India CCTV Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

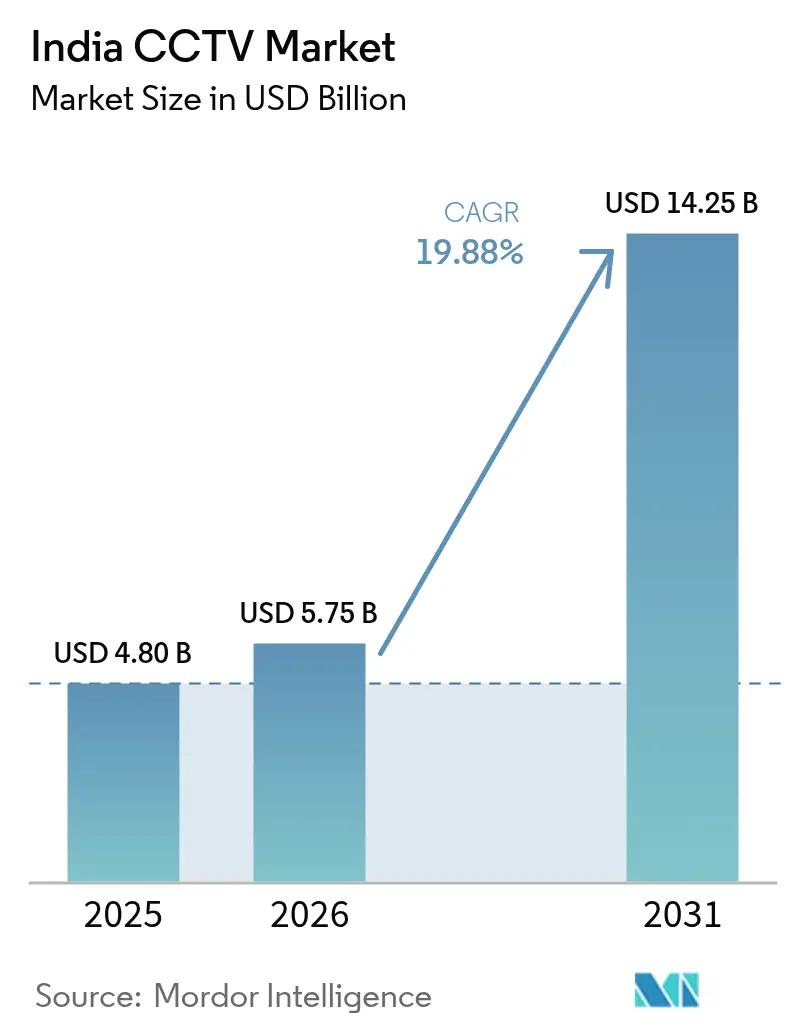

| Base Year Market Size (2025) | USD 4.8 Billion |

| Market Size (2026) | USD 5.75 Billion |

| Market Size (2031) | USD 14.25 Billion |

| Growth Rate (2026 - 2031) | 19.88% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India CCTV Market Analysis by Mordor Intelligence

The India CCTV market size was valued at USD 4.8 billion in 2025 and estimated to grow from USD 5.75 billion in 2026 to reach USD 14.25 billion by 2031, at a CAGR of 19.88% during the forecast period (2026-2031). Smart Cities Mission rollouts, mandatory public-safety regulations, and a push for indigenous manufacturing, spurred by the STQC certification mandate, fuel the current growth. These initiatives aim to enhance urban infrastructure, improve public safety, and promote self-reliance in technology manufacturing, creating a favorable environment for market expansion. Additionally, the government's focus on digital transformation and smart infrastructure development further accelerates the adoption of advanced technologies in urban planning and public safety systems.

With 76,000 cameras installed in 100 cities and ongoing upgrades at airports and metros, demand remains robust. The deployment of surveillance systems in urban areas and transportation hubs underscores the growing emphasis on security and operational efficiency, further driving the market's momentum. Moreover, the integration of advanced analytics and artificial intelligence in these systems is expected to enhance their effectiveness, contributing to sustained growth in the forecast period.

Key Report Takeaways

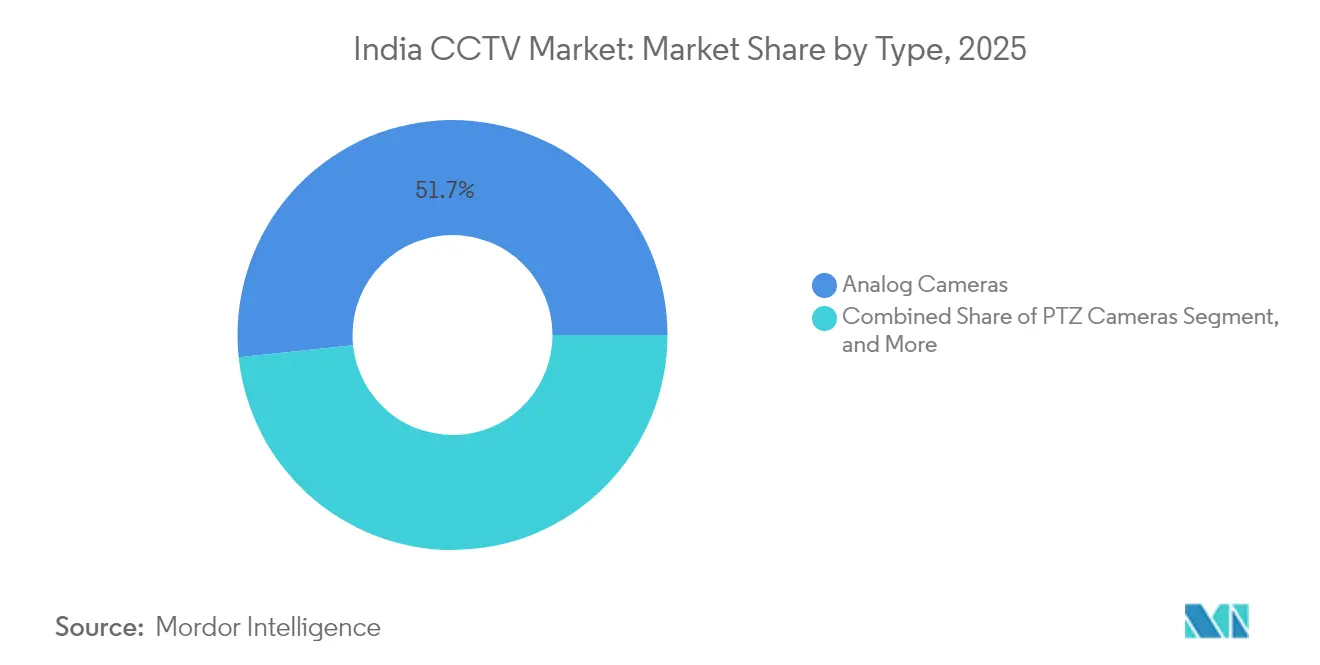

- By type, analog cameras controlled 51.65% of the India CCTV market share in 2025; AI-enabled cameras are projected to advance at a 20.55% CAGR through 2031.

- By end-user, government accounted for 38.05% revenue share in 2025, while residential and smart-home deployments are poised for a 20.15% CAGR to 2031.

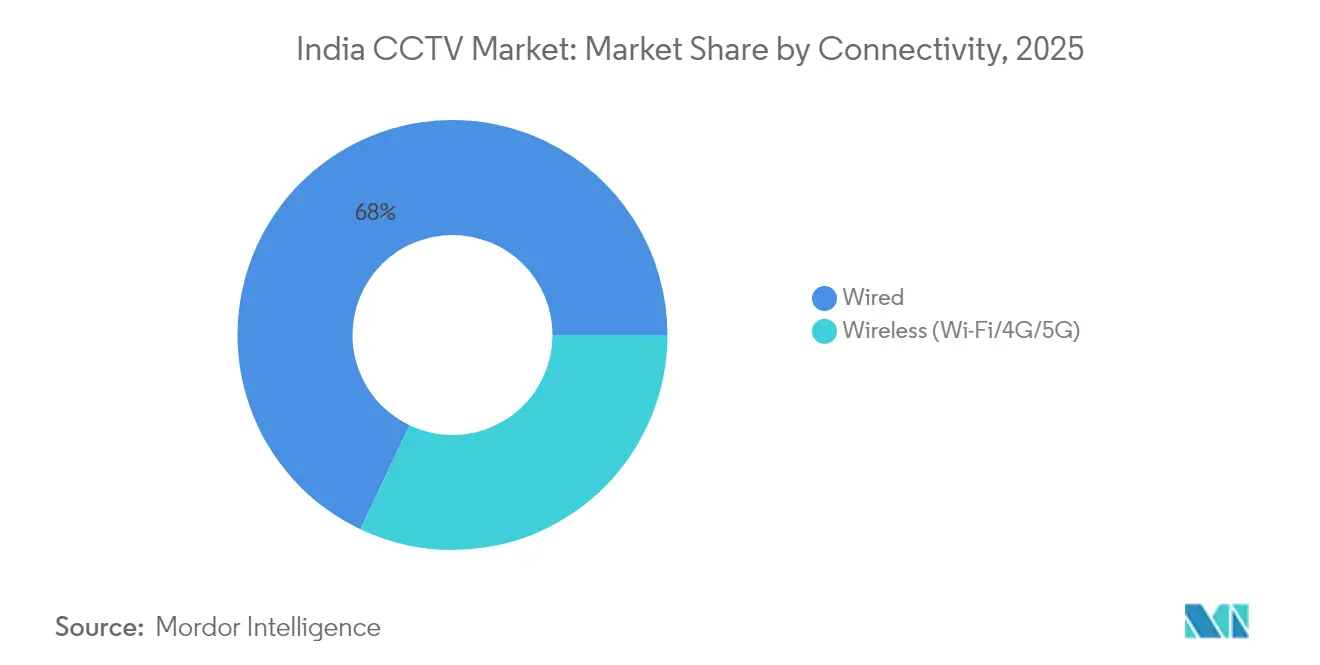

- By connectivity, wired solutions secured 67.95% of the India CCTV market size in 2025; wireless installations are forecast to rise at a 21.05% CAGR between 2026 and 2031.

- By region, North India led with 42.25% revenue share of the India CCTV market in 2025, whereas South India is estimated to witness a 20.40% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with India representing one among them. The global report on cctv market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

India CCTV Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government smart-city surveillance push | +4.2% | National, concentrated in 100 Smart Cities | Medium term (2-4 years) |

| Mandatory surveillance regulations for public spaces | +3.8% | National, with early adoption in metro cities | Short term (≤ 2 years) |

| Rapid infrastructure expansion of airports and metros | +3.1% | Metro cities, major transport hubs | Medium term (2-4 years) |

| AI-driven compliance and safety analytics adoption | +2.9% | Urban centers, government facilities | Long term (≥ 4 years) |

| Shift toward indigenous manufacturing post STQC/BIS norms | +2.7% | National manufacturing hubs | Medium term (2-4 years) |

| Solar-powered edge CCTV deployments in rural schemes | +1.8% | Rural India, border areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Smart-City Surveillance Push

The Smart Cities Mission elevated surveillance from reactive policing to predictive city management. With 90% of projects worth INR 1.44 trillion (USD 16.06 billion) finalized by March 2025, 76,000 cameras now integrate with command-and-control centers that funnel data to traffic, waste, and emergency modules. Standardized procurement favors suppliers able to meet interoperability benchmarks. Cloud-hosted platforms, such as Madhya Pradesh’s Integrated Control and Command Centre, illustrate resource optimization across utilities. The same backbone supports predictive analytics that pre-empt congestion and criminal activity, reinforcing steady demand across the India CCTV market.

Mandatory Surveillance Regulations for Public Spaces

State legislation is turning CCTV expenditure into a compliance item. Karnataka’s Public Safety Enforcement Act requires establishments with 500-plus monthly footfall to connect cameras to police networks, impacting roughly 10,000 Bengaluru outlets. Similar statutes follow Supreme Court directives for police-station coverage, exposing non-compliance gaps that spur immediate procurement. specifications standardize frame rates, encryption, and retention periods, elevating product quality while weeding out sub-standard imports.

Rapid Infrastructure Expansion of Airports and Metro Systems

Transport corridors are demanding biometric-ready surveillance. Delhi Metro introduced facial-recognition cameras on its Airport Express Line and will outfit 45 more stations in Phase 4. Mumbai Airport’s USD 1.2 billion upgrade includes integrated CCTV, full-body scanners, and self-service kiosks, all feeding a unified threat-detection layer. Noida International Airport opened with 24/7 AI-assisted monitoring, setting blueprints for future brownfield projects. Such projects lock in multi-year equipment and service contracts, bolstering volume across the India CCTV market.

AI-Driven Compliance and Safety Analytics Adoption

Artificial intelligence shifts video security toward real-time exception management. The Ministry of Road Transport and Highways pilots AI camera networks targeting a 50% cut in road fatalities by 2030. Academic trials using v8 achieved 98.6% accuracy in helmet-violation detection, proving readiness for mass deployment. Delhi Police is planning citywide facial recognition surveillance, while retrospective analytics upgrades unlock replacement demand for legacy analog estates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership for multi-site rollouts | -2.8% | National, particularly affecting SME segment | Short term (≤ 2 years) |

| Rising privacy and data-protection obligations (DPDP Act) | -2.1% | National, with stricter enforcement in metros | Medium term (2-4 years) |

| Cyber-security certification burden slowing launches | -1.9% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Semiconductor and import restrictions disrupting supply | -1.6% | National, concentrated in manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Multi-Site Rollouts

Large networks incur costs far beyond hardware, covering maintenance, bandwidth, and cloud storage that can outstrip initial capital outlay within three years. Dispersed sites often need satellite or private fiber links costing INR 50,000–100,000 yearly per location. High-definition video can generate several terabytes monthly, pushing enterprises toward edge storage or higher-tier cloud plans. Skilled labor shortages in tier-2 and tier-3 cities inflate installation fees and delay commissioning. These dynamics slow adoption among SMEs and may cap the expansion speed of the India CCTV market in less bankable segments.

Rising Privacy and Data-Protection Obligations (DPDP Act)

The Digital Personal Data Protection Act 2023 demands explicit consent, robust encryption, and local grievance mechanisms, requirements that add compliance costs for end users.[1]Nishith Desai Associates, “India’s Digital Personal Data Protection Act, 2023,” nishithdesai.com Cross-border vendors must set up domestic processing or risk penalties, narrowing the supplier field. Consent capture in public venues is difficult, driving interest in privacy-by-design architectures such as pixelation or selective recording. Pending Data Protection Board guidelines create uncertainty, prompting some buyers to delay procurement. When biometric data are processed, additional safeguards amplify hardware and software costs, trimming near-term growth headroom.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Analog Dominance Faces AI Disruption

Analog units retained a 51.65% share of the India CCTV market in 2025, supported by cost-sensitive public-sector tenders and legacy coaxial cabling. IP models reached 40.55% share thanks to remote monitoring and PoE convenience. PTZ cameras contributed 5.85%, addressing large-area coverage in airports and oil terminals. AI-enabled smart cameras, although niche, are forecast to expand at a 20.55% CAGR, directly lifting the India CCTV market size for intelligent endpoints.

Low acquisition cost and ease of swap-out keep analog in play, yet STQC rules that took effect in April 2025 push buyers toward cyber-secure, upgradeable devices. Domestic firms such as Aditya Infotech and Prama Hikvision now bundle on-device analytics and secure boot to comply with the Ministry of Electronics mandates. AI-ready models thereby erode analog headroom, reshaping future India CCTV market share trajectories.

By End-User Verticals: Government Leadership Drives Market Evolution

Government accounted for 38.05% of the India CCTV market in 2025, propelled by Safe City and border-security funds. Industrial and manufacturing sites followed at 28.75% on the back of workplace-safety mandates. BFSI branches and ATMs secured a 14.10% share under Reserve Bank audit norms.

Residential and smart-home demand is the fastest-growing at 20.15% CAGR, supported by sub-USD 25 Wi-Fi camera kits sold via e-commerce. Transportation and logistics clock in at 8.65% share but gain from e-commerce warehousing. Retail and hospitality spend on people-counting analytics, while healthcare and education favor privacy-compliant edge storage. Such varied use cases extend the India CCTV market size across both public and private domains.

By Connectivity: Wired Infrastructure Meets Wireless Innovation

Wired solutions claimed 67.95% India CCTV market share in 2025, anchored by PoE reliability for 24/7 public-safety feeds. Gigabit switching costs have fallen, reinforcing this hold.

Wireless deployments, however, are climbing at a 21.05% CAGR, buoyed by 5G, Wi-Fi 6, and solar-powered edge appliances. Rural schemes use LTE back-up to circumvent fiber gaps, and mesh topologies lower trenching costs. Edge compute trims bandwidth by relaying only flagged events, making wireless a viable alternative for new smart-city phases and boosting future India CCTV market share in connectivity-flexible segments.

Geography Analysis

North India led with a 42.25% share in 2025, underpinned by Delhi’s 700,000-camera network and Punjab’s border grids. West India contributed 18.10% on the strength of Gujarat’s public-safety acts and Maharashtra’s housing boom.

South India leads growth with a 20.40% CAGR outlook. Bengaluru’s police, aviation, and metro agencies jointly deploy facial recognition under an INR 496 crore (USD 55.2 million) budget. Foxconn’s 1,170-camera housing complex and the Rs 27,000 crore (USD 301.0 million) Brand Bengaluru corridor guarantee ongoing procurement. Tamil Nadu’s industrial corridors standardize AI-ready surveillance, accelerating adoption through local integrators.

West India secured an 18.10% share on the back of Ahmedabad’s 25,000-camera grid that helped it top the 2025 safety index. Maharashtra’s housing policy embeds CCTV as a planning prerequisite, expanding residential uptake. East India, at 13.15%, benefits from West Bengal’s perimeter-intrusion sensors and Odisha’s facial recognition corridor at Puri temple. Central India closes at 7.85%, yet Bhopal’s AI-equipped border nodes and India’s first smart-city control center underscore latent upside. Uniform STQC compliance across zones ensures consistent baseline quality, favoring certified vendors across the India CCTV market.

Competitive Landscape

Moderate consolidation characterizes the India CCTV market, where the top five suppliers held about 55% share in 2024. CP Plus (Aditya Infotech) led with 20.8%, leveraging the world’s third-largest CCTV plant in Andhra Pradesh and a 1,000-strong distributor web. Its July 2025 IPO, oversubscribed 106 × and listing at a 50% premium, evidences investor faith in localized supply chains.[3]Moneycontrol Markets Desk, “Aditya Infotech Shares Debut at 50% Premium,” moneycontrol.com

Honeywell teamed with VVDN to release the India-made 50-Series cameras that bundle real-time motion and facial analytics, meeting STQC cybersecurity norms.[4]Honeywell India, “Made in India: New Security Cameras,” honeywell.com Bosch divested its Building Technologies arm to Keenfinity India for INR 595 crore to tighten its focus on specialized security platforms. Prama Hikvision opened an INR 500 crore Vasai factory targeting 1.5 million units monthly with 50% localization, a hedge against possible import blacklists.

Strategic alliances now pivot on silicon access and AI stacks. Aditya Infotech is linked with L&T Semiconductor to co-develop edge-AI chipsets. Dixon Technologies swapped its 50% JV stake for a 6.5% equity slice in Aditya Infotech, securing downstream demand. Foreign majors chase high-value niches, Axis for critical infra, Hanwha for airport analytics, while domestic newcomers seek opportunities in solar-powered rural kits. Cyber-secure firmware, STQC labels, and AI features remain the decisive differentiators across the India CCTV market.

India CCTV Industry Leaders

HIKVISION Digital Technology Co. Ltd (Hikvision India)

Dahua Technology India Pvt. Ltd

Aditya Infotech Ltd (CP Plus)

Godrej Security Solutions

Honeywell Commercial Security

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Honeywell and VVDN introduced India-designed 50 Series cameras with embedded cybersecurity and facial-recognition functions.

- July 2025: Aditya Infotech closed an INR 1,300 crore IPO to fund debt retirement and capacity expansion to 17.2 million units per year.

- May 2025: Government enforced STQC certification for all internet-connected CCTV devices, including source-code escrow and factory audits.

- January 2025: Bosch sold its Video, Access and Intrusion business to Keenfinity India for INR 595 crore, aligning with global restructuring.

India CCTV Market Report Scope

Closed-circuit television (CCTV), also known as videotape surveillance, is used to send a signal to a specific site using a limited number of monitors. In India, the demand for CCTVs is surging due to privacy concerns and innovative city initiatives. The study encompasses market drivers and challenges, as well as enterprise attractiveness.

The India CCTV Market Report is Segmented by Type (Analog Cameras, IP Cameras, PTZ Cameras, AI-enabled Smart Cameras), End-user Verticals (Government, Industrial and Manufacturing, BFSI, Transportation and Logistics, Residential and Smart Homes, Retail and Hospitality, Healthcare and Education), Connectivity (Wired, Wireless), and Geography (North India, South India, East India, West India, Central India). The Market Forecasts are Provided in Terms of Value (USD).

| Analog Cameras |

| IP Cameras (Non-PTZ) |

| PTZ Cameras |

| AI-enabled Smart Cameras |

| Government |

| Industrial and Manufacturing |

| BFSI |

| Transportation and Logistics |

| Residential and Smart Homes |

| Retail and Hospitality |

| Healthcare and Education |

| Other End-user Verticals |

| Wired |

| Wireless (Wi-Fi/4G/5G) |

| North India |

| South India |

| East India |

| West India |

| Central India |

| By Type | Analog Cameras |

| IP Cameras (Non-PTZ) | |

| PTZ Cameras | |

| AI-enabled Smart Cameras | |

| By End-user Verticals | Government |

| Industrial and Manufacturing | |

| BFSI | |

| Transportation and Logistics | |

| Residential and Smart Homes | |

| Retail and Hospitality | |

| Healthcare and Education | |

| Other End-user Verticals | |

| By Connectivity | Wired |

| Wireless (Wi-Fi/4G/5G) | |

| By Region | North India |

| South India | |

| East India | |

| West India | |

| Central India |

Key Questions Answered in the Report

What is the current size of the India CCTV market?

The market stood at USD 5.75 billion in 2026 and is forecast to hit USD 14.25 billion by 2031.

Which camera type dominates sales in India?

Analog cameras led with a 51.65% share in 2025, though AI-enabled smart cameras show the fastest growth trajectory.

How fast is residential adoption growing?

Residential and smart-home installations are expanding at an 20.15% CAGR through 2031 as camera prices fall and DIY kits proliferate.

What regulations impact CCTV procurement the most?

The Digital Personal Data Protection Act 2023 and mandatory STQC certification drive compliance costs and influence supplier selection.

Page last updated on: