Global Cannabis Testing Market Size and Share

Market Overview

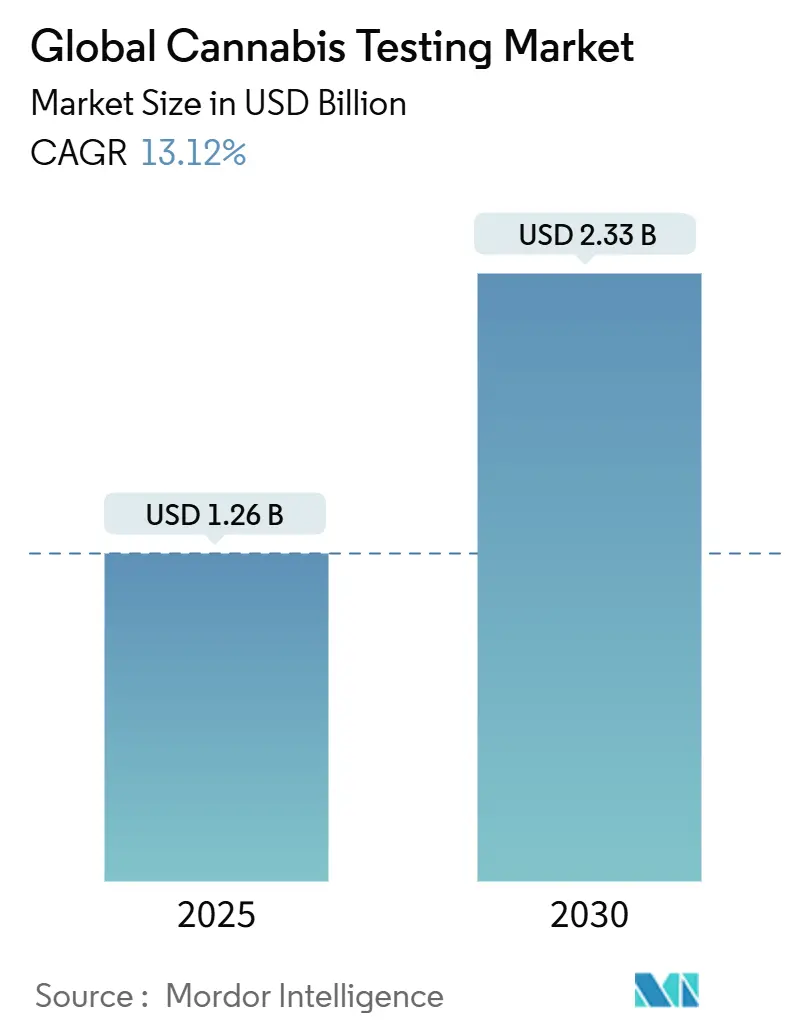

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 1.26 Billion |

| Market Size (2030) | USD 2.33 Billion |

| Growth Rate (2025 - 2030) | 13.12% CAGR |

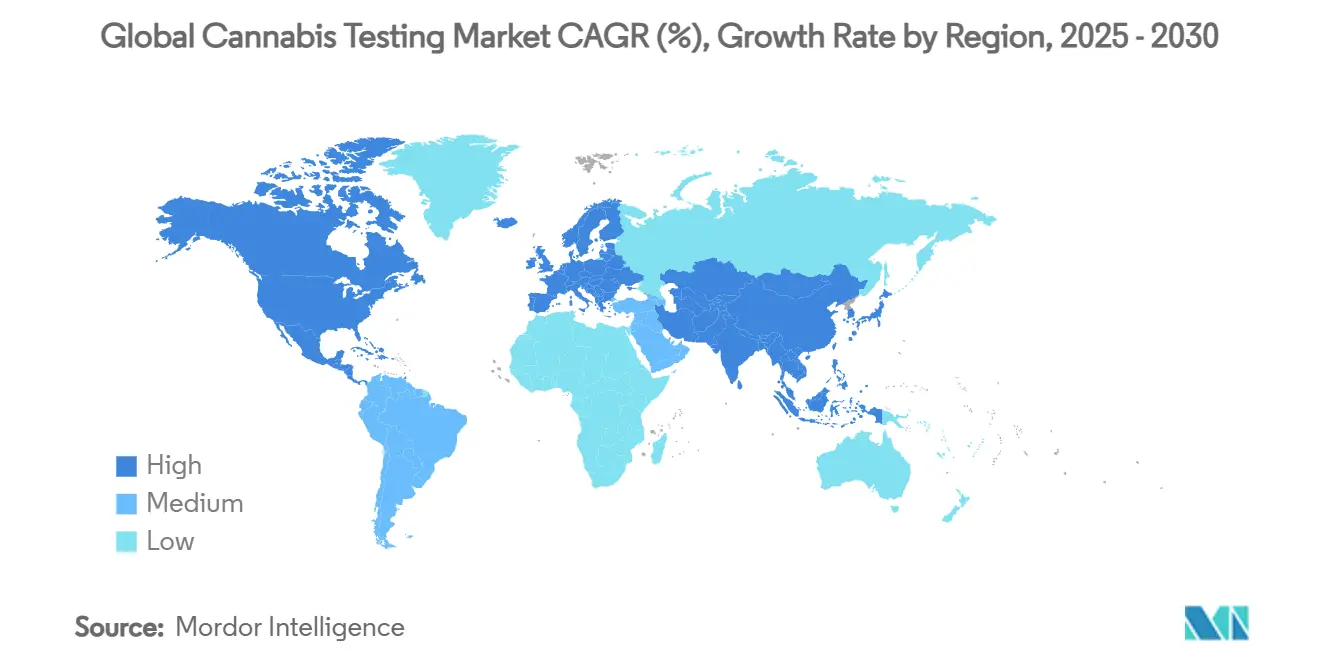

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Global Cannabis Testing Market Analysis by Mordor Intelligence

The global cannabis testing market is valued at USD 1.26 billion in 2025 and is projected to reach USD 2.33 billion by 2030, translating into a 13.12% CAGR through the forecast period. Sustained legalization momentum, mandatory quality-and-safety protocols, and rising pharmaceutical‐grade requirements keep demand strong while forcing laboratories to upgrade analytical depth and data traceability. Laboratories able to meet multi-jurisdictional standards secure early-mover gains, particularly in Europe, where the July 2024 European Pharmacopoeia monographs set standard contaminant limits and methods. Strategic mergers such as the SC Laboratories–Agricor–Botanacor combination signal an era of scale seeking, even as “lab shopping” scandals pressure regulators to tighten oversight. Emerging opportunities are most visible in Asia Pacific, where Thailand and Australia refine medical cannabis laws, while North America retains absolute leadership despite intensified license reviews.

Key Report Takeaways

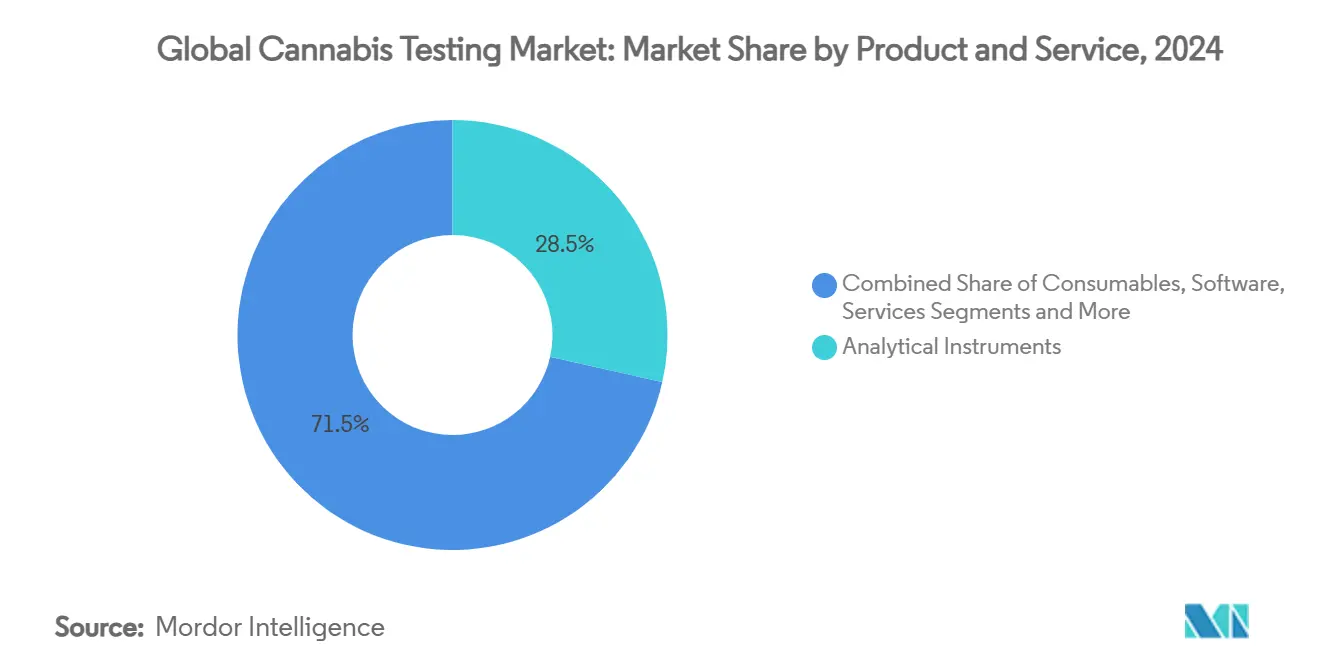

- By product category, Analytical Instruments led with 28.5% revenue share in 2024; Software is projected to expand at a 15.5% CAGR through 2030.

- By testing type, Potency Testing accounted for 22.4% of the cannabis testing market share in 2024; Terpene Profiling is advancing at a 14.7% CAGR through 2030.

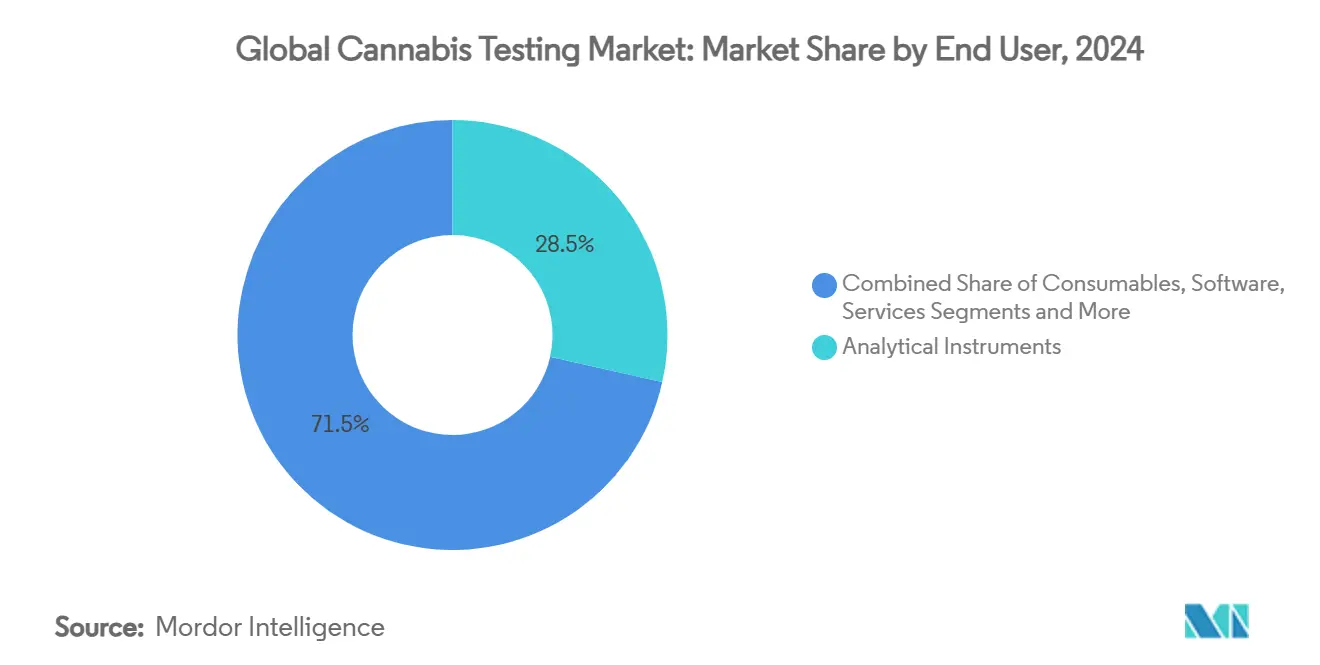

- By end user, Independent Testing Laboratories held 33.7% share of the cannabis testing market size in 2024, while Pharmaceutical & Research Institutes post the fastest CAGR at 13.7% to 2030.

- By geography, North America dominated with 28.6% revenue share in 2024; Asia Pacific is forecast to grow at 12.2% CAGR between 2025–2030

Global Cannabis Testing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legalization of Cannabis Wave Across Few Countries | +2.80% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Mandatory Quality-&-Safety Compliance Testing In All Regulated Markets | +3.20% | Global | Short term (≤ 2 years) |

| Growing R&D Spend On Cannabinoid-Based Pharmaceuticals | +1.90% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Proliferation Of Contract Testing Laboratories In Emerging LATAM & APAC | +1.70% | LATAM & APAC core, spill-over to MEA | Medium term (2-4 years) |

| Premiumization: Minor-Cannabinoid & Terpene Differentiation Needs | +1.40% | North America & EU premium markets | Medium term (2-4 years) |

| Complex Edible/Beverage Matrices Requiring Multi-Residue Methods | +1.20% | Global, with early adoption in mature markets | Short term (≤ 2 years) |

Source: Mordor Intelligence

Legalization of Cannabis Wave Across Few Countries

Germany’s Cannabis Act in 2024 created the first G-20 adult-use blueprint, prompting other EU members to review prohibition-era rules.[1]German Bundestag, “Cannabisgesetz 2024,” bundestag.de Maryland’s 2025 law permitting on-site consumption lounges mandates full-panel testing for lounge sales, opening a secondary laboratory market. The DEA proposal to move cannabis to Schedule III would remove the federal–state conflict and may unify laboratory standards once hearings conclude in 2025. Thailand’s medical framework positions Bangkok as an Asia Pacific testing hub as regional regulators benchmark its protocols.

Mandatory Quality-&-Safety Compliance Testing In All Regulated Markets

New Jersey’s 2025 rules make a Certificate of Analysis a consumer-facing document listing cannabinoids, contaminants, and water activity.[2]New Jersey Cannabis Regulatory Commission, “Laboratory Testing Guidance 2025,” nj.gov Massachusetts expanded safety panels to include new pesticide classes in 2025, rewarding labs with LC-MS/MS capability. USDA requires hemp labs to register with the DEA by 31 December 2025, foreshadowing a federal gatekeeper role for cannabis once rescheduling clears. Canada raised micro-class production ceilings in March 2025 while keeping full testing, illustrating how mature markets cut red tape without reducing safety.

Growing R&D Spend On Cannabinoid-Based Pharmaceuticals

FDA-aligned inhaler projects, such as Rapid Therapeutic Science Laboratories, require stability, dose uniformity, and extractable leachables studies beyond the scope of normal cannabis panels. Brazil’s ANVISA demands pharmaceutical-quality validation for CBD oral solutions, spurring outsourcing of chromatographic and microbiological assays.[3]Rodrigo P. Piochi, “Medicinal Cannabis in Brazil: Regulatory Advances and Analytical Challenges,” Química Nova, quimicanova.sbq.org.br Raman microscopy coupled with AI now delivers 99.83% cannabinoid classification accuracy, shortening turnaround and raising the bar for potency-plus-profile tests.

Proliferation Of Contract Testing Laboratories In Emerging LATAM & APAC

ONAC accreditation prepares Colombian labs to service regional exports once quota hurdles ease, yet revenue remains muted until customs simplification arrives. Australia’s Therapeutic Goods Administration proposes aligning import and domestic GMP for medicinal cannabis, giving national labs a regional advantage. Hong Kong’s zero-THC mandate on CBD cosmetics forces high-resolution mass spectrometry deployment, a capability few regional labs currently hold.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Operating Cost Of Advanced Analytical Platforms | -1.80% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Fragmented Global Regulatory Standards Cause Result Variability | -2.10% | Global, with concentration in multi-jurisdictional operators | Medium term (2-4 years) |

| Shortage Of Skilled Analysts & Reference Standards | -1.30% | Global, with acute impact in APAC & LATAM | Medium term (2-4 years) |

| "Lab-Shopping" Scandals Eroding Data Credibility | -1.60% | North America & emerging regulated markets | Short term (≤ 2 years) |

Source: Mordor Intelligence

High Capital & Operating Cost Of Advanced Analytical Platforms

Triple quadrupole LC-MS/MS units optimized for 200+ pesticides can exceed USD 450,000, limiting adoption in start-ups. A ballistic GC-MS reducing terpene run time to six minutes still demands skilled analysts and custom gases that smaller laboratories cannot absorb. A full cannabis-specific LIMS averages USD 100,000 for licensing and validation, adding to cash burn before revenue scales.

Fragmented Global Regulatory Standards Cause Result Variability

Each US state sets its own action limits, so a California-compliant edible can fail in Oregon, forcing multi-state operators to run duplicate panels. Up to 30% of labs inflated THC in a 2024 California audit, prompting reference methods and proficiency testing by the Department of Cannabis Control. The EU caps industrial hemp THC at 0.2%, while Australia allows 1%, compelling transnational labs to maintain multiple SOPs.

Segment Analysis

By Product and Service: Instruments Drive Infrastructure Investment

Analytical Instruments dominated the cannabis testing market in 2024 with 28.5% revenue share, reflecting heavy expenditures on LC-MS/MS, GC-MS, and ICP-MS systems needed for multiresidue panels. Consumables scale proportionally with test volume, securing predictable revenues. Software is projected to grow at a 15.5% CAGR to 2030 as laboratories automate chain-of-custody and integrate AI-based chromatogram review. LC-APCI-MS/MS that quantifies both terpenes and cannabinoids in a single injection demonstrates why software capable of multivariate data interpretation is now imperative.

Instruments account for the largest capital slice, but services capture a rising share as multi-jurisdictional operators outsource validation and method transfer. SaaS LIMS modules embedded with regulatory change alerts help laboratories keep SOPs current, reducing non-conformance risk. Cloud-hosted platforms also enable remote audit, a core requirement for pharmaceutical sponsors.

Note: Segment shares of all individual segments available upon report purchase

By Testing Type: Potency Testing Dominance Challenged by Specialization

Potency Testing held 22.4% of the cannabis testing market share in 2024, remaining compulsory in every regulated jurisdiction. Yet specialization is accelerating. Terpene Profiling, growing at 14.7% CAGR, benefits from brands marketing “effect-based” SKUs whose sensory claims hinge on validated terpene ratios. Residual Solvent and Pesticide Screening expand as extraction technologies diversify and as governments tighten food safety alignment. The National Institute of Justice validated DART-HRMS for rapid THC characterization, indicating future throughput gains for law-enforcement seizures and possibly commercial labs.

Minor cannabinoid panels covering CBG, CBC, and CBDV emerge as differentiators in premium SKUs. Water activity, microbial enumeration, and mycotoxin testing become critical for edibles and inhalables, aligning cannabis test menus with pharmaceutical and food codes.

By End User: Independent Labs Face Pharmaceutical Competition

Independent Testing Laboratories captured 33.7% share of the cannabis testing market size in 2024 and remains the backbone for compliance certificates. However, Pharmaceutical & Research Institutes outpace the field at a 13.7% CAGR as inhalers, transdermals, and nano-emulsion drinks demand cGMP validation. In-house producer labs grow but face conflict-of-interest scrutiny. Vertical integration cases, such as Aurora Cannabis acquiring Anandia Labs, show producers seeking analytical intellectual property alongside compliance cost savings. Academic centers, such as the University of Mississippi’s cannabis program, continue to pioneer reference analytics that diffuse into the commercial sector.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America contributed 28.6% to global revenue in 2024 and maintains leadership through well-developed regulatory regimes. California revoked four lab licenses between 2024-2025, signaling tougher oversight that favors high-quality operators. Canada raised micro-producer thresholds in 2025 yet retained full mandatory panels, encouraging throughput growth within existing labs. The DEA rescheduling debate continues to cloud interstate commerce, but laboratories prepare SOP harmonization ahead of potential federal standardization.

Europe scaled quickly after Germany legalized non-medical adult use in 2024. The European Pharmacopoeia monographs standardize test limits for flower and CBD products, harmonizing methods and increasing equipment spend. France, Italy, and Spain expand medical programs, each requiring EU-GMP compliance that mirrors pharmaceutical quality norms. Laboratories able to certify products for multiple EU tender markets gain pricing power.

Asia Pacific is the fastest-growing geography at a projected 12.2% CAGR from 2025-2030. Thailand’s Government Pharmaceutical Organization manufactures medical oils and sets domestic analytic benchmarks adopted by neighbors. Australia’s TGA consults on GMP harmonization that could allow domestic labs to certify imports for ASEAN markets. Hong Kong’s zero-THC rule on CBD mandates high-resolution mass spectrometry, opening niche demand for ultra-low limit assays. Conversely, South Korea retains strict narcotics classification for CBD, restricting lab investment.

Competitive Landscape

The cannabis testing market remains fragmented; the top five networks hold far below 30% of global revenue, keeping entry opportunities alive. Competitive vectors revolve around analytical speed, breadth of contaminant panels, and data integrity. SC Laboratories combined with Agricor and Botanacor to create a multi-state footprint able to service large multistate operators while maintaining ISO 17025 accreditation. Eurofins Scientific’s historical acquisition strategy in broader analytical services suggests that once federal clarity emerges, similar roll-up plays may advance in cannabis testing.

Technology adoption produces step changes. High-resolution accurate-mass instruments halve turnaround time for metabolite profiling. AI-assisted chromatogram review lowers labor cost and reduces reporting errors. Labs marketing same-day terpene plus potency results command premium fees. Meanwhile, regulatory scrutiny of “lab shopping” forces a race to audit-proof LIMS and proficiency testing participation.

Regional leaders expand through joint ventures rather than outright purchase to navigate license caps. Canadian lab Valens entered Mexico via a service agreement, leveraging GMP credentials without ownership, illustrating the workaround to foreign equity limits.

Global Cannabis Testing Industry Leaders

-

Shimadzu Scientific Instruments.

-

Merck KGaA (Sigma Aldrich)

-

Restek Corporation

-

PerkinElmer Inc.

-

Agilent Technologies, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Canada amended the Cannabis Act to raise micro-class thresholds while keeping all test requirements.

- February 2025: Allegations of data falsification surfaced in New York, prompting state audits of testing labs.

- January 2025: New Jersey issued laboratory guidance mandating Certificates of Analysis for retail display.

Global Cannabis Testing Market Report Scope

As per the scope of the report, cannabis is proven to be effective in various medical applications, such as reducing nausea caused due to chemotherapy, stimulating appetite in AIDS patients, controlling muscular spasms in multiple sclerosis patients, etc. Cannabis testing refers to the analytical examination of cannabis to ensure its safety before human consumption. The Cannabis Testing Market is Segmented by Product and Software/Service (Analytical Instruments, Spectroscopy Instruments, Consumables, and Cannabis Testing Software and Services), Type (Potency Testing, Terpene Profiling, Residual Solvent Screening, Heavy Metal Testing, Mycotoxin Testing, and Other Types), End User (Laboratories, Cannabis Drug Manufacturers and Dispensaries, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The Market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Product and Service | Analytical Instruments | ||

| Consumables | |||

| Software | |||

| Services | |||

| By Testing Type | Potency (THC/CBD) | ||

| Terpene Profiling | |||

| Residual Solvent Screening | |||

| Pesticide Screening | |||

| Heavy Metal Analysis | |||

| Mycotoxin & Microbial Testing | |||

| Other Specialized Assays | |||

| By End User | Independent Testing Laboratories | ||

| Pharmaceutical & Research Institutes | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Analytical Instruments |

| Consumables |

| Software |

| Services |

| Potency (THC/CBD) |

| Terpene Profiling |

| Residual Solvent Screening |

| Pesticide Screening |

| Heavy Metal Analysis |

| Mycotoxin & Microbial Testing |

| Other Specialized Assays |

| Independent Testing Laboratories |

| Pharmaceutical & Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

How big is the Global Cannabis Testing Market?

The Global Cannabis Testing Market size is expected to reach USD 1.26 billion in 2025 and grow at a CAGR of 13.12% to reach USD 2.33 billion by 2030.

What is the current Global Cannabis Testing Market size?

In 2025, the Global Cannabis Testing Market size is expected to reach USD 1.26 billion.

Who are the key players in Global Cannabis Testing Market?

Shimadzu Scientific Instruments., Merck KGaA (Sigma Aldrich), Restek Corporation, PerkinElmer Inc. and Agilent Technologies, Inc are the major companies operating in the Global Cannabis Testing Market.

Which is the fastest growing region in Global Cannabis Testing Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Global Cannabis Testing Market?

In 2025, the North America accounts for the largest market share in Global Cannabis Testing Market.

What years does this Global Cannabis Testing Market cover, and what was the market size in 2024?

In 2024, the Global Cannabis Testing Market size was estimated at USD 1.09 billion. The report covers the Global Cannabis Testing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Cannabis Testing Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.