Global Cannabis Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

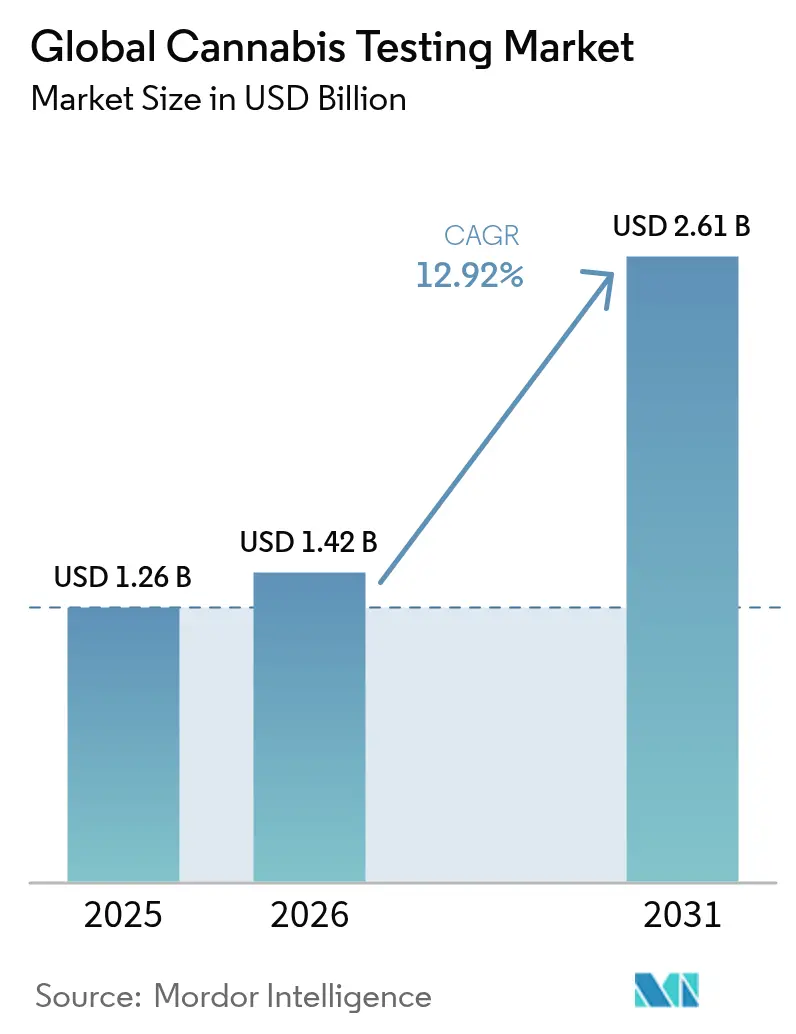

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 2.61 Billion |

| Growth Rate (2026 - 2031) | 12.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

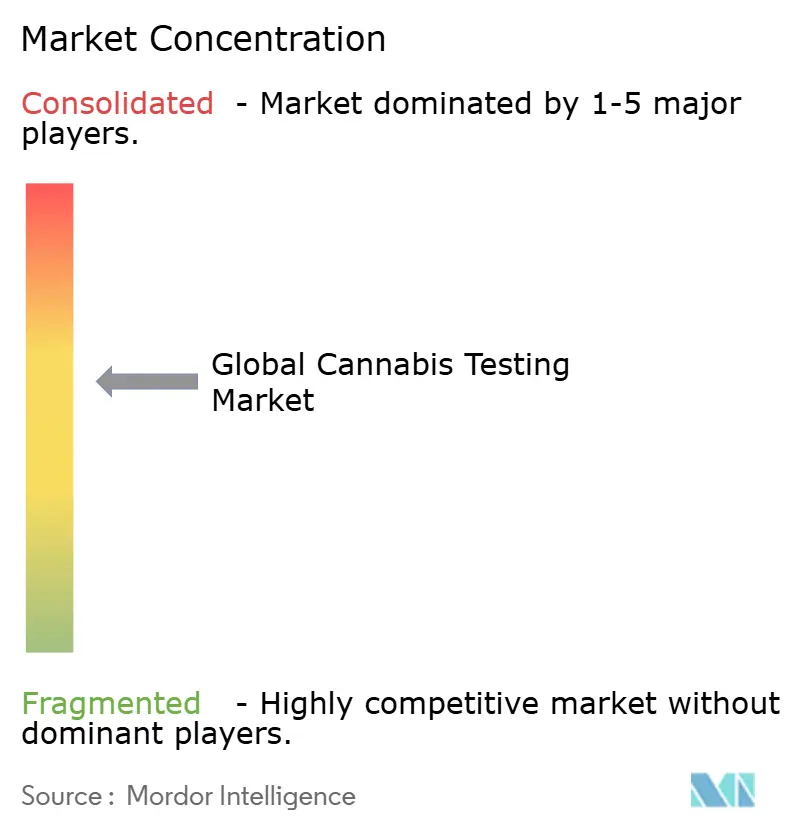

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Cannabis Testing Market Analysis by Mordor Intelligence

The cannabis testing market size is expected to grow from USD 1.26 billion in 2025 to USD 1.42 billion in 2026 and is forecast to reach USD 2.61 billion by 2031 at 12.92% CAGR over 2026-2031. Sustained legalization momentum, mandatory quality-and-safety protocols, and rising pharmaceutical‐grade requirements keep demand strong while forcing laboratories to upgrade analytical depth and data traceability. Laboratories able to meet multi-jurisdictional standards secure early-mover gains, particularly in Europe, where the July 2024 European Pharmacopoeia monographs set standard contaminant limits and methods. Strategic mergers such as the SC Laboratories–Agricor–Botanacor combination signal an era of scale seeking, even as “lab shopping” scandals pressure regulators to tighten oversight. Emerging opportunities are most visible in Asia Pacific, where Thailand and Australia refine medical cannabis laws, while North America retains absolute leadership despite intensified license reviews.

Key Report Takeaways

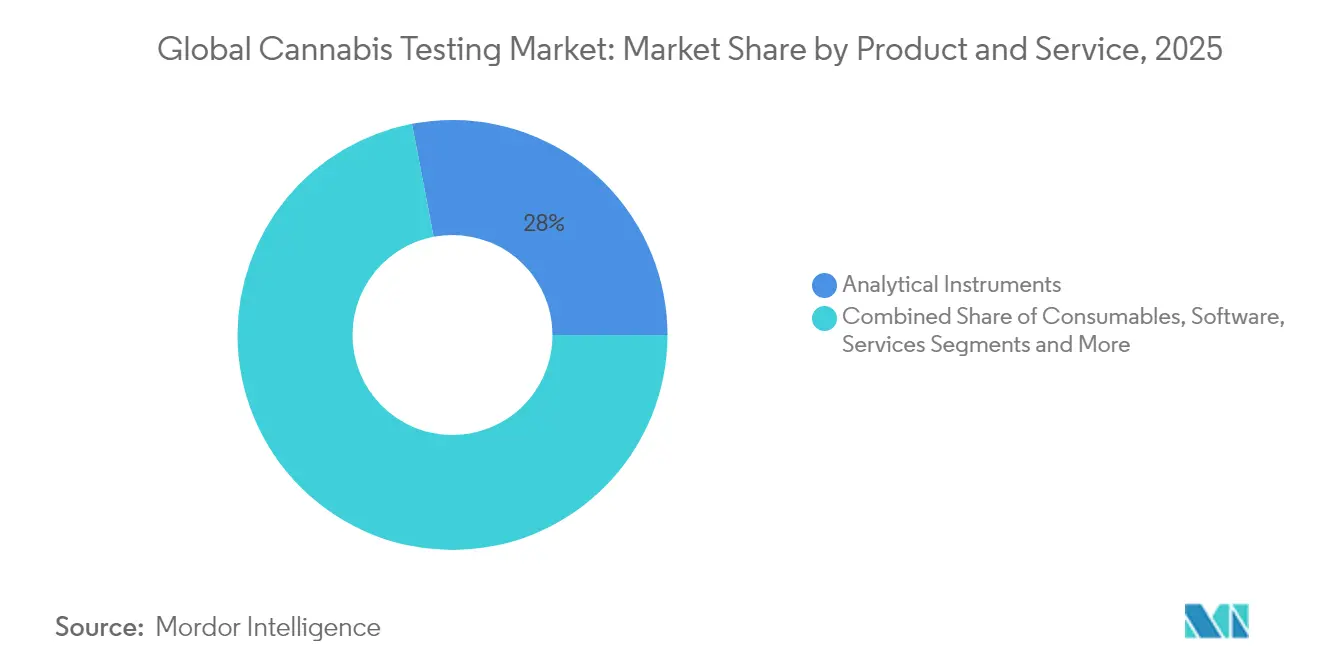

- By product category, Analytical Instruments led with 28.02% revenue share in 2025; Software is projected to expand at a 15.19% CAGR through 2031.

- By testing type, Potency Testing accounted for 22.05% of the cannabis testing market share in 2025; Terpene Profiling is advancing at a 14.39% CAGR through 2031.

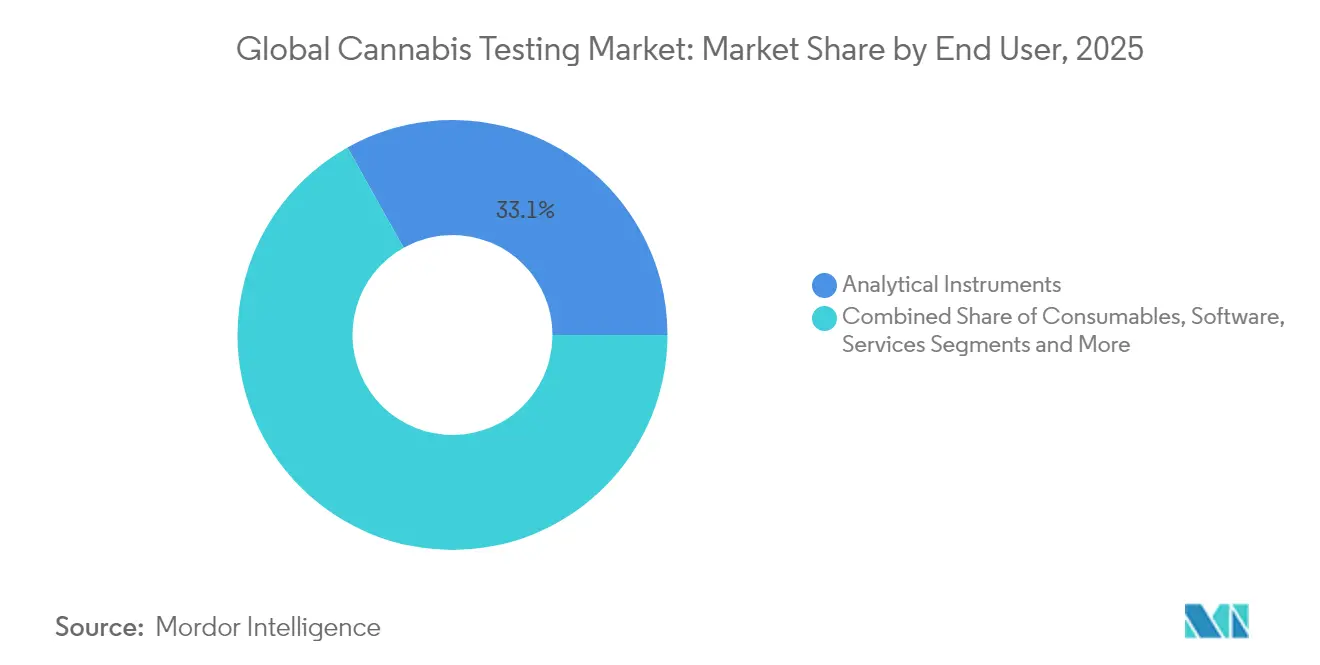

- By end user, Independent Testing Laboratories held 33.12% share of the cannabis testing market size in 2025, while Pharmaceutical & Research Institutes post the fastest CAGR at 13.33% to 2031.

- By geography, North America dominated with 28.15% revenue share in 2025; Asia Pacific is forecast to grow at 11.92% CAGR between 2026-2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Global Cannabis Testing Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legalization of Cannabis Wave Across Few Countries | +2.80% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Mandatory Quality-&-Safety Compliance Testing In All Regulated Markets | +3.20% | Global | Short term (≤ 2 years) |

| Growing R&D Spend On Cannabinoid-Based Pharmaceuticals | +1.90% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Proliferation Of Contract Testing Laboratories In Emerging LATAM & APAC | +1.70% | LATAM & APAC core, spill-over to MEA | Medium term (2-4 years) |

| Premiumization: Minor-Cannabinoid & Terpene Differentiation Needs | +1.40% | North America & EU premium markets | Medium term (2-4 years) |

| Complex Edible/Beverage Matrices Requiring Multi-Residue Methods | +1.20% | Global, with early adoption in mature markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legalization of Cannabis Wave Across Few Countries

Germany’s Cannabis Act in 2024 created the first G-20 adult-use blueprint, prompting other EU members to review prohibition-era rules.[1]German Bundestag, “Cannabisgesetz 2024,” bundestag.de Maryland’s 2025 law permitting on-site consumption lounges mandates full-panel testing for lounge sales, opening a secondary laboratory market. The DEA proposal to move cannabis to Schedule III would remove the federal–state conflict and may unify laboratory standards once hearings conclude in 2025. Thailand’s medical framework positions Bangkok as an Asia Pacific testing hub as regional regulators benchmark its protocols.

Mandatory Quality-&-Safety Compliance Testing In All Regulated Markets

New Jersey’s 2025 rules make a Certificate of Analysis a consumer-facing document listing cannabinoids, contaminants, and water activity.[2]New Jersey Cannabis Regulatory Commission, “Laboratory Testing Guidance 2025,” nj.gov Massachusetts expanded safety panels to include new pesticide classes in 2025, rewarding labs with LC-MS/MS capability. USDA requires hemp labs to register with the DEA by 31 December 2025, foreshadowing a federal gatekeeper role for cannabis once rescheduling clears. Canada raised micro-class production ceilings in March 2025 while keeping full testing, illustrating how mature markets cut red tape without reducing safety.

Growing R&D Spend On Cannabinoid-Based Pharmaceuticals

FDA-aligned inhaler projects, such as Rapid Therapeutic Science Laboratories, require stability, dose uniformity, and extractable leachables studies beyond the scope of normal cannabis panels. Brazil’s ANVISA demands pharmaceutical-quality validation for CBD oral solutions, spurring outsourcing of chromatographic and microbiological assays.[3]Rodrigo P. Piochi, “Medicinal Cannabis in Brazil: Regulatory Advances and Analytical Challenges,” Química Nova, quimicanova.sbq.org.br Raman microscopy coupled with AI now delivers 99.83% cannabinoid classification accuracy, shortening turnaround and raising the bar for potency-plus-profile tests.

Proliferation Of Contract Testing Laboratories In Emerging LATAM & APAC

ONAC accreditation prepares Colombian labs to service regional exports once quota hurdles ease, yet revenue remains muted until customs simplification arrives. Australia’s Therapeutic Goods Administration proposes aligning import and domestic GMP for medicinal cannabis, giving national labs a regional advantage. Hong Kong’s zero-THC mandate on CBD cosmetics forces high-resolution mass spectrometry deployment, a capability few regional labs currently hold.

Restraints Impact Analysis of Global Cannabis Testing Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Operating Cost Of Advanced Analytical Platforms | -1.80% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Fragmented Global Regulatory Standards Cause Result Variability | -2.10% | Global, with concentration in multi-jurisdictional operators | Medium term (2-4 years) |

| Shortage Of Skilled Analysts & Reference Standards | -1.30% | Global, with acute impact in APAC & LATAM | Medium term (2-4 years) |

| "Lab-Shopping" Scandals Eroding Data Credibility | -1.60% | North America & emerging regulated markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital & Operating Cost Of Advanced Analytical Platforms

Triple quadrupole LC-MS/MS units optimized for 200+ pesticides can exceed USD 450,000, limiting adoption in start-ups. A ballistic GC-MS reducing terpene run time to six minutes still demands skilled analysts and custom gases that smaller laboratories cannot absorb. A full cannabis-specific LIMS averages USD 100,000 for licensing and validation, adding to cash burn before revenue scales.

Fragmented Global Regulatory Standards Cause Result Variability

Each US state sets its own action limits, so a California-compliant edible can fail in Oregon, forcing multi-state operators to run duplicate panels. Up to 30% of labs inflated THC in a 2024 California audit, prompting reference methods and proficiency testing by the Department of Cannabis Control. The EU caps industrial hemp THC at 0.2%, while Australia allows 1%, compelling transnational labs to maintain multiple SOPs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Global Cannabis Testing Market Segment Analysis

By Product and Service:

Instruments Drive Infrastructure InvestmentAnalytical Instruments dominated the cannabis testing market in 2025 with 28.02% revenue share, reflecting heavy expenditures on LC-MS/MS, GC-MS, and ICP-MS systems needed for multiresidue panels. Consumables scale proportionally with test volume, securing predictable revenues. Software is projected to grow at a 15.19% CAGR to 2031 as laboratories automate chain-of-custody and integrate AI-based chromatogram review. LC-APCI-MS/MS that quantifies both terpenes and cannabinoids in a single injection demonstrates why software capable of multivariate data interpretation is now imperative.

Instruments account for the largest capital slice, but services capture a rising share as multi-jurisdictional operators outsource validation and method transfer. SaaS LIMS modules embedded with regulatory change alerts help laboratories keep SOPs current, reducing non-conformance risk. Cloud-hosted platforms also enable remote audit, a core requirement for pharmaceutical sponsors.

By Testing Type:

Potency Testing Dominance Challenged by SpecializationPotency Testing held 22.05% of the cannabis testing market share in 2025, remaining compulsory in every regulated jurisdiction. Yet specialization is accelerating. Terpene Profiling, growing at 14.39% CAGR, benefits from brands marketing “effect-based” SKUs whose sensory claims hinge on validated terpene ratios. Residual Solvent and Pesticide Screening expand as extraction technologies diversify and as governments tighten food safety alignment. The National Institute of Justice validated DART-HRMS for rapid THC characterization, indicating future throughput gains for law-enforcement seizures and possibly commercial labs.

Minor cannabinoid panels covering CBG, CBC, and CBDV emerge as differentiators in premium SKUs. Water activity, microbial enumeration, and mycotoxin testing become critical for edibles and inhalables, aligning cannabis test menus with pharmaceutical and food codes.

By End User:

Independent Labs Face Pharmaceutical CompetitionIndependent Testing Laboratories captured 33.12% share of the cannabis testing market size in 2025 and remains the backbone for compliance certificates. However, Pharmaceutical & Research Institutes outpace the field at a 13.33% CAGR as inhalers, transdermals, and nano-emulsion drinks demand cGMP validation. In-house producer labs grow but face conflict-of-interest scrutiny. Vertical integration cases, such as Aurora Cannabis acquiring Anandia Labs, show producers seeking analytical intellectual property alongside compliance cost savings. Academic centers, such as the University of Mississippi’s cannabis program, continue to pioneer reference analytics that diffuse into the commercial sector.

Geography Analysis

North America Cannabis Testing Market

North America contributed 28.15% to global revenue in 2025 and maintains leadership through well-developed regulatory regimes. California revoked four lab licenses between 2024-2025, signaling tougher oversight that favors high-quality operators. Canada raised micro-producer thresholds in 2025 yet retained full mandatory panels, encouraging throughput growth within existing labs. The DEA rescheduling debate continues to cloud interstate commerce, but laboratories prepare SOP harmonization ahead of potential federal standardization.

Europe Cannabis Testing Market

Europe scaled quickly after Germany legalized non-medical adult use in 2024. The European Pharmacopoeia monographs standardize test limits for flower and CBD products, harmonizing methods and increasing equipment spend. France, Italy, and Spain expand medical programs, each requiring EU-GMP compliance that mirrors pharmaceutical quality norms. Laboratories able to certify products for multiple EU tender markets gain pricing power.

APAC Cannabis Testing Market

Asia Pacific is the fastest-growing geography at a projected 11.92% CAGR from 2026-2031. Thailand’s Government Pharmaceutical Organization manufactures medical oils and sets domestic analytic benchmarks adopted by neighbors. Australia’s TGA consults on GMP harmonization that could allow domestic labs to certify imports for ASEAN markets. Hong Kong’s zero-THC rule on CBD mandates high-resolution mass spectrometry, opening niche demand for ultra-low limit assays. Conversely, South Korea retains strict narcotics classification for CBD, restricting lab investment.

Regulatory Landscape

Cannabis testing requirements remain primarily jurisdiction-led, with regulators embedding sampling, action limits, and reporting rules into technical authority documents. In the United States, several states tightened or clarified laboratory requirements during 2025, including Maryland Cannabis Administration updates to its Technical Authority (effective February 2025) and Virginia amendments to 3VAC10-60 (effective February 10, 2025) specifying expectations across microbiological, mycotoxin, and residual solvent testing. Minnesota Office of Cannabis Management also updated its Cannabis Technical Authority (version 1.3 in October 2025) with performance criteria and conflict-of-interest provisions for OCM-licensed laboratories. Across regulated markets, ISO/IEC 17025 accreditation is a common baseline for laboratory competency, supported by accrediting bodies such as ANAB and A2LA.

Beyond cannabis-specific rules, adjacent quality frameworks affect the instrument and software tooling used in testing. The US FDA Quality Management System Regulation (QMSR) aligns device quality-system requirements with ISO 13485:2016, with an effective date in February 2026, raising compliance expectations for regulated device manufacturers whose systems, components, or software may be used in analytical workflows. For clinical research and pharmaceutical-grade cannabinoid development, FDA guidance reinforces quality considerations and reference to recognized standards, pushing labs toward validated methods, traceable chain-of-custody, and audit-ready data integrity controls beyond basic compliance panels.

Value Chain Analysis

The cannabis testing value chain starts with method and standards inputs (reference materials, solvents, columns, sample-prep supplies), then moves through analytical hardware and software (LC-MS/MS, GC-MS, ICP-MS, LIMS) from instrument and consumables vendors. Accredited laboratories perform compliance and specialized assays, and the workflow ends with reporting and regulatory submission or retail-facing Certificates of Analysis. Laboratories operate within state licensing and accreditation frameworks, commonly ISO/IEC 17025 via ANAB or A2LA, and they increasingly feed results into track-and-trace and compliance platforms used by regulators and licensees.

Operational bottlenecks typically center on skilled analyst availability, matrix-driven method complexity (edibles, beverages, concentrates), and access to fit-for-purpose equipment and validated workflows, with many labs adapting general analytical platforms for cannabis. Consolidation and network formation are also reshaping midstream capacity and quality-system standardization, as reflected in Anresco Laboratories and NJ Labs combining into Anresco NJ Labs to build a broader testing network. Regulatory-technology linkages also raise interoperability needs, with Metrc partnering with BioTrack (via BT Government, Inc.) to connect lab data, chain-of-custody, and enforcement systems.

Competitive Landscape

The cannabis testing market remains fragmented; the top five networks hold far below 30% of global revenue, keeping entry opportunities alive. Competitive vectors revolve around analytical speed, breadth of contaminant panels, and data integrity. SC Laboratories combined with Agricor and Botanacor to create a multi-state footprint able to service large multistate operators while maintaining ISO 17025 accreditation. Eurofins Scientific’s historical acquisition strategy in broader analytical services suggests that once federal clarity emerges, similar roll-up plays may advance in cannabis testing.

Technology adoption produces step changes. High-resolution accurate-mass instruments halve turnaround time for metabolite profiling. AI-assisted chromatogram review lowers labor cost and reduces reporting errors. Labs marketing same-day terpene plus potency results command premium fees. Meanwhile, regulatory scrutiny of “lab shopping” forces a race to audit-proof LIMS and proficiency testing participation.

Regional leaders expand through joint ventures rather than outright purchase to navigate license caps. Canadian lab Valens entered Mexico via a service agreement, leveraging GMP credentials without ownership, illustrating the workaround to foreign equity limits.

Global Cannabis Testing Industry Leaders

Shimadzu Scientific Instruments.

Merck KGaA (Sigma Aldrich)

Restek Corporation

PerkinElmer Inc.

Agilent Technologies, Inc

- *Disclaimer: Major Players sorted in no particular order

Global Cannabis Testing Market Companies Covered in this Report

- Agilent Technologies

- Thermo Fisher Scientific

- Shimadzu

- PerkinElmer

- Danaher Corp. (AB SCIEX)

- Merck

- Waters Corporation

- Restek

- Sartorius

- Accelerated Technology Laboratories

- SC Laboratories

- CannaSafe Analytics

- Steep Hill Labs Inc.

- Digipath

- Pharmlabs

- Eurofins

- Aurora Cannabis Inc. (Anandia Labs)

- LabLynx

- ACS Laboratory

- Signal Bay Inc.

Market Opportunities and Future Outlook

Demand is increasing for higher-throughput, more defensible analytics that reduce matrix effects and improve precision across multi-cannabinoid quantification, contaminant panels, and challenging product formats. Peer-reviewed method advances published in 2026, including high-throughput LC-MS/MS approaches for multi-cannabinoid quantification and updated calibration strategies to address matrix effects, support expansion opportunities for instrument vendors, consumables suppliers, and laboratories that can productize these workflows into routine, validated test menus with robust QA/QC. Standardization efforts anchored in ISO/IEC 17025 accreditation and ASTM International Committee D37 programs, including laboratory-focused certification frameworks, also create room for LIMS providers and QA consultancies that can operationalize validation, proficiency testing, and change-control across multi-jurisdictional footprints.

Capacity management and regulator onboarding processes are tightening in newly scaling programs, which opens near-term opportunities for accredited labs and for mobile or satellite sample logistics models. Minnesota Office of Cannabis Management reported 2026 testing bottlenecks tied to lab closures and initiated emergency measures to onboard additional certified labs, highlighting a gap for compliant capacity, rapid onboarding playbooks, and standardized methods that can be replicated across sites. At the governance level, Washington State moved laboratory accreditation oversight from the Liquor and Cannabis Board to the Department of Agriculture, with labs required to comply with updated accreditation standards by December 2024, signaling how governance shifts can reset accreditation and documentation expectations and drive spend on audit-ready systems, method validation services, and proficiency testing participation.

Recent Industry Developments in Global Cannabis Testing Market

- April 2026: Smithers announced an exclusive partnership with CannaMetrix to offer biological potency testing using a patented human cell-based assay. The announcement expands cannabis testing beyond chemical potency into functional response readouts, creating a premium testing tier for product developers and research-led brands.

- October 2025: Anresco Laboratories and NJ Labs completed a merger to form Anresco NJ Labs, creating a broader testing network. The larger footprint supports shared quality systems and standardized methods across regions, which can help multi-state operators reduce variability in results and compliance documentation.

- August 2025: Metrc announced a strategic partnership with BioTrack and established BT Government, Inc. to manage regulatory technology for state programs. Increased interoperability between track-and-trace systems and compliance data flows can raise the importance of consistent lab reporting formats and integration-ready LIMS capabilities.

Global Cannabis Testing Market Report Scope and Research Methodology

Market Definition and Coverage

For this methodology, the cannabis testing market is defined as revenue generated from services and supporting products used to test cannabis and hemp items for quality and regulatory compliance, including potency and contaminant screening across legal markets.

Scope exclusions: Excluded from sizing are purely internal, in-house process checks done by cultivators or manufacturers that are not monetized as testing revenue.

Segments Covered in This Report

- By Product and Service

- Analytical Instruments

- Consumables

- Software

- Services

- By Testing Type

- Potency (THC/CBD)

- Terpene Profiling

- Residual Solvent Screening

- Pesticide Screening

- Heavy Metal Analysis

- Mycotoxin & Microbial Testing

- Other Specialized Assays

- By End User

- Independent Testing Laboratories

- Pharmaceutical & Research Institutes

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping what drives testing demand, which is mainly legal market volumes and the local rules on mandatory panels and sampling frequency. Public sources, such as cannabis regulator rulebooks and lab accreditation directories, are reviewed to understand required tests, reporting formats, and enforcement intensity.

We also reference official trade and health data that help anchor the demand pool, such as state or national cannabis program dashboards, customs and trade statistics for hemp-derived inputs where relevant, and standards and method notes published by organizations like AOAC and ISO, along with peer-reviewed analytical chemistry journals for typical assay workflows. Company filings, investor presentations, and reputable press are used to confirm lab expansion signals, pricing commentary, and instrumentation replacement cycles, and a paid subscription for company financials and news helps verify timelines and ownership changes. These desk sources are illustrative, and other public documents were reviewed for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focuses on lab operators, quality heads at cannabis manufacturers, and procurement roles that buy outsourced tests or instruments, since they can describe real test volumes, panel mix, and pricing movements. We also speak with regulatory and accreditation-facing experts to confirm how consistently rules are applied in practice. Inputs are balanced across APAC, EMEA, and the Americas so regional legalization pace does not skew the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 16% | APAC: 37% |

| Mid tier: 58% | Functional/Unit leaders: 37% | EMEA: 36% |

| Smaller Players: 17% | Managers: 47% | Americas: 27% |

Market-Sizing & Forecasting

Market sizing is built using a top-down approach where legal cannabis and hemp output, together with regulated testing rules, are used to reconstruct a realistic annual testing demand pool by geography. The model then converts demand into revenue by applying average pricing for common panels and by accounting for the product side that supports testing activity.

Key inputs used include the count of licensed labs and their typical throughput utilization, mandatory test-panel composition (potency, residual solvents, pesticides, heavy metals, and microbial or mycotoxin screens), average tests per batch and retest frequency, and the split between third-party testing versus bundled testing done under contract. Assumptions are checked using selective bottom-up approximations, such as sampled price lists and interviews on annual sample volumes, which are then used to adjust totals when a region appears over or under stated capacity.

For forecasting, scenario analysis is used because legalization timelines and enforcement strictness can move faster or slower than a smooth trend. Growth cases are shaped around expected changes in new market openings, shifts toward concentrates and edibles that require wider panels, and productivity changes from lab automation. The final forecast path is aligned to what practitioners described as most likely. Where a country lacks usable public signals, gaps are handled through proxying from similar regulatory markets and then moderated using capacity and licensing checks so the result stays realistic.

Data Validation & Update Cycle

Outputs are validated by comparing implied tests per batch, implied revenue per lab, and year-to-year step changes against independent signals like licensing counts, lab expansion announcements, and changes in mandated panels. If a region shows a sudden jump that is not supported by policy changes or capacity additions, the assumptions are reviewed and, when needed, experts are re-contacted to confirm what changed.

Before sign-off, the model and notes go through a multi-step review so calculations, units, and currency timing stay consistent. Reports are refreshed annually, and interim updates are made when material events occur, such as major rule changes, rapid legalization moves, or notable supply constraints. Right before delivery, a final check is completed so clients receive the most current view available.

Mordor Intelligence's Cannabis Testing Market Size Measured Against Other Published Estimates

Published market sizes for cannabis testing often vary because each publisher draws the market boundary differently and also selects a different year to anchor the estimate. The result is that one figure may lean more toward service revenue, while another may pull in more instruments, software, or certification-related work.

The differences usually come from what gets counted as testing revenue and how regulated demand is translated into dollars, especially when pricing is moving and panel requirements differ by state or country. Some estimates also roll in broader inspection, certification, or R&D services, and others may assume higher testing frequency per batch without a capacity or licensing check, which can push totals upward.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.42 B (2026) | |

| Global Consultancy A | USD 1.84 B (2024) | Uses an earlier base year and a wider service bucket that can include inspection, certification, and R&D services, which raises the counted revenue beyond routine compliance testing. |

| Industry Brief B | USD 2.05 B (2026) | Presents a single-point value aligned to a growth window and does not clearly state whether equipment and consumables are counted only when linked to regulated panel requirements, which can inflate comparability. |

The table shows how year selection and scope choices create most of the spread. In the Mordor Intelligence model, the 2026 value is built from regulated test-panel demand signals (potency, pesticides, heavy metals, residual solvents, and microbial screens) cross-checked with lab licensing and throughput, with non-monetized internal process checks excluded. This makes the total easier to trace back to repeatable inputs like tests per batch, retest rates, and price ranges that can be refreshed when rules or product formats change.

Key Questions Answered in the Report

How big is the Global Cannabis Testing Market?

The Global Cannabis Testing Market size is expected to reach USD 1.42 billion in 2026 and grow at a CAGR of 12.92% to reach USD 2.61 billion by 2031.

What is the current Global Cannabis Testing Market size?

In 2026, the Global Cannabis Testing Market size is expected to reach USD 1.42 billion.

Who are the key players in Global Cannabis Testing Market?

Shimadzu Scientific Instruments., Merck KGaA (Sigma Aldrich), Restek Corporation, PerkinElmer Inc. and Agilent Technologies, Inc are the major companies operating in the Global Cannabis Testing Market.

Which is the fastest growing region in Global Cannabis Testing Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Global Cannabis Testing Market?

In 2025, the North America accounts for the largest market share in Global Cannabis Testing Market.

What years does this Global Cannabis Testing Market cover, and what was the market size in 2025?

In 2025, the Global Cannabis Testing Market size was estimated at USD 1.42 billion. The report covers the Global Cannabis Testing Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Cannabis Testing Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: