Canada Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

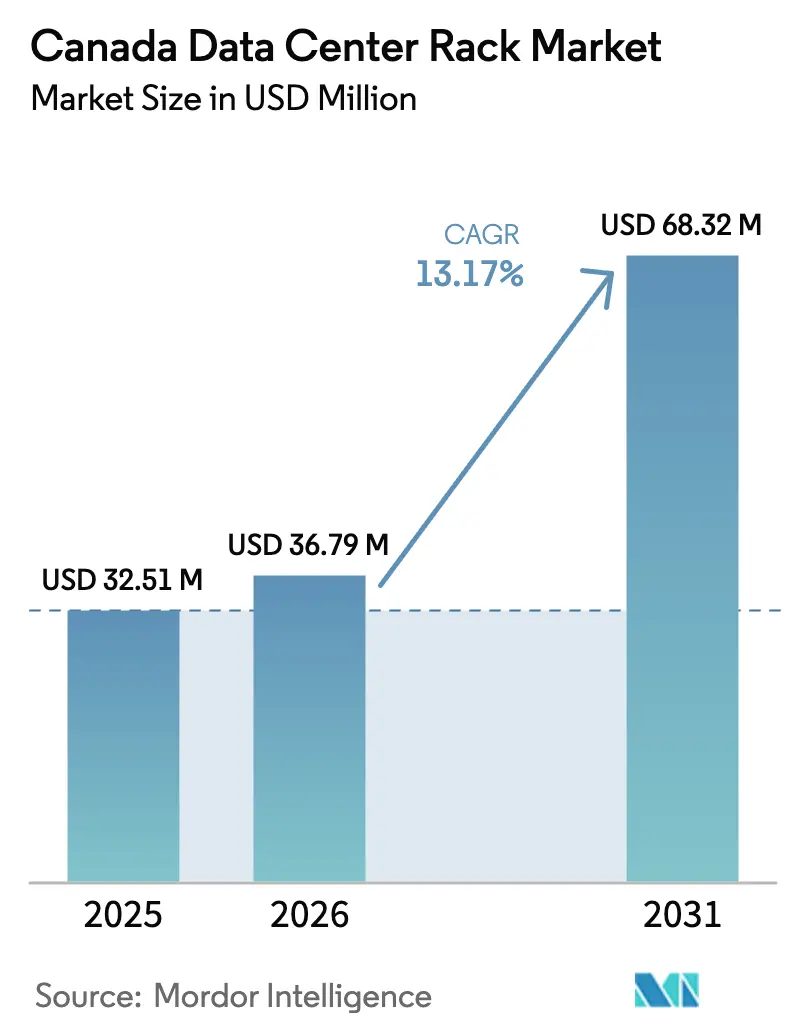

| Base Year Market Size (2025) | USD 32.51 Million |

| Market Size (2026) | USD 36.79 Million |

| Market Size (2031) | USD 68.32 Million |

| Growth Rate (2026 - 2031) | 13.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Data Center Rack Market Analysis by Mordor Intelligence

Canada data center rack market size in 2026 is estimated at USD 36.79 million, growing from 2025 value of USD 32.51 million with 2031 projections showing USD 68.32 million, growing at 13.17% CAGR over 2026-2031. Power-dense deployments above 60 kW per rack, regulatory data-sovereignty mandates and hyperscale expansion are converging to sustain double-digit growth. Canada’s colocation providers are capitalizing on provincial incentives for renewable power and on stringent privacy laws that keep workloads within national borders, while AI training clusters create fresh demand for integrated liquid-cooled racks. Rising tariffs on Chinese steel and aluminum are nudging buyers toward North American supply chains, and labor shortages for high-density commissioning are encouraging turnkey rack solutions that minimize on-site work. These dynamics collectively favor vendors capable of delivering factory-integrated, AI-ready cabinets to hyperscale and colocation sites in Toronto, Montréal, Calgary and Vancouver.

Key Report Takeaways

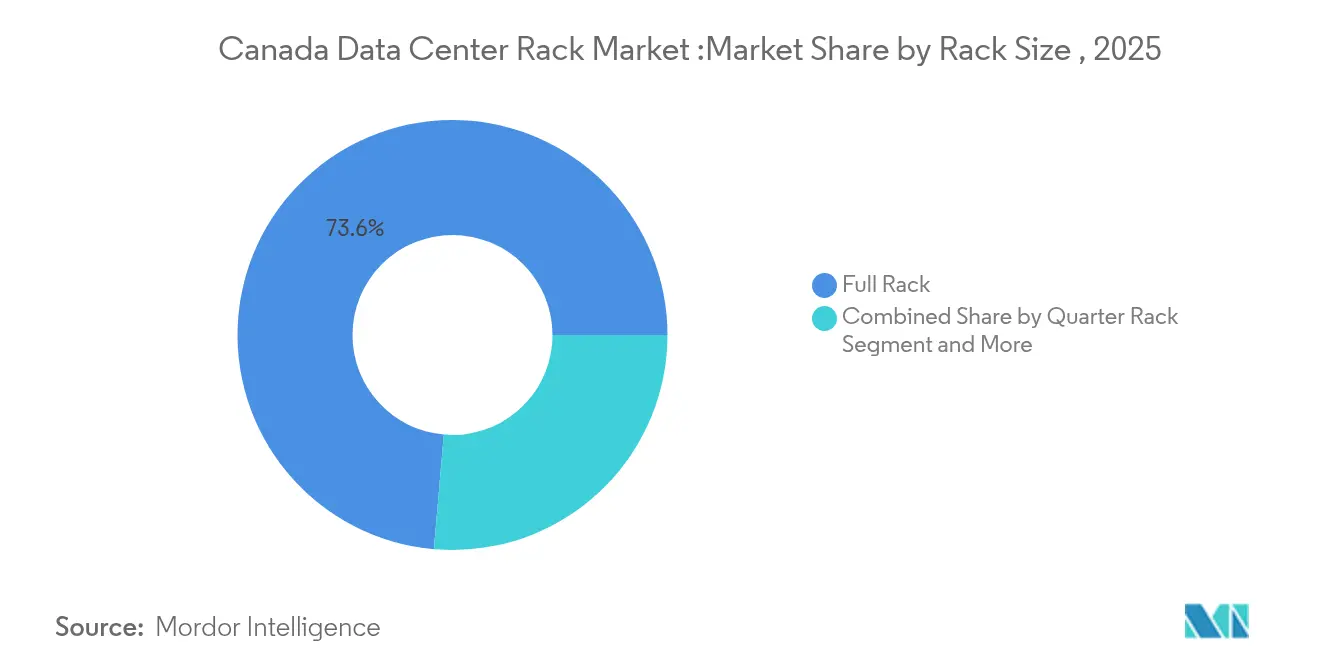

- By rack configuration, Full Rack designs held 73.62% of the Canada data center rack market share in 2025, and the segment is growing at 14.02% CAGR through 2031.

- By rack height, the 48U category is the fastest mover, expanding at 14.92% CAGR, while 42U units retain 55.98% share of the Canada data center rack market size in 2025.

- By rack type, Cabinet (Closed) models accounted for 71.05% of revenue in 2025 and are poised to rise at a 15.88% CAGR to 2031.

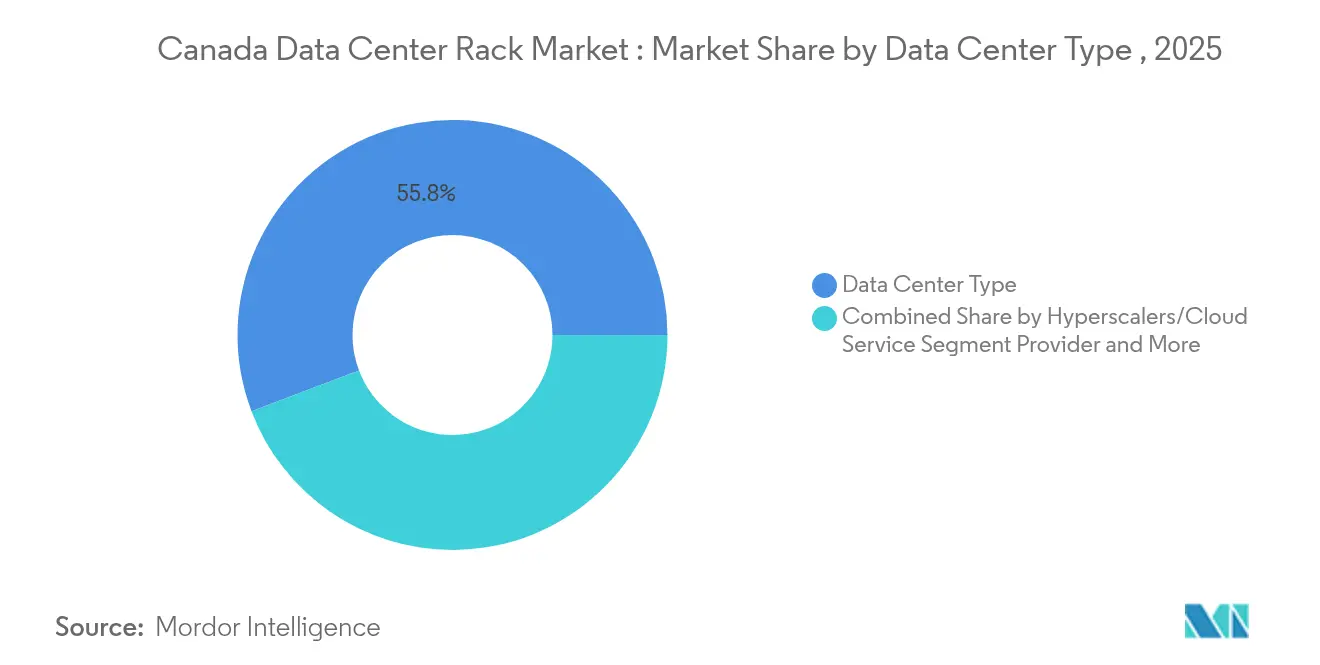

- By data-center type, Hyperscale/Cloud Service Provider deployments are advancing at 16.84% CAGR, even as Colocation Facilities captured 55.77% of the Canada data center rack market size in 2025.

- By material, Steel racks dominated with 77.66% share in 2025, but Aluminum solutions are expanding at 13.98% CAGR on the back of liquid-cooling retrofits.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

The pace and direction of global change depend on shifts occurring across countries and regions simultaneously, not within any one of them alone. The global data center rack market outlook research of Mordor Intelligence reflects this combined progression.

Canada Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first enterprise and SMB IT strategies | +2.8% | National (Toronto, Montréal, Vancouver) | Medium term (2-4 years) |

| Hyperscale and AI rack-density leap (≥60 kW/rack) | +3.2% | Alberta, Ontario, Quebec | Short term (≤ 2 years) |

| Provincial data-sovereignty mandates (PIPEDA, Bill C-27) | +2.1% | National (focus on Quebec, Ontario) | Long term (≥ 4 years) |

| Surge in colocation capacity commitments through 2027 | +2.4% | Toronto, Montréal, Calgary, Vancouver | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Enterprise and SMB IT Strategies

Canadian firms are embedding hybrid-cloud architectures that blend on-premises racks with direct links to hyperscale nodes, driving uniform 42U-48U cabinets that suit edge and core alike. The federal CAD 700 million AI Compute Challenge is accelerating adoption of GPU-dense clusters that must reside close to users for latency reasons, especially in secondary metros such as Calgary and Edmonton. SMBs are shifting capex to opex by leasing colocation racks, pushing operators to standardize heights and power distribution for quick scale-up. Major cloud providers’ metro edge programs now specify pre-certified racks that can slide into regional facilities with minimal electrical work. This convergence is underpinning steady demand for flexible, cloud-attached enclosures across the Canada data center rack market.

Hyperscale and AI Rack-Density Leap (≥60 kW/rack)

Artificial-intelligence workloads are forcing hyperscalers to exceed 100 kW—and, in pilot programs, 250 kW—per rack, a step-change from legacy 10-15 kW norms. The University of Calgary’s CCIT hall already operates 20 cabinets totaling 600 kW with integrated rear-door heat exchangers. Hyperscalers are ordering custom frames that marry liquid distribution units, busbar power trunks and structural reinforcement in a single bill of materials, slashing floor-space per petaflop. Vendors able to factory-install manifolds and quick-disconnect lines are winning contracts because they shorten on-site commissioning. As AI density rises, cabinet strength and fire suppression systems must also evolve, spawning retrofit opportunities for seismic-rated, high-load frames in existing Canadian halls.

Provincial Data-Sovereignty Mandates (PIPEDA, Bill C-27)

Bill C-27 and the proposed Artificial Intelligence and Data Act impose strict residency rules for personal data, spurring banks and hospitals to favor domestic hosting.[2]Government of Canada, “Bill C-27: Digital Charter Implementation Act,” canada.ca Quebec’s Act 25 adds provincial layers that restrict cross-border transfers in sectors like fintech and life sciences. These requirements channel workloads into compliant facilities, creating a captive market for racks inside Canadian borders. Public agencies are embedding residency clauses in procurement, locking in long-term demand for regional colocation suites equipped with tamper-proof cabinets and audit-ready monitoring. As regulators finalize enforcement frameworks, operators expect a multi-year uplift in AI-ready, compliance-certified rack orders across the Canada data center rack market.

Surge in Colocation Capacity Commitments Through 2027

Vacancy below 4% in Toronto and Montréal has triggered a build-boom: eStruxture’s eight-site Aptum purchase pushes its footprint past 100 MW, while its Calgary AI campus is budgeted at CAD 750 million for 130 kW per rack formats . Grain Management’s Brampton expansion from 2.5 MW to 20 MW illustrates how metro Toronto sites are scaling by an order of magnitude. Developers want standardized cabinets, PDUs and containment that can ship in modules for multi-site rollouts. Suppliers offering bundled rack-power-cooling kits are securing multiyear frame agreements that anchor recurring revenue in the Canada data center rack market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of 10-20 MW power parcels in Toronto core | -1.9% | Greater Toronto Area | Short term (≤ 2 years) |

| Lengthy provincial permitting for water-based cooling loops | -1.2% | Ontario, Quebec, Alberta | Medium term (2-4 years) |

| Skilled-labour gap for high-density rack commissioning | -0.8% | National (Calgary, Vancouver) | Long term (≥ 4 years) |

| Steel/aluminum import tariffs driving rack CAPEX volatility | -1.1% | National (manufacturing in Ontario) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of 10-20 MW Power Parcels in Toronto Core

The Independent Electricity System Operator warns that securing substation access in downtown Toronto now entails multi-year queue positions. Hyperscalers are splitting loads into clusters across Mississauga and Hamilton, increasing the count of smaller halls rather than one big farm. Each site needs identical racks to simplify logistics, benefiting vendors of pre-engineered cabinets that deploy anywhere on short notice. Power scarcity also propels edge micro-data-centers that fit within existing retail and office footprints, again boosting orders for compact enclosed racks in the Canada data center rack market.

Steel/Aluminum Import Tariffs Driving Rack CAPEX Volatility

Canada’s 25% surtax on Chinese metals adds unpredictable cost swings to rack bills of material.[3]Department of Finance Canada, “Countermeasures on Imports of Steel and Aluminum Products,” canada.ca OEMs are dual-sourcing panels from USMCA mills, but conversion lines must re-tool for alternative alloys, stretching lead-times. Aluminum cabinets—lighter and more thermally conductive—offset shipping and cooling costs, partially neutralizing tariff headwinds, yet price indexing in colocation contracts is rising. Suppliers with domestic sheet-metal fabs are locking in volumes, while buyers hedge with forward-purchased inventory, affecting working capital across the Canada data center rack market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Full Rack Dominance Driven by AI Workloads

Full Rack units commanded 73.62% of revenue in 2025 and will grow 14.02% annually as AI clusters require full-height frames with integrated manifolds. This dominance places Full Rack formats at the core of the Canada data center rack market size discussion, especially when hyperscalers standardize on 48U full cabinets that deliver consistent airflow and power anchoring. Quarter and Half Rack offerings remain relevant for edge closets but contribute marginal revenue compared with AI-dense cores.

Most hyperscale requests for proposal now bundle racks, rear-door heat exchangers and busbar distribution as a single SKU. Colocation operators mirror this design to accommodate unknown future tenants. Suppliers achieving economies of scale around full-size frames are improving margins even while raw-material prices fluctuate, reinforcing the competitive moat in the Canada data center rack market.

By Rack Height: 48U Emerging as AI-Optimized Standard

Though 42U cabinets hold 55.98% of 2025 revenue, 48U units are accelerating at 14.92% CAGR and are forecast to capture a sizable share of the Canada data center rack market size by 2031. The extra six rack units accommodate in-row pump skids and overhead busways without sacrificing server count.

Operators deploying NVIDIA H100 and forthcoming B100 accelerators often choose 48U to house both compute nodes and coolant distribution in one enclosure. With liquid loops rising, 48U allocations future-proof floorspace while avoiding custom height extensions that complicate containment design. Compact 38U and 52U specials continue to support telecom or seismic zones, yet bulk demand is clustering around the two mainstream heights, helping integrators streamline part numbers and logistics.

By Rack Type: Cabinet Solutions Lead Cooling Integration

Cabinet (Closed) frames captured 71.05% of 2025 spending and will outpace the broader Canada data center rack market at 15.88% CAGR. Enclosed sides allow direct-to-chip circuits and rear-door heat exchangers to run safely, preventing condensation in aisles.

Large colocation providers are layering biometric doors and branch-circuit monitoring into sealed cabinets, selling them as premium “AI suites.” Open-frame racks still serve network corridors where airflow is king and security is less stringent, but their share is eroding as more workloads become power-intensive. Wall-mount enclosures address 5G edge shelters and industrial IoT nodes, yet remain a niche use case relative to sealed cabinets.

By Data Center Type: Hyperscale Growth Outpaces Traditional Segments

Colocation halls led revenue with 55.77% of the Canada data center rack market size in 2025, yet Hyperscale/Cloud deployments are sprinting ahead at 16.84% CAGR. Hyperscalers demand integrated liquid-cool-ready frames that drop into robot-assisted loading bays.

Colos are countering by offering dedicated AI halls, requiring the same specialized cabinets. Enterprise on-prem still matters in regulated verticals like healthcare, but spending tilts toward hybrid racks hosting both private GPUs and cloud-link routers. Edge micro-sites in retail or cell-tower compounds prioritize lightweight, pre-cabled racks sized for elevator transport.

By Material: Aluminum Gains Traction in High-Density Applications

Steel still rules with 77.66% share, but Aluminum is climbing at 13.98% CAGR as operators value lower weight when floors must support 130 kW cabinets. The Canada data center rack market share shift toward Aluminum matches the switch to liquid cooling, where thermal conductivity improves exchanger efficiency.

Vendors investing in aluminum welding lines are shortening lead-times because the metal machines faster than cold-rolled steel. Composite racks serving electromagnetic-sensitive labs remain tiny yet profitable, signaling future diversification possibilities if AI inference expands into healthcare imaging suites and autonomous-vehicle test rigs.

Geography Analysis

Ontario remains the largest provincial buyer thanks to Toronto’s finance and tech demand, but grid congestion has lengthened interconnection queues and raised power costs, nudging capacity into Hamilton and Kitchener. Québec’s hydroelectric surplus and renewable portfolio attract hyperscalers seeking ESG credentials; Hydro-Québec’s unlock of additional industrial rates is spurring multi-hundred-megawatt campuses near Montréal.

Alberta is the fastest-growing node in the Canada data center rack market, leveraging deregulated power and abundant natural gas to entice CAD 75-100 billion in planned data-center capital by 2030. eStruxture’s Calgary campus typifies 130 kW racks cooled by rear-door exchangers, showcasing how local energy expertise translates into data-center engineering. Edmonton’s emerging AI health-research corridor is also driving regional rack orders.

British Columbia leverages hydro assets and Pacific fiber routes to pitch itself as a low-latency CDN hub; racks here often integrate seismic bracing and liquid loops suited for temperate diets. The Maritime provinces court edge workloads linked to offshore wind projects, requiring compact enclosures that withstand salt air. Nationwide, the Canada data center rack market sees policy differences on water-loop permits and clean-energy credits, compelling suppliers to customize cabinet ancillaries by province.

Mordor Intelligence examines the data center rack market across diverse other regional markets as well, including North America, Africa, and Middle East, while also offering granular country-level perspectives for Brazil, United States, Nigeria, Saudi Arabia, Mexico, and Belgium and more.

Competitive Landscape

Global OEMs control the top tier, yet the field stays moderately fragmented as local metal-fabrication shops protect regional accounts. Schneider Electric’s EUR 38 billion 2024 turnover included 24% from data-center buyers, and its Motivair acquisition cements liquid-cooling depth.[1]Schneider Electric, “Q1 2025 Revenues,” se.com Vertiv printed USD 8.0 billion in 2024 sales and entered 2025 with a USD 7.9 billion backlog after sealing AI-platform alliances. Eaton’s USD 1.4 billion Fibrebond purchase extends from power gear to enclosures, giving it cradle-to-grave supply for hyperscale bids.

Competitive differentiation now hinges on turnkey delivery—factory-cabled racks, coolant loops, smart PDUs and DCIM sensors shipped as one crate. Players with domestic sheet-metal mills dodge tariff exposure and shorten lead-times, winning colocation rollouts that demand 300-cabinet drops inside three weeks. Regional fabricators lacking cooling know-how risk relegation to build-to-print orders.

Vendor roadmaps converge on Open Compute Project-compatible frames to woo hyperscale giants, alongside AI-ready cabinets that integrate leak-detection, micro-channel plates and structured cabling. Compliance modules for Bill C-27 record-keeping and ESG scoring provide further stickiness. M&A remains likely among mid-range players seeking scale, especially those with limited aluminum tooling.

Canada Data Center Rack Industry Leaders

Rittal GMBH & Co.KG

Schneider Electric SE

Vertiv Group Corp.

Eaton Corporation plc

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Schneider Electric posted EUR 9.3 billion Q1 revenue, up 15.2% in North America, and closed the Motivair buy to deepen liquid-cooling know-how

- April 2025: Vertiv logged USD 2.036 billion Q1 sales, 24% higher year-over-year, raising full-year guidance by USD 250 million as AI orders surged

- March 2025: Eaton finalized its USD 1.4 billion Fibrebond acquisition, adding enclosure fabrication to its power portfolio

- March 2025: eStruxture began a 55H Brampton expansion from 2.5 MW to 20 MW, engineering racks for 130 kW AI loads

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Canada data center rack market as revenue generated from new, factory-built enclosures, quarter, half, and full cabinets, as well as open-frame and wall-mount formats, used inside colocation, hyperscale, enterprise, and edge data centers across the country. Each unit must house IT, power, and networking equipment and meet ANSI/EIA-310-E compliance.

Telecom street-side cabinets, pure server chassis, and refurbished racks are excluded from our sizing.

Segmentation Overview

- By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

- By Rack Height

- 42U

- 45U

- 48U

- Other Heights (?52U and Custom)

- By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

- By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

- By Material

- Steel

- Aluminum

- Other Alloys and Composites

Detailed Research Methodology and Data Validation

Primary Research

Conversations with facility engineers, colocation procurement heads, and rack OEM product managers across Ontario, Quebec, Alberta, and British Columbia refined utilization ratios, average selling prices, and height preference shifts. Short e-surveys with cloud architects validated forecast assumptions on power density and aluminum adoption.

Desk Research

We began with public datasets from Statistics Canada, the Canada Border Services Agency import ledger, and Natural Resources Canada's electricity price dashboards, which helped estimate rack demand drivers and operating costs. Industry association briefs from the Canadian Data Center Association, Uptime Institute outage logs, and patent filings accessed via Questel traced technology adoption curves. Company 10-Ks, SEDAR filings, and reputable press such as The Globe and Mail supplied spend plans of key operators. Our analysts also pulled facility counts and MW adds from D&B Hoovers and Dow Jones Factiva news archives. The sources mentioned are illustrative; many additional references informed our desk work.

Market-Sizing & Forecasting

A top-down reconstruction converts installed and planned IT load (MW) into rack slots using verified density bands before multiplying by blended ASPs. Selective bottom-up checks, supplier roll-ups and channel pricing audits, tighten totals. Key variables include data-center MW additions, average rack power (kW), 42U versus 48U mix, steel-to-aluminum shift, and hyperscale share gains. A multivariate regression, supported by ARIMA smoothing for macro shocks, projects each driver through 2030, after which results are aligned to expert consensus and adjusted for currency movements.

Data Validation & Update Cycle

Outputs pass automated variance scans, peer review, and senior sign-off. We refresh models annually and trigger interim updates when new build announcements, tariff changes, or component price swings exceed predefined thresholds.

Why Mordor's Canada Data Center Rack Baseline Earns Trust

Published market values often diverge because firms choose different product scopes, base years, and conversion factors. Our disciplined selection of rack-only revenue, Canada-specific facility counts, and an annually refreshed model narrows those gaps for decision makers.

Key gap drivers include competitors bundling telecom enclosures, applying shipment-based estimates without local density checks, or using static ASPs despite metal cost swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 32.51 million (2025) | Mordor Intelligence | - |

| USD 164.5 million (2023) | Regional Consultancy A | Includes smaller telecom and broadcast cabinets, older base year, no power-density adjustment |

| USD 1.24 billion (2024) | Global Consultancy B | Bundles enterprise server rooms and accessory rails, shipment extrapolation replaces facility counts |

| USD 300 million (2023) | Industry Portal C | Uses high ASP from retail quotations, mixes cabinets with outdoor telecom racks |

In summary, Mordor Intelligence delivers a balanced, transparent baseline grounded in facility data, validated prices, and repeatable steps, giving stakeholders a dependable view of Canada's data center rack opportunity.

Key Questions Answered in the Report

What is the current size of the Canada data center rack market?

The market is valued at USD 36.79 million in 2026 and is on track to hit USD 68.32 million by 2031.

Which rack configuration leads Canadian demand?

Full Rack units dominate with 73.62% market share in 2025 thanks to AI workloads requiring full-height, high-density cabinets

Why are 48U racks gaining popularity?

They provide extra vertical space for liquid-cooling manifolds and power gear, supporting densities above 60 kW per rack while future-proofing new builds.

How do data-sovereignty laws influence rack purchases?

Bill C-27 and provincial privacy acts force sensitive datasets to stay in Canada, driving domestic colocation spending and boosting demand for compliant racks.

Page last updated on: