Europe Car Loan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

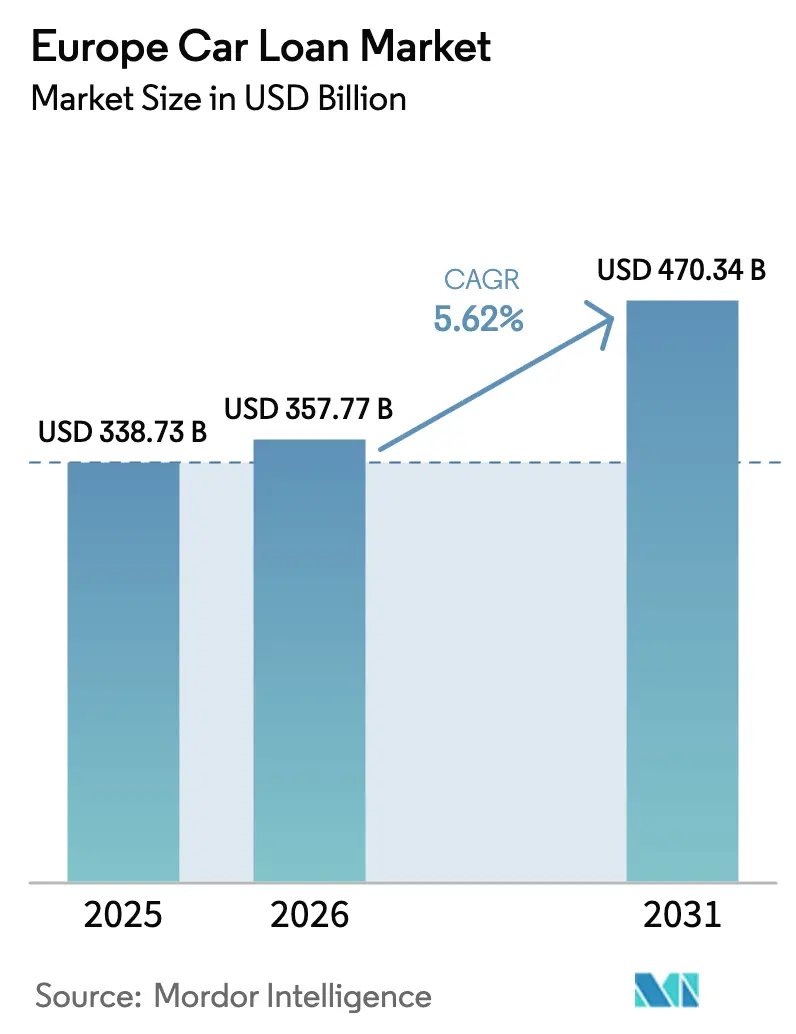

| Base Year Market Size (2025) | USD 338.73 Billion |

| Market Size (2026) | USD 357.77 Billion |

| Market Size (2031) | USD 470.34 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

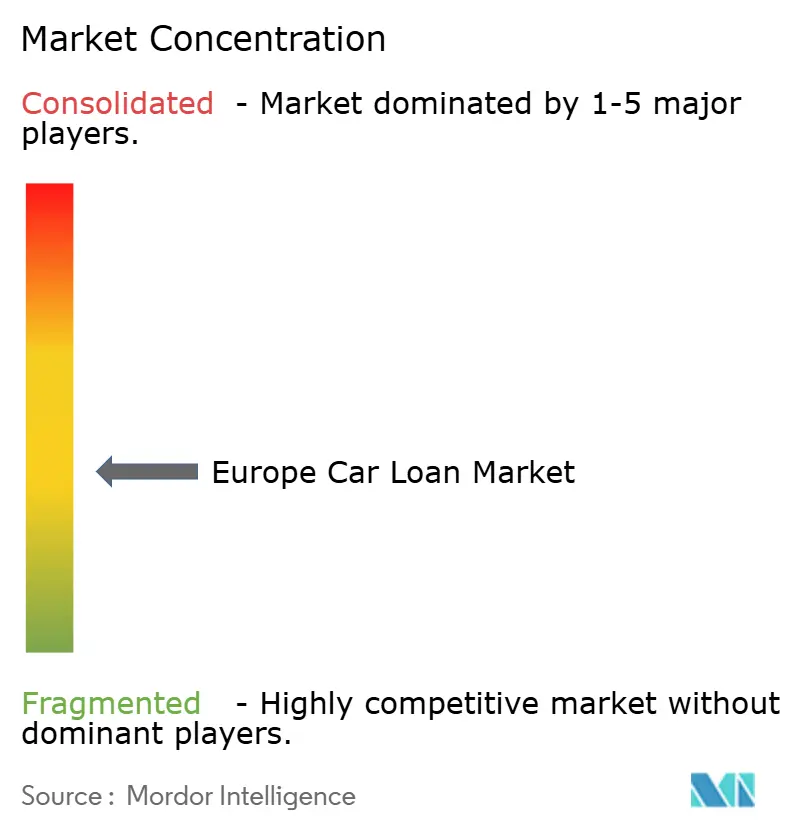

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Car Loan Market Analysis by Mordor Intelligence

The Europe Car Loan Market size was valued at USD 338.73 billion in 2025 and is estimated to grow from USD 357.77 billion in 2026 to reach USD 470.34 billion by 2031, at a CAGR of 5.62% during the forecast period (2026-2031).

A shift is underway from lease-heavy portfolios toward income-tested credit as lenders recalibrate around residual-value risk for battery electric vehicles, while the regulatory outlook evolves with the European Union’s 2035 target adjusted to a 90% tailpipe emission reduction in late-2025. Battery-electric vehicles accounted for 17.4% of new registrations in 2025, which reinforces loan demand for higher-ticket vehicles but also amplifies residual-value uncertainty. Lenders in Spain and Italy have already tightened underwriting on used EVs after loan-to-value ratios drifted above prudent ranges in 2025, a pivot that coincided with sharper risk controls across non-captive franchises following the United Kingdom’s compensation program for historical commission practices. Digital origination keeps gaining share, helped by open-banking data flows under PSD2, while captive finance arms wield pricing power on EV loans and balloon structures to support OEM sales even as they narrow credit boxes on volatile collateral.

Key Report Takeaways

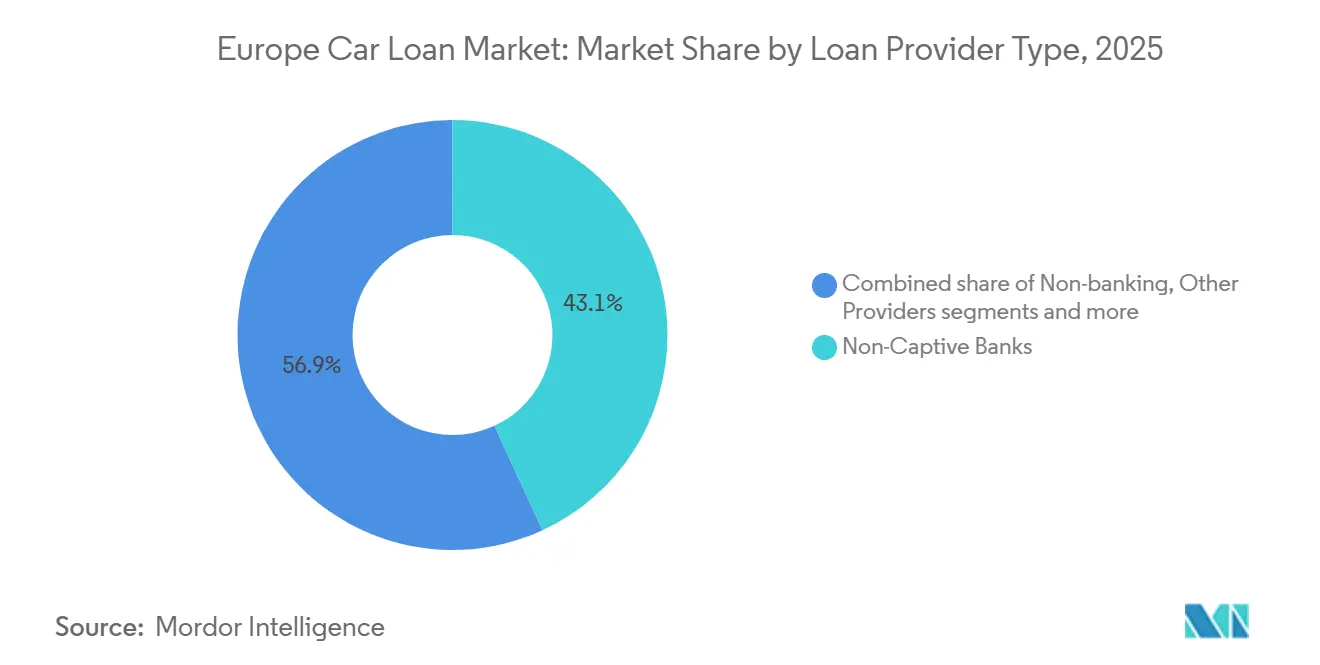

- By provider type, non-captive banks held 43.12% of the Europe car loan market share in 2025, while non-banking financial services providers posted the fastest growth at 7.42% CAGR through 2031.

- By vehicle type, used-car financing accounted for a 54.31% share of the Europe car loan market size in 2025 and is expanding at a 6.39% CAGR over the forecast period.

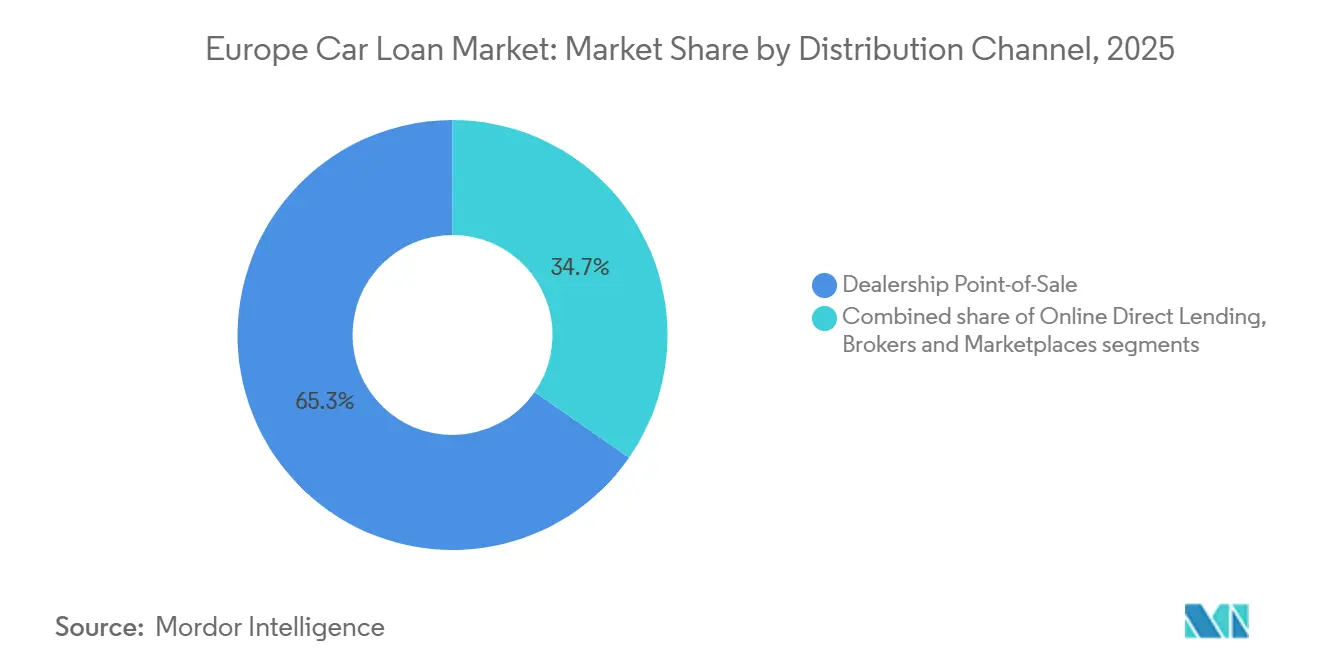

- By distribution channel, dealership point-of-sale financing led with 65.34% share of the Europe car loan market in 2025; online direct lending registers the highest projected CAGR at 6.83% to 2031.

- By geography, Germany commanded a 26.75% share of Europe car loan market in 2025, whereas Spain is forecast to rise at an 8.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on car loan market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Car Loan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-Adoption Incentives Accelerating Loan Demand | +1.2% | EU-27, Germany, France, Nordics, Benelux, Spain | Medium term (2-4 years) |

| Digital / Online Origination Platforms Scale-Up | +0.9% | EU core markets, UK, Germany, Netherlands | Short term (≤ 2 years) |

| Rising Used-Car Finance Penetration | +1.5% | Southern Europe, EU-27, wider Europe | Long term (≥ 4 years) |

| PSD2-Enabled Alternative Credit Assessment | +0.7% | EU-27, UK, Netherlands, Belgium, Nordics | Medium term (2-4 years) |

| ABS / Private-Credit Inflows Lowering Funding Costs | +0.6% | Spain, Germany, France, wider Europe | Short term (≤ 2 years) |

| EU CO2 Targets and Subsidies Lifting EV Demand and Ticket Sizes | +1.3% | EU-27 and Norway, strongest in Germany, France, Spain, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Adoption Incentives Accelerating Loan Demand

Germany relaunched a socially scaled EV subsidy program on January 1, 2026, with a EUR 3 billion budget that targets up to 800,000 vehicles through 2029, which supports entry-level affordability and anchors forward loan pipelines in the largest country market[1]European Alternative Fuels Observatory, “Germany’s 2026 EV Incentive Programme,” EAFO, alternative-fuels-observatory.ec.europa.eu. Battery electric vehicles claimed 17.4% of EU new-car registrations in 2025, lifting the share of higher-ticket loans while also pressuring lenders to refine EV-specific underwriting. ACEA.AUTO. France kept fiscal support in place through its eco-bonus framework, while Spain’s 15% income-tax deduction for EV purchases provided incremental demand support and influenced loan affordability outcomes in 2025[2]European Alternative Fuels Observatory, “Germany’s 2026 EV Incentive Programme,” EAFO, alternative-fuels-observatory.ec.europa.eu. Norway’s long-standing policy mix achieved an 88% BEV sales share in 2025, a high-penetration example that informs the ceiling for EV-led loan origination under sustained incentives and mature charging ecosystems. The EU’s end-of-decade regulatory framework keeps pressure on OEMs to sell a critical mass of zero-emission vehicles, a dynamic that pushes captives to offer promotional APRs and balloon products to convert showroom interest into funded contracts. These supports collectively raise the floor for EV-oriented portfolios within the Europe car loan market as households respond to upfront price gaps with structured finance that spreads costs over longer tenors.

Digital / Online Origination Platforms Scale-Up

Digitization of loan origination continues to compress acquisition costs and improve time-to-yes, with lenders reporting double-digit growth in paperless volumes and deeper adoption of e-signing and remote KYC[3]Wolters Kluwer, “Current Trends in Auto Lending Digitization,” Wolters Kluwer, wolterskluwer.com. Open banking under PSD2 enables real-time affordability checks based on transaction data rather than static payslips, which expands addressable credit while helping manage risk for thin-file or variable-income customers. In Belgium, KBC observed pronounced digital adoption for EV finance in 2025, including widespread selection of balloon structures for electric cars under three years old and strong consumer willingness to complete the journey fully online. United Kingdom lenders are reinforcing digital audit trails after the Financial Conduct Authority’s compensation initiative elevated the compliance bar and increased the value of clean, broker-free journeys. Embedded finance features now appear in OEM and bank platforms across the continent, and tools like BBVA’s online car-loan simulator shorten decisions while tailoring APR offers to powertrain choices. These trends are reinforcing the structural shift toward digital channels within the Europe car loan market as lenders align technology investments with evolving consumer behavior.

Rising Used-Car Finance Penetration

Used-car financing has taken a durable lead by value share and growth, supported by affordability needs and deeper secondary-market activity, including extended vehicle ownership cycles and fleet returns that refresh supply. In the United Kingdom, used-car transactions rose again in 2025, and in Spain the secondary market passed 2 million transactions, both signals that the financing base is tilting toward older vehicles even as EV penetration builds gradually from a low base. Residual-value divergence is now a core underwriting issue, with Italy’s BEV three-year value retention near 26% compared to much higher levels for diesel and hybrid models, which constrains balloon financing without buy-back protection. Spain’s central bank highlighted more cautious practices in consumer credit relative to mortgages as lenders manage the collateral volatility that accompanies newer powertrains. Corporate disclosures confirm the pressure, with a Q4 2025 impairment at a large European lessor after management marked down used-EV remarketing values in line with fast-moving technology cycles. Subscription and rental formats that cycle assets rapidly are adding to financing pathways for older inventory, which further reinforces the position of used vehicles in the Europe car loan market.

PSD2-Enabled Alternative Credit Assessment

PSD2 has become a practical foundation for consent-based, data-driven underwriting, allowing lenders to capture spending and income dynamics that traditional bureaus overlook and to tailor credit lines with more precision. Supervisors have flagged consumer over-indebtedness as a watchpoint in 2025, which encourages responsible-use models that rely on up-to-date transaction feeds and demonstrable affordability screens. Spain’s household credit data show a pickup in consumer credit in 2025, helped in part by stronger employment and the wider adoption of digital origination, which underscores the role of open finance in expanding addressable borrowers. The coming Consumer Credit Directive 2 extends consumer-protection scope to smaller-ticket and short-duration products by late 2026, which will raise baseline compliance costs and strengthen the case for pan-regional platforms. Platform lenders that fuse PSD2 data with explainable machine learning now enjoy a speed and risk-calibration edge, especially in segments with fluctuating income, which is enlarging their role within the Europe car loan market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Interest-Rate and Macro Volatility | -1.0% | Peripheral euro area and broader Europe | Medium term (2-4 years) |

| Residual-Value Swings, Especially for EVs | -0.8% | EU-27 and UK, acute in Germany, France, Italy | Long term (≥ 4 years) |

| Regulatory Scrutiny and FCA-Style Redress Risk | -0.5% | UK, with spill-over to EU | Short term (≤ 2 years) |

| Battery-Health Uncertainty as Collateral | -0.4% | EV markets across Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Interest-Rate and Macro Volatility

Policy-rate declines in 2025 did not fully translate into cheaper consumer lending, and spreads on unsecured credit stayed elevated compared with the pre-pandemic era, a headwind for affordability-sensitive segments[4]Banco de España, “Report on the Financial Situation of Households and Firms, H1 2025,” Banco de España, bde.es. Spanish data show steady consumer credit growth supported by employment gains, yet surveys in major markets reflected caution in late 2025 as households managed inflation and fiscal uncertainty. United Kingdom lenders also adjusted expectations amid regulatory changes, which weighed on non-prime volumes and introduced stricter affordability testing. Nordic supervisors highlighted measures that affect bank funding costs and capital planning in late 2025, which can pass through to pricing for consumer credit. These dynamics limit elasticity in demand for higher-ticket EV purchases, which shapes product design and tenor options in the Europe car loan market.

Residual-Value Swings, Especially for EVs

Observed three-year residual values for BEVs fell well below combustion and hybrid benchmarks in several large markets in 2025, pressuring balloon structures and increasing the need for OEM guarantees at the end of term. One of Europe’s largest lessors recognized significant impairments in Q4 2025 on used-EV portfolios after applying more conservative remarketing assumptions, which reset expectations for value retention. United Kingdom data showed signs of convergence between EV and ICE depreciation by late 2025 as battery-health reporting improved and a second-hand pipeline formed, although model-specific volatility persisted. Consumer organizations also documented persistent residual gaps between BEVs and petrol cars through 2024, driven by higher new prices and faster technology cycles. These swings increase capital charges and narrow credit boxes, which constrain origination growth for used EVs in the Europe car loan market without robust guarantees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loan Provider Type: Non-Bank Lenders Build Data Advantages

Non-captive banks held 43.12% of 2025 origination by value, while non-banking financial services providers are projected to grow at 7.42% CAGR through 2031, the fastest among provider types in the Europe car loan market. This growth reflects embedded finance roadmaps, PSD2-enabled underwriting, and green-oriented products configured for EV customers, all of which appeal to younger and digital-first borrowers. Market share dynamics also favor platforms that combine low-cost deposits or securitization access with digital channels, positioning scale institutions to widen their funnels while controlling unit economics. In parallel, industry associations in the Nordics documented expansion of non-bank credit intermediation through 2025, which reinforces the role of leasing and private-credit vehicles in vehicle finance. These patterns indicate that the Europe car loan market will keep allocating share to providers that marry data moats with diversified funding.

Non-banking financial services providers leverage open-banking feeds and machine learning to reach underserved segments, while captive arms concentrate on converting EV showroom traffic with subsidized APRs and balloon structures. Volkswagen Financial Services reported strong first-half 2025 performance and higher BEV contracts in Europe, a sign that product innovation and balance-sheet depth remain essential for EV penetration. Multi-country lender groups optimized regulatory capital with synthetic risk transfers in late 2025, which supports larger lending books without sacrificing risk discipline. As regulations around consumer credit tighten in late 2026, scale and compliance readiness will separate providers in the Europe car loan industry.

By Vehicle Type: Used Vehicles Anchor Affordability and Volume

Used cars held 54.31% of 2025 originations by value, and their growth outlook at 6.39% CAGR through 2031 reflects durable demand for lower monthly payments and deeper secondary-market activity in the Europe car loan market. Several large countries reported healthy used-vehicle transaction volumes in 2025, reinforcing a financing mix that skews older while EVs start to build a second-hand base. Residual-value data point to persistent dispersion by powertrain, which is shaping LTV ceilings and the need for end-of-term guarantees in used-EV loan designs. Central bank commentary in Spain confirmed a more conservative orientation for vehicle credit standards relative to mortgages, reflecting the heightened collateral volatility for emerging technologies. These features support the case that used vehicles will remain the anchor of value and volume in the Europe car loan market.

New-car finance still plays a strategic role as the channel for subsidies, OEM incentives, and captive promotional APRs, which lift EV uptake and help define product features for future used-EV cycles. In markets such as Belgium, average amounts borrowed for recent-vintage EVs were materially higher than for non-electric cars in 2025, which validates the use of balloon structures to manage affordability. Corporate disclosures in 2025 signal that residual-value risk requires continuous recalibration for EVs, which informs captive strategies on credit boxes and guarantees. As subscription and rental penetrate, vehicles cycle through multiple users before resale, which gradually improves data on EV depreciation and supporting finance structures across the Europe car loan market.

By Distribution Channel: Online Direct Lending Gains Momentum

Dealership point-of-sale retained 65.34% of 2025 distribution, though online direct lending is the fastest-growing channel with a 6.83% CAGR outlook to 2031 in the Europe car loan market. The digital channel’s cost advantage and speed to decision are reinforced by PSD2-enabled data and embedded finance workflows on OEM and bank platforms. Lenders report strong customer willingness to complete purchase and financing journeys online, especially for EVs, where younger buyers expect end-to-end digital services. The United Kingdom compensation initiative accelerated a shift away from broker-heavy models toward direct channels with better documentation and standardized disclosures. Digital simulators and real-time pricing, such as those offered by large Spanish banks, help align term structures with borrowers’ affordability constraints. As CCD2 comes into force, cross-border providers with harmonized workflows will gain operating leverage across the Europe car loan market.

Market participants expect dealership POS to defend share where bundled products and in-person delivery remain valued, but omnichannel models are converging toward embedded journeys that preserve margin and speed. Captives strengthened funding resilience through deposit growth and operating performance in 2025, enabling competitive direct pricing while advancing digitization strategies. As data pipelines broaden and underwriting models evolve, the Europe car loan market share of online channels should continue to rise alongside tighter compliance norms and uniform disclosures.

Geography Analysis

Germany held 26.75% of the Europe car loan market share in 2025 by value, reflecting the scale of its economy and auto manufacturing base, while Spain is projected to grow at 8.51% CAGR through 2031, making it the fastest-growing country market. Spanish consumer credit strengthened in 2025 as employment and wage dynamics supported demand, which, combined with greater digital adoption, lifted approval funnels. Germany’s policy reset on EV incentives in 2026 targets social scaling and should stabilize entry-level affordability, which can help sustain EV-oriented originations as the product mix changes. The United Kingdom market navigated a dual transition of regulation and digitization in late 2025, with association data reflecting short-term caution yet a higher-quality origination base for 2026. These conditions are reshaping country growth profiles within the Europe car loan market as regulation and household balance-sheet health diverge across borders.

France saw a resilient used-vehicle market in 2025, including rising second-hand EV sales, which broadens the base for used-EV finance even as underwriting stays conservative on collateral assumptions. Italy’s used-vehicle activity remained high, but residual-value challenges for BEVs created headwinds for end-of-term pricing and loan design, a constraint that financiers addressed with recalibrated assumptions. In Benelux, market preferences for leasing, rental, and subscription models continued to shape finance structures, while the Netherlands recorded a strong used-car market that supports lender focus on secondary transactions. Nordic policy environments showcased high EV penetration in Norway and disciplined bank practices in Sweden, with industry associations noting the growing role of non-bank intermediation. These regional contrasts influence origination mix and risk metrics across the Europe car loan market.

Regulatory context is increasingly central to country-level outcomes, from Spain’s consumer-credit dynamics and Germany’s over-indebtedness signals to the United Kingdom’s redress program, all of which shape pricing, approval rates, and product structures. Harmonization under CCD2 is on track to tighten standards for microcredit and short-duration products by late 2026, which will likely favor lenders with pan-EU platforms and stronger compliance operating models. The interaction of national incentives, infrastructure readiness, and household balance sheets will continue to differentiate growth and risk-adjusted returns across the Europe car loan market.

Mordor Intelligence provides coverage of the car loan market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United Kingdom, France, Russia, South Korea, China, India, Japan, and India incorporating local coverage and market participation, as required.

Competitive Landscape

The Europe car loan market remains moderately fragmented, with the top ten providers estimated to account for a little more than half of originations by value, leaving room for regional banks and digital challengers to scale. Captive finance arms advanced deposit-led funding and digital journeys in 2025, which bolstered their ability to support OEM EV targets with competitive pricing. In parallel, industry associations reported that non-bank financial intermediation expanded in the Nordics, reflecting the growing role of leasing and private-credit structures in vehicle finance. Lender strategies increasingly focus on data integration, embedded finance, and synthetic securitization to balance growth with capital efficiency.

M&A and partnerships shaped the 2025–2026 landscape, including exclusive talks by a leading European lessor to acquire a peer that would create a co-leader in full-service leasing, subject to approvals. Automaker-linked finance platforms expanded tie-ups with global OEMs to deliver credit, leasing, and rental solutions across multiple countries starting January 2026. Electric mobility partnerships extended to fast-growing entrants as well, with tailored consumer and fleet solutions rolled out through national dealer networks in 2025. Together, these moves underscore an emphasis on scale, cross-border reach, and EV-centric propositions in the Europe car loan market.

At the same time, 2025 results from large auto-finance divisions and diversified lenders highlighted stronger operating performance, deposit inflows, and risk-transfer activity that collectively support sustained origination. Pan-European groups disclosed sizeable outstandings and mobility targets through 2026, reinforcing their strategic role in EV financing and fleet electrification. Automaker groups announced new model launches in Enlarged Europe for 2026 with a focus on electrified line-ups, which strengthens the new-vehicle pipeline that captive and partner lenders will finance. These strategic and operating patterns point to continued competition on digital experience, EV-specific finance, and funding flexibility across the Europe car loan market.

Europe Car Loan Industry Leaders

Santander Consumer Finance

Volkswagen Financial Services

Stellantis Financial Services

BNP Paribas Personal Finance (Cetelem)

Deutsche Bank

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Crédit Agricole Personal Finance & Mobility and Honda Motor Europe signed a pan-European partnership for financing Honda cars and motorcycles across eight countries, effective January 1, 2026, in four markets, with phased rollouts in others.

- December 2025: Arval, a BNP Paribas subsidiary, entered exclusive negotiations with Mercedes-Benz Group to acquire Athlon, aiming to build a European co-leader in full-service vehicle leasing, with closing targeted in 2026 pending approvals.

- May 2025: Crédit Agricole Auto Bank and BYD agreed to expand tailored financing solutions for electromobility in France through more than 50 points of sale.

- October 2025: BNP Paribas Cardif and Stellantis Financial Services, through subsidiaries Icare and Stellantis Insurance, partnered to support the used-vehicle market and Spoticar across Europe.

Europe Car Loan Market Report Scope

The European car loan market is segmented by product type, provider type, and region. By product type, the market is sub-segmented into used cars and new cars. By provider type, the market is sub-segmented into banks, non-banking financial services, original equipment manufacturers, and other provider types. By region, the market is sub-segmented into Germany, the United Kingdom, France, Italy, Spain, and the Rest Of Europe. The report offers the value (USD) for the above segments.

A financial institution or lender may offer a type of financing called a car loan, also called an auto loan or vehicle loan, to assist people in buying a car. A complete background analysis of the European car loan market includes an assessment of the industry associations, the overall economy, and emerging market trends by segment. Significant changes in the market dynamics and market overview are also covered in the report.

| Non-Captive Banks |

| Non-banking Financial Services |

| Original Equipment Manufacturers (Captives) |

| Other Providers |

| New Car |

| Used Car |

| Dealership Point-of-Sale |

| Online Direct Lending |

| Brokers & Marketplaces |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Loan Provider Type (Value) | Non-Captive Banks |

| Non-banking Financial Services | |

| Original Equipment Manufacturers (Captives) | |

| Other Providers | |

| By Vehicle Type (Value) | New Car |

| Used Car | |

| By Distribution Channel (Value) | Dealership Point-of-Sale |

| Online Direct Lending | |

| Brokers & Marketplaces | |

| By Country (Value) | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size and growth outlook for the Europe car loan market?

The Europe car loan market size is USD 338.73 billion in 2025 and is expected to reach USD 470.34 billion by 2031 at 5.62% CAGR over 2026-2031.

Which vehicle segment is leading origination in Europe?

Used vehicles lead by value and are projected to grow at 6.39% CAGR to 2031, anchored by affordability and strong secondary-market activity.

How are regulations shaping EV loan growth?

EU emissions targets and national incentives increase EV loan demand and ticket sizes, while lenders use balloon structures and guarantees to balance residual-value risk.

Which countries are most significant for growth and share?

Germany holds the largest share, while Spain is the fastest-growing through 2031, supported by consumer-credit momentum and digital origination.

What distribution channels are expanding fastest?

Online direct lending is the fastest-growing channel due to PSD2-enabled underwriting, embedded finance, and lower acquisition costs.

What risks are lenders monitoring most closely?

Lenders focus on EV residual-value volatility, macro and rate sensitivity, regulatory redress exposure, and battery-health transparency as they calibrate credit boxes.

Page last updated on: