Cast Iron Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 33.91 Billion |

| Market Size (2031) | USD 42.22 Billion |

| Growth Rate (2026 - 2031) | 4.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

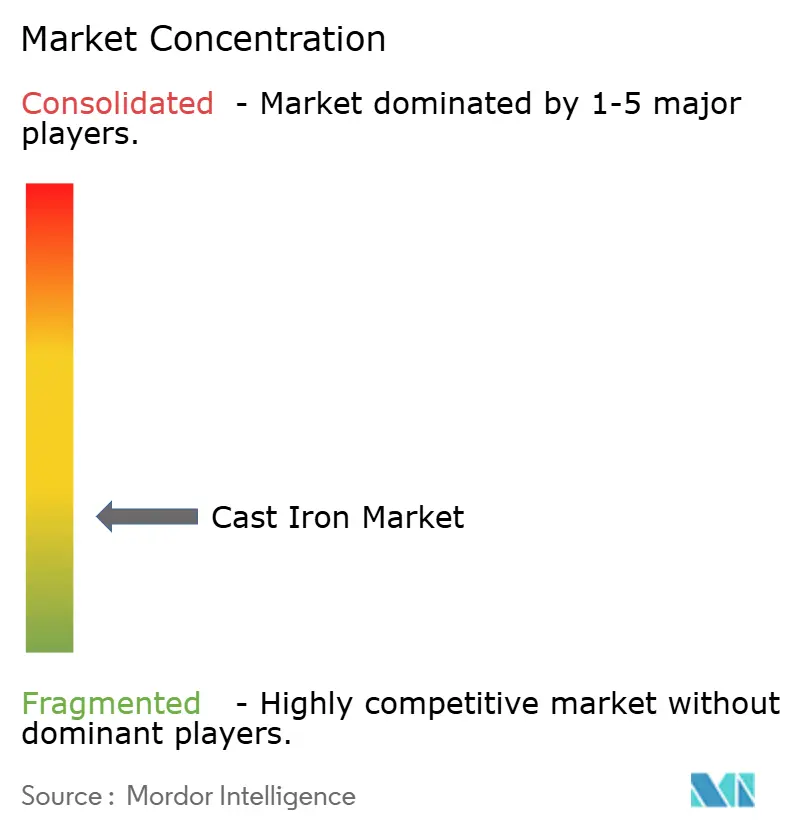

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cast Iron Market Analysis by Mordor Intelligence

The Cast Iron Market size is expected to grow from USD 32.56 billion in 2025 to USD 33.91 billion in 2026 and is forecast to reach USD 42.22 billion by 2031 at a 4.48% CAGR over 2026-2031. Forward momentum rests on resilient automotive power-train demand, record infrastructure outlays in the Middle East, and wind-energy buildouts that specify ductile grades for turbine drivetrains. Process innovations, most notably 3D sand-printing, shorten prototype lead times and help foundries protect margins even as iron-ore oversupply presses raw-material prices downward. Regional expansion concentrates in Asia-Pacific, where India’s steel roadmap and China’s pivot to austempered ductile iron offset slowing residential construction. Conversely, lightweighting and volatile coke prices temper growth in Europe and North America, compelling producers to consolidate and automate to stay cost-competitive.

Key Report Takeaways

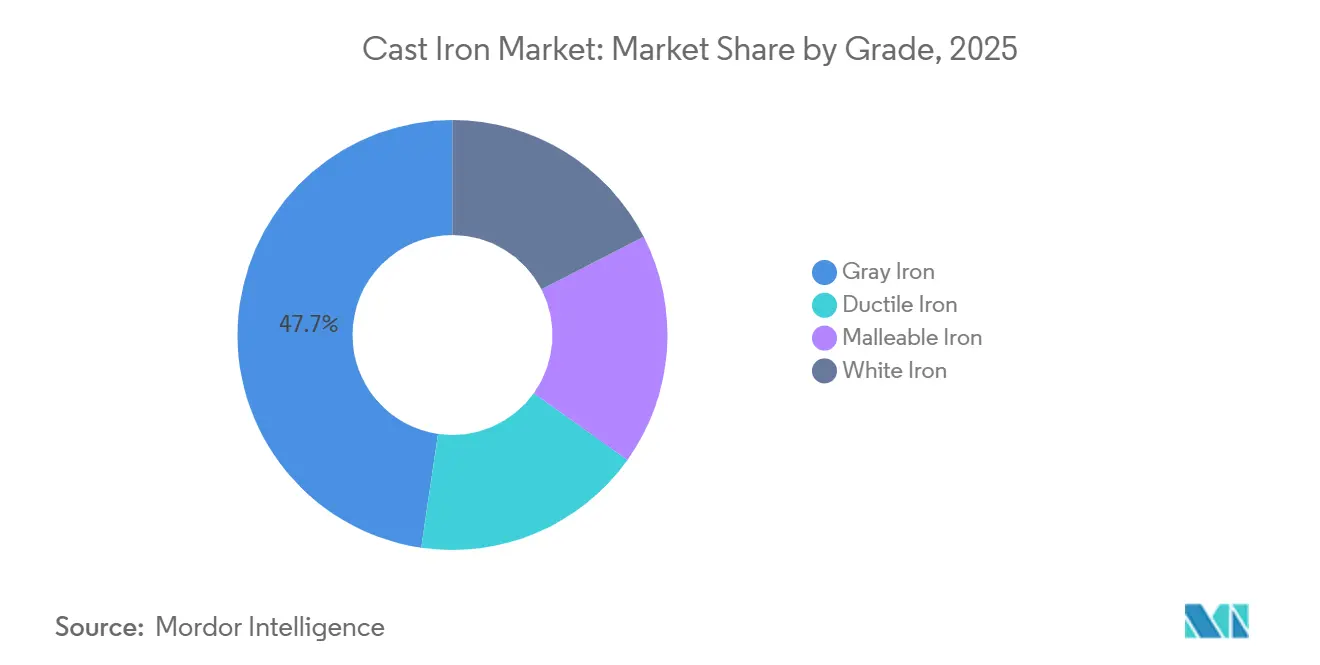

- By grade, gray iron led with 47.68% volume in 2025, while malleable iron is projected to advance at a 5.15% CAGR through 2031.

- By casting process, sand casting retained 31.59% of the 2025 cast iron market share, whereas centrifugal casting will post the fastest 5.30% annual rise to 2031.

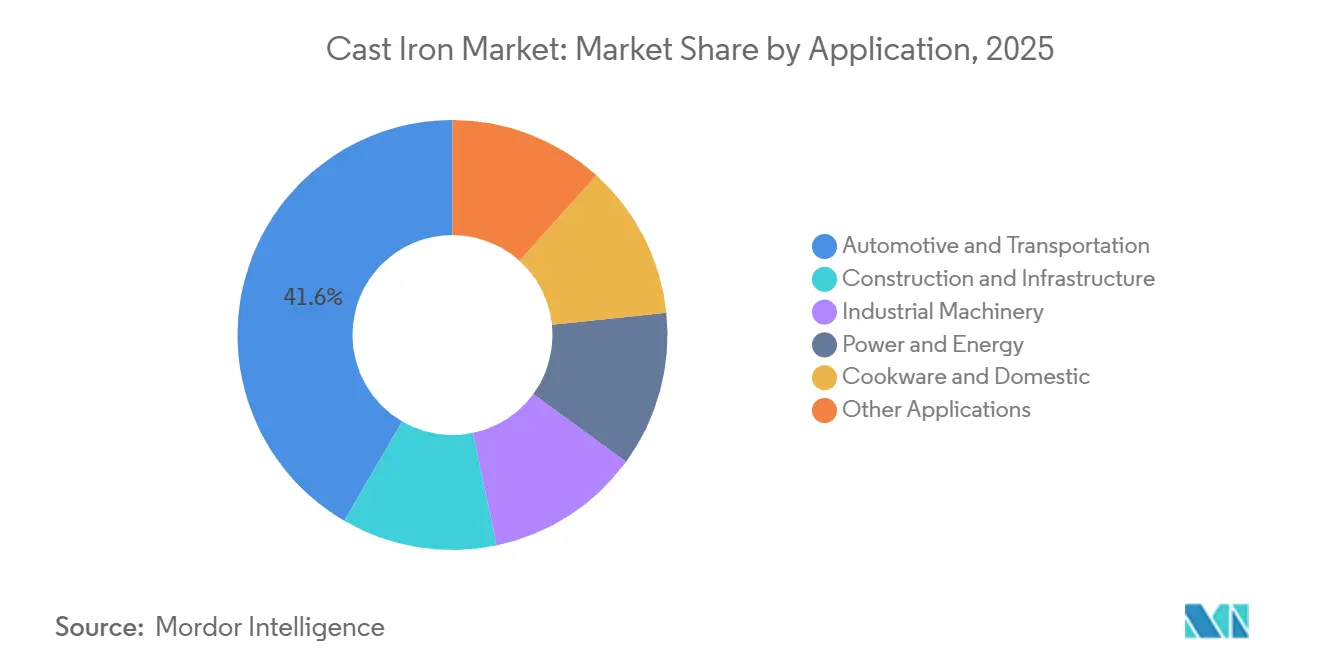

- By application, automotive and transportation accounted for 41.62% revenue in 2025, yet power and energy uses are forecast to expand at a 5.82% CAGR through 2031.

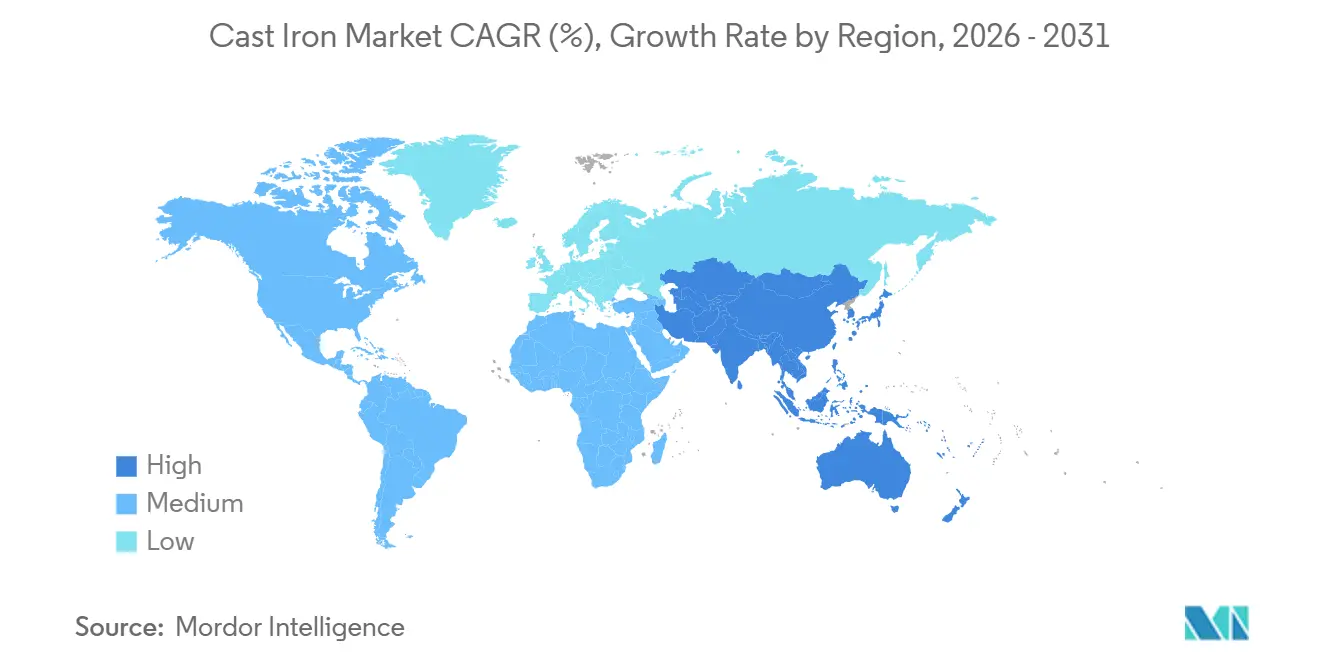

- By geography, Asia-Pacific captured 38.81% value in 2025 and is anticipated to grow at a 5.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cast Iron Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Significant Demand from the Automotive Sector | +1.2% | Global, with concentration in APAC (China, India, Japan) and North America | Medium term (2-4 years) |

| Expansion in Construction and Infrastructure | +1.0% | APAC core, spill-over to Middle East (Saudi Arabia, UAE) and South America (Brazil) | Long term (≥ 4 years) |

| Growth in Industrial Machinery Investments | +0.8% | North America and Europe, emerging gains in India and Southeast Asia | Medium term (2-4 years) |

| Adoption of Ductile Iron for High-Strength Parts | +0.7% | Global, early adoption in wind energy (Europe, North America) and water utilities (Middle East, APAC) | Long term (≥ 4 years) |

| 3-D Sand-Printing Enabling Short Production Runs | +0.5% | North America and Europe foundry clusters, pilot deployments in China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Significant Demand from the Automotive Sector

In 2025, the automotive and transportation sectors accounted for a 41.62% share of total sales, with the pace of electrification playing a pivotal role. Toyota forecasts that by 2030, battery-electric vehicles will only make up a part of global sales. This projection ensures continued demand for components like gray-iron blocks, ductile-iron crankshafts, and brake rotors. Similarly, the U.S. Environmental Protection Agency’s endorsement of renewable diesel and eFuels bolsters the longevity of heavy-duty internal combustion engines, supporting the demand for ductile-iron cylinder liners[1]Sean Kilcarr, “Electric Truck Sales Remain Sluggish Despite EPA Push,” thetrucker.com . Furthermore, regional investments highlight suppliers' strategic positioning. They're gearing up for an increase in export demand, particularly in hybrid-vehicle suspension and axle castings.

Expansion in Construction and Infrastructure

Saudi Arabia's Vision 2030 agenda, bolstered by large-scale pipeline projects, is set to boost the national demand for centrifugal ductile pipes. Utilities favor ductile iron due to its superior pressure tolerance and corrosion resistance. This preference extends to oil-and-gas gathering lines throughout the Middle East. Concurrent renewal initiatives in Brazil and the UAE are generating additional orders for sand- and centrifugal-cast fittings. This trend is further propelling the adoption of the cast iron market in these emerging regions.

Growth in Industrial Machinery Investments

In 2024, U.S. expenditures on metal-working machinery increased, marking growth since 2020. Simultaneously, capital expenditures in the mining sector surged year-over-year. These investments have led to heightened orders for gray-iron machine bases and white-iron wear parts. Meanwhile, Europe and Japan are witnessing a similar trend, particularly in high-precision gearboxes and compressors. This has resulted in a steady mid-single-digit boost for the cast iron market, even as segments catering directly to consumers show signs of softening.

Adoption of Ductile Iron for High-Strength Parts

Wind-turbine builders are turning to ductile iron for their 3-MW main shafts, each weighing in at around 25 tons and capable of handling multimegawatt torque. Meanwhile, in China, there's a push to adopt austempered ductile iron, a move aimed at replacing the pricier forged steel and ensuring compliance with ISO 1083 standards. Foundries boasting integrated heat-treatment capabilities are seizing this lucrative niche, managing to elevate their average selling prices, even in the face of stiff competition from gray iron volumes.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy and Coke Prices Inflate Costs | -0.6% | Global, acute in Europe and North America with limited coal access | Short term (≤ 2 years) |

| Light-Weight Materials Substituting Cast Iron | -0.9% | North America and Europe automotive sectors, spreading to APAC | Medium term (2-4 years) |

| Volatile Iron-Ore Tariffs and Trade Barriers | -0.5% | Global, concentrated impact on China, Vietnam, South Korea exporters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy and Coke Prices Inflate Costs

In 2024, North American foundry coke prices increased. In contrast, Chinese prices fluctuated. This fluctuation has tightened margins for furnaces that depend on cupola melting. Meanwhile, in 30 countries, scrap-export taxes have heightened reliance on pig iron. This shift undermines the advantages of using recycled feedstock in a circular economy. Additionally, energy price swings are not only jeopardizing fixed-price supply contracts but also hastening consolidation among smaller producers.

Light-Weight Materials Substituting Cast Iron

Battery-electric vehicles (BEVs) are replacing numerous gray-iron engine components, leading to a shift in mass savings towards aluminum die-castings and composites. Global BEV penetration is forecast to grow significantly by 2030, gradually diminishing the cast iron market for power-train parts. Just as the aerospace sector's adoption of titanium has set a precedent, commercial-vehicle manufacturers are increasingly following suit to extend their range.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Gray Iron Anchors Volume, Malleable Surges

Gray iron held a 47.68% share of the 2025 volume thanks to its low cost and vibration-damping qualities in engine blocks and machine bases, anchoring the cast iron market size for high-volume commodities. Malleable iron is forecast to grow at 5.15% to 2031 as farm-equipment makers adopt it for axle housings that need greater ductility but at lower cost than ductile grades.

Malleable elongation between 5% and 10% suits drawbars and valve bodies where gray iron is too brittle. Ductile iron, offering high tensile strength, captures wind-turbine hubs and municipal pipe. White iron, with high hardness, limits itself to wear parts, keeping its cast iron market share minimal. China’s austempered ducts provide high yield but require lengthy heat-treat cycles that concentrate output in specialized shops.

By Casting Process: Sand Casting Dominates, Centrifugal Accelerates

Sand casting represented 31.59% of the 2025 value and underpins much of the global cast iron market through green-sand flexibility that spans sub-kg brackets to multi-ton turbine hubs[2]“Additive Manufacturing for Metal Casting,” American Foundry Society, afsinc.org. Centrifugal casting, however, will lift at 5.30% CAGR on water-utility pipe replacements that must satisfy AWWA C151 pressure ratings up to 350 psi.

Shell-mold and investment processes split precision niches. Shell-mold parts like pump impellers hit tolerances, but resin adds cost per kg. Investment wax patterns achieve tighter control yet stretch cycle times to 8-12 weeks. Printed sand molds erase pattern costs and create a fresh lane where small-batch prototypes once defaulted to machined billet, strengthening the cast iron market long tail.

By Application: Automotive Leads, Power Sector Surges

Automotive and transportation commanded 41.62% of 2025 demand, supported by hybrids that still use gray-iron blocks and ductile-iron crankshafts. Power and energy rise the quickest at 5.82% CAGR as each 3-MW turbine consumes significant tons of ductile components in shafts and bedplates, augmenting the cast iron market size in renewables.

Upgrades in construction are leaning heavily on ductile pipes for water grids in megacities. Notably, projects in Saudi Arabia are set to double the national tonnage by 2030. In the industrial machinery realm, U.S. metalworking investments have surged, leading to renewed orders for gray-iron bases and white-iron liners. While premium cookware remains a niche market, enameled Dutch ovens consistently command high price points, emphasizing brand prestige over volume sales.

Geography Analysis

The Asia-Pacific secured 38.81% revenue in 2025 and is projected to deliver a 5.34% CAGR through 2031, fueled by India’s path to 300 million t steel and China’s shift to high-strength austempered ductile grades. Rising infrastructure and renewable-energy commitments funnel orders to regional foundries even amid trade tensions.

North America benefits from tariffs that incentivize domestic pipe and auto casting, while USMCA rules channel volume toward Canadian and Mexican plants connected to Detroit supply chains. Europe leverages wind-energy growth and the Carbon Border Adjustment Mechanism to preference local low-emission foundries, though energy prices curb margins.

Middle East and Africa show outsized infrastructure pull: Saudi water pipelines, UAE desalination lines, and Nigeria mining parts accelerate ductile-pipe and white-iron liner consumption. South America’s demand ties to Brazilian farm-equipment exports and Argentinian grain cycles, offering mid-single-digit upside for the cast iron market.

Competitive Landscape

The cast iron market is fragmented. Technology is a key separator: 3D sand-printing installations enable low-volume prototypes that command higher margins, whereas pattern-dependent shops lose such orders. White-space opportunities include austempered ductile iron for renewable energy and malleable iron for electric-vehicle battery trays, neither yet dominated by incumbents. Patent filings in nodularization run below fifty per year, so tacit metallurgical expertise, rather than formal IP, drives competitive edge in the cast iron market.

Cast Iron Industry Leaders

WAUPACA FOUNDRY, INC.

Tupy

Grede LLC

Proterial

GF Casting Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Xinxing Ductile Pipe announced that it had partnered with Kazakhstan to supply cast iron for pipe and fittings production projects.

- March 2024: Brakes India announced USD 70 million for a new Aguascalientes, Mexico smelting plant that will create 700 jobs, with phase 1 completion slated for January 2026.

Global Cast Iron Market Report Scope

Cast iron is a versatile ferrous alloy primarily composed of iron (Fe), carbon (C) (typically 2.0–4.5%), and silicon (Si) (1–3%). It is defined by its low melting point, excellent fluidity, and high casting integrity, which allow it to be molded into complex shapes. The microstructure, influenced by cooling rates and alloying elements, determines its mechanical properties, resulting in a durable yet non-malleable material.

The cast iron market is segmented by grade, casting process, application, and geography. By grade, the market is segmented into gray iron, ductile iron, malleable iron, and white iron. By casting process, the market is segmented into sand casting, centrifugal casting, shell-mold casting, investment casting, and other processes. By application, the market is segmented into automotive and transportation, construction and infrastructure, industrial machinery, power and energy, cookware and domestic, and other applications. The report also covers the market size and forecasts for the market in 26 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Gray Iron |

| Ductile Iron |

| Malleable Iron |

| White Iron |

| Sand Casting |

| Centrifugal Casting |

| Shell-Mold Casting |

| Investment Casting |

| Other Processes |

| Automotive and Transportation |

| Construction and Infrastructure |

| Industrial Machinery |

| Power and Energy |

| Cookware and Domestic |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Egypt | |

| Nigeria | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Gray Iron | |

| Ductile Iron | ||

| Malleable Iron | ||

| White Iron | ||

| By Casting Process | Sand Casting | |

| Centrifugal Casting | ||

| Shell-Mold Casting | ||

| Investment Casting | ||

| Other Processes | ||

| By Application | Automotive and Transportation | |

| Construction and Infrastructure | ||

| Industrial Machinery | ||

| Power and Energy | ||

| Cookware and Domestic | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Egypt | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the cast iron market today, and where is it headed by 2031?

The cast iron market size reached USD 32.56 billion in 2025, is valued at USD 33.91 billion in 2026, and is forecast to reach USD 42.22 billion by 2031 at a 4.48% CAGR.

Which material grades are growing the fastest?

Malleable iron is projected to expand at 5.15% a year to 2031 as agricultural and light-equipment makers favor its higher ductility at lower cost than ductile iron.

Which region is leading growth?

Asia-Pacific dominates with 38.81% revenue in 2025 and a projected 5.34% CAGR as India ramps up steel output and China upgrades renewable-energy castings.

How are foundries coping with shorter prototype cycles?

Many install 3D sand-printing systems that cut mold lead times from weeks to days, allowing economical runs below 50 units and safeguarding margins on complex parts.

Page last updated on: