Canine Atopic Dermatitis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

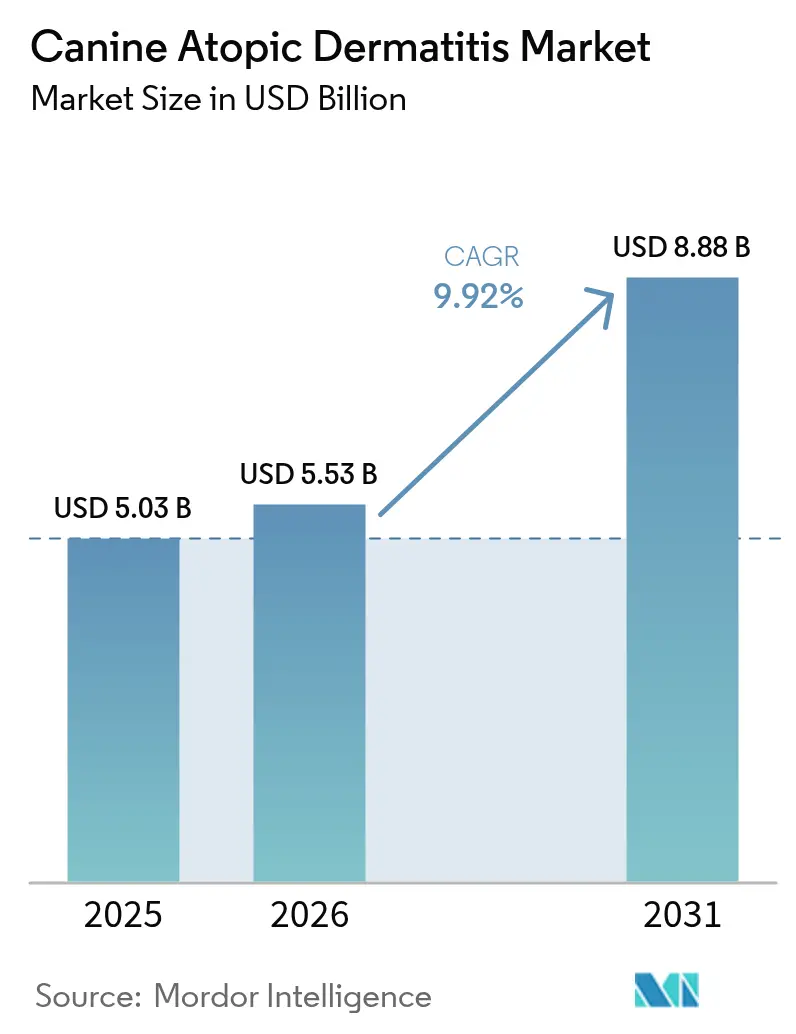

| Market Size (2026) | USD 5.53 Billion |

| Market Size (2031) | USD 8.88 Billion |

| Growth Rate (2026 - 2031) | 9.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canine Atopic Dermatitis Market Analysis by Mordor Intelligence

The canine atopic dermatitis market size in 2026 is estimated at USD 5.53 billion, growing from 2025 value of USD 5.03 billion with 2031 projections showing USD 8.88 billion, growing at 9.92% CAGR over 2026-2031. Rapid sales growth in targeted biologics, rising pet humanization, and wider veterinary insurance coverage are the leading contributors. Veterinarians pivot toward precision therapy that tackles specific inflammatory pathways, while pet owners increasingly accept premium pricing for treatments positioned as quality-of-life investments. Regulatory agencies in the United States and European Union have introduced expedited approval programs that shorten development timelines for novel dermatology drugs[1]Food and Drug Administration, “Animal and Veterinary Innovation Agenda,” fda.gov. The convergence of these drivers sustains double-digit revenue gains for manufacturers, firmly establishing dermatology as a strategic pillar in companion-animal health portfolios.

Key Report Takeaways

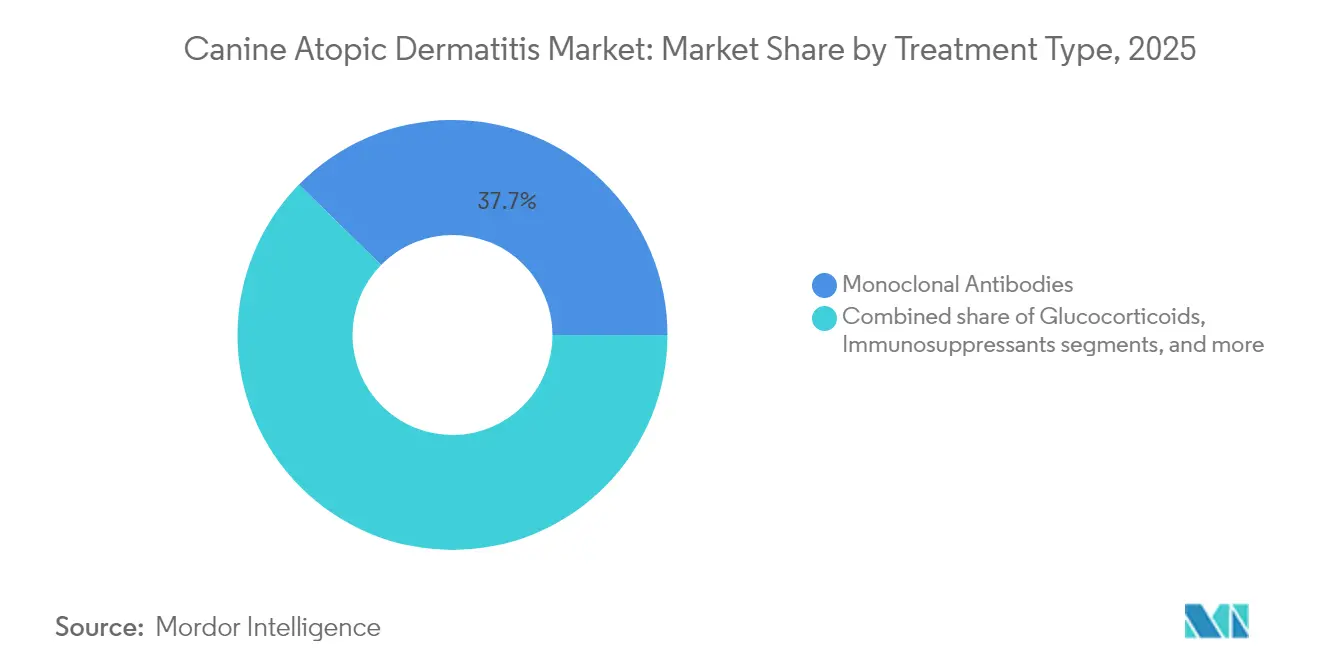

- By treatment class, monoclonal antibodies led with 37.66% of canine atopic dermatitis market share in 2025; stem-cell and exosome therapies are projected to grow fastest at 12.12% CAGR through 2031.

- By route of administration, oral formulations accounted for 51.92% of revenue in 2025, while injectables are advancing at an 11.05% CAGR through 2031.

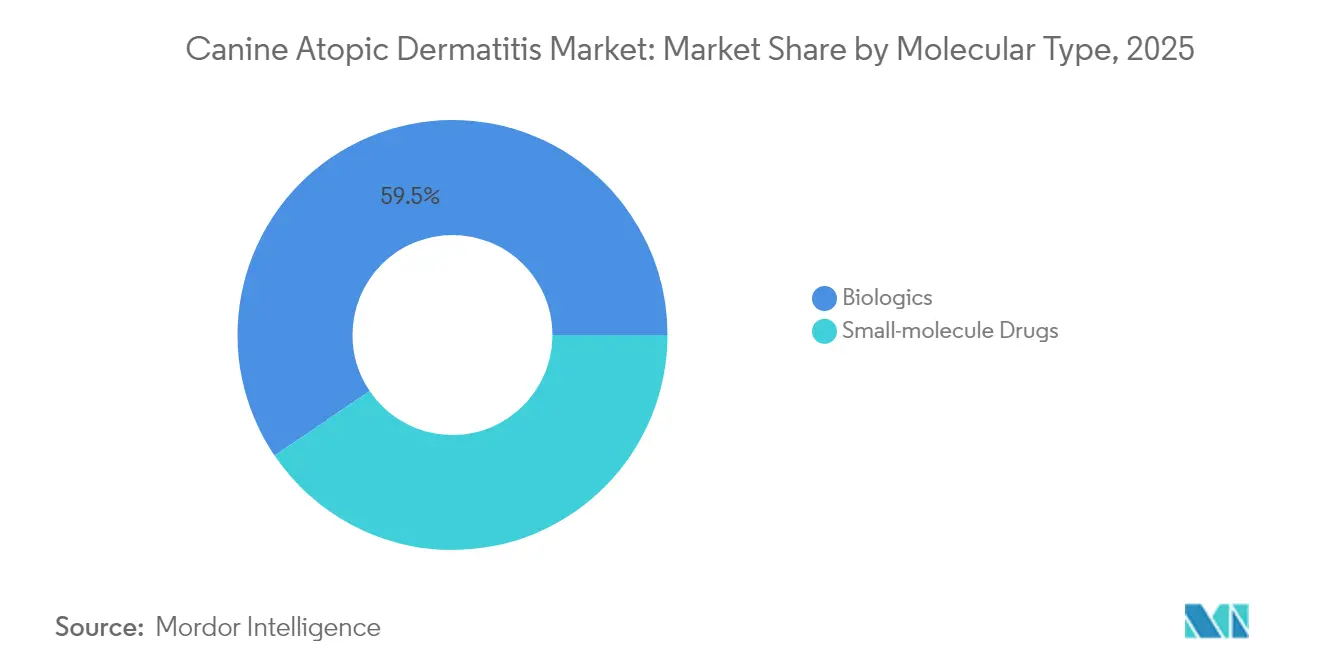

- By molecule type, biologics commanded 59.48% of the canine atopic dermatitis market size in 2025 and are forecast to expand at a 10.34% CAGR to 2031.

- By distribution channel, veterinary clinics held 44.03% share in 2025; veterinary hospitals and referral centers exhibit the highest projected CAGR at 12.78% through 2031.

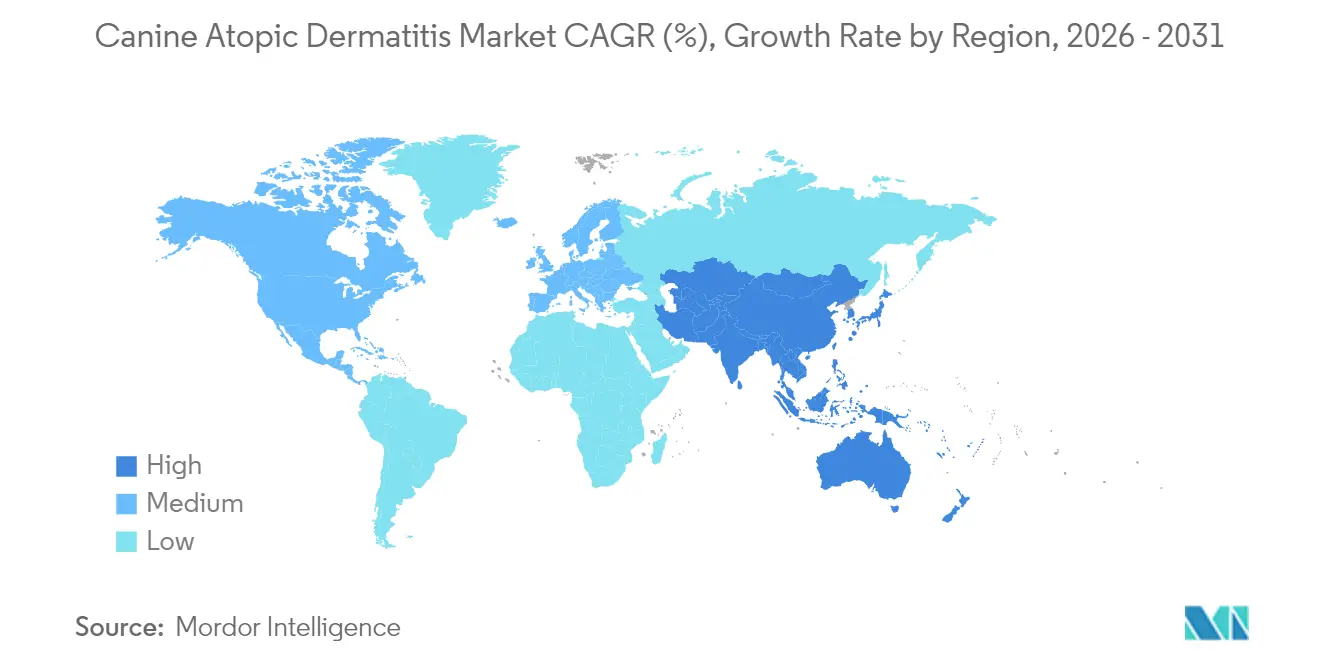

- By geography, North America captured 41.88% revenue share in 2025, whereas Asia-Pacific is set to log the fastest growth at 11.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Canine Atopic Dermatitis Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of canine allergic skin disorders | +2.1% | Global, highest in developed regions | Medium term (2-4 years) |

| Growing companion-animal healthcare spend & insurance coverage | +1.8% | North America & Europe, extending to Asia-Pacific | Long term (≥ 4 years) |

| Accelerated regulatory pathways for veterinary biologics | +1.4% | Global, led by the FDA and EMA | Short term (≤ 2 years) |

| Expansion of pet e-commerce improving prescription access | +1.2% | Urban areas worldwide | Medium term (2-4 years) |

| Advances in long-acting biologics & targeted small molecules | +1.6% | Early uptake in premium markets | Medium term (2-4 years) |

| Precision dermatology diagnostics enabling earlier intervention | +0.9% | North America & Europe first, then global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Canine Allergic Skin Disorders

Global incidence is climbing to an estimated 10–15% of the dog population, with Golden Retrievers, Labrador Retrievers, and German Shepherds showing heightened risk. Environmental allergens such as house-dust mites drive persistent pruritus that warrants continuous medical management. Climate change and urbanization elevate allergen load, while diagnostic complexity often delays therapy onset because definitive diagnosis requires meeting at least five of Favrot’s criteria. As veterinarians reclassify atopic dermatitis as a lifelong condition demanding chronic care, consistent demand lifts the canine atopic dermatitis market.

Accelerated Regulatory Pathways for Veterinary Biologics

The FDA’s Animal and Veterinary Innovation Agenda and the EMA’s parallel initiatives compress review times via adaptive trial design, expanded conditional approvals, and AI-enabled toxicology models. Conditional approvals under the Minor Use and Minor Species Act grant seven-year exclusivity, stimulating innovation for niche dermatology indications. These programs lower capital risk and hasten market entry, directly enlarging the canine atopic dermatitis market.

Advances in Long-Acting Biologics & Targeted Small Molecules

Monthly injectable biologics such as Cytopoint demonstrated superior owner adherence compared with daily tablets. JAK inhibitors like Elanco’s Zenrelia provide rapid itch relief while limiting systemic immunosuppression, capturing switch patients from corticosteroids[2]Elanco Animal Health, “2024 Form 10-K,” elanco.com. R&D pipelines now target multiple cytokines simultaneously, seeking synergistic efficacy. Enhanced convenience and efficacy spur sustained uptake across all practice types, supporting continued double-digit expansion in the canine atopic dermatitis market.

Precision dermatology diagnostics enabling earlier intervention

Point-of-care imaging, AI-based lesion scoring, and wearable behavior trackers achieve 87.5% concordance with specialist assessment, prompting earlier therapy starts[3]MDPI Animals, “Stem-Cell Therapy in Canine Dermatitis,” mdpi.com. Standardized allergen panels refine treatment selection and support tailored immunotherapy. Practices adopting these tools report higher client satisfaction and better clinical outcomes, reinforcing demand for advanced drugs.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & reimbursement gaps for novel biologics | -1.9% | Global, sharper in price-sensitive markets | Medium term (2-4 years) |

| Shortage of veterinary dermatology specialists in emerging markets | -1.3% | Asia-Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Biologic cold-chain and fill-finish capacity bottlenecks | -0.8% | Worldwide, acute in temperature-extreme areas | Short term (≤ 2 years) |

| Rising scrutiny over long-term immunomodulator safety | -0.7% | Global regulators, strictest in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost & Reimbursement Gaps for Novel Biologics

Monthly monoclonal antibody injections exceed USD 100 per dose, pushing annual treatment beyond the budgets of many households. Although insurance coverage is broadening, exclusions for pre-existing conditions and annual benefit caps still leave significant out-of-pocket exposure. Tiered pricing, patient-assistance programs, and on-label generic entry could ease pressure, yet affordability remains a binding constraint in developing economies.

Shortage Of Veterinary Dermatology Specialists in Emerging Markets

The Federation of Veterinarians of Europe highlights specialist shortages even within mature regions, an issue amplified in Asia-Pacific and Latin America where postgraduate dermatology programs are scarce. Limited access to board-certified expertise slows accurate diagnosis, curbs biologic prescription, and dampens regional uptake in the canine atopic dermatitis market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Class: Biologics Reshape Therapeutic Paradigms

Biologics, led by monoclonal antibodies, held 37.66% of revenue in 2025, translating into the single largest tranche of canine atopic dermatitis market share. Stem-cell and exosome therapies are gaining prominence at a 12.12% CAGR and are widely viewed as the next innovation wave, thanks to data showing improved skin-barrier integrity without systemic adverse events. Traditional glucocorticoids retain a niche in acute flare management but face displacement as veterinarians prefer targeted immune modulation. Immunosuppressants such as cyclosporine are under pressure from selective JAK inhibitors offering faster itch relief with fewer metabolic effects.

The competitive pipeline is increasingly diversified. Ongoing trials explore mesenchymal stem-cell–derived exosomes packaged via nano-liposomes to boost epidermal uptake and prolong therapeutic presence. Regenerative approaches that combine cell therapy with targeted biologics aim to halt pruritus while repairing structural damage, positioning “one-two punch” protocols for widespread adoption. These developments reinforce the leadership of biologics and regenerate-based solutions in the canine atopic dermatitis market.

By Route of Administration: Convenience Drives Oral Dominance

Oral medications represented 51.92% of 2025 revenue, underlining pet owner preference for familiar pill or chewable formats that fit daily routines. Injectables, however, are expanding at 11.05% CAGR as long-acting biologics deliver monthly relief and reduce missed doses. Topical preparations retain utility for focal lesions but seldom suffice for generalized disease.

Long-acting injectables improve compliance by requiring only four to six veterinary visits per year. Industry pipelines also feature transdermal microneedle arrays that could provide depot delivery without needles, a potential breakthrough for needle-averse owners. Meanwhile, flavor-masking technologies and smaller tablet sizes are being introduced to cut pill rejection rates, ensuring oral products sustain their prominent position within the canine atopic dermatitis market.

By Molecule Type: Biologics Establish Market Leadership

Biologics generated 59.48% of 2025 revenue and are forecast to grow 10.34% annually through 2031, reinforcing their primacy in the canine atopic dermatitis market size avma. Small-molecule options remain relevant for cost-sensitive clients and rapid onset needs, yet their share is gradually eroding. Biosimilar entrants could temper biologic pricing over time, though complex manufacturing sustains barriers to commoditization.

Next-generation monoclonal antibodies now target multiple cytokines in a single construct, seeking additive efficacy without higher dosing. R&D in oral JAK inhibitors aims to blend small-molecule convenience with biologic-level selectivity, extending choice along the cost-benefit continuum. The interplay of these modalities supports steady overall market growth while offering differentiated value propositions to varied customer segments.

By Distribution Channel: Specialization Drives Hospital Growth

Veterinary clinics maintained 44.03% revenue share in 2025, reflecting their role as first-contact care providers. Referral hospitals and specialty centers are projected to grow 12.78% annually as biologic regimens necessitate advanced diagnostics, follow-up titration, and pharmacovigilance fve. Retail and online pharmacies compete on refill convenience and price, although legal mandates still require veterinarian oversight for prescription sales.

Private-equity–backed consolidation is accelerating, assembling regional networks of dermatology-focused clinics capable of handling complex cases and clinical trials. At the same time, digital pharmacy partnerships allow brick-and-mortar practices to offer home delivery without surrendering prescription control. This hybrid distribution model underpins evolving service demand across the canine atopic dermatitis market.

Geography Analysis

North America commanded 41.88% of global revenue in 2025, benefiting from USD 38.3 billion of pet healthcare spending and a large pool of dermatology specialists. The region also hosts leading manufacturers and a robust clinical-trial infrastructure, facilitating rapid uptake of first-to-market biologics. Regulatory agility under the FDA’s Veterinary Innovation Program further cements North America’s dominance in the canine atopic dermatitis market.

Asia-Pacific is advancing fastest at 11.21% CAGR thanks to sustained growth in China’s USD 42 billion pet-care sector and expanding middle classes across India, Japan, and Southeast Asia cfaw. Urbanization, rising disposable income, and improving veterinary infrastructure combine to widen product accessibility. Still, specialist shortages and fragmented distribution pose obstacles that manufacturers must address with localized training and robust cold-chain investment.

Europe remains a steady contributor. Centralized EMA approvals enable region-wide launches, while heightened welfare standards spur interest in therapies avoiding long-term corticosteroid use. Workforce deficits and Brexit-related logistics challenges marginally temper growth, yet consistent insurance coverage and high owner awareness secure ongoing demand for premium options in the canine atopic dermatitis market.

Competitive Landscape

The market shows moderate concentration. Zoetis, Inc. controls roughly 16.0% of global animal-health revenue and earns 18.0% of corporate sales from dermatology products such as Apoquel and Cytopoint. Elanco Animal Health holds 12.0% and has disrupted incumbents with Zenrelia, a daily JAK inhibitor priced competitively while achieving superior remission rates. Boehringer Ingelheim and Merck Animal Health round out the top tier at roughly 13.0% and 12.0%, respectively, together exerting oligopolistic influence.

Strategic priorities include lifecycle extension for flagship brands through chewable formats, pediatric indications, and combination biologic offerings. Digital health add-ons, notably AI-enabled diagnostic platforms, differentiate service portfolios and anchor brand loyalty dvm360. Mid-cap firms such as Virbac and Nextmune pursue region-centric or niche biologic strategies, often positioning themselves for partnership or acquisition. Consolidation momentum remains strong as scale efficiencies in R&D and distribution underpin competitive advantage within the canine atopic dermatitis market.

Canine Atopic Dermatitis Industry Leaders

Zoetis Inc.

Elanco Animal Health

Virbac

Ceva Santé Animale

Dechra Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Medicus Pharma obtained Minor Use in Major Species designation for a microneedle array therapy, opening a seven-year exclusivity path biospace.

- May 2025: Merck Animal Health received FDA approval for MOMETAMAX Single, broadening its dermatology range.

- April 2025: The FDA announced plans to phase out animal testing for monoclonal antibodies in favor of AI-based models.

- February 2025: Elanco reported USD 4.439 billion 2024 revenue, citing Zenrelia approvals in Brazil, Canada, and Japan.

- February 2025: Zoetis disclosed dermatology contributions of 18% to 2024 revenue and pledged increased AI-discovery investment.

- January 2025: Kane Biotech sold its STEM Animal Health division to Dechra for USD 12.5 million, signaling continued sector consolidation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts global revenue from prescription and over-the-counter pharmacologic or biologic therapies expressly approved to prevent, soothe, or cure allergen-driven skin inflammation in dogs, irrespective of route or molecule.

Scope exclusion: We exclude non-medicated shampoos, feline-only products, and clinic service fees.

Segmentation Overview

- By Treatment Class

- Glucocorticoids

- Immunosuppressants

- Monoclonal Antibodies

- Stem-cell/Exosome Therapies

- Other Testment Classess

- By Route of Administration

- Topical

- Oral

- Injectable

- By Molecule Type

- Small-molecule Drugs

- Biologics

- By Distribution Channel

- Veterinary Hospitals & Referral Centers

- Veterinary Clinics

- Retail & Companion-Animal Pharmacies

- Online Pet Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We conducted semi-structured interviews with small-animal dermatologists, hospital buyers, and distributors across North America, Europe, and Asia-Pacific. This clarified treated-dog shares, average selling prices, and adoption curves for new JAK inhibitors and monoclonal antibodies.

Desk Research

We mapped approved actives and patent cliffs through the US FDA Green Book, USDA-APHIS, and EMA listings, while PubMed and the Journal of Veterinary Dermatology furnished prevalence ratios. We also harvested ownership and spend patterns from AVMA, FEDIAF, and insurance dashboards such as Nationwide.

To cross-check revenue signals, we pulled trade data from UN Comtrade, parsed company 10-Ks via D&B Hoovers, and monitored Dow Jones Factiva alerts for launches and recalls. The sources named are illustrative; many additional publications informed data capture, validation, and context.

Market-Sizing & Forecasting

A prevalence-to-treated pool, developed through a top-down build, anchored 2025 spend. Sampled ASP × volume roll-ups then served as bottom-up checks. Variables such as dog counts, insurance uptake, biologic price erosion, refill compliance, approval cadence, and household income fuel the model. A five-driver multivariate regression guides 2026-2030 projections, while scenario sweeps adjust for sudden price caps. Expert calls filled residual data gaps.

Data Validation & Update Cycle

Our outputs pass automated variance scripts, peer review, and senior sign-off. We refresh annually and reopen the model whenever pivotal approvals or safety withdrawals arise.

Why Mordor's Canine Atopic Dermatitis Baseline Commands Reliability

Published values diverge because other firms juggle different scopes, price bands, and refresh rhythms. Our strict inclusion of every therapy cleared by Q3-2025 and yearly updates curb those drifts.

Common gap drivers elsewhere include skipped 2024 biologic launches, fixed 2023 exchange rates, or mixing feline revenue with canine.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.03 Bn (2025) | Mordor Intelligence | - |

| USD 4.86 Bn (2024) | Global Consultancy A | Biologics omitted; outdated FX |

| USD 3.21 Bn (2024) | Industry Association B | Only oral steroids; biennial update |

Mordor's transparent, repeatable approach yields a dependable baseline that product and investment teams can trust.

Key Questions Answered in the Report

What is the current value of the canine atopic dermatitis market?

The canine atopic dermatitis market size is USD 5.53 billion in 2026 and is forecast to reach USD 8.88 billion by 2031.

Which treatment class generates the highest revenue?

Monoclonal antibodies lead, accounting for 37.66% of 2025 sales, underscoring the shift toward targeted biologics.

Why are injectables growing faster than oral medications?

Long-acting injectable biologics require fewer doses, boosting owner compliance and driving an 11.05% CAGR for the segment.

Which region is expanding quickest?

Asia-Pacific is growing at 11.21% CAGR, propelled by rising pet ownership, expanding middle classes, and improving veterinary infrastructure.

Who are the major players in this market?

Zoetis, Elanco, Boehringer Ingelheim, and Merck Animal Health form the top tier, together controlling more than half of global revenue.

What key factor could slow market growth?

High biologic treatment costs and incomplete insurance coverage remain the most significant restraint, particularly in price-sensitive markets.

Page last updated on: