Cellulosic And Regenerated Cellulose Films In Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

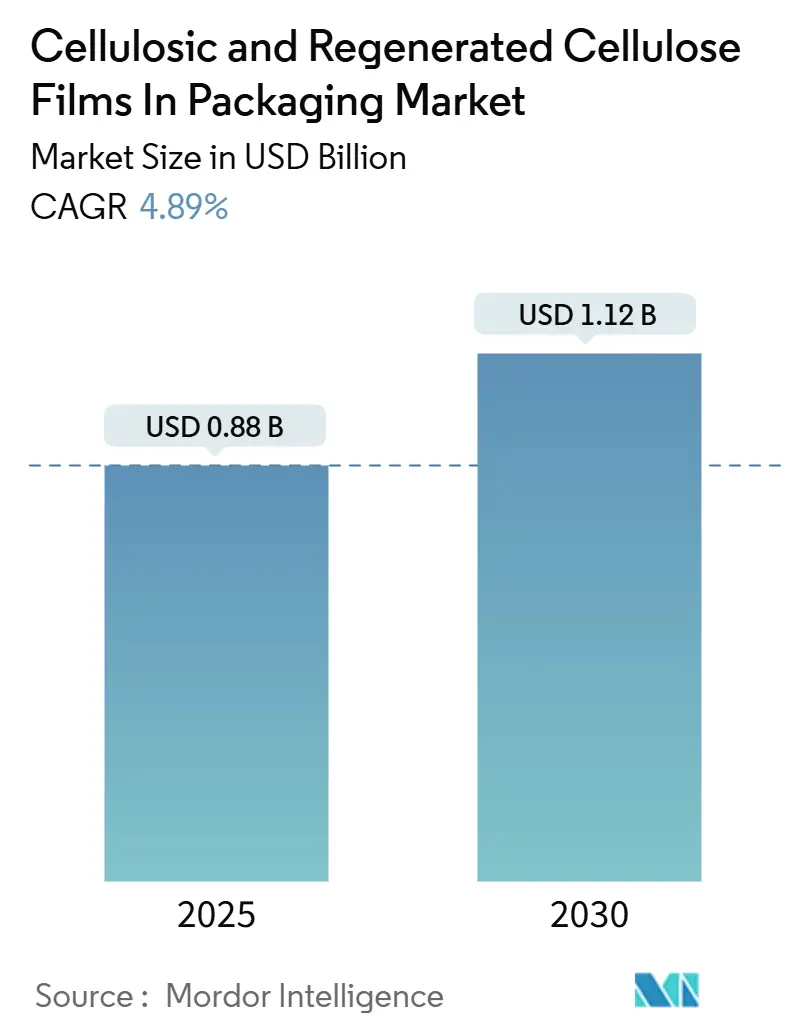

| Market Size (2025) | USD 0.88 Billion |

| Market Size (2030) | USD 1.12 Billion |

| Growth Rate (2025 - 2030) | 4.89% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cellulosic And Regenerated Cellulose Films In Packaging Market Analysis by Mordor Intelligence

The cellulosic and regenerated cellulose films in the packaging market size is valued at USD 0.88 billion in 2025 and is forecast to reach USD 1.12 billion by 2030, advancing at a 4.89% CAGR. Global brands, regulators, and consumers are increasingly favoring compostable solutions, which positions cellulose films as an immediate alternative to single-use plastics. Consistent progress in water-based barrier coatings, fresh produce packaging mandates, and advanced dissolving pulp supply chains reinforces demand momentum. Moderate market concentration allows established producers to secure pricing premiums, yet Asian newcomers narrow the gap by offering cost-effective capacity expansions. Ongoing vertical integration into agricultural residue-based pulp strengthens raw-material security, while innovations in ultra-thin gauges broaden application scope beyond conventional wrapping.

Key Report Takeaways

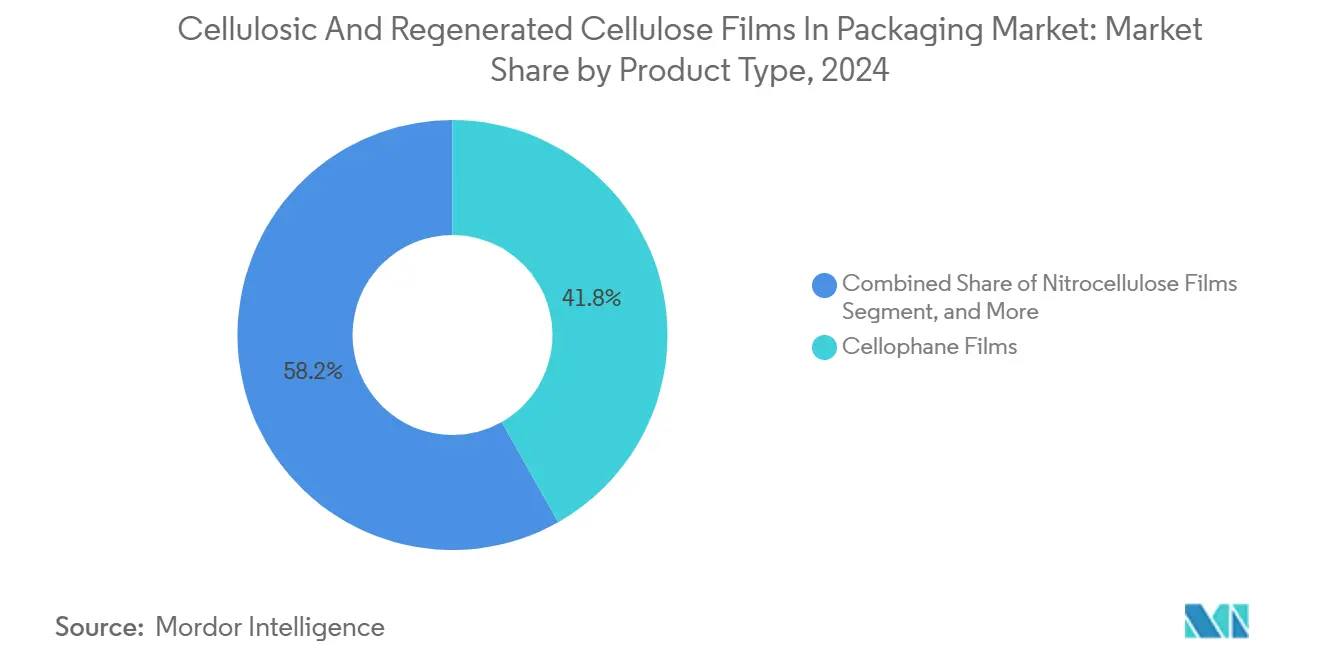

- By product type, cellophane captured 41.81% of the cellulosic and regenerated cellulose films in packaging market share in 2024.

- By thickness, the cellulosic and regenerated cellulose films in packaging market size for up to 20 micrometer are projected to advance at a 5.79% CAGR between 2025-2030.

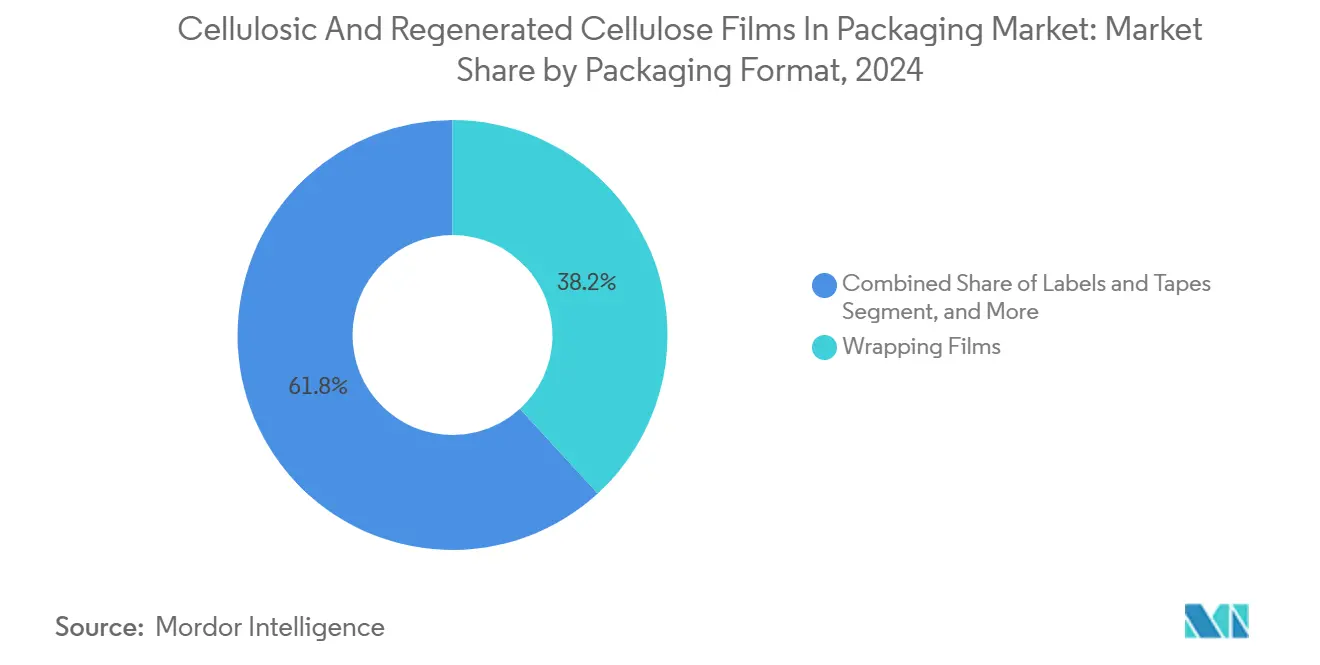

- By packaging format, wrapping films held 38.19% revenue share of the cellulosic and regenerated cellulose films in packaging market in 2024.

- By end-use industry, the cellulosic and regenerated cellulose films in packaging market size for personal care and cosmetics is projected to grow at a 5.63% CAGR through 2030.

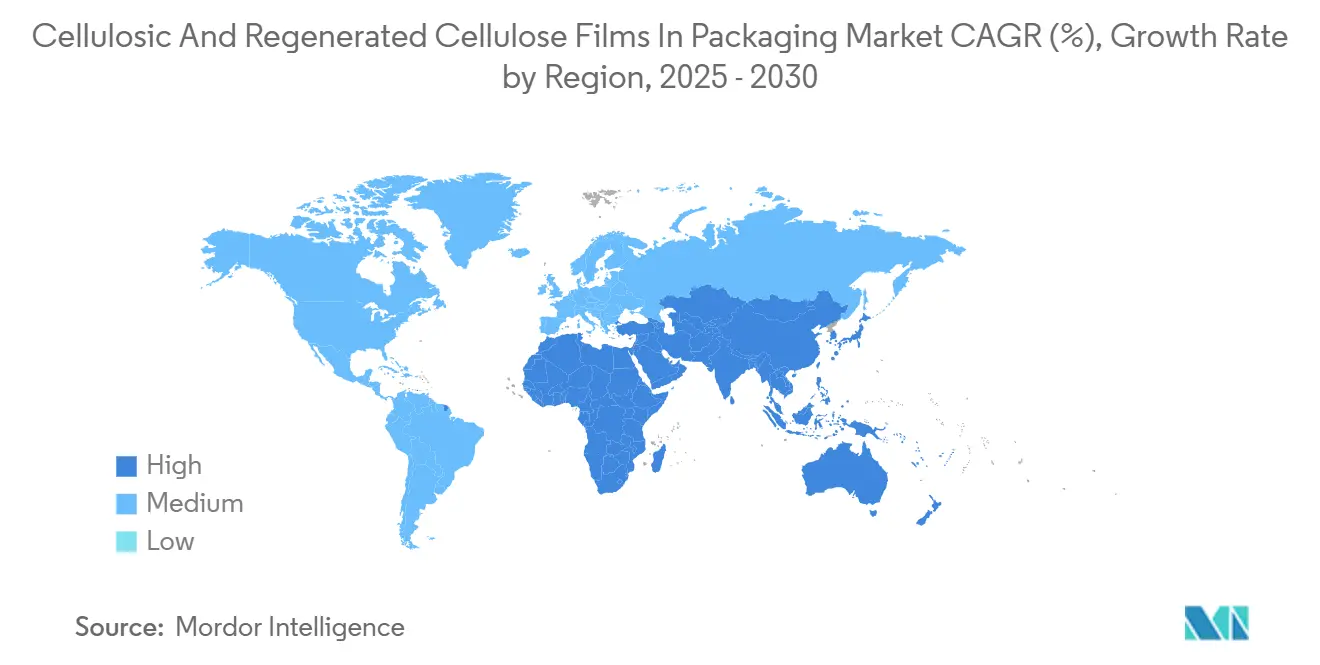

- By geography, Asia-Pacific accounted for 46.51% of the cellulosic and regenerated cellulose films in packaging market share in 2024.

Global Cellulosic And Regenerated Cellulose Films In Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on single-use plastics | +1.2% | Global, led by EU and North America | Short term (≤ 2 years) |

| Premium fresh-produce demand for compostable wraps | +0.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Superior oxygen and aroma barrier vs PVDC films | +0.9% | Global food packaging | Medium term (2-4 years) |

| Solvent-free coating tech boosts moisture resistance | +0.6% | Asia-Pacific manufacturing hubs, global adoption | Long term (≥ 4 years) |

| Brand 2030 circular-packaging pledges | +1.1% | Global, concentrated in developed markets | Medium term (2-4 years) |

| New dissolving-pulp capacity from agri-residue | +0.4% | Asia-Pacific and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans on Single-Use Plastics Drive Market Transformation

Immediate demand for cellulose films surged after the 2024 enforcement of the EU Single-Use Plastics Directive, mirrored by California’s SB 54 and Canada’s prohibition schedule.[1]California Department of Resources Recycling and Recovery, “SB 54 Implementation Guidelines,” calrecycle.ca.gov Legislators specify compostability benchmarks, such as ASTM D6400 and EN 13432, which cellulose substrates meet without the use of petrochemical additives. France extended restrictions to small fruit and vegetable packs, accelerating shifts from polyolefin wraps. Similar mandates in India and select Latin American markets widen the adoption base, enabling scale efficiencies that lower average production costs.

Premium Fresh-Produce Demand Elevates Compostable Packaging Requirements

Organic and premium produce suppliers differentiate through compostable films that quickly disintegrate in home-compost systems, a specification now embedded in Whole Foods Market procurement policies. European grocery chains Carrefour and Tesco issued comparable directives, locking in multi-year volume contracts that underpin investments in additional coating lines. Higher retail price points absorb incremental packaging costs, sustaining profitability for converters and film makers. As mainstream produce segments emulate premium positioning, order volumes for coated cellophane and nitrocellulose films continue to rise.

Superior Barrier Properties Challenge PVDC Film Dominance

Coated cellulose films demonstrate oxygen transmission rates below 1 cc/m²/day and water vapor rates under 2 g/m²/day, rivaling PVDC while eliminating chlorinated compounds. The switch reduces hazardous-waste classification concerns and aligns with brand pledges to remove halogenated materials. Nestlé and Unilever procurement guidelines already exclude PVDC in favored-material lists, giving coated cellulose substrates a competitive edge in snacks, confectionery and instant beverages.

Solvent-Free Coating Technologies Enhance Performance Economics

Water-based and UV-curable systems reduce manufacturing energy consumption by up to 20% and eliminate the need for solvent-recovery infrastructure, thereby reducing capital expenditures for retrofit lines.[2]Coating World Magazine, “Solvent-Free Coating Technologies in Packaging,” coatingsworld.com Plasma and corona treatments raise surface energy, promoting high-quality adhesion without compromising compostability. These gains close the cost gap with polyolefins and enable adoption in moisture-sensitive foods, pharmaceuticals, and nutraceuticals that previously required synthetic laminates. As major Asian facilities upgrade to solvent-free lines, global supply grows and price differentials narrow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price swings in dissolving pulp and energy | -0.9% | Global, especially Asia-Pacific | Short term (≤ 2 years) |

| Limited heat-sealability vs polyolefins | -0.6% | Global packaging lines | Medium term (2-4 years) |

| Consumer confusion on compostability certification | -0.4% | North America and Europe | Short term (≤ 2 years) |

| EU deforestation rules restrict FSC pulp supply | -0.5% | Europe and global FSC supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility Challenges Cost-Competitive Positioning

Dissolving pulp price spikes of 23% in early 2024 exposed cost sensitivity, as the feedstock forms up to half of the finished film's value. Energy surcharges further strained European and North American plants dependent on natural-gas grids. Weather-linked logistics delays compounded volatility, complicating fixed-price supply contracts. Producers counter with hedging, biomass boiler upgrades, and agricultural-residue feedstocks that diversify sourcing and dampen future price shocks.

Heat-Sealing Limitations Constrain Application Scope

Cellulose films require tighter temperature windows and specialized seal bars, which limits their compatibility with high-speed vertical form-fill-seal lines that are typically tuned for polyolefins.[3]Packaging Technology and Science, “Heat Sealing Characteristics of Cellulose Films,” wiley.com Equipment retrofits increase capital spending for converters, and fluctuations in moisture can compromise seal integrity. Emerging water-activated adhesives and ultrasonic sealing mitigate constraints but demand operator training and process adjustments that slow immediate adoption in mass-market categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cellophane Dominance Faces Nitrocellulose Disruption

Cellophane retained the largest 41.81% stake in the cellulosic and regenerated cellulose film market in 2024, backed by decades of converter familiarity and integrated supply chains. Nitrocellulose, however, achieves a robust 5.81% CAGR, driven by print-friendly surfaces and superior heat-seal properties that suit pharmaceutical blister packs and premium food packaging. The cellulosic and regenerated cellulose films in the packaging market size for nitrocellulose grades is projected to expand steadily as brand owners pursue high-graphic recyclable wrappers without PVDC layers. Other regenerated cellulose variants, such as viscose and lyocell, find niche use in luxury confectionery and personal-care secondary packs that command aesthetic appeal.

Competition within product categories now hinges on the differentiation of coating systems. Proprietary chitosan or alginate layers give cellophane new life in moisture-rich applications, while nitrocellulose formulators widen color-density ranges to satisfy brand design palettes. Tobacco packaging, still reliant on cellulose acetate, maintains a steady offtake despite falling cigarette volumes in Europe and North America, because mandated warning labels demand print clarity and low-migration inks. Collectively, these product-specific dynamics preserve a balanced revenue mix that mitigates over-dependence on any single film family.

By Thickness: Ultra-Thin Innovation Drives Market Evolution

Films in the 20-30 micrometer band captured 44.78% share of the cellulosic and regenerated cellulose films in the packaging market size in 2024, representing the sweet spot between barrier protection and cost for everyday snacks and bakery items. Up to 20 micrometers, however, accelerate at a 5.79% CAGR, as plasma-enhanced coatings allow for equivalent oxygen and water vapor barriers with less material. Lightweight packs result in lower shipping emissions and help meet corporate carbon-reduction targets outlined in many 2030 roadmaps. Converters incorporate these films into horizontal flow-wrap lines for candy and energy bars, lowering wrap weight per unit by up to 18%.

Thicker formats, ranging from 30-40 micrometers, remain relevant for stand-up pouches and bulk rice sacks that demand puncture resistance, while products exceeding 40 micrometers serve heavy-duty industrial components requiring anti-static properties. The cellulosic and regenerated cellulose films' packaging market share for thickness classes thus reflects a nuanced application landscape: thinner gauges for high-volume FMCG, mid-range thicknesses for premium foods, and thicker laminates for specialty or industrial goods. As ISO 527 dictates tensile benchmarks, specifiers can confidently transition between gauges without compromising quality.

By Packaging Format: Specialty Applications Accelerate Growth

Wrapping films continued to dominate the cellulosic and regenerated cellulose film market in packaging, accounting for a 38.19% share in 2024. However, laminates and specialty structures are poised to outpace this growth, with a 5.85% CAGR projected through the next decade. Two- and three-layer laminates combine cellulose with PLA or bio-based PU adhesives, providing high oxygen barriers for coffee and spices while maintaining full compostability. Modified-atmosphere pouches extend the shelf life of produce, reducing food waste costs for retailers.

E-commerce drives uptake of cellulose-based mailers and cushioning pads, leveraging biodegradability to offset consumer backlash against plastic bubble wrap. Label stock makers enjoy print reception comparable to synthetic facestocks yet achieve recyclability within paper streams, eliminating liner-waste disposal charges. Water-soluble grades serve detergent pods and ag-chem doses, erasing secondary packaging waste at the point of use. Such diversification lifts average selling prices and spreads volume risk across numerous end-markets.

By End Use Industry: Personal Care Drives Premium Growth

Food and beverage’s entrenched 57.62% contribution underscores continued reliance on high-clarity wraps, oven-reheat snack bags, and confectionery twist films. Nevertheless, personal care and cosmetics products advance at a 5.63% CAGR, reshaping the narrative of cellulosic and regenerated cellulose films in the packaging market toward luxury sustainability. Beauty brands deploy embossed cellophane sleeves and window cartons that telegraph eco-credentials to ingredient-conscious shoppers. Moisture-sensitive serums and solid shampoo bars utilize coated cellulose to eliminate PVDC liners while achieving comparable vapor barriers.

Pharmaceutical adoption intensifies following USP Class VI certification for selected cellulose acetate and nitrocellulose films, opening blister-pack lines that previously defaulted to PVC. Home and fabric-care innovators deploy water-soluble cellulose sachets for single-dose cleaners, aligning with consumer calls for plastic-free conveniences. Tobacco, despite volume stagnation, remains a steady niche due to stringent print and barrier criteria that few competing substrates match economically. Emerging electronics and industrial segments test anti-static cellulose wraps to secure static-sensitive components during shipment.

Geography Analysis

Asia-Pacific retained a 46.51% stake in 2024 due to mature dissolving-pulp ecosystems in China and Indonesia, state incentives for reducing plastic waste, and Japan’s stringent food safety standards. Local production hubs benefit from cost advantages derived from integrated forestry resources and scale economies on coating lines. Government programs, such as South Korea’s K-Green New Deal, subsidize research and development of compostable packaging, further accelerating regional supply. Multinational fast-moving consumer goods firms replicate global sustainability pledges in this geography, anchoring long-term demand for cellulose films.

The Middle East is projected to chart the fastest growth at 5.92% CAGR, buoyed by Saudi Arabia’s Vision 2030 and the United Arab Emirates' circular economy directives, which include compostables in government procurement scorecards. Rapid growth in packaged food output, tourism-driven food service, and modern retail creates incremental demand for high-barrier wraps and laminates. As local petrochemical majors diversify, joint ventures with Japanese and European film specialists establish pilot lines in Dammam and Jebel Ali, thereby shortening lead times for exports to African and South Asian markets.

North America and Europe continue to experience steady expansion, helped by extended producer responsibility clauses and consumer willingness to pay green premiums. The EU Corporate Sustainability Reporting Directive requires large enterprises to disclose their packaging footprints, steering converters toward cellulose-based solutions. Canada’s prohibition of six single-use plastic categories and multiple U.S. state bans collectively push grocers and QSR chains to trial coated cellophane sandwich wraps and salad tubs. Robust paper recycling networks in both regions simplify cellulose-film end-of-life pathways, reinforcing adoption.

Competitive Landscape

The cellulosic and regenerated cellulose films in the packaging industry are characterized by a mid-tier concentration, with the top five players controlling an estimated 55% of global capacity. Futamura Chemical leverages heritage cellophane technology and vertically integrated pulp assets in Japan and the U.K., enabling premium pricing in Europe’s delicatessen wrap segment. Innovia Films, a CCL Industries subsidiary, leverages recent water-based coating acquisitions to develop mozzarella and cured-meat barrier grades specifically suited for North American cold chains. Asian newcomers such as Weifang Henglian and Yibin Grace scale 20,000 tons per year lines, driving price competition in commodity gauges and stimulating process innovation among incumbents.

Strategic differentiation centers on solvent-free coaters, inline plasma treatment, and the integration of agri-residue pulp. Sappi’s South African mill retrofits aim to secure low-cost hemicellulose streams, while Eastman’s bespoke pharmaceutical film targets USP compliance niches. Patent activity in 2024 totaled 47 filings for barrier chemistries and seal-layer enhancements, with 63% originating from applicants in the Asia-Pacific region. Licensing deals enable smaller converters to access these coatings without incurring heavy R&D spending, thereby broadening the competitive set.

Despite moderate rivalry, buyers still face switching costs tied to packaging-line validation and regulatory clearances. This dynamic grants established suppliers margin resilience even as capacity grows. However, cost-driven offtakers such as private-label snack brands increasingly dual-source between incumbents and emerging Chinese producers, eroding single-supplier dominance and nudging average selling prices downward.

Cellulosic And Regenerated Cellulose Films In Packaging Industry Leaders

Futamura Chemical Co., Ltd.

CCL Industries Inc. (Innovia Films)

Eastman Chemical Company

Celanese Corporation (Clarifoil Films)

Daicel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Futamura Chemical announced a USD 45 million expansion of its United Kingdom cellophane plant, adding 15,000 tons in annual capacity and installing energy-efficient coating lines.

- August 2024: Innovia Films, a CCL Industries division, acquired a specialized water-based coating firm for USD 28 million to strengthen high-barrier food-wrap offerings.

- July 2024: Eastman Chemical Company introduced a new cellulose acetate grade certified to USP Class VI for pharmaceutical blister packs.

- June 2024: Sappi Limited committed USD 120 million to boost dissolving-pulp output in South Africa, incorporating agricultural-residue feedstocks.

Global Cellulosic And Regenerated Cellulose Films In Packaging Market Report Scope

| Cellophane Films |

| Cellulose Acetate Films |

| Nitrocellulose Films |

| Other Regenerated Cellulose Films |

| Up to 20 micrometer |

| 20-30 micrometer |

| 30-40 micrometer |

| Above 40 micrometer |

| Wrapping Films |

| Bags and Pouches |

| Labels and Tapes |

| Laminates and Others |

| Food and Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals |

| Tobacco |

| Home and Personal Care |

| Other End Use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Cellophane Films | ||

| Cellulose Acetate Films | |||

| Nitrocellulose Films | |||

| Other Regenerated Cellulose Films | |||

| By Thickness | Up to 20 micrometer | ||

| 20-30 micrometer | |||

| 30-40 micrometer | |||

| Above 40 micrometer | |||

| By Packaging Format | Wrapping Films | ||

| Bags and Pouches | |||

| Labels and Tapes | |||

| Laminates and Others | |||

| By End Use Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| Pharmaceuticals | |||

| Tobacco | |||

| Home and Personal Care | |||

| Other End Use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast value for cellulosic and regenerated cellulose films in packaging by 2030?

The market is projected to reach USD 1.12 billion by 2030.

Which product segment is growing fastest within cellulose-based packaging films?

Nitrocellulose films are advancing at 5.81% CAGR through 2030 thanks to printability and heat-seal advantages.

Why are ultra-thin cellulose films gaining traction?

Sub-20 µm gauges cut material weight while maintaining barrier performance, supporting brand lightweighting goals and lowering shipping emissions.

Which region currently leads in cellulose film consumption?

Asia-Pacific holds 46.51% share because of integrated pulp resources and proactive plastic-reduction policies.

What restrains broader adoption of cellulose films on high-speed lines?

Heat-seal requirements differ from polyolefins, necessitating equipment upgrades and precise process control to secure hermetic seals.

How are producers mitigating raw-material price swings?

Strategies include hedging pulp contracts, investing in agricultural-residue feedstocks and installing biomass boilers to offset energy volatility.

Page last updated on: