Canada HVAC Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

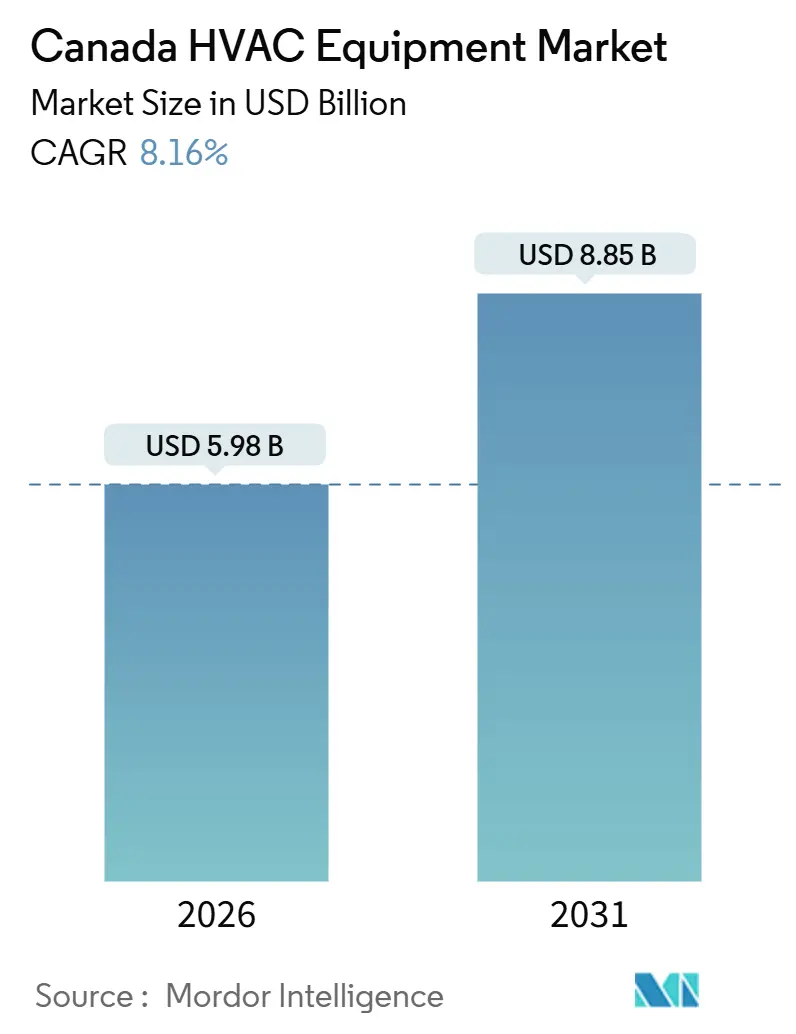

| Market Size (2026) | USD 5.98 Billion |

| Market Size (2031) | USD 8.85 Billion |

| Growth Rate (2026 - 2031) | 8.16% CAGR |

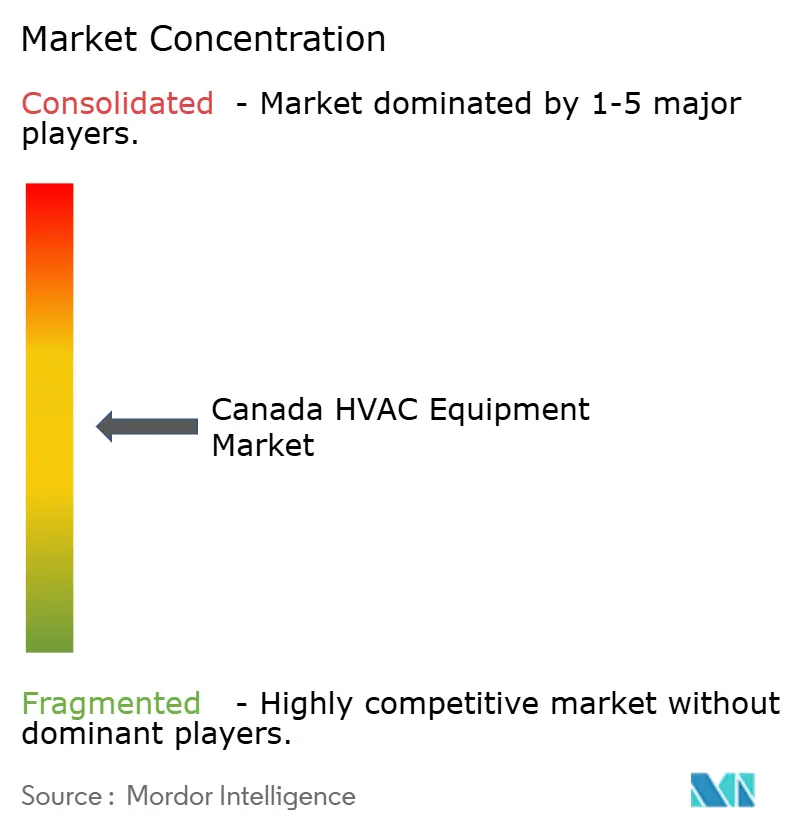

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada HVAC Equipment Market Analysis by Mordor Intelligence

The Canada HVAC equipment market size reached USD 5.98 billion in 2026 and is projected to climb to USD 8.85 billion by 2031, translating into an 8.16% CAGR. The forecast is anchored in carbon-pricing escalations, layered federal incentives for cold-climate heat pumps, and code-driven demand for heat-recovery ventilation in mixed-use construction. HVAC distributors are reshaping inventory around inverter-driven compressors, while building owners are bundling equipment procurement with energy-performance contracts that shift risk to engineering firms. Precision-cooling demand from hyperscale data centers, combined with stringent infection-control requirements in hospital expansions, is steering specifications toward modular air-handling units and variable-refrigerant-flow systems. Meanwhile, cannabis cultivation, now a mainstream commercial sub-sector, is fostering niche opportunities in integrated dehumidification and carbon-filtration HVAC packages.

Key Report Takeaways

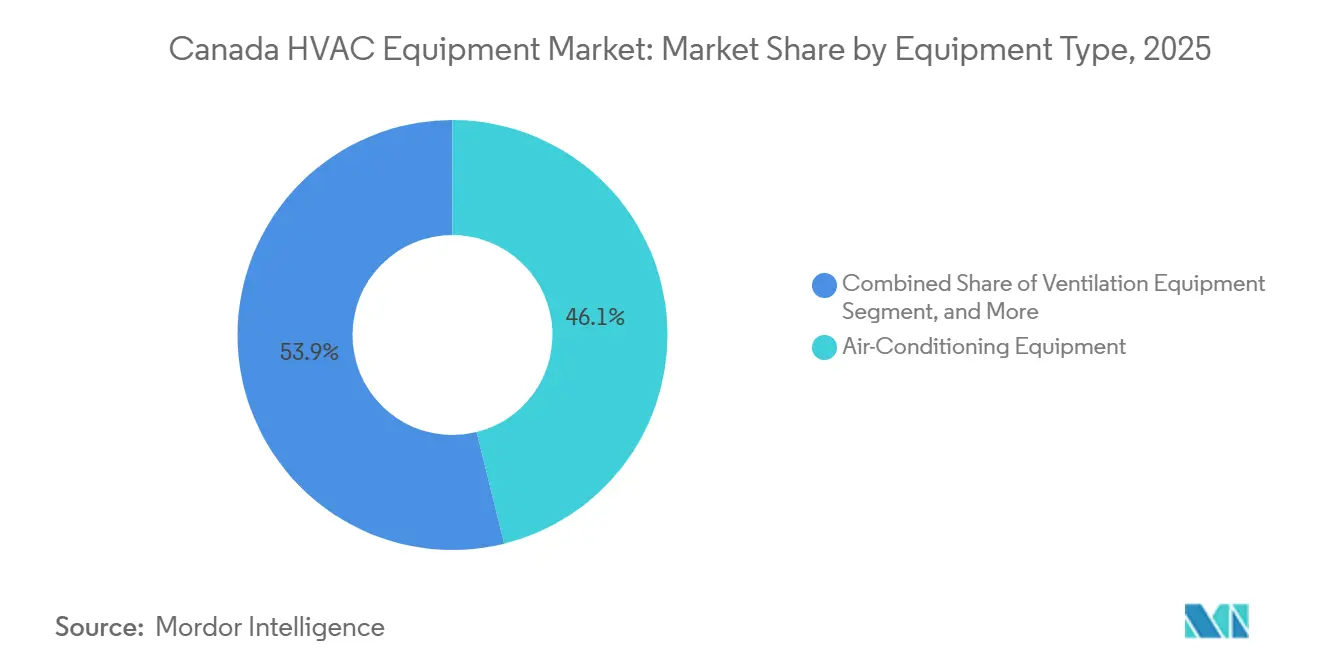

- By equipment type, air-conditioning equipment accounted for 46.14% of Canada's HVAC equipment market share in 2025, and the cooling segment is poised to grow at a 9.49% CAGR through 2031.

- By installation type, retrofit and replacement projects represented 62.35% of the Canada HVAC equipment market in 2025, whereas new construction is set to expand at a 9.84% CAGR on the back of density-friendly zoning reforms.

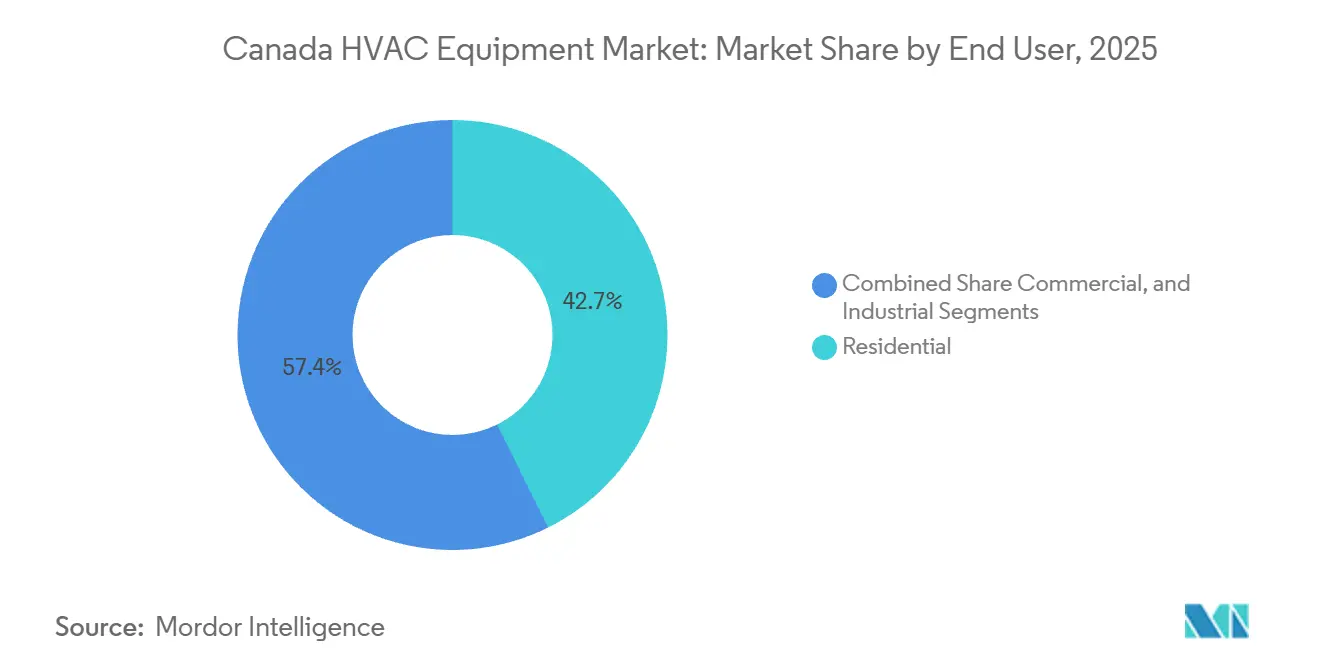

- By end user, the residential segment held 42.65% of revenue in 2025, but the commercial segment is forecast to grow at a 9.68% CAGR through 2031.

- By commercial building type, office buildings led with 35.63% of the Canada HVAC equipment market size in 2025, while data centers are advancing at a 10.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada HVAC Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Construction Activity | +1.50% | National, concentrated in Ontario, British Columbia and Quebec | Medium term (2-4 years) |

| Expansion of Green Building Standards and Energy Efficiency Regulations | +1.80% | National, led by Ontario and British Columbia early adoption | Long term (≥ 4 years) |

| Rising Demand for Heat Pumps Supported by Federal Incentives | +2.10% | National, heightened in Atlantic provinces and Quebec | Short term (≤ 2 years) |

| Electrification Mandates in Remote Communities Accelerating Modular HVAC Adoption | +0.80% | Northern territories and remote Indigenous communities | Medium term (2-4 years) |

| Federal Carbon Pricing Driving Early Replacement Cycles | +1.30% | National, excluding territories with exemptions | Short term (≤ 2 years) |

| Growth of Cannabis Cultivation Facilities Requiring Specialized HVAC | +0.40% | British Columbia, Ontario, Quebec and Alberta | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Heat Pumps Supported by Federal Incentives

Rebates that average CAD 10,000 (USD 7,299) per home under the Oil to Heat Pump Affordability Program helped fund 274,000 residential installations by November 2025.[1]National Research Council Canada, “National Energy Code for Buildings 2025,” Nrc-cnrc.gc.ca Cold-climate units designed for −25 °C operation accounted for 68% of those projects, reflecting OEM advances in enhanced-vapor-injection compressors. Provincial stack-on schemes such as Quebec’s Chauffez vert trimmed net homeowner costs to CAD 3,500 (USD 2,554), lifting regional installations by 34% year over year. Federal plans to phase out oil heating in public buildings before 2030 are amplifying the demonstration effect, as early adopters report annual fuel-cost savings of up to 50%. Distributors are therefore bulking up on variable-speed inventory, anticipating a threefold rise in annual heat-pump shipments by 2030.

Expansion of Green Building Standards and Energy Efficiency Regulations

The National Energy Code for Buildings 2025 edition tightens energy-use-intensity limits by 15%, effectively mandating heat-recovery ventilation across Canada’s new multi-family stock. Ontario’s SB-10 revision compels demand-controlled ventilation in commercial properties over 10,000 m², triggering retrofits of constant-air-volume systems. British Columbia’s mandatory Step Code grants density bonuses to projects surpassing baseline heat-pump performance by 20%, fast-tracking electrified HVAC adoption.[2]BC Housing, “BC Energy Step Code,” Bchousing.org Green procurement frameworks such as LEED v4.1 and the Canada Green Building Council’s Zero Carbon Building standard now treat HVAC efficiency as a bid qualifier. Together, these policies steer market demand toward OEMs with third-party-verified seasonal energy-efficiency ratios above 18.

Surge in Construction Activity

Residential building permits reached 252,000 units in 2025, after zoning liberalization enabled laneway housing and multiplexes on single-family lots. Non-residential investment reached CAD 89 billion that same year, with hospital and data center projects accounting for 22% of the total. The 2026 pipeline lists 18 hospital expansions requiring N+1 redundancy and tight humidity control, alongside 12 hyperscale data centers engineered for ±2 % humidity tolerance. Developers increasingly embed HVAC procurement in energy-performance contracts, transferring equipment-selection risk to engineering firms. Building information modeling workflows are therefore optimizing duct routing and refrigerant-line length before ground is broken, compressing project timelines by up to 6 %.

Federal Carbon Pricing Driving Early Replacement Cycles

Canada’s carbon levy rose to CAD 80 (USD 58.3) per tonne in April 2024 and will reach CAD 170 (USD 124.08) by 2030, adding CAD 0.18 (USD 0.13) per cubic meter to natural-gas costs. The levy shortens heat-pump payback from 9 years to 5.5 years in provinces without exemptions. In Calgary, heat pumps accounted for 18% of furnace replacements during the 2024-2025 heating season, up from 4% in 2022. Office landlords are fast-tracking boiler retirements as tenants pursue net-zero commitments, with 62% of Toronto's Class B towers initiating feasibility studies in 2025. OEMs are accordingly phasing out mid-efficiency furnaces in favor of condensing or hybrid systems that align with the escalating carbon-pricing trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Maintenance and Repair Costs | -0.60% | National, higher impact in remote and rural areas | Medium term (2-4 years) |

| Shortage of Skilled HVAC Technicians | -0.90% | National, acute in Alberta, Saskatchewan and Atlantic regions | Short term (≤ 2 years) |

| Supply-Chain Dependence on US Components Creating Currency Risk | -0.50% | National, all equipment types | Short term (≤ 2 years) |

| Low-GWP Refrigerant Phase-Down Increasing Retrofit Complexity | -0.70% | National, early impact in commercial and industrial segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled HVAC Technicians

Vacancies for 10,000 qualified technicians in 2025 lengthened commercial retrofit schedules by up to six weeks.[3]Heating, Refrigeration and Air Conditioning Institute of Canada, “Labour Market Intelligence,” Hrai.ca Alberta and Saskatchewan face the highest pressure because oil-and-gas trades pay CAD 20,000 (USD 14,598) more in average annual wages than HVAC employers. Apprenticeship completion for refrigeration mechanics fell to 52% in 2024, complicating the deployment of variable-refrigerant-flow and A2L refrigerant systems, which demand advanced commissioning skills. Some OEMs have opened factory-direct installation arms and remote diagnostic centers to offset contractor bottlenecks, raising internal overhead by nearly 10%. Unless workforce pipelines recover, skill shortages could cap growth in the Canada HVAC Equipment market during peak retrofit seasons.

Low-GWP Refrigerant Phase-Down Increasing Retrofit Complexity

Canada must cut hydrofluorocarbon consumption 10% below the 2020-2022 baseline by 2029. Transitioning from R-410A to mildly flammable A2L blends requires leak detection, revised brazing practices, and new service-van tooling under CSA B52-21. Distributors now finance dual inventories of legacy and next-generation refrigerants, boosting working capital by up to 15%. Office-tower chiller retrofits often demand electrical-panel upgrades to meet A2L safety codes, adding CAD 15,000-25,000 (USD 10,948-18,248) per system. Recovered R-410A prices climbed 40% in 2024-2025, underscoring the need for reclamation equipment but also inflating service costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Cooling Dominates Amid Climate Volatility

Air-conditioning equipment captured 46.14% of the Canada HVAC Equipment market share in 2025, and the segment is on track for a 9.49% CAGR through 2031. Ductless mini-splits have become the retrofit solution of choice for early-twentieth-century housing and low-rise condos that lack ductwork. Shipments of multi-zone units climbed 22% year over year in 2025 as SEER2-20 models offered sub-six-year payback in provinces with time-of-use tariffs. In commercial mid-rise projects, variable-refrigerant-flow systems are displacing conventional rooftop units owing to their zoning flexibility and simultaneous heating and cooling capability.

Heating equipment accounts for the second-largest slice of the Canada HVAC Equipment market, led by heat pumps, which now outsell gas furnaces in British Columbia after the 2024 natural-gas connection ban for low-rise buildings. Ventilation products, especially MERV 13 and HEPA filters, enjoyed an 18% boost in 2025 as school boards and hospitals responded to infection-control mandates. Water-cooled chillers are gaining share in Toronto’s district-energy loop, while packaged rooftop units remain the workhorse for single-story retail and cannabis grow facilities that need easy roof access.

By Installation Type: Retrofit Leads, New Construction Accelerates

Retrofit and replacement projects accounted for 62.35% of the Canada HVAC Equipment market in 2025, as federal rebates shortened the lifecycles of fossil-fuel equipment. In Atlantic Canada, fuel-oil furnace retirements now occur 3.2 years sooner than historical norms because heat-pump subsidies compress payback periods. Class B office towers built between 1980 and 2000 are allocating capital for HVAC upgrades to retain tenants who demand LEED-aligned premises. Integrating variable-speed heat pumps into constant-air-volume ductwork often requires panel upgrades and control reprogramming, raising installed costs to CAD 12,000-18,000 (USD 8,759-13,138) per residential unit.

New construction, expanding at 9.84% CAGR, is driven by zoning reforms such as Ontario’s More Homes Built Faster Act, which released higher-density permits and accelerated mixed-use starts by 19% in H1 2025. Developers now pre-install heat-recovery ventilators and cold-climate heat pumps, raising HVAC content per dwelling to CAD 9,500 (USD 6,934) in 2025. Data centers remain a premium sub-niche, with precision-cooling packages that can exceed CAD 15 million (USD 10.9 million) per site and demand PUE below 1.15.

By End User: Commercial Segment Outpaces Residential Growth

Residential still accounted for 42.65% of revenue in 2025, yet commercial demand is progressing at a 9.68% CAGR, underscoring the pivot toward office-to-residential conversions, hospital retrofits, and data-center builds. In Toronto and Vancouver, double-digit office vacancy rates are catalyzing conversions that require modular air-handling units compatible with legacy shafts. Provincial health ministries allocated CAD 680 million (USD 496 million) in 2025 for HVAC upgrades aligned with CSA Z317 infection-control standards, boosting uptake of HEPA-ready variable-air-volume systems.

Industrial users, notably cannabis cultivation and cold storage, are smaller yet rapidly scaling. Grow rooms added 220,000 m² in 2025, each square meter demanding up to 200 W of cooling. Cold-storage warehouses are specifying ammonia refrigeration with smart defrost controls, accepting 20% higher capex for 15% energy savings. Ottawa’s goal of 5.8 million installed heat pumps by 2030 necessitates tripling annual shipments versus 2023 levels.

By Building Type (Commercial): Data Centers Lead Expansion

Office structures held 35.63% of the Canadian HVAC Equipment market in 2025, but data centers led the growth chart with a 10.14% CAGR. Hyperscalers committed CAD 4.2 billion (USD 3.06 billion) to new capacity in Montreal, Calgary, and Toronto during 2024-2025, each facility requiring N+1 precision cooling and rack densities above 30 kW. Liquid-cooling architectures featuring rear-door heat exchangers from Vertiv and direct-to-chip modules are becoming mainstream.

Healthcare ranks second in growth, with 18 hospital expansions underway in 2025 that stipulate HEPA-filtered variable-air-volume systems and energy-recovery wheels. Educational institutions benefit from the CAD 420 million (USD 306 million) Healthy Schools Initiative, which finances demand-controlled ventilation upgrades in 1,200 facilities. Hotels and arenas are installing heat-recovery chillers that recycle waste heat into domestic hot-water loops, trimming gas bills by up to 40%. Retail malls are reinventing anchor boxes into mixed-use zones, necessitating flexible zoning and smart controls.

Geography Analysis

Ontario and Quebec combined accounted for 52% of national HVAC revenue in 2025, driven by dense populations, ambitious electrification timelines, and stringent code updates. Ontario’s 2025 building code now caps thermal-energy-demand intensity at 25 kWh/m²-year, virtually ensuring heat-pump adoption in new dwellings. Quebec’s Chauffez vert stacked rebates slashed homeowner costs to CAD 3,500 (USD 2,554) in 2025 and turned the province into Canada’s largest heat-pump market by units. British Columbia’s mandatory Step Code, operational since 2024, rewards builders with density incentives for exceeding heat-pump performance benchmarks, accelerating the displacement of gas furnaces.

Alberta and Saskatchewan historically favored gas heat because of cheap local supply, yet the federal carbon levy, rising CAD 15 (USD 10.9) annually, narrowed the operating-cost gap, spurring a jump in heat-pump share of furnace replacements to 18% in 2024-2025. Atlantic provinces reap outsized gains from the Oil to Heat Pump Affordability Program, which delivered 274,000 subsidized installations by November 2025, concentrated in fuel-oil-dependent rural communities. Northern territories and remote Indigenous settlements represent a high-growth niche, with the CAD 300 million (USD 218 million) REACHE initiative funding off-grid microgrids that demand -40 °C-rated packaged heat pumps.

Provincial utilities further shape demand through rate design. Hydro-Québec offers CAD 0.04/kWh (USD 0.029/kWh) off-peak industrial pricing, encouraging thermal storage that shifts the cooling load overnight. Ontario’s Independent Electricity System Operator launched a demand-response pilot in 2025, paying CAD 150 (USD 109) per curtailed kilowatt, catalyzing the adoption of grid-interactive controls. British Columbia’s CleanBC commits to a 40% cut in building emissions by 2030, financing heat-pump retrofits in social housing that set precedents for private adoption.

Competitive Landscape

The Canada HVAC Equipment market remains moderately fragmented, with major players including Carrier, Daikin, Trane, Johnson Controls, and Lennox. Competitive intensity is sharpening as electrification and refrigerant mandates compress product lifecycles. Daikin’s 60% stake in a Quebec heat-pump distributor, acquired in early 2025, secures last-mile installation capability and recurring service income. Carrier launched rooftop units with integrated photovoltaics in mid-2025, carving a foothold in cannabis cultivation facilities with high daytime cooling loads.

Regional specialists such as Engineered Air and Yorkland Controls thrive on custom projects with runs below 50 units, supplying modular air handlers for healthcare isolation rooms and data-center white spaces where global OEMs struggle to meet lead-time expectations. The refrigerant transition offers another front; early A2L-certified lineups from Mitsubishi Electric, LG Electronics, and Fujitsu General are winning spec preference among owners keen to future-proof assets ahead of the 2029 hydrofluorocarbon cut.

Patent activity tracked by the Canadian Intellectual Property Office highlights variable-speed compressors with vapor-injection, heat-recovery modules and predictive-maintenance algorithms that trigger service calls up to 72 hours before fault. Standards bodies, notably CSA Group and HRAI, are fast-tracking guidelines for A2L installations and grid-interactive rooftop units, removing ambiguity that once slowed adoption. Collectively, these dynamics underscore an innovation-driven trajectory for the Canada HVAC Equipment market.

Canada HVAC Equipment Industry Leaders

Daikin Industries Ltd

LG Electronics Inc.

Rheem Manufacturing Company Inc.

Trane Technologies plc

Nortek Air Solutions LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: LG Electronics received AHRI certification for a variable-refrigerant-flow system using R-454B, targeting commercial retrofits in advance of the 2029 refrigerant phase-down milestone.

- October 2025: Daikin Industries announced a CAD 45 million (USD 32.8 million) expansion of its Toronto-area distribution center, adding training labs for A2L installation.

- August 2025: Carrier Global launched packaged rooftop units with integrated solar PV panels aimed at cannabis cultivation and cold-storage facilities in western provinces.

- July 2025: Nortek Air Solutions introduced a modular air handler purpose-built for cannabis grows, undercutting rivals by 15% while integrating real-time CO₂ and humidity control.

- June 2025: Trane Technologies partnered with Enwave Energy to supply 120 water-cooled chillers for Toronto’s Deep Lake Water Cooling network expansion.

Canada HVAC Equipment Market Report Scope

HVAC equipment is a comfort technology for indoor and vehicle environments that provides thermal comfort and acceptable indoor air quality. This applies to residential buildings such as apartments, single-family homes, hotels, and elderly communities, as well as to medium- and large-scale industrial buildings such as clinics, where safe and healthy building conditions are controlled for temperature and humidity. It is also essential for office buildings as it adjusts humidity using fresh air from outside.

The Canada HVAC Equipment Market Report is Segmented by Equipment Type (Heating Equipment, Ventilation Equipment, and Air-Conditioning Equipment), Installation Type (New Construction, and Retrofit/Replacement), End User (Residential, Commercial, and Industrial), and Building Type (Office, Healthcare, Hospitality, Retail, Educational, and Data Centers). The Market Forecasts are Provided in Terms of Value (USD).

| Heating Equipment | Boilers and Furnaces | |

| Heat Pumps | ||

| Unitary Heaters | ||

| Ventilation Equipment | Air Handling Units (AHUs) | |

| Air Filters | ||

| Fan Coil Units | ||

| Humidifiers and Dehumidifiers | ||

| Air-Conditioning Equipment | Unitary Air Conditioners | Ducted Splits |

| Ductless Mini-Splits | ||

| Packaged Rooftops | ||

| Variable Refrigerant Flow (VRF) Systems | ||

| Room Air Conditioners | ||

| Packaged Terminal Air Conditioners | ||

| Chillers | ||

| New Construction |

| Retrofit / Replacement |

| Residential |

| Commercial |

| Industrial |

| Office Buildings |

| Healthcare Facilities |

| Hospitality and Leisure |

| Retail Stores and Malls |

| Educational Institutions |

| Data Centers |

| By Equipment Type | Heating Equipment | Boilers and Furnaces | |

| Heat Pumps | |||

| Unitary Heaters | |||

| Ventilation Equipment | Air Handling Units (AHUs) | ||

| Air Filters | |||

| Fan Coil Units | |||

| Humidifiers and Dehumidifiers | |||

| Air-Conditioning Equipment | Unitary Air Conditioners | Ducted Splits | |

| Ductless Mini-Splits | |||

| Packaged Rooftops | |||

| Variable Refrigerant Flow (VRF) Systems | |||

| Room Air Conditioners | |||

| Packaged Terminal Air Conditioners | |||

| Chillers | |||

| By Installation Type | New Construction | ||

| Retrofit / Replacement | |||

| By End User | Residential | ||

| Commercial | |||

| Industrial | |||

| By Building Type (Commercial) | Office Buildings | ||

| Healthcare Facilities | |||

| Hospitality and Leisure | |||

| Retail Stores and Malls | |||

| Educational Institutions | |||

| Data Centers | |||

Key Questions Answered in the Report

How large is the Canada HVAC Equipment market in 2026?

The Canada HVAC Equipment market size reached USD 5.98 billion in 2026 and is projected to hit USD 8.85 billion by 2031.

What is the expected growth rate for Canadian HVAC equipment through 2031?

The market is forecast to register an 8.16% CAGR during the 2026-2031 period.

Which equipment type leads Canada’s HVAC demand?

Air-conditioning systems, especially ductless mini-splits and VRF units, held 46.14% of 2025 revenue and remain the dominant category.

Why are heat pumps gaining traction across provinces?

Federal and provincial rebates, carbon-pricing pressures and updated building codes have shortened payback periods, triggering widespread heat-pump adoption.

Which commercial sub-sector is expanding fastest?

Data centers are advancing at a 10.14% CAGR thanks to hyperscale investments that require precision cooling and low PUE targets.

What factors limit HVAC growth in Canada?

Skill shortages among technicians and the complexity of transitioning to low-GWP refrigerants are restraining near-term expansion.

Page last updated on: