Central Fill Pharmacy Automation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

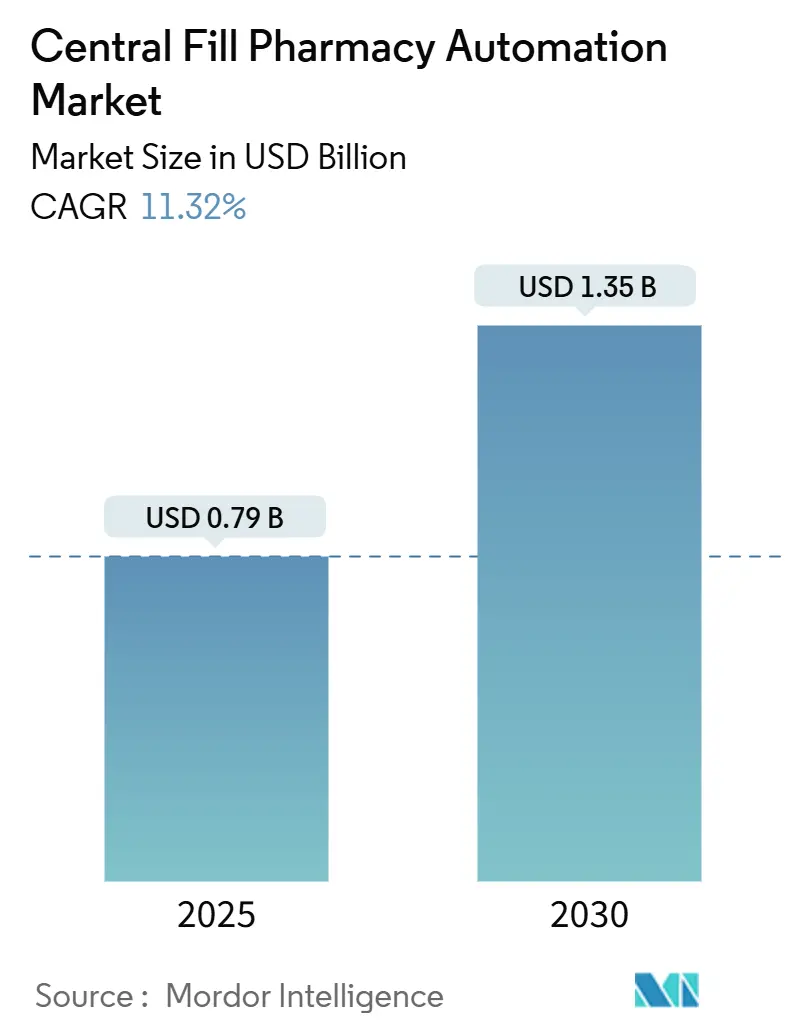

| Market Size (2025) | USD 0.79 Billion |

| Market Size (2030) | USD 1.35 Billion |

| Growth Rate (2025 - 2030) | 11.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Central Fill Pharmacy Automation Market Analysis by Mordor Intelligence

The central fill pharmacy automation market size is valued at USD 0.79 billion in 2025 and is forecast to reach USD 1.35 billion in 2030, reflecting an 11.32% CAGR. The growth trajectory mirrors rising labor costs, widening pharmacist shortages, and accelerating mail-order volumes that already exceed 16 million prescriptions each month. Investment momentum is further reinforced by stricter track-and-trace rules under the Drug Supply Chain Security Act, heightened demand for medication accuracy, and retailer cost-saving successes such as Walgreens’ USD 500 million in annual fulfillment savings after rolling out micro-fulfillment hubs. Artificial-intelligence tools that spot drug shortages, IoT-linked robotics that run 24/7, and service-based financing models continue to expand the addressable base of hospital, retail, and mail-order operators. Collectively, these forces position the central fill pharmacy automation market as a mission-critical pillar in pharmacy supply-chain modernization worldwide.

Key Report Takeaways

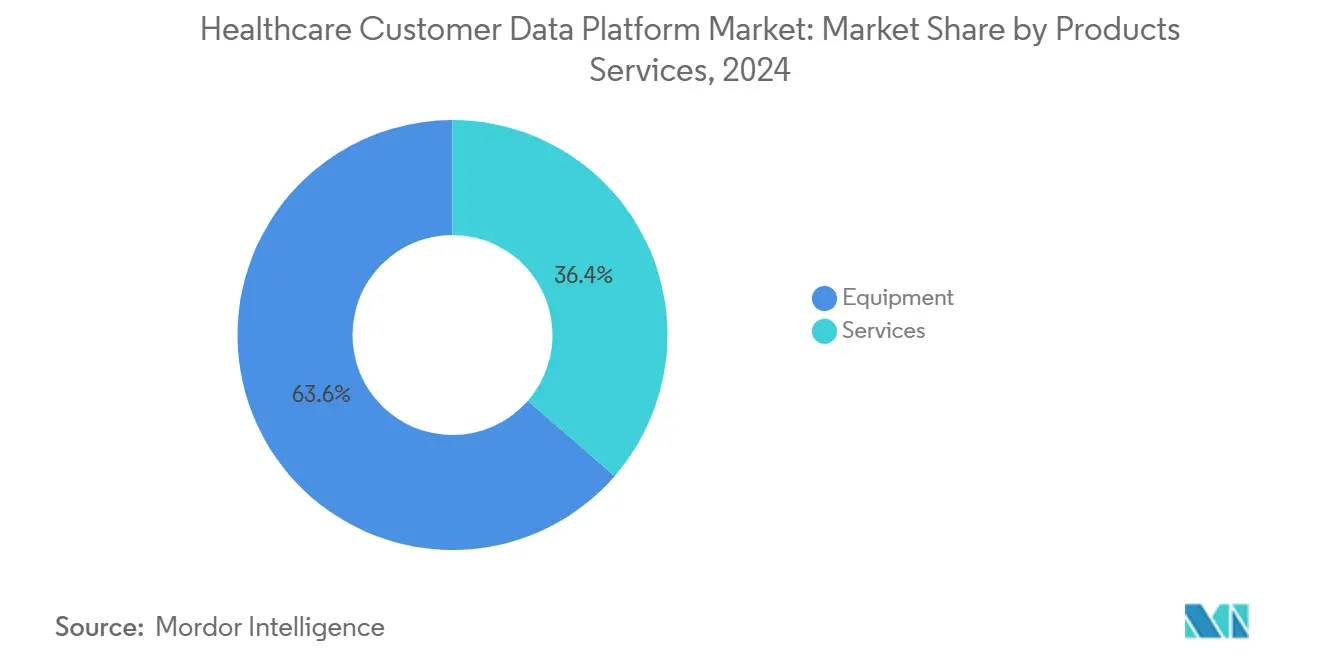

- By products & services, equipment captured 63.67% of the central fill pharmacy automation market share in 2024. Services are forecast to expand at a 13.56% CAGR to 2030

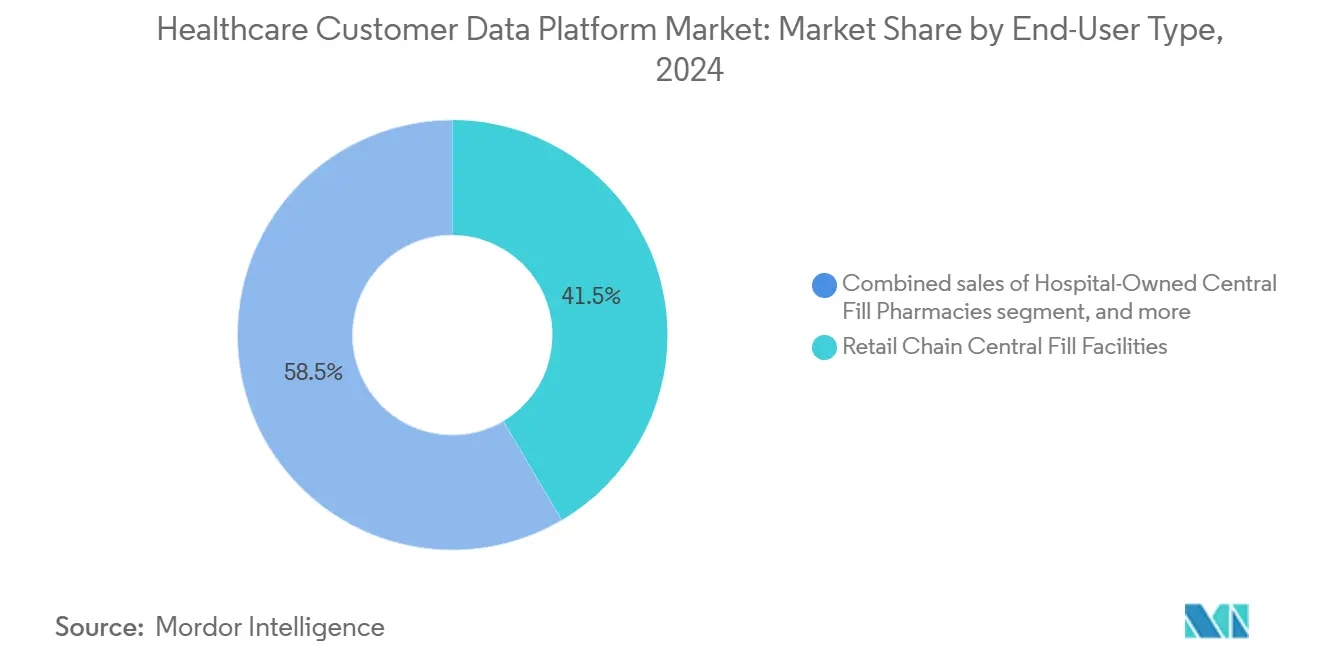

- By end-user, retail chains led with 41.56% revenue share in 2024; mail-order and online pharmacies are projected to advance at a 14.67% CAGR through 2030

- By throughput capacity, medium-volume sites held 47.55% share of the central fill pharmacy automation market size in 2024, while high-volume facilities are poised for 13.65% CAGR through 2030

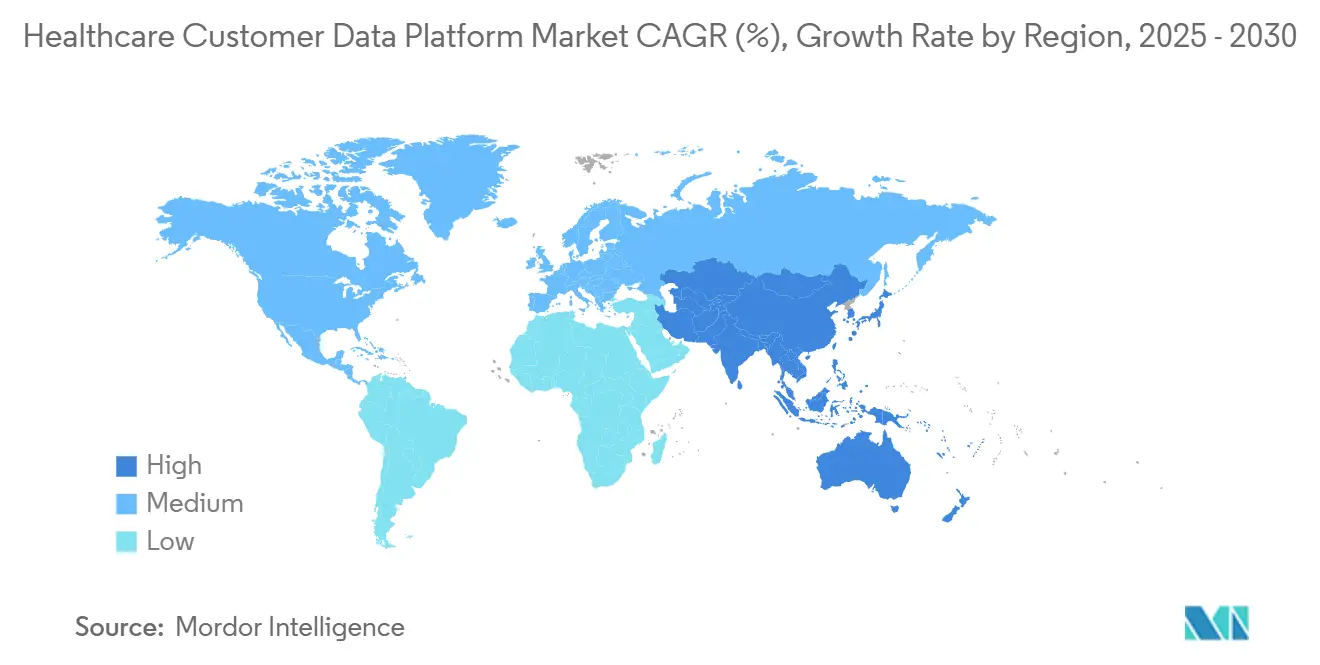

- By geography, North America commanded 46.87% share in 2024, whereas Asia-Pacific is expected to register a 12.56% CAGR between 2025-2030

Global Central Fill Pharmacy Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand For High-Throughput Prescription Fulfilment | +2.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Rising Labor Costs And Need For Operational Efficiency | +2.1% | Global, acute in North America & Western Europe | Short term (≤2 years) |

| Expansion Of Mail-Order And E-Commerce Pharmacy Channels | +1.9% | Global, led by North America, expanding in APAC | Medium term (2-4 years) |

| Emphasis On Medication Safety And Accuracy | +1.4% | Global, regulatory-driven in developed markets | Long term (≥4 years) |

| Adoption Of Advanced Analytics And Robotics | +1.6% | North America & Europe core, APAC emerging | Medium term (2-4 years) |

| Vertical Integration Across Pharmacy Supply Chain | +1.2% | North America & Europe, selective APAC markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for High-Throughput Prescription Fulfillment

Facilities processing above 20,000 prescriptions per day now require advanced robotic cells that sustain industrial-level throughput. Walgreens’ newest micro-fulfillment hub handles about 13 million prescriptions annually for roughly 200 regional stores, underscoring the scale advantage now achievable[1]Walgreens Boots Alliance, “Walgreens Opens Micro Fulfillment Center in Minnesota,” walgreensbootsalliance.com. High-volume locations are posting a 13.65% CAGR because they lower per-script costs by 13%, improve inventory turns, and embed automated image-verification checkpoints that curb dispensing errors. Mail-order volumes have grown 126% since 2020, further concentrating scripts into fewer but larger hubs that operate 24/7 with less human oversight. The trend is rapidly redefining prescription fulfillment as a manufacturing workflow requiring conveyor sequencing, robotic induction, and palletization similar to consumer-goods distribution.

Rising Labor Costs and Need for Operational Efficiency

Graduating pharmacist numbers have fallen 10% while applicant pools have shrunk 60% over the past decade, widening wage pressures that automation helps contain. California’s Assembly Bill 1286 adds mandatory staffing ratios, spurring chains to augment capacity without inflating payroll. Automated cells can cut technician prep time 59% and reduce pharmacist check time 80%, creating a swift payback in high-cost urban markets. Around-the-clock robotics also eliminate overtime premiums and mitigate scheduling gaps, allowing pharmacists to shift toward clinical services such as vaccinations, which climbed 40% once tasks moved to a hub model.

Expansion of Mail-Order and E-Commerce Pharmacy Channels

COVID-19 catalyzed a permanent shift toward remote dispensing, and mail-order now represents the fastest-growing end-user at 14.67% CAGR. Operators such as Sweden’s Apotea added a RightHand Robotics picking line that handles an extra 50,000 orders daily. U.S. telehealth rules that extend flexibility for controlled substance prescribing unlock additional mail-order volumes. Pay-per-script offerings like CoverMyMeds’ Central Fill as a Service lower adoption barrier by removing capital outlays while delivering compliance-ready labeling, verification, and track-and-trace functions. Automated pouch packaging and cold-chain modules further ensure medication integrity during last-mile delivery.

Adoption of Advanced Analytics and Robotics

Predictive platforms such as Premier’s CognitiveRx spot potential drug shortages with 76% accuracy by scanning purchase patterns across 4,300 hospitals. Omnicell’s cloud-native OmniSphere integrates inventory analytics, maintenance alerts, and robotic orchestration into a single dashboard that reduces manual data entry by 97%. AI also supports preventive maintenance, cutting downtime across high-throughput lines to below 1%. While sterile-compounding robots remain niche—hospital adoption dipped from 4.3% in 2020 to 3.7% in 2023—the continued mix of machine learning and vision systems is expected to streamline complex tasks in high-value therapies Sterile Compounding Adoption Survey 2023,” ashp.org"> Sterile Compounding Adoption Survey 2023,” ashp.org"> Sterile Compounding Adoption Survey 2023,” ashp.org">[2]American Society of Health-System Pharmacists, “USP <797> Sterile Compounding Adoption Survey 2023,” ashp.org.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Availability Of Skilled Automation Workforce | −1.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| High Capital Expenditure Requirements | −2.3% | Global, particularly challenging for smaller operators | Short term (≤2 years) |

| Legacy System Integration Challenges | −1.5% | Global, most significant in established markets with older IT infrastructure | Short term (≤2 years) |

| Regulatory Constraints On Centralized Dispensing | −1.2% | Global, with varying state- and country-level rules | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Skilled Automation Workforce

Robotics-enabled pharmacies require technicians versed in interplay between medication regulations, software integration, and mechanical troubleshooting. Yet technical talent remains scarce, particularly in emerging markets where vocational programs lag. Six-to-twelve-month specialized courses are needed, and declining pharmacy-school cohorts further shrink the talent funnel. Market leaders now bundle on-site training and remote monitoring to offset gaps, but scarcity still lengthens implementation timelines and raises support costs. In some regions, operators defer upgrades altogether until service ecosystems mature.

High Capital Expenditure Requirements

A fully automated hub can exceed USD 1 million, and recent tariff-driven component inflation wiped USD 40 million from Omnicell’s non-GAAP EBITDA in 2025. Smaller independents often struggle to secure financing, leading to a two-tier landscape where enterprise chains deploy robotics while local pharmacies rely on manual workflows. Solutions such as CoverMyMeds’ pay-per-script model and Omnicell subscription bundles mitigate capex, but retrofit projects in existing buildings still quick-ly surpass equipment costs owing to HVAC, power, and IT upgrades. Despite 2- to 3-year payback windows reported by large chains, capital hurdles remain a major break on penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products & Services: Equipment Dominance Drives Market Foundation

Equipment held 63.67% share of the central fill pharmacy automation market in 2024, anchored by high-speed robotic dispensing, automated pouch packagers, and vision-based verification lines. Automated units such as ScriptPro’s SP Series report 99.6% uptime while preparing thousands of scripts per shift. The central fill pharmacy automation market size for services, however, is expanding faster at a 13.56% CAGR as owners seek predictive maintenance, optimization analytics, and compliance support. Outcome-linked programs, typified by Omnicell’s XT Amplify, integrate clinical benchmarking with equipment upgrades to maximize error reduction and throughput. Consulting and workforce-training engagements are growing because facilities need cross-disciplinary expertise to fine-tune robotic pick paths, master new serialization mandates, and satisfy auditors.

The central fill pharmacy automation market share advantage for equipment remains intact because each greenfield hub needs conveyors, automated storage, labeling tunnels, and dispatch sorters. Even so, the recurring-revenue appeal of services is prompting vendors to create subscription bundles that include hardware refresh cycles, cloud software, and 24/7 remote monitoring. As a result, the central fill pharmacy automation industry is shifting from discrete capital sales toward solution lifecycle partnerships that lock in multiyear revenue visibility.

By End-User Type: Retail Chains Lead While Mail-Order Accelerates

Retail chains controlled 41.56% of the central fill pharmacy automation market share in 2024, driven by economies of scale that let a single facility serve thousands of stores. Walgreens’ network processes 13 million prescriptions annually at each site, freeing in-store pharmacists to deliver care services. Hospital systems adopt hubs mainly to support specialty and high-risk therapies, while long-term-care pharmacies use robotics to slash retrieval time 71% and eliminate 96% of unscheduled delivery costs, saving USD 8,900 per facility.

Mail-order and e-commerce operators hold a smaller base today but exhibit the steepest climb at 14.67% CAGR, propelled by telemed-enabled repeat prescriptions, subscription drug plans, and Medicare Part D caps that invite multi-month fills. Platform players invest heavily in automated tote sequencing, RFID-enabled cold-chain monitors, and AI-assisted routing engines to meet 48-hour delivery pledges. Consequently, the central fill pharmacy automation market size tied to direct-to-consumer models is poised to accelerate faster than any other end-user category through 2030.

By Throughput Capacity: Medium Volume Dominates, High-Capacity Drives Growth

Medium-throughput hubs (5,000-20,000 Rx/day) held 47.55% of the central fill pharmacy automation market size in 2024. Proven solutions such as Parata’s PASS enable pouch packaging, inventory cycling, and barcode auditing within mid-scale footprints that balance automation cost and script volume. Low-throughput settings (<5,000 Rx/day) lag because payback periods stretch, yet tabletop robots like Qx-Dextron now shorten breakeven to under one year for smaller independents.

High-throughput mega-facilities (≥20,000 Rx/day) are on an expansion tear with a 13.65% CAGR. Quicktron’s deployment at Sinopharm increased warehouse capacity 1.5 times and space utilization 15% through automated shuttles and vertical lifts. In these facilities, multi-aisle robotic pick stations, automated case erectors, and palletizers operate under unified WES software that keeps order latency below 2 hours. Such performance cements the mega-hub model as the next frontier in global prescription logistics.

Geography Analysis

North America captured 46.87% of the central fill pharmacy automation market in 2024, anchored by long-standing DSCSA serialization deadlines and chain-pharmacy consolidation that favors large hubs. Omnicell, BD, and ScriptPro maintain extensive service fleets and data-driven contracts, enabling rapid rollouts and cross-site benchmarking. State mandates—including e-prescribing laws in 35 states and California’s staffing ratio rule—further strengthen the case for broad automation. Financing creativity, such as CoverMyMeds’ service-based model, continues to broaden adoption among midsize groups.

Asia-Pacific is the fastest-growing territory, projected at 12.56% CAGR. China’s policy push for pharmaceutical manufacturing digitalization underpins large-scale deployments such as Sinopharm’s automated warehouse, the country’s first of its kind. Japan’s aging demographics and drug-safety mandates drive hospitals to invest in pouch inspection and traceability. Government subsidies for smart-manufacturing technology in India, South Korea, and Singapore expand the install base for robotic dispensing, inventory analytics, and cold-chain packaging[3]International Society for Pharmaceutical Engineering, “Pharma 4.0 in Asia Pacific,” ispe.org.

Europe remains a steady growth contributor, underpinned by the Pharmaceutical Inspection Co-operation Scheme and country-specific e-health reforms. Dr. Max’s 14,000 m² automation center in Italy delivers nationwide scripts with SSI SCHAEFER shuttle towers and Geekplus AMRs, showcasing multi-vendor orchestration at scale. Denmark’s 2024 Pharmacy Act amendment allows hospital pharmacies to dispense directly to outpatients, widening the addressable hub network. Sustainability targets motivate European operators to install energy-efficient shuttle systems and integrate recyclable packaging streams alongside robotic dispensing.

Competitive Landscape

The central fill pharmacy automation market is moderately fragmented, with Omnicell, BD (after its Parata purchase), and ScriptPro securing anchor positions through hardware breadth, cloud analytics, and nationwide field support. Mid-tier entrants include iA (majority owned by Walgreens) and Swisslog Healthcare, each leveraging strategic partnerships to extend portfolio depth. AI-centric newcomers such as Plenful raised USD 17 million to automate claims workflows, signaling rising venture interest in adjacent automation layers that complement dispensing lines.

M&A remains active. BD’s USD 1.5 billion Parata acquisition boosts its medication-management footprint, whereas McKesson’s USD 850 million majority stake in PRISM Vision deepens specialty fulfillment capabilities. Technology differentiation gravitates toward cloud-native orchestration, predictive analytics, and outcome-based service plans. Vendors increasingly guarantee error-rate reductions and throughput gains, aligning fee structures with verified performance metrics. White-space persists in sterile-compounding automation where hospital uptake slid to 3.7% in 2023, leaving scope for simplified, closed-system designs.

Central Fill Pharmacy Automation Industry Leaders

-

McKesson Corporation

-

Parata Systems LLC

-

Omnicell Inc

-

ARxIUM Inc

-

RxSafe LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Walgreens Boots Alliance opened a Brooklyn Park, Minnesota, hub able to fill 13 million scripts yearly for nearly 200 stores.

- May 2025: Omnicell reported Q1 2025 revenue of USD 270 million, up USD 24 million year-on-year, and raised full-year guidance.

- February 2025: McKesson agreed to acquire 80% of PRISM Vision Holdings for roughly USD 850 million, enhancing specialty-pharmacy reach.

- December 2024: Omnicell launched OmniSphere, a cloud-native workflow engine that unifies robotics and smart devices for DSCSA compliance.

- September 2024: BD completed its takeover of Parata Systems, adding central fill and outpatient automation to its medication portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study regards the central fill pharmacy automation market as the sale of equipment, software, and related integration services that enable off-site, high-throughput facilities to aggregate prescriptions from multiple pharmacies, robotically dispense, pack, and route them back for final check and pickup or mail-out. This definition captures conveyor and workflow systems, automated medication dispensing, labeling, storage, retrieval, and the supervisory software that synchronizes them.

Scope exclusion: stand-alone automated dispensing cabinets installed inside hospitals or long-term-care wards fall outside this perimeter.

Segmentation Overview

-

By Products & Services

-

Equipment

- Automated Medication Dispensing Systems

- Automated Packaging & Labeling Systems

- Automated Medication Compounding Systems

- Other Equipments

-

Services

- Implementation & Integration Services

- Maintenance & Support Services

- Consulting & Training Services

-

Equipment

-

By End-User Type

- Hospital-Owned Central Fill Pharmacies

- Retail Chain Central Fill Facilities

- Mail-Order & Online Pharmacies

- Long-Term Care (LTC) Pharmacies

-

By Throughput Capacity

- Low (≤5k Rx/Day)

- Medium (5k–20k Rx/Day)

- High (≥20k Rx/Day)

-

Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed pharmacists running hub-and-spoke centers, automation engineers, and regional wholesalers across North America, Europe, and Asia-Pacific. These discussions tested downtime rates, average script-per-hour metrics, and price elasticity assumptions, filling blind spots left by public data and anchoring scenario inputs.

Desk Research

We began with widely quoted public data on prescription volumes and mail-order penetration from sources such as the US National Association of Chain Drug Stores, Centers for Medicare & Medicaid Services, the FDA's Drug Supply Chain Security Act implementation updates, and comparable statistics offices in Canada, Germany, and Japan. Trade publications like Drug Topics and the European Association of Hospital Pharmacists helped trace adoption timelines, while company 10-Ks and patent filings clarified revenue splits and recent product claims. Subscription databases including D&B Hoovers and Dow Jones Factiva enriched financial and deal flow tracking. The sources noted here are illustrative; many further outlets informed fact-checking and context building.

Market-Sizing & Forecasting

A top-down reconstruction starts with country-level retail prescription counts, adjusts for chain ownership share and central-fill adoption rates, and multiplies by typical equipment refresh and software fee schedules; results are cross-checked through selective bottom-up roll-ups of supplier shipments and sampled average selling prices. Key variables like labor cost differentials, script error penalties, facility throughput bands, e-commerce pharmacy growth, and regulatory e-prescription mandates drive our multivariate regression forecast. Bottom-up gaps where shipment detail proved thin were bridged using median ASPs from channel checks before final alignment of the two views.

Data Validation & Update Cycle

Outputs pass a multi-step variance scan against external market indicators, then a peer review. Reports refresh once a year, and analysts reopen the model whenever material events, large acquisitions, guideline shifts, or double-digit currency swings occur, ensuring buyers receive the latest vetted baseline.

Why Mordor's Central Fill Pharmacy Automation Baseline Commands Reliability

Published figures often diverge because firms differ on what products they count, how they treat service revenue, and the cadence at which they refresh exchange rates and inflation factors.

Key gap drivers in this space include whether software service contracts are capitalized, if hospital-owned hubs are counted alongside retail, and the ASP progression method each firm applies to high-capacity robotic lines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.79 billion (2025) | Mordor Intelligence | - |

| USD 1.30 billion (2024) | Global Consultancy A | Bundles mail-order fulfillment software for PBMs and counts some in-hospital robot upgrades |

| USD 0.656 billion (2024) | Industry Association B | Excludes integration services, uses 2019 currency base and linear growth assumption |

The comparison shows that values swing when scope and price escalation logic differ. According to Mordor Intelligence, our disciplined mix of clarified scope, dual-angle (bottom-up and top-down) modeling, and annual refresh cadence produces a balanced, repeatable baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the central fill pharmacy automation market?

The market is valued at USD 0.79 billion in 2025 and is projected to reach USD 1.35 billion by 2030.

Which segment is expanding fastest in the central fill pharmacy automation market?

Mail-order and online pharmacies are forecast to grow at a 14.67% CAGR through 2030, outpacing all other end-user segments.

Why are high-throughput mega-facilities gaining popularity?

Sites processing at least 20,000 prescriptions daily reduce per-script costs by 13% and improve space utilization, yielding the highest ROI among capacity tiers.

How are rising labor costs influencing automation investment?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Central Fill Pharmacy Automation Market?

A 10% decline in pharmacy graduates and new staffing ratio laws make robotics attractive, as automated hubs cut technician prep time 59% and pharmacist check time 80%.

Which region shows the quickest growth pace?

Asia-Pacific is expected to achieve a 12.56% CAGR between 2025 and 2030 due to manufacturing modernization policies and growing healthcare spending.

What are the key barriers to wider adoption?

High upfront capital requirements and a limited pool of skilled automation technicians remain the two largest constraints on new deployments.

Page last updated on: