Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

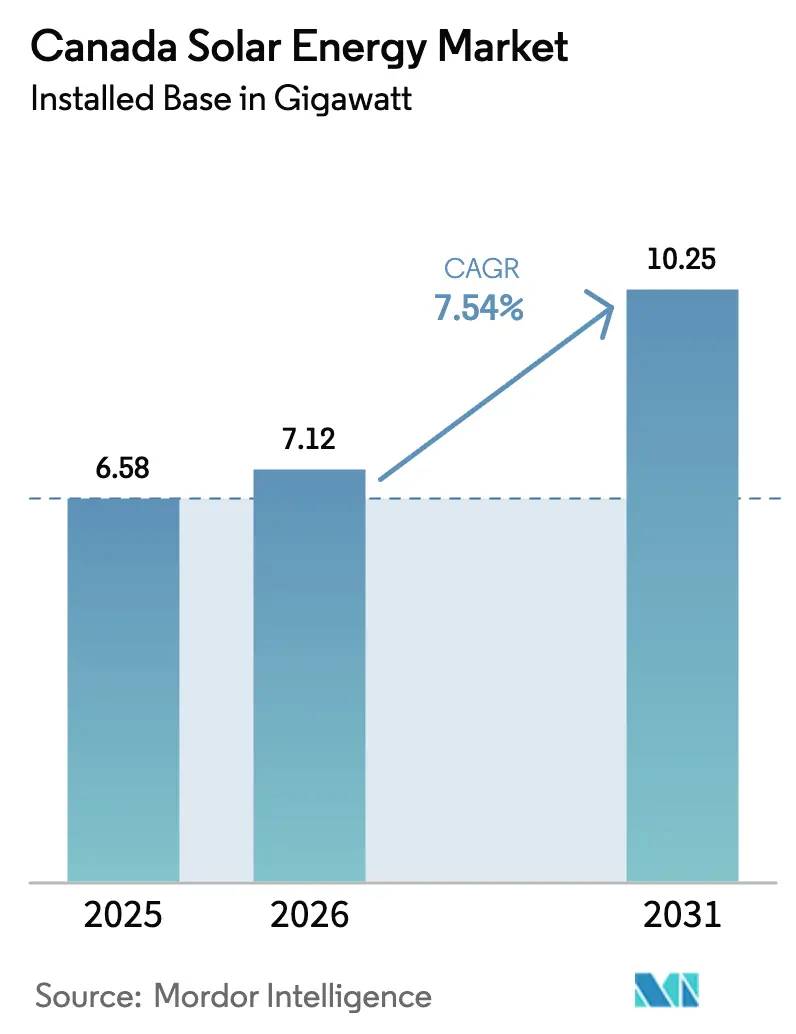

| Base Year Market Size (2025) | 6.58 gigawatt |

| Market Volume (2026) | 7.12 gigawatt |

| Market Volume (2031) | 10.25 gigawatt |

| Growth Rate (2026 - 2031) | 7.54% CAGR |

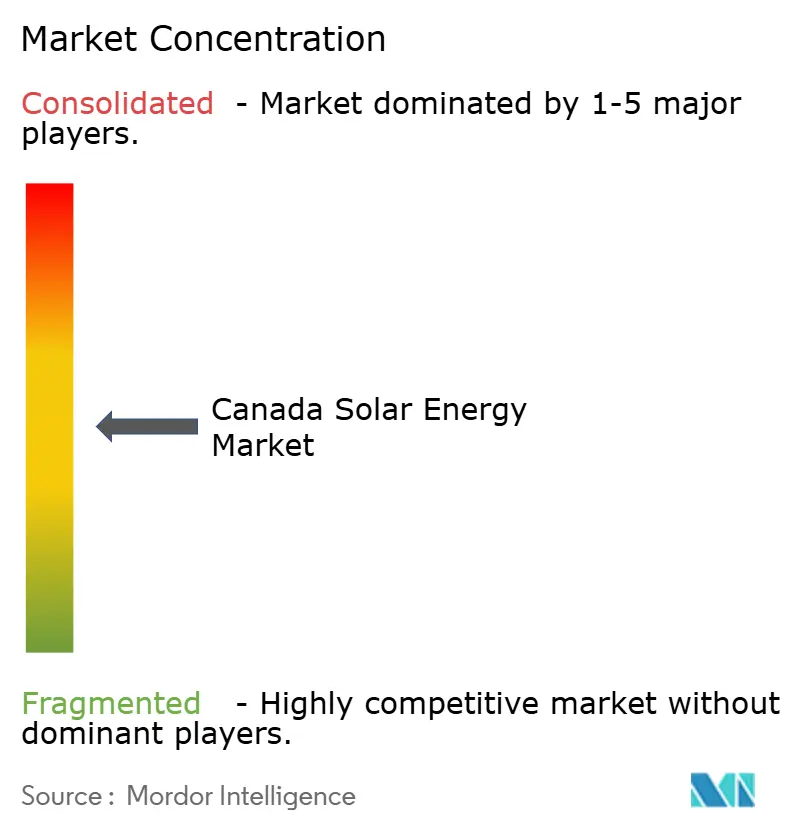

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Solar Energy Market Analysis by Mordor Intelligence

The Canada Solar Energy Market in terms of installed base was valued at 6.58 gigawatt in 2025 and expected to grow from 7.12 gigawatt in 2026 to reach 10.25 gigawatt by 2031, at a CAGR of 7.54% during the forecast period (2026-2031).

Federal investment tax credits, faster coal-plant retirements, and a jump in corporate power-purchase agreements are accelerating utility-scale procurement schedules even as provincial regulators tighten interconnection procedures. Alberta’s decision in early 2025 to end a seven-month pause on renewable approvals immediately freed more than 2 GW of shovel-ready capacity, underscoring that permitting timelines now steer deployment speed more than technology costs. Ottawa’s 30% clean-technology manufacturing credit, active since March 2024, is already lowering landed module costs by as much as 12% and cutting supply-chain lead times to under ten weeks for tier-one developers. Utility-scale projects still dominate the installed base, yet the off-grid segment is growing at a 9.9% CAGR as Indigenous communities adopt solar-plus-storage microgrids to replace diesel. Competitive pressure is increasing as vertically integrated manufacturers use domestic production to underprice stand-alone independent power producers by nearly 8% on a levelized basis.

Key Report Takeaways

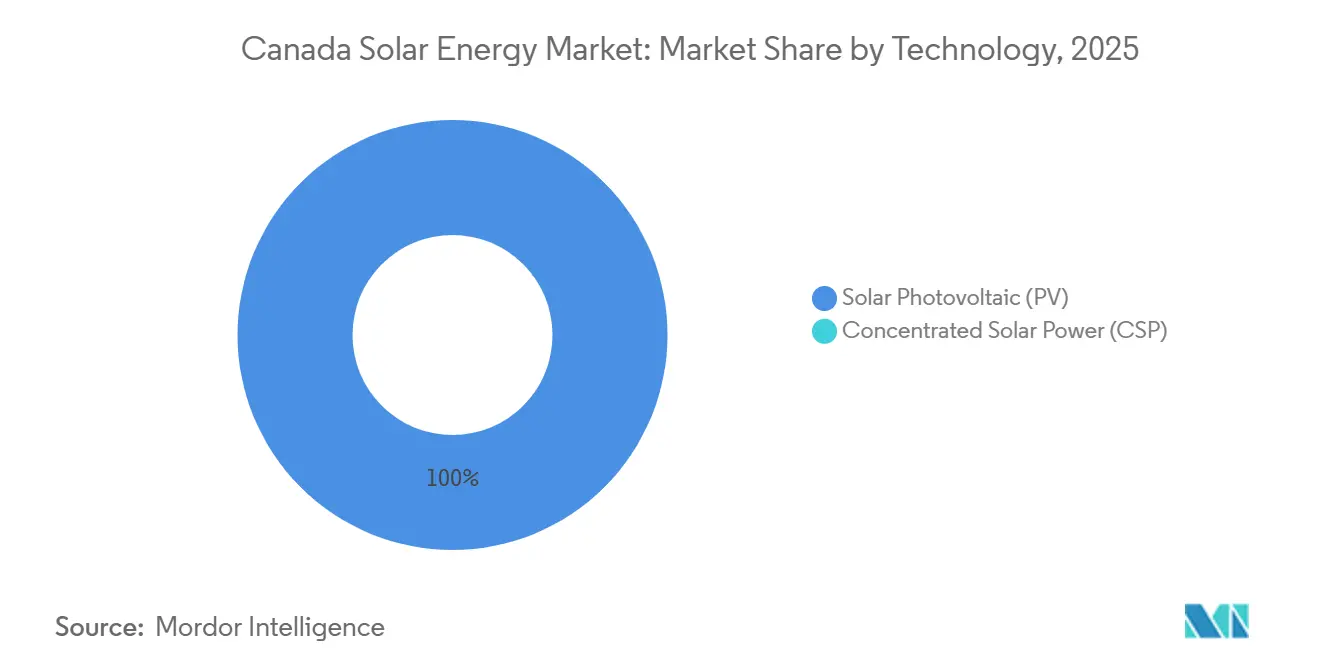

- By technology, solar photovoltaic held 100% of the Canada solar energy market share in 2025; bifacial upgrades are expanding the segment at a 7.54% CAGR through 2031.

- By grid type, on-grid assets accounted for 67.1% of installed capacity in 2025, while off-grid systems are advancing at a 9.9% CAGR as diesel displacement accelerates in northern territories.

- By end-user, utility-scale plants represented 57.6% of capacity in 2025, but residential rooftops are growing fastest at a 10.2% CAGR on the back of strengthened net-metering programs in Ontario and British Columbia.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating provincial RPS and clean-energy auctions | +1.8% | Alberta, Saskatchewan, Ontario | Medium term (2-4 years) |

| Accelerated coal-to-renewables displacement mandate | +1.5% | Alberta, Saskatchewan, Nova Scotia | Short term (≤ 2 years) |

| Declining LCOE of bifacial and TOPCon PV modules | +1.2% | National, with early gains in Alberta, Ontario | Long term (≥ 4 years) |

| Corporate PPAs from data-center and mining sectors | +1.0% | Ontario, Quebec, British Columbia | Medium term (2-4 years) |

| Federal 30% ITC on clean-tech manufacturing (2024 Budget) | +0.9% | National, manufacturing hubs in Ontario, Quebec | Long term (≥ 4 years) |

| AI-optimized grid-integration software adoption | +0.6% | Alberta, Ontario (IESO, AESO grids) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Provincial RPS & Clean-Energy Auctions

Competitive procurements in Alberta, Saskatchewan, and Ontario continue to push bid prices below CAD 50 per MWh and provide developers with long-term revenue certainty that lowers debt costs by up to 50 basis points. Auction calendars published two years in advance allow suppliers to lock in module contracts early, which in turn reduces construction risk and accelerates balance-sheet commitments from institutional investors.[1]Independent Electricity System Operator, “2026 Resource Procurement Plan,” ieso.ca Indexed pricing mechanisms, where tariffs glide with inflation but cap annual escalation, further protect cash flows for pension-fund financiers.

Accelerated Coal-To-Renewables Displacement Mandate

Federal regulations that end coal generation by 2030 are forcing utilities in Alberta and Saskatchewan to bring replacement solar and storage online faster than previously scheduled. Retiring coal sites supply existing transmission corridors, cutting connection costs by as much as CAD 200 million per GW. New solar farms deployed adjacent to decommissioned units access pre-built substations, shaving nine to twelve months from project timelines and raising internal rates of return by roughly two percentage points for sponsors such as TransAlta and Capital Power.

Declining LCOE of Bifacial & TOPCon PV Modules

Domestic production of bifacial TOPCon modules with 24.5% efficiency began in Ontario in late 2024, bringing module prices below USD 0.16 per watt after federal incentives. Higher yield lifts capacity factors beyond 20% in southern Alberta, enabling solar to compete directly with gas peakers that cleared Alberta’s energy-only market at an average CAD 87 per MWh in 2025. Balance-of-system costs fall 10% per installed watt because fewer modules are needed to reach the same output.

Corporate PPAs from Data-Center & Mining Sectors

Hyperscale operators booked 2.3 GW of long-term solar contracts by end-2025, with AWS and Microsoft each signing 200-MW-plus deals priced below CAD 50 per MWh. These agreements stabilize cash flows, allowing projects to obtain non-recourse loans at rates 100-basis-points cheaper than merchant plants. In remote mining, Teck Resources showed that a 20 MW solar-plus-storage system can remove 12 million liters of diesel annually and cut operating expenditure by CAD 18 million.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interconnection queue congestion in Alberta & Ontario | -0.8% | Alberta, Ontario - provinces with centralized grid operators and capacity-constrained transmission corridors | Short term (≤ 2 years) |

| Seasonal irradiance mismatch affecting capacity-factors | -0.5% | National, with acute impact in northern Ontario, Quebec, and Atlantic provinces where winter capacity factors drop below 12% | Long term (≥ 4 years) |

| Rising anti-dumping vigilance on Asian module imports | -0.8% | National, with heightened scrutiny on Southeast Asian manufacturers with alleged Chinese ownership links | Medium term (2-4 years) |

| Skilled-labour shortages in remote provinces | -0.5% | Saskatchewan, Manitoba, Atlantic provinces, and northern territories—regions with limited solar installation workforce | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interconnection Queue Congestion in Alberta & Ontario

System-impact studies stretch to 18 months in Alberta and 24 months in Ontario, delaying project cash flows and eroding developer returns.[2]Alberta Electric System Operator, “2025 Solar Integration Study,” aeso.ca Fast-track pathways for projects under 50 MW shorten timelines to nine months, yet utility-scale assets that account for 58% of provincial capacity additions remain subject to lengthy reviews. Cluster-study pilots that evaluate multiple projects together may cut per-project costs by 30%, but full deployment is unlikely before 2027.

Seasonal Irradiance Mismatch Affecting Capacity Factors

Canada’s high-latitude profile creates a six-month output imbalance that forces grid operators to maintain gas peakers for winter demand spikes, adding up to CAD 12 per MWh to system costs. Four-hour lithium-ion batteries can cover daily ramps but fall short during week-long low-sun stretches. Developers respond by pairing solar with wind, which peaks in winter, raising combined capacity factors above 38% in hybrids such as Boralex’s 150 MW Apuiat project.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Dominates, CSP Absent

Photovoltaic systems represented the entire installed base in 2025 and will remain the sole commercial technology through 2031, expanding in lockstep with the overall Canada solar power market. Breakthroughs in bifacial TOPCon cells have pushed module efficiency to 24.5%, lowering installed costs to CAD 1,200 per kW for utility-scale plants. Fixed-tilt projects are giving way to single-axis trackers that lift annual energy yield by 20%, a gain that compensates for winter irradiance losses.

Cost and performance metrics leave concentrated solar power economically unviable because direct normal irradiance averages only 1,300 kWh per square meter compared with the 2,000 kWh benchmark required for CSP competitiveness.[3]Natural Resources Canada, “Photovoltaic Performance in Canada,” nrcan.gc.ca Half-cut cell formats, multi-busbar interconnects, and string inverters further raise production efficiency while trimming maintenance expense.

By Grid Type: Off-Grid Surges In Remote Regions

On-grid installations maintained 67.1% of capacity in 2025, driven by Alberta and Ontario auction pipelines. Yet off-grid systems are climbing at 9.9% CAGR as communities north of 60° latitude displace diesel that costs CAD 0.45 per kWh. Natural Resources Canada funded 18 microgrids totaling 35 MW in 2025, each pairing 4-hour to 8-hour batteries with PV arrays sized between 500 kW and 5 MW.

Diesel savings translate into six-year to nine-year paybacks even before carbon-price credits. Mining operators such as Agnico Eagle have validated economics by trimming 8 million liters of fuel annually at the Meadowbank site in Nunavut, confirming a template now replicating across Yukon and the Northwest Territories.

By End User: Residential Outpaces Utility-Scale Growth

Utility-scale facilities still held 57.6% of total capacity in 2025, but the residential slice is growing fastest at 10.2% CAGR. Net-metering reforms adopted in Ontario and British Columbia allow households to bank surplus generation for up to one year, slashing payback periods to six years on a 5 kW system priced near CAD 2.50 per watt.

Commercial-and-industrial customers follow close behind, motivated by time-of-use tariffs that can swing CAD 0.12 per kWh between peak and off-peak windows. Integrators such as Saturn Power bundle rooftop PV with 2-hour batteries and demand-response software, creating new revenue streams in Ontario’s capacity auction and ancillary-service markets.

Geography Analysis

Alberta commanded 42% of national solar capacity in 2025 thanks to superior isolation and an energy-only market that rewards flexible assets during high-price hours. Removing the 2024–2025 permitting pause unleashed 2 GW of ready-to-build projects, and the province expects solar additions to equal 35% to 40% of all new generation by 2030. Ontario followed with 28%, supported by a 2 GW clean-capacity tender that may allocate half of the awarded volume to solar-plus-storage assets slated for 2028 startup.

Saskatchewan is rising rapidly from a smaller base as SaskPower’s 300 MW solicitation targets brownfield sites at retiring coal plants where transmission is already in place, trimming interconnection costs by up to 50%.[4]SaskPower, “Solar RFP 2025,” saskpower.com British Columbia and Quebec have historically leaned on hydro, but now see faster rooftop uptake after net-metering revisions in 2025 that expanded credit-carry rules for households and data-center operators.

Remote northern territories deploy solar-plus-storage microgrids to displace imported diesel. Eighteen funded projects totaling 35 MW relied on Natural Resources Canada’s Indigenous Off-Diesel Initiative, producing fuel savings of up to 75% and reducing generation costs by CAD 0.30 per kWh. Atlantic provinces lag because of lower irradiance and constrained transmission, though Nova Scotia Power’s 100 MW tender announced in 2025 suggests early momentum as the last coal unit retires in 2030.

Competitive Landscape

The Canada solar power market is moderately fragmented. The five largest players, Canadian Solar, Brookfield Renewable, Boralex, Innergex, and EDF Renewables, jointly controlled about 48% of installed capacity in 2025, but no single participant exceeded a 12% share. Vertically integrated manufacturers capitalize on domestic module production to underprice independent developers by up to 8% on levelized cost, while international firms such as EDF Renewables leverage global procurement to secure lower-cost financing.

Strategic moves pivot toward supply-chain localization. Canadian Solar added 1 GW of annual assembly capacity in Ontario under the 30% investment tax credit, and Siemens Energy will open a 500 MW inverter line in Quebec during 2026. Brookfield Renewable expanded via the acquisition of a 150 MW Alberta portfolio in 2024, signaling a gradual consolidation path. Indigenous-owned developers like Lumos Energy continue to capture niche off-grid projects with community-equity models that resonate in federal grant programs.

Technology leadership is becoming a differentiator. Northland Power’s 200 MW Claresholm plant employs AI dispatch to time battery discharge for price spikes, lifting project returns by three percentage points in Alberta’s merchant market. Patent filings for bifacial optimization climbed 35% from 2023 to 2025, with Canadian Solar and Siemens Energy filing 40% of applications.

Canada Solar Energy Industry Leaders

Canadian Solar Inc.

Brookfield Renewable Partners

Boralex Inc.

Innergex Renewable Energy Inc.

EDF Renewables Canada

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Canada Infrastructure Bank invested CAD 108.3 million in the 102.2 MW Mesgi’g Ugju’s’n 2 wind farm, issuing its first Indigenous equity loan.

- April 2025: TotalEnergies has finalized the acquisition of three renewable energy portfolios spanning Europe, Africa, and Canada. Notably, this encompasses the purchase of VSB Group and SN Power, targeting projects in Europe and Africa. Additionally, TotalEnergies has struck deals with RES to acquire renewable energy projects located in Alberta.

- May 2024: In Japan's inaugural Long-Term Decarbonization Power Source Auction (LTDA), Canadian Solar clinched three Battery Energy Storage System (BESS) projects, amassing a total of 193 MW. This achievement accounts for 13.3% of the total storage capacity awarded.

- December 2024: The Government of Canada invested CAD 152 million in nine clean-electricity projects in Alberta via the Smart Renewables and Electrification Pathways Program.

Canada Solar Energy Market Report Scope

Solar energy is the energy obtained from the sun's rays converted into thermal or electrical energy. It is the cleanest form of energy that is abundant in nature. Solar energy is harnessed by photovoltaics, heating & cooling, and concentrated solar power. Due to the development of resilient technology, today, solar energy is mainly used to generate electricity by various consumers, including residential, industrial, and commercial.

The Canada solar energy market is segmented by technology, grid type, end-user, and geography. By technology, the market is segmented into solar photovoltaic and concentrated solar power. By grid type, the market is segmented into on-grid and off-grid systems. By end-user, the market is segmented into utility-scale, commercial and industrial, and residential installations. For each segment, the market sizing and forecasts have been conducted on the basis of installed capacity (GW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How large is the Canada solar power market in 2026?

Installed capacity is on track to reach 7.12 GW by 2026, in line with the 7.54% CAGR trajectory.

Which province is adding solar capacity the fastest?

Alberta leads additions due to high insolation and an energy-only market that streamlines financing and dispatch.

What incentive supports domestic solar manufacturing?

A 30% refundable investment tax credit introduced in 2024 reduces capital costs for module, inverter, and racking production.

Are off-grid solar systems economical in northern Canada?

Yes, microgrids already cut diesel use by up to 75% and achieve six-year to nine-year paybacks, even before carbon credits.

How are corporate PPAs shaping new projects?

Data-center and mining firms locked in 2.3 GW of PPAs by 2025, providing bankable revenues that lower borrowing costs by up to 100 basis points.

Page last updated on: