Market Overview

| Study Period | 2020 - 2031 |

|---|---|

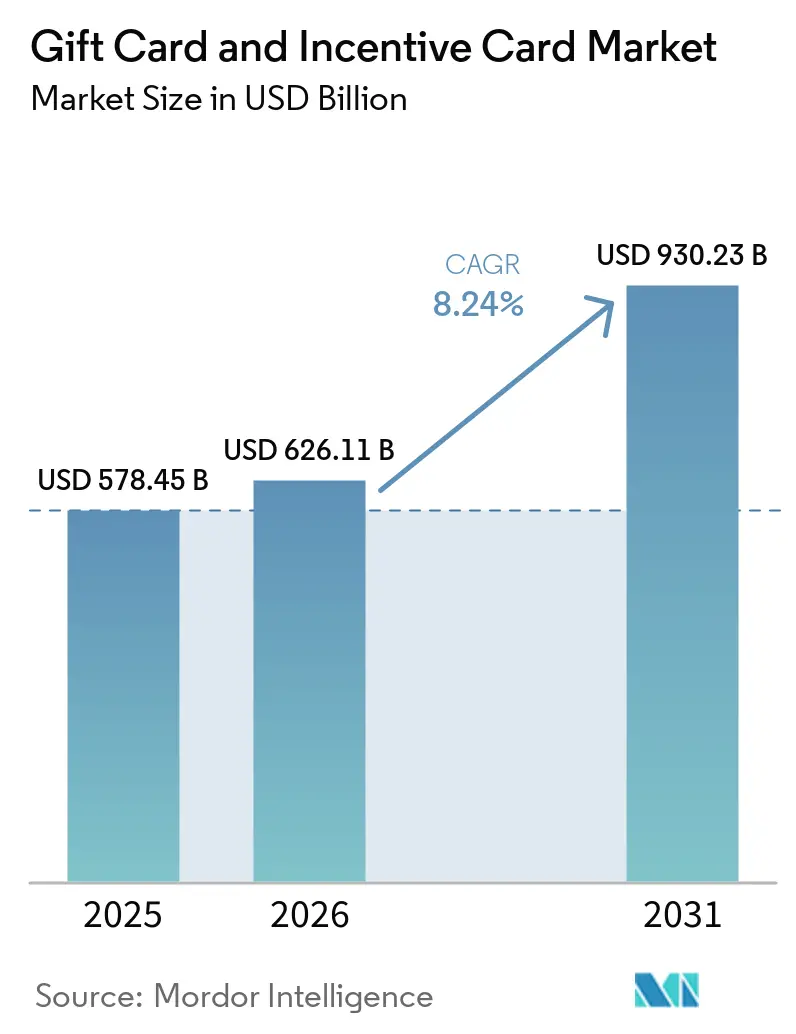

| Market Size (2026) | USD 626.11 Billion |

| Market Size (2031) | USD 930.23 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

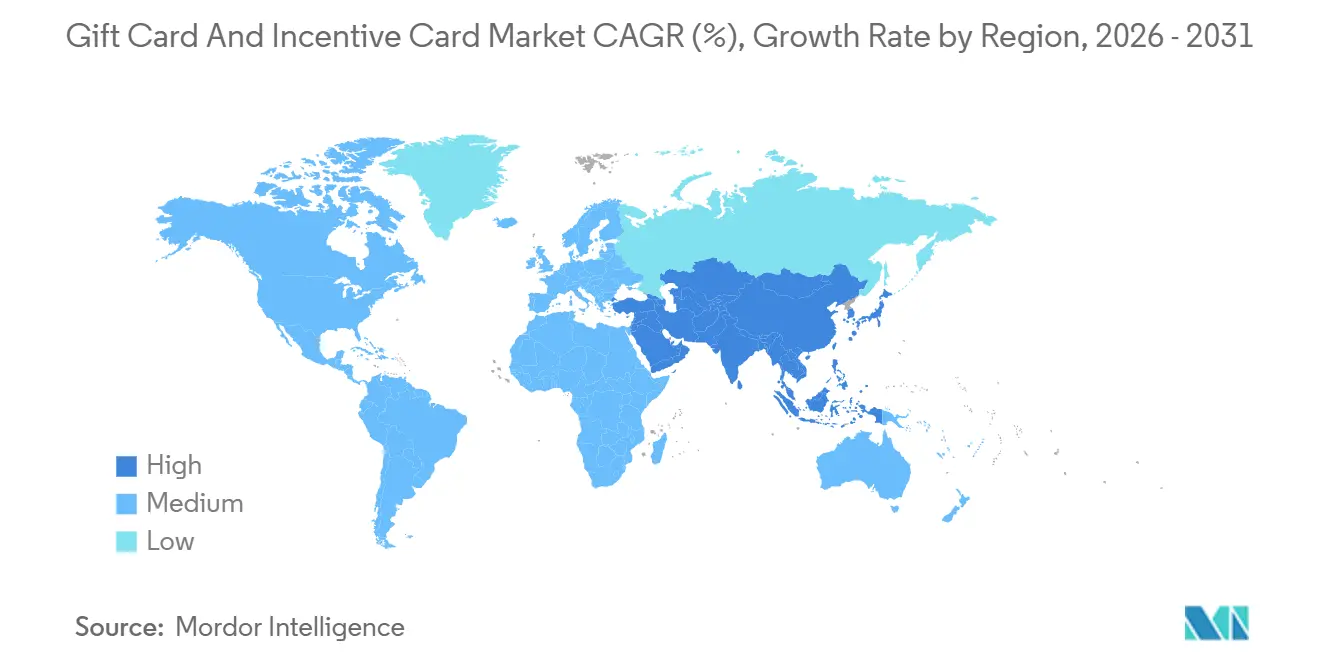

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gift Card and Incentive Card Market Analysis by Mordor Intelligence

The Gift Card And Incentive Card Market size is projected to expand from USD 578.45 billion in 2025 and USD 626.11 billion in 2026 to USD 930.23 billion by 2031, registering a CAGR of 8.24% between 2026 to 2031.

Growth is supported by e-commerce platforms elevating digital gifting into core checkout flows, and corporate procurement shifting bonuses and rewards to prepaid instruments that are simple to distribute and easy to account for. Open-loop networks strengthen real-time authorization and tokenization, which improves security while reducing pre-funding friction for issuers and distributors. Digital formats benefit from wallet integration that reduces redemption delays as balances sit alongside payments and loyalty credentials. Regional momentum is uneven as North America sustains a large installed base while Asia-Pacific records faster expansion on the back of wallet ubiquity and interoperable payment rails[1]Source: Marie-Hélène Felt, Angelika Welte, and Anna Chernesky, “2024 Methods-of-Payment Survey Report: Cash in an Era of Alternatives,” Bank of Canada, bankofcanada.ca.

Key Report Takeaways

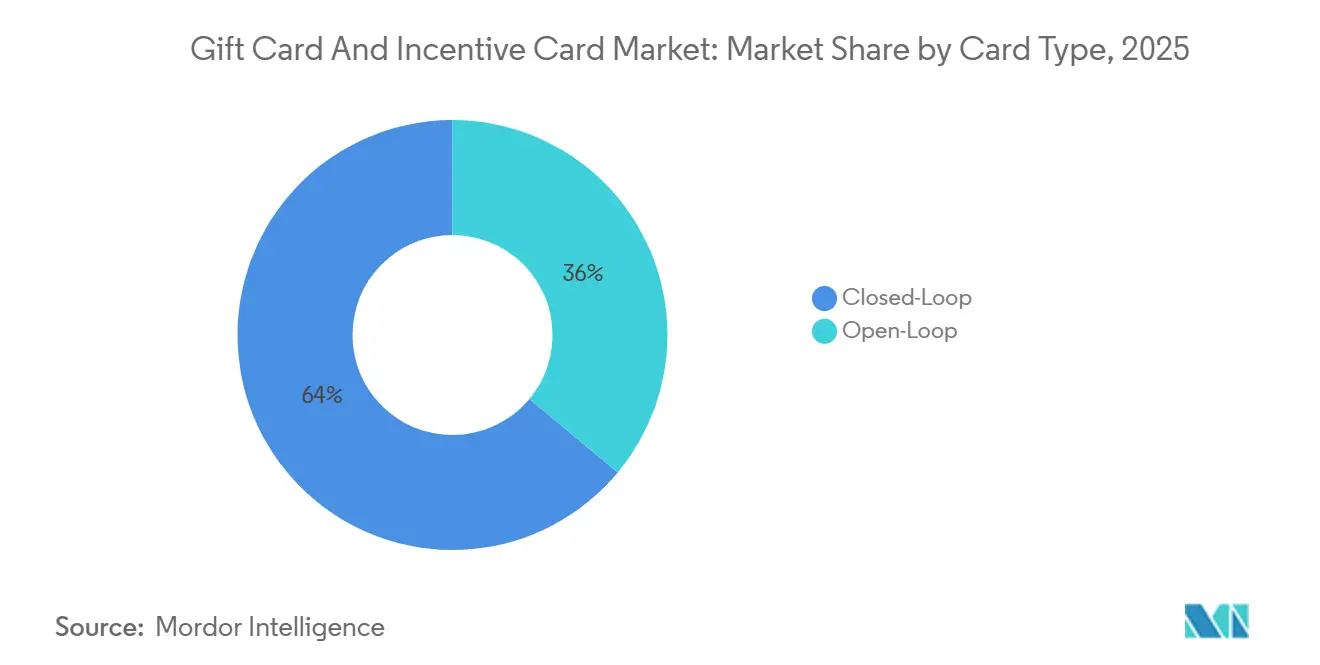

- By card type, closed-loop held 63.96% share in 2025, while open-loop is forecast to grow at 9.77% CAGR through 2031.

- By format type, physical cards held a 56.61% share in 2025, while digital is forecast to rise at a 13.45% CAGR to 2031.

- By consumer type, the individual segment held a 70.55% share in 2025, while the corporate segment is projected to advance at a 10.09% CAGR through 2031.

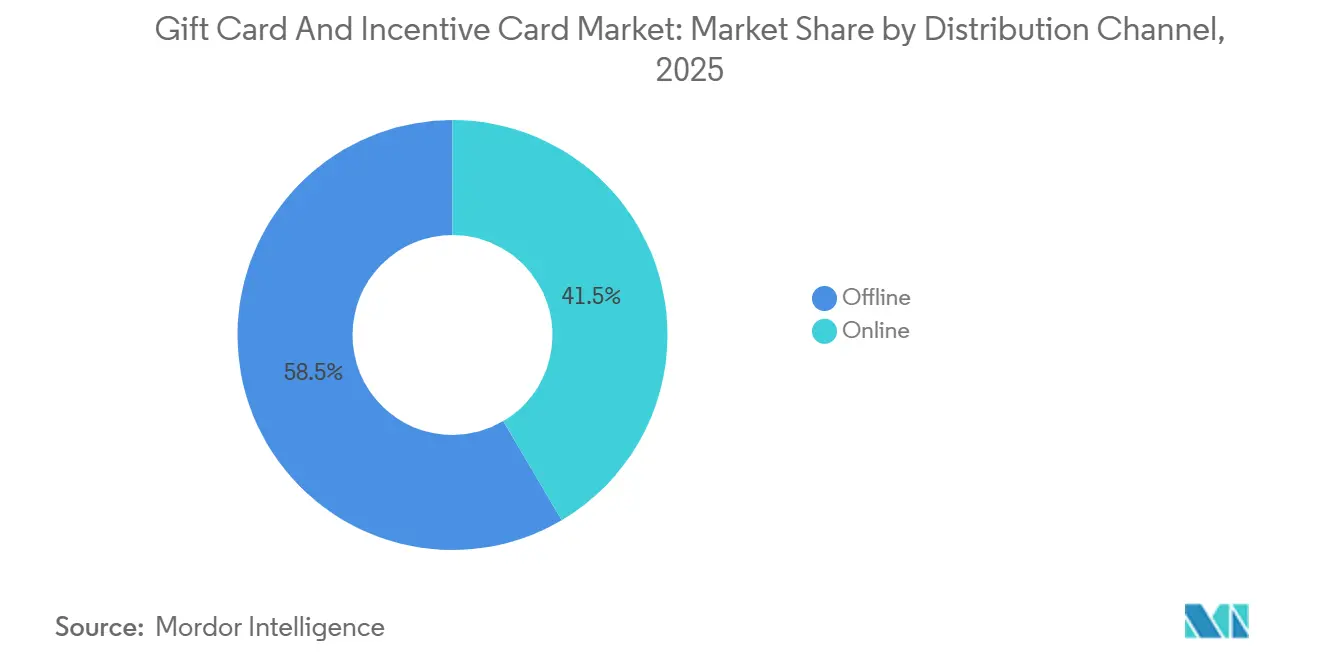

- By distribution channel, offline held 58.49% share in 2025, while online is expected to grow at a 12.69% CAGR through 2031.

- By industry of application, food and beverages accounted for a 28.12% share in 2025, while consumer electronics is set to expand at an 11.02% CAGR through 2031.

- By geography, North America held a 40.06% share in 2025, while Asia-Pacific is projected to grow at a 10.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gift Card and Incentive Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| The e-commerce boom is accelerating digital gift-card adoption | +2.1% | Global, with Asia-Pacific core spillover to Middle East and Africa | Medium term (2-4 years) |

| Rise of corporate loyalty & incentive programs | +1.8% | North America & Europe, expanding to South America | Medium term (2-4 years) |

| Cashless payment ecosystems & digital wallets proliferation | +2.3% | Asia-Pacific dominance, North America adoption acceleration | Short term (≤ 2 years) |

| AI-driven personalization improving breakage economics | +0.9% | North America, early Europe deployment | Long term (≥ 4 years) |

| Sustainability push favouring dematerialised gift cards | +0.7% | Europe regulatory-led, North America brand-driven | Medium term (2-4 years) |

| Blockchain-secured, cross-border gift-card platforms | +0.5% | Global pilot phase, Middle East and Africa remittance corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Boom Accelerating Digital Gift-Card Adoption

Online retail captured 27% of U.S. holiday purchases in the 2025 season, climbing 7.8% year-over-year, as consumers leveraged early promotions and mobile-first checkout flows that embed gift-card funding directly into cart workflows[2]. Digital gift cards now command over 50% of total unit sales globally, reversing the dominance of physical formats for the first time, with Millennials showing 70% preference for instant-delivery e-gifts that bypass postal latency[3]WUPEX, “Why Digital Gift Cards Market Is Going Digital in 2025-2026: Expert Insights & Future Trends,” WUPEX, www.paymentsdive.com. The presence of gift balances within wallets further shortens time-to-first redemption as consumers no longer need to keep or handle physical cards. Online payment studies also show broad wallet linking by cardholders, a shift that helps new digital gift issuers meet consumers at their preferred payment method during peak seasons.

Rise of Corporate Loyalty & Incentive Programs

Corporate gift-card allocations account for 30% of program budgets in North America and 34% in Europe, with 70% of North American firms anticipating moderate-to-significant increases in 2026 usage as enterprises shift from cash bonuses to prepaid instruments that avoid payroll-tax triggers and deliver instant digital deployment[4]Incentive Research Foundation, “Industry Outlook for 2026: Merchandise, Gift Cards, and Event Gifting,” Incentive Research Foundation, theirf.org. The average North American B2B gift-card denomination climbed to USD 193 in 2025, up from USD 142 the prior year, as channel incentive programs targeting sales teams favor higher-value cards to reward quarterly quotas. API-first platforms plug into HR and CRM systems to trigger reward issuance automatically upon defined milestones, which cuts manual processing and speeds delivery at scale. Consolidation activity in 2024 also strengthened API catalogs and enterprise reach, improving coverage across brands and payout options for corporate-led programs.

Cashless-Payment Ecosystems & Digital Wallets Proliferation

Digital wallets continue to absorb more consumer payment volume and functionality, including storage of gift balances and loyalty points. Global wallet user counts and transaction trajectories indicate sustained growth through the forecast horizon, which expands the addressable surface for instant digital issuance and tap-to-redeem use cases. In North America, more cardholders link debit and credit to mobile wallets, and mobile payments increase their point-of-sale share, a pattern aligned with higher acceptance and familiarity in everyday transactions. In India, ecosystem players introduced intelligent gift-card platforms that allow configuration by customer or product, shrinking deployment times for tailored programs and aligning value to user behavior in real time. Wallet coverage across online and in-store touchpoints supports omnichannel gift redemption, which reduces checkout abandonment when issuers support preferred methods.

AI-Driven Personalization Improving Breakage Economics

Issuers and aggregators apply AI to pattern seasonal demand and recommend denomination, design, and timing that lift engagement. One platform rolled out natural-language agents to let brand managers query holiday patterns and transaction cohorts, producing short-horizon forecasts that update as seasons approach. Restaurants and retailers connect gift themes and offers to purchase histories, which lifts campaign revenue compared with static creative and supports higher conversion from message to redemption. AI-based personalization also improves targeting of top categories at the moment of gifting, which strengthens the perceived fit between card and recipient. As programs reduce irrelevant offers, they encourage first use and reload, which decreases dormant balances and improves unit economics over time. Digital channels compound these effects because delivery and redemption occur in the same session, removing many legacy frictions for first-time gifters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating gift-card fraud & cybercrime | -1.4% | Global, acute in North America | Short term (≤ 2 years) |

| Divergent global fee/expiry regulations | -0.9% | Europe harmonization vs. United States' state patchwork | Medium term (2-4 years) |

| Rising open-loop activation & interchange fees for SMEs | -0.7% | North America, Europe-regulated markets | Medium term (2-4 years) |

| Tariff-driven cost spikes in plastic card supply chains | -0.6% | Global, concentrated in the United States-China corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Gift-Card Fraud & Cyber-Crime

Total reported fraud losses grew strongly in 2024, and gift cards remain a common vector for scammers where the payment method is specified. The Federal Trade Commission data shows increased losses and a large share of impostor-scam activity, which places pressure on issuers and retailers to enhance consumer education and in-store controls. Platforms deploy advanced threat intelligence and apply AI to detect anomalies, while tokenization replaces sensitive data across a growing share of transactions. Technology vendors also highlight the mechanics of account takeover and code harvesting, recommending secure packaging and monitoring to reduce draining schemes. New rules coming into effect in 2026 mandate reasonable procedures for fraud prevention at retail, which will further institutionalize best practices for staff training and point-of-sale safeguards. These measures converge with online security standards to strengthen the consumer protection baseline across channels.

Rising Open-Loop Activation & Interchange Fees for SMEs

Small and midsize businesses face higher relative costs when deploying open-loop instruments due to activation fees and interchange on card-not-present transactions. These economics can favor closed-loop alternatives where merchants avoid network tolls and keep funds within their ecosystems. Compliance obligations for data security add to the cost burden for smaller programs, which makes partner selection and scope control important for sustaining margins. Merchants also weigh card-present flows that benefit from lower rates against online gifting that dominates convenience-driven sales. As issuers and acquirers refine small merchant programs, economics may improve, but near-term pressure remains a practical restraint for open-loop uptake among SMEs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Card Type: Open-Loop Variants Outpace Closed-Loop Incumbents on Network Interoperability

Closed-loop cards held 63.96% in 2025, while open-loop options are projected to grow faster at 9.77% CAGR through 2031 as acceptance breadth attracts corporate and cross-merchant use. The largest retailers continue to prefer closed-loop cards to retain margin and data visibility, but open-loop networks widen coverage through partnerships and real-time authorization improvements that reduce funding delays. Network acceptance growth among major card brands increases the utility of open-loop prepaid gift cards in domestic and cross-border contexts, lifting buyer confidence in universal redemption. An API that supports on-demand issuance and loading enables program managers to align card types to use cases, from highly targeted offers in closed ecosystems to general-purpose rewards that spend anywhere. This flexibility sustains a bifurcated structure in the gift card and incentive cards market as large retailers continue to lean on proprietary programs while enterprise buyers diversify into open-loop for broad acceptance.

Open-loop programs also benefit from security advances such as tokenization and risk-scoring tools at authorization, which reduce false positives and fraud risk on prepaid flows. On the closed-loop side, network exclusions lessen regulatory overhead and give issuers freedom to design product features that reinforce loyalty, app adoption, and reload behaviors. Aggregators support both models by adding packaging safeguards and encryption for activation flows that mitigate card-draining schemes at retail as more brands layer QR codes and wallets into issuance, open-loop and closed-loop formats converge on instant digital experiences that replace plastic as the default. The net effect is a gradual expansion of open-loop share, though closed-loop scale remains resilient where mobile ordering, loyalty integrations, and breakage economics favor proprietary ecosystems.

By Format Type: Digital Delivery Eclipses Physical Cards via Mobile-Wallet Integration

Physical cards held a 56.61% share in 2025, and digital formats are projected to grow at a 13.45% CAGR as issuance, delivery, and redemption consolidate in mobile workflows. Digital balances accessed through wallets eliminate the need to handle plastic, which accelerates first-use timing and reduces the chance of loss or damage. Top digital programs now integrate personalization features from SMS delivery to scheduled gifting and video messages, which expand engagement beyond holidays into everyday occasions. Retailers and restaurants that moved to digital gifts report significant reductions in single-use plastic, aligning with sustainability commitments and packaging regulations that favor dematerialization. Wallet ubiquity also lowers friction at the physical point of sale because balances are ready for tap-to-pay alongside cards and loyalty IDs.

Physical cards maintain relevance when presentation matters, such as corporate events or occasions where a tangible token adds perceived value. Merchants mitigate fraud risks on physical units with secure packaging and clearer tamper indicators while adding QR-based activation that links to immediate digital use. Hybrid formats that blend greeting cards with scannable codes bridge sentiment and instant redemption, widening appeal to senders preferring a physical artifact with digital convenience. As environmental standards tighten and network targets phase out first-use PVC, dematerialized formats gain a structural cost and compliance advantage. This creates room for faster innovation cycles in the gift card and incentive cards market as issuers iterate digital features without retooling physical supply chains.

By Consumer Type: Corporate B2B Surges as Enterprises Tokenize Incentives

Individuals held 70.55% in 2025 on the strength of holiday and occasion gifting, and corporate programs are projected to grow at a 10.09% CAGR as enterprises shift bonuses, sales incentives, and recognition to prepaid instruments. Budget outlooks for 2026 show broad plans to increase usage as gift cards streamline disbursement and reporting, which supports larger average denominations in B2B orders. Pay-over-time options for bulk digital orders address procurement cash cycles during peak gifting periods, making it easier for HR and sales operations to execute large campaigns. API distribution via HR and CRM systems automates delivery tied to performance events, which compresses lead times from days to seconds and scales globally with localized catalogs. As corporate deployments mature, analytics on redemption patterns support better category targeting and supplier negotiation in the gift card and incentive cards industry.

Individual buyers continue to prize flexibility, with digital cards improving speed from purchase to first redemption. Corporate program managers prioritize the availability of cross-border catalogs, tax-compliant reporting, and wallet compatibility to fit both hybrid and remote workforces. Aggregators deepen enterprise value by offering large brand networks, fraud screening, and audit trails that satisfy internal control requirements. Program complexity rises with geography, so partners that address data protection and payment compliance across regions strengthen their position with multinational buyers. These dynamics keep the gift card and incentive cards market balanced between high-frequency B2C use and faster-growing B2B adoption.

By Distribution Channel: Online Platforms Overtake Brick-and-Mortar via Frictionless Checkout

Offline held 58.49% in 2025 through grocery, pharmacy, and big-box displays, and online is projected to grow at a 12.69% CAGR as one-click checkout and wallet storage reduce friction. Dedicated digital storefronts now offer large brand catalogs with scheduling, personalization, and installment options that simplify both consumer and corporate purchases. Restaurants, hotels, and retailers with POS integrations activate and redeem cards within existing terminals, which unifies in-store and online acceptance and improves reporting. Online channels also benefit from better data capture, which feeds AI-driven targeting to improve offer fit and conversion over time. As wallet usage expands, consumers expect gift-card balances to be ready across web and in-store acceptance, narrowing the gap between channels.

Offline remains important for corporate bulk buys, last-minute gifting, and households preferring tactile selection from endcap displays. Issuers expand distribution by stocking digital open-loop products in physical stores with QR activation and instant wallet loading, giving walk-in buyers immediate digital convenience. Packaging enhancements and serial management reduce exposure to code harvesting and draining schemes that target retail racks. Omnichannel portfolios that support Apple Pay, Google Pay, and Samsung Pay across checkout types keep abandonment low when preferred methods are available. The net result is a steady mix shift toward online as the gift card and incentive cards market embeds issuance and redemption natively into digital journeys.

By Industry of Application: QSR Dominance Yields to Consumer Electronics' API-Driven Surge

Food and beverages held a 28.12% share in 2025, supported by mobile ordering, loyalty integration, and app-centered reloading that drive frequent use. Coffee and quick-service leaders leverage closed-loop programs for margin retention and data insight, while aggregators extend category reach for cross-brand rewards. Consumer electronics is projected to grow at an 11.02% CAGR as gaming, subscriptions, and app ecosystems route purchases through gift value, expanding use cases beyond holiday cycles. Category leaders pair gift cards with subscription credits, in-app currency, and content bundles to deepen engagement and recurring spend patterns. As more issuers provide real-time delivery through wallets, electronics, and entertainment tilt toward always-on gifting in the gift card and incentive cards market.

Beauty and health programs apply targeted offers that map to customer preferences, while apparel and footwear brands use recommendation engines to match denominations and designs with customer intent. Travel and entertainment issuers emphasize experiences, which keeps gift value attractive even when goods inflation pressures traditional retail categories. Hybrid greeting-plus-digital formats add a tactile option without sacrificing instant redemption. Enterprise buyers also direct spend into electronics categories during recognition campaigns, which aligns reward form with devices and services used in daily work. This diversification across verticals broadens the base of high-frequency use within the gift card and incentive cards industry.

Geography Analysis

North America held 40.06% in 2025, with the United States providing a large base of consumers and enterprises using gift value across retail and dining. Consumer payments surveys show wallet linking rising among both debit and credit holders, and mobile payments are increasing their share of point-of-sale transactions compared to the prior year. State-level policy actions increase focus on secure packaging and fraud-prevention expectations for retailers, which shape implementation timelines and cost models for physical programs. Corporate incentive outlooks signal larger budgets in 2026, pointing to continued B2B scaling as companies automate issuance flows into employee and channel programs. Acceptance expansion among networks also improves the practicality of open-loop prepaid for cross-merchant use, complementing the large footprint of closed-loop leaders.

Asia-Pacific leads growth at a projected 10.23% CAGR, supported by interoperable real-time payment systems and high mobile wallet penetration. In India, program managers launched intelligent gift-card platforms with configurable discounts and product scoping, reducing time-to-personalization and aligning issuance to local consumer behavior. Network acceptance continues to widen in Japan and other markets, which raises utility for open-loop products in face-to-face and online flows. As wallet ecosystems become the default for transit, retail, and services, digital gift storage and redemption become native behaviors. These patterns align Asia-Pacific to higher digital growth for the gift card and incentive cards market, with corporate and consumer demand converging on mobile use cases.

Europe shows steady expansion amid increasing environmental standards and data protection obligations that shape program design. Producer responsibility and packaging content rules tighten, which supports paper substrates and digital format adoption among issuers seeking to reduce plastic content. In employee benefits, a 2024 spin-off added capital flexibility and acquisition optionality, enabling growth in digital-native benefits platforms across Spain and Mexico while sustaining core European markets. Central and Eastern Europe sees closed-loop hybrids progressing as mall operators and retail networks adopt data-rich gift platforms that favor local commerce and on-premise redemption. As wallet coverage grows and network acceptance expands, open-loop utility increases, but closed-loop programs continue to anchor merchant loyalty strategies across key countries.

Competitive Landscape

The gift card and incentive cards market features moderate concentration, with issuance infrastructure, network rails, and aggregation APIs driving competitive advantage. Aggregators advanced their enterprise stack through acquisitions in 2024 and deeper fintech partnerships in 2025, which expanded digital catalogs, installment options, and workflow automation for B2B buyers. Integration between gift platforms and POS systems improved activation and redemption for restaurants, hospitality, and retail, lowering operational friction for omnichannel acceptance. Card networks invested in AI fraud detection and tokenization at scale to strengthen trust in prepaid flows while also enabling agentic commerce patterns that anticipate automated shopping behaviors. Leading digital stores continued to demonstrate high mobile optimization benchmarks, reflecting a focus on instant delivery and personalization as differentiators in program performance.

Strategic moves highlight two paths: horizontal scale and vertical specialization. Payments firms introduced crypto acceptance for merchants with simplified pricing and broad asset support, creating a bridge from digital assets to retail gift value across large user bases. In India, a new intelligent gift-card platform launched in March 2025 to give businesses granular control over discounting and product scope, shortening design-to-launch cycles for tailored programs. Employee benefits providers expanded portfolios and regional reach through acquisitions and long-term distribution partnerships, reinforcing their role in corporate reward ecosystems across Europe and Latin America. Blockchain pilots in the United States introduced secure wallet storage and traceable redemption for gift cards, which address widely reported vulnerabilities in physical packaging and code exposure.

Acceptance growth by major card brands increased parity and reach across categories from airlines and transit to retail and hospitality, strengthening the case for open-loop prepaid instruments in corporate programs. Issuers and aggregators also emphasized environmental targets with paper conversion and dematerialization to meet 2028 PVC-elimination objectives that align with network standards. As POS integrations deepen and digital storefronts widen, leaders leverage data and AI to refine timing, personalization, and denomination strategies at scale. Together, these moves consolidate enterprise demand within platforms that combine wide brand catalogs, robust fraud controls, and omnichannel acceptance in the gift card and incentive cards market.

Gift Card and Incentive Card Industry Leaders

Amazon.com Inc.

Apple Inc.

Walmart Inc.

Blackhawk Network Holdings Inc.

InComm Payments

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Blackhawk Network and Klarna expand their partnership to allow consumers to purchase digital gift cards from over 350 brands on Giftcards.com using flexible payment options, including “Pay in 4” interest-free installments.

- July 2025: Blackhawk Network expands its strategic partnership with Recharge Group to provide global access to digital gift cards across Recharge’s platforms, including Recharge.com and Startselect.com.

- February 2025: Raise, a United States digital gift-card and blockchain payments company, raised USD 63 million in funding to support development of its blockchain-backed Smart Cards program aimed at transforming gift cards into programmable retail currency.

- December 2024: Mastercard finalizes its acquisition of Recorded Future, a global threat-intelligence company, to enhance its cybersecurity and AI-powered analytics capabilities across payments and fraud detection.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the gift card and incentive card market as the total face value of open-loop and closed-loop cards, physical or digital, issued for consumer gifting or for corporate rewards and loyalty programs, across retail, travel, hospitality, and digital platforms worldwide.

Scope exclusion: prepaid debit products meant for general spending or payroll disbursement are outside this definition.

Segmentation Overview

- By Card Type

- Open-Loop Card

- Closed-Loop Card

- By Format Type

- Digital Card

- Physical Card

- By Consumer Type

- Individual (B2C)

- Corporate (B2B)

- By Distribution Channel

- Online

- Offline

- By Industry of Application

- Food and Beverages

- Health, Wellness, and Beauty

- Apparel, Footwear, and Accessories

- Consumer Electronics

- Other Industries

- By Region

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor interviewers survey issuers, program managers, B2B distributors, and large employers in North America, Europe, Asia-Pacific, and the GCC. Dialogues confirm average load values, breakage, and the share of incentives in total volume, letting us close gaps left by desk work.

Desk Research

We first map the payment landscape using publicly available series from central banks, BIS Red Book tables, the World Bank Global Findex, and card-network disclosures. Trade bodies such as the Gift Card & Voucher Association, National Retail Federation, and Ecommerce Europe help us size B2C flows, while white papers from fintech watchdogs enrich our view on digital breakage rates. Company 10-Ks, investor decks, and news archived in Dow Jones Factiva and D&B Hoovers provide issuer-level revenue clues. These sources illustrate but do not exhaust the wider pool reviewed by Mordor analysts.

Market-Sizing & Forecasting

We reconstruct the 2024 baseline with a top-down roll-up of card load and redemption data reported by regulators and schemes. We then cross-check it with bottom-up samples of leading issuers' volumes multiplied by blended ASPs. Key variables like e-commerce penetration, smartphone adoption, corporate reward outlays, digital wallet usage, and inflation-adjusted face values feed a multivariate regression to project demand through 2030. Where issuer data are partial, regional averages inferred from primary interviews bridge the gap.

Data Validation & Update Cycle

Outputs pass breakage ratio checks, currency reconversions, and peer review by a senior analyst panel. We refresh every twelve months and re-open the model whenever a material event, for example, new interchange rules, shifts the underlying metrics.

Why Mordor's Gift Card and Incentive Card Baseline Commands Confidence

Published estimates often diverge; scopes, face value definitions, and refresh cadences rarely align. By anchoring on regulator-verified transaction data and validating with live issuer feedback, Mordor limits noise and yields a balanced midpoint buyers can rely on.

Key gap drivers include whether breakage is netted, if corporate incentives are counted, the choice between gross loads versus active balances, and how multi-currency values are translated. Faster refreshes and our blended top-down and bottom-up logic further narrow variance.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 578.45 B (2025) | Mordor Intelligence | - |

| USD 1.24 T (2025) | Global Consultancy A | Adds transit and telecom stored value not in our scope |

| USD 614.7 B (2025) | Industry Databook B | Uses gross loads and single-day FX conversion |

| USD 271.2 B (2024) | Regional Forecasting C | Excludes corporate incentive and physical cards |

In short, our disciplined variable selection, timely updates, and transparent reconciliation steps give decision-makers a dependable, reproducible baseline, while alternative figures, though insightful, reflect different and less validated constructs.

Key Questions Answered in the Report

What is the current size and growth outlook for the global gift card and incentive cards market?

The gift card and incentive cards market size is USD 626.11 billion in 2026 and is projected to reach USD 930.23 billion by 2031 at an 8.24% CAGR.

Which segments are leading and growing fastest within the gift card and incentive cards market?

Closed-loop cards lead by share while open-loop records the fastest growth, physical formats remain larger today while digital grows quickest, and food and beverages lead by application while consumer electronics grow fastest.

How are digital wallets shaping adoption in the gift card and incentive cards market?

Wallet linking and usage are increasing, placing gift balances alongside payment credentials and reducing redemption friction across online and in-store acceptance.

What are the main risks restraining the gift card and incentive cards market?

Fraud and cybercrime trends, divergent fee and expiry regulations, SME cost pressure for open-loop programs, and tariff-driven input costs for physical cards act as key restraints.

How are enterprises using gift cards in recognition and incentive programs?

Companies scale B2B issuance through API integrations with HR and CRM systems, adopt installment options for bulk orders, and expand budgets to align rewards with performance events.

Where are the strongest regional opportunities in the gift card and incentive cards market?

Asia-Pacific leads growth due to wallet ubiquity and interoperable payment rails, while North America sustains the largest base with wide acceptance and established corporate use cases.

Page last updated on: