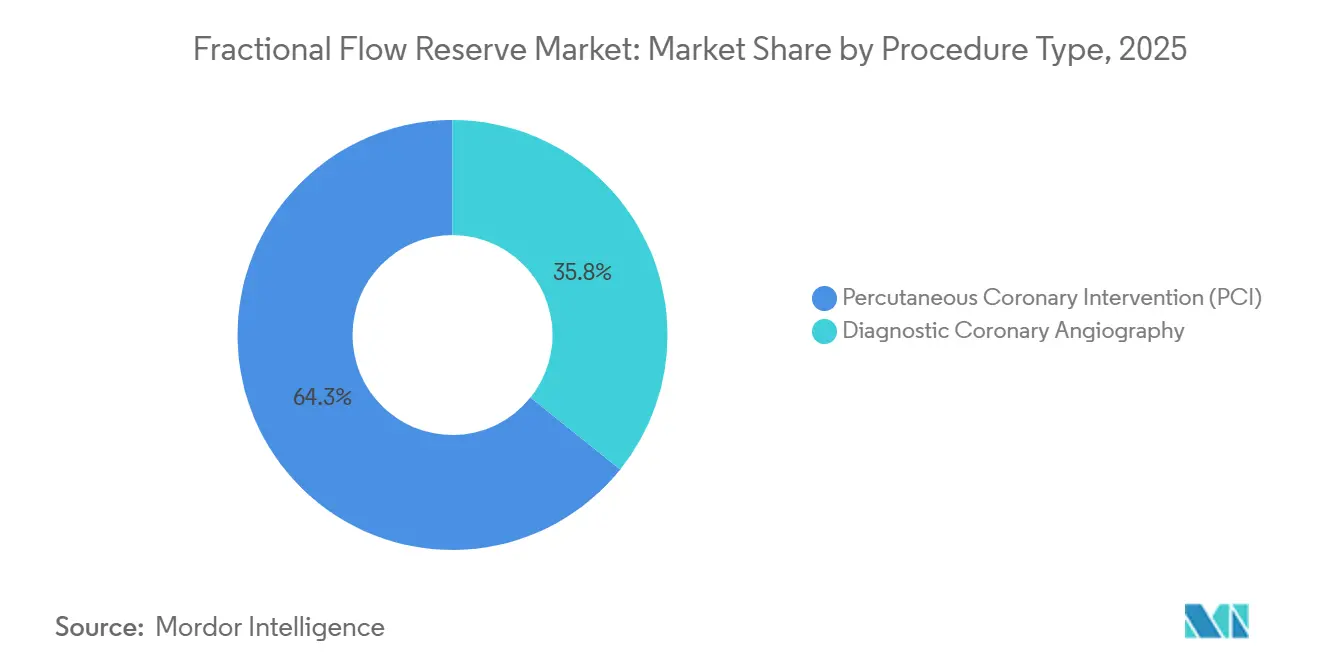

- By procedure, PCI procedures accounted for 64.25% of 2025 utilization, and diagnostic angiography is set to rise at a 12.52% CAGR to 2031.

- By Modality, Invasive FFR maintained 59.73% share in 2025, while non-invasive FFR-CT is expected to post a 15.64% CAGR through 2031.

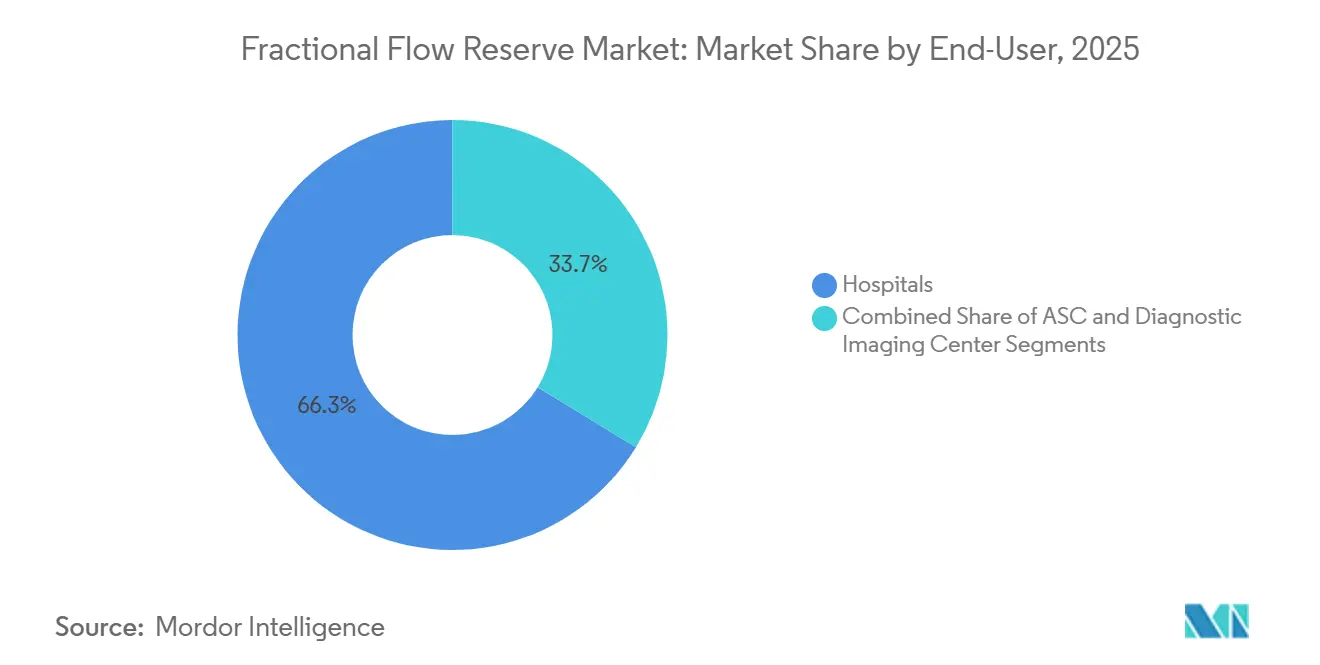

- By end user, hospitals captured 66.26% of 2025 spending, whereas diagnostic imaging centers are projected to advance at a 13.77% CAGR by 2031.

- By geography, North America held 39.73% revenue share in 2025, while Asia-Pacific is forecast to expand at a 13.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fractional Flow Reserve Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of CAD | 2.1% | Global, with highest burden in Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Guideline-Mandated FFR-Guided PCI | 2.5% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rapid Adoption of Non-Invasive FFR-CT | 2.8% | North America, Western Europe, urban Asia-Pacific hubs | Medium term (2-4 years) |

| Cost-Effectiveness Vs. Angiography-Only PCI | 1.4% | Global, particularly in value-based care systems (US, UK, Nordics) | Short term (≤ 2 years) |

| AI-Driven Real-Time Angio-FFR Analytics | 1.6% | North America, Europe, Japan, South Korea | Short term (≤ 2 years) |

| Emerging Reimbursement in Emerging Markets | 0.9% | China, India, Brazil, GCC countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of CAD

Coronary artery disease caused 19.8 million deaths in 2022, with three-quarters in low- and middle-income nations. Rapid urbanization and a doubling of diabetes prevalence across Asia-Pacific since 2000 are producing younger cohorts with diffuse disease that require physiology-based triage. Japan’s share of citizens aged ≥ 65 reached 29% in 2024, pushing stable angina volumes higher.[1]Ministry of Health, Labour and Welfare, “Statistical Handbook of Japan 2024,” Government of Japan, mhlw.go.jpIndia’s catheterization procedures jumped 34% between 2020 and 2024, yet only 15% used physiologic guidance, signaling sizable headroom for fractional flow reserve market penetration.[2]Ministry of Health and Family Welfare, “National Health Mission Annual Report 2024,” Government of India, nhm.gov.inHealth systems are turning to both invasive pressure wires and outpatient FFR-CT to manage referrals without proportionate interventional expansion.

Guideline-Mandated FFR-Guided PCI

The 2024 ESC chronic coronary syndromes guideline and the 2025 ACC/AHA acute coronary syndromes update each granted Class I status to wire-based FFR for intermediate lesions, shifting payer logic toward physiology first.[3]European Society of Cardiology, “2024 ESC Guidelines for the Management of Chronic Coronary Syndromes,” European Society of Cardiology, escardio.org FLOWER-MI showed a 22% drop in major adverse events with FFR-guided complete revascularization versus angiography alone. Reimbursement denials for angiography-only PCI now prompt hospitals to stock pressure wires and train operators, while AI-driven angio-FFR offers a lower-cost path to meeting the mandate.

Rapid Adoption of Non-Invasive FFR-CT

Medicare expanded FFR-CT coverage in January 2024, opening outpatient billing and deferring invasive work-ups in low-risk patients. HeartFlow, Siemens Healthineers, and GE Healthcare delivered radiology-integrated platforms that return physiology within 24 hours. DEFINE-FLOW reported a 31% reduction in unnecessary catheterizations and USD 1,200 savings per patient when FFR-CT guided triage. Uptake concentrates in regions with mature CT density and supportive payer models.

Cost-Effectiveness vs Angiography-Only PCI

Five-year FAME follow-up confirmed that deferring PCI in lesions with FFR > 0.80 yields equivalent outcomes and saves the USD 8,000 stent cost in the United States. NICE concluded in 2025 that FFR adds 0.14 QALY at only GBP 600 (USD 750) incremental cost, well under the NHS threshold. U.S. value-based contracts reward hospitals for cutting 30-day readmissions, propelling physiology-guided practice even in profit-focused systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device and Software Cost | -1.8% | Global, most acute in low- and middle-income countries | Medium term (2-4 years) |

| Limited Operator Skillset & Training | -1.3% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Diagnostic Uncertainty in Micro-Vascular Disease | -0.7% | Global, particularly in diabetic and female patient cohorts | Long term (≥ 4 years) |

| Competitive Pressure From iFR/OFR Modalities | -1.1% | Europe, North America, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device and Software Cost

Single-use pressure wires cost USD 600-1,200, while FFR-CT licenses run USD 50,000-150,000 plus USD 300-500 per scan, challenging budgets where annual health spend per capita is under USD 200. Even U.S. hospitals face margin squeeze when inexperienced teams extend procedures beyond 60 minutes.

Limited Operator Skillset & Training

SCAI reported in 2024 that only 40% of U.S. interventionalists apply FFR in more than 10% of cases, citing wire-handling and hyperemia knowledge gaps. Japan’s 2024 certification program mandates 25 supervised cases, yet remains confined to academic centers, mirroring capacity shortfalls across emerging regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wire Systems Remain Core While Software Outpaces

Pressure-wire systems commanded 55.22% of fractional flow reserve market share in 2025, underscoring the entrenched role of disposable sensor wires in real-time decision making. Adoption remains strongest in academic and high-volume community hospitals where guideline mandates and operator familiarity sustain procedure volumes. The fractional flow reserve market size generated by these wires is expected to rise steadily as replacement cycles and training programs reinforce their procedural status. FFR-CT software, though starting from a smaller base, is projected to expand at a 15.24% CAGR through 2031 because outpatient imaging centers can now bill Medicare directly for physiology studies.

Radiology departments favor software because it defers invasive work-ups and cuts total episode costs, benefits that resonate with value-based purchasing. Early U.S. adopters report a 30% fall in unnecessary catheterizations after integrating FFR-CT into chest-pain workflows, a trend mirrored in Western Europe. Vendors are tailoring platforms for seamless plug-ins to existing CT scanners, reducing capital barriers for mid-sized centers. This bifurcation means wire-based systems will keep servicing complex, on-table decisions, while software platforms open new revenues in outpatient diagnostics rather than cannibalizing established volumes.

By Sensor Technology: Optical Fiber Leads as MEMS Gains Momentum

Optical-fiber pressure sensors delivered 46.52% of 2025 revenue thanks to electromagnetic immunity and long-term stability, qualities prized in catheterization laboratories. They anchor premium offerings such as Abbott’s PressureWire X and Opsens’ OptoWire, which combine thin profiles with quick signal fidelity. Hospitals value the reduced drift that limits recalibration and shortens procedure time, helping maintain throughput under fixed reimbursement schedules.

Micro-electromechanical-systems sensors are forecast to grow at 14.55% annually through 2031 as semiconductor manufacturing lowers unit cost toward USD 400 per wire and boosts supply for emerging markets. Boston Scientific’s latest MEMS-based Comet wire cuts response time below 10 milliseconds, giving operators near-instant pressure feedback. The scalable economics appeal to health systems in Asia-Pacific and Latin America that face budget ceilings yet rising coronary-disease caseloads. As MEMS maturity narrows performance gaps, optical-fiber incumbents will defend share through ecosystem services, while mid-tier buyers migrate to lower-priced MEMS alternatives.

By Procedure Type: PCI Holds Majority While Diagnostic Angio Accelerates

Percutaneous coronary intervention accounted for 64.25% of fractional flow reserve market size in 2025, reflecting Class I guideline status for physiology-guided stenting in multi-vessel and left-main disease. Operators rely on wire-based readings to confirm ischemia before deploying costly devices, aligning with payer scrutiny over inappropriate stenting. Hospitals embed FFR checks into pre-dilation workflows, making wire use a routine step rather than an optional add-on.

Diagnostic coronary angiography, however, is climbing at a 12.52% CAGR as AI-driven angio-FFR estimates pressure from routine cine loops without wires or adenosine. The software trims 10-15 minutes per case, a saving that compounds across busy labs and frees capacity for complex interventions. Early data show 92% agreement with wire-based FFR in intermediate lesions, encouraging adoption in North America, Europe, and Japan. As licensing fees fall and accuracy improves in small vessels, diagnostic physiology could shift more decision making to the angiography suite, easing pressure on cath-lab schedules.

By Modality: Invasive Assessment Remains Core, FFR-CT Expands Fastest

Invasive measurements retained 59.73% share in 2025 because interventionalists want real-time data before committing to stents. Wireless consoles now stream waveforms to cloud dashboards, allowing remote experts to advise community operators in complex anatomy. Such connectivity shores up the modality’s dominance and widens its reach beyond quaternary hospitals.

Non-invasive FFR-CT is the fastest-growing modality, projected at a 15.64% CAGR through 2031, after Medicare’s 2024 coverage determination for outpatient billing unlocked broad U.S. access. DEFINE-FLOW demonstrated 92% concordance with invasive values in 40–70% stenoses, giving clinicians confidence to rule out unnecessary cath in stable chest-pain cohorts. Western Europe mirrors this trend as radiology reimbursement rewards advanced post-processing. Adoption remains slower in tier-2 Asian cities where CT density and payer models lag, but ongoing infrastructure programs signal gradual catch-up.

By End-User: Hospitals Dominate, Imaging Centers Grow Rapidly

Hospitals generated 66.26% of 2025 revenue, benefitting from entrenched catheterization laboratories, bundled purchasing, and fellowship-trained staff. Seven- to ten-year console lifecycles lock facilities into vendor ecosystems, creating switching costs and keeping wire volumes stable under fixed budgets. Integrated quality metrics that penalize inappropriate stenting further entrench physiologic checks at the bedside.

Diagnostic imaging centers are forecast to rise at a 13.77% CAGR to 2031 on the back of FFR-CT reimbursement that no longer requires hospital affiliation. Freestanding sites market one-stop chest-pain evaluations that spare patients invasive diagnostics unless physiology justifies referral. The model appeals to payers looking to shift care from high-cost hospital settings, especially in U.S. metropolitan areas. Vendors now bundle cloud analytics and technical support aimed at radiologists rather than cardiologists, broadening the fractional flow reserve market and diversifying revenue beyond acute-care facilities.

Geographical Analysis

North America held 39.73% share in 2025, buoyed by Medicare’s national FFR-CT coverage and FDA clearance for angio-FFR reimbursements that pay USD 350 per case. Canada lags under provincial patchwork, and rural Mexico lacks labs despite IMSS coverage.

Asia-Pacific is set for 13.34% CAGR to 2031 as China funds one cath lab per 300,000 citizens and reimburses 70% of wire cost. Japan’s 29% senior population raises stable angina incidence, while India’s procedure boom still misses physiologic guidance in 85% of cases.

Europe commands roughly 25% share, led by NICE’s 2025 endorsement and Germany’s automatic statutory coverage. Southern Europe trails due to budget constraints. MEA and South America combine for single digits, yet GCC oil revenues finance full adoption, and Brazil’s private sector now pays for FFR despite public-sector gaps.

Competitive Landscape

Abbott, Philips, Boston Scientific, and Opsens are among the key players in the market. The market is moderately fragmented. Incumbents add wireless data, cloud analytics, and training to lock accounts, whereas CathWorks and Medis attack with disposable-free software. Patent filings on MEMS miniaturization and machine-learning surged 40% between 2023 and 2025. Emerging entrants from China and India pitch sub-USD 500 wires but lack global validation.

White space lies in micro-vascular assessment; Abbott’s Coroventis aims to pair FFR with flow reserve, but clearance is pending. Resting indices such as iFR and OFR now capture 35% of European physiology, fragmenting modality choice and pressuring FFR pricing.

Fractional Flow Reserve Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Koninklijke Philips NV.

Opsens Inc

ACIST Medical Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Royal Philips agreed to acquire SpectraWAVE, adding AI angio-physiology and near-infrared plaque imaging.

- October 2025: SpectraWAVE received FDA clearance for X1-FFR, combining NIRS plaque analysis with angio-derived pressure gradients.

- January 2024: HeartFlow secured expanded Medicare coverage for FFR-CT in outpatient centers, boosting its U.S. addressable market by 40%.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the fractional flow reserve (FFR) market as all invasive or image-derived systems that quantify coronary lesion-specific blood-flow pressure ratios during a diagnostic or pre-intervention work-up. Hardware (pressure guidewires, micro-catheters, console platforms) and software used to calculate FFR-CT values are counted wherever they are sold to clinical settings.

Scope exclusion: veterinary cardiology devices and research-only bench analyzers are outside this estimate.

Segmentation Overview

- By Product Type

- Pressure-Wire FFR Systems

- Micro-catheter FFR Systems

- FFR-CT Software Platforms

- Disposable Sensor Wires & Accessories

- By Sensor Technology

- Optical Fiber Pressure Sensors

- Piezoelectric / Strain-Gauge Sensors

- MEMS-based Sensors

- Other Emerging Sensors

- By Procedure Type

- Diagnostic Coronary Angiography

- Percutaneous Coronary Intervention (PCI)

- By Modality

- Invasive FFR

- Non-Invasive FFR-CT

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Diagnostic Imaging Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Cardiologists, cath-lab managers, imaging physicists, and procurement heads across North America, Europe, and fast-growing Asian hubs shared real-world utilization ratios, disposable usage patterns, and discount brackets. Follow-up surveys captured sentiment on AI-enabled FFR-CT and likely substitution rates, letting us reconcile desk assumptions with frontline realities.

Desk Research

We began with open datasets from bodies such as the World Health Organization, the American College of Cardiology, Eurostat, and Japan's MHLW to size coronary angiography procedure pools. Trade associations like the Medical Imaging & Technology Alliance and customs shipment records helped refine global equipment flows. Company 10-Ks, investor decks, and reputable press articles revealed average selling prices and recent unit placements. To deepen competitive intelligence, Mordor analysts queried D&B Hoovers for supplier financials and Dow Jones Factiva for launch timelines. The sources cited here are illustrative; many additional publications informed data checks and clarifications.

Our analysts extracted reimbursement fee schedules (e.g., CMS CPT codes for FFR-CT), clinical-trial registries tracking adoption of non-invasive modalities, and patent filings accessed through Questel to spot pipeline contributions. These secondary signals offered the foundational guardrails before we validated them in the field.

Market-Sizing & Forecasting

A top-down reconstruction of FFR demand starts with national angiography volumes, prevalence of flow-limiting stenosis, and guideline-driven FFR adoption thresholds, which are then multiplied by verified device penetration and ASP curves. Selective bottom-up roll-ups of major supplier revenues and channel checks acted as cross-bars to adjust totals. Key variables like annual CAD incidence, reimbursement shifts, CT-scanner installed base, average disposable use per case, and AI-FFR accuracy gains feed a multivariate regression model that projects unit and revenue trajectories. Scenario analysis layers in regulatory or price-cut shocks, allowing gap handling where granular shipment data are sparse.

Data Validation & Update Cycle

Outputs pass anomaly checks versus hospital procurement dashboards and regional import statistics before a senior reviewer signs off. Reports refresh yearly; material events like guideline changes trigger interim updates and a new analyst pass so clients receive the freshest baseline.

Why Mordor's Fractional Flow Reserve Baseline Commands Confidence

Published estimates often diverge because firms pick different device mixes, apply varied adoption multipliers, and refresh at uneven cadences.

Key gap drivers include whether non-invasive CT-FFR kits are counted, how aggressively price erosion is modeled, and the cadence at which emerging Asia volumes are refreshed. Mordor's study aligns scope with clinical guidelines, applies consensus ASP decay, and updates every 12 months, yielding a balanced view.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.18 B (2025) | Mordor Intelligence | - |

| USD 1.06 B (2025) | Regional Consultancy A | Excludes CT-FFR software; relies on 2019 ASPs |

| USD 1.16 B (2025) | Trade Journal B | Uses conservative Asia procedure base; no price erosion curve |

| USD 1.03 B (2024) | Global Consultancy C | Forecast frozen since 2023; limited primary validation |

Taken together, the comparison shows that numbers swing when scope, price dynamics, and update rigor vary. By triangulating multiple inputs and refreshing frequently, Mordor Intelligence delivers a transparent, reproducible baseline decision-makers can trust.

Key Questions Answered in the Report

How large is the fractional flow reserve market in 2026?

The fractional flow reserve market size is USD 1.28 billion in 2026.

What is the expected CAGR for fractional flow reserve products to 2031?

Revenue is projected to grow at an 11.03% CAGR through 2031.

Which product category is expanding fastest?

FFR-CT software platforms are forecast to post a 15.24% CAGR on wider outpatient imaging use.

Why is Asia-Pacific the quickest-growing region?

Government reimbursement, new catheterization labs in China, and Japan’s aging population underpin a 13.34% regional CAGR.

Which companies dominate non-invasive FFR-CT?

HeartFlow leads with about 60% share, while Siemens Healthineers and GE Healthcare are gaining ground.

How do AI angio-FFR platforms benefit hospitals?

They cut procedure time by up to 15 minutes and avoid adenosine costs, boosting workflow efficiency without adding disposables.

Page last updated on: