Platelet-Rich Fibrin (PRF) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

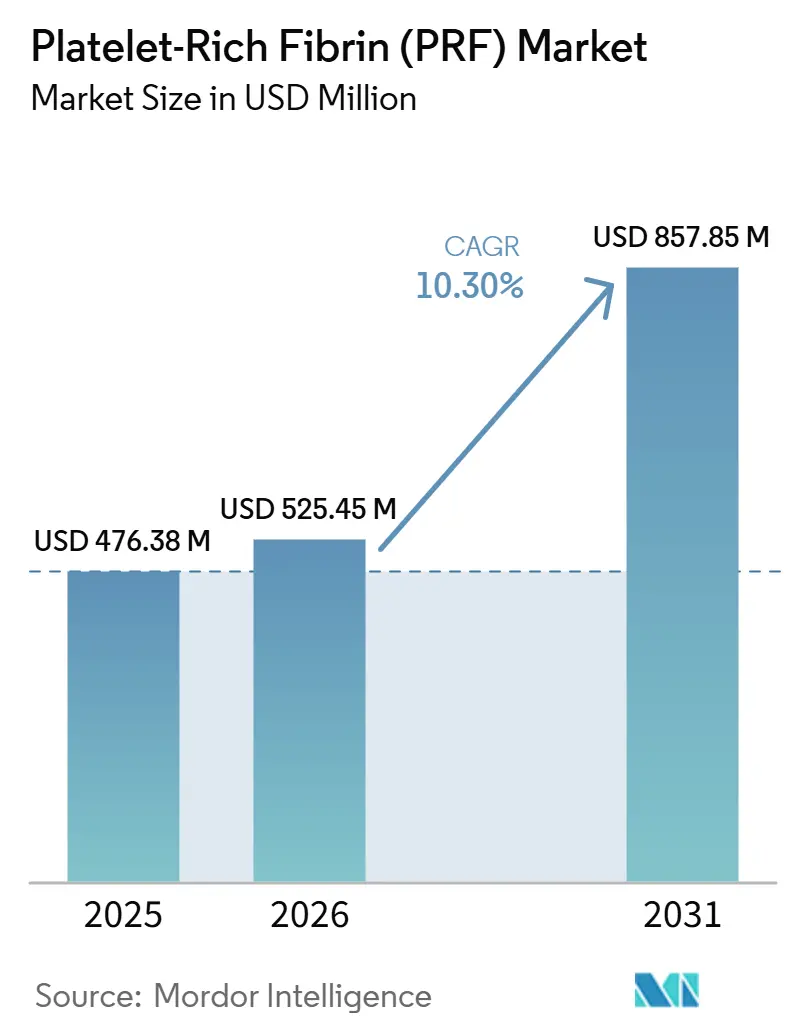

| Market Size (2026) | USD 525.45 Million |

| Market Size (2031) | USD 857.85 Million |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

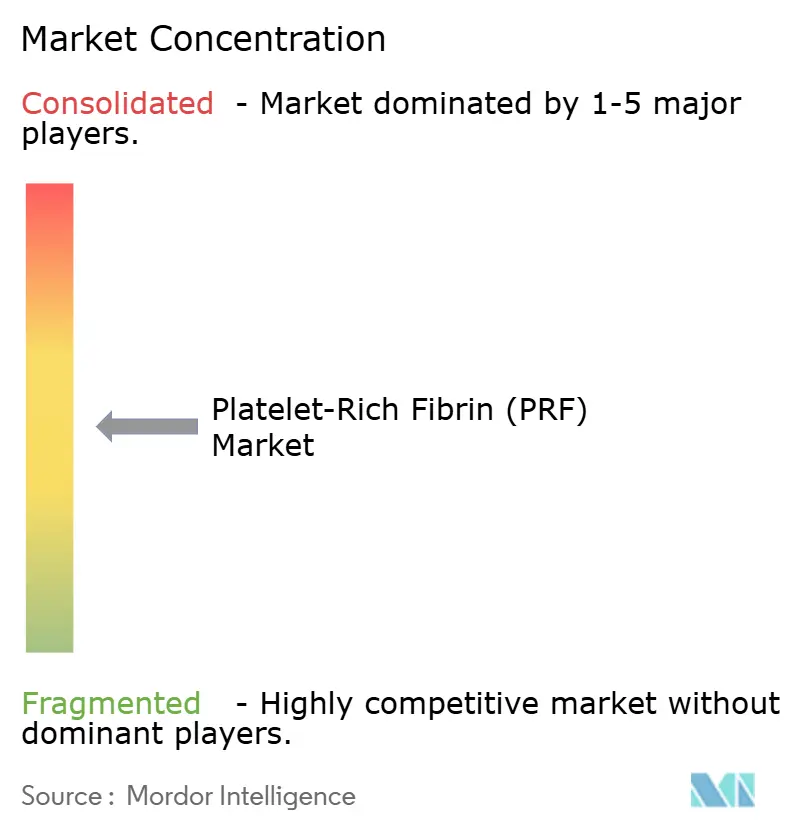

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Platelet-Rich Fibrin (PRF) Market Analysis by Mordor Intelligence

The Platelet-Rich Fibrin Market size is projected to expand from USD 476.38 million in 2025 and USD 525.45 million in 2026 to USD 857.85 million by 2031, registering a CAGR of 10.30% between 2026 to 2031.

Growth in the Platelet-Rich Fibrin market is driven by rising dental implant volumes, broader adoption of autologous wound care, and increasing demand for point-of-care biologic preparation using the patient’s own blood. Its favorable cost profile supports adoption, as it reduces the material acquisition burden associated with many exogenous biologics amid tighter procedure economics for hospitals and outpatient providers. Faster chairside preparation and closed-system devices are improving usability in routine clinical settings, while reimbursement-linked regulatory progress is strengthening commercial visibility, particularly for FDA-cleared wound care indications aligned with Medicare coverage pathways. Competitive activity is becoming more structured as specialist biologics firms, adjacent medtech players, and new aesthetics-focused entrants strengthen the market’s operating model.

Key Report Takeaways

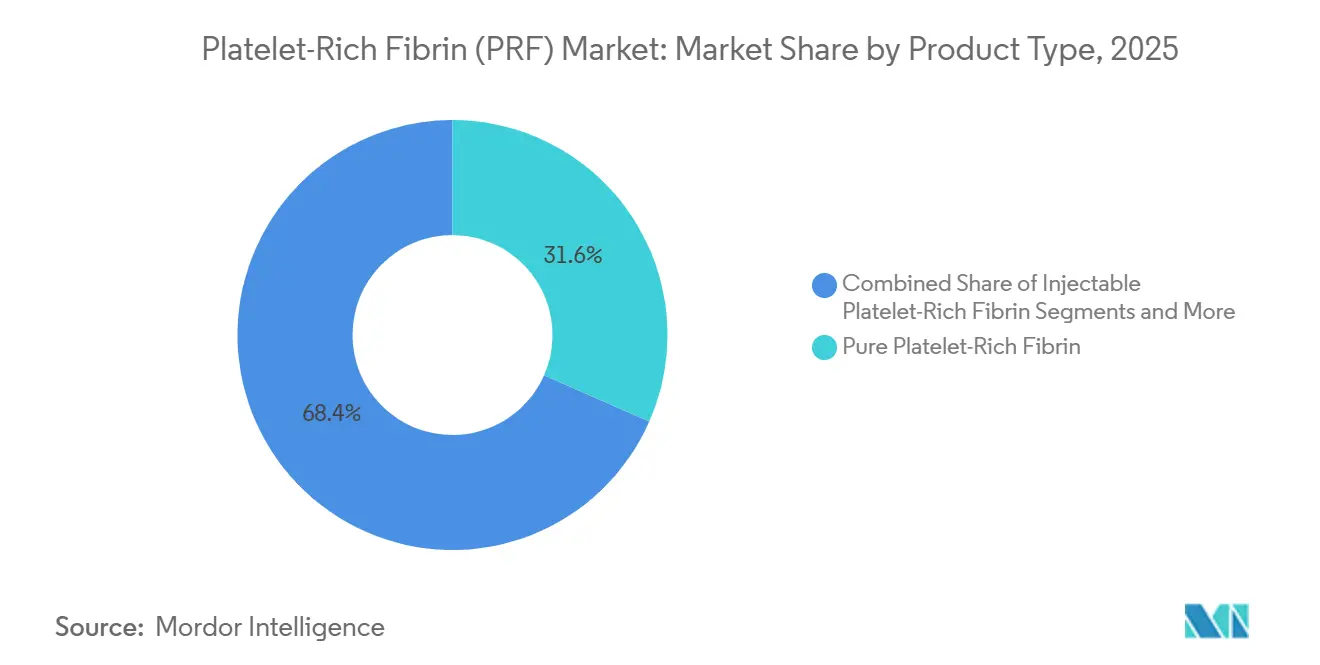

- By product type, pure platelet-rich fibrin led with 31.60% share in 2025, while injectable PRF is projected to grow at 11.32% CAGR through 2031.

- By component, PRF kits and consumables accounted for 44.21% of the Platelet-Rich Fibrin market size in 2025, while centrifuges and processing systems are projected to expand at 10.88% CAGR through 2031.

- By application, orthopedics and sports medicine held 38.58% share in 2025, while dentistry and oral surgery is forecast to advance at 12.45% CAGR through 2031.

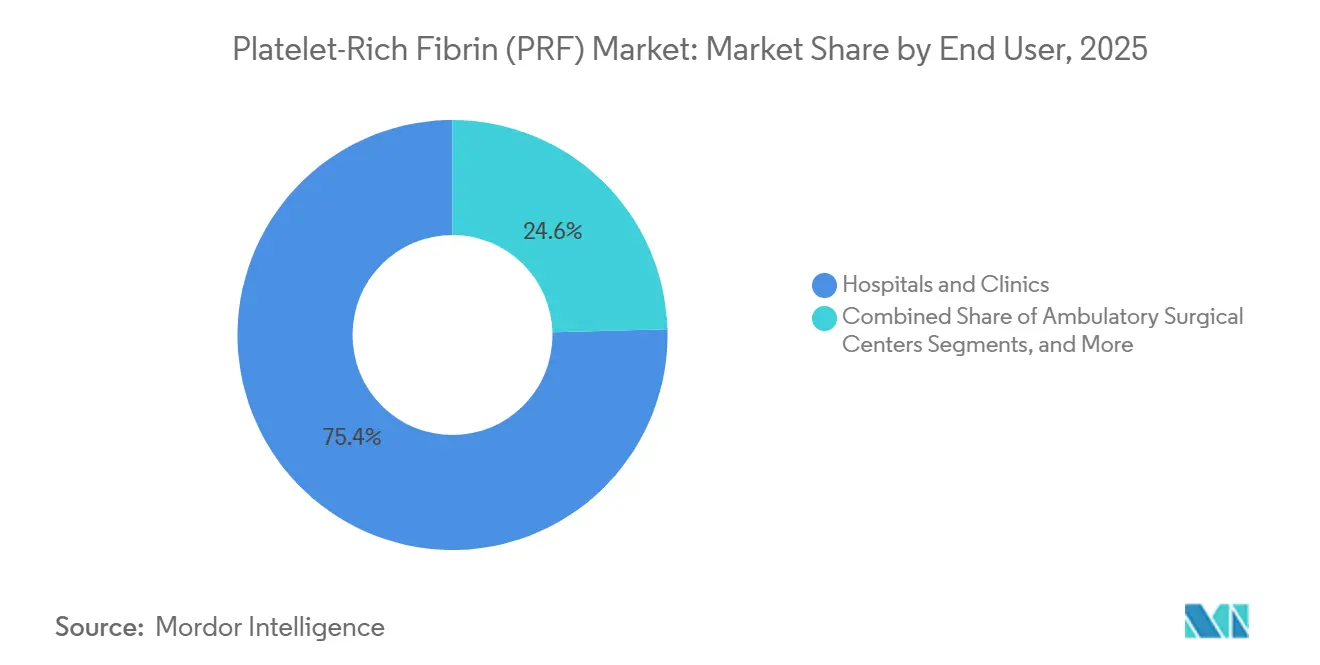

- By end user, hospitals and clinics represented 75.43% share in 2025, while ambulatory surgical centers are projected to record 11.67% CAGR through 2031.

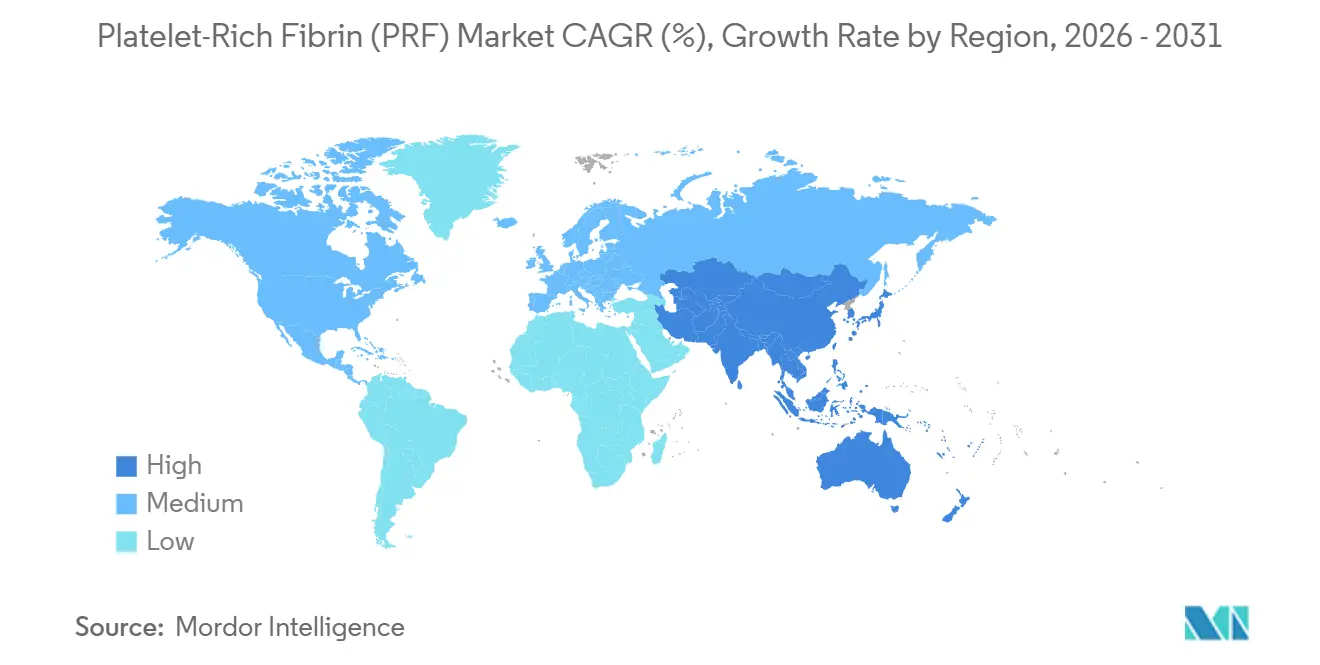

- By geography, North America held 39.95% of the Platelet-Rich Fibrin market share in 2025, while Asia-Pacific is projected to grow at 12.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Platelet-Rich Fibrin (PRF) Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for autologous regenerative therapies in dental surgery | +2.5% | Global, strongest in North America, Europe, and Asia-Pacific dental corridors | Short term (≤ 2 years) |

| Expanding use in soft tissue healing and wound closure protocols | +2.0% | North America and Europe | Short term (≤ 2 years) |

| Growing shift toward outpatient, minimally invasive biologic procedures | +1.7% | North America and Europe, with early momentum in Asia-Pacific private ASC networks | Medium term (2-4 years) |

| Standardized PRF kits and closed systems improving procedural reproducibility | +1.5% | Global, with highest impact in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| New aesthetic and hair restoration use cases extending addressable demand | +1.2% | Asia-Pacific and Middle East | Medium term (2-4 years) |

| Regulatory momentum for point-of-care biologic devices in mature markets | +1.3% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Autologous Regenerative Therapies in Dental Surgery

Dental applications remain the clearest volume driver for the Platelet-Rich Fibrin market, as a single procedure can support both bone regeneration and soft tissue closure. This dual benefit gives PRF a practical advantage in implant site preparation and socket preservation, where clinicians prioritize simpler workflows and lower biologic costs. A 2026 randomized controlled trial is expected to show that injectable PRF combined with xenograft improves early wound closure within two weeks compared with xenograft alone, supporting adoption in high-volume dental settings.[1]BMC Oral Health, “Comparison of the Effect of Injectable Platelet Rich Fibrin and Advanced Platelet Rich Fibrin with Xenograft on the Socket Preservation of Extracted Mandibular Molars,” BMC Oral Health, link.springer.com As evidence quality improves, the Platelet-Rich Fibrin market is expanding from specialist oral surgeons into larger general dental networks with higher procedure volumes.

Expanding Use in Soft Tissue Healing and Wound Closure Protocols

Wound care is becoming a stronger growth avenue for the Platelet-Rich Fibrin market, as regulatory progress is expected to align clinical use more closely with reimbursement. In April 2026, Royal Biologics is expected to receive FDA clearance for Fibrinet PRF Wound Matrix for exuding cutaneous wounds, including diabetic and venous ulcers. This clearance would be significant because CMS NCD 270.3 links Medicare coverage to platelet therapies prepared with FDA-cleared devices for wound management, addressing a key adoption barrier in the United States. Royal Biologics reported that 92% of treated wounds achieved at least a 50% size reduction, 57% achieved complete closure at 12 weeks, and the mean healing time was 6.75 weeks.

Growing Shift Toward Outpatient, Minimally Invasive Biologic Procedures

The shift toward day-surgery and outpatient care is shaping the fastest-growing opportunities in the Platelet-Rich Fibrin market. Injectable PRF aligns well with this care model because clinicians can deliver it chairside and use it in indications where membrane implantation is less practical. A 2025 meta-analysis is expected to find that PRP and PRF augmentation in arthroscopic rotator cuff repair improves early functional scores, especially in medium-to-large tears treated with leukocyte-poor formulations.[2]Frontiers in Bioengineering and Biotechnology, “Platelet-Rich Plasma in Arthroscopic Rotator Cuff Repair: A Meta-Analysis of Biomaterial Efficacy and Future Directions for Personalized Sports Medicine,” Frontiers in Bioengineering and Biotechnology, frontiersin.org A 2026 pre-clinical study on Croma-Pharma’s Exprecell is also expected to show that a five-minute, single-spin, anticoagulant-free protocol can produce biologically active Fluid-PRF suitable for outpatient injection use.[3]Frontiers in Pharmacology, “Anticoagulant-Free Preparation of Autologous Platelet-Rich Plasma (PRP) / Fluid Platelet-Rich Fibrin (f-PRF): A Pre-Clinical Comparative Performance Study,” Frontiers in Pharmacology, frontiersin.org

Standardized PRF Kits and Closed Systems Improving Procedural Reproducibility

Standardization is gaining importance in the Platelet-Rich Fibrin market, as inconsistent centrifugation methods have long created variability in biological quality and published outcomes. Closed-system kits reduce differences in tube type, blood volume, and handling steps, improving procedural reproducibility across sites. A March 2026 study is expected to report that Albumin-PRF outperforms traditional PRP and H-PRF in endothelial function, supporting the shift toward more precise fraction-specific preparation systems.[4]Scientific Reports, “Albumin-PRF Validation Data on Endothelial Function,” Scientific Reports, nature.com This evidence supports equipment upgrades and explains why centrifuges and processing systems are projected to grow faster than other component categories in the Platelet-Rich Fibrin market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Lack of global standardization in centrifugation protocols | -1.5% | Global, most acute in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Variable clinical outcomes across indications and operators | -1.3% | Global, with greater effect on orthopedic reimbursement in North America and Europe | Medium term (2-4 years) |

| Reimbursement gaps for PRF procedures outside core dental uses | -1.1% | North America, Europe, and Middle East and Africa | Medium term (2-4 years) |

| Limited high-quality long-term evidence in non-dental indications | -0.9% | Global, especially in wound care and sports medicine | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Global Standardization in Centrifugation Protocols

The Platelet-Rich Fibrin market continues to face a major structural limitation due to the absence of an internationally accepted centrifugation standard. Published protocols vary significantly in centrifugal force, spin duration, tube material, and blood volume, which can lead to different biological performance among products with the same label. A 2026 review reports that centrifugation speed and relative centrifugal force can materially affect PRF’s regenerative potential, contributing to inconsistent clinical outcomes. This variability limits cross-study comparisons and slows payer confidence, especially as providers expand PRF use beyond core dental indications.

Variable Clinical Outcomes Across Indications and Operators

Clinical variability remains a key restraint for the Platelet-Rich Fibrin market, as operator technique affects final composition and PRF subtypes perform differently across tissues. A 2025 rotator cuff meta-analysis reports stronger benefits with leukocyte-poor formulations, while a 2026 meta-analysis on ACL reconstruction finds only marginal early improvement that does not continue at longer follow-up. These findings highlight the need for better subtype selection and provider training. Until operator practices become more consistent and outcome data become more durable, reimbursement expansion will likely remain slower than procedure interest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Injectable PRF Reshaping the Outpatient Biologic

Pure Platelet-Rich Fibrin is expected to hold the largest product share, at 31.60%, in 2025, supported by its long clinical use in dental implantology, socket preservation, and periodontal regeneration. Its membrane format remains familiar to oral surgeons and continues to support adoption in established surgical workflows. Leukocyte-Rich Platelet-Rich Fibrin maintains relevance in complex wound management and burn-related procedures, while Advanced Platelet-Rich Fibrin is gaining traction in maxillofacial reconstruction due to its stronger fibrin architecture and improved handling properties.

Injectable PRF is projected to be the fastest-growing product type, registering an 11.32% CAGR from 2026 to 2031, as the Platelet-Rich Fibrin market expands beyond membrane-based surgery. Demand is increasing in orthopedic joint injections, facial rejuvenation, and hair restoration, where fluid delivery better fits clinical requirements. A 2026 randomized study in BMC Oral Health reported better early wound healing with injectable PRF in socket preservation, supporting faster adoption in high-volume dental practices.

By Component: PRF Kits’ Recurring Revenue Model Attracting Capital Deployment

PRF kits and consumables are expected to account for 44.21% of the Platelet-Rich Fibrin market size in 2025, reflecting the category’s recurring revenue structure. Centrifuges are typically one-time capital purchases, while tubes, preparation kits, and related consumables scale directly with procedure volume. This model encourages manufacturers to build proprietary closed systems that connect consumables with specific devices and strengthen customer retention.

Accessories and ancillary supplies generate lower revenue, but their relevance is increasing as PRF use expands into surgical settings that require varied application formats. Centrifuges and processing systems are projected to grow at a 10.88% CAGR from 2026 to 2031, indicating continued scope for installation growth and technology upgrades in the Platelet-Rich Fibrin market.

By Application: Dentistry Accelerating as Orthopedics Faces Evidence Pressure

Orthopedics and sports medicine are expected to hold the largest application share, at 38.58%, in 2025, while dentistry and oral surgery are projected to grow at a 12.45% CAGR through 2031. Orthopedic use remains broad across osteoarthritis management, ACL reconstruction support, and rotator cuff repair augmentation in high-volume sports medicine practices. Dentistry is expanding faster due to shorter clinical protocols, stronger outcome consistency, and easier commercial adoption when evidence and workflow are aligned.

Wound healing and reconstruction are also becoming more relevant following the expected April 2026 FDA clearance for Fibrinet PRF Wound Matrix, which would create a clearer path for reimbursed use in diabetic and venous ulcers. The Platelet-Rich Fibrin market shows a clear split between dental confidence and orthopedic caution. Rotator cuff evidence remains supportive in selected settings, but ACL reconstruction meta-analysis findings showed only limited early benefit that did not persist, keeping reimbursement discussions more conservative in sports medicine.

By End User: Ambulatory Surgical Centers Redefining Growth Dynamics

Hospitals and clinics are expected to represent 75.43% of the Platelet-Rich Fibrin market share in 2025, supported by established centrifugation infrastructure, trained staff, and broad procedural coverage across surgery, dentistry, and wound care. Their scale and operational depth are expected to keep them as the main revenue base for the Platelet-Rich Fibrin market in 2026. Dental clinics remain the second-largest end-user group and continue to drive demand for kits and consumables as PRF protocols expand from specialist practices into wider dental networks.

Academic and research institutes contribute less revenue, but they remain important because their studies shape protocol credibility and influence future commercial adoption. Ambulatory surgical centers are projected to record an 11.67% CAGR from 2026 to 2031, making them the fastest-growing end-user group in the Platelet-Rich Fibrin market. Their interest is closely linked to cost control, as PRF avoids the acquisition cost of many exogenous biologics while serving as a useful adjunct in selected procedures.

Geography Analysis

North America is expected to hold a 39.95% share in 2025 and remain the largest regional Platelet-Rich Fibrin market by value. The United States drives regional demand through a strong network of private dental and orthopedic practices, mature device adoption, and improving reimbursement clarity for selected wound care applications. The anticipated April 2026 FDA clearance for Fibrinet® PRF Wound Matrix is significant as it would align PRF use more directly with the CMS NCD 270.3 coverage framework for wound management. Canada and Mexico add smaller but growing demand, with Mexico also benefiting from medical travel for lower-cost dental and aesthetic procedures.

Europe continues to account for a meaningful share of the Platelet-Rich Fibrin market, supported by an established dental surgery base and stricter supplier standards under the MDR environment. Higher evidence requirements are shifting share toward manufacturers that can demonstrate documented and reproducible device performance. This strengthens the position of closed-system suppliers, particularly where clinical teams prioritize easier compliance and controlled preparation. Europe also remains relevant for newer aesthetic applications, with devices such as Exprecell™ available across the EU, the UK, and Switzerland for autologous PRP and Fluid-PRF preparation.

Asia-Pacific is projected to grow at a CAGR of 12.56% from 2026 to 2031, making it the fastest-growing regional Platelet-Rich Fibrin market. Growth is supported by expanding private dental capacity, rising acceptance of outpatient biologic procedures, and wider use of minimally invasive aesthetics. Demand also favors injectable formats across dermatology, cosmetic surgery, and chairside dental workflows. The Middle East and Africa remains an emerging opportunity, while South America, led by Brazil, is positioned for volume growth as kit availability and distribution improve.

Competitive Landscape

The Platelet-Rich Fibrin market remains moderately consolidated, with specialist biologics companies such as Vivostat A/S, Regen Lab SA, EmCyte Corporation, and Royal Biologics holding strong positions. Larger medtech companies, including Stryker, Zimmer Biomet, Arthrex, and Dentsply Sirona, compete through adjacent PRP and biologic augmentation portfolios. Specialist firms lead in dedicated PRF system design, while larger players influence purchasing through broader procedural relationships. The market remains competitive and continues to allow new product formats and application-focused entrants.

Companies in the Platelet-Rich Fibrin market are using closed-system devices to improve differentiation, compliance, and recurring consumables demand. Vivostat’s preparation and application model reflects the shift toward integrated workflow control, while its expected ownership change in January 2026 indicates growing investor interest in formal consolidation.Competitive success in the Platelet-Rich Fibrin market depends on more than the centrifuge. Companies must demonstrate clinical evidence, ease of use, procedural fit, and the ability to secure steady consumables demand. Newer variants, such as Albumin-PRF, could become disruptive if they deliver measurable biological advantages and require more specialized preparation systems.

Companies are also extending PRF into newer applications to expand total addressable demand. Royal Biologics is expected to set an important benchmark in April 2026 with an FDA-cleared PRF wound matrix linked to a defined wound management indication and Medicare-relevant reimbursement logic. Croma-Pharma’s December 2025 launch of Exprecell reflects a similar push into aesthetics and minimally invasive care, where speed and ease of use are key purchase factors. Supply chain influence remains important, as Henry Schein, Becton Dickinson, and Envista can shape kit selection through distribution reach and practice-level integration.

Platelet-Rich Fibrin (PRF) Industry Leaders

Zimmer Biomet Holdings, Inc.

Stryker Corporation

Arthrex, Inc.

Terumo Corporation

EmCyte Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Royal Biologics received FDA clearance for Fibrinet PRF Wound Matrix for exuding cutaneous wounds, including diabetic and venous ulcers, enabling Medicare coverage under CMS NCD 270.3.

- February 2026: StimLabs and Geistlich Pharma expanded their regenerative wound care partnership for a novel product targeted for launch in Q2 2026.

- December 2026: Croma-Pharma launched Exprecell, an MDR-certified closed-system device for Fluid-PRF and PRP preparation, targeting minimally invasive aesthetic and dental applications.

- November 2025: The FDA issued 510(k) clearance for PlateletQuick PRP for rapid point-of-care preparation of autologous PRP for orthopedic bone graft applications.

Global Platelet-Rich Fibrin (PRF) Market Report Scope

As per the scope of the report, Platelet-Rich Fibrin (PRF) is a natural, blood-derived biomaterial rich in platelets, white blood cells, and growth factors. Spun from a patient's own blood without anticoagulants, it forms a 3D matrix that slowly releases healing proteins to accelerate soft and hard tissue regeneration.

The platelet-rich fibrin (PRF) market is segmented by product type, component, application, end user, and geography. By product type, the market includes pure platelet-rich fibrin, leukocyte-rich platelet-rich fibrin, injectable platelet-rich fibrin, and advanced platelet-rich fibrin. By component, the market is segmented into centrifuges and processing systems, PRF kits and consumables, and accessories and ancillary supplies. By application, the market is categorized into dentistry and oral surgery, orthopedics and sports medicine, wound healing and reconstruction, plastic and aesthetic surgery, maxillofacial and craniofacial surgery, and other PRF applications. By end user, the market is segmented into hospitals and clinics, dental clinics, ambulatory surgical centers, and academic and research institutes. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Pure Platelet-Rich Fibrin |

| Leukocyte-Rich Platelet-Rich Fibrin |

| Injectable Platelet-Rich Fibrin |

| Advanced Platelet-Rich Fibrin |

| Centrifuges and Processing Systems |

| PRF Kits and Consumables |

| Accessories and Ancillary Supplies |

| Dentistry and Oral Surgery |

| Orthopedics and Sports Medicine |

| Wound Healing and Reconstruction |

| Plastic and Aesthetic Surgery |

| Maxillofacial and Craniofacial Surgery |

| Other PRF Applications |

| Hospitals and Clinics |

| Dental Clinics |

| Ambulatory Surgical Centers |

| Academic and Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Pure Platelet-Rich Fibrin | |

| Leukocyte-Rich Platelet-Rich Fibrin | ||

| Injectable Platelet-Rich Fibrin | ||

| Advanced Platelet-Rich Fibrin | ||

| By Component | Centrifuges and Processing Systems | |

| PRF Kits and Consumables | ||

| Accessories and Ancillary Supplies | ||

| By Application | Dentistry and Oral Surgery | |

| Orthopedics and Sports Medicine | ||

| Wound Healing and Reconstruction | ||

| Plastic and Aesthetic Surgery | ||

| Maxillofacial and Craniofacial Surgery | ||

| Other PRF Applications | ||

| By End User | Hospitals and Clinics | |

| Dental Clinics | ||

| Ambulatory Surgical Centers | ||

| Academic and Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Platelet-Rich Fibrin space in 2026?

It stands at USD 525.45 million in 2026 and is forecast to reach USD 857.85 million by 2031 at a CAGR of 10.30%.

Which application area is growing the fastest?

Dentistry and Oral Surgery is the fastest-growing application, with a projected CAGR of 12.45% through 2031.

Which region leads demand today?

North America led with 39.95% share in 2025 and remains the largest regional revenue contributor.

Why are ambulatory surgical centers becoming more important?

They are projected to grow at 11.67% CAGR through 2031 because PRF fits cost-controlled, point-of-care outpatient workflows.

What is driving adoption in wound care?

The main trigger is the April 2026 FDA clearance for Fibrinet PRF Wound Matrix, which also aligns with CMS NCD 270.3 reimbursement logic.

What is the biggest barrier to wider adoption?

Lack of standardized centrifugation protocols remains the main structural barrier because it leads to uneven product composition and variable clinical outcomes.

Page last updated on: