Iron Ore Pellets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

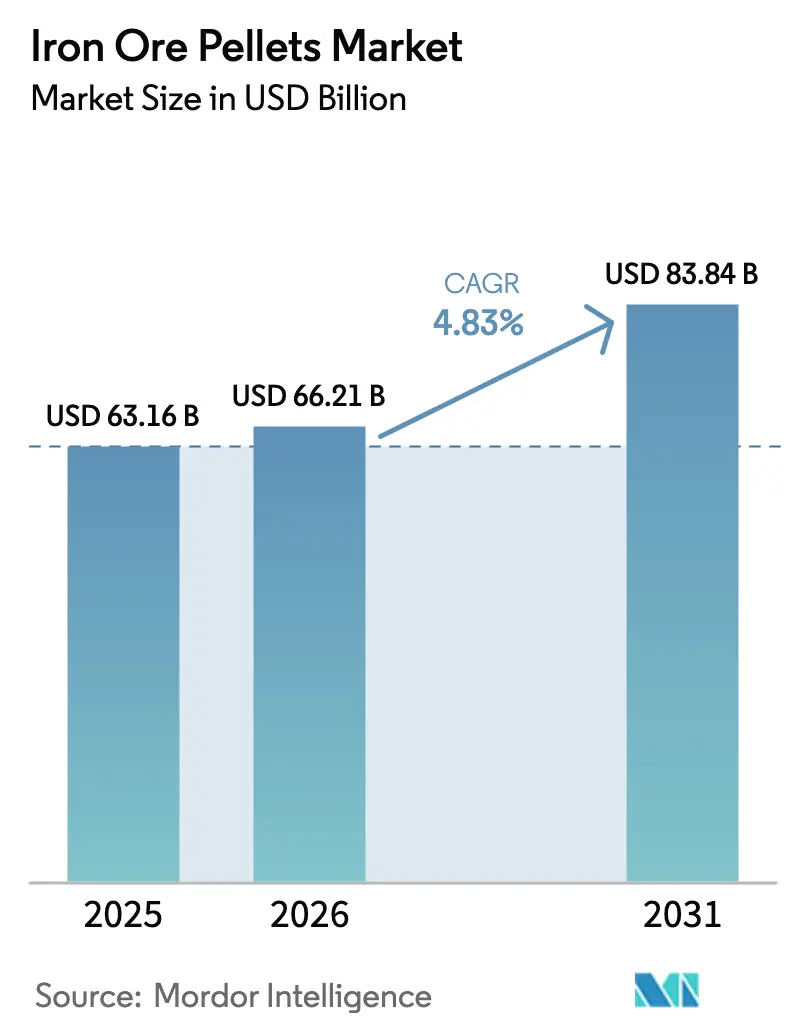

| Market Size (2026) | USD 66.21 Billion |

| Market Size (2031) | USD 83.84 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

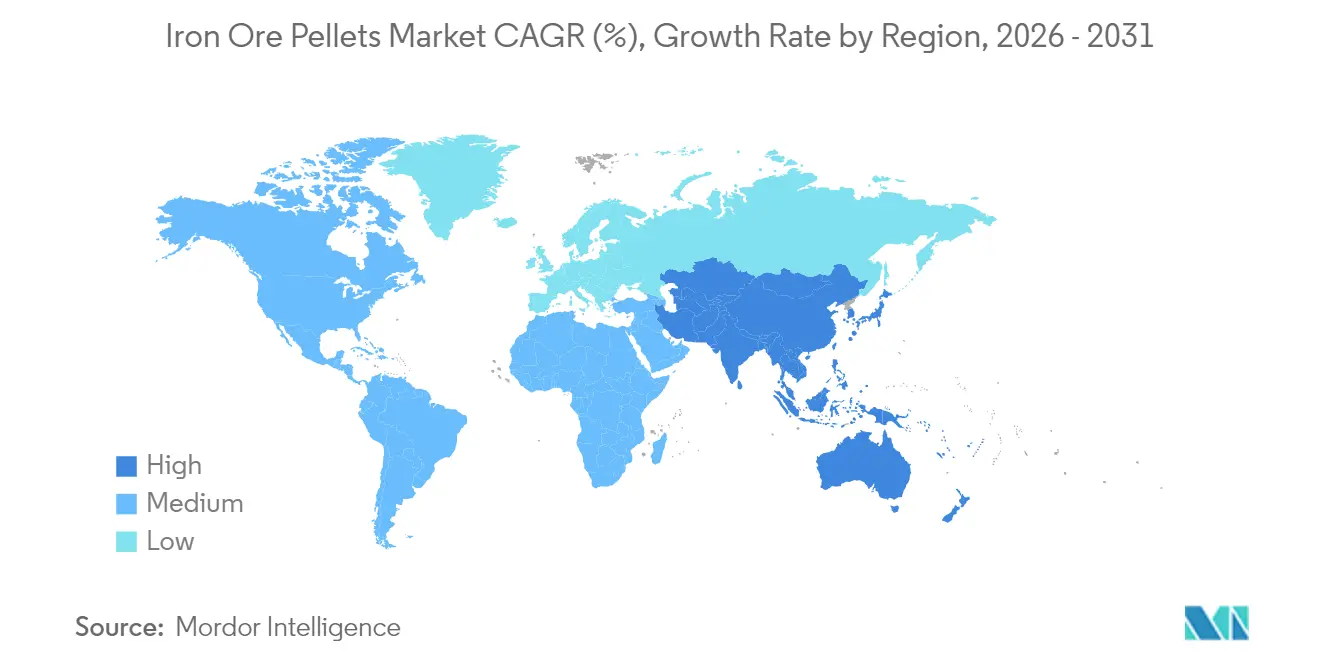

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

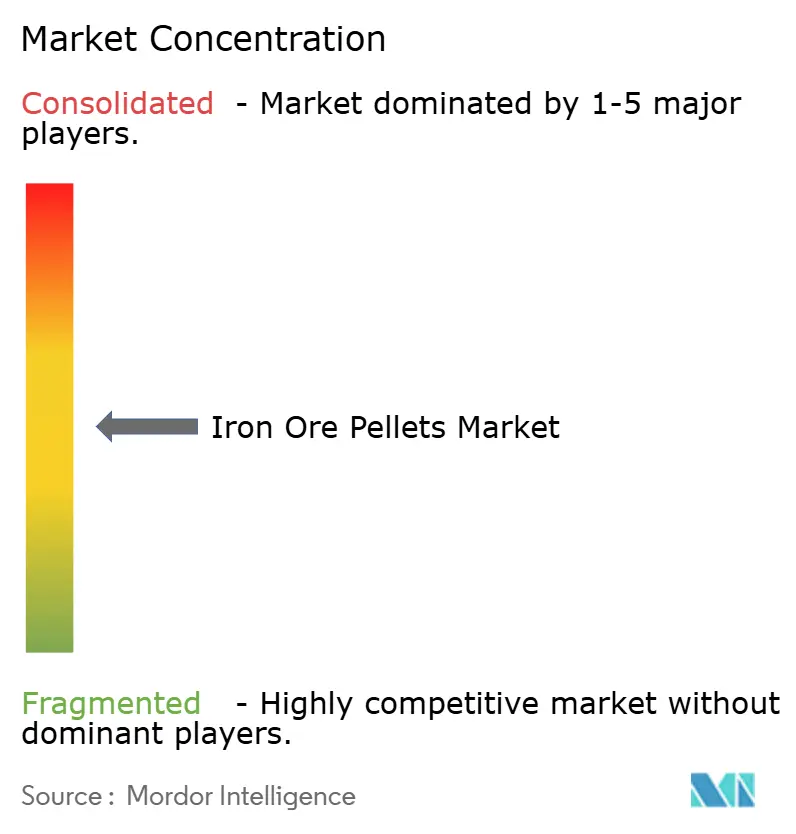

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iron Ore Pellets Market Analysis by Mordor Intelligence

The iron ore pellets market size is expected to grow from USD 63.16 billion in 2025 to USD 66.21 billion in 2026 and is forecast to reach USD 83.84 billion by 2031 at 4.83% CAGR over 2026-2031. Robust steel demand recovery, the gradual shift toward hydrogen‐ready direct reduction iron (DRI) routes, and tightening environmental regulations that favor high-grade pelletized feedstock are the primary forces behind this growth. Asia-Pacific anchors consumption because China continues to operate the world’s largest blast furnace fleet while India accelerates capacity additions under its national infrastructure push. Parallel momentum comes from the Middle East and North America, where low-carbon DRI capacity is scaling and pulling scarce DR-grade pellets into premium territory. Competitive dynamics remain moderately concentrated; leading miners such as Vale, Rio Tinto and Cleveland-Cliffs leverage integrated mining-to-pelletizing chains, whereas mid-tier producers increasingly pursue consolidation to secure high-grade resources. Technology choices are also evolving, with hybrid or low-carbon induration systems gaining ground as operators seek to cut fuel costs and CO₂ emissions.

Key Report Takeaways

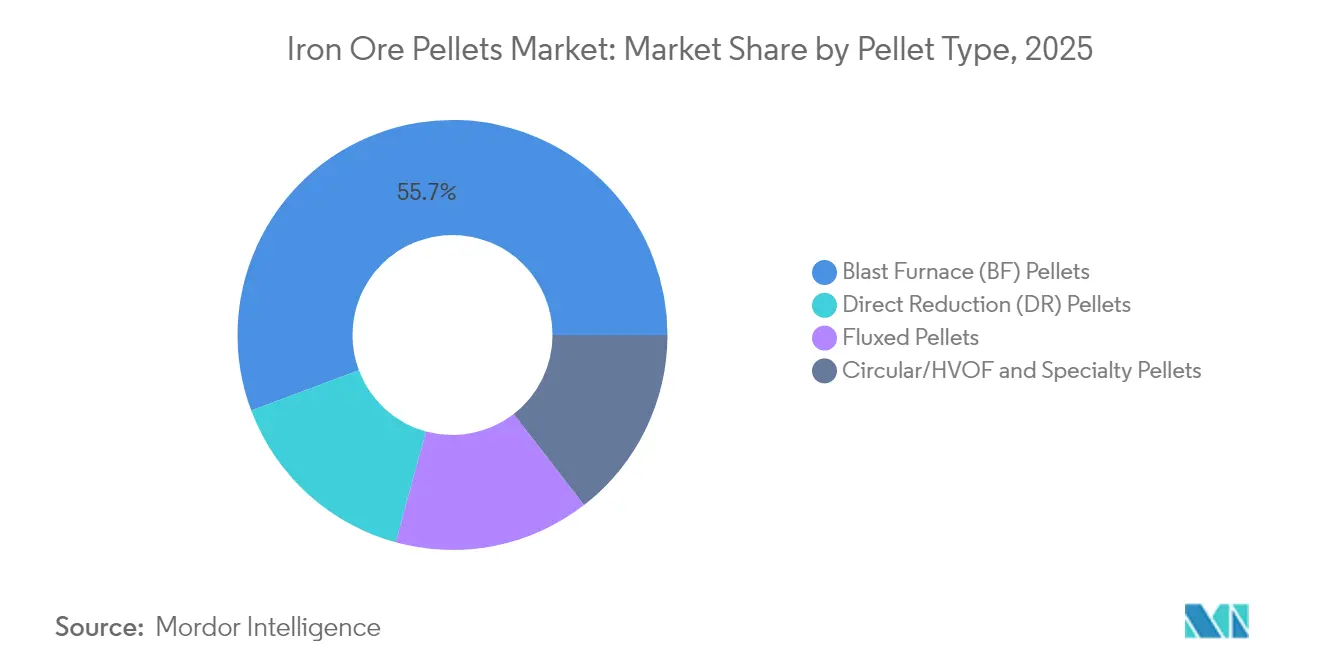

- By pellet type, blast furnace pellets led with 55.72% revenue share in 2025, while direct reduction pellets are forecast to expand at a 5.28% CAGR through 2031.

- By grade, hematite accounted for a 59.68% share of the iron ore pellets market size in 2025, whereas super-high-grade pellets are forecast to grow at a 5.39% CAGR to 2031.

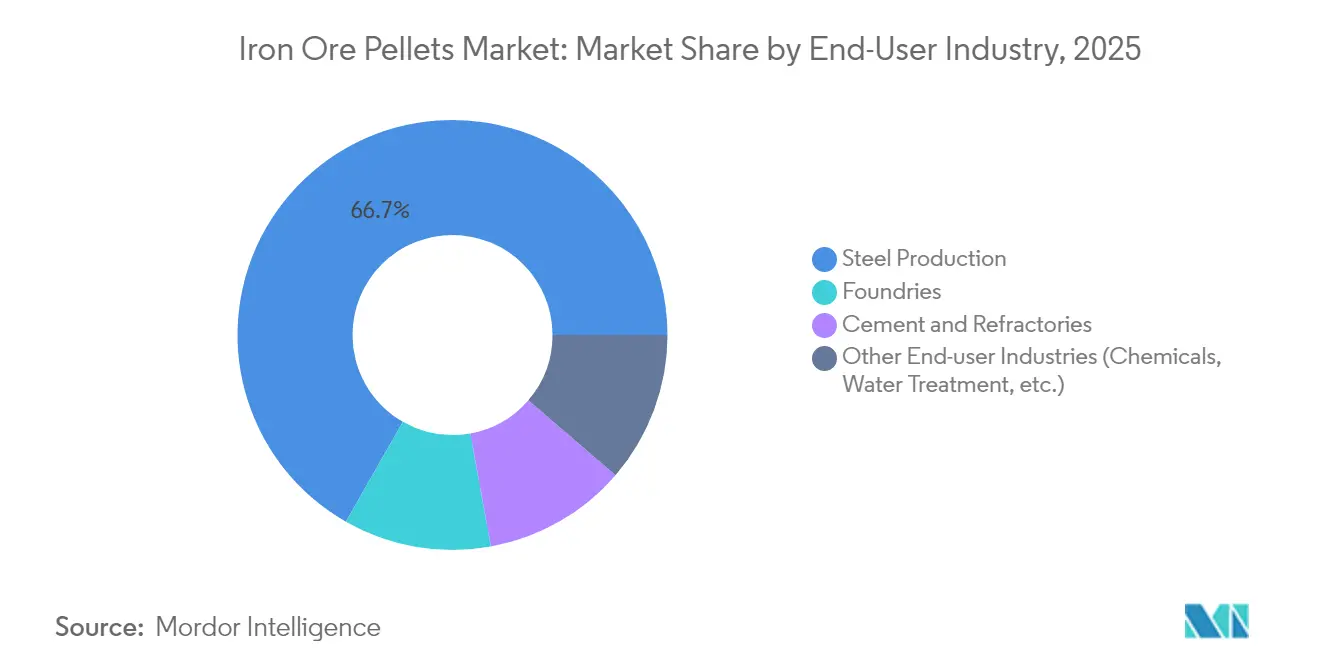

- By end-user industry, steel production held 66.74% of the iron ore pellets market share in 2025, and is advancing at a 5.44% CAGR through 2031.

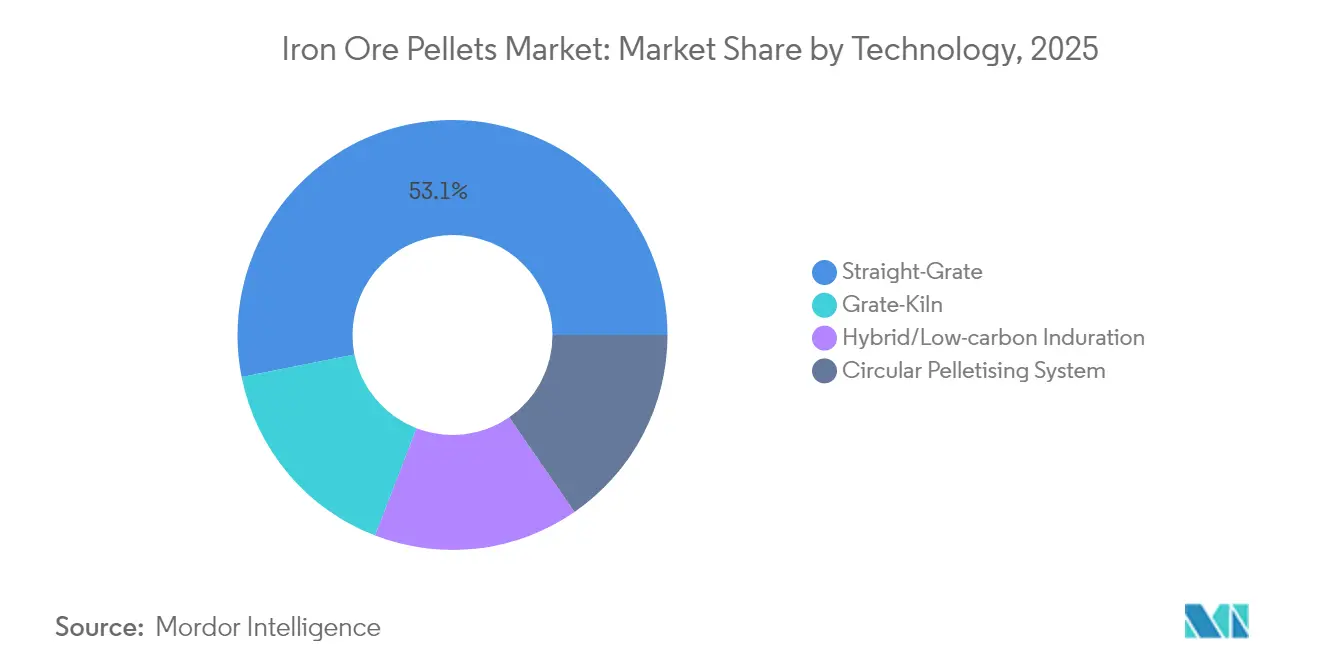

- By technology, straight-grate systems captured 53.12% share in 2025, while hybrid/low-carbon induration is projected to register the fastest 5.73% CAGR to 2031.

- By geography, Asia-Pacific dominated with 50.96% share in 2025 and is expected to expand at a 5.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Iron Ore Pellets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from blast-furnace steelmaking | +1.80% | Global, with concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Growing Direct Reduction/Electric Arc Furnace pellet usage | +1.20% | Global, led by MENA, North America, and emerging Asian markets | Long term (≥ 4 years) |

| Supportive Government Policies for Low-carbon Steel Production | +0.90% | North America, Europe, with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Advances in pellet-induration technology | +1.10% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Increase in Hydrogen-based direct reduction iron project pipeline | +0.80% | Europe, Middle East, with expansion to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand from Blast-Furnace Steelmaking

Global blast furnace fleets keep the iron ore pellets market anchored because the installed base in China alone exceeds 1.17 billion t of crude steel capacity. India’s steel consumption is projected to climb, reinforcing the appetite for blast-furnace grade pellets in South Asia. Pellet optimization reduces coke rates and marginally lowers emissions, which helps operators meet interim climate targets before hydrogen infrastructure becomes mainstream. Consequently, premium pellets remain a practical near-term decarbonization lever even inside ostensibly carbon-intensive production routes. This paradox underpins stable volume off-take for traditional pellet producers while the sector plots its longer-term transition.

Growing Direct Reduction/Electric Arc Furnace Pellet Usage

Consumption of DR-grade pellets is rising at a 5.36% CAGR because DRI furnaces can integrate renewable electricity and hydrogen, thus offering a long-term decarbonization pathway. The MENA region already accounts for 45% of global DRI output, helped by abundant gas and solar resources[1]Institute for Energy Economics and Financial Analysis, “MENA Poised to Lead Global Green Iron,” ieefa.org . ArcelorMittal’s Dofasco project in Canada will add 2.5 million t of hot DRI capacity using Energiron technology, signaling a broader migration toward hydrogen-ready furnaces. However, only 4% of global iron ore qualifies as DR-grade (greater than 67% Fe), creating supply tightness that lifts price premiums. Producers with access to super-high-grade ore deposits therefore enjoy structural pricing advantages as green steel scales.

Supportive Government Policies for Low-Carbon Steel Production

Government intervention is accelerating low-carbon investment across the iron ore pellets industry. The EU implemented its Carbon Border Adjustment Mechanism (CBAM) in January 2024, and the UK will follow in 2027, effectively embedding a carbon price into pellets entering European supply chains[2]European Commission, “Implementing Regulation 2023/1773,” eur-lex.europa.eu . In the United States, the Department of Energy awarded Cleveland-Cliffs USD 575 million to build hydrogen-ready DRI plants targeting a 50% carbon-intensity cut. China released national greenhouse-gas accounting guidelines for steel in January 2025, signaling that even the largest producer is tightening oversight. These converging policies reward early movers that invest in cleaner pelletization technologies and penalize high-carbon assets, thereby reshaping capital allocation across the value chain.

Increase in Hydrogen-Based Direct Reduction Iron Project Pipeline

A surge of commercial hydrogen projects in Europe and the Middle East underpins long-term pellet demand. Projects such as H2 Green Steel in Sweden and Emirates Steel’s partnership with Masdar aim to commission large-scale hydrogen DRI capacity post-2027, which will intensify the need for super-high-grade pellets. Early project finance decisions indicate that secure access to DR-grade feedstock is a gating factor for investor confidence, thereby incentivizing miners to fast-track grade-enhancement projects like Kumba Iron Ore’s UHDMS processing at Sishen.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Iron-ore price volatility | -0.70% | Global, with particular impact on import-dependent regions | Short term (≤ 2 years) |

| High energy and Carbon Dioxide footprint of induration | -0.50% | Global, with stricter enforcement in Europe and North America | Medium term (2-4 years) |

| Competition from high-quality scrap | -0.90% | Global, with concentration in developed markets and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Iron-Ore Price Volatility

Spot prices remain sensitive to Chinese macro-policy signals and new supply additions. Rio Tinto’s Simandou asset is slated to inject 120 million t annually from 2025, equivalent to roughly 5% of seaborne supply, creating downward pressure on benchmark fines. Price swings squeeze margins at smaller pelletizers lacking long-term offtake contracts and have already spurred consolidation, exemplified by Cleveland-Cliffs’ acquisition of Stelco in 2024. Investment decisions on new pellet lines are often deferred during low-price phases, risking future supply shortages when demand rebounds.

High Energy and Carbon Dioxide Footprint of Induration

Conventional straight-grate induration uses natural gas or pulverized coal, making pellets one of the most energy-intensive steps in the metallics chain. The US EPA tightened hazardous-air-pollutant limits for taconite plants in March 2024, triggering retrofit costs at multiple Minnesota sites[3]EPA, “NESHAP: Taconite Iron Ore Processing,” federalregister.gov . South Australian gas-based DRI proposals face feedstock risks because annual demand could reach 30-40 PJ against a constrained domestic supply. The International Maritime Organization’s looming carbon levy on bunker fuel will also inflate freight costs for long-distance ore shipments. Collectively, these pressures elevate operating costs and accelerate the pivot toward lower-carbon induration methods, but the transition burden falls unevenly across producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pellet Type: Direct Reduction Drives Premium Demand

In 2025, blast furnace pellets accounted for 55.72% of the iron ore pellets market share thanks to entrenched BF steel capacity in Asia-Pacific and parts of Europe. Yet the segment’s growth is slower than the overall iron ore pellets market because operators face rising carbon costs. Direct reduction pellets, by contrast, are forecast to post a 5.28% CAGR and increasingly command premium prices as hydrogen-ready furnaces expand in MENA and North America. The iron ore pellets market size for direct reduction pellets is projected to widen materially by 2031, reflecting both volume growth and a widening quality premium tied to DR-compatible chemistry. Fluxed pellets satisfy niche demand for blast furnace chemistry optimization, while circular, HVOF, and specialty products cater to foundries and advanced alloy makers. Vale’s USD 282.9 million Louisiana briquette project illustrates how miners are expanding DR-grade capacity to capture this high-margin window. The resulting competitive landscape favors integrated miners that can guarantee chemical consistency and low residuals demanded by modern DRI units.

Further expansion in DR-grade supply hinges on ore-grade enhancement and beneficiation. Premium deposits remain geographically concentrated, and logistical constraints can deter incremental capacity in remote regions. Consequently, buyers often enter long-term contracts with miners to secure DR-grade feed, contributing to a relatively tight market structure that supports sustained price premiums even through commodity cycles.

By Grade: Super-High-Grade Pellets Command Premium Growth

Hematite pellets maintained the lion’s share at 59.68% in 2025 because of the abundance of hematite ore across Brazil, Australia, and South Africa. Despite this dominance, demand is gradually tilting toward super-high-grade (greater than 67% Fe) pellets to reduce gangue burden and energy intensity in both blast furnaces and DRI modules. The super-high-grade category is forecast to grow at a 5.39% CAGR, outpacing aggregate iron ore pellets market growth. Iron ore pellets market size for super-high-grade products is expected to compound especially sharply in Europe and the Middle East, where green steel projects require ultra-low residuals. Kumba Iron Ore’s ZAR 11.2 billion UHDMS upgrade will lift the share of premium ore from 18% to 55%, underscoring the strategic value of higher-grade output. Magnetite pellets, though smaller in volume, offer superior reducibility and magnetic separation advantages that position them for specialized steel applications.

The grade-based shift strengthens the bargaining power of miners controlling premium resources. Supply scarcity shields margins against raw-material price cycles, while lower-grade suppliers face steeper discounts as carbon pricing expands. Investors increasingly scrutinize grade consistency and ore-quality transformation projects when allocating capital, suggesting that grade enhancement is becoming a decisive value lever for pellet producers.

By End-User Industry: Steel Production Maintains Dominance

Steelmakers consumed 66.74% of all pellets in 2025 and remain the fastest-growing customer base at 5.44% CAGR to 2031 as infrastructure, automotive, and energy transition projects unfold worldwide. This concentration means the iron ore pellets market size is tightly correlated with crude steel output and regional capacity cycling. Foundries represent a smaller but stable niche, requiring narrow pellet size distributions and low silica levels to ensure casting precision. Cement and refractories constitute additional outlets, using pellets mainly as flux or colorant, yet volumes here are marginal compared with steel. Other downstream sectors, such as water treatment, consume specialty pellets in comparatively minor quantities.

Because steel production remains both the largest and most dynamic demand center, pellet producers pursue geographic alignment with new EAF and DRI plant announcements. Indian capacity additions and North American EAF conversions underpin robust forward order books. However, the rising share of scrap—expected to reach up to half of metallic input by 2050—may cap long-term volume growth, although advanced grades still command a premium for high-strength or low-impurity steels.

By Technology: Hybrid Systems Lead Innovation Adoption

Straight-grate lines retained a 53.12% share in 2025 because they represent the incumbency across legacy facilities worldwide. Nonetheless, hybrid or low-carbon induration is forecast to post a 5.73% CAGR, benefitting from regulatory credits and lower fuel intensity. Grate-kiln technology, widely used for DR-grade pellets, continues to capture upgrades in Brazil and India because of its superior metallurgical control. Circular pelletizing systems fill niche roles where compact footprints and lower capital costs are required. The iron ore pellets market size allocated to hybrid equipment is anticipated to rise sharply as operators retrofit existing furnaces with renewable electricity, plasma heating, or hydrogen burners.

Technology selection is increasingly driven by lifecycle emissions rather than initial capex. For instance, Tata Steel Nederland’s pilot pellet pot testing facility will allow rapid prototyping of low-carbon flux additions and firing regimes. Producers adopting next-generation induration early are better positioned to negotiate green-steel premiums, highlighting technology adoption as a competitive differentiator.

Geography Analysis

Asia-Pacific held 50.96% of global iron ore pellets market share in 2025, reflecting China’s vast blast-furnace capacity and India’s double-digit pellet production growth. Iron ore pellets market size in the region is projected to expand at 5.63% CAGR, mirroring continued industrialization and infrastructure development. China’s output discipline policies create periodic volatility, yet the scale of domestic demand sustains large pellet off-take volumes. India posted 284 million t of iron ore output in 2024 and exceeded 100 million t of pellet production, signalling its growing self-sufficiency and export potential. Japan and South Korea, though smaller in volume, require consistent high-grade pellets for advanced automotive steels, while emerging ASEAN markets form the next wave of demand as they commission new EAF capacity.

North America constitutes a mature but strategically pivotal arena where vertical integration and low-carbon policy incentives shape market evolution. Cleveland-Cliffs operates five active mines with 28 million long-t pellet capacity and enjoys 22% regional share, giving it scale benefits and proximity to Great Lakes steel mills. Federal grants toward hydrogen-ready DRI plants bolster future DR-grade pellet demand, and U.S. Steel has earmarked USD 150 million for DR-grade pellet upgrades in Minnesota. Canada solidifies its resource position through projects such as Champion Iron’s Kami development in partnership with Nippon Steel and Sojitz.

Europe’s pellet landscape is defined by decarbonization imperatives. LKAB’s approval to switch from pellets to carbon-free sponge iron indicates a strategic pivot toward higher-value, lower-carbon products. The EU CBAM forces importers to internalize carbon costs, likely favoring local DR-grade suppliers with low upstream emissions. Tata Steel’s Dutch unit is in dialogue with the government on hydrogen DRI deployment funded by a multiyear INR 10,000 crore annual capital plan. Although Europe’s share of global pellet volumes is smaller than Asia-Pacific’s, its regulatory stringency accelerates innovation, making it a reference market for low-carbon pellet technologies.

South America remains an export-oriented supplier, with Vale’s Carajás complex targeting production of 310-320 million t in 2024 and embarking on a USD 12 billion investment program to raise output by 13% through 2030. Samarco ramped pellet and fines output 91% year-on-year in Q2 2025, reaching the highest level since operations resumed after the Fundão dam failure. These expansions ensure steady feed to customers across Europe, MENA and Asia.

The Middle East & Africa leverages natural-gas abundance to emerge as a global DRI hub. Emirates Steel, Qatar Steel and Algerian Qatari Steel are each expanding capacity, while Saudi Arabia and the UAE explore blue and green hydrogen DRI projects. Local access to DR-grade pellets remains critical; hence, regional mills secure long-term supply contracts with Brazilian and South African miners. Ongoing beneficiation projects in Mauritania and Liberia may diversify supply over the next decade.

Competitive Landscape

The iron ore pellets market is moderately fragmented, with large integrated miners controlling premium ore deposits and captive pellet capacity. Vale recorded 310-320 million t of iron ore output in 2024 and allocates USD 12 billion for Carajás debottlenecking, reinforcing its status as the largest pellet supplier. Cleveland-Cliffs commands a significant share of the North American pellet market through five mines and secured its downstream position by acquiring Stelco in 2024. Rio Tinto’s Simandou development will deliver 120 million t of high-grade fines annually, potentially supporting future pelletizing ventures in Guinea and China.

Strategic acquisitions continue to reshape market structure as players chase grade security and geographical reach. Anglo American secured multi-billion-tonne reserves at Minas-Rio in 2024, preserving long-term feedstock for DR-grade pellet projects. Technology differentiation is another battleground: PyroGenesis markets plasma torch solutions that slash natural-gas usage in induration, while Primetals’ hydrogen reduction technology could eventually bypass pellets altogether. Producers able to pair resource ownership with low-carbon processing stand to lock in premium pricing and regulatory headroom.

Competitive intensity is likely to climb as more end-users lock in DR-grade offtake contracts before green-steel demand fully materializes. Miners without premium resources may pursue beneficiation or blending strategies, though these require significant capital and energy inputs. Overall, market power is trending toward firms that combine high-grade ore access with proven decarbonization roadmaps.

Iron Ore Pellets Industry Leaders

ArcelorMittal

Bahrain Steel

Ferrexpo Plc

LKAB

Vale S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: ArcelorMittal has commenced construction of the Port-Cartier flotation project, the largest greenhouse gas emission reduction initiative in Quebec, Canada. This project will upgrade the Port-Cartier pellet plant to produce up to 10 million tonnes of direct-reduced iron pellets annually.

- August 2024: Tata Steel Nederland has ordered an advanced pellet testing facility from Primetals Technologies, capable of conducting up to 500 tests annually to optimize raw material combinations and induration parameters. This initiative is expected to foster innovation in the iron ore pellets market by improving pellet quality and enhancing production efficiency.

Global Iron Ore Pellets Market Report Scope

| Blast Furnace (BF) Pellets |

| Direct Reduction (DR) Pellets |

| Fluxed Pellets |

| Circular/HVOF and Specialty Pellets |

| Hematite |

| Magnetite |

| Super-High-Grade (Greater than equal to 67% Fe) |

| Steel Production |

| Foundries |

| Cement and Refractories |

| Other End-user Industries (Chemicals, Water Treatment, etc.) |

| Straight-Grate |

| Grate-Kiln |

| Circular Pelletising System |

| Hybrid/Low-carbon Induration |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Pellet Type | Blast Furnace (BF) Pellets | |

| Direct Reduction (DR) Pellets | ||

| Fluxed Pellets | ||

| Circular/HVOF and Specialty Pellets | ||

| By Grade | Hematite | |

| Magnetite | ||

| Super-High-Grade (Greater than equal to 67% Fe) | ||

| By End-user Industry | Steel Production | |

| Foundries | ||

| Cement and Refractories | ||

| Other End-user Industries (Chemicals, Water Treatment, etc.) | ||

| By Technology | Straight-Grate | |

| Grate-Kiln | ||

| Circular Pelletising System | ||

| Hybrid/Low-carbon Induration | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the iron ore pellets market in 2026 and how fast is it growing?

The market is valued at USD 66.21 billion in 2026 and is forecast to expand at a 4.83% CAGR to 2031.

Which pellet type is expected to grow the fastest by 2031?

Direct reduction pellets are projected to post the highest 5.28% CAGR due to hydrogen-ready DRI capacity additions.

Why are super-high-grade pellets gaining attention?

Pellets with greater than or equal to 67% Fe lower energy use and CO₂ per ton of steel, making them crucial feedstock for green-steel initiatives.

Which region dominates demand for iron ore pellets?

Asia-Pacific holds 50.96% of global consumption, driven by China’s and India’s steel industries.

How are government policies influencing pellet producers?

Carbon pricing schemes such as the EU CBAM and US DOE decarbonization grants incentivize investments in low-carbon induration and DR-grade capacity.

What technological shift is most significant for future pellet plants?

Hybrid or low-carbon induration systems that use plasma torches or renewable power are emerging fastest, growing at 5.73% CAGR.

Page last updated on: