Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 28.29 Billion |

| Market Size (2026) | USD 29.31 Billion |

| Market Size (2031) | USD 34.95 Billion |

| Growth Rate (2026 - 2031) | 3.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Office Real Estate Market Analysis by Mordor Intelligence

The Canada Office Real Estate Market size is expected to grow from USD 28.29 billion in 2025 to USD 29.31 billion in 2026 and is forecast to reach USD 34.95 billion by 2031 at 3.60% CAGR over 2026-2031. A widening gulf has emerged between premium towers that enjoy healthy absorption and legacy properties whose vacancies remain stubbornly high. Demand is strongest for Grade A assets as employers seek modern air systems, robust digital connectivity, and green credentials that help attract talent and satisfy ESG auditors. Technology, finance, and professional-services tenants account for the bulk of net absorption, pushing landlords to retrofit or reposition older stock. Meanwhile, monetary easing by the Bank of Canada supports refinancing and selective acquisitions even as construction-cost inflation curbs new supply.

Key Report Takeaways

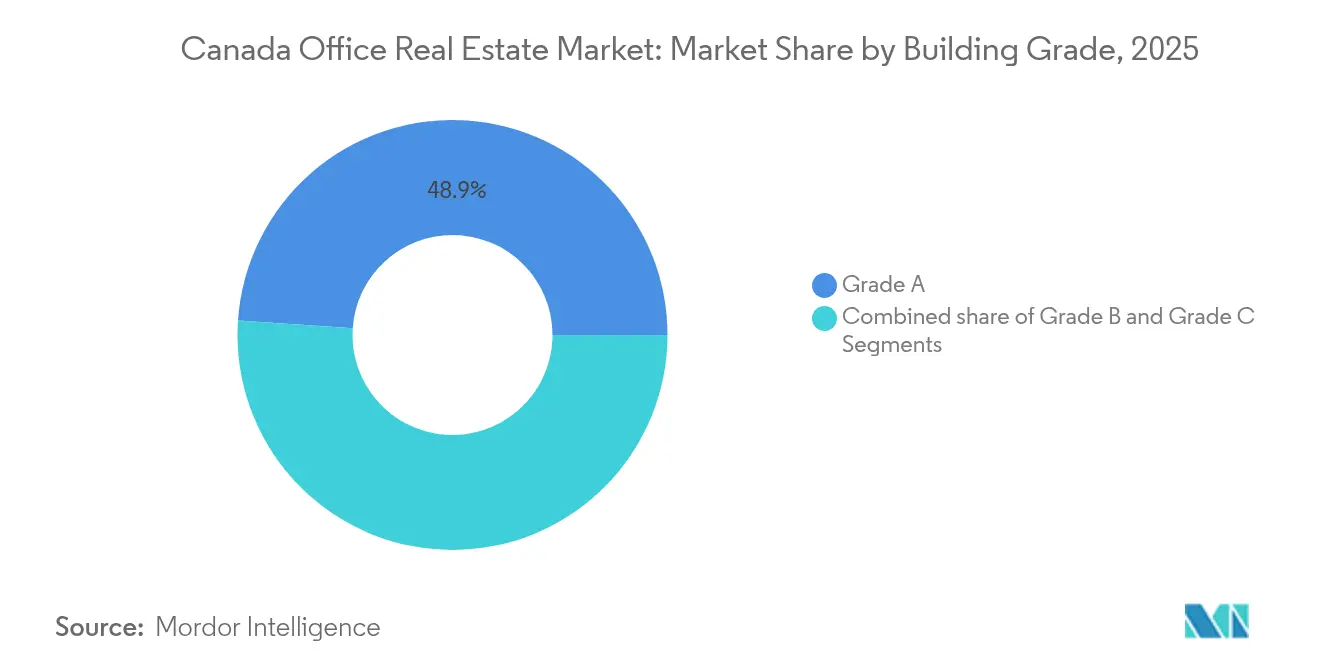

- By building grade, Grade A offices led with 48.92% of the Canada office real estate market share in 2025, while Grade A is set to expand at a 3.98% CAGR through 2031.

- By transaction type, rentals accounted for 68.52% of the Canada office real estate market size in 2025; sales transactions post the fastest growth at a 4.05% CAGR to 2031.

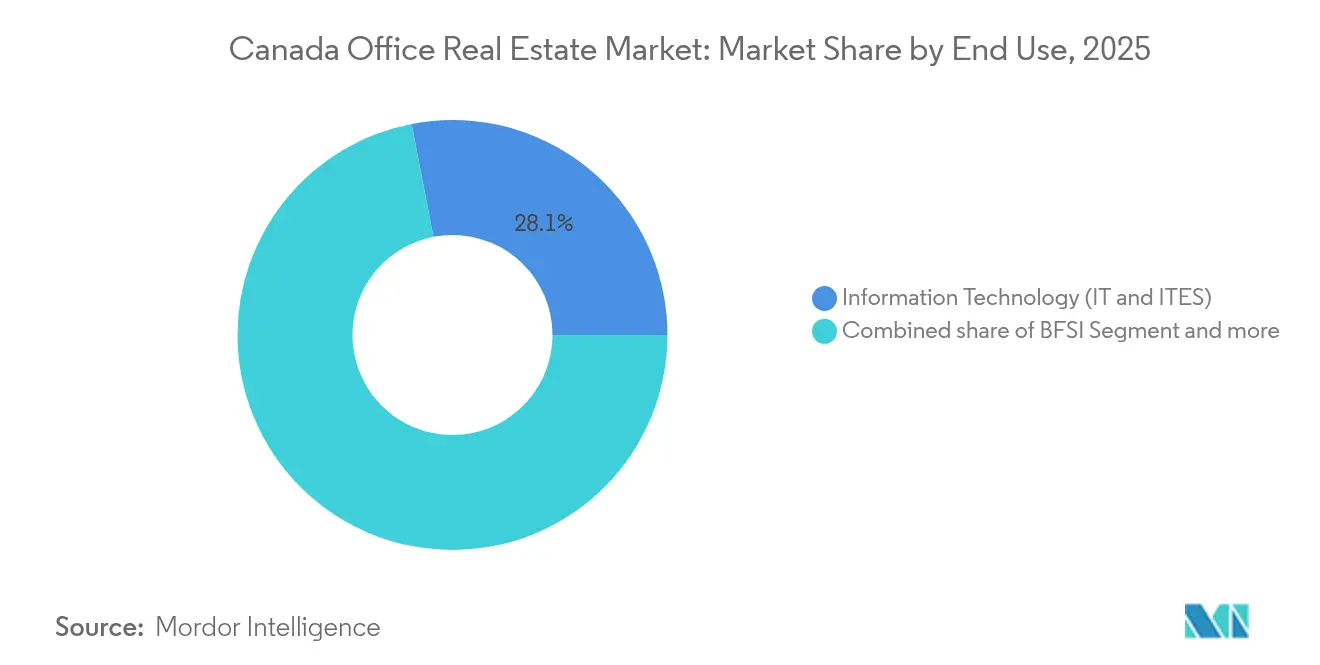

- By end use, information technology and IT-enabled services captured a 28.05% share of the Canada office real estate market size in 2025 and are forecast to rise at a 4.12% CAGR.

- By province, Ontario held 38.12% of the Canada office real estate market share in 2025, whereas Quebec is projected to grow the fastest at a 4.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Office Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flight to quality for Class A & sustainable stock | +1.2% | Toronto, Vancouver, Montreal and other major metros | Medium term (2-4 years) |

| Expansion of tech, finance & professional services | +0.8% | Ontario, British Columbia, Quebec urban hubs | Long term (≥ 4 years) |

| Flexible and short-term leasing uptake | +0.6% | Major metropolitan areas | Short term (≤ 2 years) |

| Urban transit-linked infrastructure projects | +0.5% | Toronto, Vancouver, Montreal, Calgary | Long term (≥ 4 years) |

| Federal push for advanced green certifications | +0.4% | Nationwide, early in federal portfolios | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Flight to Quality Driving Demand for Class A and Sustainable Buildings

Tenant migration to premium towers is accelerating as firms compete for skilled workers and must demonstrate credible ESG performance. In Q2 2024 the Class A downtown vacancy rate fell in six of the ten largest markets, widening the rent gap versus secondary space to 35% on new leases. Brookfield reported that fresh Class A leases command rents 35% higher than expiring agreements. The Canada Green Building Council tightened embodied-carbon limits under its Zero Carbon Building Version 4 standard in June 2024, giving certified towers a pricing edge. Federal departments must now run net-zero audits on real-estate portfolios every five years, adding steady institutional demand for top-tier assets. As a result, investors continue to deploy capital into smart HVAC, touchless access, and on-site renewable systems to future-proof assets.

Growth in Tech, Finance, and Professional Services Sectors

High-tech hiring grew 4.6% in 2023 and Toronto alone added 17,600 net tech jobs, lifting the sector to 15.2% of 2024 office leasing activity. Artificial-intelligence labs require dense power loads and secure collaboration zones, steering take-up toward new-build cores. Finance and insurance roles expanded by 79,000 since October 2024, translating into fresh demand in the nation’s banking centres. Advisory and legal practices are consolidating footprints into landmark addresses that signal brand strength while supporting hybrid schedules. Venture-capital inflows rose 13.3% year-on-year, encouraging scale-ups to ink agile leases with expansion clauses that favour downtown tech clusters.

Increased Adoption of Flexible and Short-Term Leasing Solutions

Corporations prize agility amid shifting headcount forecasts. Allied Properties completed 300 lease tours in Q1 2024, achieving 69% tenant retention as it adapted suite sizes and term structures. Premium for short-term leases runs 15-25% above standard terms, which landlords accept to boost near-term cash flow. Federal policies mandating three days in office create fluctuating density, further supporting demand for turnkey coworking floors. Flexible-space operators now anchor major towers, offering enterprise suites with swing-space options that hedge against project uncertainty while preserving a high-service environment.

Urban Infrastructure Investments and Transit Expansions

A USD 30 billion national transit fund is reshaping location calculus, with TOD zoning enabling higher-density offices along rail corridors. Calgary revived its Downtown Development Incentive Program with USD 52.5 million to spur conversions and amenity upgrades. CN committed to a 20-year, 440,000-sq-ft lease at 600 De La Gauchetière W., citing multi-modal access for staff. Prospective high-speed rail connecting major corridors positions parcels near future stations for valuation upside, already influencing underwriting assumptions[1]Government of Canada, “The Largest Public Transit Investment in Canadian History,” canada.ca.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated vacancy in aging & suburban assets | -0.9% | Older urban cores, suburban belts nationwide | Medium term (2-4 years) |

| Slower return-to-office in largest CBDs | -0.7% | Downtown Toronto, Vancouver, Montreal | Short term (≤ 2 years) |

| High borrowing costs & macro uncertainty | -0.5% | Development-heavy markets nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Elevated Vacancy Rates in Older and Suburban Office Buildings

Overall national vacancy rested at 18.5% in Q2 2024, yet Class B/C inventories see far higher rates as tenants flight to quality. Suburban parks struggle because hybrid policies limit long commutes and encourage consolidation downtown. Although sublet availability fell for five straight quarters to 14.8 million sq ft by Q3 2024, the decline benefits mostly new-build cores. Municipalities promote office-to-residential conversions, but retrofit costs and zoning delays temper the pace of removals, leaving a structural glut among outdated blocks that depresses rents.

Slow Return-to-Office Trends in Major Urban Centers

In May 2024, 18.7% of Canadians still worked from home, far above the 2019 level of 7%. Federal compliance with the three-day directive ranged from 60% at National Defence to 80% at Canada Revenue Agency, underscoring uneven adoption. Slack downtown footfall has lifted Toronto core vacancy to 12.6%, sparking negative headlines about asset write-downs. Landlords must now differentiate on flexibility and tenant experience rather than pure location, trimming effective rents and extending improvement allowances to secure occupants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Building Grade: Premium Assets Drive Market Differentiation

Grade A offices held a commanding 48.92% Canada office real estate market share in 2025, and this cohort is forecast to expand at 3.98% annually to 2031. Flight-to-quality underpins steady leasing, allowing landlords of trophy towers to lift asking rents even as broader vacancies persist. Brookfield leased 27 million sq ft across its global portfolio in 2024, achieving 35% rent uplifts on new Canada mandates, a statistic that underscores pricing power in top-tier stock.

Investor focus has shifted toward deep retrofits that elevate older towers to near-Grade A specifications. Allied Properties is divesting lower-priority buildings worth up to USD 150 million to fund upgrades across its urban workspace holdings. Such capital recycling reflects a recognition that the Canada office real estate market size premium commanded by best-in-class assets justifies intensive spending on HVAC modernization, smart-building platforms, and wellness-oriented amenities. Grade B owners face an existential choice between heavy reinvestment and conversion to alternative uses.

By Transaction Type: Rental Dominance Reflects Market Caution

Rentals represented 68.52% of the Canada office real estate market size in 2025, confirming occupiers’ preference for balance-sheet agility. Shorter terms, pandemic exit clauses, and turnkey spec suites allow tenants to scale space in step with headcount. Allied’s Q1 2024 results showed 4.7% rental re-leasing spreads, an outcome that highlights pricing resilience in well-located buildings despite macro uncertainty.

Sales, though a smaller slice, are forecast to grow faster at 4.05% CAGR. Lower policy rates have revived underwriting appetite, and repricing of legacy portfolios is drawing institutional capital. Canada Pension Plan Investment Board sold two Vancouver towers for roughly USD 300 million at notable discounts, paving a path for value-add operators to reposition these assets for the green economy. Such trades illustrate how the Canada office real estate market share within the investment segment is tilting toward specialists willing to inject capex for carbon-reduction upgrades and flexible-floor plate conversions.

By End Use: Technology Sector Leads Recovery

Information technology and IT-enabled services captured 28.05% end-user demand, the largest slice of the Canada office real estate market share in 2025, and will grow at a 4.12% CAGR. Toronto’s tech ecosystem added 17,600 net roles, boosting take-up in AI-ready towers with redundant power and secure fibre loops. Banking and insurance remain sizeable but pace themselves as digital platforms compress desk requirements. Professional-services firms are rightsizing into high-spec collaborative hubs that reinforce culture while trimming under-utilised back-office space.

Start-ups favour campus-style layouts in mixed-use cores offering transit and lifestyle amenities. Lease clauses routinely embed expansion and contraction rights, demonstrating how digital firms’ fluid space needs increasingly dictate the Canada office real estate market size. Laboratory-office hybrids for life-sciences tenants draw premium rents, spotlighting the value of specialised HVAC and safety-code compliance. Energy and legal sectors post steady though flatter take-up, with ESG targets nudging oil-patch occupiers toward efficient builds in Calgary.

Geography Analysis

Ontario’s 38.12% share anchors the Canada office real estate market, yet the province grapples with elevated Class A vacancy of 16.3% as hybrid routines cap daily utilisation. Tech employment growth has moderated but remains positive, ensuring a core of steady demand for leading smart-enabled towers. Provincial funding for GO Transit expansions ties future supply to regional rail, reinforcing downtown valuations for sites near Union Station.

Quebec charts the fastest trajectory at a 4.37% CAGR to 2031. Montreal’s competitive rent profile, deep talent pool, and metro upgrades help lure multinationals seeking bilingual hubs. The provincial administration’s tax incentives for AI and aerospace underpin pre-leasing in new towers, while older stock benefits from conversion grants aimed at reducing surplus inventory.

British Columbia and Alberta represent mature but distinct narratives. Vancouver holds near-single-digit vacancy for downtown Class AAA stock, allowing landlords to raise face rents even as suburban sub-lease space lingers. Morguard’s Telus Garden stake signals sustained investor conviction in that supply-constrained corridor. Calgary reversed years of negative absorption, adding tenants from renewables and logistics that value the city’s cost edge and skilled workforce. Smaller Atlantic and Prairie centres attract back-office expansions by firms chasing workforce affordability and provincial incentives, broadening the geographic base of the Canada office real estate market.

Competitive Landscape

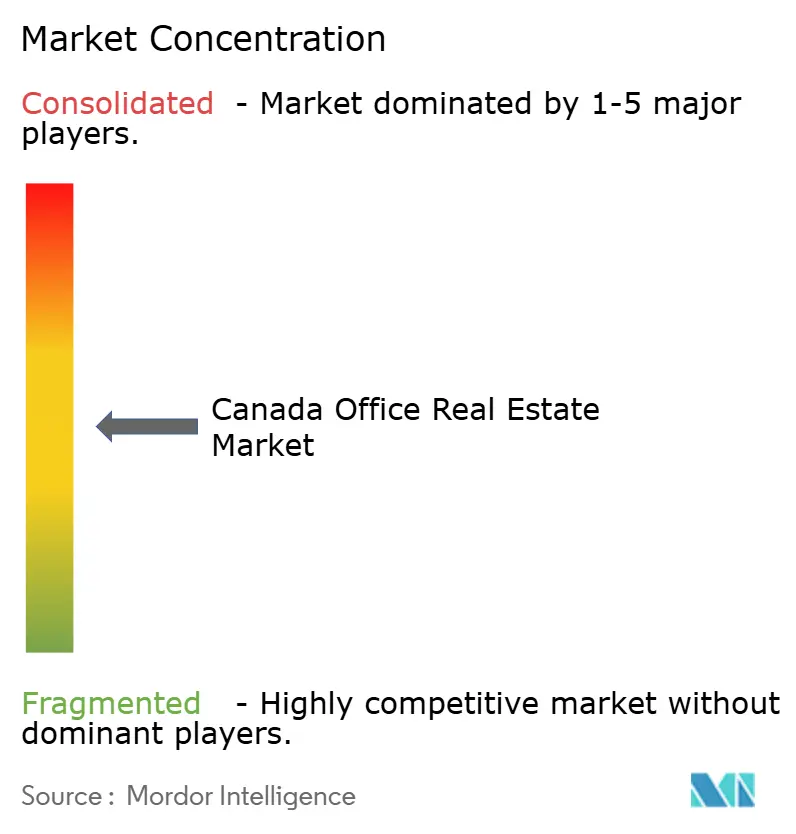

Canada’s office arena is moderately concentrated, with the top five landlords controlling a significant share of trophy assets in Toronto, Vancouver, and Montreal. Brookfield stands out, signing 27 million sq ft of leases in 2024 and lifting same-property NOI 4%, evidence of disciplined asset management and ESG-led capex. Allied Properties pivots to a sharpened urban thesis, selling lower-priority blocks to redeploy USD 150 million into high-spec upgrades.

Institutional sellers such as CPPIB are pruning exposure—its USD 300 million Vancouver tower sale underscores an ongoing price reset that opens doors for value-add specialists. Flexible-workspace brands partner with legacy owners, inserting serviced suites and data tracking to raise tenant engagement and retention. Sustainability is the new battleground: landlords publicise carbon-reduction road maps, seek Zero Carbon or LEED Platinum badges, and integrate smart meters to satisfy corporate reporting duties.

Private-equity entrants target conversion plays, snapping up well-located but obsolete blocks for mixed-use transformations that tap housing credits and GST/HST rebates on purpose-built rental components. Cross-border capital is also re-emerging: Ivanhoé Cambridge’s sale of a New York trophy stake to RXR, paired with a USD 300 million modernisation plan, illustrates confidence in premium urban offices when backed by targeted capex. Overall, competitiveness now pivots on measurable ESG outcomes, operational flexibility, and access to transit-rich parcels.

Canada Office Real Estate Industry Leaders

Brookfield Asset Management

Oxford Properties Group

Ivanhoé Cambridge

Cadillac Fairview

Allied Properties Real Estate Investment Trust

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Ontario unveiled the Protect Ontario by Building Faster and Smarter Act to streamline entitlements and accelerate builds.

- March 2025: Ottawa published regulations granting a 100% GST/HST rebate on new purpose-built rental housing, encouraging office-to-residential.

- February 2025: Brookfield reported record 2024 real-estate results, with 27 million sq ft of leases at 35% higher rents than expiries.

- January 2025: RBC Canadian Core Real Estate Fund closed a USD 860 million purchase and USD 175 million sale, boosting gross assets above USD 5 billion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Canadian office real estate market as the annual gross value (sales plus rental contracts converted to USD) generated by purpose-built, multi-story office buildings across all provinces, including strata-titled suites and landlord-operated flex floors that are marketed as office premises.

Scope Exclusion: Co-working membership revenues, property-management fees, and single-family dwellings adapted for work use are outside this analysis.

Segmentation Overview

- By Building Grade

- Grade A

- Grade B

- Grade C

- By Transaction Type

- Rental

- Sales

- By End Use

- Information Technology (IT & ITES)

- BFSI (Banking, Financial Services and Insurance)

- Business Consulting & Professional Services

- Other Services (Retail, Lifescience, Energy, Legal)

- By Province

- Ontario

- Quebec

- British Columbia

- Alberta

- Rest of Canada

Detailed Research Methodology and Data Validation

Primary Research

We interviewed developers, pension-fund asset managers, municipal planning officers, and tenant-rep brokers from major metros. These conversations validated vacancy break-outs by class, clarified net-effective rent concessions, and stress-tested our cost-of-capital assumptions before final modeling.

Desk Research

Mordor analysts first culled historical stock, vacancy, and absorption data from open datasets issued by Statistics Canada, the Canada Revenue Agency's GST filings, provincial land-registry portals, and quarterly reports from national brokerages such as CBRE, Cushman & Wakefield, JLL, and Colliers. Macro indicators, office-using employment, business formation rates, and Bank of Canada prime lending trends were charted to frame demand cycles. To benchmark capital flows, we parsed Investment Canada Act disclosures, REIT financials gathered through SEDAR Plus, and building-permit tallies published by major cities. Paid resources, notably D&B Hoovers for landlord revenues and Dow Jones Factiva for deal news, filled firm-level gaps. The illustrative sources named here are a subset of many consulted during desk work.

Market-Sizing & Forecasting

A top-down, bottom-up hybrid model begins with Statistics Canada construction completions and CBRE lease-transaction ledgers to build a province-level demand pool, which is then aligned to recorded sale and rental consideration. Supplier roll-ups of Grade A towers and sampled average rents cross-check the totals.

Key variables include: 1. Average Class A net rent (USD / sq ft), 2. Quarterly net absorption (sq ft), 3. Vacancy trajectory by grade, 4. Annual office-using job growth, 5. Weighted prime cap rate shifts.

A multivariate regression, linking the above drivers to GDP and interest-rate scenarios, produces the 2025-2030 outlook. Gaps in suburban stock data are bridged through ratio allocation from assessor rolls and verified with broker surveys.

Data Validation & Update Cycle

Outputs pass three tiers of review: automated variance scans, peer analyst scrutiny, and sector-lead sign-off. Before release, we re-contact select primary sources for material-event checks. Coverage is refreshed each year, and ad-hoc updates are issued when policy or macro shocks move any driver materially.

Why Mordor's CANADA OFFICE REAL ESTATE Baseline Commands Reliability

Published figures often diverge because firms choose different asset scopes, valuation bases, and refresh cadences. The largest spreads arise when some studies quote building market values while Mordor, by design, tracks transacted sales and leases only; when competitor models fold retail and industrial floors into 'commercial'; or when unverified asking rents are uplifted without vacancy discounts.

These contrasts show that Mordor's disciplined scope, driver-tested model, and annual ground-truthing give investors a balanced, actionable baseline they can retrace and update with confidence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 28.29 B (2025) | Mordor Intelligence | |

| USD 89.58 B (2024) | Regional Consultancy A | Includes underlying asset valuations and owner-occupied headquarters, inflating totals |

| USD 76.6 B (2024) | Global Consultancy B | Bundles offices within a broader commercial basket (retail, logistics) and applies book-value conversions |

These contrasts show that Mordor's disciplined scope, driver-tested model, and annual ground-truthing give investors a balanced, actionable baseline they can retrace and update with confidence.

Key Questions Answered in the Report

What is the current value of the Canada office real estate market?

The market is valued at USD 29.31 billion for 2026 and is projected to reach USD 34.95 billion by 2031.

Which building grade holds the largest market share?

Grade A offices command 48.92% of 2025 demand and are forecast to grow at a 3.98% CAGR.

How big is the technology sector’s footprint in Canadian offices?

Technology and IT-enabled services account for 28.05% of end-user demand and should expand at 4.12% annually.

Which province is growing the fastest?

Quebec leads with a projected 4.37% CAGR between 2026 and 2031, buoyed by infrastructure spending and cost advantages.

Why are flexible leases becoming more popular?

Hybrid work patterns and economic uncertainty push firms to prioritise agility, resulting in rental premiums of 15-25% for short-term, plug-and-play space.

How are sustainability mandates shaping office demand?

Federal net-zero audits and tougher carbon standards make certified green buildings more attractive, supporting higher rents and lower vacancies in that segment.

Page last updated on: