Canada Flexible Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

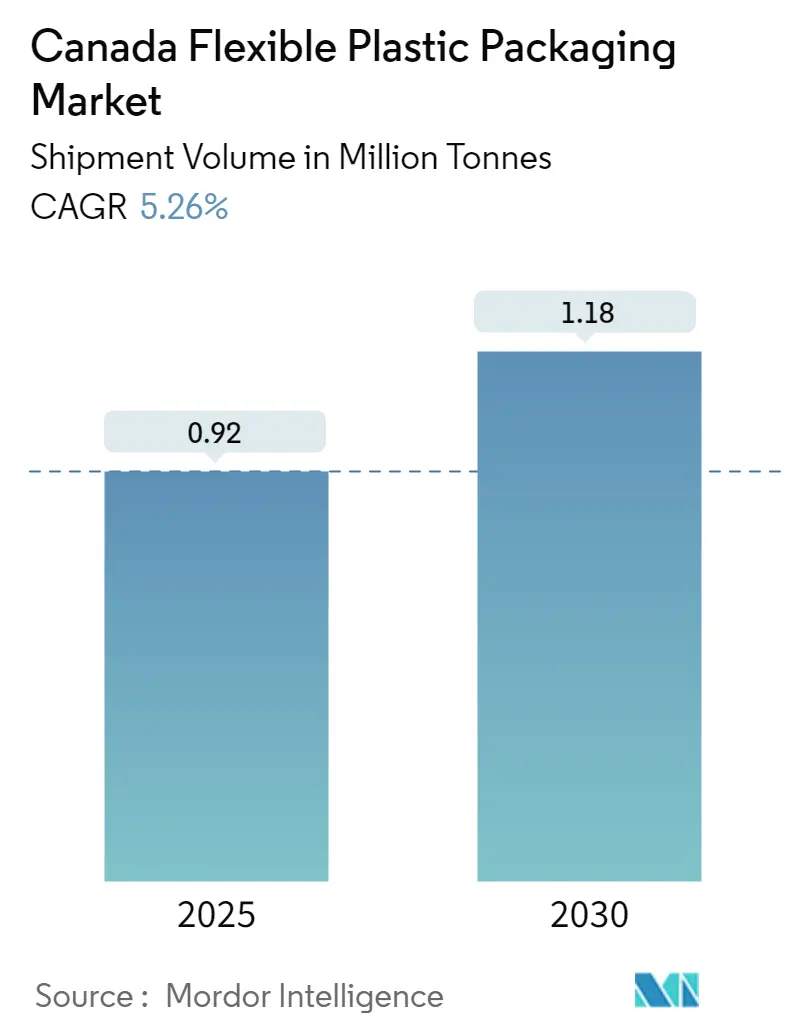

| Market Volume (2025) | 0.92 Million tonnes |

| Market Volume (2030) | 1.18 Million tonnes |

| Growth Rate (2025 - 2030) | 5.26% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Flexible Plastic Packaging Market Analysis by Mordor Intelligence

The Canada Flexible Plastic Packaging Market size in terms of shipment volume is expected to grow from 0.92 million tonnes in 2025 to 1.18 million tonnes by 2030, at a CAGR of 5.26% during the forecast period (2025-2030).

The Canadian flexible plastic packaging industry is experiencing significant transformation driven by the rapid growth of e-commerce and digital retail channels. According to Statistics Canada, retail e-commerce sales increased from CAD 3,775.46 million in August 2022 to CAD 3,902.93 million in March 2023, highlighting the growing demand for flexible packaging solutions suited for online retail. Major online retailers, including Amazon, Walmart, Canadian Tire, Costco, Best Buy, Hudson's Bay, and Etsy, have adopted advanced plastic packaging solutions to enhance their supply chain efficiency and customer experience. This shift has prompted packaging manufacturers to develop innovative solutions specifically designed for e-commerce applications.

Environmental sustainability has become a cornerstone of industry development, with manufacturers increasingly focusing on eco-friendly flexible packaging materials. The Canada Plastics Pact (CPP) has set ambitious targets for flexible plastic packaging recycling, aiming to enable over 30% of household flexible plastic packaging to be effectively recycled by 2027 and 50% by 2030. In September 2023, CPP announced a comprehensive five-year plan to boost the circular economy of flexible plastic packaging across Canada, establishing unprecedented cross-value chain collaboration among key industry partners.

The industry is witnessing significant technological advancements in materials and manufacturing processes. Digital printing in flexible packaging is gaining prominence, offering high-quality, customizable, and cost-effective solutions. The integration of smart packaging technologies, including RFID tags, QR codes, and sensors, is enhancing traceability, quality control, and consumer engagement. These innovations are particularly crucial in the pharmaceutical sector, where spending reached approximately CAD 48 billion in 2023, driving demand for advanced packaging solutions with improved barrier properties and security features.

Canada's changing demographics and immigration patterns are reshaping packaging demands across various sectors. Statistics Canada reported that 468,817 people immigrated to Canada between July 2022 and June 2023, representing a significant increase from previous years. This demographic shift has led to diverse consumer preferences and increased demand for varied packaging solutions. In response, manufacturers are developing more versatile and culturally adaptive packaging designs, while also focusing on multilingual labeling and region-specific requirements to cater to this growing multicultural market.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Canada representing one among them. The global report on flexible plastic packaging market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Canada Flexible Plastic Packaging Market Trends and Insights

Flexible Plastics Currently Account for the Largest Share in the Canadian Packaging Industry and is Expected to Retain its Position Over the Forecast Period

The dominance of flexible plastics in Canada's packaging industry is driven by its versatility and superior performance characteristics. Polyethylene, in particular, has emerged as a crucial material due to its lightweight properties, chemical resistance, and excellent moisture barrier capabilities. The material's adaptability allows manufacturers to create various flexible packaging solutions, from simple bags to complex multilayer structures, catering to diverse industry needs from food preservation to industrial applications.

The material's economic advantages and efficiency in the production process have solidified its position in the market. High-density polyethylene (HDPE) and low-density polyethylene (LDPE) offer distinct advantages for different applications. HDPE provides superior stiffness and strength, making it ideal for applications requiring structural integrity, while LDPE offers greater flexibility and clarity, perfect for applications where transparency and malleability are crucial. The industry has also seen significant innovations in material science, with developments in biaxially oriented polypropylene (BOPP) and cast polypropylene (CPP) films providing enhanced barrier properties and improved processing capabilities.

Growing Demand for Convenience Foods

The increasing workforce participation and busy lifestyles in Canada have created a substantial market for convenience foods, directly impacting the flexible packaging industry. According to the International Monetary Fund, the number of employed people in Canada is forecast to increase by 0.1 million people (+0.5 percent) between 2023 and 2024, reaching 20.22 million people. This growing workforce has led to increased demand for on-the-go packaging solutions that offer convenience and portability.

High-demand frozen food categories are driving innovation in packaging design to meet specific requirements such as maintaining freshness, ease of use, and shelf appeal. Manufacturers are investing in developing new types of flexible packaging tailored to these food categories' needs, with features like resealable closures, easy-pour spouts, and enhanced barrier properties. The segment's growth is particularly evident in the ready-to-eat meals sector, where flexible packaging solutions provide optimal protection while ensuring convenience in handling and storage. These packaging solutions are designed to withstand various temperature conditions while maintaining food quality and safety, making them ideal for the growing convenience food market.

Segment Analysis: By Material Type

Polyethylene (PE) Segment in Canada Flexible Plastic Packaging Market

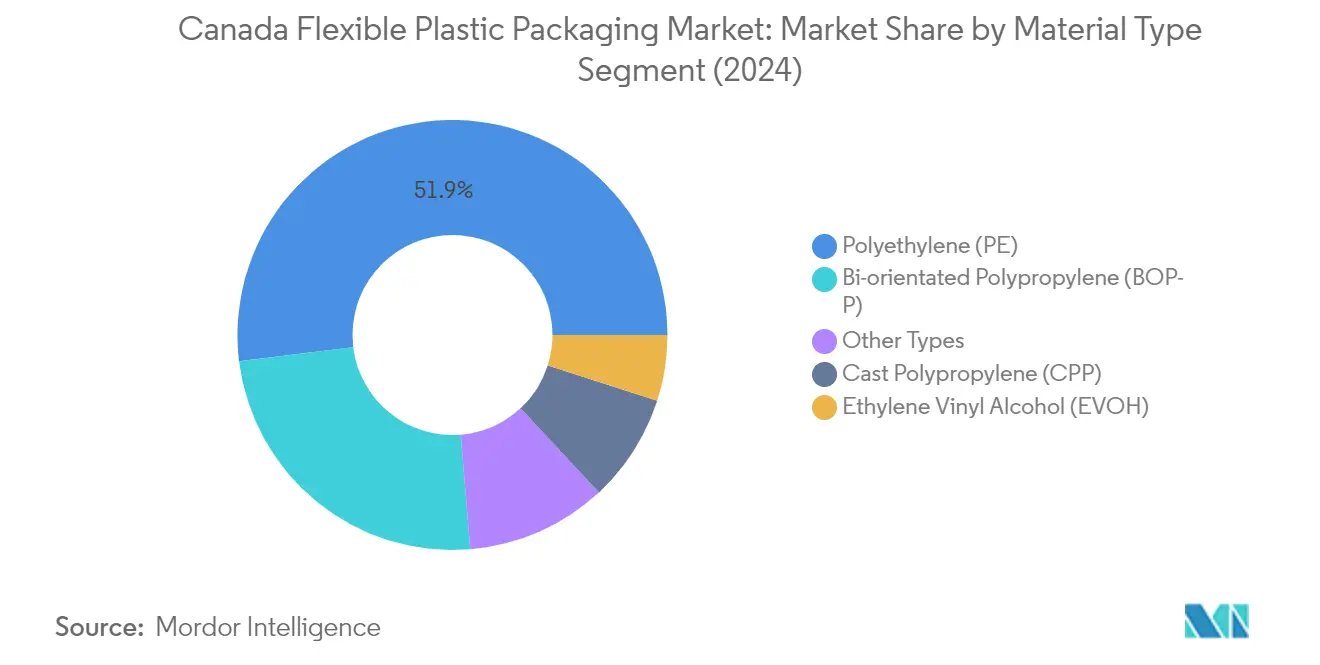

Polyethylene (PE) maintains its dominant position in Canada's flexible plastic packaging market, commanding approximately 52% of the market share in 2024. This material's widespread adoption is primarily attributed to its versatility and superior properties, including high resistance to chemicals, low moisture absorption, and sound-insulating characteristics. PE's dominance spans various applications, from packaging plastic bags to plastic films and geomembranes. The segment's strength is particularly evident in the food packaging sector, where LDPE's flexibility and HDPE's durability make them ideal choices for different flexible food packaging requirements. The material's cost-effectiveness and adaptability to various manufacturing processes have made it the preferred choice among manufacturers, while its ability to be customized for different barrier properties and sealing requirements has further cemented its market leadership.

Bi-orientated Polypropylene (BOPP) Segment in Canada Flexible Plastic Packaging Market

The Bi-orientated Polypropylene (BOPP) segment is experiencing remarkable growth in the Canadian market, projected to expand at approximately 7% CAGR from 2024 to 2029. This growth is driven by BOPP's exceptional versatility and superior performance characteristics, including high tensile strength and improved stiffness. The material's ability to provide excellent barrier properties against moisture and gases makes it particularly attractive for flexible food packaging applications. BOPP's growing popularity is also attributed to its sustainability advantages, as it can be laminated with polyethylene film while maintaining recyclability in the waste stream. The segment's growth is further supported by technological advancements in manufacturing processes, enabling the production of films with enhanced clarity, better heat resistance, and improved printability, making it increasingly preferred for premium flexible packaging applications.

Remaining Segments in Material Type

The other significant segments in the market include Cast Polypropylene (CPP), Ethylene Vinyl Alcohol (EVOH), and various other materials such as PVC, PA, and Bioplastics. CPP has carved out a niche in applications requiring higher tear and impact resistance, particularly in the healthcare and pharmaceutical industries. EVOH continues to be crucial in applications requiring superior barrier properties, especially for packaging perishable products. The emergence of bioplastics and other innovative materials reflects the industry's response to growing environmental concerns and sustainability requirements. These segments collectively contribute to the market's diversity and innovation, offering specialized solutions for specific packaging needs while addressing various industry challenges and requirements.

Segment Analysis: By End-User Industry

Food Segment in Canada Flexible Plastic Packaging Market

The food segment dominates the Canada flexible packaging market, commanding approximately 50% market share in 2024. This significant market position is driven by the increasing demand for convenient and portable flexible packaging solutions across various food categories, including bakery and confectionery, pet food, seafood and meat, and convenience foods. The segment's dominance is further strengthened by the growing urban lifestyle of consumers in the region who are seeking easy-to-use and lightweight flexible packaging products. The food segment's strong position is also supported by the expanding organized retail market and changing consumer demands, particularly in the convenience and processed food categories. Additionally, the transformation of busy lifestyles and rising e-retail penetration across Canada are macro factors boosting the demand for flexible plastic packaging in food applications.

Cosmetics and Personal Care Segment in Canada Flexible Plastic Packaging Market

The cosmetics and personal care segment is emerging as the fastest-growing segment in the Canada flexible packaging market, with a projected growth rate of approximately 8% during 2024-2029. This robust growth is primarily driven by the increasing adoption of flexible packaging solutions in the cosmetics industry, particularly in Ontario and Quebec, which are home to the most prominent manufacturers of cosmetic products and skincare. The segment's growth is further accelerated by manufacturers seeking innovative and customizable packaging solutions to stand out in the competitive market. The versatility of flexible films packaging in design, allowing for unique shapes, sizes, and printing options, has made it particularly attractive for cosmetic brands looking to enhance their shelf presence. Additionally, the increasing focus on sustainable packaging solutions in the cosmetics industry is driving innovations in eco-friendly flexible films packaging materials.

Remaining Segments in End-User Industry

The other significant segments in the Canada flexible packaging market include beverages, pharmaceutical and medical devices, household care, and other end-user industries. The beverages segment is particularly notable for its adoption of innovative packaging solutions, especially in the premium spirits, beer, and wine categories. The pharmaceutical and medical devices segment is driven by the need for high-barrier protection and sterile packaging solutions. The household care segment benefits from the growing demand for convenient and portable packaging options. Other end-user industries, including tobacco, chemicals, and agriculture, contribute to the market's diversity by requiring specialized flexible industrial packaging solutions for their unique applications. Each of these segments plays a crucial role in driving innovation and sustainability initiatives in the flexible packaging industry.

Competitive Landscape

Top Companies in Canada Flexible Plastic Packaging Market

The Canadian flexible plastic packaging market features a mix of global leaders and regional specialists, including prominent players like Amcor Group, Mondi Plc, Berry Global, Constantia Flexibles, and domestic companies like Flair Flexible Packaging Corporation and Emmerson Packaging. These companies demonstrate strong product innovation capabilities, particularly in sustainable flexible packaging solutions like recyclable materials and mono-material structures. Operational agility is evidenced through vertical integration strategies and investments in advanced manufacturing technologies, enabling quick responses to market demands. Strategic moves focus heavily on sustainability initiatives, with companies investing in recycling infrastructure and developing eco-friendly alternatives. Market expansion strategies include both organic growth through capacity enhancement and inorganic growth via strategic acquisitions, with particular emphasis on strengthening presence in high-growth segments like food packaging and e-commerce solutions.

Consolidated Market with Strong Global Players

The flexible packaging market in Canada exhibits a relatively consolidated structure dominated by multinational corporations with extensive manufacturing capabilities and broad product portfolios. These global players leverage their research and development capabilities, established distribution networks, and economies of scale to maintain competitive advantages. Regional players carve out niches through specialized product offerings and strong local customer relationships, though they face increasing pressure from larger competitors. The market has witnessed significant consolidation through mergers and acquisitions, as larger companies seek to expand their technological capabilities and geographic reach.

The competitive landscape is characterized by a mix of diversified packaging conglomerates and specialized flexible packaging manufacturers. Major global players often operate through multiple divisions serving various end-user industries, while specialized players focus on specific market segments or technologies. Merger and acquisition activity has been particularly strong in recent years, with companies seeking to acquire complementary technologies, enhance sustainability capabilities, and strengthen their position in key end-user markets like food and beverage, healthcare, and personal care.

Innovation and Sustainability Drive Future Success

For established players to maintain and expand their market share, a focus on sustainable flexible packaging solutions and technological innovation is crucial. Companies must invest in research and development to create recyclable and eco-friendly products while maintaining performance characteristics. Building strong relationships with key customers through collaborative innovation and customized solutions helps defend against competitive pressures. Vertical integration and operational efficiency improvements are essential to manage costs and maintain pricing flexibility, while strategic acquisitions can help consolidate market position and acquire new capabilities.

Emerging players can gain ground by focusing on niche markets and specialized applications where larger competitors may be less active. Success factors include developing innovative solutions for specific end-user needs, particularly in growing segments like e-commerce packaging. Companies must navigate increasing regulatory pressure regarding plastic waste and recycling, making sustainability credentials increasingly important for market success. The risk of substitution from alternative packaging materials necessitates continuous innovation in product performance and sustainability features. End-user concentration in sectors like food and beverage requires strong customer relationship management and the ability to meet stringent quality and performance requirements.

Canada Flexible Plastic Packaging Industry Leaders

FLAIR Flexible Packaging Corporation

Mondi Plc

Amcor Group GmbH

Constantia Flexibles Group GmbH

C-P Flexible Packaging, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2023: Berry Global Group Inc. launched a new version of its Omni Xtra polyethylene cling film for fresh food applications. It provides a high-performance alternative to traditional polyvinyl chloride (PVC) cling films. Omni Xtra is already established, while the new Omni Xtra+ film improved elasticity, uniform stretching behavior, and improved impact resistance.

- June 2023: Novolex’s flagship tote bag, the ProWAVE, is now available in 2.25 mm gauge film. Hilex, a brand of Novolex, announced new options for its popular tote bag. The ProWAVE is a recyclable and reusable tote bag designed to streamline the delivery and carry-out process for supermarkets, restaurants, retailers, and their customers. Hilex’s ProWAVE Totes are made with 40% after-consumer recycled material, which allows them to meet most of the legislative requirements for reusable tote bags, including in California. ProWAVE Totes now come in 1.7 mm film.

Canada Flexible Plastic Packaging Market Report Scope

Flexible plastic packaging refers to plastics that are easily compressed into a ball, thanks to their flexible nature. Typical items include grocery and bread bags, snack wrappers, netted produce bags, and zipper-lock pouches.

The Canada Flexible Plastic Packaging Market Report is Segmented by Material (Polyethene [PE], Bi-Oriented Polypropylene [BOPP], Cast Polypropylene [CPP], Polyvinyl Chloride [PVC], Ethylene Vinyl Alcohol [EVOH], and Other Material Types [Polycarbonate, PHA, PLA, Acrylic, and ABS]), Product Type (Pouches, Bags, Films and Wraps, and Other Product Types), End-User Industry (Food [Frozen Food, Dry Food, Meat, Poultry, and Sea Food, Candy & Confectionery, Pet Food, Dairy Products, Fresh Produce and Other Food (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)], Beverage, Medical and Pharmaceutical, Personal Care and Household Care, and Other End User Industry [Automotive, Chemical, Agriculture ]). The Report Offers the Market Size inTerms of Volume (Tonnes) for all the above-mentioned Segments.

| Polyethene (PE) |

| Bi-oriented Polypropylene (BOPP) |

| Cast Polypropylene (CPP) |

| Polyvinyl Chloride (PVC) |

| Ethylene Vinyl Alcohol (EVOH) |

| Other Material Types (Polycarbonate, PHA, PLA, Acrylic, and ABS) |

| Pouches |

| Bags |

| Films and Wraps |

| Other Product Types (Blister Packs, Liners, etc) |

| Food | Candy & Confectionery |

| Frozen Foods | |

| Fresh Produce | |

| Dairy Products | |

| Dry Foods | |

| Meat, Poultry, And Seafood | |

| Pet Food | |

| Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.) | |

| Beverage | |

| Medical and Pharmaceutical | |

| Personal Care and Household Care | |

| Other End user Industries ( Automotive, Chemical, Agriculture) |

| By Material Type | Polyethene (PE) | |

| Bi-oriented Polypropylene (BOPP) | ||

| Cast Polypropylene (CPP) | ||

| Polyvinyl Chloride (PVC) | ||

| Ethylene Vinyl Alcohol (EVOH) | ||

| Other Material Types (Polycarbonate, PHA, PLA, Acrylic, and ABS) | ||

| By Product Type | Pouches | |

| Bags | ||

| Films and Wraps | ||

| Other Product Types (Blister Packs, Liners, etc) | ||

| By End-User Industry | Food | Candy & Confectionery |

| Frozen Foods | ||

| Fresh Produce | ||

| Dairy Products | ||

| Dry Foods | ||

| Meat, Poultry, And Seafood | ||

| Pet Food | ||

| Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.) | ||

| Beverage | ||

| Medical and Pharmaceutical | ||

| Personal Care and Household Care | ||

| Other End user Industries ( Automotive, Chemical, Agriculture) | ||

Key Questions Answered in the Report

How big is the Canada Flexible Plastic Packaging Market?

The Canada Flexible Plastic Packaging Market size is expected to reach 0.92 million tonnes in 2025 and grow at a CAGR of 5.26% to reach 1.18 million tonnes by 2030.

What is the current Canada Flexible Plastic Packaging Market size?

In 2025, the Canada Flexible Plastic Packaging Market size is expected to reach 0.92 million tonnes.

Who are the key players in Canada Flexible Plastic Packaging Market?

FLAIR Flexible Packaging Corporation, Mondi Plc, Amcor Group GmbH, Constantia Flexibles Group GmbH and C-P Flexible Packaging, Inc are the major companies operating in the Canada Flexible Plastic Packaging Market.

What years does this Canada Flexible Plastic Packaging Market cover, and what was the market size in 2024?

In 2024, the Canada Flexible Plastic Packaging Market size was estimated at 0.87 million tonnes. The report covers the Canada Flexible Plastic Packaging Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Canada Flexible Plastic Packaging Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: