GCC Plastic Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

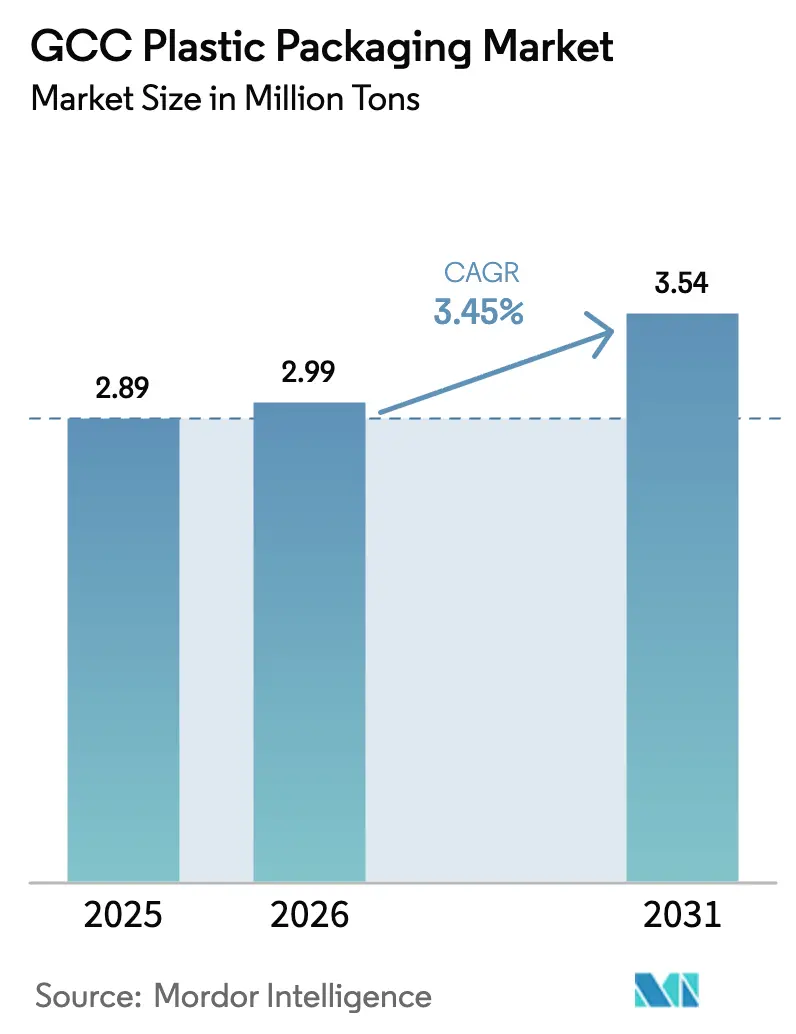

| Base Year Market Size (2025) | 2.89 Million tons |

| Market Volume (2026) | 2.99 Million tons |

| Market Volume (2031) | 3.54 Million tons |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

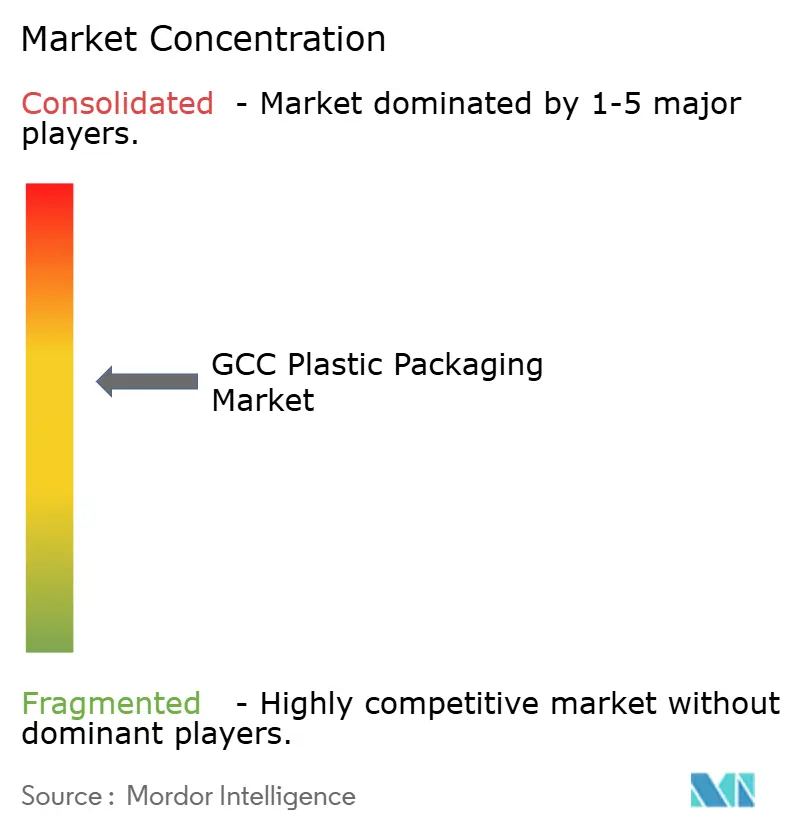

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Plastic Packaging Market Analysis by Mordor Intelligence

GCC Plastic Packaging Market size in 2026 is estimated at 2.99 Million tons, growing from 2025 value of 2.89 Million tons with 2031 projections showing 3.54 Million tons, growing at 3.45% CAGR over 2026-2031. Strong feedstock integration, rising consumption of packaged foods, and sustained bottled water demand underpin this expansion while new recycling mandates reshape value-addition opportunities. Export-oriented capacity additions, such as Borouge’s USD 6.2 billion fourth complex in Abu Dhabi, reinforce price competitiveness that import-dependent regions struggle to match. Accelerated factory growth under Saudi Arabia Vision 2030 and the United Arab Emirates industrial agenda expands local FMCG output, tightening ties between resin suppliers, converters, and brand owners.[1]Saudi Press Agency, “Saudi Arabia’s Industrial Development Under Vision 2030,” spa.gov.sa Climate-driven hydration habits and e-commerce fulfillment spur flexible and protective formats, while petrochemical majors and specialty recyclers vie to satisfy circular-economy rules introduced across several GCC states.

Key Report Takeaways

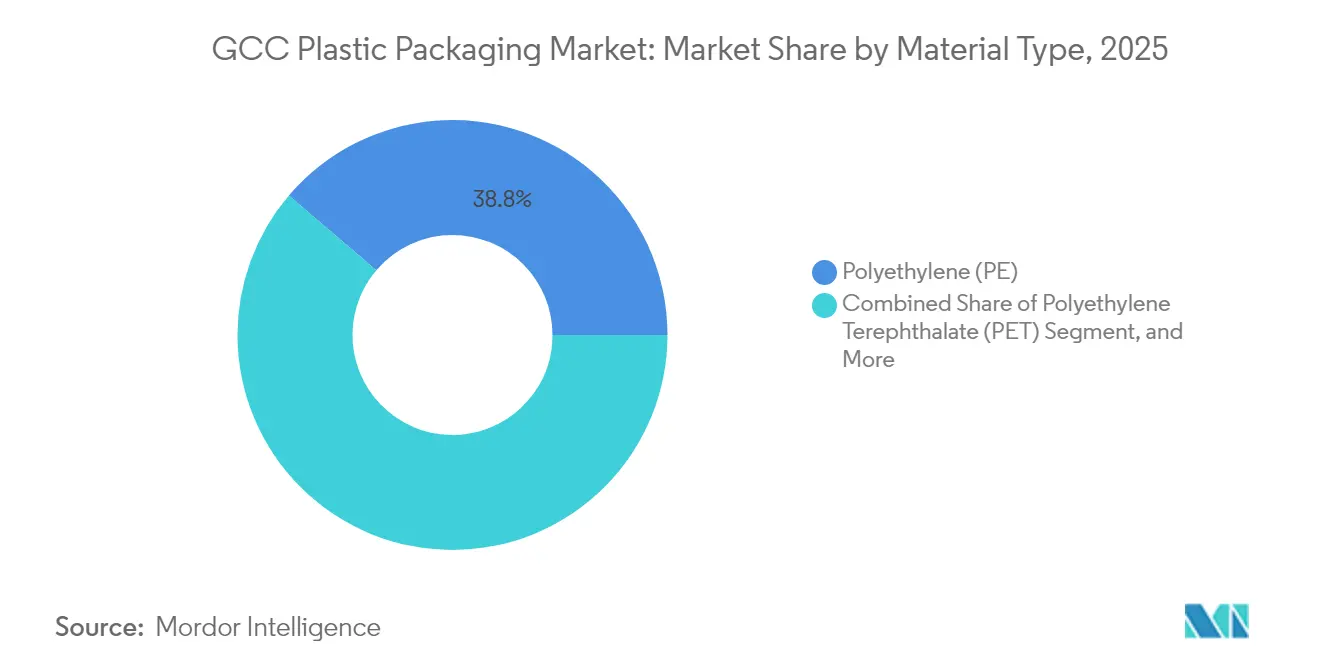

- By material type, polyethylene led with 38.77% of GCC plastic packaging market share in 2025, while PET is projected to expand at a 4.48% CAGR through 2031.

- By packaging type, flexible solutions accounted for 54.60% share of the GCC plastic packaging market size in 2025 and are advancing at a 5.02% CAGR to 2031.

- By product form, pouches and sachets commanded 35.62% of GCC plastic packaging market share in 2025; films and wraps record the fastest 4.30% CAGR through 2031.

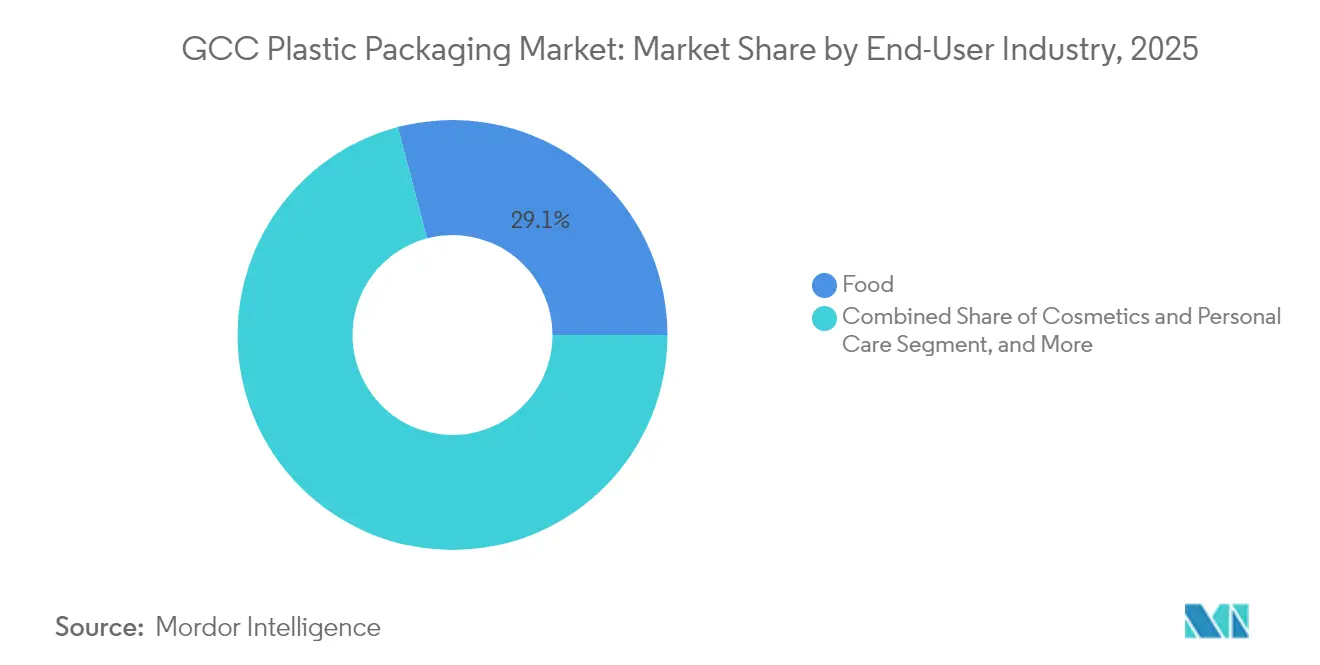

- By end-user industry, food applications captured 29.10% share of the GCC plastic packaging market size in 2025, whereas cosmetics and personal care packaging is progressing at a 5.55% CAGR between 2026-2031.

- By manufacturing process, extrusion held 28.95% share of the GCC plastic packaging market size in 2025, while thermoforming posts the highest 4.27% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing packaged food and beverage demand | +1.2% | GCC-wide, strongest in Saudi Arabia and UAE | Medium term (2-4 years) |

| Climate-driven bottled water consumption surge | +0.8% | GCC-wide, peak in summer months | Short term (≤ 2 years) |

| E-commerce boom raising protective packaging needs | +0.6% | UAE and Saudi Arabia, emerging in Qatar and Kuwait | Medium term (2-4 years) |

| GCC industrial diversification boosting local FMCG output | +0.9% | Saudi Arabia and UAE leading | Long term (≥ 4 years) |

| Mandatory “UTC” UV-protection label accelerating multilayer film uptake | +0.3% | Saudi Arabia initially | Medium term (2-4 years) |

| Zero-waste city pilots spurring recycled-content deals | +0.4% | UAE and Saudi Arabia pilot cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Packaged Food and Beverage Demand

Rapid population growth and localization of food supply have lifted the baseline for packaging consumption across the GCC. Saudi Arabia recorded a 60% expansion in food manufacturing capacity since Vision 2030 took effect, with multinational brands channeling new capital into dairy, confectionery, and ready-meal plants that specify multilayer barrier films for oxygen and moisture control. The United Arab Emirates National Food Security Strategy aims for high self-sufficiency and favors converters that provide traceable, food-grade resins aligned with Gulf Cooperation Council Standardization Organization (GSO) rules. Portion-controlled pouches designed for hot climates and modified-atmosphere trays that extend shelf life are gaining premium placement at retailers. This sustained offtake underpins both volume growth and value-added film innovation across the GCC plastic packaging market.

Climate-Driven Bottled Water Consumption Surge

Ambient temperatures surpassing 45 °C for extended periods make packaged water an everyday necessity. The regional bottled water value reached USD 6.79 billion in 2024, expanding 11.16% yearly, with plastic containers accounting for 82% of volumes. PET dominates due to clarity, strength-to-weight ratio, and cost advantages, while HDPE jugs serve bulk consumption. Government recycling targets such as the United Arab Emirates goal to achieve a 79% PET bottle recovery rate by 2040 trigger investments in collection and flake production facilities that supply local converters.[2]United Arab Emirates Government, “Policy for Valorisation of Industrial-Use Waste,” uaelegislation.gov.ae

E-Commerce Boom Raising Protective Packaging Needs

Online retail revenue in the United Arab Emirates and Saudi Arabia is recording compound growth above 25%, shifting packaging specifications toward impact-resistant mailers, temperature-shielded liners, and QR-enabled traceability labels. Dubai’s role as a transshipment center magnifies demand for formats compliant with international freight regulations. Flexible bubble-wrap substitutes fashioned from multi-layer PE plus recycled content secure fragile goods during multi-leg delivery. Reusable cooler pouches for grocery delivery mitigate extreme outdoor heat, signalling fresh opportunities for converters with advanced lamination and insulation capabilities.

GCC Industrial Diversification Boosting Local FMCG Output

Manufacturing policy drives such as Saudi Arabia NUSANED and the UAE “Make it in the Emirates” program add thousands of new factories and mandate higher local content. Rubber and plastic products rank among the fastest-growing subsectors, ensuring forward demand visibility for pellet suppliers and processors. Domestic production of processed foods, soft drinks, and home-care items reduces import exposure and shortens supply cycles, favoring packaging plants situated near brand owners. Certified ISO-compliant producers tap government procurement contracts more readily, anchoring longer-term offtake agreements within the GCC plastic packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening EPR and single-use plastic regulations | -0.7% | UAE and Saudi Arabia leading | Short term (≤ 2 years) |

| Petrochemical feedstock price volatility | -0.5% | GCC-wide | Short term (≤ 2 years) |

| Scarcity of food-grade rPET flakes | -0.3% | GCC-wide, acute in UAE and Qatar | Medium term (2-4 years) |

| Summer port congestion delaying film imports | -0.2% | Red Sea and Persian Gulf ports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening EPR and Single-Use Plastic Regulations

The United Arab Emirates extended producer responsibility law assigns fee structures that rise as recyclability falls, compelling converters to integrate design-for-recycling features and traceability systems. Saudi Arabia’s oxo-biodegradable mandate for PE and PP items obliges suppliers to source certified masterbatches carrying the Saudi Standards, Metrology and Quality Organization logo. Compliance heightens working-capital needs for smaller firms and drives portfolio shifts toward multi-use or compostable alternatives. While short-term volume could tighten, long-term winners will likely be processors that align offerings with harmonized Gulf standards and recycled-content thresholds.

Petrochemical Feedstock Price Volatility

Benchmark crude swings permeate ethylene and propylene contract prices, compressing margins for converters that sell into price-sensitive segments like water bottles or stretch film. The Red Sea shipping disruptions demonstrated how logistical shocks amplify resin cost spikes and delivery delays, forcing converters to hedge inventories and diversify sourcing. Integrated majors such as SABIC offset volatility through captive feedstock streams, but independent processors remain exposed until forward-pricing mechanisms or take-or-pay supply agreements gain wider acceptance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyethylene Dominance Faces PET Innovation Challenge

Polyethylene controlled 38.77% of GCC plastic packaging market share in 2025, reflecting its versatility in sachets, films, and industrial liners. Abundant ethane-based feedstock keeps high-pressure LDPE and versatile LLDPE grades cost-competitive. Nonetheless, PET is accelerating at a 4.48% CAGR to 2031 as beverage demand and deposit-return schemes expand flake supply, boosting the GCC plastic packaging market size for circular PET solutions. SABIC’s certified renewable polyolefins for in-mold labeling expand low-carbon options while maintaining mechanical performance. Specialty barrier resins and biodegradable PLA capture niche applications that command premium pricing in cosmetics and medical packaging.

Polystyrene and EPS face regulatory headwinds from single-use plastic bans, creating substitution opportunities for alternative materials and driving innovation in biodegradable options. The UAE's Emirates Biotech announced the world's largest PLA production facility with 160,000 tonnes annual capacity, targeting replacement of conventional plastics in packaging applications with projected CO2 emissions reduction exceeding 300,000 tonnes annually. Other material types, including specialty polymers and barrier materials, benefit from premiumization trends in cosmetics and pharmaceutical packaging, where performance requirements justify higher material costs. Regulatory compliance with GSO standards for UV protection and food contact applications drives demand for specialized material formulations and certified supply chains.

By Packaging Type: Flexible Solutions Capture Climate Adaptation Premium

Flexible formats represented 54.60% of the GCC plastic packaging market size in 2025 and are projected to grow 5.02% annually through 2031. Weight-to-product ratios as low as 3% enhance transport efficiency, an advantage magnified by long-haul desert logistics. Borouge leverages Borstar technology to supply bimodal PE tailored for high-stiffness yet thin-gauge films that reduce overall plastic tonnage. Multilayer pouches resist puncture and UV degradation, supporting dairy and snack exports across the wider Middle East. Rigid HDPE drums, PET jars, and PP cups retain relevance for premium beverages and personal-care segments but cede share where lightweighting and e-commerce drive specifications.

The flexible packaging advantage becomes particularly pronounced in e-commerce applications where protective performance must balance with material efficiency and consumer convenience. Advanced multilayer film technologies incorporating recycled content and barrier properties address both regulatory requirements and performance demands, creating differentiation opportunities for converters investing in sophisticated manufacturing capabilities. Rigid packaging segments focus on premium applications including cosmetics, pharmaceuticals, and industrial chemicals where container integrity and tamper evidence justify higher material costs and transportation impacts.

By Product Form: Pouches Lead Innovation While Films Accelerate

Pouches and sachets held 35.62% of GCC plastic packaging market share in 2025 due to portion control, easy dispensing, and reduced storage footprint. Ultra-high barrier structures with EVOH or metallized layers protect flavor integrity under high ambient temperatures. Films and wraps post the fastest 4.30% CAGR, propelled by pallet stretch wraps, shrink hoods, and automated bag-in-box liners required by expanding fulfillment centers. Blown-film lines with up to nine layers enable downgauging without sacrificing mechanical strength, meeting both cost and sustainability objectives.

Bottles and jars maintain steady demand in beverage and personal care applications, though growth remains constrained by recycling infrastructure limitations and regulatory pressures on single-use formats. Trays and containers benefit from food service expansion and ready-meal consumption trends, particularly in urban centers where convenience drives packaging format selection.

By End-User Industry: Food Security Drives Base Demand While Beauty Accelerates

Food applications captured 29.10% of GCC plastic packaging market size in 2025, anchored by milk, yogurt, and ambient snacks distributed through modern retail. Shelf-stable formats such as retort pouches and barrier trays lower refrigeration needs, aligning with national energy efficiency programs. Cosmetics and personal care demand is advancing 5.55% annually as affluent consumers favor prestige skin-care and fragrance housed in visually distinctive packaging. High-clarity PET bottles, metallized PP jars, and airless pumps showcase premium brand positioning that offsets rising raw-material costs.

Beverage applications benefit from climate-driven consumption patterns and bottled water market expansion at 11.16% CAGR, where plastic packaging accounts for 82% of total volume. The pharmaceutical and healthcare segment demonstrates resilience through demographic trends and healthcare infrastructure expansion, requiring specialized packaging with tamper evidence and stability characteristics.

By Manufacturing Process: Extrusion Scale Meets Thermoforming Innovation

Extrusion occupied 28.95% of GCC plastic packaging market size in 2025, supplying film rolls and profiles at volumes exceeding 3 million tpa. Continuous operations maximize output from local ethylene crackers, sustaining the cost leadership of the GCC plastic packaging market. Thermoforming is climbing 4.27% per year thanks to yogurt cups, portion-ready meal trays, and medical blister packs that need tight dimensional tolerances. Inline sheet lamination combined with post-consumer PET flakes reduces virgin feedstock by up to 30%, supporting circular-economy scorecards demanded by multinational brands.

Injection molding serves rigid packaging applications including bottles, containers, and closures, with steady demand from beverage and personal care sectors, Blow molding maintains market presence in bottle production, particularly for large-format containers and industrial applications, while facing competitive pressure from alternative packaging formats and regulatory restrictions on single-use plastics.

Geography Analysis

Saudi Arabia commands the largest share of the GCC plastic packaging market, buoyed by Vision 2030 industrial expansion that increased factory count from 7,206 to 11,549 and prioritized rubber and plastic product output. National food security projects require vast volumes of pouch films, HDPE dairy bottles, and multilayer bread bags. Waste-management rules seek 79% recycling by 2040, stimulating investment in flake, pellet, and pyrolysis plants.

The United Arab Emirates records the highest projected CAGR through 2031, supported by Dubai’s single-use plastic ban and a 79% recycling target that reward converters capable of closed-loop supply. Abu Dhabi’s Borouge 4 lifts regional PE capacity, ensuring resin availability for domestic processors and export contracts.

Qatar, Kuwait, Oman, and Bahrain collectively capture a moderate share yet post steady mid-single-digit growth. World Cup legacy infrastructure in Qatar sustains hospitality packaging demand, while Kuwait integrates downstream petrochemical projects to lure processors. Oman’s ports at Duqm and Sohar facilitate regional exports, and Bahrain’s service-sector orientation raises demand for luxury rigid packaging in banking giveaways and promotional items.

Competitive Landscape

Market concentration is moderate as petrochemical majors, including SABIC and Borouge, combine advantaged feedstock with downstream film and rigid-container units. Vertical integration cushions resin price swings and enables tailored grade development. Global converters such as Amcor and Novolex expand regional footprints via acquisitions that add local talent and regulatory familiarity. Emirates Biotech is constructing a 160,000 tonne PLA plant, signaling a push into bio-based polymers that could displace a portion of commodity plastics.[3]Zawya Projects Monitor, “UAE’s Emirates Biotech to Build World’s Largest PLA Production Facility,” zawya.com

Circular-economy imperatives drive investment in mechanical and chemical recycling. Recycling Services LLC installed a Repro-Flex pelletizer capable of processing multilayer waste into PCR granules for film extrusion.[4]K-Online, “Advancing Circular Economy in the GCC Region,” k-online.com Policy-induced differentiation favors players that certify recycled content and life-cycle emissions, heightening barriers for smaller converters without capital to upgrade lines or validate materials.

Strategic collaborations emerge as ADNOC and OMV agreed to merge Borealis with Borouge into a USD 60 billion polyolefins powerhouse, creating supply chain synergies and global market access. Consolidation trends continue as brand owners demand multi-region supply resilience and standardized sustainability credentials.

GCC Plastic Packaging Industry Leaders

Amcor plc

Huhtamaki Oyj

Sealed Air Corporation

Mondi plc

AptarGroup, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Borouge announced expansion projects expected to add USD 165-200 million in annual EBITDA, including upgrades that lift overall polyolefin capacity to more than 6.6 million tonnes.

- April 2025: The Gulf Petrochemicals and Chemicals Association calculated that every 1 million tonnes of GCC-produced recycled plastic can create 1,500 jobs and USD 650 million in GDP impact.

- March 2025: ADNOC and OMV unveiled a binding deal to combine Borealis and Borouge into Borouge Group International, forming a USD 60 billion polyolefins leader with 13.6 million tpa capacity.

- January 2025: Novolex agreed to acquire Pactiv Evergreen for USD 6.7 billion, reshaping global food-service packaging supply chains.

GCC Plastic Packaging Market Report Scope

The market is defined by the revenues accrued from the sales of flexible plastic packaging, i.e., the consumption of plastic packaging material and rigid plastic packaging in the GCC region. The study also considers the export-import dynamics of plastic packaging materials, the planned ban on plastic (including single-use plastics), and other relevant factors in the GCC region.

The GCC plastic packaging market is segmented by flexible plastic packaging (resin type [polyethylene (PE), polyethylene terephthalate (PET), polypropylene (PP), polystyrene (PS) and expanded polystyrene (EPS), polyvinyl chloride (PVC), and other resin types], product type [pouches, bag, films and wraps, and other product type], end-use industries [food, beverages, pharmaceuticals and healthcare, personal care and cosmetics, household care, and other end-use industries], country [Saudi Arabia, United Arab Emirates, and the Rest of GCC]), and rigid plastic packaging (resin type [polypropylene (PP), polyethylene terephthalate (PET), polyethylene (PE), polystyrene (PS) and expanded polystyrene (EPS), and other resin types], product type [bottles and jars, trays and containers, caps and closures, and other product type], end-use industry [food, foodservice, beverages, pharmaceuticals and healthcare, personal care and cosmetics, household care, and other end-user industries], country [Saudi Arabia, United Arab Emirates, and the Rest of GCC]). The report offers market forecasts and size in volume (units) and value (USD) for all the above segments.

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Polystyrene and EPS |

| Other Material Types |

| Flexible Plastic Packaging |

| Rigid Plastic Packaging |

| Bottles and Jars |

| Trays and Containers |

| Pouches and Sachets |

| Bags and Sacks |

| Films and Wraps |

| Other Product Forms |

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Cosmetics and Personal Care |

| Industrial |

| Other End-User Industries |

| Extrusion |

| Injection Molding |

| Blow Molding |

| Thermoforming |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polystyrene and EPS | |

| Other Material Types | |

| By Packaging Type | Flexible Plastic Packaging |

| Rigid Plastic Packaging | |

| By Product Form | Bottles and Jars |

| Trays and Containers | |

| Pouches and Sachets | |

| Bags and Sacks | |

| Films and Wraps | |

| Other Product Forms | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceuticals and Healthcare | |

| Cosmetics and Personal Care | |

| Industrial | |

| Other End-User Industries | |

| By Manufacturing Process | Extrusion |

| Injection Molding | |

| Blow Molding | |

| Thermoforming | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the current value of the GCC plastic packaging market?

The sector is valued at 2.99 million tons in 2026 and is projected to reach 3.54 million tons by 2031.

How fast is PET packaging growing in the GCC?

PET applications are expanding at a 4.48% CAGR due to bottled water and improved recycling capacity.

Which packaging format holds the largest share?

Flexible packaging leads with 54.60% of market share, thanks to lightweight and climate-resilient barriers.

How do new EPR rules affect converters?

Extended producer responsibility fees push converters to integrate recycled content and certify traceability to remain competitive.

Which country is the fastest-growing contributor?

The United Arab Emirates shows the highest forecast growth through 2031, supported by circular-economy policy and new resin capacity.

What opportunities exist for recycled plastics?

Each 1 million tonnes of recycled output can add USD 650 million to regional GDP and create 1,500 jobs, signaling significant economic upside.

Page last updated on: