Nigeria Location-based Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

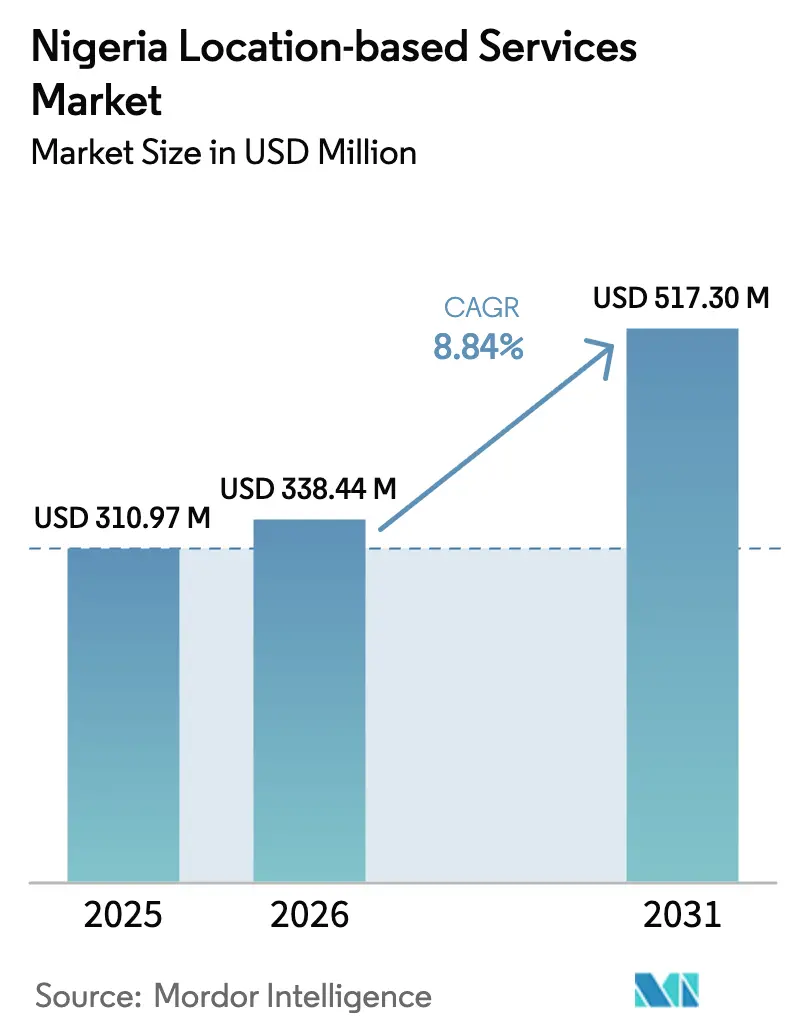

| Base Year Market Size (2025) | USD 310.97 Million |

| Market Size (2026) | USD 338.44 Million |

| Market Size (2031) | USD 517.3 Million |

| Growth Rate (2026 - 2031) | 8.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Location-based Services Market Analysis by Mordor Intelligence

Nigeria location-based services market size in 2026 is estimated at USD 338.44 million, growing from 2025 value of USD 310.97 million with 2031 projections showing USD 517.3 million, growing at 8.84% CAGR over 2026-2031. Uptake accelerates because mobile data already contributes 13.5% of GDP and policy reforms now require real-time geographic verification for many digital transactions. Fast 5G take-up, satellite back-haul and falling data tariffs extend coverage beyond large cities, enabling platforms in logistics, fintech and healthcare to embed precise location intelligence. Services rather than hardware dominate spending, as enterprises prefer turnkey integration to navigate Nigeria’s complex addressing environment. At the same time, Indoor mapping gains momentum alongside new malls and mixed-use complexes in Lagos and Abuja, indicating a shift from pure outdoor navigation toward hybrid environments.

Key Report Takeaways

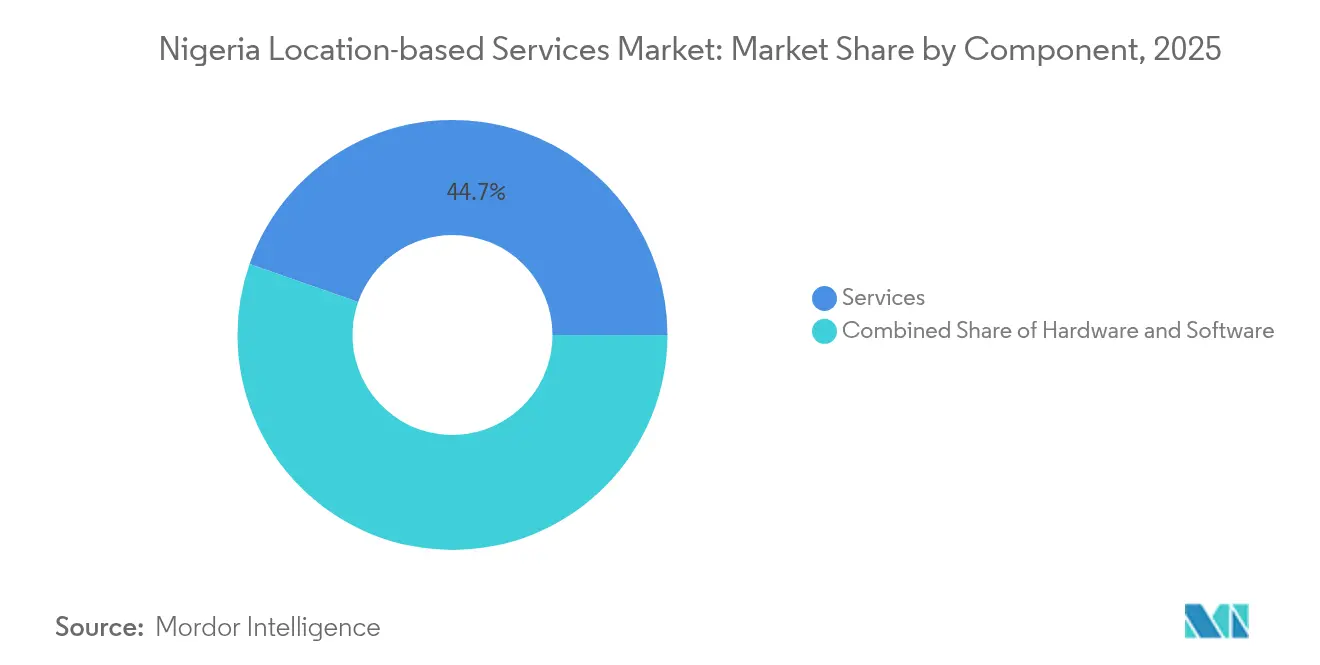

- By component, Services captured 44.65% of Nigeria location-based services market share in 2025 while advancing at a 15.03% CAGR to 2031.

- By location type, Outdoor applications commanded 51.70% share of the Nigeria location-based services market size in 2025, whereas Indoor solutions are expanding at 20.33% CAGR through 2031.

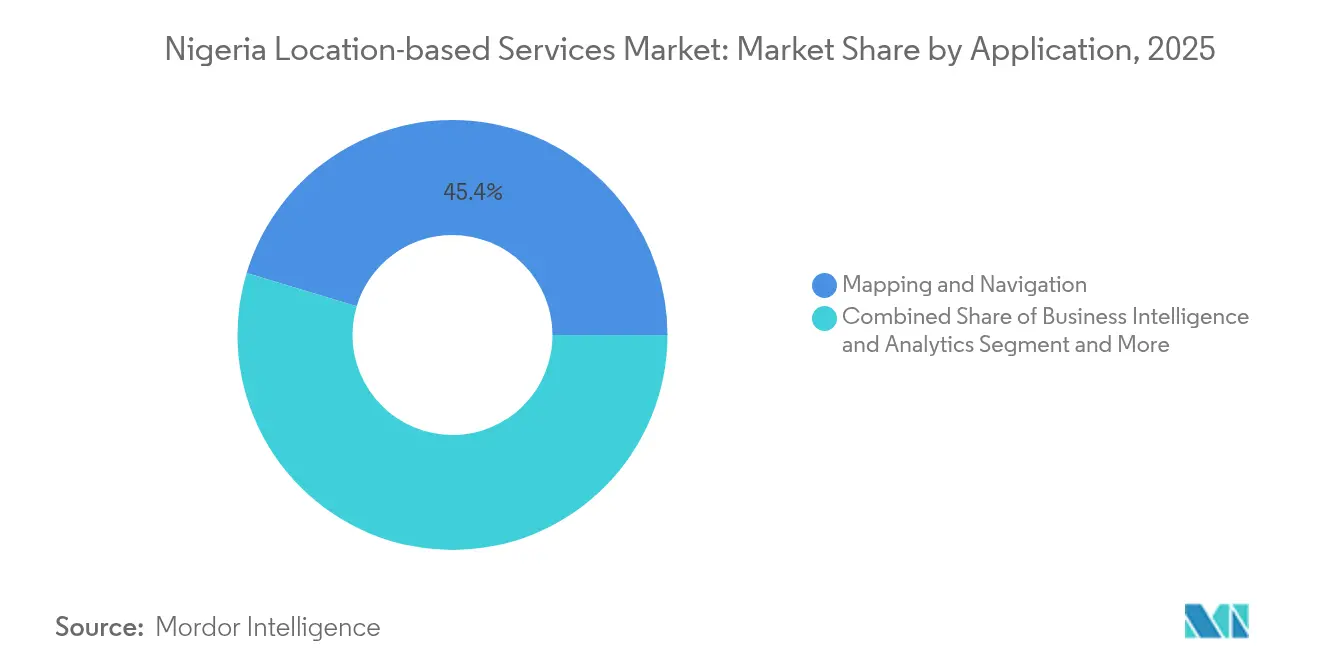

- By application, Mapping & Navigation held 45.35% share of the Nigeria location-based services market size in 2025, yet Social Networking & Entertainment is projected to grow at 25.32% CAGR between 2026-2031.

- By end-user, Transportation & Logistics led with 40.85% of Nigeria location-based services market share in 2025; Healthcare records the fastest forecast CAGR at 18.91% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Figures recorded within Nigeria feed into a worldwide estimate while studying the global industry. Mordor Intelligence's location based services market size captures this aggregation.

Nigeria Location-based Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising e-commerce and on-demand delivery boom | +2.1% | Lagos, Abuja, Port Harcourt | Medium term (2-4 years) |

| Rapid smartphone adoption and falling data tariffs | +1.8% | Nationwide, rural catch-up | Short term (≤ 2 years) |

| State-supported digital economy and cash-lite push | +1.5% | National | Long term (≥ 4 years) |

| Telco mini-satellite projects improving coverage | +1.3% | Rural and underserved zones | Medium term (2-4 years) |

| Indoor mapping demand from new mega-malls | +0.9% | Lagos and Abuja retail hubs | Short term (≤ 2 years) |

| Government proof-of-address roll-out | +0.7% | 774 local government areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising e-commerce and on-demand delivery boom

Nigeria’s online retail revenues surge on platforms such as Jumia, whose national GMV share rose to 40.1% in 2023, making accurate geolocation essential for fraud screening and last-mile routing. Automated locker networks launched in 2024 depend on precise coordinates for parcel sorting. Digital freight start-ups like Kobo360 match cargo with drivers in real time, cutting empty-backhaul miles [1]BBC News, “How Cargo Delivery Is Going Digital in Nigeria,” bbc.com. Supermarket chains are opening fulfilment hubs that require indoor-to-outdoor navigation continuity, pushing demand for advanced mapping APIs. The postal authority’s partnership with What3words further institutionalizes granular addressing that underpins delivery efficiency.

Rapid smartphone adoption and falling data tariffs

Smartphone data usage almost doubled in 2025 as operators trimmed tariffs, even though handset shipments fell 7% amid currency pressure. Existing users therefore spend more time using location-enabled apps, lifting service revenues; MTN’s Q1 2025 data income jumped 51.5% to NGN 1 trillion. Low-latency 5G now covers 35.7% of connections, enabling immersive AR navigation on lower-spec devices. Continued affordability drives depend on easing inflation and local assembly incentives to arrest handset price spikes.

State-supported digital economy and cash-lite push

The National Digital Economy Policy clarifies that geospatial data is critical infrastructure, while the payments vision mandate’s location verification for high-value transfers. Federal upskilling schemes backed by Google.org produce developers able to build secure geolocation modules. The cash-lite mandate lifted proximity-based mobile transfer volumes on banking apps such as GTWorld, reinforcing everyday reliance on precise positioning. Implementation setbacks, like last year’s note redesign shortfall, demonstrate the need for coordinated infrastructure rollouts to sustain momentum.

Telco mini-satellite projects improving coverage

Satellite back-haul initiatives let operators fill rural gaps at lower capex than fibre; Intelsat’s CellBackhaul service and MTN’s Omnispace deal extend signal reach for IoT and navigation apps. AMN is running Starlink-powered base stations that offer consistent latency, a prerequisite for real-time asset tracking. Federal approval for four new surveillance satellites underscores long-term policy support for space-enabled location accuracy. Subscription fees remain high, so hybrid terrestrial-satellite models will dominate until unit costs fall.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy legislation compliance costs | −1.2% | Nationwide, multinationals affected | Short term (≤ 2 years) |

| Patchy 4G/5G coverage in hinterland | −0.8% | Rural and remote districts | Medium term (2-4 years) |

| Fragmented addressing system outside cities | −0.7% | Semi-urban and rural areas | Long term (≥ 4 years) |

| Low consumer trust in ride-hailing accuracy | −0.5% | Major cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-privacy legislation compliance costs

The Nigeria Data Protection Act 2023 obliges major data controllers to register, appoint officers and localise processing, raising fixed costs for smaller geolocation start-ups. Breaches attract fines up to NGN 10 million or 2% of revenue, a risk highlighted by the Central Bank’s NGN 250 million penalty on a fintech in April 2025. Cross-border transfer restrictions force global providers to invest in Nigerian data centres, shifting capex toward compliance rather than product upgrades. Mandatory user consent adds friction, so ride-hailing firms face stricter controls over trip data sharing with regulators.

Patchy 4G/5G coverage in hinterland

Only MTN and Airtel deliver >70% 4G availability, while rural communities often rely on 2G, limiting uptake of latency-sensitive location apps. Operators estimate USD 3-8 billion is still needed for full 5G rollout, delaying nationwide parity. Roughly 40 million citizens remain uncovered, shrinking the immediate addressable base. Satellite alternatives help but remain expensive as Starlink raised tariffs in late 2024.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services gain from integration complexity

Services hold 44.65% of Nigeria location-based services market share in 2025 because banks and retailers prefer turnkey geolocation suites that integrate compliance and mapping layers. Nigeria location-based services market size for Services is projected to expand at 15.03% CAGR through 2031 as providers like OkHi verify addresses for KYC in minutes. Hardware adoption lags as smartphone imports dip due to currency swings, yet local innovators showcase micro-tracking devices that could spur niche demand when prices stabilise. Software vendors embed modules in existing mobile apps, evident in Access Bank’s “access more” rollout featuring nearby payment prompts. Continuous evolution of the Nigeria Data Protection Act pushes corporates to outsource location compliance rather than build in-house stacks, reinforcing Service dominance.

Conversely, the Hardware slice faces price shocks from import duties and naira devaluation, constraining mass upgrades. Cloud-native Software benefits from low entry barriers, yet fragmentation drives buyers toward end-to-end subscription bundles. The resulting Services premium supports healthy margins and encourages international vendors to seek local partnerships that adapt mapping layers to Nigeria’s dynamic address code systems.

By Location Type: Indoor growth narrows outdoor lead

Outdoor use cases still account for 51.70% of Nigeria location-based services market share thanks to freight, ride-hailing and agriculture. Nigeria location-based services market size for Indoor applications, however, is on track to grow 20.33% CAGR as malls, hospitals and airports deploy Bluetooth beacons to guide visitors . Abuja and Lagos anchor several 20,000 m²-plus mixed-use centres where tenants demand floor-level analytics. Retailers integrate shelf-level heat maps with stock systems to curb lost sales, while hospitals map ward-to-pharmacy routes to cut turnaround time.

Indoor roll-outs face signal attenuation and need hybrid Wi-Fi, Bluetooth and magnetic tech. The arrival of local government proof-of-address databases will ease indoor-to-door delivery, spurring further investment. Outdoor services will keep leading in revenue thanks to road freight volumes, yet address standardization and construction of new malls suggest indoor usage will close the gap by decade-end.

By Application: Social entertainment disrupts navigation leadership

Mapping and Navigation delivers 45.35% of Nigeria location-based services market size in 2025 and remains core infrastructure for third-party apps. Nigeria location-based services market share for Social Networking and Entertainment, though smaller, is forecast to expand at 25.32% CAGR as young urban users share location-tagged video and AR games. Platforms like TikTok reach nearly 24 million adults, encouraging advertisers to target micro-locations. Messaging apps integrate ticket purchases tied to venue coordinates, broadening monetisation. Business Intelligence adopters in fast-food chains overlay footfall data on delivery zones to refine site selection, while targeted advertising faces tighter consent rules under the data act.

Navigation remains mature but diversifies into sector-specific APIs—fleet management, drone corridors and hazard alerts. Entertainment will outpace as 5G AR games bridge social interaction and physical spaces, challenging category definitions.

By End-user Vertical: Healthcare accelerates against transport dominance

Transportation and Logistics comprised 40.85% of Nigeria location-based services market share in 2025 as ko-loc platforms orchestrated everything from ride-hailing to bulk cargo. Healthcare now shows the fastest 18.91% CAGR because telemedicine platforms rely on geotagging to dispatch community nurses and direct patients to nearest facilities.

Location-enabled maternal-care app OMOMi has scaled nationwide usage, illustrating sector potential. Banks deploy proximity transfer features to meet cash-lite mandates, while telecoms harness location analytics to plan base-station upgrades. Government usage rises via cadastral surveys and address verification, and hospitality players use beacons to raise guest satisfaction in a reviving travel market. Manufacturing uptake stays modest until Industry 4.0 pilots move beyond proof-of-concept, leaving room for late-cycle acceleration.

Geography Analysis

Lagos dominates the Nigeria location-based services market because it hosts most corporate headquarters and handles a quarter of national commerce. Starlink’s first Nigerian earth station and MTN’s new USD 150 million Tier III data centre both sit in Lagos, ensuring low-latency processing for ride-hailing and fintech apps. The state’s revised cadastral policy improves spatial data integrity, supporting land-registry digitisation and urban planning. Regulatory activism—such as hearings on ride-hailing commission caps—signals a demanding but structured environment for innovators. Abuja ranks second because federal ministries embed geolocation in public services and incubate e-government tools. Startup grants and the DeepTech training programme attract developers who create sovereign alternatives to foreign APIs. Local deployment of proof-of-address frameworks further deepens demand for secure mapping layers in identity verification and public safety.

Port Harcourt, Kano and Ibadan form the next tier. Port Harcourt’s oil base needs asset tracking and pipeline monitoring that hinge on rugged GPS and satellite links, especially under new local-content directives. Kano’s trading heritage drives cross-border logistics, although patchy coverage elevates interest in satellite back-haul. Ibadan’s trio of malls records higher foot traffic when indoor wayfinding apps are available, showcasing latent commercial potential. Rural belts lag due to 4G gaps that reduce coverage for about 40 million citizens, yet pilot Starlink base stations hint at faster inclusion once terminal costs fall.

Mordor Intelligence evaluates the location based services market across all key regional markets, including Africa and Middle East, with deeper country-level insights covering United Arab Emirates, Brazil, South Korea, China, Japan, India, and France.

Competitive Landscape

The Nigeria location-based services market hosts a mix of multinationals and agile locals, yielding moderate concentration. Google Maps still anchors most consumer navigation, but banks, logistics firms and health start-ups often prefer niche providers that tailor to Nigeria’s addressing gaps. OkHi and What3words both bid to standardise address codes, driving differentiation through financial-service integrations. MTN, Airtel and Globacom exploit vast subscriber data to upsell location analytics, while Uber and Bolt refine matching algorithms to stay ahead of 2,500 smaller ride-hailing entrants.

Satellite access is an emerging battleground. Starlink rose to second-largest ISP within two years, forcing mobile operators to accelerate rural coverage partnerships. Data-centre builds, exemplified by MTN’s Dabengwa facility, enable global cloud players to keep latency low and comply with data-localisation mandates, favoring deeper collaboration rather than direct rivalry. Compliance with the Data Protection Act screens out under-funded aspirants, subtly raising entry barriers and nudging the market toward higher professionalism.

White-space opportunities lie in indoor analytics, emergency dispatch, and agriculture drones. Providers that embed secure APIs into everyday consumer apps—such as GTBank’s Near Me transfer—gain stickiness without expensive customer acquisition campaigns. Continuous regulatory engagement, local talent development and address-system innovation remain decisive factors for sustained share gains.

Nigeria Location-based Services Industry Leaders

Google LLC

Microsoft Corporation

Apple Inc.

Huawei Technologies Co. Ltd

Uber Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Government approved four new satellites for surveillance and communications, enhancing nationwide positioning accuracy.

- March 2025: Starlink became Nigeria’s second-largest ISP with 65,564 subscribers, widening satellite coverage for rural location apps.

- February 2025: Nigeria-based remittance start-up Raenest raised USD 11 million Series A to scale location-enabled cross-border payments.

- January 2025: Federal Ministry launched first cohort of DeepTech_Ready Upskilling Programme supported by Google.org, boosting talent for geospatial product development.

Nigeria Location-based Services Market Report Scope

Location-based services can be defined as software services that utilize geographic data and information to provide services or information to users. The application collects geodata, data gathered in real-time using one or more location-tracking technologies, including GPS satellites, cellular tower pings, and short-range positioning beacons.

The Nigeria location-based services market is segmented by location (indoor and outdoor), service type (professional and managed), and end-user industry (transportation and logistics, manufacturing, retail, consumer goods, automotive, healthcare, and other end-user industries). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

| Hardware |

| Software |

| Services |

| Indoor |

| Outdoor |

| Mapping and Navigation |

| Business Intelligence and Analytics |

| Location-based Advertising |

| Social Networking and Entertainment |

| Other Applications |

| Transportation and Logistics |

| IT and Telecom |

| Healthcare |

| Government |

| BFSI |

| Hospitality |

| Manufacturing |

| Other End-users |

| By Component | Hardware |

| Software | |

| Services | |

| By Location Type | Indoor |

| Outdoor | |

| By Application | Mapping and Navigation |

| Business Intelligence and Analytics | |

| Location-based Advertising | |

| Social Networking and Entertainment | |

| Other Applications | |

| By End-user Vertical | Transportation and Logistics |

| IT and Telecom | |

| Healthcare | |

| Government | |

| BFSI | |

| Hospitality | |

| Manufacturing | |

| Other End-users |

Key Questions Answered in the Report

What is the current value of the Nigeria location-based services market?

The market is valued at USD 338.44 million in 2026, with a forecast to reach USD 517.3 million by 2031.

Which segment grows fastest in the Nigeria location-based services market?

Social Networking and Entertainment applications show the highest growth trajectory at 25.32% CAGR through 2031.

Why are Services the largest spending category?

Enterprises prefer turnkey geolocation solutions that bundle compliance, mapping and support, giving Services 44.65% market share in 2025.

How does regulation affect market growth?

The Nigeria Data Protection Act raises compliance costs and data-localisation requirements, trimming projected CAGR by 1.2 percentage points.

Page last updated on: