Canada Data Center Construction Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

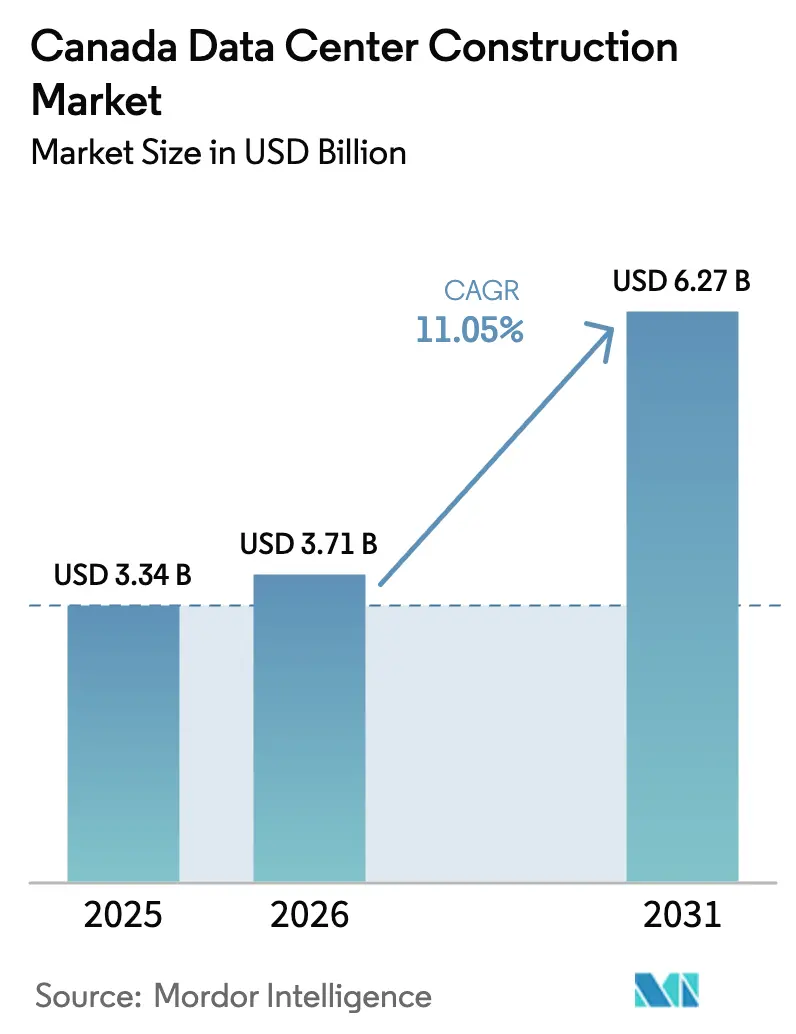

| Base Year Market Size (2025) | USD 3.34 Billion |

| Market Size (2026) | USD 3.71 Billion |

| Market Size (2031) | USD 6.27 Billion |

| Growth Rate (2026 - 2031) | 11.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Data Center Construction Market Analysis by Mordor Intelligence

The Canada data center construction market size was valued at USD 3.34 billion in 2025 and estimated to grow from USD 3.71 billion in 2026 to reach USD 6.27 billion by 2031, at a CAGR of 11.05% during the forecast period (2026-2031). This growth is powered by Ottawa’s CAD 2.4 billion (USD 1.75 billion) sovereign AI compute package, hyperscale capital-expenditure programs, and abundant low-carbon hydroelectric capacity. Hyperscalers are pivoting from leased colocation halls to purpose-built campuses, spurring a rapid shift in design norms toward high-density racks, liquid cooling, and on-site generation. Alberta’s 1.2 GW phased grid-connection framework is accelerating self-build projects, while Quebec and British Columbia attract investment with renewable baseloads despite tighter water-use rules. Skilled-labor shortages and 4.3% year-over-year inflation in non-residential construction costs are lifting capital intensity, but bulk-procurement tactics and joint ventures with power developers are easing some pressure.

Key Report Takeaways

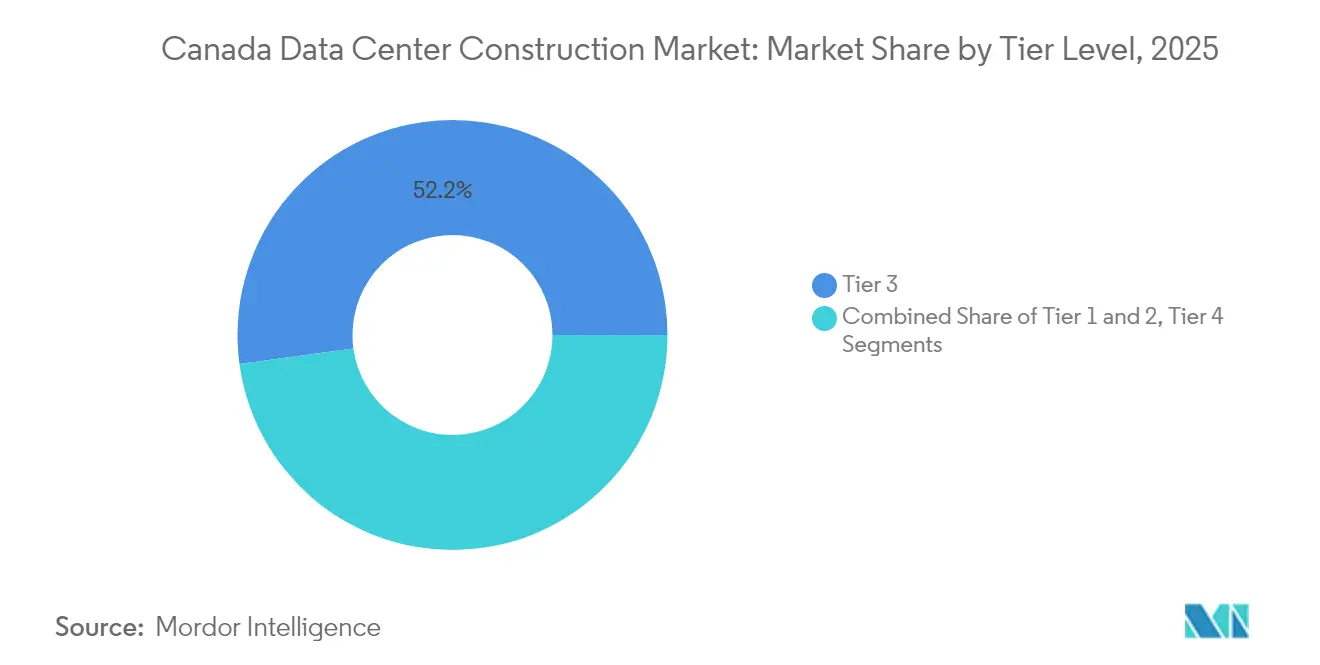

- By tier type, Tier 3 installations commanded 52.15% of the Canada data center construction market share in 2025, while Tier 4 projects are projected to post the fastest 12.95% CAGR to 2031.

- By data-center type, colocation facilities held 53.95% revenue share of the Canada data center construction market size in 2025; self-build hyperscalers are forecast to expand at 11.88% CAGR through 2031.

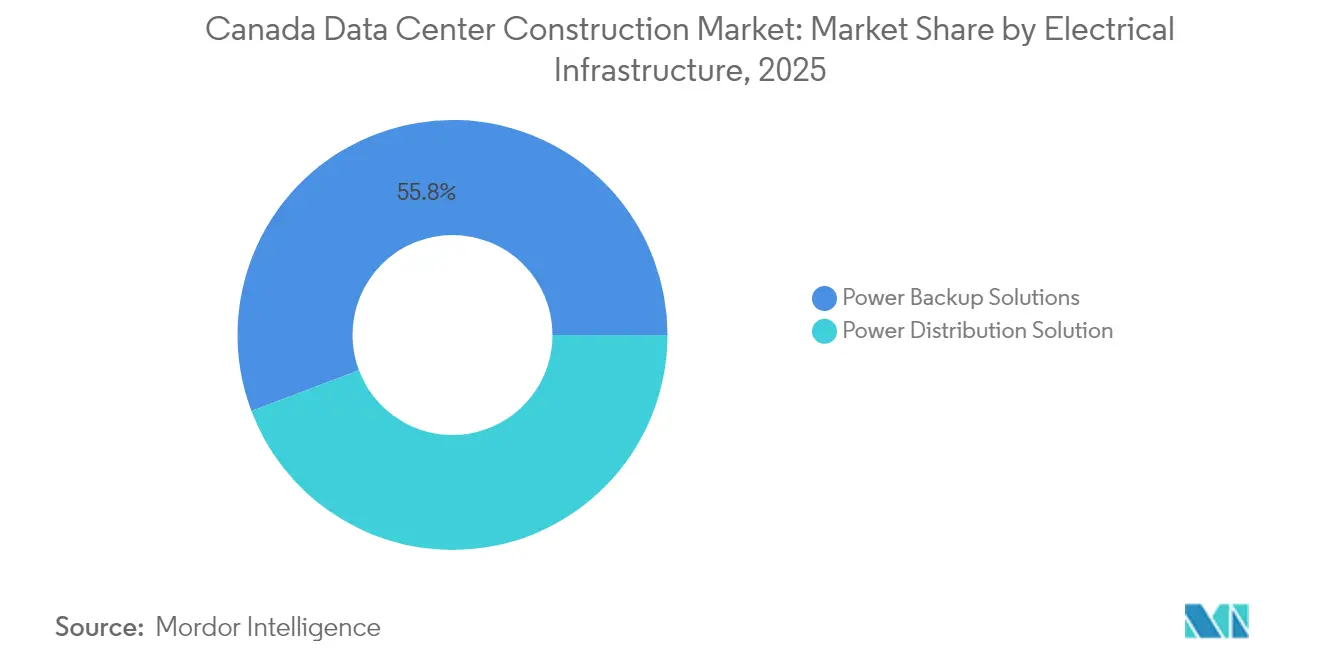

- By electrical infrastructure, power-backup systems accounted for 55.75% spending in 2025; power-distribution solutions lead growth at 13.02% CAGR to 2031.

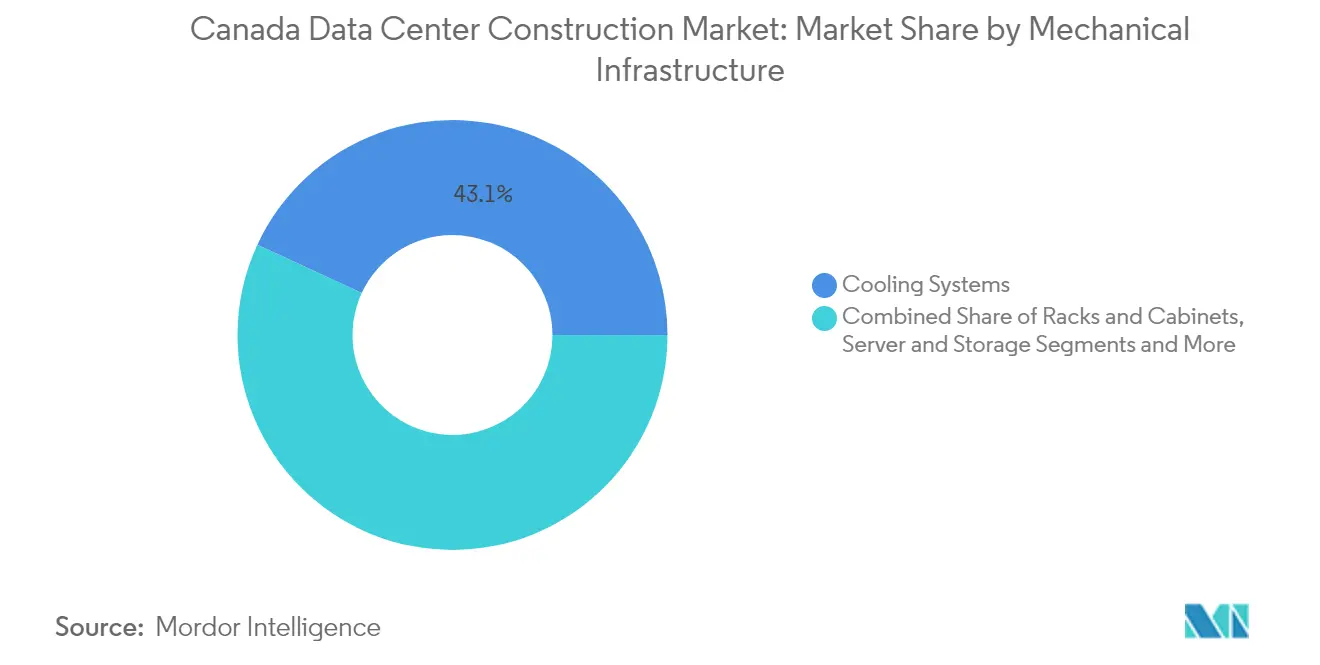

- By mechanical infrastructure, cooling systems captured 43.10% share of the Canada data center construction market size in 2025; servers and storage register the highest 12.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring cloud and AI workload demand | +2.8% | Global, with concentration in Toronto, Montreal, Calgary | Medium term (2-4 years) |

| Accelerating hyperscale CAPEX commitments | +2.1% | Alberta, Ontario, British Columbia | Short term (≤ 2 years) |

| Federal CAD 2.4 billion (USD 1.74 billion) Sovereign AI Compute Strategy | +1.9% | National, with early gains in Toronto, Calgary, Montreal | Medium term (2-4 years) |

| Abundant low-carbon hydro-power capacity | +1.6% | Quebec, British Columbia, Ontario | Long term (≥ 4 years) |

| Alberta's 1.2 GW phased grid-connection program | +1.4% | Alberta, with spillover to Saskatchewan | Short term (≤ 2 years) |

| Adaptive-reuse of vacant industrial assets | +0.8% | Toronto, Montreal, Vancouver metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Soaring Cloud and AI Workload Demand

AI inference and training jobs consume 160% more energy than conventional workloads, prompting builders to specify liquid cooling, reinforced flooring, and surge-ready electrical topologies.[1]Canada Energy Regulator, “Energy Demand Outlook for AI Workloads,” cer-rec.gc.caBell Canada’s 500 MW AI supercluster in British Columbia illustrates how AI demand is dictating province selection, cooling modality, and megawatt scale. Developers now design for rack power densities that routinely exceed 50 kW. Grid interconnection studies incorporate transient peak-load modelling, and contracts with hydro utilities embed priority-service clauses that reduce downtime risk. The Canada data center construction market, therefore, sees growing bids for modular chillers, immersion cooling vats, and high-amp busways that minimize stranded capacity.

Accelerating Hyperscale CAPEX Commitments

AWS, Microsoft, and Google are redirecting multi-tenant budgets toward single-tenant Canadian campuses aligned with AI compute roadmaps. eStruxture’s 90 MW CAL-3 project in Calgary shows how hyperscalers value greenfield parcels that allow 100 acre layouts and tax-advantaged power-purchase agreements.[2]eStruxture Data Centers, “CAL-3 Hyperscale Campus Announcement,” estruxture.comCapital intensity exceeds USD 11 million per MW because facilities integrate on-site switchyards and three-stage liquid-cool loops. Longer lead times for transformers and generators are prompting design-build contracts with fixed-price escalation clauses. The Canada data center construction market is therefore experiencing a shift in tender criteria, rewarding contractors with pre-secured power-equipment supply chains

Federal CAD 2.4 Billion (USD 1.74 billion) Sovereign AI Compute Strategy

Ottawa’s program mandates that datasets and compute remain on Canadian soil, pushing builders to deliver Tier 4-equivalent redundancy plus isolated meet-me rooms. Cohere’s federally backed campus will include electromagnetic shielding and multi-factor security perimeters, boosting per-square-foot spend. Domestic ownership clauses favour Canadian REITs and pension funds, tightening local capital pools. Consequently, the Canada data center construction market is pivoting toward alliances that blend civil-works firms with cybersecurity specialists to satisfy bespoke bid specifications.

Abundant Low-Carbon Hydro-Power Capacity

Hydro-Québec’s CAD 50 billion (USD 36.42 billion) grid-expansion plan underwrites long-term renewable capacity, yet 2023 drought-induced export cuts remind planners to provision dual-fuel backup. Wonder Valley’s 1.4 GW off-grid campus pairs gas turbines with geothermal wells, reducing grid-interconnect delays.[3]Government of Alberta, “Wonder Valley Off-Grid Power Project Details,” alberta.caContractors must therefore integrate medium-voltage switchgear, black-start turbines, and heat-recovery chillers during initial pours. These hybrid designs lift mechanical-electrical-plumbing complexity and keep the Canada data center construction market on a steep learning curve for power-system integration.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-level power-availability bottlenecks | -1.8% | Alberta, Ontario, with emerging constraints in Quebec | Short term (≤ 2 years) |

| Escalating construction & MEP equipment costs | -1.2% | National, with highest impact in Toronto, Vancouver | Medium term (2-4 years) |

| Shortage of Uptime-tier-certified labour | -0.9% | National, particularly acute in specialized MEP trades | Long term (≥ 4 years) |

| Municipal water-use limits on liquid cooling | -0.6% | British Columbia, select Ontario municipalities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Level Power-Availability Bottlenecks

Alberta’s system operator now caps new load at 1.2 GW, compelling developers to commission on-site generation before permitting. Pembina and Kineticor’s 1.8 GW gas plant, dedicated to data-center clients, extends build cycles by up to 18 months. Land negotiations must now coordinate pipeline easements and emissions-offset plans alongside traditional zoning. These factors lengthen critical-path schedules, constraining near-term capacity additions across the Canada data center construction market.

Escalating Construction and MEP Equipment Costs

Non-residential building costs rose 4.3% year over year in Q2 2024, outpacing headline inflation . UPS, chiller, and switchgear manufacturers report lead times stretching beyond 60 weeks, driving bulk-purchase consortiums among builders. Pipe, valve, and fitting spend is forecast at CAD 42.5 billion (USD 30.89 billion) for 2025, squeezing subcontractor cash flows. Contractors are passing through indexed material clauses and adopting prefab modular skids to reduce site labor. The Canada data center construction market therefore faces margin compression that could deter smaller entrants lacking scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tier Type: Tier 4 Drives Premium Construction

The Canada data center construction market size allocated to Tier 3 facilities stood at USD 1.74 billion in 2025, yet Tier 4 projects post the leading 12.95% CAGR. Tier 4 specifications mandate dual power trains, isolated switchboards, and concurrently maintainable paths, lifting capex by more than 40% per MW. Borden’s CAD 322 million (USD 234.51 million) expansion that achieved Tier III certification showcases federal appetite for fault-tolerant assets. Contractors with Uptime Institute credentials command pricing premiums, and training pipelines lag demand, limiting bid competition across the Canada data center construction market. Standards Council of Canada’s immersion-cooling fluid code advances specialist fluid-handling skills that further differentiate Tier 4 builders.

Second-generation operators still refurbish legacy Tier 2 halls, but new enterprise workloads push procurement teams toward Tier 3 minimums. Insurance underwriters are tightening uptime covenants, prompting risk-sharing clauses that embed performance penalties. These trends sustain the Tier 4 momentum, underscoring rising technical-barrier moats in the Canada data center construction industry.

By Data Center Type: Hyperscaler Self-Build Momentum

Colocation still dominates with 53.95% revenue share of the Canada data center construction market size in 2025, but self-built hyperscale campuses race ahead at 11.88% CAGR. Bell Canada’s six-site AI Fabric demonstrates how telecom incumbents spin up vertically integrated builds to guarantee GPU access. CoreWeave’s tie-up with Cohere illustrates collaboration between AI model developers and infrastructure financiers. Builders respond by pre-leasing adjacent parcels to enable 100-MW add-on phases. Edge and enterprise footprints grow incrementally, favoring 5–15 MW standardized shells that can be deployed in 9–12 months, a cadence well-suited to metropolitan retail bandwidth demand.

Contractors therefore diversify product lines, offering both hyperscale mega-campus frameworks and prefabricated edge pods. The Canada data center construction market consequently exhibits a bimodal project-size distribution, with few mid-tier builds outside adaptively reused industrial stock.

By Electrical Infrastructure: Power Backup Solutions Lead

Power-backup assets represented 55.75% of electrical-infrastructure spend in 2025 as AI workloads heighten risk tolerance thresholds. The Canada data center construction market share for power-distribution systems is climbing on a 13.02% CAGR, driven by bus-duct retrofits that handle growing rack amperage. Wonder Valley’s 1.4 GW hybrid station demonstrates scale requirements when public grids lag. Natural Resources Canada’s revised energy-efficiency rules spur adoption of high-efficiency UPS blocks that cut PUE but raise capital cost.

Demand for intelligent switchgear that dynamically routes power between utility feeds, gas turbines, and battery farms is surging. Electrical contractors with in-house SCADA teams gain competitive edge as real-time energy management becomes a procurement criterion in the Canada data center construction market.

By Mechanical Infrastructure: Cooling Systems Evolution

Cooling systems captured 43.10% spend in 2025, yet servers and storage assemblies grow fastest at 12.29% CAGR as GPU-rich nodes proliferate. British Columbia’s ban on once-through potable-water cooling after 2028 is pushing designs toward closed-loop adiabatic and immersion systems. CSA B52:23 refrigerant code revisions add installation checkpoints for low-GWP blends, lengthening inspection timelines.

Immersion-cool tanks enable 100 kW-plus rack densities, but they require dielectric-fluid handling and vapor-recovery gear, enlarging mechanical-room footprints. Contractors invest in fluid-technician certification programs to stay bid-eligible. The Canada data center construction industry therefore intersects with chemical-safety regulation, forcing firms to master multi-disciplinary compliance.

Geography Analysis

Alberta leads near-term capacity additions due to CAD 100 billion( USD 72.83 billion) policy backing and competitively priced gas. Its 1.2 GW phased grid-connection pathway lowers queue uncertainty, catalyzing eStruxture’s 90 MW CAL-3 build, Beacon AI’s 400 MW blueprint, and Wonder Valley’s off-grid 1.4 GW park. Provincial regulators fast-track brownfield wellsites for substation placement, compressing locality approval cycles within the Canada data center construction market.

Ontario retains the largest installed base with 93 sites across 291 MW, anchored in Toronto’s financial hub. Adaptive reuse of industrial shells is prevalent; DuPont Fabros converted a printing plant in Vaughan into a 46 MW hall at CAD 41.6 million (USD 30.30 million), evidencing the viability of repurposing to overcome scarce greenfield plots. Construction costs run CAD 280–350 sq ft (USD 203.93- 254.91), challenging project economics, but offset by fiber richness and talent access.

Quebec and British Columbia appeal to operators seeking renewable baseloads. Hydro-Québec’s CAD 50 billion(USD 36.42 billion) transmission plan enables 5,000 km of new lines through 2035, supporting QScale’s GPU-ready campus backed by Aligned Data Centers and Desjardins Capital. British Columbia hosts Bell Canada’s 500 MW AI supercluster, leveraging cool ambient temperatures for free-air cooling nine months per year

Competitive Landscape

Industry structure is tightening as pension funds and infrastructure investors consolidate construction platforms. Fengate’s CAD 1.8 billion outlay for eStruxture exemplifies capital pooling that accelerates multi-province rollout. EllisDon deepens its technology depth with Palantir and Scale AI partnerships to forecast cost overruns and schedule slippage. H5 and Novacap’s joint venture adds private-equity dry powder, enabling rapid site acquisition aligned with hyperscale pre-leases.

Traditional contractors such as Bird Construction pivot into data-center-adjacent works, winning CAD 575 million(USD 418.78 billion) in industrial foundations that overlap power-station scopes. Specialist players holding Uptime Institute and CSA B52 credentials command premiums, creating a two-tier vendor pool in the Canada data center construction market. Technology adoption—digital twins, drone progress scans, and AI-driven quality checking—emerges as a win factor.

Emerging disruptors target niche pain points. Start-ups focusing on immersion-cool deployment, modular substation kits, and rapid-erect steel frames compress schedules by 30%. Off-grid power integrators bundle gas turbines, heat-recovery generators, and carbon-capture add-ons, appealing to hyperscalers under emissions scrutiny. Competitive intensity therefore stems from capability breadth rather than sheer contractor count in the Canada data center construction industry.

Canada Data Center Construction Industry Leaders

Black & Veatch Holding Company

PCL Construction

Bird Construction

EllisDon

DPR Construction

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bell Canada launched its first AI Fabric facility in Kamloops, British Columbia, as part of a 500 MW hydro-electric powered supercluster spanning 6 facilities across the province. This initiative represents Canada’s largest AI compute project and establishes Bell as a major player in sovereign AI infrastructure, with partnerships including Groq for AI inference capabilities and Thompson Rivers University for academic integration

- May 2025: Prologis announced the conversion of an Illinois warehouse into a 32 MW turnkey data center in partnership with Skybox Datacenters, marking the industrial real-estate leader’s entry into data center development. The company secured 1.6 GW of power globally and plans to develop approximately 20 data center opportunities over the next 4 years with USD 7–8 billion in investment.

- March 2025: The Government of Canada finalized a CAD 240 million(USD 174.79 million) investment in Cohere Inc.’s CAD 725 million (USD 528.02 million) project to enhance domestic compute capacity, facilitating the construction of a new multibillion-dollar AI data center set to launch in 2025. This investment is part of the AI Compute Challenge under the Canadian Sovereign AI Compute Strategy

- March 2025: EllisDon Corporation announced progress on its partnership with Palantir Technologies to enhance AI and operational efficiencies, building on the company’s data environment modernization since 2010. The collaboration aims to optimize construction operations and drive growth through advanced data analytics.

- March 2025: Pembina and Kineticor formed a joint venture to develop a 1.8 GW natural gas project in Alberta specifically designed to serve the Canadian data center market, addressing power availability constraints that are limiting construction growth.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Canada's data center construction market as all greenfield and major expansion projects that deliver purpose-built facilities whose core function is to house IT equipment, including buildings, electrical and mechanical systems, and associated professional services completed within Canadian provinces. Small, in-house server room retrofits and purely IT hardware upgrades are outside this scope.

Scope Exclusions: Minor refurbishment work that does not alter structural load-bearing elements or add new power or cooling capacity remains excluded.

Segmentation Overview

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- By Electrical Infrastructure

- Power Distribution Solution

- Power Backup Solutions

- By Mechanical Infrastructure

- Cooling Systems

- Racks and Cabinets

- Servers and Storage

- Other Mechanical Infrastructure

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- By Electrical Infrastructure

- Tier 1 and 2

Detailed Research Methodology and Data Validation

Primary Research

Conversations with EPC contractors, real-estate consultants, utility planners, and hyperscale procurement managers across Quebec, Ontario, Alberta, and British Columbia allow us to validate typical cost per megawatt, lead times, and labor constraints, and to challenge secondary assumptions before figures are finalized.

Desk Research

We begin with structured pulls from public datasets such as Statistics Canada's non-residential building permits, Natural Resources Canada electricity price bulletins, and Innovation, Science and Economic Development Canada investment trackers, which clarify build volumes and power economics. Supplemental context is taken from federal and provincial budget documents, Uptime Institute availability standards, and trade association briefs issued by the Canadian Construction Association and the Canadian Data Center Coalition, ensuring geographic and regulatory nuance.

Mordor analysts then mine company filings, press releases, and construction tender portals inside D&B Hoovers and Dow Jones Factiva to log project timelines, megawatt ratings, and indicative costs. Patent abstracts through Questel help us capture emerging cooling and modular design trends. The examples above are illustrative; many additional sources aid collection, corroboration, and clarification.

Market-Sizing & Forecasting

A top-down construction spending rebuild aligns Statistics Canada permit values with import-export flows of key equipment, which are then segmented by tier classification and province. Select bottom-up checkpoints, sampled contractor roll-ups and average selling price (ASP) × capacity checks, calibrate the totals. Key variables include average megawatts per project, steel and concrete cost indices, grid interconnection cycle times, renewable power share, and hyperscale capex intentions disclosed in earnings calls. Multivariate regression coupled with scenario analysis forecasts these drivers through 2030, while gaps in bottom-up evidence are bridged using weighted regional proxies endorsed by interviewees.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst audits, and senior sign-off. Models refresh annually, with interim tweaks when policy shifts, large project announcements, or material cost swings breach preset thresholds. A fresh validation sweep precedes every client delivery.

Why Mordor's Canada Data Center Construction Baseline Commands Reliability

Published estimates diverge because firms vary project-type inclusion, cost benchmarks, currency timing, and refresh cadence.

Key gap drivers center on whether retrofit spend is counted, how contingency margins are applied, and if renewable-ready design premiums are isolated or bundled. Our scope sticks to new capacity, applies province-specific cost curves, and converts at Bank of Canada average annual rates, whereas others often mix retrofit and hardware spend or use single-city price books.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.34 B (2025) | Mordor Intelligence | - |

| USD 4.21 B (2024) | Regional Consultancy A | Counts retrofit refurbishments and bundles IT hardware spend |

| USD 10.67 B (2024) | Global Consultancy B | Uses global ASPs without provincial cost adjustment; includes announced but unfunded projects |

| USD 3.02 B (2025) | Industry Association C | Relies on media reports, omits self-build hyperscale campuses north of 50 MW |

These comparisons show that when consistent scope, localized cost inputs, and annual verification are enforced, Mordor delivers a balanced, transparent baseline that decision-makers can retrace and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the Canada data center construction market?

The market stands at USD 3.71 billion in 2026 and is projected to reach USD 6.27 billion by 2031.

Which province is adding capacity fastest?

Alberta leads near-term expansion with a 1.2 GW phased grid-connection program and CAD 100 billion policy incentives.

Why are Tier 4 facilities gaining traction?

Mission-critical AI workloads require fault-tolerant power and cooling redundancies, driving a 12.95% CAGR in Tier 4 builds.

How are power constraints influencing construction timelines?

Limited grid headroom forces developers to integrate on-site generation, extending schedules by up to 18 months in some provinces.

Page last updated on: