Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

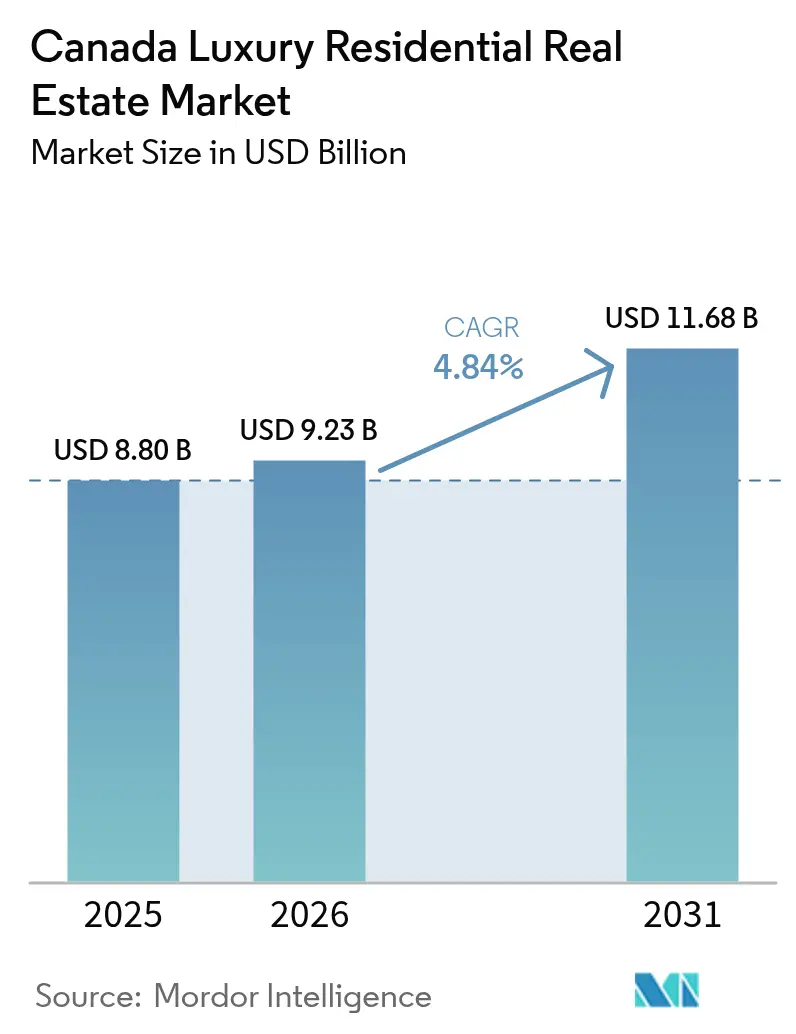

| Base Year Market Size (2025) | USD 8.8 Billion |

| Market Size (2026) | USD 9.23 Billion |

| Market Size (2031) | USD 11.68 Billion |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Canada luxury residential real estate market size is expected to grow from USD 8.8 billion in 2025 to USD 9.23 billion in 2026 and is forecast to reach USD 11.68 billion by 2031 at 4.84% CAGR over 2026-2031. Robust demand endures despite tighter regulations, buoyed by a USD 740 billion wealth transfer from baby boomers to younger households and sustained inflows of affluent immigrants. Transparent transaction processes introduced by Bill C-2, alongside foreign-buyer taxes, have re-balanced activity toward well-capitalized domestic purchasers and vetted international investors. Construction cost inflation, averaging 4.2% year-over-year in 2024, is reinforcing price resilience by limiting new luxury supply, while the Canada Green Buildings Strategy is nudging premium pricing for certified energy-efficient homes. These intertwined forces position the Canada luxury residential real estate market for measured, policy-aligned growth through 2030.

Key Report Takeaways

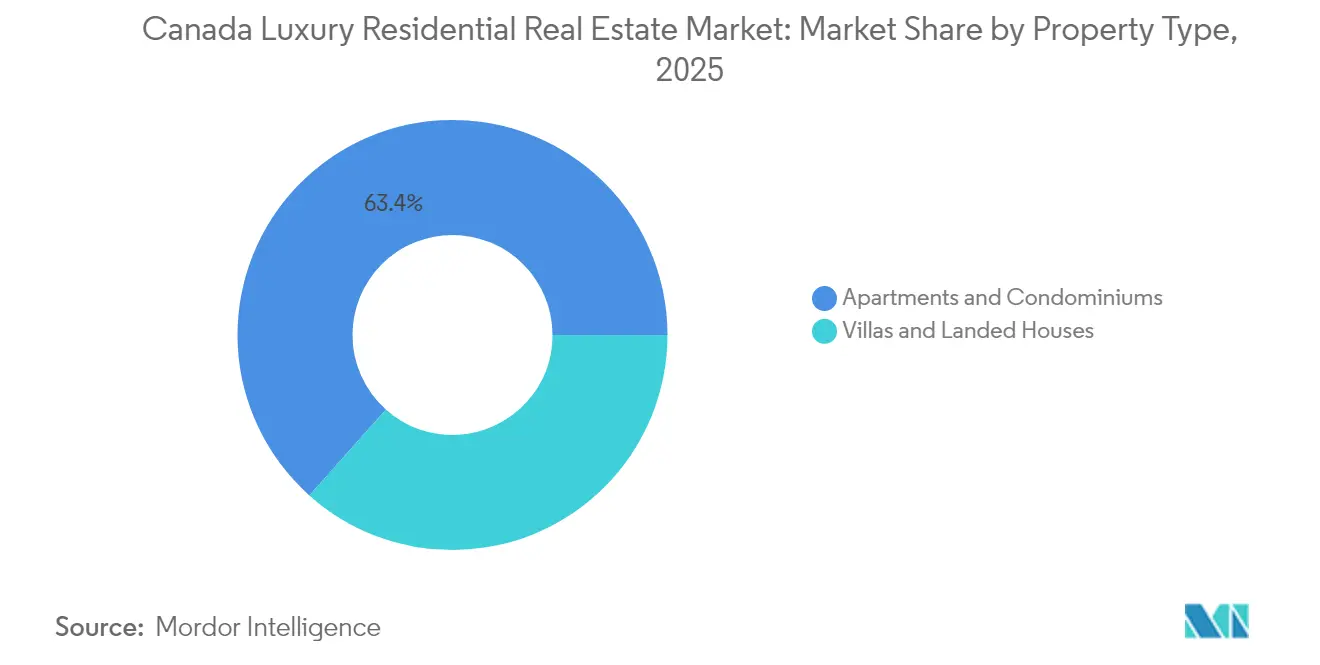

- By property type, apartments and condominiums led with a 63.40% revenue share of the Canada luxury residential real estate market in 2025; villas and landed houses are advancing at a 5.06% CAGR to 2031.

- By business model, the sales segment held 71.20% of the Canada luxury residential real estate market share in 2025, while rentals are projected to expand at a 5.12% CAGR through 2031.

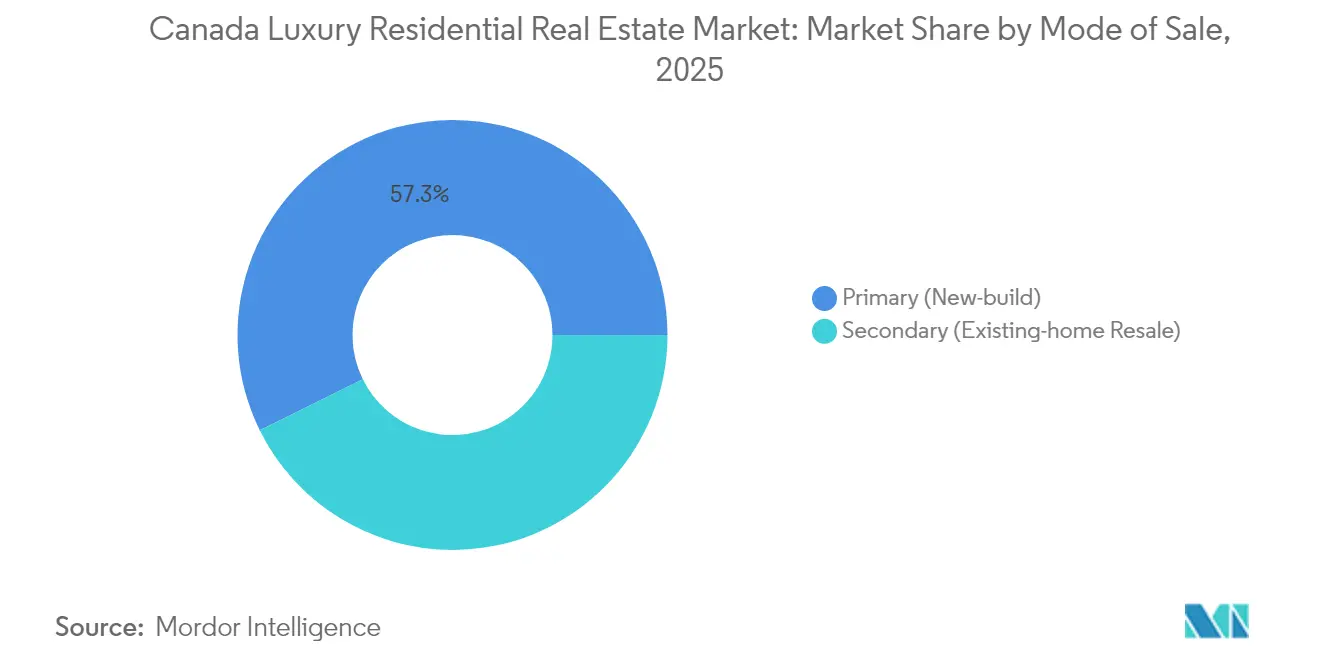

- By mode of sale, primary new-builds accounted for 57.30% share of the Canada luxury residential real estate market size in 2025 and are outpacing secondary resales at a 5.22% CAGR to 2031.

- By province, Ontario commanded 41.60% of the Canada luxury residential real estate market in 2025; British Columbia shows the fastest CAGR at 5.07% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging affluent population & inter-generational wealth transfer | +1.2% | National, concentrated in Toronto, Vancouver, Montreal | Long term (≥ 4 years) |

| Elite immigration & Golden Visa style pathways | +0.8% | Ontario, British Columbia, Quebec urban centers | Medium term (2-4 years) |

| Tight land-use regulations in Toronto & Vancouver | +0.6% | Greater Toronto Area, Greater Vancouver Area | Long term (≥ 4 years) |

| Tech-sector millionaire boom in Greater Toronto Area | +0.5% | Greater Toronto Area, spillover to Greater Vancouver Area | Medium term (2-4 years) |

| High adoption of green-building certifications in luxury segment | +0.4% | National, early adoption in BC and Ontario | Medium term (2-4 years) |

| Remote-work-driven demand in secondary resort towns | +0.3% | Alberta, Quebec, Atlantic Canada resort regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Affluent Population & Inter-Generational Wealth Transfer

Canada is witnessing its largest wealth handover, funnelling USD 740 billion primarily through real estate into next-generation portfolios. In 2024, 31% of first-time buyers received family gifts averaging USD 85,100, allowing younger cohorts to secure high-end condominiums in Toronto and Vancouver. Co-ownership structures are rising, with 17.3% of properties held jointly by 1990s-born owners and parents, amplifying purchasing power. This demographic force underpins sustained absorption in the Canada luxury residential real estate market and encourages developers to tailor multi-generational layouts. Over the long term, the wealth shift should keep transaction volumes robust even as policy hurdles intensify.

Elite Immigration & Golden-Visa Pathways

Fast-track visa streams—namely the Start-Up Visa and the Global Skills Strategy—are luring entrepreneurs who tend to purchase luxury homes within two years of arrival. Canada attracted 367,500 high-net-worth migrants in 2024, most settling in Toronto and Vancouver, where tech ecosystems align with global business ambitions. Two-week work-permit processing and a forthcoming Innovation Stream reduce relocation friction and fuel consistent top-tier housing demand. As a result, the Canada luxury residential real estate market benefits from a predictable influx of buyers with strong liquidity. Medium-term momentum remains favourable as provinces compete to refine nominee programs that bundle residency with property investment[1]Immigration, Refugees and Citizenship Canada, “Canada’s Tech Talent Strategy 2024,” Government of Canada, canada.ca.

Tight Land-Use Regulations in Major Hubs

Urban containment policies inflate replacement costs by USD 962,000 in Vancouver and USD 259,000 in Toronto, elevating entry prices for detached luxury stock. Lengthy 20.3-month approval timelines and development fees of USD 122,100 per unit push developers toward vertical luxury projects that maximize scarce land. Consequently, high-rise condominiums dominate the urban core while landed estates move to outer suburbs and resort towns. The regulatory premium strengthens margins for established players who possess entitlements and streamlines purchaser expectations toward condensed, amenity-rich living. Over the long term, constrained land supply is expected to reinforce capital appreciation in the Canada luxury residential real estate market.

High Adoption of Green-Building Certifications

Net-zero objectives enshrined in the Canada Green Buildings Strategy are turning LEED Platinum and similar certifications into standard fare for upscale developments. Shared mechanical systems in luxury towers spread the added cost of renewable energy installations, making sustainable features cost-effective. Buyers reward these attributes with quicker absorption and price premiums, while institutional investors channel ESG-linked capital—exemplified by a USD 185 million green bond from RBC’s core real estate fund—into compliant projects. Over the medium term, environmental credentials will be a mandatory differentiator across the Canada luxury residential real estate market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding foreign-buyer taxes & ownership bans | -0.7% | Ontario, British Columbia, select municipalities | Short term (≤ 2 years) |

| Run-up in land & construction input costs | -0.5% | National, acute in Toronto, Vancouver, Calgary | Medium term (2-4 years) |

| FINTRAC anti-money-laundering scrutiny on offshore capital | -0.4% | National, concentrated in major urban centers | Short term (≤ 2 years) |

| Climate-risk-driven insurance premium surge on coastal assets | -0.3% | British Columbia, Atlantic Canada coastal regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Foreign-Buyer Taxes & Ownership Bans

New levies include Toronto’s 10% Municipal Non-Resident Speculation Tax and British Columbia’s 20% Home Flipping Tax, layering on top of earlier provincial and federal restrictions. These measures have thinned casual offshore demand yet channel remaining interest toward rental partnerships and long-term immigrants with stronger local ties. Developers are recalibrating product mixes to cater to domestic families and permanent residents, mitigating price volatility. Although growth moderates in the short term, clearer rules foster healthier absorption patterns in the Canada luxury residential real estate market as speculative churn subsides.

FINTRAC Anti-Money-Laundering Scrutiny on Offshore Capital

Expanded reporting rules now cover mortgage brokers and outlaw cash payments over USD 7,400, adding compliance layers to large-ticket home deals. FINTRAC levied USD 6.8 million in penalties on real estate entities in 2024, signalling tough oversight. Additional due diligence costs lengthen closings, especially when foreign trusts or layered ownership structures are involved, temporarily cooling transaction velocity at the luxury end. However, heightened transparency ultimately boosts buyer confidence and aligns the Canada luxury residential real estate market with global best practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Condominiums Anchor Urban Luxury Demand

Apartments and condominiums captured 63.40% of the Canada luxury residential real estate market share in 2025, making them the clear volume leader. Land scarcity in Toronto and Vancouver, combined with planning policies that encourage density, cements the dominance of tower living. Construction input costs rose 0.6% quarter-over-quarter for high-rise projects versus 0.9% for single-family builds, giving developers greater pricing flexibility on condominiums. Energy-efficient glazing, concierge-level services, and smart-building systems reinforce value perception among affluent professionals and international executives.

Villas and landed houses, while holding a smaller slice, represent the fastest-growing niche with a 5.06% CAGR through 2031. Upscale buyers seeking privacy are turning to edge-city enclaves in Oakville, West Vancouver, and Mont-Tremblant, where larger parcels permit bespoke architecture. This sub-segment benefits from the Canada Green Buildings Strategy’s retrofit incentives, enabling owners to elevate heritage properties to net-zero status and preserve long-term appeal. Accordingly, the Canada luxury residential real estate market size for landed estates is projected to expand meaningfully even under supply restrictions.

By Business Model: Sales Still Rule, Rentals Rising

Sales transactions retained a 71.20% foothold in 2025, underlining the inclination of wealthy households to lock in capital gains within bricks and mortar. Inter-generational co-ownership, facilitated by parental equity transfers, continues to underpin down-payments in prime cities. Corporate relocations and cross-border executives, however, are boosting luxury leases, driving the rental channel at a brisk 5.12% CAGR to 2031. Minto Apartment REIT’s average monthly rent climbed to USD 1,496 in early 2025, a signal that premium yields remain intact.

Foreign-buyer taxes have nudged some global investors toward income-generating strategies that avoid title transfer complications yet still capture exposure to the Canada luxury residential real estate market. High-end furnished leasing platforms now bundle concierge services, aligning with expectations of nomadic tech founders and entertainment talent. As a result, rental growth provides a safety valve that maintains occupancy levels when policy deterrents temporarily cool purchase volumes.

By Mode of Sale: New-Builds Maintain Premium

Primary new-builds accounted for 57.30% of the Canada luxury residential real estate market size in 2025, reflecting buyer appetite for modern layouts, touchless technologies, and ESG credentials. Development fees of USD 122,100 per unit are more absorbable at luxury price points, leaving gross margins intact. Builders with deep land banks and in-house approval expertise, such as Concord Pacific and Westbank, are rolling out landmark towers that set new benchmarks for amenity design.

Secondary resales are forecast to climb at a 5.22% CAGR as inventory tightening pushes price premiums in established districts like Forest Hill and Shaughnessy. Retrofit subsidies under the Canada Green Buildings Strategy reduce the energy-efficiency gap versus new stock, defending the value proposition of older mansions. Consequently, the Canada luxury residential real estate market share of resales is inching upward, balancing the supply mix across the forecast horizon.

Geography Analysis

Ontario’s 41.60% share underscores Toronto’s gravitational pull on capital from banking, insurance, and a surging tech workforce. Price resilience owes much to constrained new-build pipelines, where approval times stretch past 20 months and development charges exceed USD 122,100 per unit. The new 10% foreign-buyer levy encourages partnerships with permanent residents, rerouting some international demand toward rent-to-own structures that keep funds circulating within the Canada luxury residential real estate market. Sellers also benefit from the wealth transfer tailwind, unlocking equity to assist children with urban condo purchases.

British Columbia is the growth pacesetter, supported by strong immigration inflows and enduring demand from Asia-Pacific entrepreneurs. Vancouver’s home sales rose 21% year-over-year in early 2025 compared with Toronto’s 8% uptick, highlighting firmer underlying momentum. The province’s Home Flipping Tax curbs short-term churn, favouring end-users and long-horizon investors who elevate the quality of stock through energy-saving retrofits. Elevated renovation costs—up 5.8% year-over-year—have yet to deter buyers seeking panoramic waterfront views and proximity to U.S. West Coast venture hubs.

Secondary markets such as Quebec’s Laurentians, Alberta’s Canmore–Banff corridor, and Atlantic Canada’s coastal retreats are benefiting from remote-work freedoms. Calgary’s New Housing Price Index gained 4.5% during 2024, a sign that energy-sector bonuses are filtering into prestige property purchases. In Atlantic Canada, improved air connectivity and favorable taxation are drawing Toronto expatriates who can now maintain metropolitan careers while enjoying resort lifestyles. This dispersion broadens the Canada luxury residential real estate market, smoothing regional volatilities and promoting cross-country liquidity.

Competitive Landscape

The Canada luxury residential real estate market is fragmented, with regional titans leveraging political know-how and capital heft to secure coveted sites. Brookfield Residential and Tridel are deepening joint-venture pipelines that share approval risk while accelerating project launches. Concurrently, niche developers such as Westbank integrate art collaborations and climate-positive design to command global attention and premium pricing. Technology adoption—ranging from AI-driven energy management to blockchain title platforms—serves as a key differentiator amid rising buyer sophistication.

Institutional capital is scaling up: RBC’s core real estate fund lifted gross assets beyond USD 5 billion in 2025 after issuing a USD 185 million green bond, channeling proceeds into LEED Platinum towers in Vancouver and Ottawa. Pension funds favor ESG-compliant luxury rental projects that hedge inflation and meet sustainability mandates, reinforcing competition for shovel-ready land. Meanwhile, private equity groups are quietly amassing secondary-city land banks, anticipating remote-work-induced migration that will broaden the Canada luxury residential real estate market footprint[3]Office of the Superintendent of Financial Institutions, “Residential Mortgage Underwriting Practices Review 2025,” OSFI, osfi-bsif.gc.ca.

Regulatory compliance now shapes strategic choices. Larger players maintain in-house anti-money-laundering teams to navigate FINTRAC rules, a capability smaller rivals struggle to replicate. Developers able to prove transaction transparency gain smoother funding approvals from banks mindful of hefty AML fines. As a result, consolidation is likely to intensify, with joint ventures and platform acquisitions offering scale economies that uphold pricing power in a cost-inflation environment.

Canada Luxury Residential Real Estate Industry Leaders

Westbank Corp

Concord Pacific

Brookfield Residential

Mattamy Homes

Tridel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Minto Apartment REIT purchased a 50% stake in Vancouver’s Lonsdale Square, expanding its luxury rental footprint in a supply-constrained market. The trust also reported average monthly rents of USD 1,496, up 5.3% year over year, confirming robust demand for high-end leases.

- March 2025: Ottawa enacted sweeping anti-money-laundering amendments that require detailed beneficial-ownership disclosure for every real-estate deal. The new rules strengthen coordination among FINTRAC, banks, and the Canada Border Services Agency, lengthening closing timelines but boosting market transparency.

- January 2025: The RBC Canadian Core Real Estate Fund closed USD 860 million in asset purchases and issued a USD 185 million green bond, lifting its gross assets above USD 5 billion. Proceeds target LEED-certified residential towers in Vancouver and Ottawa, signaling institutional appetite for ESG-aligned luxury projects.

- January 2025: Toronto introduced a 10% Municipal Non-Resident Speculation Tax on foreign buyers, supplementing existing provincial and federal levies. The surcharge pushes many offshore investors toward joint ventures with permanent residents or premium rental strategies.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Canadian luxury residential real-estate market as the annual dollar value of completed sales and new-build commitments for owner-occupied or investment homes that sit in the top decile of local price distributions, typically above CAD 1 million in major metros, covering detached houses, villas, townhomes, apartments, and condominiums.

Scope Exclusion: raw land held for future subdivision and commercial-residential mixed-use towers are omitted.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Business Model

- Sales

- Rental

- By Mode of Sale

- Primary (New-build)

- Secondary (Existing-home Resale)

- By Province

- Ontario

- British Columbia

- Quebec

- Alberta

- Rest of Canada

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed brokers, private-bank mortgage officers, boutique developers, and valuation surveyors across Ontario, British Columbia, Québec, and Alberta. These conversations validated absorption assumptions, clarified effective luxury tax burdens, and revealed average selling-price spreads between pre-sale and resale channels, which desk research alone could not capture.

Desk Research

We began with Statistics Canada deed-level transaction data, Canada Mortgage and Housing Corporation completions, and Canada Revenue Agency migration filings. We then added provincial land-registry extracts and luxury price indices compiled by the Canadian Real Estate Association. Trade associations such as the Urban Development Institute and the Canadian Home Builders' Association offered pipeline and cost benchmarks, while peer-reviewed pieces in the Journal of Property Investment & Finance clarified risk-adjusted discount rates. Paid datasets, including D&B Hoovers for developer revenues and Dow Jones Factiva for deal news, helped map corporate footprints. This list is illustrative; many additional sources informed our desk work.

Market-Sizing & Forecasting

A top-down construct starts with national luxury turnover reported by provincial registries, adjusted for under-reported private deals, and then split by province using luxury share of total residential sales. Bottom-up checks, sampling developer disclosures and MLS closed prices, calibrate average selling prices and unit counts. Key variables include high-net-worth migrant inflows, prime mortgage rates, luxury inventory months, and the Teranet-National Bank home price index. Multivariate regression ties these drivers to value growth; scenario analysis stress-tests interest-rate and tax shocks before results are finalized.

Data Validation & Update Cycle

Outputs pass three layers: automated variance scans, peer review by a senior real-estate specialist, and a final sign-off before publication. Models refresh each year, with mid-cycle updates triggered by policy shifts or greater than 5 percent price swings.

Why Mordor's Canada Luxury Residential Real Estate Baseline Is Trustworthy

Published estimates often diverge because firms choose dissimilar price thresholds, bundle land transfers, or rely on listing prices rather than closed values.

Key gap drivers include differing scope, as some fold in mixed-use towers, currency treatment, and refresh cadence; several providers also apply headline average prices to all units without inventory aging adjustments, inflating totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.80 B (2025) | Mordor Intelligence | |

| USD 66.58 B (2024) | Global Consultancy A | Applies national luxury turnover without filtering for decile thresholds and includes land-only trades |

| USD 183.8 B (2024) | Regional Consultancy B | Bundles commercial mixed-use, relies on asking prices, and lacks inflation normalization |

The comparison shows that by selecting a clear luxury threshold, cross-checking registry data with broker intelligence, and updating annually, Mordor delivers a balanced, transparent baseline clients can replicate and trust.

Key Questions Answered in the Report

What is the current size of the Canada luxury residential real estate market?

The market is valued at USD 9.23 billion in 2026, with a forecast value of USD 11.68 billion by 2031.

Which property type dominates the Canada luxury residential real estate market?

Apartments and condominiums command 63.40% of 2025 revenue, reflecting high-density development trends in Toronto and Vancouver.

Why is British Columbia the fastest-growing provincial market?

Vancouver’s tech expansion, Pacific Rim investment links, and strategic immigration policies support a 5.07% CAGR from 2026 to 2031.

How are foreign-buyer taxes affecting luxury sales?

Higher levies are trimming speculative offshore demand but steering remaining interest toward rental structures and long-term residency buyers.

What competitive edge do green-certified projects offer?

LEED-level buildings attract ESG-focused capital and command price premiums, aligning with Net-Zero 2050 targets outlined by Natural Resources Canada.

How big is the anticipated inter-generational wealth transfer influencing the market?

An estimated USD 740 billion in real-estate-linked wealth is shifting to younger Canadians between 2023 and 2026, fueling luxury purchases.

Page last updated on: