Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

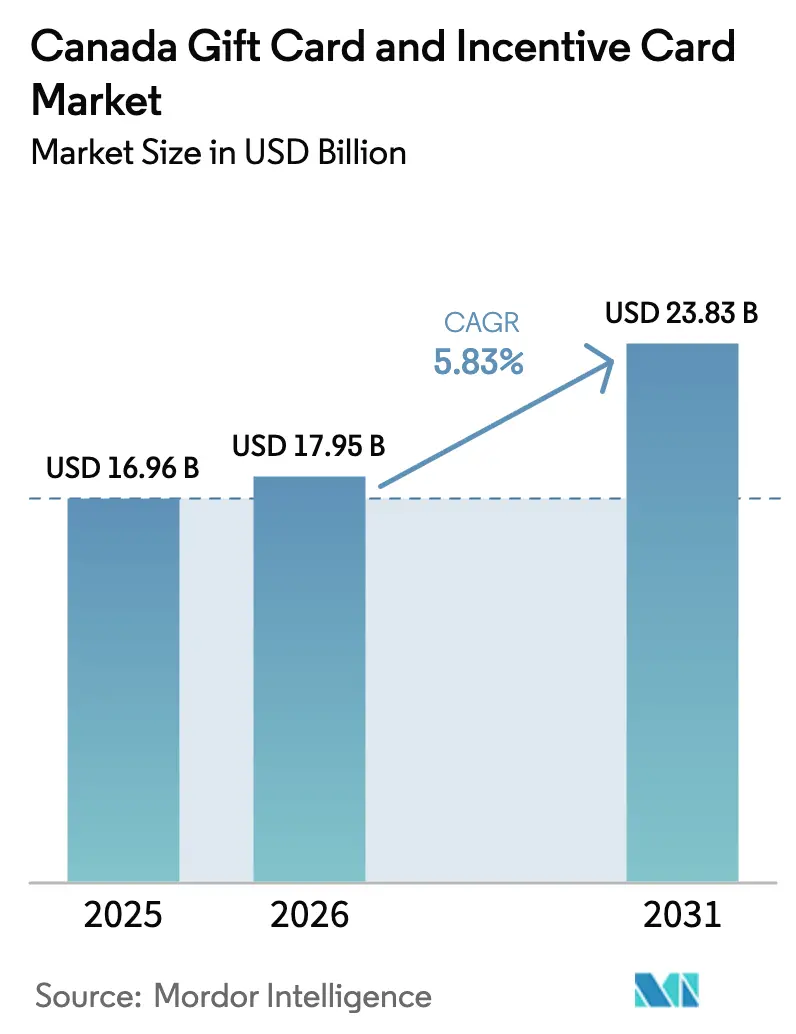

| Base Year Market Size (2025) | USD 16.96 Billion |

| Market Size (2026) | USD 17.95 Billion |

| Market Size (2031) | USD 23.83 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

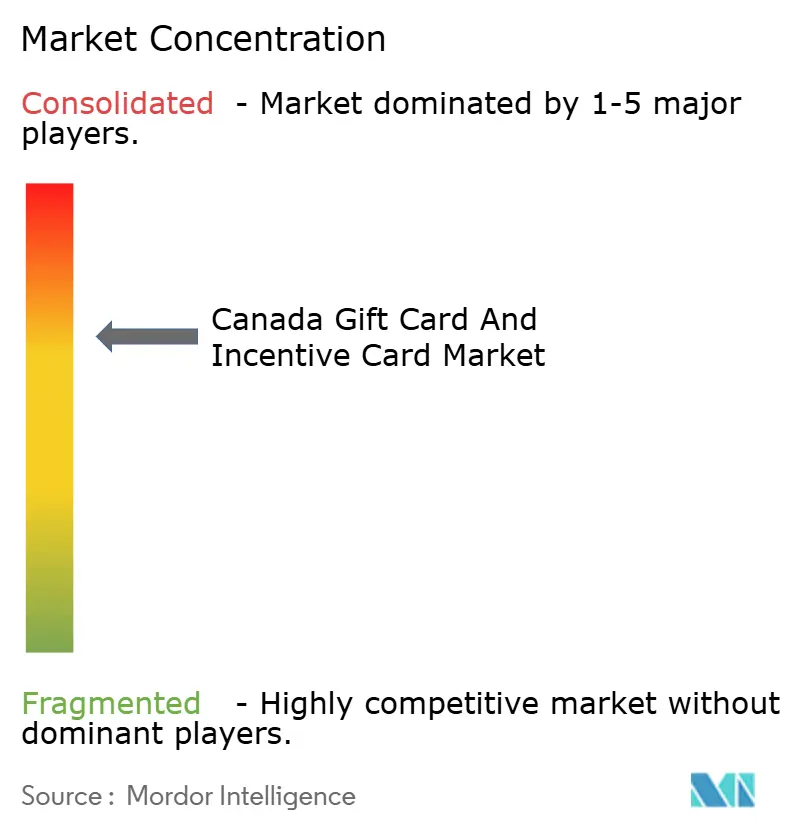

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Gift Card And Incentive Card Market Analysis by Mordor Intelligence

The Canada gift card and incentive card market size in 2026 is estimated at USD 17.95 billion, growing from 2025 value of USD 16.96 billion with 2031 projections showing USD 23.83 billion, growing at 5.83% CAGR over 2026-2031. Rising household e-commerce spending, wider corporate uptake of employee recognition programs, mobile wallet ubiquity, and open-loop prepaid network expansion collectively underpin this steady trajectory [1]Bank of Canada, “Staff Analytical Note 2024-19: The Adoption of Central Bank Digital Currency in Canada,” bankofcanada.ca. . Greater provincial regulatory harmony lowers compliance costs for national issuers while interchange fee caps enacted in 2024 improve merchant margins and stimulate broader acceptance among small retailers. Digitization also reduces physical production costs, propelling e-gift cards to majority status and allowing issuers to reinvest savings in fraud-mitigation technology that preserves consumer trust. Consolidation among processors, such as the pending GTCR–Blackhawk Network transaction, reinforces scale advantages without yet suppressing competitive differentiation, keeping the Canada gift card and incentive card market opportunistic for agile API-driven entrants.

Key Report Takeaways

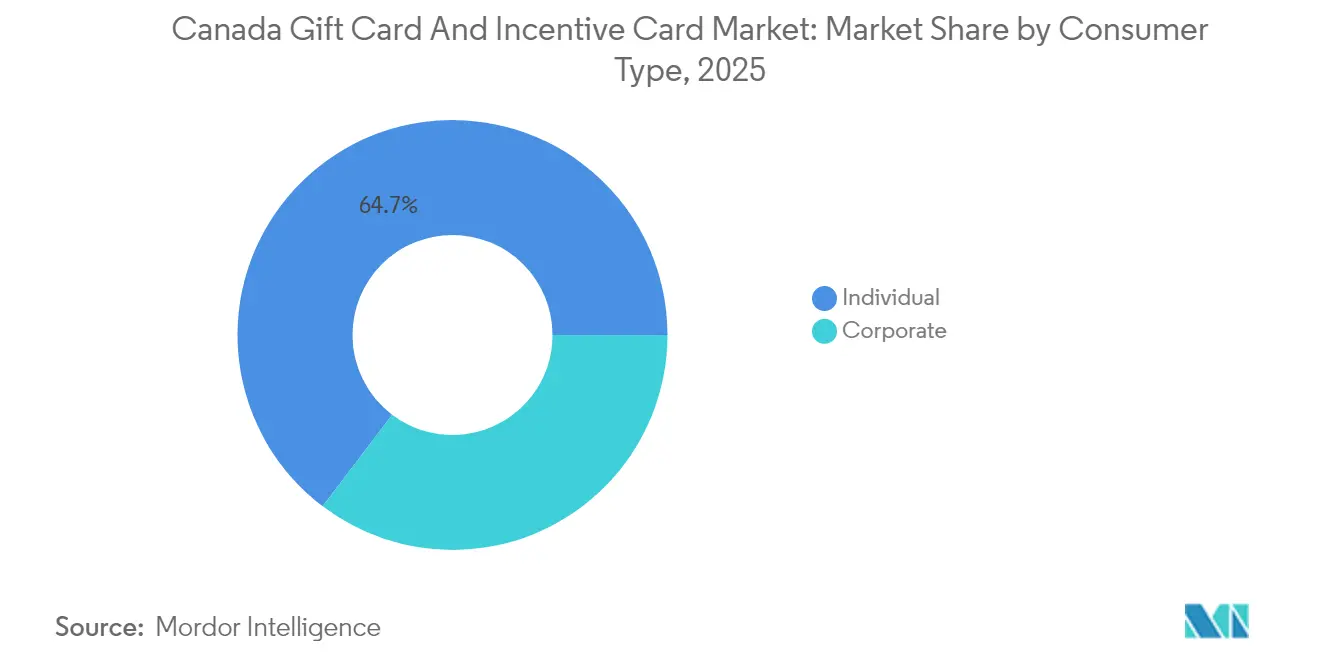

- By consumer type, individual buyers accounted for 64.68% of the Canada gift card and incentive card market share in 2025, whereas small-scale enterprises are projected to register the fastest 14.40% CAGR through 2031.

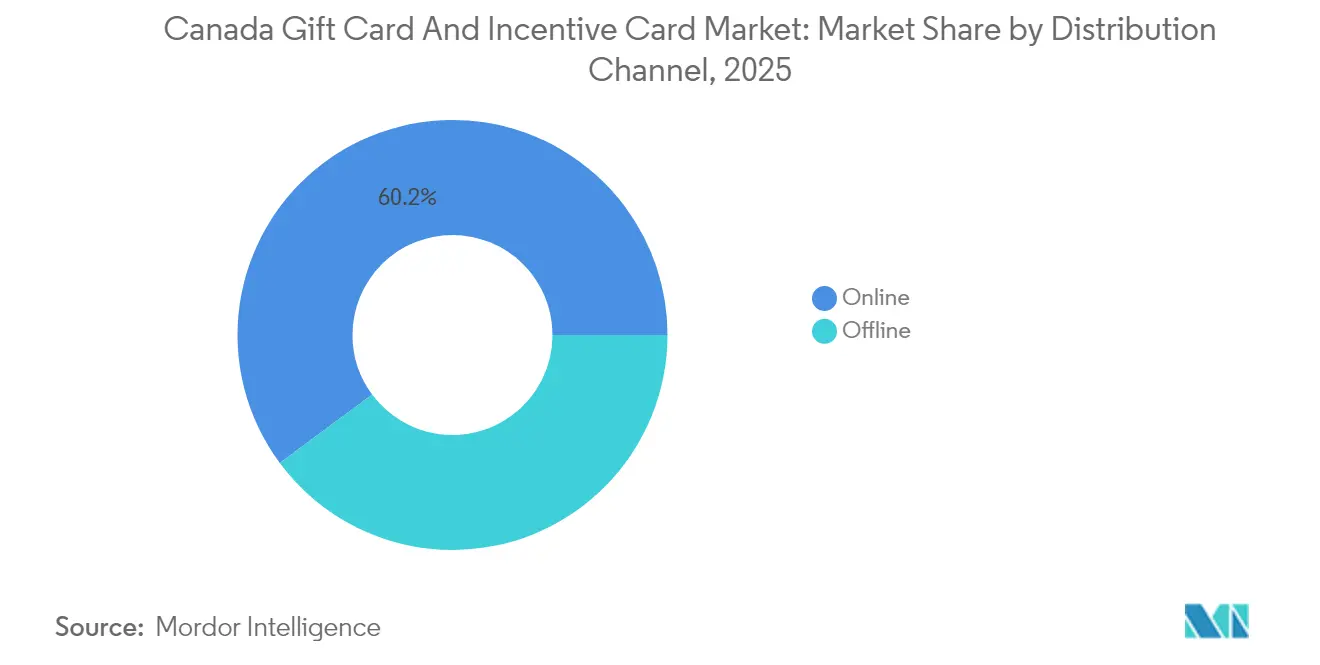

- By distribution channel, online platforms commanded 60.15% share of the Canada gift card and incentive card market size in 2025 and are anticipated to advance at a robust 15.95% CAGR to 2031.

- By product type, e-gift cards captured 61.85% of the Canada gift card and incentive card market share in 2025 and exhibit the highest 16.40% CAGR outlook through 2031.

- By geography, Ontario commanded 41.05% of the Canada gift card and incentive card market share in 2025, while British Columbia is anticipated to advance at a robust 13.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Gift Card And Incentive Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce–driven digital gifting | +1.8% | National, with strongest impact in Ontario, BC | Short term (≤ 2 years) |

| Expansion of corporate rewards & recognition budgets | +1.4% | National, concentrated in major business centers | Medium term (2-4 years) |

| Growing acceptance of mobile wallets for card storage | +1.2% | Urban centers, led by Toronto, Vancouver, Montreal | Short term (≤ 2 years) |

| Mainstream adoption of open-loop prepaid payment networks | +0.9% | National, with rural expansion focus | Long term (≥ 4 years) |

| Multicultural gifting occasions fueled by immigration waves | +1.0% | Urban and suburban areas with high newcomer populations | Medium term (2–4 years) |

| Loyalty-blockchain integrations enabling card interoperability | +0.8% | National, with pilot programs in tech-forward provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce–Driven Digital Gifting

Canada’s online retail sales reached CAD 84.3 billion in 2024, and consumers increasingly turn to instantaneous digital gift options that remove shipping hurdles [2]Statistics Canada, “Retail Trade, December 2024,” statcan.gc.ca. . Holiday peaks illustrate the preference as last-minute shoppers choose email-delivered codes that settle within seconds, preserving gifting intent without logistical risk. Retailers integrate branded e-gift modules into existing storefronts, gaining incremental revenue with marginal tech lift while enlarging customer data pools for targeted promotions. Corporate buyers likewise appreciate API connections that automate bulk issuance, reconcile balances, and monitor redemption behavior in real time. Mobile wallet pass-through further streamlines the journey by embedding codes directly into Apple Pay and Google Pay, cutting two steps from the redemption funnel. Standardized disclosure rules under Ontario and Quebec consumer protection statutes, meanwhile, prevent value-eroding fees, reinforcing public confidence and fueling broader uptake across the Canada gift card and incentive card market.

Expansion of Corporate Rewards & Recognition Budgets

Tight national labor markets spur employers to improve retention levers, and non-cash incentives below CAD 500 per employee enjoy favorable tax treatment, strengthening the appeal of prepaid rewards [3]Department of Finance Canada, “Reducing Credit Card Transaction Fees for Small Businesses,” canada.ca. . Small firms experiencing the fiercest competition for talent gravitate toward digital gift cards because setup is rapid, administrative overhead is minimal, and recipients enjoy merchant flexibility. Mid-sized and large enterprises are integrating incentive engines with HRIS software, personalizing rewards via rule-based triggers tied to performance metrics and thus deepening engagement. Post-pandemic hybrid work norms also necessitate remote-friendly benefits, and digital delivery meets employees wherever they log in. Sustainability targets add another angle: brands now bundle carbon-offset e-gift options, aligning ESG commitments with employee recognition initiatives. Collectively, these forces inject near-double-digit gains into the corporate slice of the Canada gift card and incentive card market.

Growing Acceptance of Mobile Wallets for Card Storage

Contactless payments represented 87% of retail transactions in 2024, reflecting sturdy NFC penetration and consumer comfort with phone-based tap-to-pay. Gift card integration piggybacks on that habit, giving users a single pane to track balances and redeem funds without plastic. Retailers accelerate POS upgrades to read dynamic QR codes and tokenized credentials, shrinking checkout times and lowering queue abandonment. Issuers leverage tokenization to mask underlying card numbers, dramatically curbing account-takeover vulnerabilities that plagued older mag-stripe formats. Biometric gates within smartphones handle authentication duties, limiting fraud exposure for merchants and consumers alike. Provincial privacy statutes such as British Columbia’s PIPA compel transparent data-usage consent, ensuring mobile storage gains do not come at the expense of personal autonomy.

Mainstream Adoption of Open-Loop Prepaid Networks

Visa and Mastercard-branded gift instruments expand spending freedom beyond single-merchant ecosystems, a versatility prized by both G2C disbursement programs and consumer gift recipients. Fee caps introduced in late 2024 shaved 10 basis points off small-merchant interchange, incentivizing even micro-vendors to accept open-loop cards and widening the usable merchant universe. Travelers value the cross-border utility of network-branded cards, and issuers cross-sell travel insurance tie-ins, enlarging ancillary revenue pools. Government agencies pilot open-loop rails for disaster relief payouts, shortening fund-delivery windows compared with mailed checks. These additional use cases expand volume density, delivering scale-economy benefits that ripple across processing, settlement, and card production. As open-loop penetration mounts, the Canada gift card and incentive card market deepens its linkages to the broader payments stack, reinforcing systemic relevance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing fraud & account takeover incidents | -0.8% | National, with higher impact in urban centers | Short term (≤ 2 years) |

| Breakage-related regulatory scrutiny on unused balances | -0.6% | Provincial variations, strongest in Ontario, Quebec | Medium term (2-4 years) |

| Interchange-fee caps squeezing issuer profitability | -0.7% | National, with pronounced effects in regulated markets | Medium term (2–4 years) |

| Heightened consumer data-privacy expectations | -0.5% | National, with stronger enforcement in urban regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Fraud & Account Takeover Incidents

Reported gift-card fraud climbed to USD 54.1 million (CAD 74.1 million) in 2024, with romance-swap schemes and bogus tech-support calls funneling unsuspecting victims toward prepaid codes that criminals launder rapidly. Corporate portals face credential-stuffing waves that siphon balances en masse, prompting CIOs to invest in multi-factor authentication and behavioral analytics. For smaller issuers, these upgrades elevate operating costs and elongate onboarding cycles, counteracting some growth momentum. Provincial consumer-affairs departments now mandate point-of-sale signage warning shoppers against impersonation scams, and noncompliance risks fines that add further burden for retailers. Insurance carriers raise premiums for cybercrime coverage tied to prepaid assets, nudging program managers toward tighter internal controls. Although technology countermeasures gradually blunt attack vectors, the near-term uptick in criminal activity tempers overall CAGR expansion within the Canada gift card and incentive card market.

Breakage-Related Regulatory Scrutiny on Unused Balances

Quebec’s 2024 mandate for five-year minimum expiry periods catalyzed broader provincial moves to rein in breakage income, reducing a historical profit lever for issuers [4]Office de la protection du consommateur, “Gift Cards,” opc.gouv.qc.ca. . Lengthier validity drives higher redemption likelihood, compressing deferred-revenue cushions and nudging providers to seek alternative earnings from interchange or value-added services. Jurisdictional patchwork complicates nationwide program design because Quebec’s French-language disclosure rules and Ontario’s distinct reporting requirements require variant card art, packaging, and accounting treatment. Compliance workloads absorb capital that might otherwise fuel innovation or marketing. Rising consumer awareness campaigns teach cardholders to retrieve dormancy-fee reimbursements, further trimming issuer margins. Collectively, these dynamics subtract modestly from the Canada gift card and incentive card market’s headline growth, even as they enhance end-user protection.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consumer Type: Corporate Budgets Propel Uptake

Corporate demand added meaningful velocity to the Canada gift card and incentive card market in 2025, as small enterprises alone posted a 14.40% CAGR outlook to 2031. Individual consumers still commanda 64.68% share, rooted in traditional birthday, holiday, and celebratory gifting habits that remain culturally ingrained nationwide. Yet tight labor conditions push employers to layer recognition schemes atop base pay, turning prepaid instruments into agile engagement tools that bypass payroll taxes beneath the USD 365 (CAD 500) threshold. Human-resources teams appreciate instant issuance features that slot neatly into existing SaaS workflows, reducing procurement cycles from weeks to minutes. Regional labor standards acts, particularly in Ontario and Quebec, clarify that gift cards do not constitute wages, shielding employers from overtime accrual implications. Remote-work dispersion magnifies appeal because digital codes are delivered uniformly to staff from Vancouver to St. John’s without logistical friction. As macro-economic uncertainty keeps salary increases muted, flexible non-cash rewards expand in strategic importance, and corporate slices should account for a rising proportion of the Canada gift card and incentive card market size by decade’s end.

The corporate cohort also diversifies product design. Environmental, social, and governance committees curate card catalogs that favor carbon-neutral retailers, aligning incentives with corporate citizenship narratives. Data science teams mine redemption patterns to forecast employee sentiment, correlating gift types with attrition risk to inform retention playbooks. Procurement officers negotiate bulk buys that embed variable load amounts, supporting tiered reward ladders within leadership-recognition frameworks. Financial controllers leverage prepaid structures to disburse incidental field-expense allowances, replacing cash floats and improving audit trails. Non-profit organizations tap donated gift cards as charity aid devices that preserve beneficiary dignity by granting choice, further broadening use cases. Such versatility cements corporate participation as a long-term catalyst within the Canada gift card and incentive card market.

By Distribution Channel: Online Momentum Outpaces Storefronts

Digital channels generated 60.15% of the 2025 transaction value and are forecast to surge at a 15.95% CAGR, reflecting consumers’ broader migration to frictionless online purchasing experiences. Pandemic-era behavior changes embedded expectations for instant gratification, and e-gift portals now embed one-click buy flows fully optimized for mobile screens. Multichannel retailers integrate card-buy widgets into checkout pages, converting gift purchases that historically diverted to physical kiosks. Application-programming-interface frameworks enable third-party marketplaces and employer portals to embed issuance directly, expanding reach without incremental app downloads. Fraud-screening vendors integrate velocity checks and machine-learning agents that score transactions in milliseconds, preserving conversion rates while curbing chargebacks. Consequently, online provisioning stands as the growth locomotive for the Canada gift card and incentive card market.

Brick-and-mortar outlets are not obsolete; they still appeal to spontaneous buyers and demographics less comfortable with purely digital value. Grocery chains position high-margin prepaid racks near checkouts where dwell time prompts impulse purchases, and QR-equipped hangtags now let shoppers instantly load values into mobile wallets, bridging analog and digital universes. Gas stations and convenience stores function as last-mile cash-conversion hubs where under-banked consumers trade currency for open-loop cards usable online, highlighting inclusion benefits. Retailers increasingly adopt tablet-based kiosk screens that allow self-service selection of multiple brands in a single location, refreshing the physical aisle experience. These hybrid innovations slow share erosion even as pureplay online channels sprint ahead, ensuring distribution diversification inside the Canada gift card and incentive card market.

By Product Type: E-Gift Cards Capture Majority Preference

E-gift cards already constituted 61.85% of market value in 2025 and are projected to grow at a 16.40% CAGR, their appeal anchored in instant delivery, inventory-free economics, and mobile-first lifestyles. Issuers capitalize on cost savings by eliminating plastic manufacture and postage, redirecting budgets toward personalization engines that embed recipient names, event-specific artwork, and video greetings. Integration into iOS and Android wallet passes minimizes orphan balances by serving low-balance push reminders, lifting redemption rates, and curtailing regulatory breakage risk. Restaurants equip POS systems to scan phone-displayed barcodes, shaving order-line seconds that translate into appreciable throughput gains during peak shifts. Environmental considerations also resonate; ESG-conscious consumers favor zero-plastic options that shrink carbon footprints. These cumulative factors place e-gift solutions at the forefront of the Canada gift card and incentive card market.

Physical cards, while shrinking in share, still serve ceremonial gifting rituals and enable tangible unwrapping moments prized during cultural festivals. Retailers experiment with biodegradable card stock and soy-ink printing to address sustainability critiques without sacrificing tactile value. Hybrid “phygital” products package a scannable code within a slim envelope, giving purchasers the satisfaction of handing over a present while ultimately delivering value into the recipient’s mobile wallet. Collectors cherish limited-edition designs linked to pop-culture franchises, a merchandising tactic that moves units well beyond face value and illustrates ongoing potential. Corporate buyers sometimes prefer physical deliveries for high-stakes recognition ceremonies where handing over a branded card reinforces achievement symbolism. Hence, diversity in form factors ensures broad audience coverage, sustaining overall resilience for the Canada gift card and incentive card market.

Geography Analysis

Ontario commanded 41.05% of the 2025 value, underpinned by its population scale, headquarters density, and sophisticated retail infrastructure that eases omnichannel redemption. The Greater Toronto Area especially benefits from fintech clustering, fostering pilot collaborations between issuers and tech startups that iterate APIs quickly. Provincial consumer-protection rules require clear expiry disclosures and ban inactivity fees, elevating transparency standards that ripple nationwide. Small-merchant interchange relief introduced in October 2024 further widened acceptance footprints among independent retailers. Cultural multiplicity fuels year-round gifting diversity, with Diwali, Lunar New Year, and Eid seasons layering incremental demand atop Christmas and Mother’s Day peaks. These dynamics entrench Ontario as the cornerstone of the Canada gift card and incentive card market.

Quebec followed in market share and recorded solid mid-single-digit growth despite linguistic and regulatory uniqueness. French-language packaging and marketing collateral are mandatory, compelling issuers to allocate dedicated compliance resources but also fostering localized creative campaigns that resonate with Quebecois audiences. Montréal’s tech scene nurtures digital-only challengers that cater to millennial and Gen-Z users by embedding gift functionality inside social-commerce feeds. Retailers integrate “cartes-cadeaux” modules within transactional emails, ensuring bilingual parity across touchpoints. Provincial enforcement of a five-year minimum validity dampens breakage reliance, pushing providers toward value-added subscription models that upsell greeting-card templates and personalization bundles. Collectively, these factors shape a distinct but lucrative segment of the Canada gift card and incentive card market.

British Columbia outpaces national averages with a 13.60% CAGR thanks to technology-sector growth and hospitality rebound in Vancouver, Whistler, and Victoria. High environmental awareness drives disproportionate demand for digital-only instruments, and retailers proudly advertise paperless gifting to eco-minded patrons. Provincial privacy legislation places stringent consent controls on data collection, influencing app UX designs that foreground permission toggles and data-usage dashboards. Cross-border tourism from U.S. Pacific Northwest visitors increases interest in open-loop cards convertible to U.S. dollars at competitive FX rates. Urban multiculturalism stimulates niche gift programs timed to Lunar New Year, Persian Nowruz, and Filipino Christmas traditions, boosting seasonal revenue spikes. These attributes cement British Columbia’s prominence within the broader Canada gift card and incentive card market.

Competitive Landscape

The top five issuers, Blackhawk Network, InComm Payments, Giftogram, EML Payments, and Givex, dominate the market, reflecting a moderately concentrated landscape. This structure offers large players the advantage of scale while still leaving room for innovation and disruption by emerging challengers. Blackhawk’s pending USD 4.44 billion take-private deal by GTCR will supply capital for platform modernization, potentially enabling deeper machine-learning personalization engines and international currency support. InComm doubles down on point-of-sale activation hardware that simplifies multi-brand racks for retailers, a tactic that keeps physical channels sticky even as digital ascends. Givex, freshly absorbed by Shift4 Payments, pivots to hospitality integrations that merge restaurant loyalty, gift, and stored-value tools under one dashboard. Smaller fintechs such as Nuvei and Paymi exploit open-banking APIs to bundle instant-rebate gift cards into shopping-cart journeys, providing agile go-to-market wedges.

Product innovation stands as the noisy battleground. Blockchain-secured prepaid tokens promise tradeable, brand-agnostic value and secondary-market liquidity, a concept EML trials through pilot merchants in Alberta’s ski-resort corridor. Mastercard’s Touch Card tactile markings extend inclusive design to the visually impaired, ensuring accessibility compliance while generating positive CSR narratives. Fraud analytics vendors, including Featurespace, integrate adaptive modeling engines into issuer stacks, differentiating on risk-score accuracy and false-positive reduction. ESG alignment emerges as another lever; providers curate catalog sections spotlighting sustainably certified merchants, winning enterprise contracts that tie procurement to climate goals. This mosaic of technology, partnerships, and purpose delineates competitive vectors shaping the Canada gift card and incentive card market.

Regulatory sophistication produces both a hurdle and a moat. FINTRAC anti-money-laundering directives demand robust customer due diligence processes, favoring incumbents with established compliance teams while raising barriers for entrants. Yet savvy newcomers offer compliance-as-a-service overlays, monetizing the burden itself and smoothing entry for niche brand-specific issuers. Data-sovereignty rules compel domestic hosting, and cloud providers jockey for PCI-compliant regional data centers to capture workloads. The market thus displays dynamic equilibrium: concentration sufficient for economies of scale yet porous enough to admit specialists that address unmet vertical or technical needs. The outcome is a competitive tapestry that keeps the Canada gift card and incentive card market both innovative and relatively balanced.

Canada Gift Card And Incentive Card Industry Leaders

Blackhawk Network

InComm Payments

Paystone

Buyatab

Neo Financial (Gift Card Mall)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Walmart Canada enhanced its Walmart Rewards Mastercard program with expanded gift card earning categories and digital wallet integration, targeting increased customer engagement and transaction frequency across its retail network.

- July 2025: GTCR entered advanced negotiations to acquire Blackhawk Network for approximately CAD 6.08 billion (USD 4.5 billion), representing the largest gift card industry transaction in Canadian market history and signaling institutional confidence in long-term growth prospects.

- July 2025: InComm Payments partnered with NCR Atleos to launch cardless cash withdrawal services at Canadian ATMs, enabling gift card balance conversion to cash through mobile app integration and expanding redemption flexibility for consumers.

- May 2025: Mastercard launched its Touch Card accessibility initiative in Canada, introducing tactile features for visually impaired users and demonstrating a commitment to inclusive payment design that extends to gift card applications.

Canada Gift Card And Incentive Card Market Report Scope

A gift card is a prepaid debit card with a predetermined amount of money on it that may be used for a range of purchases. A loyalty, prize, incentive, or promotional card that is funded by a business and not available for purchase by the general public is referred to as an incentive card. This report aims to provide a detailed analysis of the Canada Gift Card and Incentive Card Market. It focuses on the market dynamics, emerging trends in the segments, the future of markets, and insights into various drivers and restraints. Also, it analyses the key players and the competitive landscape in the market. The Canada Gift Card and Incentive Card Market are segmented based on Card Type (E-Gift card, Physical card), Consumer Type (Retail Consumer, Corporate Consumer), and Distribution Channel (Online, Offline). The report offers market size and forecasts for Canada Gift Card and Incentive Market in value (USD Million) for all the above segments.

By Consumer Type

| Individual | |

| Corporate | Small-scale Enterprise |

| Mid-tier Enterprise | |

| Large Enterprise |

By Distribution Channel

| Online |

| Offline |

By Product Type

| E-gift Card |

| Physical Card |

By Geography

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Other Territories |

| By Consumer Type | Individual | |

| Corporate | Small-scale Enterprise | |

| Mid-tier Enterprise | ||

| Large Enterprise | ||

| By Distribution Channel | Online | |

| Offline | ||

| By Product Type | E-gift Card | |

| Physical Card | ||

| By Geography | Ontario | |

| Quebec | ||

| British Columbia | ||

| Alberta | ||

| Other Territories | ||

Key Questions Answered in the Report

How large is the Canada gift card and incentive card market in 2026?

The Canada gift card and incentive card market size stands at CAD 17.95 billion (USD 17.95 billion) in 2026 and is projected to climb to CAD 23.83 billion (USD 23.83 billion) by 2031.

Which consumer segment is expanding fastest within Canada’s prepaid landscape?

Small-scale enterprises drive the quickest gains, forecast to grow at 14.40% CAGR through 2031 as employers leverage gift cards for tax-efficient employee rewards.

What share do online channels hold in Canadian gift card sales?

Online platforms account for 60.15% of transaction value and are advancing at a 15.95% CAGR owing to mobile-first purchasing and instant delivery expectations.

Why are e-gift cards preferred over physical cards in Canada?

E-gift cards offer instant delivery, seamless mobile wallet storage, lower production costs, and align with environmental priorities that resonate strongly with Canadian consumers.

How is regulation affecting breakage income for issuers?

Provinces such as Quebec mandate five-year expiry minimums, lowering unredeemed-balance revenue and compelling issuers to shift toward interchange and value-added service income streams.

Which provinces dominate Canada’s prepaid card market?

Ontario leads with 41.05% share, followed by Quebec at 24.30%, while British Columbia shows the fastest growth, supported by technology adoption and strong tourism recovery.

Page last updated on: