Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

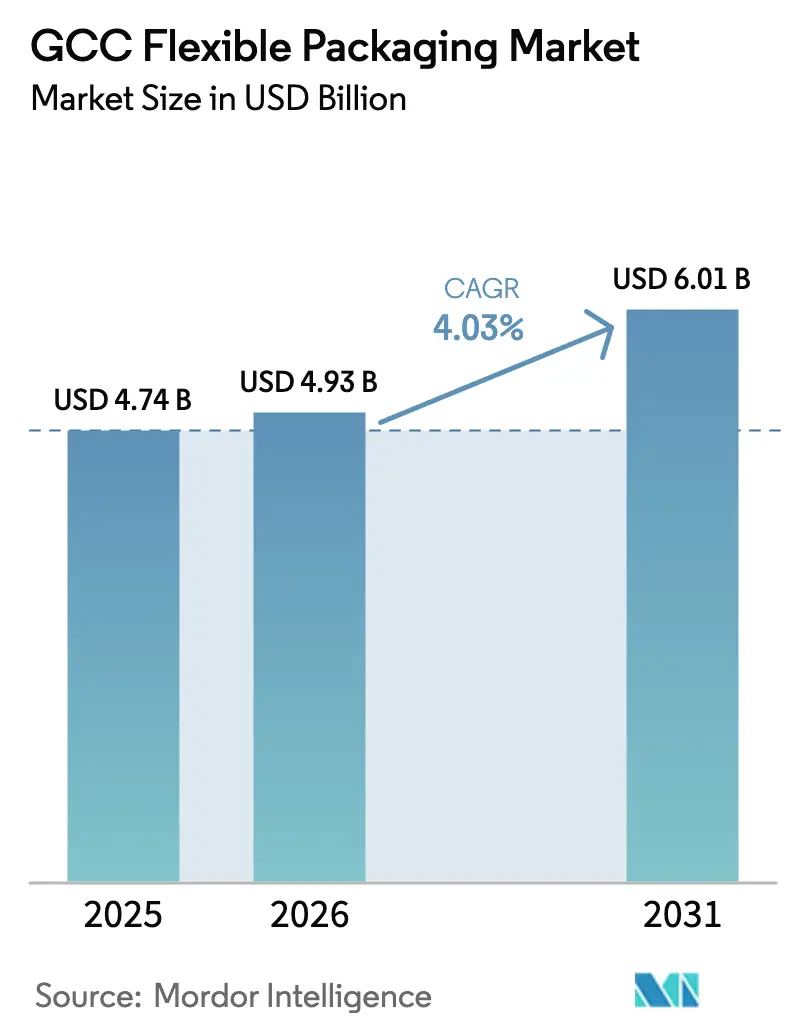

| Base Year Market Size (2025) | USD 4.74 Billion |

| Market Size (2026) | USD 4.93 Billion |

| Market Size (2031) | USD 6.01 Billion |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

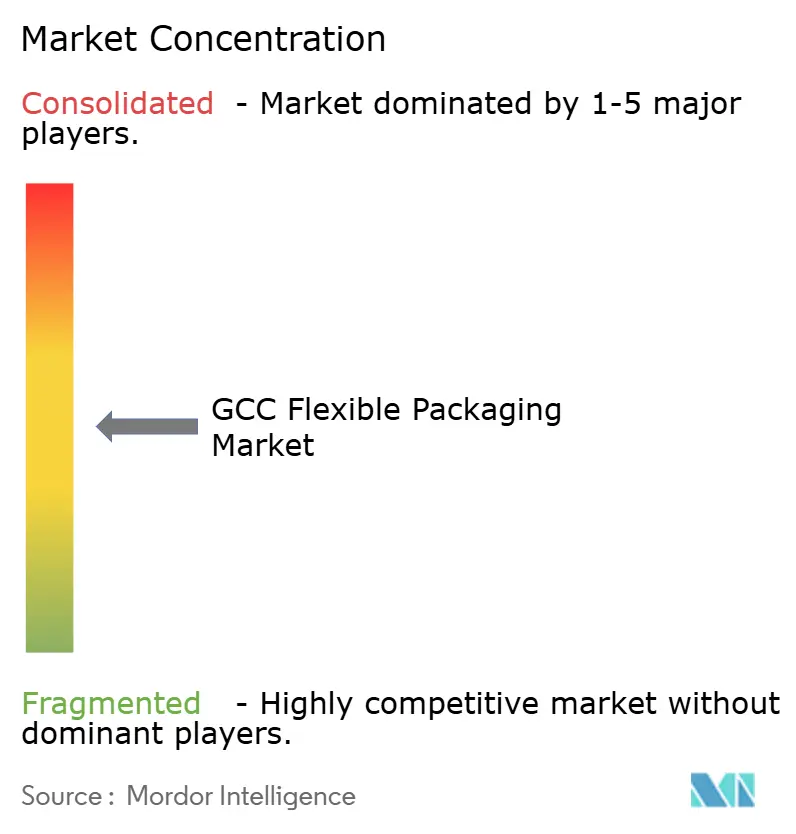

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Flexible Packaging Market Analysis by Mordor Intelligence

The GCC flexible packaging market size was valued at USD 4.74 billion in 2025 and estimated to grow from USD 4.93 billion in 2026 to reach USD 6.01 billion by 2031, at a CAGR of 4.03% during the forecast period (2026-2031). The outlook is supported by record logistics investments, rapid industrial diversification, and sustained demand for consumer goods, which together anchor a favorable demand cycle for flexible formats. Saudi Arabia’s USD 106.6 billion commitment to freight corridors, combined with the UAE’s positioning as a manufacturing and re-export hub, ensures steady throughput for converters as brands localize their supply chains for shorter lead times.[1]A.P. Møller-Mærsk, “Make way for the Middle East: UAE and KSA’s ambitious drive to become global integrated logistics hubs,” maersk.com Brand owners prioritize cost-efficient barrier performance, quick artwork changeovers, and lighter shipping weights, benefits that keep flexible formats at the center of packaging procurement strategies. Parallel government circular-economy policies drive incremental shifts toward recyclable substrates, even as access to petrochemical feedstock keeps virgin-resin economics highly competitive. Competitive intensity rises as global converters establish regional plants, spurring technology upgrades and sustainability investments among entrenched local suppliers.

Key Report Takeaways

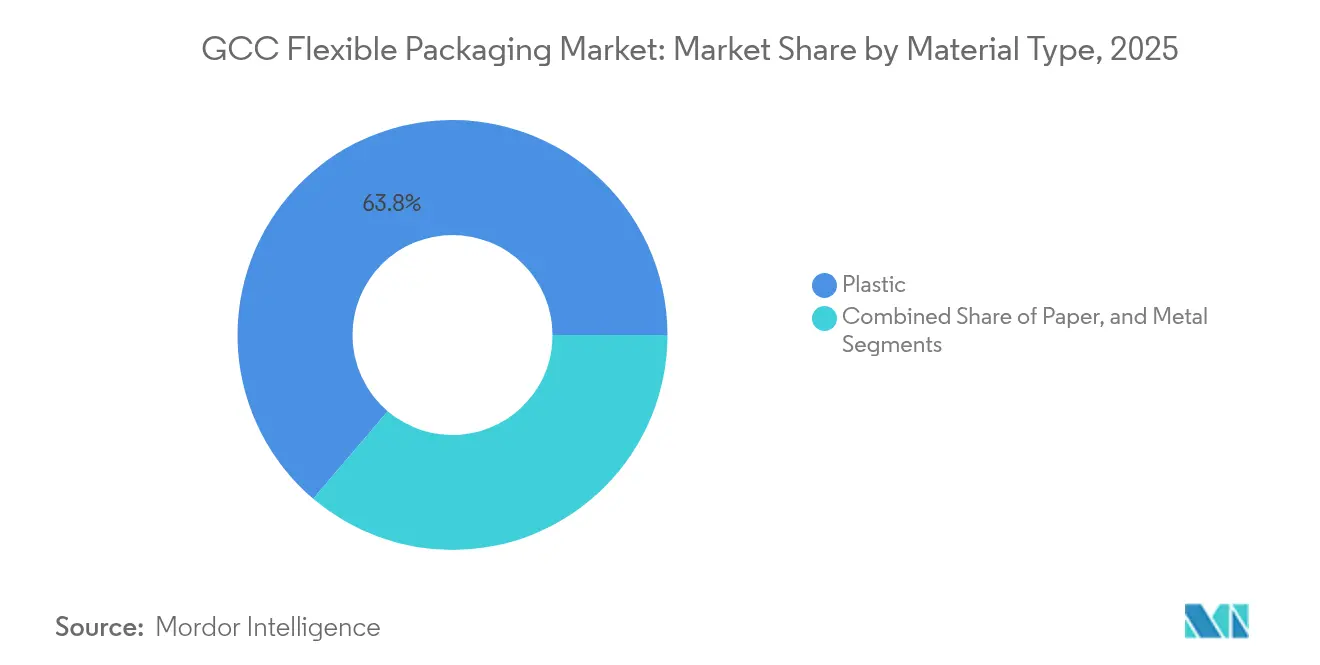

- By material type, plastic captured 63.78% of the GCC flexible packaging market share in 2025.

- By product type, the GCC flexible packaging market size for the sachets and stick packs segment is projected to grow at a 5.22% CAGR between 2026-2031.

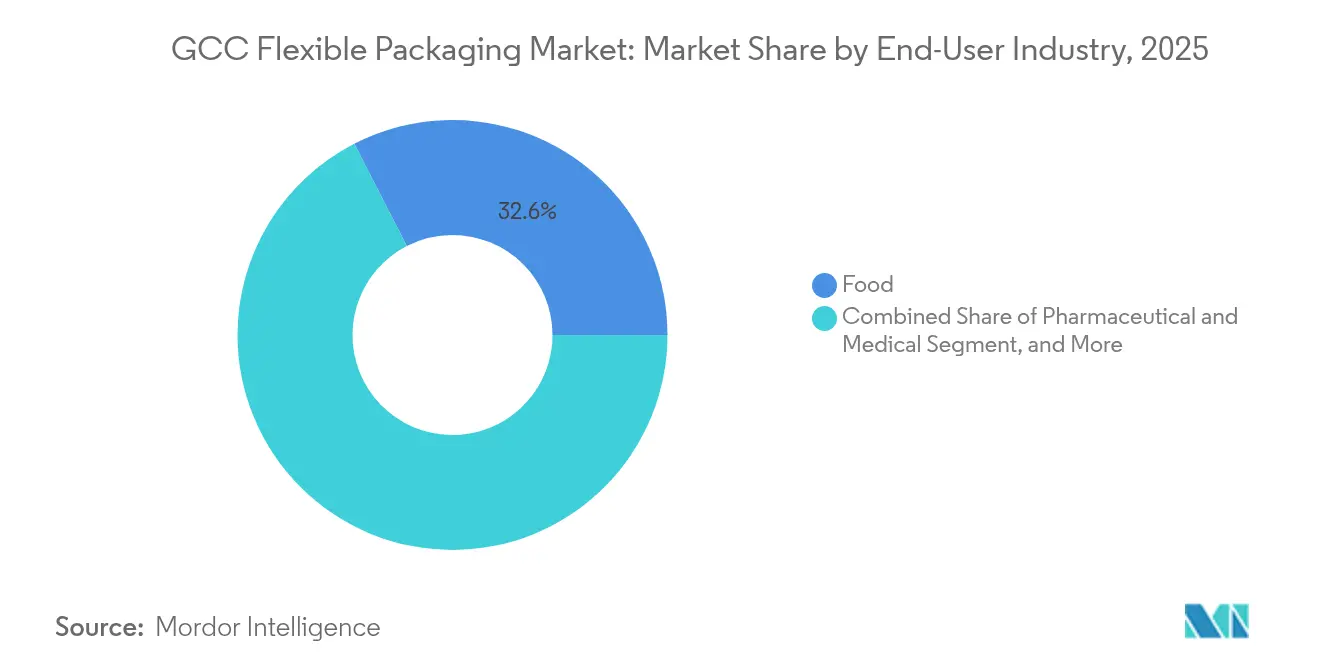

- By end-user industry, food applications captured 32.55% of the GCC flexible packaging market share in 2025.

- By printing technology, the GCC flexible packaging market size for the digital printing segment is projected to grow at a 6.08% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban population boom boosts modern retail | +0.8% | Saudi Arabia and the UAE are core; spillover to Qatar and Kuwait | Medium term (2-4 years) |

| Rapid FMCG SKU proliferation | +0.9% | Highest in the UAE and Saudi Arabia | Short term (≤ 2 years) |

| Surge in halal-packaged food exports | +0.6% | GCC-wide, led by Saudi Arabia and the UAE | Medium term (2-4 years) |

| Petrochemical feedstock cost advantage | +0.7% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Government-backed circular-economy initiatives | +0.5% | Saudi Arabia and the UAE are leading | Long term (≥ 4 years) |

| E-commerce grocery fulfillment acceleration | +0.8% | UAE and Saudi Arabia, gradual to other GCC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban Population Boom Boosting Modern Retail

Eight-plus percent annual urban growth in core GCC economies concentrates purchasing power in large, modern retail formats that rely on display-ready, lightweight, and durable packaging. Flexible pouches enable deeper shelving, single-serve merchandising, and in-store waste reduction, advantages that resonate with multinational retailers entering the high-street corridors of Riyadh and Dubai. Growing metro rail and tourism mega-projects further funnel consumers into organized retail channels, where eye-catching laminates and portioned packs command premium price points. The same density supports high-frequency e-commerce drops, magnifying the value of space-saving flexible mailers that lower last-mile costs.

Rapid FMCG SKU Proliferation

Regional food and personal-care brands are expanding their offerings by multiplying flavors, pack sizes, and seasonal editions to meet increasingly segmented shopper preferences. Digital presses that run variable data without requiring a cylinder change have reduced lead times from weeks to days, enabling manufacturers to execute localized launches with minimal inventory risk. Coupled with small-batch co-packing facilities around the Jebel Ali Free Zone, flexible formats unlock agile market testing for retailers’ private-label lines, reinforcing demand for top-up orders and micro-runs. The virtuous circle of more SKUs and faster refresh cycles sustains material volume growth even when per-SKU run-lengths fall.

Surge in Halal-Packaged Food Exports

GCC producers leverage internationally recognized halal certification to supply Asia and Africa, regions where halal claims carry pricing premiums. Exporters specify high-barrier pouches, retort sachets, and nitrogen-flushed wraps that preserve the organoleptic quality of products across long transit times. Lightweight multilayer films reduce freight weight by up to 70% compared to tins, amplifying margin gains on outbound lanes. Flexibles also simplify multi-language labeling during final assembly, allowing a single print run to serve multiple customs jurisdictions.[2]IFFCO Group, “Corporate factsheet,” iffco.com Specialized converters attuned to halal compliance secure long-term supply agreements that underpin capacity expansions in Saudi Arabia and the UAE.

E-Commerce Grocery Fulfillment Acceleration

Online grocery baskets in the Gulf are growing at a rate of 20% or more, prompting the development of automated fulfillment centers where packages are sorted through high-speed sorters and loaded into mixed-item totes. Films with superior puncture resistance and flex-crack durability prevent leaks under conveyor compression, reducing damage that erodes courier profits. Subscription meal-kit models prefer zipper and peel-seal pouches that keep contents fresh after partial use, reducing food waste and enhancing customer loyalty. Direct-to-consumer formats shift graphic priorities from shelf exposure to unboxing aesthetics, stimulating demand for matte varnishes, QR-enabled panels, and mono-material laminates that are recoverable in new recycling streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycling-infrastructure gap | -0.4% | GCC-wide, Saudi Arabia and the UAE are leading the build-out | Medium term (2-4 years) |

| Single-use plastics regulatory pressure | -0.6% | UAE from January 2025, the Saudi Arabia Vision 2030 targets | Short term (≤ 2 years) |

| Supply volatility of imported barrier resins | -0.3% | GCC-wide | Short term (≤ 2 years) |

| Brand-owner shift to rigid mono-materials | -0.2% | Global trend with selective GCC uptake | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recycling-Infrastructure Gap

Less than 15% of Saudi municipal solid waste was entered into recycling streams in 2024, resulting in flexible laminates being under-collected and under-processed. Although Riyadh earmarked USD 32 billion for 840 material-recovery facilities, build-out lags packaging growth, keeping recycled-content films scarce and costly.[3]Ministry of Environment, Water and Agriculture, “MEWA signs MoU to launch integrated waste management and recycling activities in Riyadh,” mewa.gov.sa Converters face uncertain compliance horizons for emerging extended producer responsibility schemes and must invest ahead of clear off-take markets, which squeezes cash flows and prolongs payback on washing and densifying lines.

Single-Use Plastics Regulatory Pressure

The UAE’s January 2025 ban on most single-use carrier bags intensified scrutiny of multi-layer pouches and sachets, prompting retailers to demand recyclability certifications long before formal mandates were introduced. Saudi regulators signaled similar moves under Vision 2030, accelerating redesign cycles that swap metallized layers for clear barrier coatings and encourage a shift to recyclable mono-PE structures. These redesign projects increase raw material and qualification costs, compressing converter margins until economies of scale are achieved. While the transition drives innovation, it also risks near-term volume softness as brand owners test alternate pack formats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastic Dominance Faces Sustainable Alternatives

Plastic retained a 63.78% share of the GCC flexible packaging market in 2025, backed by advantaged feedstock from integrated petrochemical complexes in Jubail and Ruwais that secure resin at globally competitive costs. This foundation enables volume discounts for converters servicing large FMCG and industrial accounts, cementing plastics’ price-performance appeal. The GCC flexible packaging market size for plastic substrates is projected to grow steadily even as governments introduce recycling targets, because mono-PE and BOPE structures now meet mandated recyclability thresholds. Paper-based formats are expected to book a 4.93% CAGR, driven by the adoption of grease-resistant wraps by quick-service restaurants to replace banned multilayer plastics. Brand storytelling around renewable fibers drives shopper pull, although humidity and barrier gaps still confine paper uptake to dry and secondary applications.

Momentum toward foil-based laminates remains specialized. Aluminum maintains niche relevance in pharmaceutical blister lidding and high-value dairy desserts where total oxygen and light barrier trump cost. As regional drug plants scale under import-substitution policies, metalized laminate tonnage increases, yet the overall metal share remains in single digits. Sustainability scrutiny spurs interest in ultra-thin gauge foil to reduce aluminum content without compromising shelf life, leading to collaboration between foil mills and GCC converters on downgauging initiatives.

By Product Type: Traditional Formats Meet Innovation Demands

Bags and pouches dominated the GCC flexible packaging market, accounting for 41.20% of the volume in 2025, due to their suitability for staple foods, rice, snacks, and pet care. Continuous-motion forming lines in Dammam and Dubai crank out high speeds that tame unit costs, and bottom-gusset stand-up designs deliver in-store billboard space brands crave. The format’s compatibility with reseal sliders, spouts, and laser scoring supports premiumization campaigns across edible-oil refills and liquid detergents. Sachets and stick packs, though smaller in tonnage, claim the fastest 5.22% CAGR as millennials embrace single-serve coffee, nutraceutical powders, and on-the-go condiments. Unit-dose medicine packs are also transitioning to easy-tear sticks that aid in regimen adherence. Films and wraps sustain mid-single-digit expansion on the back of export-grade meat, cheese, and industrial pallet shrink bands, with blown-film lines upgrading to five-layer configurations that dial in oxygen and moisture barriers for extended distribution.

By End-User Industry: Food Leadership with Healthcare Acceleration

The food sector holds a 32.55% market share in 2025, maintaining its position as the largest end-user segment in the GCC flexible packaging market. This dominance stems from the region's established role as a hub for food processing and export. IFFCO's USD 272 million consolidated food and beverage manufacturing facility in Dubai exemplifies this market strength, producing for more than 20 global brands with diverse packaging needs across breakfast cereals, edible oils, and processed meats. The sector's growth continues through increased exports to Asian and African markets, where flexible packaging offers logistical advantages due to its reduced weight and enhanced barrier protection. Regional packaging converters hold a competitive advantage in meeting halal certification requirements through their established supply chain networks and regulatory expertise.

The pharmaceutical and medical segment exhibits the highest growth rate, at 5.38% CAGR, driven by Saudi Arabia's USD 50.4 billion healthcare budget and the UAE's development as a pharmaceutical manufacturing hub. This segment requires advanced barrier properties, sterile packaging capabilities, and strict regulatory compliance, resulting in higher pricing and limited competition from standard packaging providers. The beverage sector experiences consistent growth, driven by increased soft drink and dairy production, while the household and personal care segments expand due to urbanization and higher consumer spending. The industrial and chemical packaging segment serves the specific needs of petrochemical products and construction materials, building on the region's established industrial infrastructure and export activities.

By Printing Technology: Digital Innovation Challenges Flexography

Flexography holds a 51.65% market share in 2025, maintaining its leadership position in the GCC flexible packaging market. This dominance results from its established infrastructure, cost advantages in high-volume production, compatibility with various substrates, and consistent quality output in FMCG applications. Digital printing shows significant momentum with a 6.08% CAGR, supported by increasing demands for customization, efficient short-run production, and variable data printing capabilities for market-specific products and promotions.

Digital printing technology has matured, overcoming previous limitations in speed and substrate compatibility, thereby expanding its application range. Taghleef Industries exemplifies this advancement through its specialized film technologies and sustainability initiatives that enhance digital printing performance. Rotogravure continues to serve high-volume, premium applications, particularly in food and beverage packaging, where superior image quality justifies higher setup costs. Offset printing serves niche applications that require exact color matching and detailed reproduction, although substrate constraints and production volume requirements limit its market presence.

Geography Analysis

Saudi Arabia captured 46.05% of 2025 spending as Vision 2030 spurred the development of factories for snacks, bakery, and pharmaceuticals, which anchor domestic demand for film and laminate rollstock. Low propane feedstock pricing from Aramco continues to underwrite competitive resin conversion economics, and the land bridge rail project trims inland freight times for finished packs moving from Gulf ports to Riyadh supermarkets. The Saudi Food and Drug Authority’s fast-track certification program reduces time-to-market for new formats, encouraging brand experimentation and larger artwork refresh cycles that stoke demand for flexible substrates.

The UAE represents the most dynamic expansion node, forecasted to post a 4.74% CAGR to 2031, as Dubai repositions itself from a re-export gateway to a finished-goods manufacturing base. Free-zone incentives and a robust cold chain enable snack, dairy, and plant-based meat startups to scale with limited capital, opting for flexible pouches over metal cans to achieve competitive price points while maintaining freshness. January 2025 single-use bans act as a catalyst, accelerating the adoption of recyclable mono-material sachets and compostable coffee capsules. Abu Dhabi’s KIZAD polymer cluster further integrates upstream resin production with downstream conversion, shaving logistics costs across the value chain.

Qatar, Kuwait, Oman, and Bahrain collectively account for a modest share, yet they benefit from regional harmonization of material standards, which allows converters to service multiple states from a single plant. QatarEnergy’s USD 6 billion ethane cracker, coming online in 2026, will inject additional low-cost PE into the supply pool, thereby softening resin volatility for converters across the peninsula. Oman’s new Duqm petrochemical complex supports the production of specialty films aimed at seafood exports, while Bahrain leverages its aluminum heritage to supply foil for regional blister packaging lines.

Competitive Landscape

The supplier base is moderately fragmented, with the five largest converters accounting for roughly 28% of the collective revenue, leaving ample whitespace for agile mid-tier players who are attuned to localized regulatory and cultural nuances. Global majors such as Huhtamaki, Amcor, and Constantia establish liaison offices and pilot lines in Jebel Ali to shorten development cycles for multinational CPG clients seeking to harmonize GCC artwork with their global brand books. Huhtamaki’s blueloop portfolio of mono-PE and paper laminates secures early orders from UAE retailers seeking to comply with plastic bans and earn sustainability credits on imported private-label items.

Regional champions like Hotpack Global and Napco National counter by touting proximity advantages, faster delivery, and fluency in halal, Arabic, and bilingual labelling protocols. Investments are tilting toward high-barrier vacuum pouches, digital presses, and solventless lamination, which reduce VOC emissions. Technology alliances play out as Taghleef Industries furnishes designed-for-recycling BOPE films, compatible with new PE recycling streams, giving partner converters a head start on achieving their post-consumer-recycled content goals. Meanwhile, Saudi government funding for advanced recycling startups is expected to feed PCR resin pipelines, creating early supply security for converters willing to trial recycled layers.

Competitive rivalry is also evident in contract packing, where beverage brands outsource to fill-and-seal specialists who can handle short-run SKUs. These packers value digital print-ready rollstock and score suppliers on lead-time discipline. As mergers like Novolex-Pactiv Evergreen reshape global capacity allocations, GCC buyers hedge risk with multi-sourcing strategies, reinforcing fragmentation rather than consolidation in the near term.

GCC Flexible Packaging Industry Leaders

Huhtamaki Oyj

Rotopacking Materials Industry Company LLC

ENPI Group LLC

Amber Packaging Industries LLC

Arabian Flexible Packaging LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sidel signed an MoU with the Saudi National Industrial Development Center to evaluate local food and beverage packaging production under Vision 2030.

- May 2025: Hotpack Global committed USD 100 million for a New Jersey plant to serve North America, extending its UAE production footprint.

- March 2025: IFFCO Group increased shareholdings following a transition with Griffith Foods, adding Saudi manufacturing sites targeting QSR and catering channels.

- December 2024: Novolex and Pactiv Evergreen announced a USD 6.7 billion merger supported by Apollo funds and CPP Investments to create a leading food and specialty packaging group.

GCC Flexible Packaging Market Report Scope

Flexible packaging is a type of packaging made from flexible materials which can be readily changed in shape. This report analyzes the factors influencing the impact of the geo-political scenarios on the studied market based on the prevalent base scenarios, key themes, and end-user vertical-related demand cycles.

The GCC flexible packaging market is segmented by material type (Plastic, Paper, Metal), by product type (Bags and Pouches, Films and Wraps and Other Product Types), by end-user industry (Food, Beverage, Pharmaceutical, and Medical, Household, and Personal care, and Other End-Use Industries), and by country (Saudi Arabia, the United Arab Emirates, Qatar, and the Rest of the GCC). The market sizes and forecasts are provided in terms of value in (USD) for all the segments.

By Material Type

| Plastic |

| Paper |

| Metal |

By Product Type

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Other Product Types |

By End-User Industry

| Food |

| Beverage |

| Pharmaceutical and Medical |

| Household and Personal Care |

| Industrial and Chemicals |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital |

| Offset |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Material Type | Plastic |

| Paper | |

| Metal | |

| By Product Type | Bags and Pouches |

| Films and Wraps | |

| Sachets and Stick Packs | |

| Other Product Types | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceutical and Medical | |

| Household and Personal Care | |

| Industrial and Chemicals | |

| By Printing Technology | Flexography |

| Rotogravure | |

| Digital | |

| Offset | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the current value of GCC flexible packaging?

The market is estimated at USD 4.93 billion in 2026 and is forecast to reach USD 6.01 billion by 2031.

Which packaging format leads demand in the Gulf?

Bags and pouches account for 41.20% of the 2025 volume, thanks to their versatility across food and personal-care categories.

How quickly is paper-based flexible packaging growing?

Paper formats are projected to show a 4.93% CAGR through 2031, outpacing other substrates as retailers seek recyclable options.

Which end-use sector is expanding the fastest?

Pharmaceutical and medical packaging is projected to post a 5.38% CAGR, driven by investments in Saudi Arabia and the UAE for drug manufacturing.

Why is digital printing gaining share?

Variable data capability and low setup costs allow brand owners to launch localized SKUs rapidly, supporting a 6.08% CAGR for digital printing.

How strict are plastic regulations in the GCC?

The UAE implemented a broad single-use ban in January 2025, and Saudi Arabia plans similar measures under Vision 2030, pressuring converters to adopt recyclable mono-material films.

Page last updated on: