Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 128.39 Billion |

| Market Size (2031) | USD 172.31 Billion |

| Growth Rate (2026 - 2031) | 6.06% CAGR |

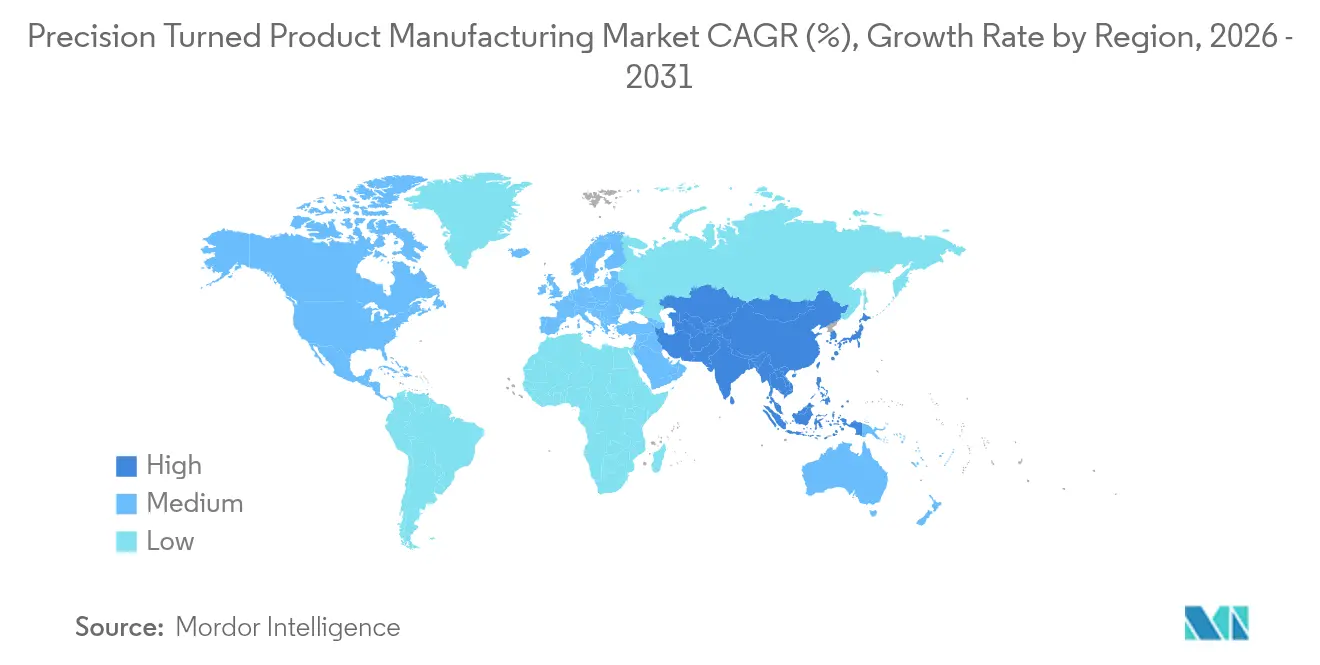

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precision Turned Product Manufacturing Market Analysis by Mordor Intelligence

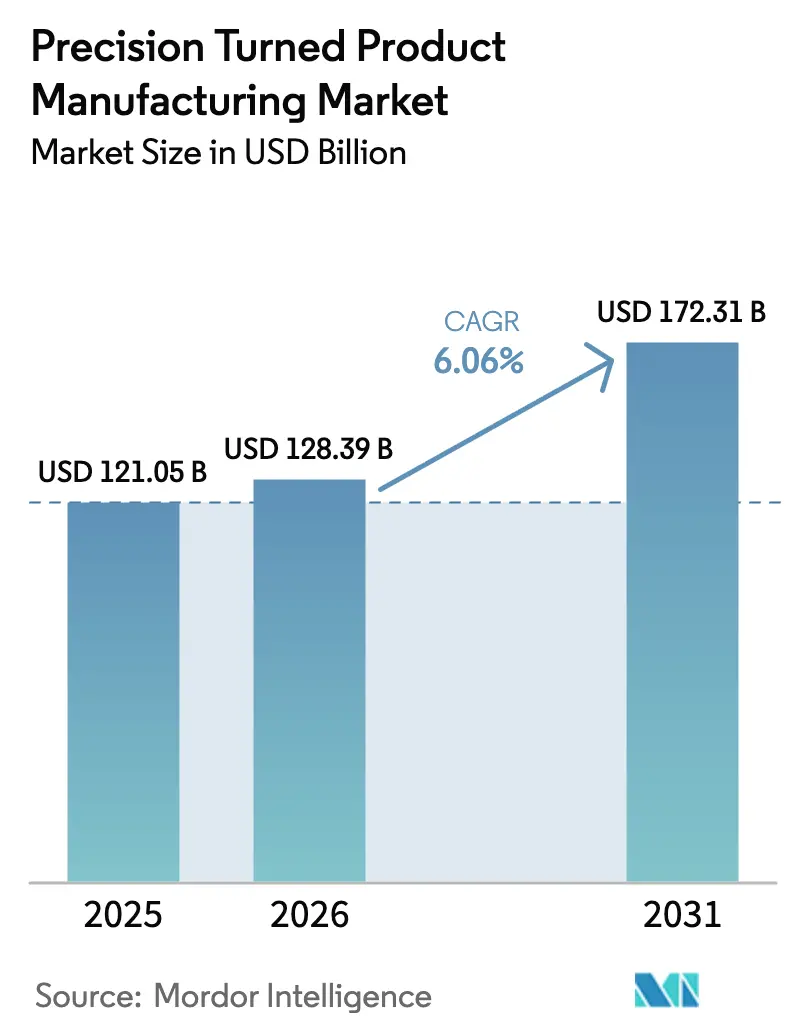

The Precision Turned Product Manufacturing Market size is projected to expand from USD 121.05 billion in 2025 and USD 128.39 billion in 2026 to USD 172.31 billion by 2031, registering a CAGR of 6.06% between 2026 to 2031.

This outlook reflects a decisive migration from manual screw-machine operations toward computer-numerical-control (CNC) Swiss-type platforms that deliver sub-micron repeatability for aerospace, electric-vehicle (EV), and implantable-medical-device programs. Lockheed Martin now specifies ±0.005-millimeter tolerances under AS9100D for F-35 hydraulic pistons, compelling tier-two suppliers to replace rotary-transfer lines with multi-axis turning centers.[1]Source: Lockheed Martin, “AS9100D Supplier Requirements,” lockheedmartin.com Simultaneously, EV power-train miniaturization is driving demand for precision shafts that accommodate hairpin stator windings and axial-flux motors, a shift that favors shops running live-tooling lathes capable of one-setup interpolation. Defense modernization adds further pull through titanium and super-alloy bar, while Food and Drug Administration (FDA) Quality Management System Regulation (QMSR) compliance, effective February 2026, is accelerating the outsourcing of micro-machined medical parts. Against this backdrop, the precision turned product manufacturing market is also absorbing Industry 4.0 retrofits that raise overall-equipment-effectiveness (OEE) toward 85%, stretching spindle uptime and shortening prototype lead times.

Key Report Takeaways

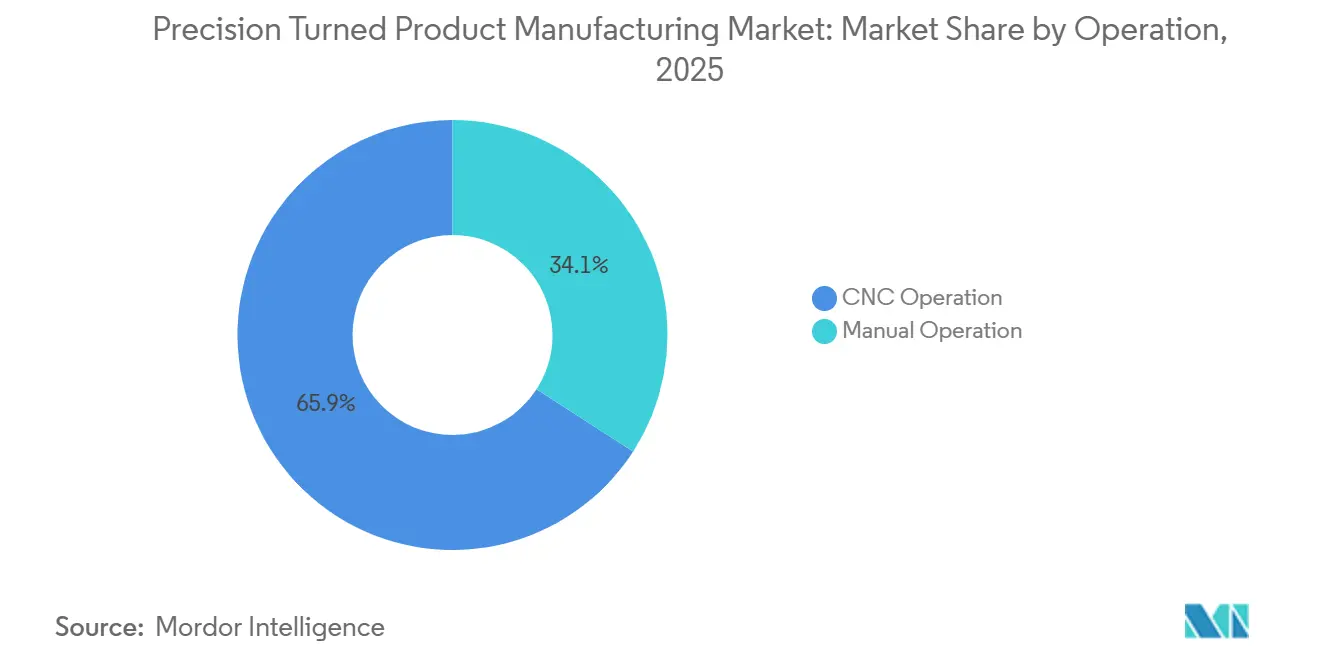

- By operation, CNC Operation commanded 65.88% of the precision turned product manufacturing market share in 2025 and is projected to expand at an 8.41% CAGR through 2031.

- By machine type, CNC Swiss-type machines commanded 36.20% of the 2025 value within the precision turned product manufacturing market size and are projected to expand at a 9.92% CAGR through 2031.

- By material type, steel commanded 45.10% of the precision turned product manufacturing market share in 2025, while titanium and super-alloys are projected to expand at a 7.72% CAGR through 2031, driven by defense and medical demand.

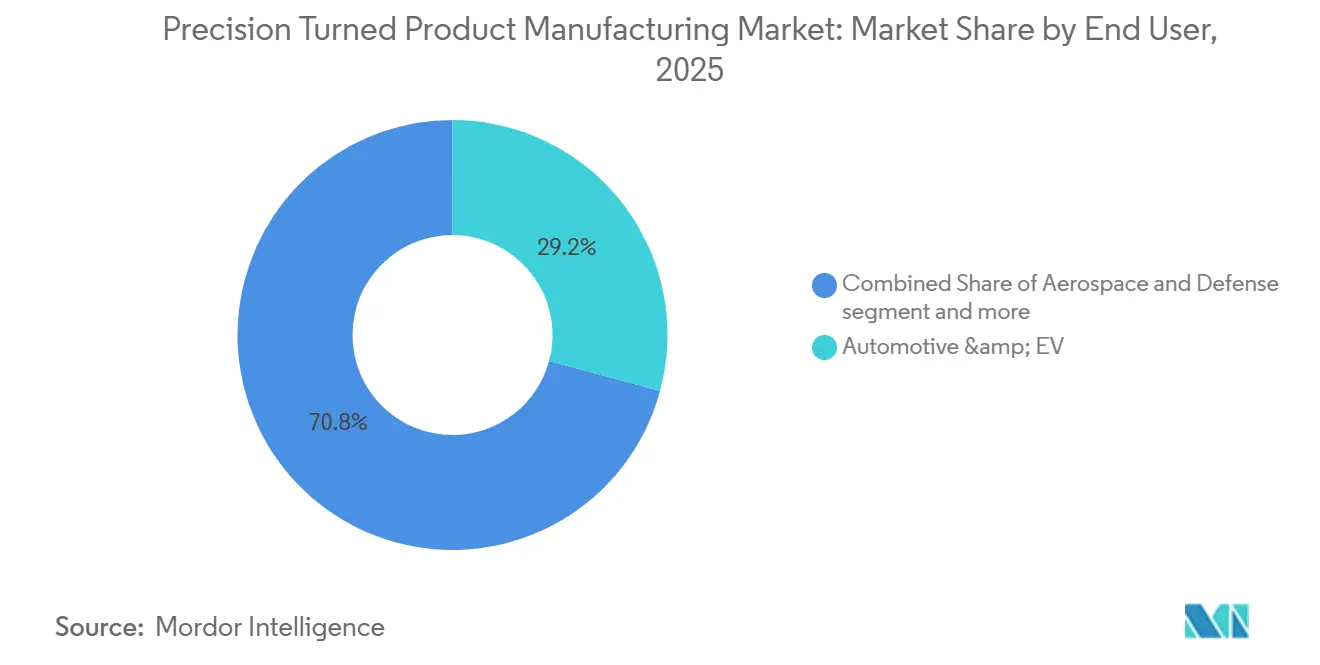

- By end-user industry, automotive and EV commanded 29.20% of the precision turned product manufacturing market share in 2025, while medical and dental are projected to expand at a 6.66% CAGR through 2031.

- By geography, Asia-Pacific commanded 38.60% of the precision turned product manufacturing market share in 2025 and is projected to expand at a 7.33% CAGR through 2031, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Precision Turned Product Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV power-train miniaturization drives demand for precision shafts and fittings | +1.4% | Asia-Pacific core, spill-over to North America & Europe | Short term (≤ 2 years) |

| Aerospace OEMs mandate ultra-tight tolerance turned components | +1.2% | North America, Europe | Medium term (2-4 years) |

| Industry 4.0 retrofits enhance CNC throughput and cost efficiency | +1.1% | Global early adoption in Japan, Germany, USA | Short term (≤ 2 years) |

| Medical device manufacturers outsource micro-machining to meet strict regulatory standards | +0.9% | North America, Europe, India | Medium term (2-4 years) |

| Defense modernization programs increase procurement of complex-alloy turned components | +0.8% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Rapid prototyping requirements boost quick-turn machining demand | +0.7% | Automotive & electronics hubs worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV Power-Train Miniaturization Drives Demand for Precision Shafts and Fittings

Automakers transitioning to 800-volt architectures and axial-flux motors are specifying shaft runout below 0.010 millimeters to curb vibration at 20,000 rpm. BYD’s Seal sedan uses aluminum 6063 battery-coolant manifolds cut to ±0.015-millimeter flatness on five-axis machines, illustrating the jump from cast-and-grind to direct turning.[2]BYD Company, “Seal Model Technical Specifications,” byd.com Tesla’s hollow rotor shafts trim inertia by 8% and demand Swiss-type turning with programmable steady rests. As pack energy density pushes toward 300 Wh/kg, stainless-steel 316L nipples and expansion-valve bodies that must pass 10-kV dielectric tests further widen the quality gap over manual processes. Precision shops able to meet these profiles stand to win long-term nomination in EV platforms whose production volumes exceed 500,000 units annually.

Aerospace OEMs Mandate Ultra-Tight Tolerance Turned Components

Aerospace primes now routinely call for ±0.005-millimeter tolerances on turbine-shaft journals, landing-gear bushings, and control-valve spools, eliminating manual screw machines from approved vendor lists. Lockheed Martin requires AS9100D certification and 1.33 Cpk statistical-process-control minimums for the F-35 program, pushing tier-two shops to invest in thermal-compensated CNC lathes and in-process gauging. Next-generation engines such as Pratt & Whitney’s Geared Turbofan (GTF) Advantage operate beyond 1,650 °C, leaving no tolerance for dimensional drift. Facilities are therefore adding spindle-mounted laser micrometers that close the feedback loop in real time, while the International Aerospace Quality Group (IAQG) now embeds first-article inspection traceability in digital twins. Combined, these forces hard-wire demand for CNC Swiss-type systems across global aircraft supply chains.

Industry 4.0 Retrofits Lift CNC Throughput and Cost Efficiency

Precision-turning cells now embed vibration, temperature, and power-draw sensors that stream data to edge computers for real-time OEE dashboards. Early adopters consistently raise spindle utilization from 60% toward 85% and slash unplanned downtime by half, according to field audits conducted across Japanese and German job shops. Citizen Machinery’s Cincom L32 integrates laser probes that auto-correct offsets, supporting lights-out operation for medical batches that once required mid-shift checks. Digital twins let process engineers trial tool paths in a virtual environment, reducing first-article approval from weeks to days. The upshot is leaner labor scheduling and shorter queue times, both of which strengthen the profitability of the precision turned product manufacturing market.

Medical Device Manufacturers Outsource Micro-Machining to Meet Strict Regulatory Standards

The FDA’s QMSR has been in force since February 2026, harmonizing U.S. rules with International Organization for Standardization (ISO) 13485:2016, heightening the paperwork burden for in-house machining wings. Orthopedic OEMs, therefore, funnel titanium-alloy femoral stems, spinal screws, and arthroscopic-shaver collets to contract manufacturers that validate every lot under micro-tolerance bands. These parts often sit in the 2-millimeter-to-8-millimeter diameter window, a range where Swiss-type guide bushings minimize deflection and hit surface finishes under 0.4 µm Ra. Outsourcing also sidesteps capital outlays for temperature-controlled cells and sub-micron spindle monitoring, letting OEMs redeploy cash to R&D. The result is a sustained pipeline of orders that keeps the precision turned product manufacturing market on an elevated growth path through 2031.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Additive manufacturing replaces simple cylindrical and low-complexity turned components | -0.6% | Global with aerospace focus | Medium term (2-4 years) |

| Volatile stainless steel and titanium prices compress machining shop profit margins | -0.5% | Global, acute in Asia-Pacific & Europe | Short term (≤ 2 years) |

| Shortage of skilled CNC programmers restricts capacity expansion across machining facilities | -0.4% | North America, Europe, China | Long term (≥ 4 years) |

| Stricter coolant disposal and environmental regulations increase operational compliance costs | -0.3% | Europe, North America, spreading to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Additive Manufacturing Replaces Simple Cylindrical and Low-Complexity Turned Components

Directed-energy deposition (DED) and laser-powder-bed fusion (L-PBF) systems now print turbine-blade roots that are then finish-turned on the same machine, slicing total lead time by up to 50%. Rolls-Royce’s Pearl 10X engine already incorporates AM fuel nozzles that displace turned swirl-vanes and cut part counts by 25%. Trumpf’s TruPrint 3000 platform hits ±0.050-millimeter as-printed tolerances, closing the gap for non-critical bushings. Economics still favor turning on runs above 500 units, yet AM’s march into lower volumes keeps a lid on certain sub-segments of the precision turned product manufacturing market.

Volatile Stainless Steel and Titanium Prices Compress Machining Shop Profit Margins

Nickel-driven stainless-steel bar costs swung more than 20% during 2024-2025 as Chinese mills dialed output up and down. Titanium sponge supply disruptions in Russia and Ukraine lifted Ti-6Al-4V bar premiums by 25% over pre-2022 levels. Small turning shops, operating on 8%-to-12% net margins, cannot hedge commodities and often absorb spikes for 60-to-90 days under fixed-price contracts. Material surcharges tied to nickel, chromium, and molybdenum further complicate quoting on long-lead aerospace jobs. As titanium and super-alloy demand rise, the precision turned product manufacturing market faces persistent cost pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operation: CNC Dominance Reshapes Capacity Planning

CNC Operation accounted for 65.88% of the precision turned product manufacturing market share in 2025, illustrating its entrenched status in high-precision volumes. Manual Operation lingers mainly in legacy fastener lines, but its relevance shrinks each year as audits demand digital traceability that cam-driven screw machines cannot deliver. A modern Swiss-type lathe with bar-feed automation generates up to 200 parts per hour at scrap rates below 0.3%, while a manual screw machine averages 80 parts with three times the waste. The skills shortage adds complexity; BLS data show machinist attrition that CNC-focused vendors partially offset by installing user-friendly HMIs. As more plants overlay vibration and temperature sensors for predictive maintenance, real-time dashboards drive OEE toward 85%, widening the cost gap over manual cells.

Lights-out production is the new target. Citizen’s Cincom L32 incorporates laser probes that correct offsets mid-cycle, supporting overnight runs without human oversight. Edge analytics flag tool wear in real time, trimming insert changeovers by 15% and elevating first-pass yield above 99.5%. These advances underpin the fastest sub-segment pace: CNC Operation revenues are forecast to post an 8.41% CAGR through 2031. In contrast, manual setups face a sunset trajectory as OEM qualification thresholds march steadily tighter.

By Machine Type: Swiss-Type Platforms Capture High-Mix Programs

CNC Swiss-type machines secured 36.20% of 2025 revenue and are projected to climb at a 9.92% CAGR, the highest among architectures. Guide-bushing designs clamp slender workpieces close to the cutting edge, holding ±0.005-millimeter tolerances on 12-inch-long spinal screws without secondary support. Medical-device OEMs gravitate toward this stability for titanium pedicle screws and stainless cannulas that demand surface finishes under 0.4 µm Ra. In electronics, test-socket pins and fiber-optic ferrules likewise sit in the sub-32-millimeter diameter band where Swiss-type superiority is clear.

Traditional two-axis lathes handle larger automotive shafts, while rotary-transfer machines still dominate ultra-high-volume injector bodies. Yet even here, Swiss-type lines eat share as integrated milling heads permit complete machining in one cycle, erasing fixture costs. Star Micronics’ SD-26 added a second spindle in 2024, enabling simultaneous front- and back-working on complex valve pins. Nomura’s DS 20J3XBTC, launched in 2025, doubles throughput on parts requiring cross-holes by machining the rear face while the main spindle turns the primary diameter. Those gains anchor Swiss-type momentum inside the precision turned product manufacturing market.

By Material Type: Titanium & Super-Alloys Gain Ground

Steel retained 45.10% of 2025 turnover, yet titanium and super-alloys are growing faster at 7.72% CAGR as aerospace and medical use-cases multiply. The U.S. Army’s artillery modernizations depend on high-strength steel fuze bodies, but next-generation shells now specify titanium aerodynamic fins to extend range. Lockheed Martin’s Precision Strike Missile likewise mandates Inconel 718 nozzles that keep tensile strength at 650 °C. In hospitals, single-use endoscopic shafts require lightweight, corrosion-proof titanium that withstands sterilization cycles.

Aluminum stays relevant in EV battery enclosures because 6063 alloy combines thermal conductivity with machinability; BYD’s Seal sedan relies on tight-flatness CNC faces that gasketted coolant manifolds cannot match. Plastics such as PEEK enter surgical tool handles where electrical insulation matters. Although steel maintains volume leadership, the recyclability of titanium chips, worth USD 5 to USD 15 per kilogram, softens material-cost drag and encourages further alloy migration, reinforcing overall growth inside the precision turned product manufacturing market.

By End-User Industry: Medical & Dental Outpace Automotive

Automotive and EV programs occupied 29.20% of 2025 revenue, but the Medical & Dental segment is projected to advance at 6.66% CAGR, outstripping car-sector gains. FDA QMSR rules push orthopedic firms to outsource micro-machining of femoral stems and pedicle screws to AS9100D-plus-ISO 13485 job shops. These parts sit in the 2-to-8-millimeter range, perfect for Swiss-type guide bushings, and contract houses deliver validated lots that hospitals trust.

Automotive still demands precision shafts for 20,000 rpm axial-flux motors, keeping a large base inside the precision turned product manufacturing market. Yet cost-down pressure nudges OEMs toward alternative forming on low-criticality fasteners. Aerospace and defense remain premium niches, with guidance fins and hydraulic pistons commanding high margins under ITAR contracts. Electronics uses Swiss-type lathes for fiber-optic ferrules where concentricity under 1 µm preserves signal integrity at 25 Gbps data rates, illustrating the expanding diversity of demand streams.

Geography Analysis

Asia-Pacific held 38.60% of 2025 revenue, and its precision turned product manufacturing market size is projected to grow at 7.33% CAGR on the back of China’s USD 59.5 billion CNC-machine sector and India’s USD 1.7 billion machine-tool base registering 11% year-over-year gains,. Zhejiang and Jiangsu provinces operate dense clusters of Swiss-type shops feeding global electronics exporters, while India benefits from labor costs that average one-sixth of U.S. rates plus generous Production Linked Incentives for domestic electronics sourcing. Japan extends regional leadership through Citizen Machinery’s 20% capacity expansion at Iwate and Kitakami, completed in October 2025, ensuring Swiss-type supply aligns with rising medical and automotive orders.[3]

North America’s precision turned product manufacturing market receives a structural lift from defense reshoring mandates. The U.S. Department of Defense awarded Rand Machine Products USD 330 million for naval fittings and Keel Manufacturing USD 22 million for missile fin actuators, both requiring domestic sourcing under the Berry Amendment. Hill Air Force Base’s 2025 purchase of five-axis lathes brings F-35 landing-gear overhauls in-house, nudging regional spend higher. Canada and Mexico share in that upside through USMCA rules that fix 75% North American content on auto components, drawing fresh investment near Detroit and Monterrey.

Europe faces REACH and COSHH costs that trim margins, yet ISO 14001-certified shops leverage compliance as a competitive moat. Germany’s Mittelstand retains technological edge in five-axis Swiss-type machining, and Citizen’s planned USD 27 million German headquarters slated for October 2026 testifies to sustained continental appetite. The United Kingdom, Italy, and France anchor aerospace clusters served by AS9100D job shops, while BENELUX and the Nordics specialize in medical and industrial robotics components. Elsewhere, Brazil and Argentina offer nascent demand tied to agricultural machinery, and Saudi Arabia’s Vision 2030 channels investment into indigenous precision-turning capacity.

Competitive Landscape

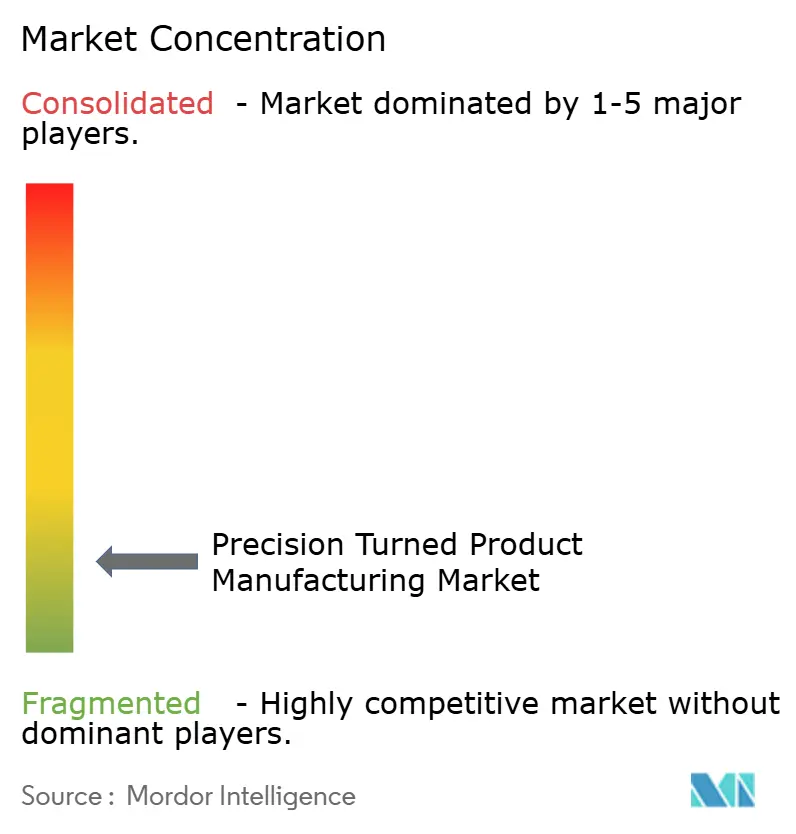

The precision turned product manufacturing market remains highly fragmented. Competition coalesces most fiercely around CNC Swiss-type niches, where Citizen Machinery, Marubeni-Citizen Cincom, and Star Micronics battle over spindle speed, tooling stations, and embedded metrology. Citizen’s Cincom L32 series, launched in May 2025, adds five-axis interpolation with laser gauging, cutting offline Coordinate Measuring Machine (CMM) checks and shrinking lot-to-ship lead time by 30%.

Strategic localization is accelerating. Marubeni-Citizen formed an Indian subsidiary in January 2025 to serve a domestic machine-tool market expanding 11% annually, pairing Swiss-type hardware with field-service hubs close to Bengaluru and Pune.[4]Marubeni Corporation, “Marubeni-Citizen Cincom India Launch,” marubeni.com Star Micronics answered by upgrading its Thai parts center and unveiling the SD-26 twin-spindle Swiss-type that finishes complex valve pins in one cycle. Contract manufacturers such as Cox Manufacturing and Hall Industries differentiate through dual AS9100D and ISO 13485 certifications, winning long-cycle aerospace and medical contracts that smaller regional shops cannot qualify for.

Emerging technologies are another front. Hybrid additive-subtractive cells from GE Aerospace combine DED printing with finish turning, trimming turbine-blade root lead times by half. Automation vendors now bundle cobot loaders with mid-range Swiss-types, extending unattended operation from 8 hours to 16 hours and easing labor shortages. Firms that pair sensor-rich Industry 4.0 retrofits with real-time OEE analytics are nudging profitability above 15% EBITDA, out-distancing traditional shops still locked in manual changeovers. These dynamics signal an escalating race to embed digital capability across every spindle in the precision turned product manufacturing market.

Precision Turned Product Manufacturing Industry Leaders

Cox Manufacturing Co.

KDK Finish-Turning

Melling Tool Co.

Astro Machine Works

E&H Precision

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Citizen Machinery finished a 20% capacity boost at its Iwate, Japan plant to meet global lathe demand.

- May 2025: Citizen Machinery released the Cincom L32 series, featuring in-process laser measurement for lights-out medical and aerospace runs.

- March 2025: Citizen Machinery debuted the Miyano BNJ51SY turning center with a touchscreen wizard that slashes programming time.

- January 2025: Marubeni-Citizen Cincom established a wholly owned Indian subsidiary focused on Swiss-type sales and service.

Global Precision Turned Product Manufacturing Market Report Scope

By Operation

| Manual Operation |

| CNC Operation |

By Machine Type

| Automatic Screw Machines |

| Rotary Transfer Machines |

| CNC Swiss-Type |

| Lathes/Turning Centers |

By Material Type

| Steel |

| Aluminum |

| Titanium & Super-alloys |

| Plastics & Composites |

By End-user Industry

| Automotive & EV |

| Aerospace & Defense |

| Medical & Dental |

| Electronics & Semiconductors |

| Industrial Machinery |

| Others (Construction, Fabrication Services, etc.) |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Operation | Manual Operation | |

| CNC Operation | ||

| By Machine Type | Automatic Screw Machines | |

| Rotary Transfer Machines | ||

| CNC Swiss-Type | ||

| Lathes/Turning Centers | ||

| By Material Type | Steel | |

| Aluminum | ||

| Titanium & Super-alloys | ||

| Plastics & Composites | ||

| By End-user Industry | Automotive & EV | |

| Aerospace & Defense | ||

| Medical & Dental | ||

| Electronics & Semiconductors | ||

| Industrial Machinery | ||

| Others (Construction, Fabrication Services, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global revenue be for precision turned products by 2031?

The precision turned product manufacturing market size is forecast to reach USD 172.31 billion by 2031 at a 6.06% CAGR.

Which operating mode dominates new capacity additions?

CNC Operation already holds 65.88% share and is expected to widen its lead thanks to 8.41% CAGR through 2031 and rising demand for lights-out production.

Why are Swiss-type machines growing faster than other lathe types?

Their guide-bushing design supports slender parts with sub-micron tolerances, making them indispensable for medical, electronics, and EV programs, which drives a 9.92% CAGR.

What region represents the largest demand pool today?

Asia-Pacific captured 38.60% of 2025 revenue, benefitting from China’s vast machine-tool sector and India’s double-digit expansion in precision machining.

How are defense contracts shaping material choices?

U.S. and NATO modernization programs specify titanium and Inconel components for missiles and artillery, lifting titanium and super-alloy demand at a 7.72% CAGR.

Page last updated on: