Propylene Glycol Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

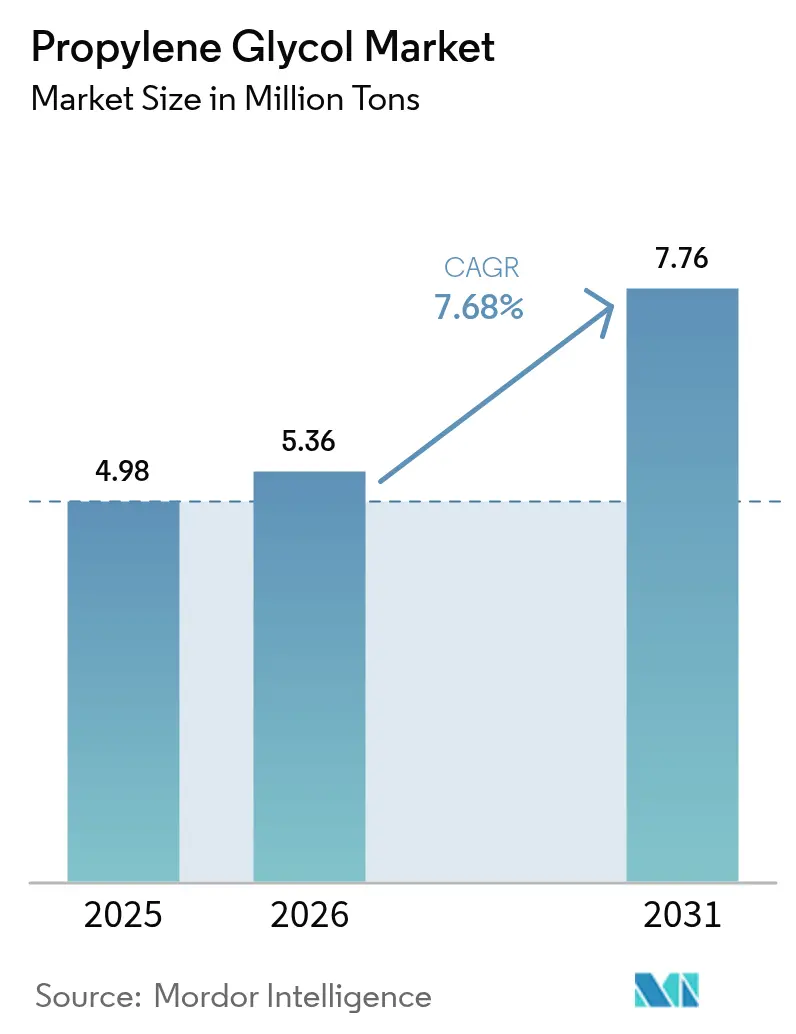

| Market Volume (2026) | 5.36 Million tons |

| Market Volume (2031) | 7.76 Million tons |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Propylene Glycol Market Analysis by Mordor Intelligence

The Propylene Glycol market size is expected to grow from 4.98 million tons in 2025 to 5.36 million tons in 2026 and is forecast to reach 7.76 million tons by 2031 at 7.68% CAGR over 2026-2031. Demand strength comes from unsaturated polyester resin (UPR) composites used in wind-energy blades, the widening use of United States Pharmacopeia-grade material in injectable drugs, and rising volumes of low-toxicity thermal-management fluids for electric vehicles. Direct catalytic technologies that convert propylene to propylene glycol in a single step are lowering unit costs and easing the integration of bio-circular feedstocks, while large Chinese capacity additions weigh on near-term margins in commodity grades. Automotive electrification, global infrastructure spending, and regulatory momentum for safer excipients underpin medium-term growth, yet price swings in propylene oxide feedstock and tighter impurity limits in high-dose pharmaceutical uses introduce volatility. Producers that secure International Sustainability and Carbon Certification (ISCC) PLUS status and scale bio-based routes capture a price premium in personal-care and drug channels, creating a two-tier market characterized by sustainability-attributed and commodity volumes.

Key Report Takeaways

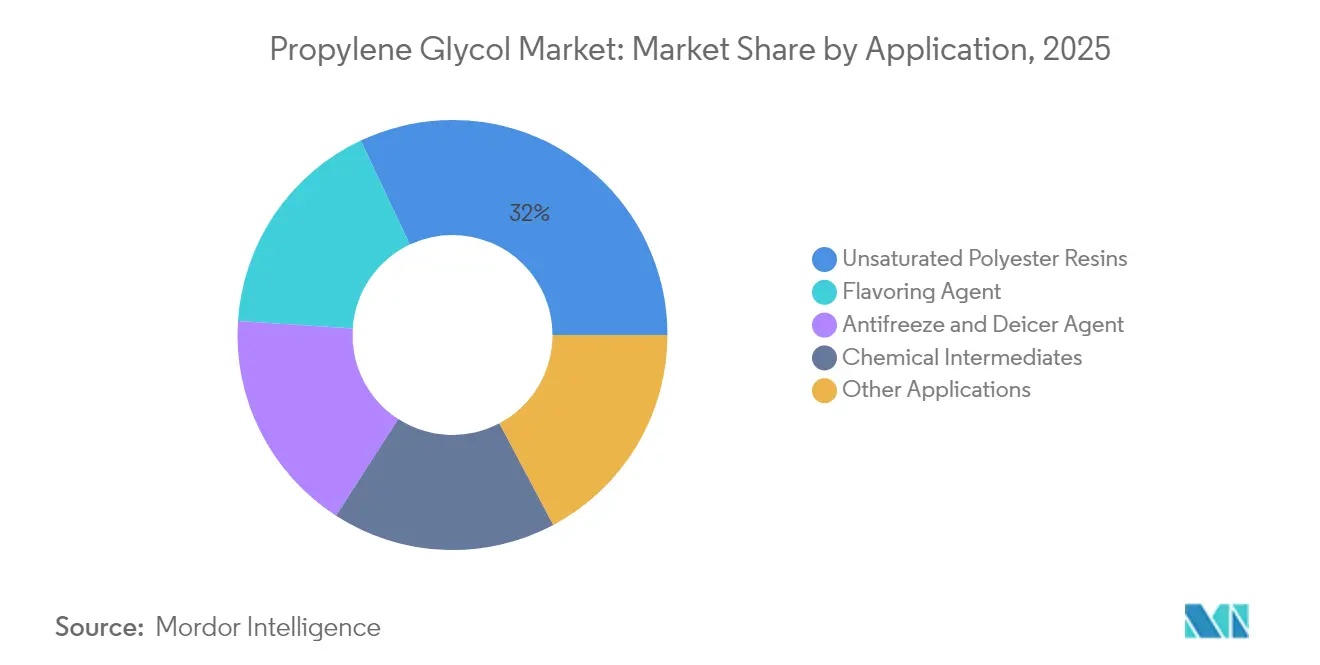

- By application, unsaturated polyester resins led with a 32.02% share of the propylene glycol market size in 2025. Personal-care intermediates are projected to expand at an 8.03% CAGR through 2031.

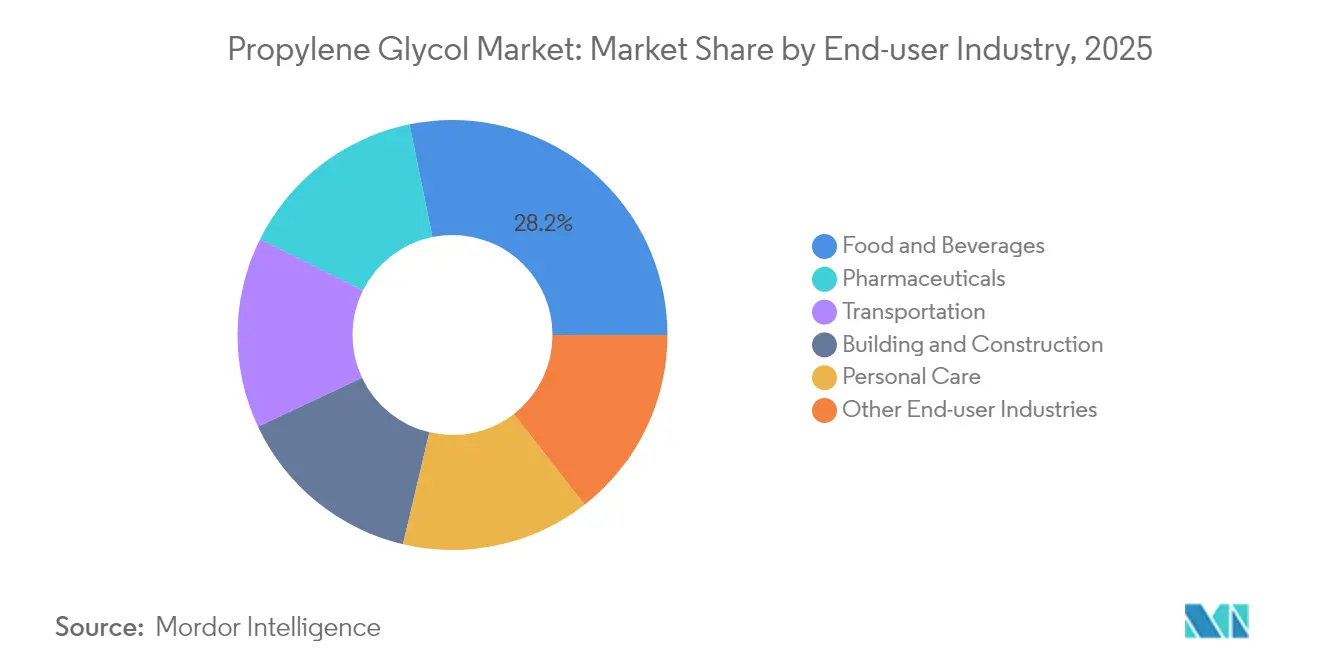

- By end-user industry, food and beverages accounted for 28.21% of the propylene glycol market share in 2025. Pharmaceuticals are forecast to post the fastest growth rate of 8.11% from 2021 to 2031.

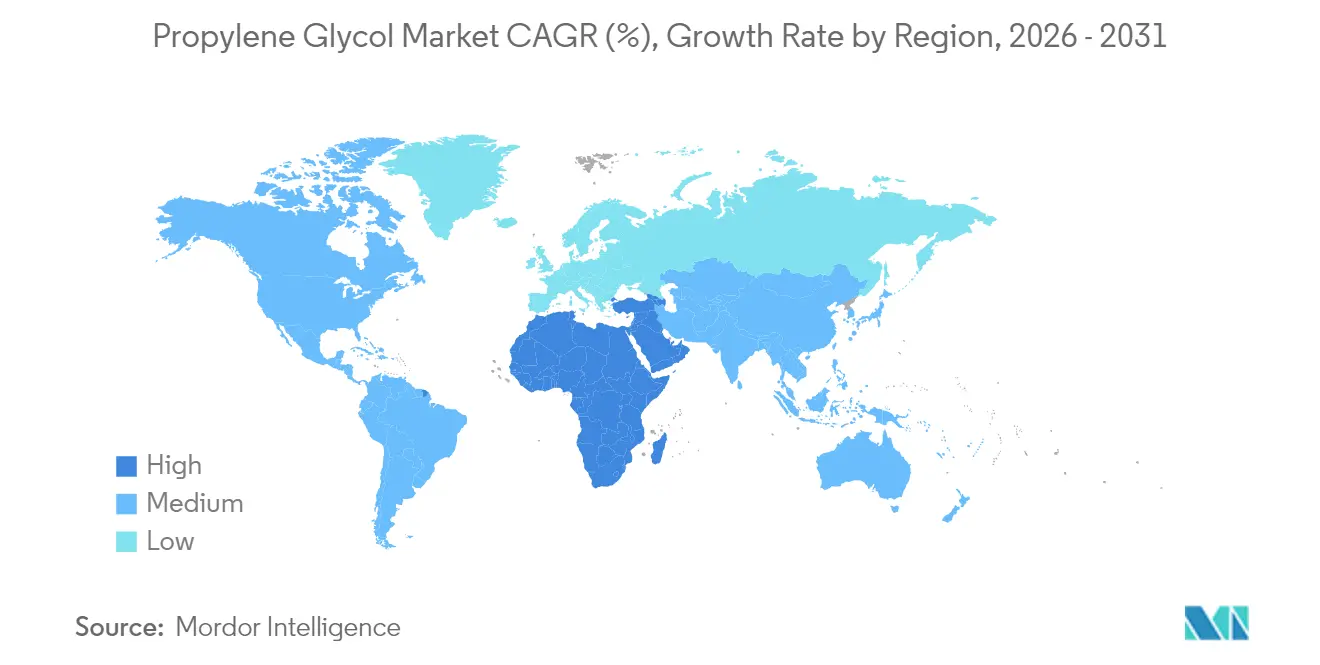

- By geography, the Asia-Pacific region captured 46.11% of the global volume in 2025, while the Middle-East and Africa are expected to register the highest 8.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Propylene Glycol Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from food and beverage formulators | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growing automotive coolant and de-icing fluid consumption | +1.8% | North America, Europe, China, Japan, South Korea | Short term (≤ 2 years) |

| Unsaturated polyester resin growth in composites and construction | +2.1% | Global, led by Asia-Pacific and Europe | Long term (≥ 4 years) |

| Bio-based capacity build-out in Asia | +1.0% | Thailand, China, spill-over to North America | Medium term (2-4 years) |

| Direct propylene-to-PG catalytic routes | +1.5% | Early adopters in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand from Food and Beverage Formulators

Regulatory recognition by the U.S. Food and Drug Administration under 21 CFR 184.1666 and the European Food Safety Authority’s E1520 listing allows formulators to use propylene glycol without labeling hurdles, making it one of the few synthetic humectants accepted in mainstream and value formulations. Beverage-alcohol producers rely on the molecule to carry flavor concentrates and preserve mouthfeel in reduced-sugar products, while bakery manufacturers use it to retain moisture and lengthen shelf life in ambient distribution. The September 2024 addition of new PG derivatives to the Environmental Protection Agency Safer Chemical Ingredients List confirmed regulators’ comfort with PG chemistry, and dairy processors across humid Asian markets now specify PG-based texture modifiers to prevent spoilage. Although premium organic brands still favor glycerin, mass-market products maintain high PG penetration in wet-snack and confectionery lines, resulting in a measurable 1.2 percentage-point lift to overall growth[1]U.S. Food and Drug Administration, “21 CFR 184.1666 Propylene Glycol,” fda.gov.

Growing Automotive Coolant and De-Icing Fluid Consumption

Electric-vehicle battery packs require thermal-management fluids that maintain cell temperatures between 15 °C and 35 °C, a specification that favors propylene glycol over ethylene glycol due to its lower toxicity and excellent low-temperature fluidity. Each battery electric vehicle consumes PG-based coolant during its lifetime, and incremental demand is substantial. Aviation safety norms also underpin growth, as Type I aircraft de-icing formulations depend on PG for freeze-point depression, and worldwide departures are projected to increase annually through 2030. Cold-climate markets in North America and Northern Europe account for a significant share of coolant volumes, but the Asia-Pacific region’s share is rising as national carbon-neutrality mandates in China and South Korea accelerate commercial-fleet electrification[2]International Air Transport Association, “Air Passenger Forecast 2025-2030,” iata.org.

Unsaturated Polyester Resin Growth in Composites and Construction

Wind-energy expansion drives UPR consumption, with each gigawatt of new capacity requiring resin that contains propylene glycol as a reactive diluent. Offshore turbines employ next-generation resins containing PG by weight to achieve salt-spray resistance and longer maintenance intervals. Municipal infrastructure, such as chemical storage tanks and wastewater systems, utilizes PG-extended resins for corrosion resistance at a competitive cost. Meanwhile, governments in India and Southeast Asia specify UPR panels in modular housing programs, targeting a long service life. The construction sector’s uptick and wind-energy buildouts combine to provide a boost to the CAGR.

Bio-Based PG Capacity Build-Out in Asia Accelerates Adoption

Thailand’s Map Ta Phut platform and China’s glycerol-to-PG pilots are bringing commercial-scale bio-routes to market. International Sustainability and Carbon Certification PLUS accreditation enables the mass-balance allocation of used cooking oil and agricultural residue feedstocks, allowing brand owners to record lower Scope 3 emissions without changing their formulations. U.S. soybean-based production exhibits lower greenhouse-gas intensity compared to petroleum-based routes, and similar metrics are attracting European personal-care brands facing 2030 recycled-content mandates. The supply push from new plants and the demand pull from sustainability scorecards contribute another 1 percentage point to growth.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Propylene-oxide price volatility linked to crude swings | −1.3% | Import-dependent Europe, India | Short term (≤ 2 years) |

| Regulatory scrutiny over residual impurities in high-dose uses | −0.6% | North America, Europe | Medium term (2-4 years) |

| Looming oversupply from rapid Chinese capacity additions | −1.8% | Global, price pressure from Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Propylene-Oxide Price Volatility Linked to Crude Swings

Propylene oxide prices can fluctuate significantly within a single year because co-product credits and cracker run rates move in tandem with crude oil prices. When Brent drops beneath a certain threshold, naphtha crackers idle and propylene scarcity lifts PO prices, just as downstream demand weakens. Conversely, crude rallies encourage cracking, flooding the propylene pool, and compressing PO margins. Such instability forces buyers to hold larger inventories and erodes producer visibility.

Regulatory Scrutiny Over Residual Impurities in High-Dose Uses

Injectable pharmaceuticals may deliver gram-level doses of PG per administration, and agencies now mandate tighter limits on diethylene glycol and propylene oxide residues after well-publicized contamination fatalities in 2022. Extra analytical steps add additional costs and extend batch release timelines. Some formulators substitute polyethylene glycol or propylene carbonate, reducing what would have been incremental pharmaceutical demand and impacting growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Composites Anchor Volume, Personal Care Leads Growth

Unsaturated polyester resins accounted for 32.02% of the propylene glycol market size in 2025, as wind-turbine blades and corrosion-resistant infrastructure absorbed large volumes of resin. Vehicle electrification and aviation safety rules demand antifreeze and de-icing agents, while chemical intermediates such as propylene carbonate and dipropylene glycol underpin the production of polyurethane and surfactants. Personal-care intermediates grow at the fastest rate, with an 8.03% CAGR, as esters and ethers penetrate leave-on cosmetics.

More formulators now pay premiums for ISCC PLUS-certified bio-circular grades, especially in the personal care sector, whereas cost-sensitive UPR compounders adopt them only when green-building certifications are required. Semiconductor photoresist strippers rely on propylene glycol monomethyl ether, a niche product that commands a premium price due to its electronics-grade purity. The diversification of demand across specialty and commodity uses enables producers to hedge cyclical exposure; however, success hinges on solvent-purity investments and quick-change logistics for multi-grade portfolios.

By End-User Industry: Pharmaceuticals Outpace Food Despite Smaller Base

Food and beverages retained 28.21% of the propylene glycol market share in 2025, as GRAS and EFSA clearances simplify formulation across beverages, bakery, and confectionery products. Pharmaceuticals, however, are expected to grow at an 8.11% CAGR as drug makers switch from ethylene glycol to meet stricter toxicity thresholds and adopt polyglycol in topical and transdermal systems. Transportation, encompassing automotive, aviation, and marine coolants, trajectory lifted by the growing needs for electric-vehicle battery thermal management.

Building and construction consume a significant portion of PG via UPR composites, and personal-care products secure a notable share through humectants and emollients. Electronics cooling in data centers and agricultural adjuvants provide smaller but rising outlets. Pharmaceutical purity requirements favor large, dedicated facilities that can quickly certify batches, pushing smaller players toward commodity niches unless they retrofit high-purity trains.

Geography Analysis

Asia-Pacific controlled 46.11% of the global propylene glycol market volume in 2025, driven by integrated propane dehydrogenation and PO chains in China, as well as export-oriented plants in Thailand. The Map Ta Phut site in Thailand, which has recently expanded, now ships ISCC PLUS-certified grades to Japan and South Korea. India is set to significantly increase its domestic capacity once Manali Petrochemicals gains operating consent, targeting high-margin food and pharmaceutical users. Yet the region’s near-term margins remain pressured by under-utilized Chinese assets that weigh on spot prices.

The Middle-East and Africa are expected to record the fastest growth rate of 8.66% from 2026 to 2031, driven by Saudi Arabian projects that monetize refinery off-gases into propylene derivatives. Low ethane costs give regional producers an energy advantage that supports exports to Europe and India, although recent feedstock price adjustments have compressed margins.

North America represents a notable portion of demand, primarily driven by the United States’ automotive, pharmaceutical, and beverage sectors. New propylene metathesis capacity at Channelview, Texas, promises feedstock flexibility, while EPA NESHAP rules could force consolidation among smaller players that lack capital for emission controls.

Europe accounts for a significant share of the global volume. The bloc’s carbon-border measures and 2030 recycled-content targets accelerate bio-PG uptake, with ISCC PLUS-certified grades from Germany and Thailand filling premium channels. Electrically heated crackers, pilot-tested in Germany, hint at a future decarbonized propylene; however, their economics depend on carbon prices reaching certain thresholds.

South America holds a smaller share, led by Brazil’s beverage and personal-care manufacturers. Limited local PO assets compel imports, which face duties and restrain growth, even though sugarcane ethanol and biodiesel glycerol present long-term bio-feedstock opportunities.

Mordor Intelligence provides coverage of the propylene glycol market across other key regional markets. Detailed country-level analysis extends to Germany incorporating local coverage and market participation, as required.

Competitive Landscape

The propylene glycol market is moderately consolidated. White-space opportunities include high-purity injectable grades, electronics-grade propylene glycol monomethyl ether for semiconductor fabs, and bio-circular volumes that satisfy European Scope 3 reporting. Technology disruptors aim to cut costs and emissions simultaneously. Process-licensing revenue is emerging as a strategic play for innovators without large balance sheets. Certification has become a competitive moat, and smaller producers lacking audit-ready traceability may seek mergers to gain market access.

Propylene Glycol Industry Leaders

Dow

LyondellBasell Industries Holdings B.V.

BASF

INEOS

ADM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Manali Petrochemicals inaugurated an expansion that lifts propylene glycol capacity by 50,000 tons per year, supporting India’s Make-in-India initiative.

- March 2025: Dow’s Thailand plant earned ISCC PLUS certification and introduced two mass-balance products, Propylene Glycol CIR (recycled) and Propylene Glycol REN (bio-circular), geared toward personal-care, pharmaceutical, and food customers.

Global Propylene Glycol Market Report Scope

Propylene glycol is a viscous, colorless liquid classed as a diol. It is miscible with a broad range of solvents, including water, acetone, and chloroform, and thus finds application across a vast range of industries. Further, polypropylene glycol is a major component in the production of polymers.

The propylene glycol market is segmented by application, end-user industry, and geography. By application, the market is segmented into flavoring agents, antifreeze and deicer agents, unsaturated polyester resins, chemical intermediates, and other applications (antioxidants, household care, etc.). By end-user industry, the market is segmented into transportation, building and construction, food and beverages, personal care, pharmaceuticals, and other end-user industries (electronics, paints and coatings, etc.). The report also covers the market sizes and forecasts for the propylene glycol market in 22 countries across the major regions. For each segment, the market sizing and forecasts have been done based on volume (Tons).

| Flavoring Agent |

| Antifreeze and Deicer Agent |

| Unsaturated Polyester Resins |

| Chemical Intermediates |

| Other Applications (Antioxidants, Household Care, etc.) |

| Transportation |

| Building and Construction |

| Food and Beverages |

| Personal Care |

| Pharmaceuticals |

| Other End-user Industries (Electronics, Paints and Coatings, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Flavoring Agent | |

| Antifreeze and Deicer Agent | ||

| Unsaturated Polyester Resins | ||

| Chemical Intermediates | ||

| Other Applications (Antioxidants, Household Care, etc.) | ||

| By End-user Industry | Transportation | |

| Building and Construction | ||

| Food and Beverages | ||

| Personal Care | ||

| Pharmaceuticals | ||

| Other End-user Industries (Electronics, Paints and Coatings, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big is the propylene glycol market in 2026?

The market is projected to stand at 5.36 million tons in 2026 and is expected to reach 7.76 million tons by 2031.

What is the expected growth rate for propylene glycol through 2031?

Volume is projected to increase at a 7.68% CAGR over the 2026-2031 period.

Which application segment consumes the most propylene glycol?

Unsaturated polyester resins lead, holding 32.02% of demand in 2025, largely from wind-energy and infrastructure composites.

Which end-user industry will grow fastest?

Pharmaceuticals will advance at an 8.11% CAGR as injectable and topical formulations adopt propylene glycol for solubilization.

Which region offers the highest growth potential?

The Middle-East and Africa are expected to lead with an 8.66% CAGR, supported by integrated petrochemical investments in Saudi Arabia and the UAE.

Page last updated on: