Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.09 Billion |

| Market Size (2026) | USD 6.34 Billion |

| Market Size (2031) | USD 7.72 Billion |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

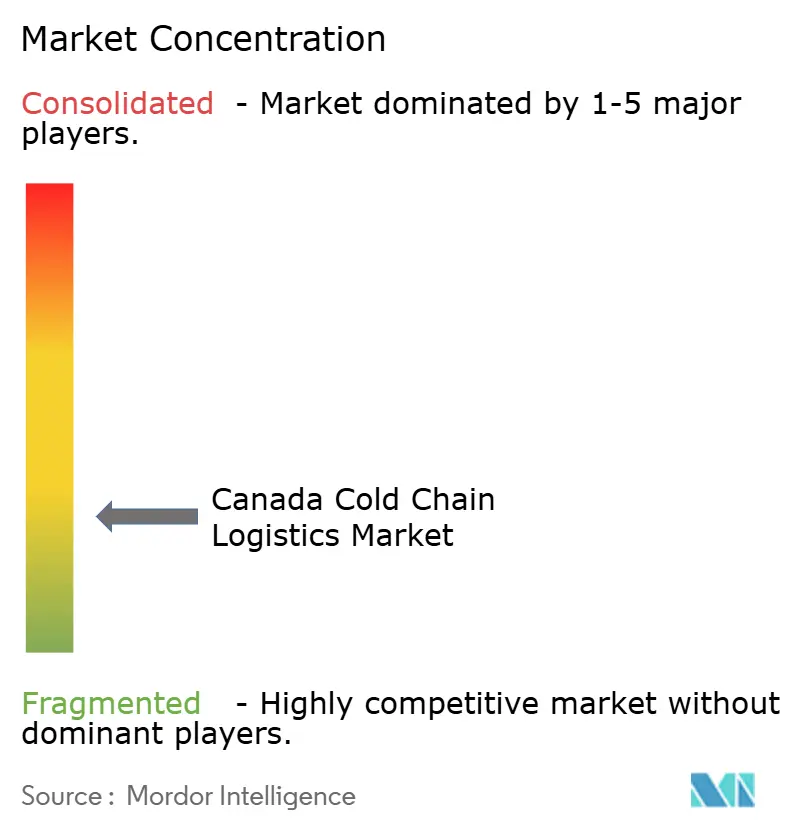

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Cold Chain Logistics Market Analysis by Mordor Intelligence

The Canada Cold Chain Logistics Market size was valued at USD 6.09 billion in 2025 and estimated to grow from USD 6.34 billion in 2026 to reach USD 7.72 billion by 2031, at a CAGR of 4.03% during the forecast period (2026-2031).

The expansion underscores how federal infrastructure funding, refrigerant-phase-down mandates, and biomanufacturing investments are re-shaping temperature-controlled supply chains. Digital visibility projects funded by Transport Canada are easing chronic pinch points, while the Kigali-driven transition to low-GWP refrigerants is prompting accelerated equipment upgrades[1]Transport Canada, “Government of Canada invests in digital infrastructure projects across Canada,” canada.ca. Strategic rail-port enhancements under the National Trade Corridors Fund are supporting long-haul export flows, and rising biologics output is shifting demand toward ultra-low-temperature solutions.

Key Report Takeaways

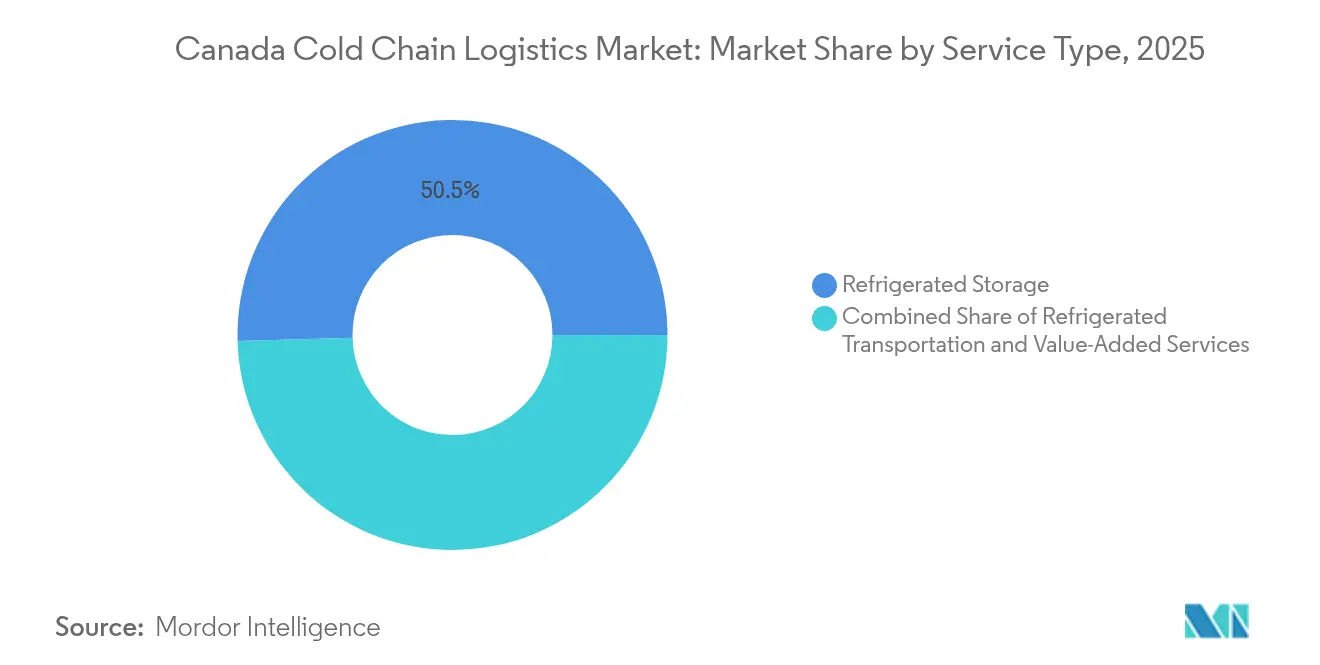

- By service type, Refrigerated Storage held 50.45% of the Canada cold chain logistics market share in 2025 and Value-Added Services is on track for a 4.06% CAGR through 2031.

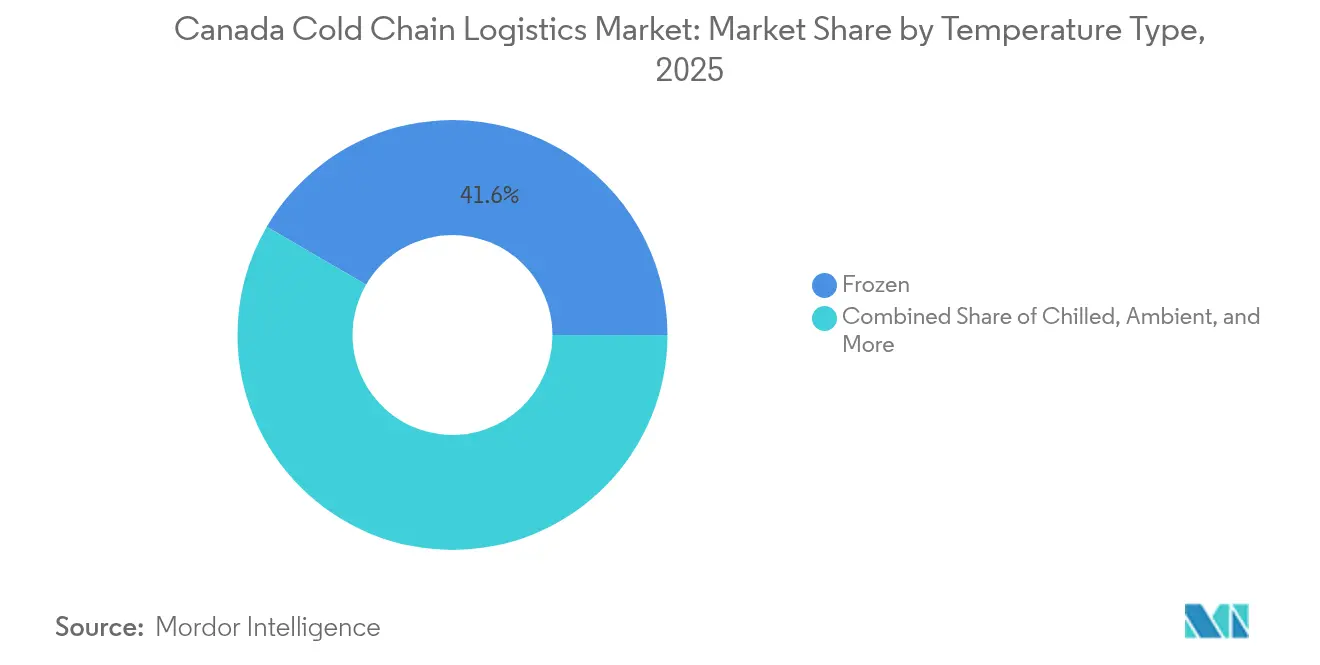

- By temperature band, Frozen applications represented 41.60% of the Canada cold chain logistics market size in 2025, while Ambient logistics is forecast to grow at a 4.41% CAGR.

- By application, Meat & Poultry captured 21.70% of the Canada cold chain logistics market size in 2025 and Pharmaceuticals & Biologics is projected to expand at a 4.98% CAGR to 2031.

- By region, Central Canada led with 30.65% of the Canada cold chain logistics market share in 2025, whereas the North region is projected to record the fastest 4.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for perishable foods & pharma | +1.2% | Central Canada, West Coast | Medium term (2-4 years) |

| Federal Trade-Corridor Infrastructure Expansion | +0.8% | Atlantic & Prairie corridors | Long term (≥ 4 years) |

| Biomanufacturing & life-sciences demand surge | +0.9% | Central Canada, West Coast | Medium term (2-4 years) |

| Agri-food export growth to U.S. & Asia | +0.7% | Prairie Provinces & West Coast | Long term (≥ 4 years) |

| Mandatory low-GWP refrigerant policies | +0.4% | National, fastest in large urban centers | Short term (≤ 2 years) |

| National supply-chain digital visibility push | +0.3% | Pilot programs in major ports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Perishable Foods & Pharma

Consumer preference for fresh meal kits and the rise of biologics are creating simultaneous pressures on warehousing and last-mile capabilities. OmniaBio’s USD 428 million Hamilton CDMO facility exemplifies how advanced therapies are pushing for tighter temperature bands and validated monitoring[2]Invest Ontario, “OmniaBio: Road to Canada's largest cell and gene therapy CDMO,” investontario.ca. Metro’s USD 738 million automated fresh network in Toronto highlights grocery e-commerce’s need for rapid throughput. Stricter GUI-0069 rules now require continuous data logging, favoring providers that already operate integrated IoT systems.

Federal Trade-Corridor Infrastructure Expansion (NTCF)

NTCF grants totaling more than USD 3 billion over the past 7 years are widening rail loops, dredging Atlantic berths, and digitizing yard operations to slash container dwell times[3]Transport Canada, "Projects funded by the National Trade Corridors Fund," tc.canada.ca. A USD 18.5 million Halifax upgrade will allow larger reefer volumes, positioning the port as an eastern gateway. Parallel rail bypass projects shorten transit between Québec and the Prairies, improving schedule integrity for chilled meat exports. Climate-resilient designs reduce outage risk during winter storms, cutting spoilage incidents.

Biomanufacturing & Life-Sciences Cold-Chain Demand Surge

Moderna’s Laval mRNA site and a new British Columbia cell-therapy plant underscore a shift from import reliance to domestic production[4]Government of Canada, "Government of Canada announces major milestone in the Canadian biomanufacturing sector, " canada.ca. Personalized medicines require −80 °C to −20 °C shipping lanes and validated packaging, opening premium revenue streams for certified 3PLs. UPS’s USD 1.6 billion purchase of Andlauer Healthcare Group signals the strategic weight of Canada’s pharma corridors. CEIV-Pharma hubs at Toronto Pearson now anchor global lanes for clinical shipments.

Agri-food Export Growth to U.S. & Asia

Indo-Pacific shipments of canola, wheat, and pulses touched USD 16.2 billion in 2024 and continue to rise. Bilateral pacts such as CPTPP grant duty-free access yet maintain stringent temperature-document requirements, rewarding operators with integrated traceability. New Cold’s USD 74 million automated warehouse in Alberta demonstrates how robotics is tackling prairie seasonality. Rail-ocean solutions trim dwell times on Vancouver berths, keeping quality intact for protein exports bound for Korea and Japan.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy & infrastructure CAPEX | −0.6% | Nationwide, most acute in the North | Long term (≥ 4 years) |

| Refrigerated-truck & warehouse labor gap | −0.5% | Urban centers | Medium term (2-4 years) |

| Northern grid-reliability disruptions | −0.3% | Remote territories | Long term (≥ 4 years) |

| HFC phase-out retrofit burden | −0.2% | Jurisdictions with early enforcement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy & Infrastructure CAPEX

Automated cold stores often exceed USD 500 per cubic meter to build, making financing a hurdle for smaller operators. Dematic’s Quebec facility shows how advanced shuttle systems can collapse pick times but require heavy upfront outlays. Although tax rebates exist for natural refrigerants, returns accrue over long payback cycles. Provinces with abundant hydroelectricity give operators up to 25% power-cost advantage, steering site-selection decisions.

Refrigerated-Truck & Warehouse Labor Shortage

Transport Canada projected a 10,000-driver shortfall in 2025 for specialized reefer lanes. Additional food-safety certifications lengthen training, raising turnover risk. Stevens Company’s AutoStore installation boosted unit-per-hour metrics fivefold, cushioning staffing gaps. Immigration fast tracks mitigate driver deficits but cannot yet fill technician roles needed for CO₂ and ammonia systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Storage Infrastructure Drives Market Foundation

Refrigerated Storage accounted for a 50.45% Canada cold chain logistics market share in 2025 by value and forms the backbone for buffer stock strategies. The segment anchors omnichannel grocery fulfillment, enabling consolidation of multi-temperature SKUs before last-mile dispatch. Energy-efficient rack designs, automation, and solar-paired ammonia systems are lowering variable costs, letting large providers scale nationwide contracts. In contrast, Value-Added Services—ranging from re-packing to kitting—are growing at a projected 4.06% CAGR, reflecting shipper appetite for one-stop outsourcing. Cross-docking and blast-freezing clusters near rail ramps shorten dwell times for export cargo.

Refrigerated Transportation adds resiliency across road, rail, air, and ocean lanes. Road still dominates e-grocery delivery windows under 24 hours, but CPKC’s north-south rail with Americold creates lower-carbon alternatives for Prairie protein flows to Mexico. Air Canada Cargo’s CEIV-certified network covers 100 destinations, opening premium lanes for high-value biologics. Ocean carriers leveraging green corridors in Halifax support seafood exporters seeking direct links to Europe.

By Temperature Type: Frozen Dominance Meets Ambient Innovation

Frozen goods held 41.60% of 2025 revenue, reflecting stable demand for proteins, ice cream, and long-haul pharma. Facilities commonly maintain −18 °C zones with automated pallet shuttles, maximizing cubic utilization. Yet the Ambient band—often +15 °C to +25 °C—will grow at 4.41% CAGR as direct-to-consumer meal kits and temperature-sensitive tablets rise. Variable-speed compressors paired with AI predictive analytics allow warehouses to toggle set-points, trimming electricity by up to 12%.

Chilled (0-5 °C) remains crucial for dairy, produce, and meal replacements. Ultra-low zones of −80 °C are expanding within biomanufacturing clusters, employing redundant LN₂ back-ups that comply with GUI-0069. Operators increasingly integrate multiple zones under one roof, optimizing throughput while cutting capital duplication.

By Application: Protein Leadership Faces Pharmaceutical Disruption

Meat & Poultry retained a 21.70% revenue share in 2025, underpinned by steady U.S. and Asian export contracts and well-established HACCP workflows. Automated deboning plants near the border allow rapid blast-freeze cycles, safeguarding product integrity during 2-day rail hauls. Pharmaceuticals & Biologics, however, is set for a 4.98% CAGR as domestic vaccine output and personalized therapies mushroom. CEIV-Pharma certifications provide competitive moats, commanding premium yields.

Dairy & Frozen Desserts gain from price-sensitive consumers opting for private-label ice cream lines. Fish & Seafood leverages Atlantic and Pacific harvests, with live lobster shipments benefiting from Halifax’s expedited reefer lanes. Fruits & Vegetables rely on controlled-atmosphere storage that extends shelf life by up to 30 days. Ready-to-Eat meals ride convenience trends and thrive on blast chilling techniques that retain flavor. Vaccine and clinical-trial consignments account for a smaller volume but generate outsized margins due to rigorous validation needs.

Geography Analysis

Central Canada’s dominance reflects integrated highways, five Class I railways, and cross-dock corridors that compress lead times to the U.S. Midwest. Montréal and Toronto host CEIV-Pharma gateways, funneling outbound biologics. Urban grocery e-commerce drives micro-fulfillment centers with ambient and chilled “dark” stores that cut delivery times to two hours. Robust intermodal nodes reduce empty miles and greenhouse-gas intensity, making Central Canada the anchor of national cold chains.

Prairie Provinces deliver scale efficiencies for durum, canola, and pork. Regina and Saskatoon consolidate chilled and frozen loads headed west through CPKC tunnels. Alberta’s cold-chain automation demonstrates how robotics can solve labor scarcity in rural hubs. The North faces energy and transport constraints, yet strategic food security programs are installing modular blast chiller units in Nunavut hubs. Seasonal ice-road closures necessitate higher on-site storage buffers, underpinning growth despite high kWh costs.

Competitive Landscape

Market concentration is fragmented, while regional specialists retain niche strengths. Lineage’s USD 221 million ColdPoint purchase added deep-frozen capacity near Montréal, signaling continued consolidation. Americold’s alliance with CPKC integrates cross-border reefer rail, yielding cost advantages for Prairie producers. Canada Cartage’s Coastal Pacific Xpress buyout extends FTL and LTL refrigerated reach from British Columbia to Ontario.

Technology remains the competitive fulcrum. Operators adopt IoT sensors, AI route planning, and blockchain traceability to win pharmaceutical contracts. Automation slashes labor costs, with AutoStore cube-storage delivering fivefold productivity lifts. CEIV-Pharma certification and Health Canada compliance act as entry barriers, protecting incumbent margins.

White-space opportunities lie in last-mile e-grocery, clinical-trial logistics, and sub-zero biologics. New entrants leverage asset-light, tech-heavy models, yet capital intensity and regulatory scrutiny favor established fleets. Overall, partnerships between logistics giants and life sciences firms continue to craft vertically integrated offerings.

Canada Cold Chain Logistics Industry Leaders

-

Americold Logistics

-

Lineage Logistics

-

Congebec Logistics

-

Conestoga Cold Storage

-

Trenton Cold Storage

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Lineage acquired three Québec cold stores near Montréal, expanding its Canadian footprint.

- January 2025: Canada Cartage bought Coastal Pacific Xpress, creating national temperature-sensitive transport capacity.

- June 2024: DSV partnered with UNICEF to enhance global emergency supply chains.

- February 2024: Dematic and Groupe Robert opened a fully automated Quebec cold store, lifting throughput and energy efficiency.

Canada Cold Chain Logistics Market Report Scope

The technology and mechanism that allows for the secure delivery of temperature-sensitive goods and items along the supply chain are known as cold chain logistics. Any product that is perishable or is branded as such would almost certainly need cold chain management. Foods including meat and fish, produce, medical supplies, and pharmaceuticals could all fall under this category.

The Canadian Cold Chain Logistics Market is segmented by Service (Storage, Transportation, and Value-added Services), by Temperature Type (Chilled, Frozen, and Ambient), and by End User (Horticulture, Dairy Products, Meats, Fish, Poultry, Processed Food Products, Pharma, Life Sciences, and Chemicals, and Other Applications). A comprehensive background analysis of the Canadian Cold Chain Logistics Market covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry. The report offers the market size and forecasts in values (USD billion) for all the above segments.

By Service Type

| Refrigerated Storage | Public Warehousing |

| Private Warehousing | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

By Application

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Perishables |

By Region

| Atlantic region |

| Central Canada |

| Prairie Provinces |

| West Coast |

| North |

| By Service Type | Refrigerated Storage | Public Warehousing |

| Private Warehousing | ||

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0–5 °C) | |

| Frozen (-18–0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits & Vegetables | |

| Meat & Poultry | ||

| Fish & Seafood | ||

| Dairy & Frozen Desserts | ||

| Bakery & Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals & Biologics | ||

| Vaccines & Clinical Trial Materials | ||

| Chemicals & Specialty Materials | ||

| Other Perishables | ||

| By Region | Atlantic region | |

| Central Canada | ||

| Prairie Provinces | ||

| West Coast | ||

| North | ||

Key Questions Answered in the Report

How large is the Canada cold chain logistics market in 2026?

It stands at USD 6.34 billion and is projected to reach USD 7.72 billion by 2031.

Which service type holds the largest share?

Refrigerated Storage leads with 50.45% of 2025 revenue, reflecting the capital-intensive nature of warehousing.

What segment is growing fastest by application?

Pharmaceuticals & Biologics will advance at a 4.98% CAGR through 2031, fueled by domestic biomanufacturing expansion.

Which region records the highest growth?

The North shows a 4.32% CAGR outlook thanks to resource projects and food-security programs.

How are refrigerant regulations affecting operators?

The Kigali-aligned HFC phase-down is driving accelerated equipment retrofits and favoring firms with natural-refrigerant expertise.

Page last updated on: